Turkey Poultry Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.43 Billion |

| Market Size (2026) | USD 14.22 Billion |

| Market Size (2031) | USD 18.93 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Turkey Poultry Market Analysis by Mordor Intelligence

The Turkey poultry market size is expected to grow from USD 13.43 billion in 2025 to USD 14.22 billion in 2026 and is forecast to reach USD 18.93 billion by 2031 at 5.89% CAGR over 2026-2031. This upward trajectory is primarily driven by shifting dietary preferences and a rising consumer appetite for quality and convenience. With strong domestic demand, exports reaching 97 countries, and steadfast government backing, the market is primed for a healthy five-year growth. While broiler meat remains the dominant choice due to its affordability and versatility, there's a discernible rise in the popularity of processed poultry products. This shift highlights a growing consumer preference for convenient meal solutions and premium product offerings. Although traditional poultry items still lead, organic variants are rapidly gaining ground, signaling a heightened consumer focus on health, animal welfare, and sustainability. While chicken remains the undisputed favorite, duck is emerging as a sought-after option, appealing to adventurous consumers in search of diverse culinary experiences. Retail channels hold the lion's share of the market, but the foodservice sector is witnessing faster growth, fueled by a hospitality industry revival and a renewed enthusiasm for dining out. This trend paves the way for innovation and expansion in both retail and foodservice distribution channels.

Key Report Takeaways

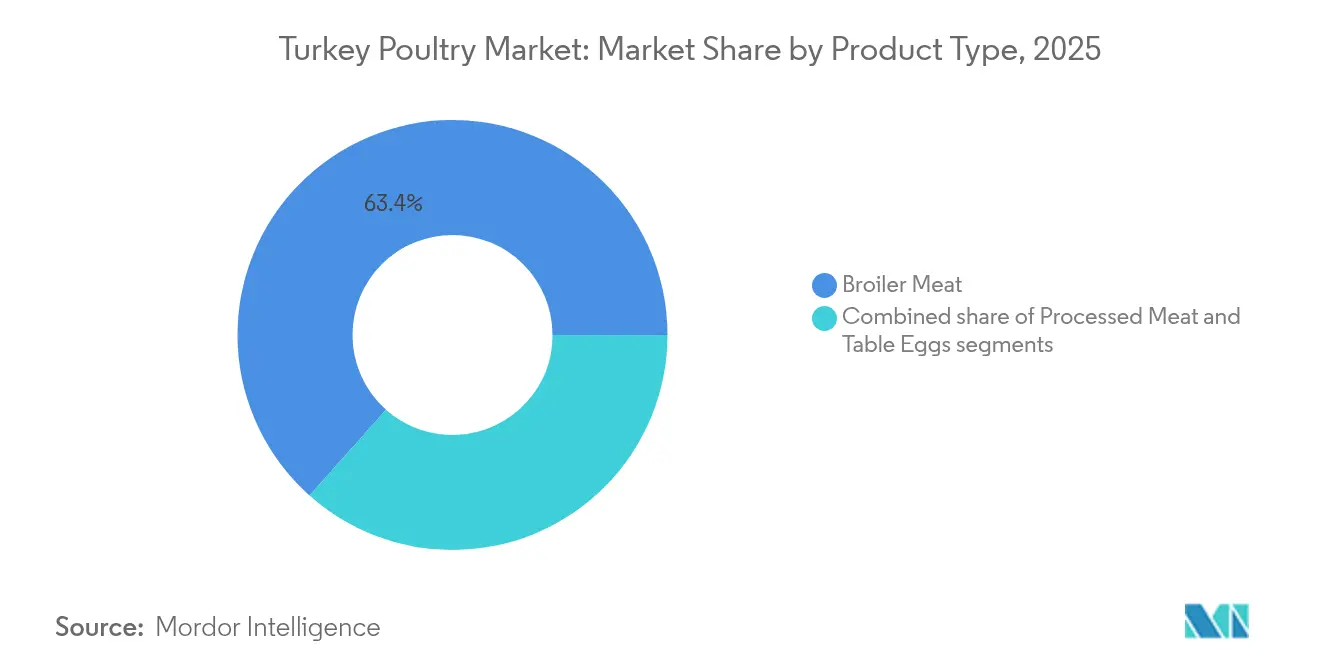

- By product type, broiler meat held 63.42% of the Turkey poultry market share in 2025; processed meat is projected to expand at a 6.73% CAGR through 2031.

- By species, chicken led with 65.02% revenue share in 2025, while duck is forecast to post a 7.53% CAGR to 2031.

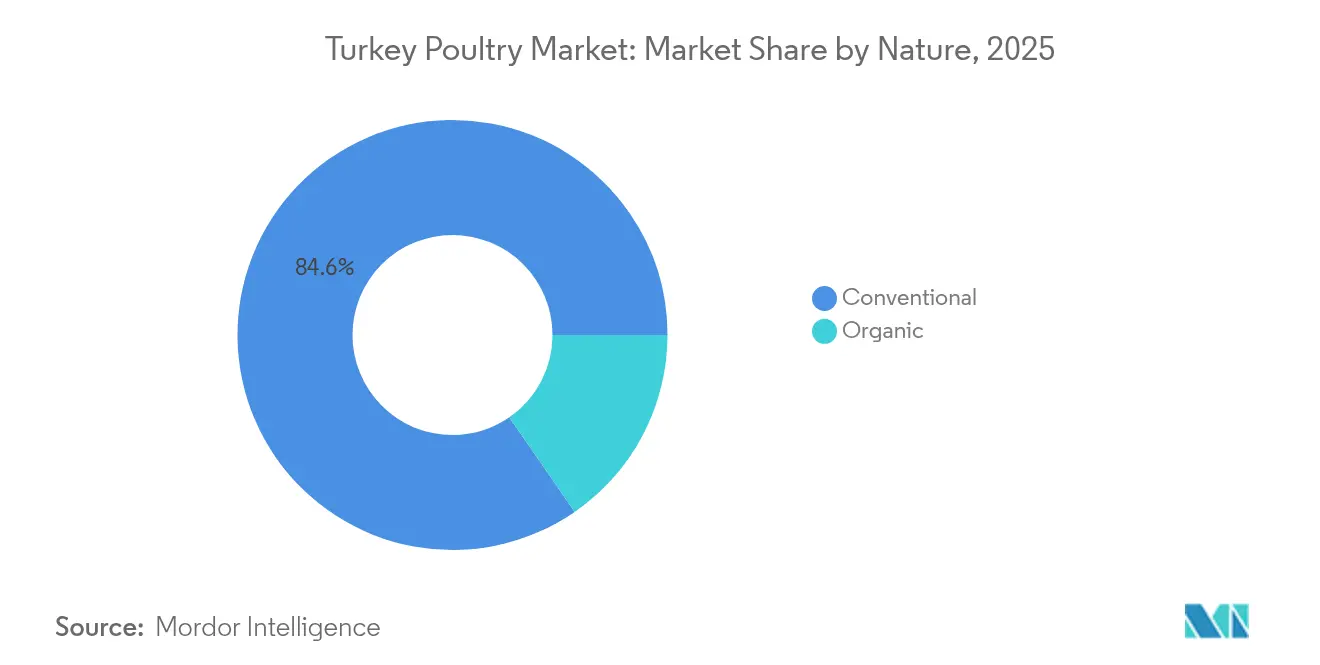

- By nature, conventional production accounted for 84.62% of the Turkey poultry market in 2025; organic is expected to grow at a 7.38% CAGR.

- By distribution channel, retail commanded 55.11% share of the Turkey poultry market in 2025; foodservice is advancing at a 5.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Poultry Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for lean protein among health-conscious consumers | +1.2% | Global, with early gains in Istanbul, Ankara, Izmir | Medium term (2-4 years) |

| Growing keto trends boosts demand for broiler meat among consumers | +0.8% | Urban centers, spill-over to secondary cities | Short term (≤ 2 years) |

| Expansion of quick service restaurants and foodservice channels | +1.1% | National, concentrated in metropolitan areas | Medium term (2-4 years) |

| Growth in convenience foods increases consumption of processed turkey products. | +0.9% | National, with premium segments in western regions | Long term (≥ 4 years) |

| Government support and subsidies encourage poultry sector investments. | +1.0% | National, targeted support in rural development zones | Long term (≥ 4 years) |

| Expanding cold chain infrastructure boosts processed meat distribution. | +0.7% | National, priority corridors linking production to consumption centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for lean protein among health-conscious consumers

Turkish consumers are increasingly prioritizing the quality of protein over its quantity, driving a sustained rise in demand for poultry products, which are widely perceived as healthier and more affordable alternatives to red meat. This shift aligns with a broader movement towards sustainable living in Turkey, where consumers are becoming more conscious of the environmental, economic, and health implications of their dietary choices. The trend is particularly pronounced in urban areas, where higher disposable incomes and changing lifestyles support the purchase of premium protein options. Consequently, per capita poultry consumption in Turkey has reached 21 kg annually, underscoring the growing reliance on poultry as a primary protein source. Turkey also maintains its position as a regional leader in milk and dairy production, with an annual output of 24 million tons in 2024[1]Source: Turkish Statistical Institute, "Raw Milk Production Statistics, 2024", www.data.tuik.gov.tr. This robust dairy sector complements the growth of the poultry market, as consumers increasingly seek diverse, high-quality protein sources to meet their nutritional needs. Additionally, the government’s agricultural policies, which emphasize food security, self-sufficiency, and sustainable production practices, are bolstering domestic protein production capabilities. These initiatives not only support the poultry and dairy industries but also encourage innovation and efficiency across the supply chain, fostering long-term market growth.

Growing keto trends boosts demand for broiler meat among consumers

The rising adoption of the ketogenic diet in Turkey is driving a notable increase in demand for high-protein, low-carbohydrate food options, with broiler meat emerging as a preferred choice due to its nutritional profile and affordability. This shift in dietary preferences aligns with Turkey's forecasted record chicken production of 2.6 million metric tons by 2025, ensuring ample supply to meet evolving consumer needs. The government's export quotas, in place until December 2024, further bolster this trend by redirecting production capacity to domestic markets, allowing producers to fully leverage the growing demand for keto-friendly products. Turkish poultry companies are strategically positioned to respond to these changes, utilizing integrated production systems that include compound feed factories and slaughterhouse facilities. These systems not only enhance operational efficiency but also ensure adherence to halal certification standards, which are essential for domestic consumers. To sustain this momentum, the industry must focus on continuous consumer education and the development of innovative, convenient product formats, such as ready-to-consume options, that cater to the fast-paced lifestyles of urban populations.

Expansion of quick service restaurants and foodservice channels

Turkey's foodservice sector is experiencing robust growth, driven by the rising demand for quick-service restaurant (QSR) chains that are strategically focusing on chicken-based menu offerings to cater to evolving consumer preferences. The country's unique geographic position, serving as a vital link between Europe, Asia, and the Middle East, provides a competitive advantage by facilitating the entry and expansion of international franchises while simultaneously supporting the growth of domestic chains. Istanbul and the Marmara region act as pivotal distribution hubs, hosting the majority of foodservice channels and sales offices. This centralization enables the creation of highly efficient supply chain networks, particularly for poultry products, which remain a cornerstone of the sector. Additionally, the Turkish government’s infrastructure development initiatives, including the planned expansion of the railway network to over 5,600 km of high-speed lines by 2025, are expected to significantly enhance logistics and distribution efficiency. These advancements will improve connectivity between production centers and urban consumption markets, positioning the sector for sustained growth, increased competitiveness, and operational excellence in the forecast period.

Growth in convenience foods increases consumption of processed turkey products.

Turkish consumers' evolving lifestyle patterns are significantly driving the demand for processed poultry products, including nuggets, sausages, burgers, and marinated options. These products cater to the increasing need for convenience while maintaining nutritional value, making them a preferred choice across various demographics. The processed meat segment is witnessing a strong 6.81% CAGR, outpacing the overall market growth. This impressive performance highlights the success of continuous product innovation, enhanced packaging solutions, and targeted marketing strategies designed to meet the demands of urban consumers with fast-paced lifestyles. Additionally, the rising trend of health-conscious eating is prompting manufacturers to introduce low-fat and high-protein processed poultry options, further expanding the consumer base. Concurrently, the growth of Turkey's baked goods market, driven by product diversification and the growing presence of global companies, is creating synergistic opportunities for incorporating processed poultry into ready-meal solutions. Furthermore, the sector is advancing technologically with the adoption of National Salmonella Control Programs and Residue Monitoring Plans. These measures are pivotal in ensuring stringent food safety standards, which are instrumental in fostering consumer trust and confidence in processed poultry products.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Disease outbreaks such as avian influenza impacting production | -0.6% | National, with concentrated impact in high-density production areas | Short term (≤ 2 years) |

| Volatile export conditions due to trade restrictions | -0.4% | Export-oriented regions, particularly Mediterranean and Marmara | Medium term (2-4 years) |

| Seasonal consumption patterns limiting year-round demand | -0.3% | National, more pronounced in traditional consumption areas | Short term (≤ 2 years) |

| Competition from cheaper protein sources like chicken | -0.2% | National, affecting premium turkey and processed segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Disease outbreaks such as avian influenza impacting production

In November 2024, Turkey reported its first avian influenza outbreak in over a year, with the H5N1 strain detected on a poultry farm in Konya province. The outbreak resulted in the death of 211 birds from a flock of approximately 790,000, highlighting the susceptibility of large-scale poultry operations to disease outbreaks and the potential economic impact on the poultry sector. Between December 2024 and March 2025, the European Food Safety Authority documented 743 cases of highly pathogenic avian influenza across 31 European countries. This widespread prevalence has amplified regional biosecurity concerns, disrupted trade flows, and underscored the critical need for comprehensive preventive measures. In response, Turkish producers have adopted stricter biosecurity protocols, including enhanced sanitation measures and controlled farm access, alongside targeted vaccination strategies to mitigate the risk of future outbreaks. Furthermore, government veterinary services are actively conducting continuous and rigorous surveillance programs to detect infections early, enabling swift containment and minimizing the risk of cross-contamination across production facilities. These proactive and coordinated measures are essential for safeguarding the poultry industry, ensuring food security, and maintaining stability in both domestic and international trade operations.

Volatile export conditions due to trade restrictions

Between June and December 2024, Turkey's implementation of export quotas seeks to stabilize domestic chicken prices. This trade policy intervention highlights the far-reaching consequences of such measures, as it disrupts established international market relationships, reduces export revenues, and undermines the global competitiveness of Turkish poultry exporters. The situation is compounded by a 30% year-over-year surge in feed costs, driven by the depreciation of the Turkish Lira and Turkey's reliance on imported feed ingredients. These escalating costs are placing significant pressure on production economics, further eroding the ability of Turkish exporters to compete effectively in international markets. While the Ministry of Trade's price stabilization measures aim to protect domestic consumers from price volatility, they inadvertently introduce supply chain uncertainties for international buyers. These buyers, who depend on consistent supply and predictable pricing for long-term procurement planning, may shift to alternative sourcing options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Broiler Meat Dominance Drives Market Foundation

In 2025, broiler meat commands a dominant 63.42% market share, underscoring Turkish consumers' longstanding preference for fresh chicken. Turkey's robust production capacity, churning out 2.4 million metric tons of chicken meat in 2023 (accounting for 97.8% of the nation's total poultry output), bolsters this dominance. Major players, such as Şenpiliç and Banvit, seamlessly integrate operations from feed production to breeding and processing. Looking ahead, the segment anticipates a boost, with a record production forecast of 2.6 million metric tons in 2025, marking an 8% uptick. This surge is largely attributed to a rebound in domestic demand, especially after the lifting of export quotas set to expire in December 2024. In rural areas, traditional wet markets remain the go-to for broiler meat, thriving on personal relationships and cash transactions. Meanwhile, urban consumers, prioritizing quality and convenience, flock to modern retail formats that prominently feature fresh chicken varieties.

Processed meat is rapidly gaining traction, boasting a 6.73% CAGR projected through 2031. This growth is fueled by urbanization, the rise of dual-income households, and a growing appetite for convenience foods among working families. Innovations in nuggets, sausages, burgers, and marinated poultry products cater to consumers' evolving tastes, emphasizing ready-to-cook options that prioritize nutritional value and reduced prep time. The segment reaps rewards from the expansion of Quick Service Restaurants (QSRs) and the rise of delivery platforms, both of which demand standardized products that ensure speed and food safety. Strategic investments in Kahramanmaras position the sector to tap into the burgeoning processed meat demand, both at home and in regional export markets, bolstered by the competitive edge of Turkish halal certification. Enhancements in cold chain infrastructure pave the way for broader distribution of frozen and chilled products.

By Species: Chicken Leadership Faces Duck Segment Disruption

In 2025, chicken continues to dominate the market with a 65.02% share, driven by decades of strategic infrastructure investments, strong consumer familiarity, and cost-effective pricing compared to alternative protein sources. These factors solidify chicken as the preferred poultry choice across all income levels. Turkey's position as the 10th largest global chicken producer and 7th in poultry trade highlights its international competitiveness and adherence to high-quality standards, enabling exports to 97 countries as of 2023. The well-established supply chains, advanced breeding programs, and optimized feed efficiency contribute to cost advantages, ensuring chicken's affordability and accessibility across diverse economic segments. Additionally, compliance with halal certification standards supports both domestic consumption and export opportunities, catering to religious dietary requirements.

Duck is emerging as the fastest-growing poultry segment, with a projected CAGR of 7.53% through 2031. This growth is fueled by evolving consumer preferences for premium dining experiences, the diversification of ethnic cuisines, and the demand from affluent urban consumers seeking unique protein options beyond traditional chicken. The segment's rapid expansion reflects the increasing popularity of premium proteins, supported by the growth of the restaurant industry and greater exposure to international cuisines through tourism and cultural exchanges. Duck farming is strategically targeting high-end restaurants and specialty food retailers, while imports are supplementing domestic production to meet the rising demand from consumers willing to pay premium prices for superior quality and culinary sophistication.

By Nature: Conventional Production Maintains Scale While Organic Captures Premium Growth

In 2025, conventional production methods command an 84.62% market share in Turkey. This dominance is rooted in cost considerations, long-standing farming practices, and infrastructure investments. These investments prioritize efficiency and scale, ensuring affordability across Turkey's varied economic landscape. Turkey's robust integrated breeding programs, coupled with optimized feed efficiency, bolster this segment. Furthermore, government subsidies, with grants ranging from 60% to 100% for registered farmers, play a pivotal role in offsetting rising feed costs and production investments, ensuring the segment's viability. Decades of technological advancements benefit conventional producers, from scientifically-formulated feeds produced in specialized mills to automated processing systems and stringent biosecurity protocols. These advancements not only maximize conversion ratios but also curtail production costs. With over 15,000 broiler houses leveraging contractual breeding arrangements, producers optimize resource allocation and manage risks effectively.

Organic poultry is on a growth trajectory, boasting a 7.38% CAGR through 2031. This surge is fueled by health-conscious consumers, especially educated urbanites, who equate organic certification with enhanced nutritional value and superior animal welfare standards. These consumers are increasingly willing to pay a premium for perceived quality and environmental benefits. The organic poultry segment is riding the wave of sustainable living trends, emphasizing circular economy principles and eco-conscious consumption. Turkish consumers are becoming more attuned to the environmental and health ramifications of their food choices. Bolstered by government-supported cluster development projects and Turkey's favorable growing conditions, the nation is laying the groundwork for organic poultry production. These initiatives align with stringent European certification standards. The segment's growth is further amplified by marketing campaigns spotlighting health benefits, environmental sustainability, and ethical animal welfare practices.

By Distribution Channel: Retail Dominance Challenged by Foodservice Momentum

In 2025, retail channels, comprising supermarkets, hypermarkets, and traditional wet markets, hold a dominant 55.11% market share. These channels effectively cater to diverse consumer segments across urban and rural areas by leveraging well-established distribution networks and aligning with consumer shopping preferences. The prominence of retail channels highlights the strength of Turkey's retail food sector, where organized retailers lead grocery sales through modern formats that offer extensive product variety and advanced cold chain capabilities. Discount chains such as BIM, A101, and Şok continue to dominate the market by employing competitive pricing strategies that resonate with price-conscious consumers. The rapid growth of e-commerce is creating additional sales opportunities for poultry products, complementing the physical retail presence and expanding the overall market reach.

The foodservice channel is emerging as the fastest-growing segment, with a projected CAGR of 5.97% through 2031. This growth is attributed to the expansion of the restaurant industry, shifting dining habits among younger demographics, and the recovery of tourism, all of which are driving increased demand for commercial food preparation. The foodservice sector encompasses hotels, restaurants, and catering services, which are benefiting from the resurgence of business dining and evolving social dining trends. Turkey's position as a leading tourism destination, coupled with the growth of international hotel chains, underscores the critical role of reliable poultry supply chains in supporting these operations.

Geography Analysis

Turkey's poultry market, supported by a robust domestic base and strategic export capabilities, has established itself as a key player in poultry trade across Europe, Asia, and the Middle East. The domestic market dominates production and consumption, with the USDA's 2023 report indicating an annual per capita poultry consumption of 21.9 kg. This strong demand is driven by cultural dietary preferences, the affordability of poultry compared to other protein sources, and the consistent availability of poultry products. The Marmara region, particularly around Istanbul, serves as the primary production hub, ensuring efficient distribution to major domestic markets. Additionally, western and central Anatolia contribute significantly to production capacity, benefiting from favorable agricultural conditions, advanced farming technologies, and continuous infrastructure development. These factors collectively enhance the supply chain's efficiency, reliability, and scalability, positioning Turkey's poultry market for sustained growth.

Turkey's poultry export market is highly diversified, reaching 97 countries, and the nation ranks as the 7th largest global player in live poultry trade. According to the ITC Trade Map, Turkey exported approximately 26,327 tons of poultry in 2024, valued at USD 65.1 million. The European Union remains a critical trade partner under the 1995 Customs Union agreement, with bilateral trade exceeding EUR 210 billion in 2024, reinforcing Turkey's position as the EU's 5th largest trade partner. The Middle East is another significant export destination, driven by the region's demand for halal-certified products that align with its dietary requirements.

Additionally, after a decade of negotiations, Turkey has successfully entered the Chinese market, unlocking substantial long-term growth opportunities for its poultry exports. To further strengthen its logistics network, Turkey is advancing its High-Speed Train Project, which aims to establish over 5,600 km of rail lines by 2025. This initiative is expected to enhance connectivity to ports and border crossings, streamline distribution networks, and solidify Turkey's competitive position in the global poultry market.

Competitive Landscape

The Turkish poultry meat market is moderately consolidated, with regional players actively competing to strengthen their market presence. Leading companies in the market include SenpiliG Glda Sanayi A.Ş., BEYPI Inc., BRF Global, and Keskinoélu Tavukquluk ve Damzllk isletmeleri San. Tic. A. S.. These players are implementing strategies such as capacity expansions, product innovations, and strategic partnerships to maintain and enhance their competitive edge in the poultry meat market.

The competitive dynamics of the sector reflect Turkey's role as a significant regional poultry hub. Companies compete on various fronts, including production scale, product innovation, distribution networks, and export capabilities to cater to diverse international markets. Technological adoption within the sector is focused on enhancing biosecurity measures, optimizing feed efficiency, and ensuring compliance with international standards. Key initiatives include the implementation of National Salmonella Control Programs and E-Prescription systems for veterinary products.

The competitive landscape is further supported by government programs such as IPARD and agricultural subsidies, which enable smaller operators to modernize their facilities. Meanwhile, larger companies are leveraging these advancements to expand their presence in export markets and diversify their product portfolios, ensuring sustained growth and competitiveness in the global poultry industry.

Turkey Poultry Industry Leaders

-

SenpiliG Glda Sanayi A.S.

-

BEYPI Inc

-

BRF Global

-

Keskinoélu Tavukquluk ve Damzllk isletmeleri San. Tic. A. S.

-

Erpilic Entegre Tavukculuk Ijretim Pazarlama ve Ticaret A.S.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Keskinoğlu introduced its range of delicious products at Yerelist, highlighting its expertise in chicken meat, table eggs, pasteurized eggs, and further processed poultry products, all produced at its advanced facilities in Manisa Akhisar. Now part of the Matlı Group of Companies, Keskinoğlu benefits from expanded capabilities across the protein chain, including feed and dairy, further strengthening its position in the Turkish poultry sector.

- June 2025: As part of its expansion efforts, Keskinoğlu became an officially approved research and development Center by the Ministry of Industry of the Republic of Turkey on June 27, 2025, marking a significant milestone in its innovation journey. This recognition enables the company to further advance its research and development activities, supporting the creation of high-value products and technologies within the poultry sector. The new research and development center status strengthens Keskinoğlu’s competitive edge, aligning with Turkey’s broader push for technology-driven growth and industry leadership

- April 2025: BRF achieved a milestone: all its slaughter units received international Animal Welfare certifications, with Turkey's operations marking the final step in this commitment.

- September 2024: In 2024, Pınar unveiled plans to align its product development with consumer insights. With an eye on broadening its audience, Pınar set out to enhance its product lineup, aiming to elevate brand awareness and reach a wider consumer base.

Turkey Poultry Market Report Scope

Poultry refers to domesticated birds kept for their meat, eggs, and feathers. The Turkish poultry market is segmented into product types and distribution channels. Based on product type, the market is segmented into table eggs, broiler meat, and processed meat. The processed meat segment is further sub-segmented into nuggets, sausages, burgers, marinated poultry products, and other processed meat products. Based on the distribution channel, the market is segmented into hotels, restaurants, catering, modern trade, and other distribution channels. The report offers the market sizes and forecasts in value terms (USD) for all the abovementioned segments.

| Table Eggs | |

| Broiler Meat | |

| Processed Meat | Nuggets |

| Sausages | |

| Burgers | |

| Marinated Poultry | |

| Other Processed Products |

| Conventional |

| Organic |

| Chicken |

| Turkey |

| Duck |

| Others |

| Foodservice | Hotels |

| Restaurants | |

| Catering | |

| Other On-Trade Channels | |

| Retail | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Other Distribution Channels |

| By Product Type | Table Eggs | |

| Broiler Meat | ||

| Processed Meat | Nuggets | |

| Sausages | ||

| Burgers | ||

| Marinated Poultry | ||

| Other Processed Products | ||

| By Nature | Conventional | |

| Organic | ||

| By Species | Chicken | |

| Turkey | ||

| Duck | ||

| Others | ||

| By Distribution Channel | Foodservice | Hotels |

| Restaurants | ||

| Catering | ||

| Other On-Trade Channels | ||

| Retail | Supermarkets/Hypermarkets | |

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the current size of the Turkey poultry market?

The Turkey poultry market is valued at USD 14.22 billion in 2026.

How fast is the Turkey poultry market expected to grow?

It is projected to expand at a 5.89% CAGR, reaching USD 18.93 billion by 2031 over 2026-2031.

Which product segment leads the Turkey poultry market?

Broiler meat leads with 63.42% market share, while processed meat is the fastest-growing at 6.73% CAGR.

What are the key growth drivers for the Turkey poultry market?

Lean-protein preferences, ketogenic diet adoption, QSR expansion, and convenience-food demand are the primary drivers.

Page last updated on: