Montan Wax Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

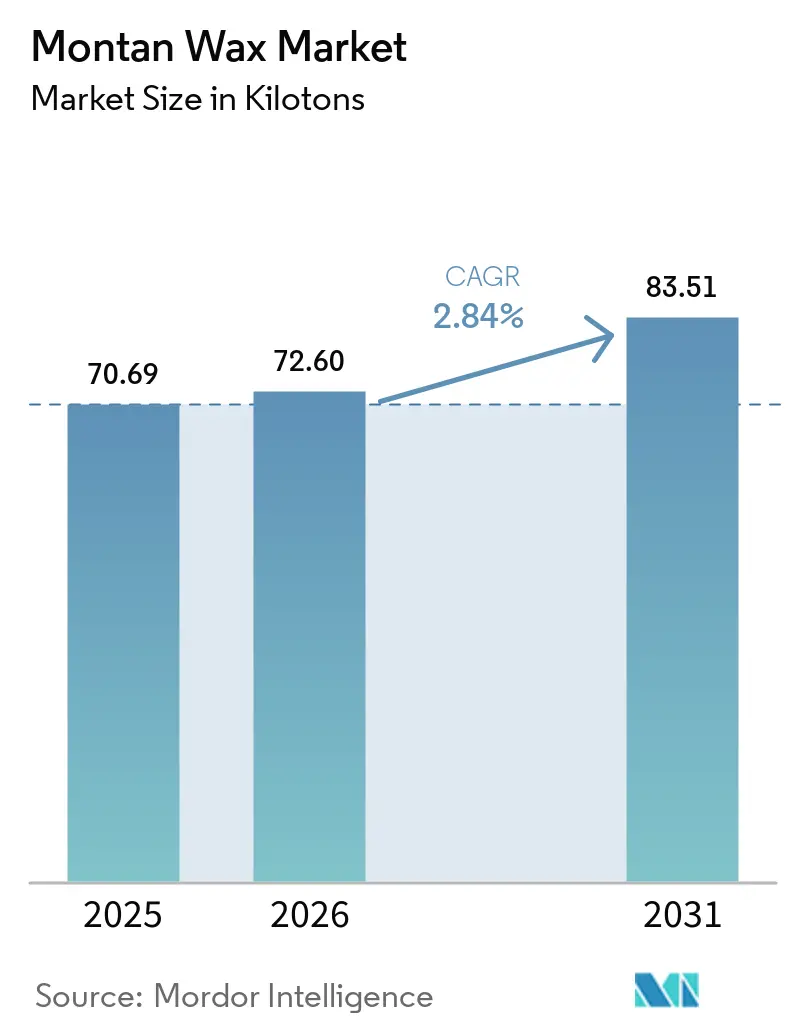

| Market Volume (2026) | 72.60 kilotons |

| Market Volume (2031) | 83.51 kilotons |

| Growth Rate (2026 - 2031) | 2.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

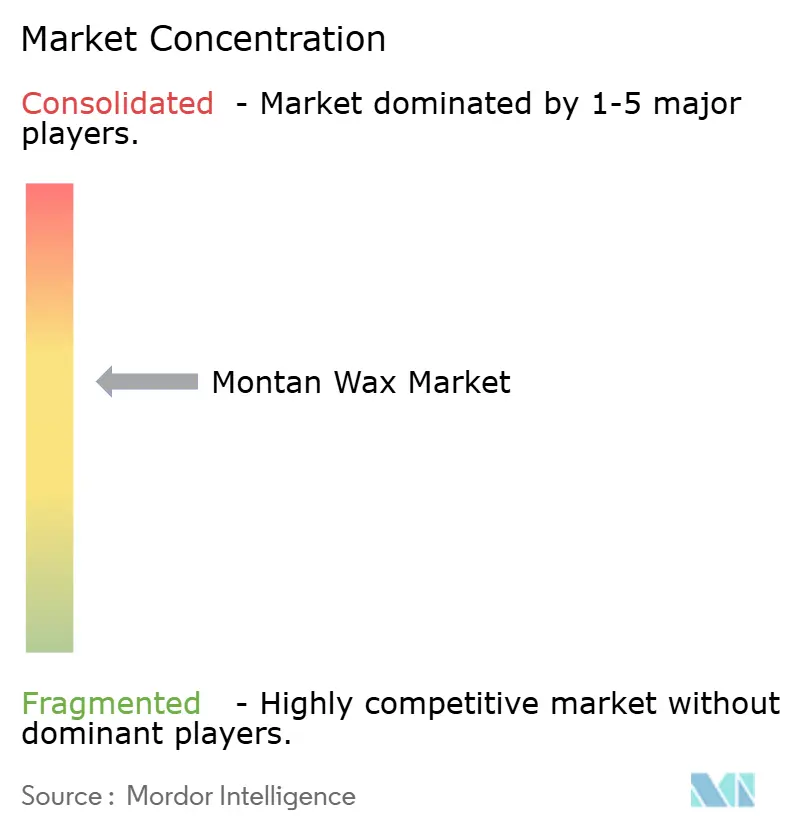

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Montan Wax Market Analysis by Mordor Intelligence

The Montan Wax Market size is expected to increase from 70.69 kilotons in 2025 to 72.60 kilotons in 2026 and reach 83.51 kilotons by 2031, growing at a CAGR of 2.84% over 2026-2031. This growth is supported by rising demand for specialty lubricants in thermoplastics, a trend toward premium detailing in automotive after-sales, and consistent orders from printing-ink and industrial-coating formulators across major regions. While there is competition from rice-bran, Fischer-Tropsch, and other bio-based waxes, the unique attributes of crude and modified grades, such as a high melting point, excellent slip, and low-abrasion profile, ensure montan wax's stronghold in cost-sensitive industrial chains. In Europe, tightening regulations on polycyclic aromatic hydrocarbons (PAHs) are pushing producers to invest in refined, low-PAH grades. Instead of exiting the category, they are making technical upgrades like bleaching, oxidation, and esterification, which are opening doors to higher-margin opportunities in cosmetics and biopolymer processing. The Asia-Pacific region, with a significant portion of global plastics conversion and a growing middle-class consumer base, is outpacing global averages. This momentum ensures the montan wax market's robust growth trajectory, even amidst concerns over feedstock scarcity.

Key Report Takeaways

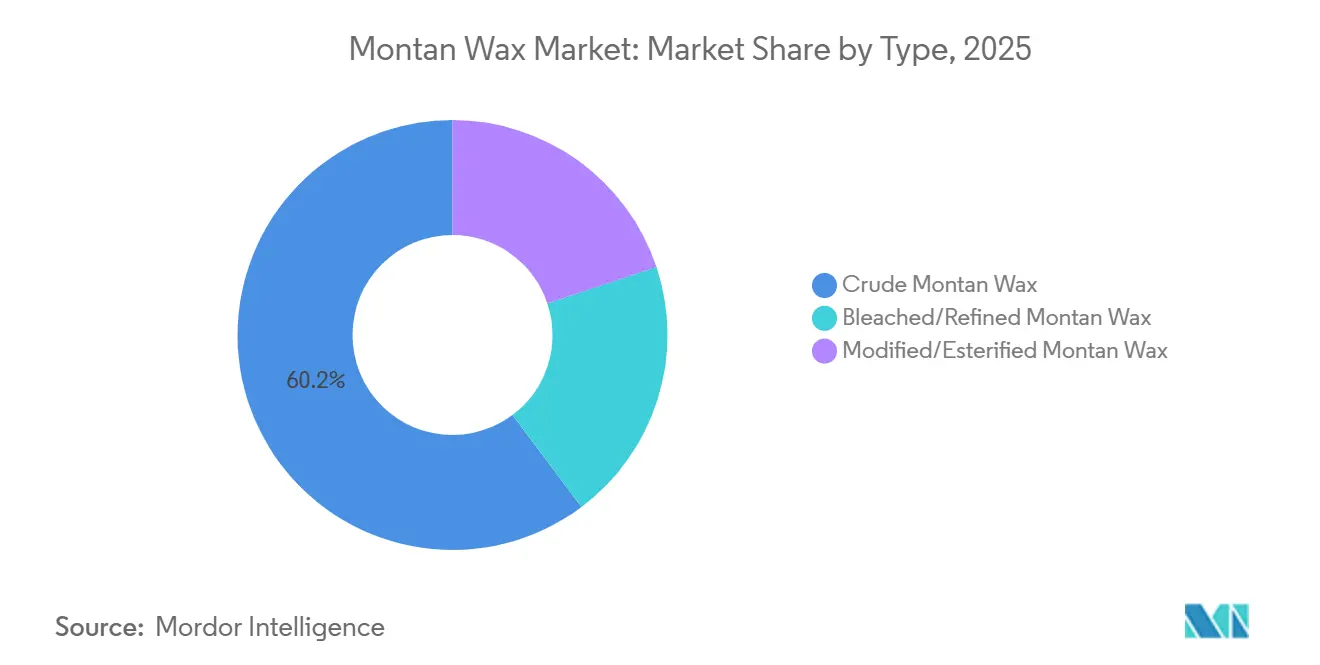

- By type, crude grades dominated with 60.24% of the montan wax market share in 2025, whereas modified and esterified variants are forecast to advance at a 3.45% CAGR from 2026 to 2031.

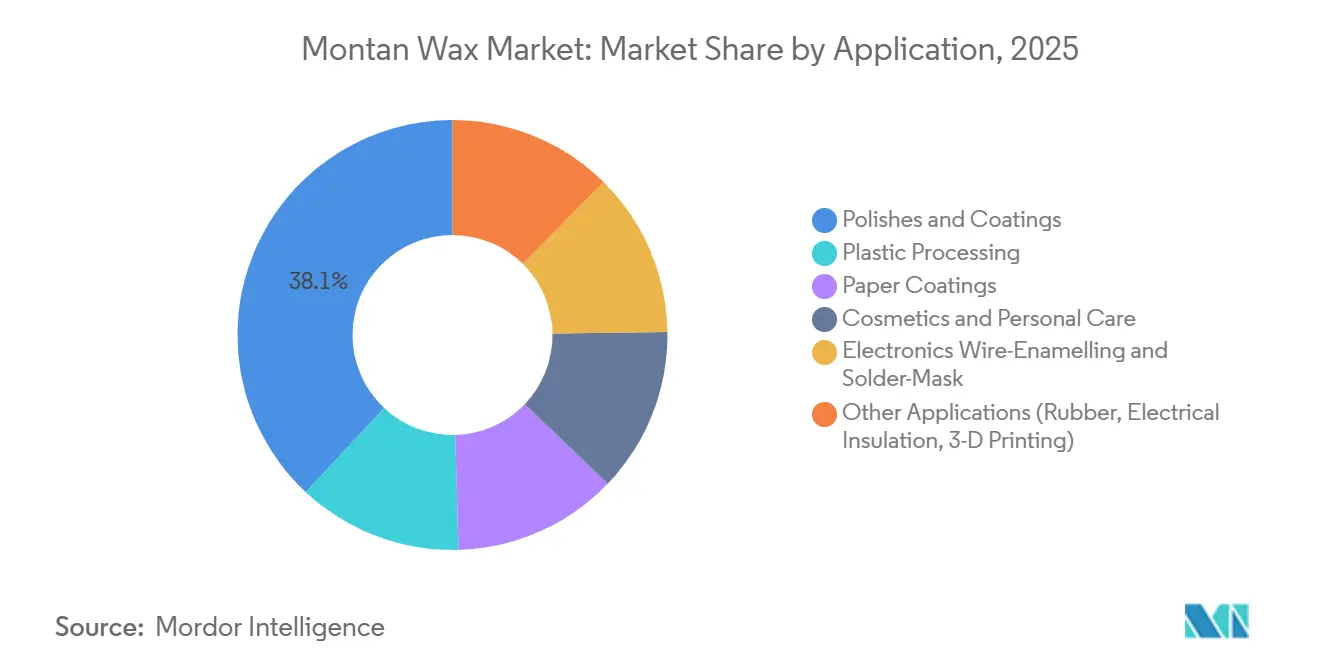

- By application, polishes and coatings led with a 38.05% revenue share of the montan wax market size in 2025, while the cosmetics and personal care segment is expected to grow 3.60% of the fastest rate from 2026 to 2031.

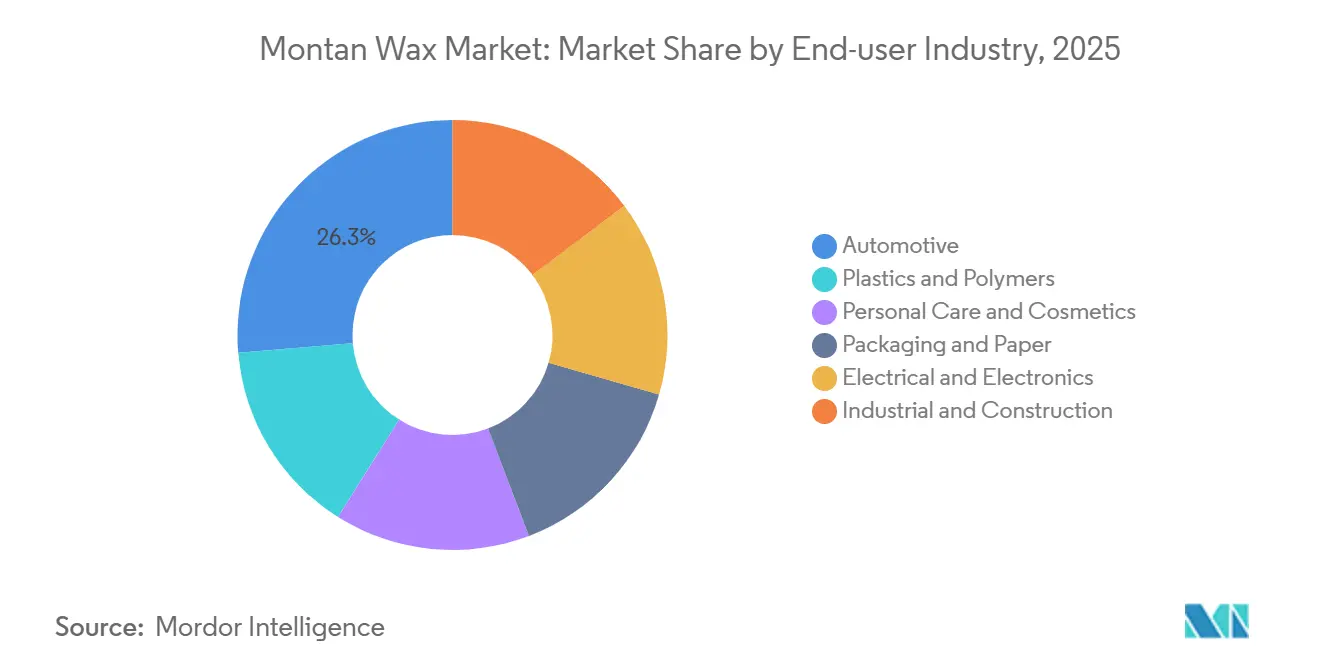

- By end user, automotive held 26.32% of the montan wax market size in 2025, whereas personal care is projected to expand at 3.56% CAGR between 2026 and 2031.

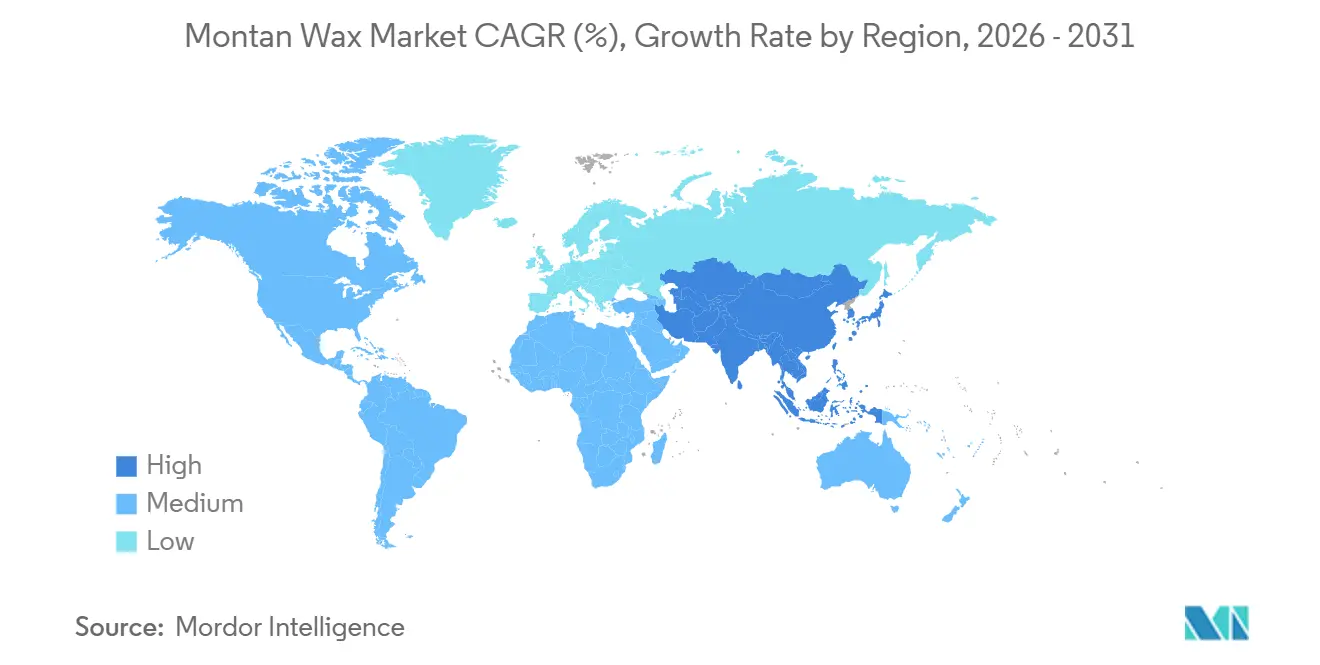

- By geography, Asia-Pacific accounted for 42.20% volume in 2025 and is on track for a 3.51% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Montan Wax Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use in automotive polishes and detailing formulations | +0.8% | Global, led by North America, Europe and APAC automotive hubs | Medium term (2–4 years) |

| Expanding demand as lubricant/release agent in thermoplastics | +0.7% | Global, highest in APAC and North America plastics clusters | Long term (≥4 years) |

| Rising adoption in cosmetics and personal-care emulsions | +0.6% | Global, led by Europe, North America and emerging APAC | Medium term (2–4 years) |

| Rapid uptake in 3-D-printing filament surface modifiers | +0.2% | North America, Europe and select APAC centers | Long term (≥4 years) |

| Utilization in encapsulating hazardous-waste barriers | +0.1% | North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Use in Automotive Polishes and Detailing Formulations

As vehicle aesthetics gain prominence, the demand for premium wax blends that offer deep gloss, UV resistance, and quick application has surged. In this landscape, formulators are increasingly gravitating toward high-melting montan grades. These grades not only resist detergent attacks but also uphold protective films during automated washes, leading to extended service intervals and heightened perceived value. The montan wax market is reaping the benefits of water-borne dispersion technology, which adheres to low-VOC standards without compromising on shine. This is particularly important for retailers in North America and Europe, where regulatory oversight is strict. Meanwhile, in China and India, a growing middle class is fueling a professional detailing surge, bolstering double-digit consumption growth in regional blending centers. Additionally, manufacturers of polishing pastes are capitalizing on montan wax's synergy with silica, alumina, and polymer micro-abrasives. This allows them to craft single-step compounds that not only correct but also safeguard paint surfaces, resulting in increased per-unit wax loadings.

Expanding Demand as Lubricant/Release Agent in Thermoplastics

High-volume plastics processors prioritize consistent melt flow and rapid cycle times. By adding 0.5% to 3% montan wax, they achieve these objectives and notably reduce plate-out, especially in high-shear applications like polyvinyl chloride and polyethylene terephthalate profiles. In the Asia-Pacific region, extrusion and injection-molding facilities are running at full capacity to meet the surging demands of packaging and electronics. These facilities are increasingly turning to bleached and oxidized montan waxes. These waxes offer internal lubrication benefits without sacrificing clarity or mechanical strength. Modified grades, especially calcium montanate, not only facilitate easy pigment dispersion but also bolster the montan wax market, granting color-masterbatch producers greater design flexibility. As biopolymers like polylactic acid gain popularity, esterified montan wax stands out for its polar compatibility, ensuring processors can maintain productivity on their current equipment.

Rising Adoption in Cosmetics and Personal-Care Emulsions

As clean-beauty claims and vegan labeling trends gain traction, ingredient formulations are increasingly favoring naturally derived, performance-oriented structuring agents. Refined montan waxes are stepping up to this challenge, enabling the creation of glossy sticks, film-forming mascaras, and transfer-resistant lipsticks, all at minimal dosage levels. European formulators appreciate montan wax's ability to craft stable anhydrous balms, resilient to summer storage temperatures without the risk of sweating, giving it an advantage over softer botanical waxes. In North America, top brands emphasize the mineral origin of their bleached grades, setting them apart from palm-derived counterparts. Meanwhile, Asian markets show a preference for hybrid systems, where montan wax is co-gelled with rice-bran wax, enhancing both payoff and glide. Consequently, the montan wax market secures incremental volume while capturing premium price points.

Rapid Uptake in 3-D-Printing Filament Surface Modifiers

Proprietary wax-infused filaments are becoming important in fused deposition modeling, as they help lower melt viscosity, reduce warpage, and achieve a smoother surface finish for easier post-processing. Modified montan grades, which provide thermal stability up to 90 °C, align perfectly with the extrusion windows of PLA and ABS, thereby minimizing the risk of nozzle clogging. In Europe and the United States, industrial printer OEMs are now bundling montan-lubricated filaments with desktop units, specifically targeting engineering-prototype users. This strategy has led to the emergence of small but scalable demand pockets, ensuring the montan wax market remains technologically relevant.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited lignite reserves and mining restrictions | –0.5% | Europe (Germany primary), global supply-chain ripple | Short term (≤ 2 years) |

| Substitution threat from synthetic and bio-based waxes | –0.4% | Global, strongest in EU and North America | Medium term (2–4 years) |

| Tightening EU-REACH limits on PAH traces in waxes | –0.2% | Europe, spillover to export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Lignite Reserves and Mining Restrictions

Germany's lignite belts, known for their crude montan wax production, are facing resource depletion and tighter environmental regulations. These challenges come at a time when downstream demand is diversifying[1]Packaging Europe, “Germany’s CO₂ Pricing Scheme and Industrial Implications,” packagingeurope.com. While ROMONTA operates with an integrated approach, its vertically aligned structure struggles against the finite limits of accessible ore. Furthermore, EU carbon-pricing regulations are set to rise from EUR 45 to EUR 55 per tonne of CO₂ by 2025. This increase in production costs is pushing spot prices higher, causing concern among converters in North America and Asia who depend on imported feedstock. As a result, the montan wax market is experiencing extended lead times, leading to inventory hoarding and forward-buying across distributor networks.

Substitution Threat from Synthetic and Bio-Based Waxes

Consumer brand owners increasingly favor renewable or lower-carbon options, such as rice-bran and Fischer-Tropsch waxes, for food-contact packaging, personal care items, and fast-moving consumer goods. Clariant's recent EU-wide approval allows converters to use up to 0.3% rice-bran wax in rigid plastics, offering an immediate compliant alternative and reducing dependence on lignite-derived materials. As a result, the montan wax market is required to compete on value, focusing on cost-effectiveness, elevated melting points, and a history of performance in demanding industrial applications spanning decades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modified Grades Capture Premium as Crude Dominates Volume

In 2025, crude material clinched 60.24% of the montan wax market share, leveraging its cost-effectiveness to secure contracts in asphalt modifiers, gypsum-board hydrophobization, and foundry release agents. However, the market is shifting toward esterified and oxidized derivatives. These derivatives are increasingly favored by the cosmetic, biopolymer, and electronics sectors, which prioritize attributes like lighter color, reduced odor, and specific melting-point ranges. Modified grades, growing at a 3.45% CAGR, are also driving advancements in 3-D printing and high-temperature fiber-spinning, bolstering the overall montan wax market. Through chemical tailoring such as acid-number adjustment and partial saponification, formulators can achieve niche rheological targets unattainable by crude wax, justifying premium pricing and, in certain instances, securing long-term offtake agreements.

Even when the cost difference can surpass 30%, end users, prioritizing regulatory compliance and brand positioning, willingly absorb the extra expense. This is particularly true when the alternative involves overhauling an entire formulation to fit a different rheology modifier. As a result, modified montan wax enjoys a profit margin that exceeds its volume contribution, shielding suppliers from fluctuations in raw material costs and underscoring the rationale for sustained R&D investments in the montan wax market.

By Application: Cosmetics Outpace Polishes Despite Smaller Base

In 2025, polishes and coatings accounted for 38.05% of consumption, maintaining their position as the largest segment in the montan wax market. Automotive waxes, wood care products, and floor finishes continue to favor montan wax for its combination of high gloss, scratch resistance, and water beading properties. While currently a smaller segment, the cosmetics and personal care industry is set to grow at an annual rate of 3.60% through 2031, supported by clean-label positioning and vegan certification initiatives. This growth trajectory suggests that the montan wax market for cosmetics will grow faster than the overall market, driven by premium unit values and higher margins compared to industrial applications.

Montan wax serves a dual role as both an internal and external lubricant in engineering plastics, enabling compounders to achieve cycle-time reductions of up to 20% on older equipment. While paper and paperboard barrier coatings still hold significance, they are increasingly challenged by PFAS-free synthetic waxes that align with repulpability standards. However, innovations in hybrid emulsions, where montan wax imparts hydrophobicity and starches provide bonding, ensure the montan wax market remains active in this domain.

By End-User Industry: Automotive Dominates, Electronics Closes Gap

Automotive accounted for 26.32% of the montan wax market size in 2025 on the back of premium polish usage during new-vehicle detailing and aftermarket upkeep. Luxury OEMs apply wax-rich sealants at factory outlets to guarantee paint-finish warranties, locking in baseline demand irrespective of passenger-car sales swings. Electric-vehicle scale-up adds new sub-segments such as ceramic-plus-wax composite films designed to reduce drag coefficients.

Driven by clean-beauty trends, a rising demand for ECOCERT certification, and innovative formulations in stick products, emulsions, and color cosmetics, the personal care and cosmetics sector is witnessing a robust growth rate of 3.56% CAGR. Völpker's WARADUR series caters to a range of personal-care applications, from hair wax and sunscreens to mascara, eyeliner, and scrubs. Notably, WARADUR XE is tailored for tablet and dragee coatings, serving both the pharmaceutical and confectionery industries. Plastics and polymers processing remains a stable mid-sized user group, where montan wax supports recycled-content blends by mitigating viscosity spikes. Construction chemicals likewise integrate wax in water-repellent admixtures for cementitious surfaces exposed to freeze-thaw cycles.

Geography Analysis

In 2025, Asia-Pacific accounted for 42.20% of the volume, driven by a robust automotive supply chain in China and Japan, coupled with a burgeoning personal-care manufacturing sector in India and ASEAN[2]Clariant AG, “Licocene and Montan Wax Capacity Expansion,” clariant.com. In the region, automotive detailing consumables are gravitating toward premium spray waxes and ceramic-infused polishes, both of which depend on montan wax for their film integrity. South Korean K-beauty brands are blending montan wax with rice-bran wax, striking a balance between sustainability and performance, indicating a trend of coexistence over outright substitution.

North America, with its established distribution channels and a strong DIY car care culture, continues to see robust demand, even with the rise of ceramic coatings. In response to stringent VOC and PFAS regulations, formulators are pivoting to water-borne montan dispersions, achieving similar gloss without solvents, bolstering the regional montan wax market. Additionally, Mexico's expanding plastics processing sector is importing refined grades for its injection-molded consumer goods, solidifying the continent's consumption.

Europe stands as both the birthplace and a testing ground for the montan wax market. While German producers like ROMONTA and Völpker set global standards for quality and expertise, challenges like carbon-pricing schemes and lignite depletion hinder their expansion. Concurrently, EU regulatory challenges are spurring R&D initiatives aimed at producing low-PAH, food-contact-compliant grades. A successful pivot here could pave the way for new growth opportunities. Looking ahead, potential substitution threats might drive European firms to forge joint ventures in Asia, where feedstock limitations are less pronounced.

Competitive Landscape

In the montan wax market, a few integrated and specialty players dominate, though the landscape remains moderately consolidated. ROMONTA, the leading global crude producer, has leveraged a century-old mining concession, operating a dedicated extraction plant and downstream formulation units that cater to 23 countries. Clariant, leveraging its strong global procurement network and a widespread continental presence, has positioned montan wax as one of its Top 20 materials by cost share, while also leading the charge in innovations for modified and bio-hybrid grades.

Specialists like Völpker, Deurex, Koster Keunen, and Poth Hille in on application-specific performance. They provide bleached, oxidized, or esterified variants tailored for cosmetics, ink, and polymer processing. Newcomers to the montan wax scene, particularly biowax innovators, are blending rice-bran or sunflower wax with montan foundations to craft hybrid properties. This evolution is nudging established players toward forming strategic alliances or pursuing targeted acquisitions. A case in point is Paramelt’s acquisition of Kahl in February 2026, highlighting the consolidation trend and the ambition to unify natural waxes under a singular technical umbrella.

Research institutions like Brookhaven National Laboratory and Michigan State University are pioneering ventures beyond conventional applications. They are exploring avenues such as nuclear-waste encapsulation and PFAS-free paper coatings. Such innovations not only promise to diversify revenue streams but also bolster entry barriers through exclusive expertise. Suppliers who can certify features like radiation resistance or biodegradability stand to secure lucrative contracts, ensuring the montan wax market's vitality in the mid-term, even as traditional segments like automotive and polishing reach maturity.

Montan Wax Industry Leaders

Clariant

ROMONTA GmbH

TianshiWax

VÖLPKER SPEZIALPRODUKTE GMBH

Yunphos

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Clariant received EU approval for Licocare rice-bran wax additives at up to 0.3% in food-contact plastics, framing a renewable alternative that claims a 70% lower carbon footprint versus montan wax.

- February 2026: Paramelt acquired a majority stake in German natural-wax maker Kahl to deepen its portfolio of nature-derived waxes for beauty, home care and food sectors.

Global Montan Wax Market Report Scope

Montan wax is a hard, naturally occurring, solvent-extracted wax derived from lignite (brown coal), valued for its high melting point, stability, and high gloss. Primarily used in polishes, plastics, and coatings, montan wax acts as a lubricant, release agent, and consistency enhancer.

The montan wax market is segmented by type, application, and end-user industry. By type, the market is segmented into crude montan wax, bleached/refined montan wax, and modified/esterified montan wax. By application, the market is segmented into polishes and coatings, plastic processing, paper coatings, cosmetics and personal care, electronics wire-enamelling and solder-mask, and other applications (including rubber, electrical insulation, and 3-D printing). By end-user industry, the montan wax market is segmented into automotive, plastics and polymers, personal care and cosmetics, packaging and paper, electrical and electronics, and industrial and construction. The report also covers the market size and forecasts for montan wax in 17 countries across the world. For each segment, market sizing and forecasts are provided in terms of volume (tons).

| Crude Montan Wax |

| Bleached / Refined Montan Wax |

| Modified / Esterified Montan Wax |

| Polishes and Coatings |

| Plastic Processing |

| Paper Coatings |

| Cosmetics and Personal Care |

| Electronics Wire-Enamelling and Solder-Mask |

| Other Applications (Rubber, Electrical Insulation, 3-D Printing) |

| Automotive |

| Plastics and Polymers |

| Personal Care and Cosmetics |

| Packaging and Paper |

| Electrical and Electronics |

| Industrial and Construction |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Crude Montan Wax | |

| Bleached / Refined Montan Wax | ||

| Modified / Esterified Montan Wax | ||

| By Application | Polishes and Coatings | |

| Plastic Processing | ||

| Paper Coatings | ||

| Cosmetics and Personal Care | ||

| Electronics Wire-Enamelling and Solder-Mask | ||

| Other Applications (Rubber, Electrical Insulation, 3-D Printing) | ||

| By End-user Industry | Automotive | |

| Plastics and Polymers | ||

| Personal Care and Cosmetics | ||

| Packaging and Paper | ||

| Electrical and Electronics | ||

| Industrial and Construction | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for the montan wax market in 2031?

The Montan Wax Market size is expected to increase from 70.69 kilotons in 2025 to 72.60 kilotons in 2026 and reach 83.51 kilotons by 2031, growing at a CAGR of 2.84% over 2026-2031.

How fast is demand for montan wax in Asia-Pacific growing?

Asia-Pacific consumption is advancing at 3.51% CAGR through 2031, the highest among all regions.

Which application segment is expanding most rapidly?

Cosmetics and personal care are forecast to grow 3.60% annually, outpacing traditional polishing uses.

Why are modified montan wax grades gaining traction?

Esterified and oxidized variants offer lower color, reduced odor and better compatibility with polar polymers, driving a 3.45% CAGR to 2031.

Page last updated on: