Microcrystalline Wax Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

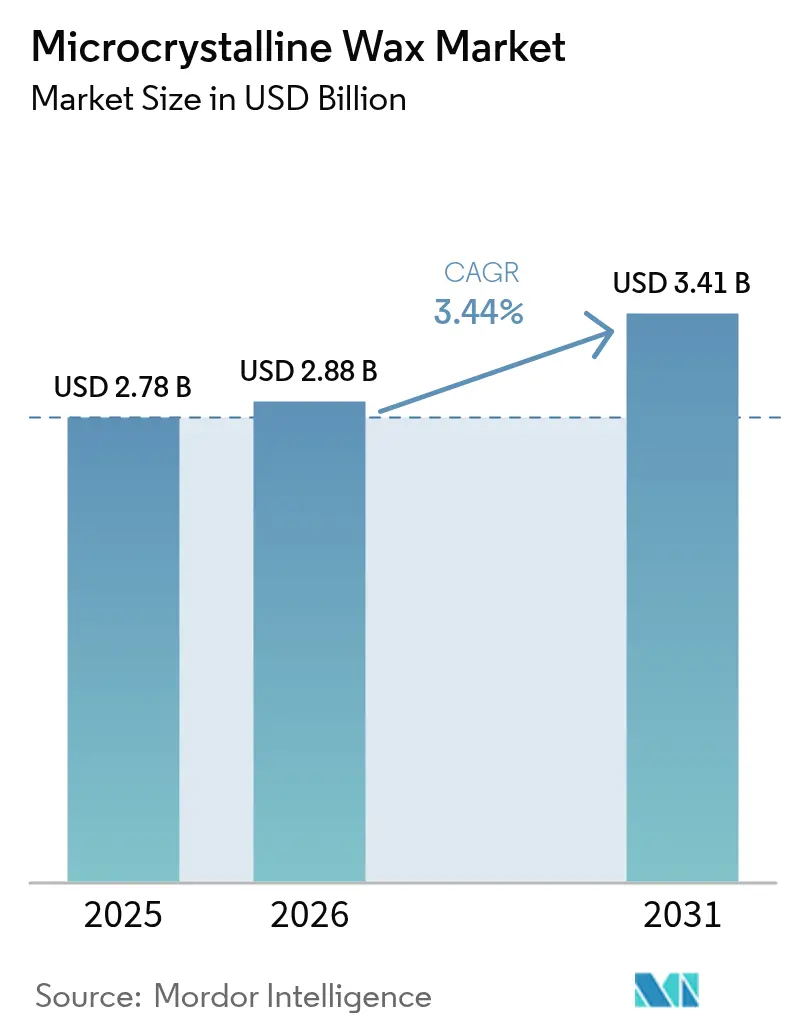

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 3.41 Billion |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microcrystalline Wax Market Analysis by Mordor Intelligence

The Microcrystalline Wax market size is expected to grow from USD 2.78 billion in 2025 to USD 2.88 billion in 2026 and is forecast to reach USD 3.41 billion by 2031 at 3.44% CAGR over 2026-2031. Steady expansion in cosmetics, adhesives and pharmaceutical uses underpins this trajectory, while the shift toward bio-based feedstocks, refinery upgrades and sustainability-driven innovation recalibrate competitive positioning. Higher melting points of 63-91 °C, excellent flexibility and superior fragrance retention continue to differentiate microcrystalline grades from paraffin, enabling formulators to meet performance demands in tropical climates. Asia-Pacific entrenches its leadership through cost-effective production, rising domestic demand and large-scale refinery projects in China and India that ensure reliable feedstock. Meanwhile, sustainability metrics—such as SASOLWAX LC100’s 35% lower emissions—now form a critical purchase criterion for downstream users, especially premium beauty brands.

Key Report Takeaways

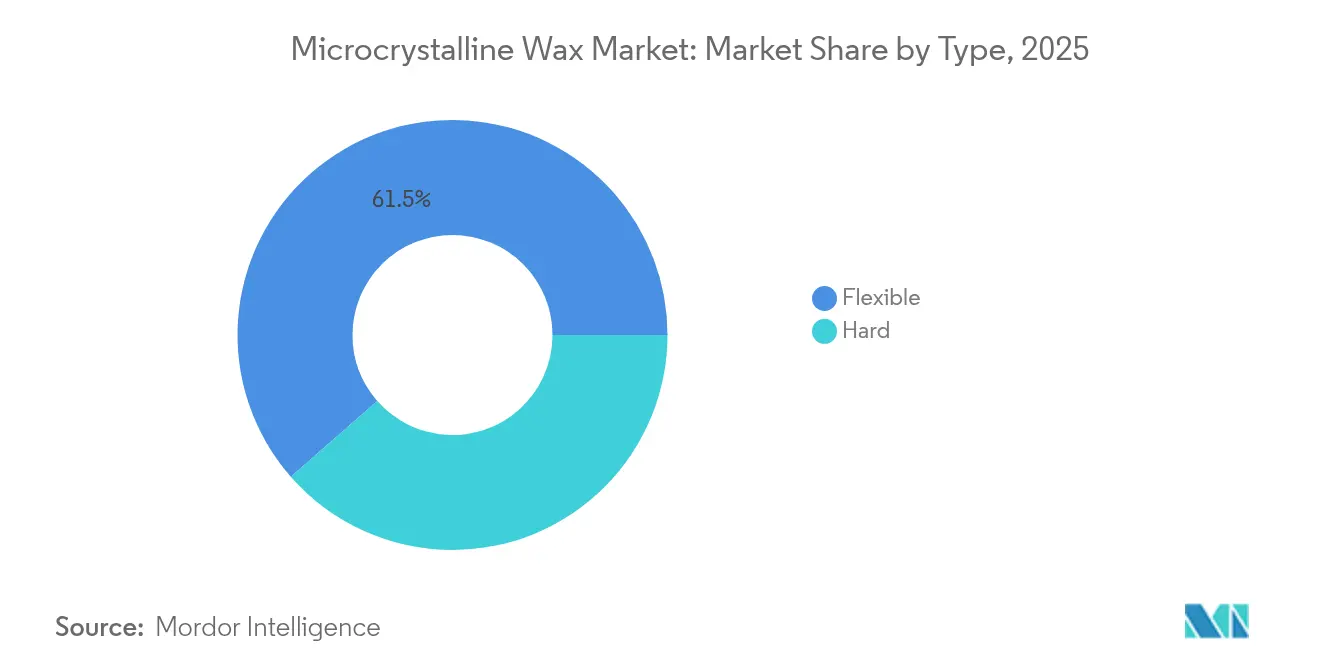

- By type, flexible variants held 61.45% of microcrystalline wax market share in 2025, while hard grades are forecast to grow at a 4.01% CAGR through 2031.

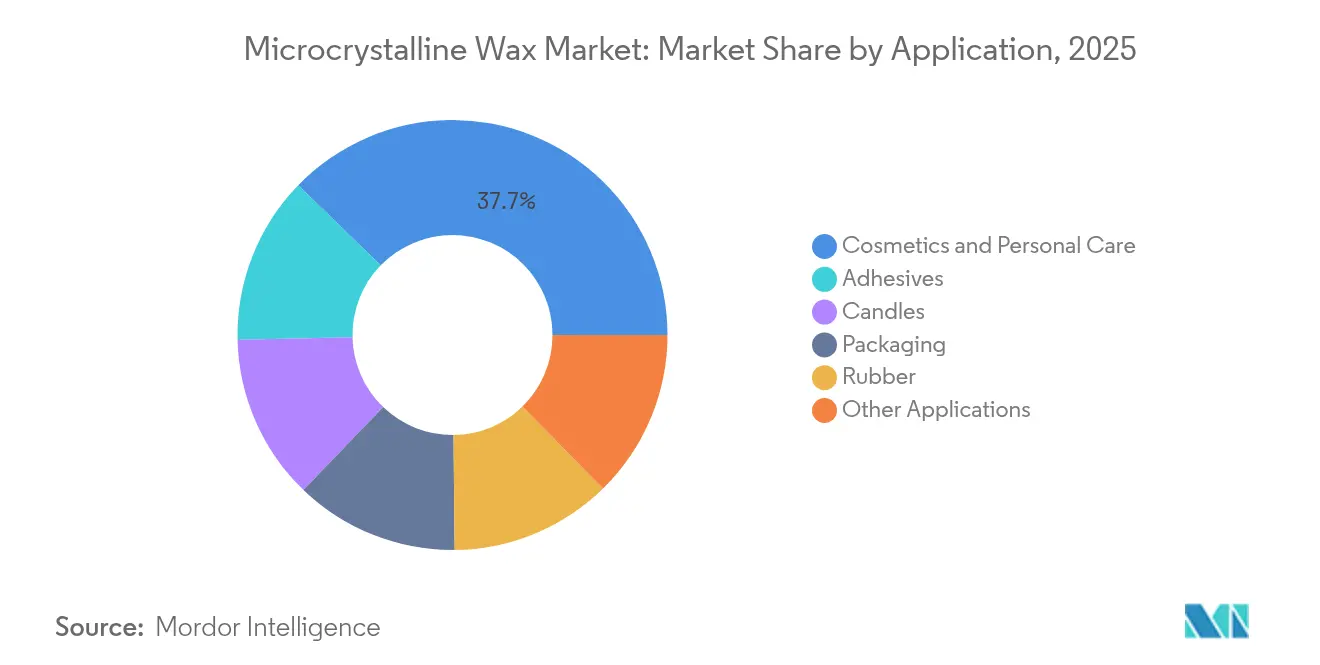

- By application, cosmetics and personal care accounted for 37.74% of the microcrystalline wax market size in 2025; adhesives are expected to post the fastest 3.96% CAGR to 2031.

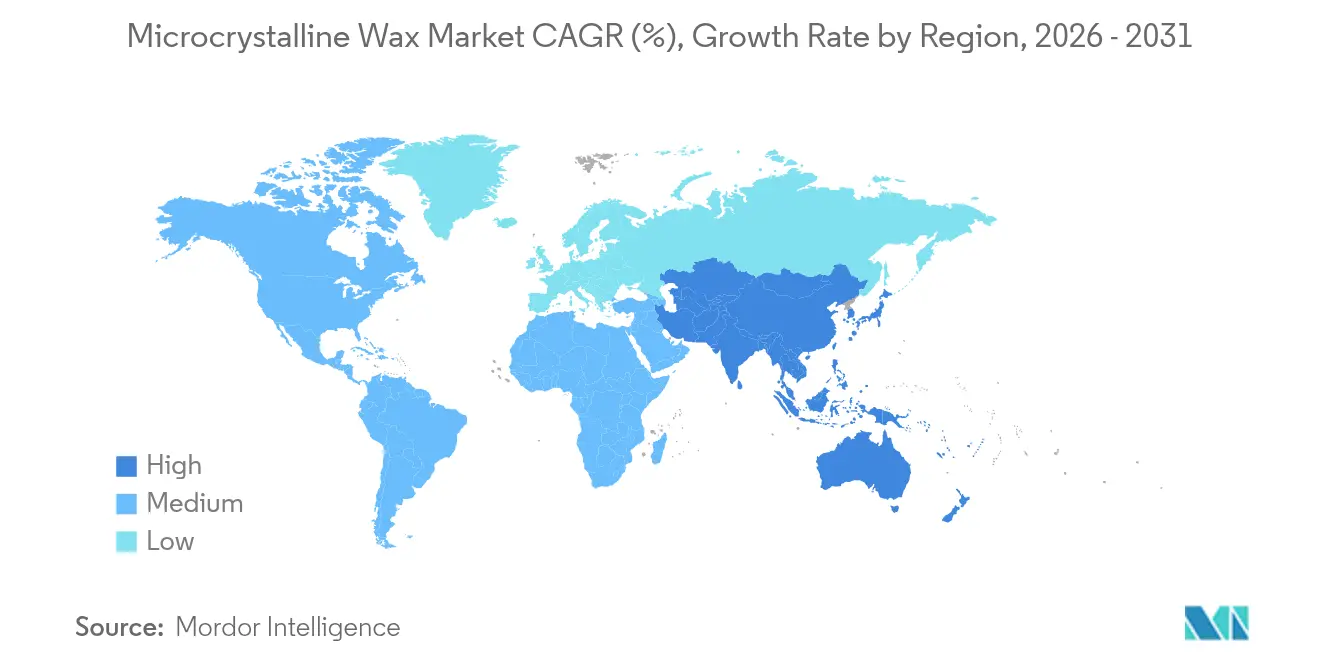

- By geography, Asia-Pacific commanded 46.85% revenue share in 2025 and is set to expand at a 3.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microcrystalline Wax Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Cosmetics and Personal-Care Manufacturing Bases | +0.8% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Growing Demand from Pharmaceutical and Medical Applications | +0.6% | Global, with concentration in North America and EU | Long term (≥ 4 years) |

| Substitution of Paraffin with Microcrystalline Wax in Hot-Melt Adhesives | +0.7% | Global, early adoption in North America | Short term (≤ 2 years) |

| Shift Toward Bio-Based Feedstock Upgrading at Refineries | +0.5% | EU and North America regulatory-driven, APAC following | Long term (≥ 4 years) |

| Growth of Low-Temperature Food-Contact Coatings for Sustainable Packaging | +0.4% | Global, with EU leading regulatory compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Cosmetics and Personal-Care Manufacturing Bases

Asia-Pacific contract manufacturers scale up lipstick, balm and premium skin-care production, and microcrystalline wax enhances texture, prevents sweating and stabilizes emulsions under tropical temperatures[1]Veda Oils, “Functions of Microcrystalline Wax in Cosmetics,” vedaoils.com. Large OEM hubs in China and India leverage lower labor costs and robust supply chains, raising bulk consumption for flexible grades that blend seamlessly with plant oils. FDA and EU approvals simplify cross-border shipping, allowing brands to consolidate output in a few mega-facilities without compromising compliance. Rising middle-class spending in Indonesia, Vietnam and the Philippines sustains double-digit growth in lip-color launches, further anchoring regional demand. Brands pursuing “clean beauty” narratives trial plant wax blends yet still rely on microcrystalline fractions to maintain payoff quality and product stability. Consequently, the microcrystalline wax market continues to secure volumes even as sustainability pressures intensify.

Growing Demand from Pharmaceutical and Medical Applications

Drug formulators adopt microcrystalline wax to build sustained-release matrices that ensure dose uniformity across 8-12 hour windows. Its chemical inertness allows direct compression with active ingredients, avoiding additional barrier coatings and shortening development timelines. Chronic disease prevalence in aging markets such as the United States, Germany and Japan elevates demand for long-acting pain management and endocrinology therapies, both of which leverage wax-based pellet technology. Global regulatory harmonization under ICH Q12 boosts cross-regional filings, lowering marginal costs for wax-enabled formulations. Contract development manufacturing organizations (CDMOs) therefore lock in long-term supply contracts to secure consistent grade specifications, reinforcing steady offtake for high-purity hard wax fractions.

Substitution of Paraffin with Microcrystalline Wax in Hot-Melt Adhesives

Packaging converters require adhesives that survive wider temperature swings in e-commerce logistics, and microcrystalline wax raises bond strength while curbing brittleness that plagues paraffin systems. Automotive wire-harness makers also prefer higher softening points of 65-105 °C to prevent joint failure during engine-bay heat cycles. Sustainability teams spur adoption of SASOLWAX LC100, which delivers identical viscosity indices with 35% lower cradle-to-gate emissions versus conventional grades. Early adopters in North America report 8-12% reduction in adhesive consumption due to improved spreading, offsetting slightly higher raw-material costs. Competitive gains and Scope 3 pressure together accelerate replacement of legacy paraffin blends, widening the addressable base for the microcrystalline wax market.

Shift Toward Bio-Based Feedstock Upgrading at Refineries

European and US refiners retrofit Fischer–Tropsch units to process biomass-derived syngas, producing low-carbon synthetic microcrystalline wax that matches ASTM melting-point bands. Fe-based χ-Fe5C2 catalysts demonstrated 15% higher CO conversion and lower CH4 selectivity, enhancing yield while trimming CO2 output. Although biomass logistics raise operating costs by 12-15%, policy incentives and brand premiums offset early economics. Downstream buyers value traceable Scope 3 savings, creating a nascent price-in-carbon advantage over petroleum counterparts. Continuous product-quality monitoring via DSC and GC–MS addresses variability concerns and accelerates broader commercialization through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-Oil Supply Volatility Impacting Feedstock Availability | -0.9% | Global, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Regulatory Pushback on Mineral-Based Ingredients in Premium Cosmetics | -0.6% | EU and North America regulatory-driven, spreading globally | Medium term (2-4 years) |

| Tight Marine Discharge Regulations on Wax Residues | -0.3% | Global maritime routes, IMO compliance required | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Supply Volatility Impacting Feedstock Availability

Geopolitical tensions and OPEC production curbs periodically tighten vacuum-resid availability, leading refiners to prioritize higher-margin fuels rather than specialty wax streams. Spot price spikes raise microcrystalline feed costs by up to 22%, compressing margins for independent compounders lacking long-term offtake contracts. Import-dependent economies in Western Europe and East Africa face the sharpest disruptions, since freight premiums amplify volatility. Integrated majors with captive crude trade desks cushion the impact through hedging, but smaller players risk stock-outs that erode customer trust. Over the medium term, diversification into synthetic and biomass-derived waxes offers partial mitigation, yet scaling remains capital intensive and time consuming.

Regulatory Pushback on Mineral-Based Ingredients in Premium Cosmetics

The European Union’s evolving stance on mineral-oil aromatic hydrocarbons (MOAH) compels prestige brands to declare mineral-oil-free positioning or adopt rigorous purification controls. Similar sentiment spreads through North American clean-beauty retailers, raising formulation hurdles for microcrystalline wax in high-end lines, even though refined grades comply with safety thresholds. Marketing narratives often outpace scientific consensus, forcing suppliers to produce low-odour, food-grade variants that add processing cost. While mass-market labels continue to rely on the ingredient, value growth in the luxury segment could shift toward plant-based alternatives, trimming upside for the microcrystalline wax market over the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hard Variants Capture Innovation Premium

Hard-type grades opened 2025 with stronger momentum, forecast to climb at a 4.01% CAGR to 2031 while flexible grades maintained 61.45% revenue dominance in 2025. Type 1 laminating wax at 65 °C safeguards photographic paper, Type 2 coating wax at 81 °C fortifies food-contact boards, and Type 3 hardening wax at 90 °C protects transformer windings. These fine-crystal structures impart superior dielectric strength and resist slump under sustained heat, attributes increasingly valued by electric-vehicle capacitor makers.

Laboratory protocols relying on differential scanning calorimetry, needle penetration and ring-and-ball softening point testing ensure batch homogeneity, meeting ISO 22007 precision benchmarks. Ongoing R&D explores nano-silica doping that lifts modulus by 18% without sacrificing viscosity, opening new niches in EMI shielding coatings. Flexible grades, meanwhile, dominate lipstick, balm and board-laminating volumes where pliability and oil-binding are critical. Rapid expansion of APAC contract filling plants underpins consistent throughput for flexible fractions, anchoring baseline demand even as hard-grade innovations lift value capture.

By Application: Adhesives Exhibit Fastest Upside

The microcrystalline wax market size for adhesives is forecast to expand at a 3.96% CAGR between 2026-2031 amid the migration from paraffin to higher-performance blends in corrugated packaging, woodworking and electronics assembly. When included at 10-20 wt % in hot-melt formulations, microcrystalline wax improves tack retention, widens service temperature and lowers cold-crack risk. Manufacturers thus advertise longer‐lasting bonds that survive warehouse extremes from -20 °C to 50 °C without deforming cartons.

Cosmetics and personal care remained the largest consumption pocket, representing 37.74% of microcrystalline wax market share in 2025 on the strength of lipstick, mascara and balm launches. Candle makers prefer the wax’s fragrance-locking ability and clean burn profile, while pharmaceutical formulators prize its GRAS status for sustained-release pellets. Rubber compounders deploy the ingredient as a surface-bloom antiozonant, and board laminators exploit its water-barrier function in chilled-food cartons. Food-contact coatings gain momentum as suppliers replace PFAS barriers with wax-based emulsions that pass EU Regulation (EU) 2023/2006 migration limits. Collectively, diversified end-use demand cushions cyclicality and moderates pricing swings across the microcrystalline wax market.

Geography Analysis

Asia-Pacific commanded 46.85% revenue in 2025 and is projected to expand at a 3.82% CAGR through 2031 on the twin engines of refinery investment and consumer-product manufacturing. India plans to add 800,000 barrels per day of refining capacity by 2030, broadening feedstock access for local wax producers. China’s vertically integrated petrochemical complexes, coupled with lifestyle-driven cosmetics uptake, secure cost leadership. Japan and South Korea concentrate on high-purity hard grades for electronics, leveraging tight process controls and advanced QC infrastructure. ASEAN nations attract contract manufacturing owing to tariff advantages and proximity to raw-material supply, reinforcing regional self-sufficiency.

North America retains technological leadership via specialty formulators and R&D-oriented refiners. FDA clearances for food-contact use and USP listings for pharmaceutical grades provide predictable regulatory paths, supporting steady downstream consumption. The United States develops next-gen bio-based wax blends within national labs, while Mexico’s expanding auto-assembly and packaging clusters stimulate adhesive and coating demand. Canadian authorities confirmed negligible human-health risk from refined microcrystalline fractions, bolstering public acceptance.

Europe balances stringent sustainability rules with specialty innovation. Brands face MOAH and MOSH purity mandates, prompting suppliers to install inline GC-FID monitoring and adopt double-hydrogenation routes. Germany champions circular-carbon projects that gasify waste biomass into Fischer–Tropsch wax intermediates, whereas the Netherlands pilots marine-biogenic feedstock. Eastern European refiners retrofit hydrocrackers to capture value from regional crude flows, raising local availability. Elsewhere, Brazil’s booming personal-care exports and Saudi Arabia’s specialty-chem investment frameworks hint at incremental pockets of growth in South America and Middle-East and Africa, respectively.

Competitive Landscape

The microcrystalline wax market is moderately concentrated: the top five producers—ExxonMobil, Sasol, Koster Keunen, Sinopec and Paramelt—collectively hold just above 60% global revenue, leveraging captive crude access, proprietary refining circuits and global distribution. Integrated majors combine vacuum-residue upgrading, hydrofinishing and Fischer–Tropsch routes, ensuring grade consistency across flexible and hard fractions. Specialty players differentiate through custom blends, small-lot packaging and technical service that aligns with customer R&D cycles.

Innovation centers on lowering carbon intensity and widening performance envelopes. Sasol’s LC100 series cuts cradle-to-gate CO2 by 35% while maintaining melt-point targets, offering a premium solution for brands chasing net-zero pledges. Shell’s 2024 commercial rollout of GTL-derived microcrystalline grades in Malaysia demonstrates scale-up viability for gas-based pathways, delivering sulfur-free profiles attractive to pharmaceutical users. ExxonMobil expanded Singapore output by 20,000 barrels per day, reinforcing APAC supply resilience and enabling downstream formulators to shorten lead times.

Competitive intensity remains moderate because refinery installation costs exceed USD 500 million and API certification regimes raise technical barriers. Nonetheless, niche entrants exploiting plant-wax chemistries—candelilla, carnauba and hydrogenated castor wax—compete in premium natural cosmetics. Material science collaborations with academia seek nano-filler reinforcement and phase-change functionality, which could unlock new revenue streams yet require heavy validation. Over the next five years, sustained investment in decarbonization, process intensification and specialty applications will shape strategic differentiation across the microcrystalline wax market.

Microcrystalline Wax Industry Leaders

Sasol Ltd

Exxon Mobil Corp

Sinopec Corp.

Paramelt BV

Koster Keunen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Shell introduced the world's first commercial GTL-derived synthetic microcrystalline wax series at its Bintulu plant. The series includes three products: MMP, MMP Plus, and HMP, expanding the supply options for microcrystalline wax users.

- May 2024: King Honor International upgraded its microcrystalline wax products to provide enhanced flexibility and bonding strength, particularly for hot-melt adhesive applications, which supports the demand for microcrystalline wax.

Global Microcrystalline Wax Market Report Scope

Microcrystalline wax is a type of petroleum wax produced by the petroleum refining industry's downstream sector. It is composed of crystalline, saturated hydrocarbons. Microcrystalline wax is primarily derived from the dewaxing process of petroleum refineries and is primarily used in the cosmetics and personal care industries.

The microcrystalline wax market is segmented by type, application, and geography. By type, the market is segmented into flexible and hard. By application, the market is segmented into cosmetics and personal care, candles, adhesives, packaging, rubber, and other applications. The report also covers the size and forecasts of the microcrystalline wax market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

| Flexible |

| Hard |

| Cosmetics and Personal Care |

| Candles |

| Adhesives |

| Packaging |

| Rubber |

| Other Applications |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Flexible | |

| Hard | ||

| By Application | Cosmetics and Personal Care | |

| Candles | ||

| Adhesives | ||

| Packaging | ||

| Rubber | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the microcrystalline wax market?

The microcrystalline wax market size is valued at USD 2.88 billion in 2026 and is projected to reach USD 3.41 billion by 2031.

Which region leads the microcrystalline wax market?

Asia-Pacific holds 46.85% of global revenue and is also the fastest-growing region with a 3.82% CAGR through 2031.

Why are adhesives the fastest-growing application?

Adhesive formulators are replacing paraffin with microcrystalline wax to gain higher bond strength and broader service-temperature windows, driving a 3.96% CAGR for the segment.

How are sustainability trends affecting product development?

Refiners are introducing low-carbon and bio-based wax variants, such as SASOLWAX LC100 and Shell’s GTL grades, to meet Scope 3 reduction goals without sacrificing performance.

What challenges does the market face?

Feedstock price volatility and increasing regulatory scrutiny of mineral-based ingredients in premium cosmetics could restrain growth, although technological innovation is mitigating some risks.

Page last updated on: