Sugarcane Wax Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 40.73 Billion |

| Market Size (2031) | USD 51.79 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

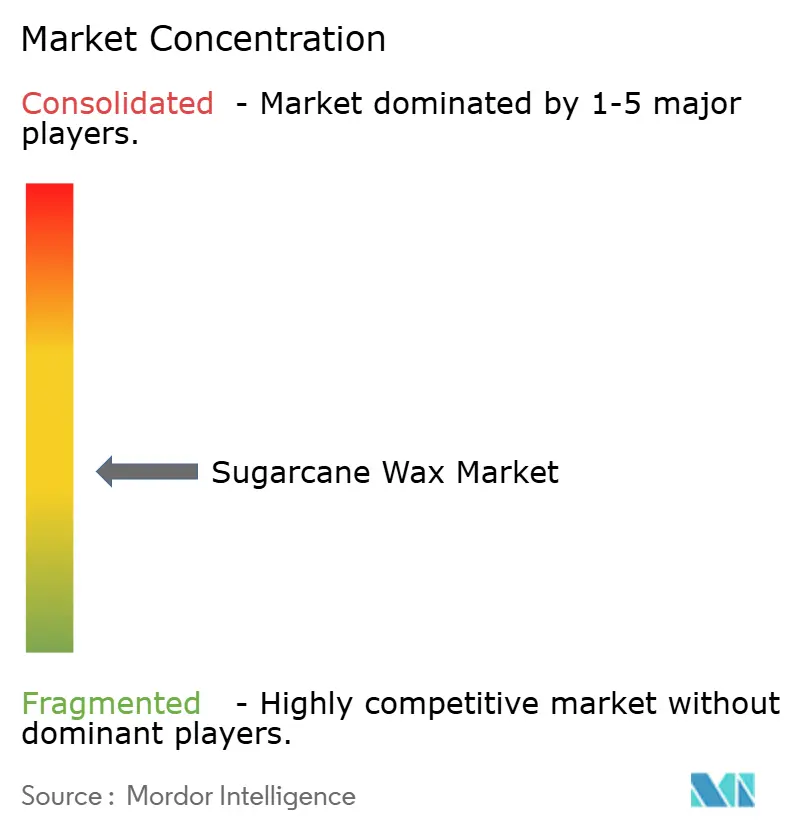

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sugarcane Wax Market Analysis by Mordor Intelligence

The Sugarcane Wax Market size is expected to grow from USD 38.82 billion in 2025 to USD 40.73 billion in 2026 and is forecast to reach USD 51.79 billion by 2031 at 4.92% CAGR over 2026-2031. Structural demand is increasing as PFAS-free packaging regulations in the European Union and several U.S. states align with consumer-goods companies’ public commitments to certified bio-based inputs. The availability of filter cake from Brazil’s record sugarcane harvest and India’s consistent production ensures raw-material security. Additionally, advancements in super-critical CO₂ extraction are improving yields and reducing energy costs, enabling refiners to enhance margins while meeting cosmetic-grade peroxide specifications. Vertical integration, as demonstrated by Paramelt’s February 2026 acquisition of KAHL GmbH, is streamlining the midstream segment and raising barriers for non-certified suppliers.

Key Report Takeaways

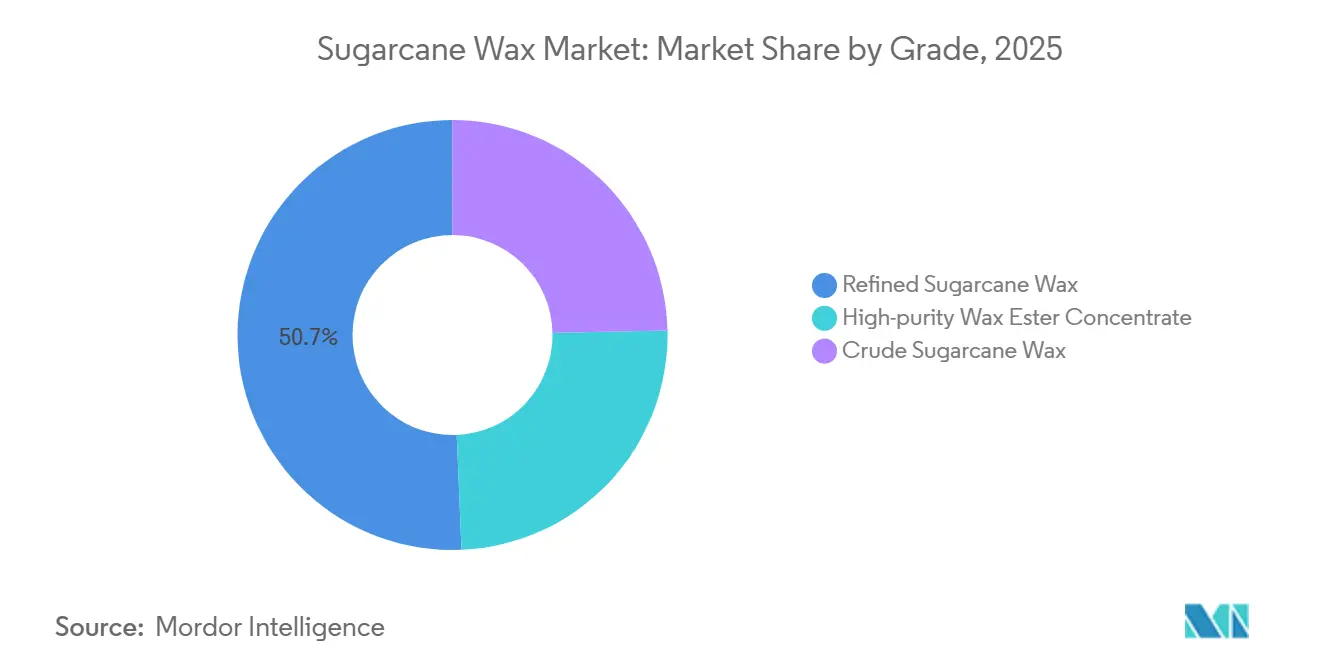

- By grade, refined sugarcane wax led with 50.67% of the sugarcane wax market share in 2025; high-purity wax ester concentrate is projected to expand at a 5.11% CAGR through 2031.

- By functionality, emollient and thickener held 47.88% of the sugarcane wax market share in 2025, while film-former and water-barrier is set to accelerate at a 4.56% CAGR through 2031.

- By application, cosmetics and personal care accounted for 33.87% of the sugarcane wax market share in 2025, and pharmaceuticals are forecast to grow at a 5.03% CAGR through 2031.

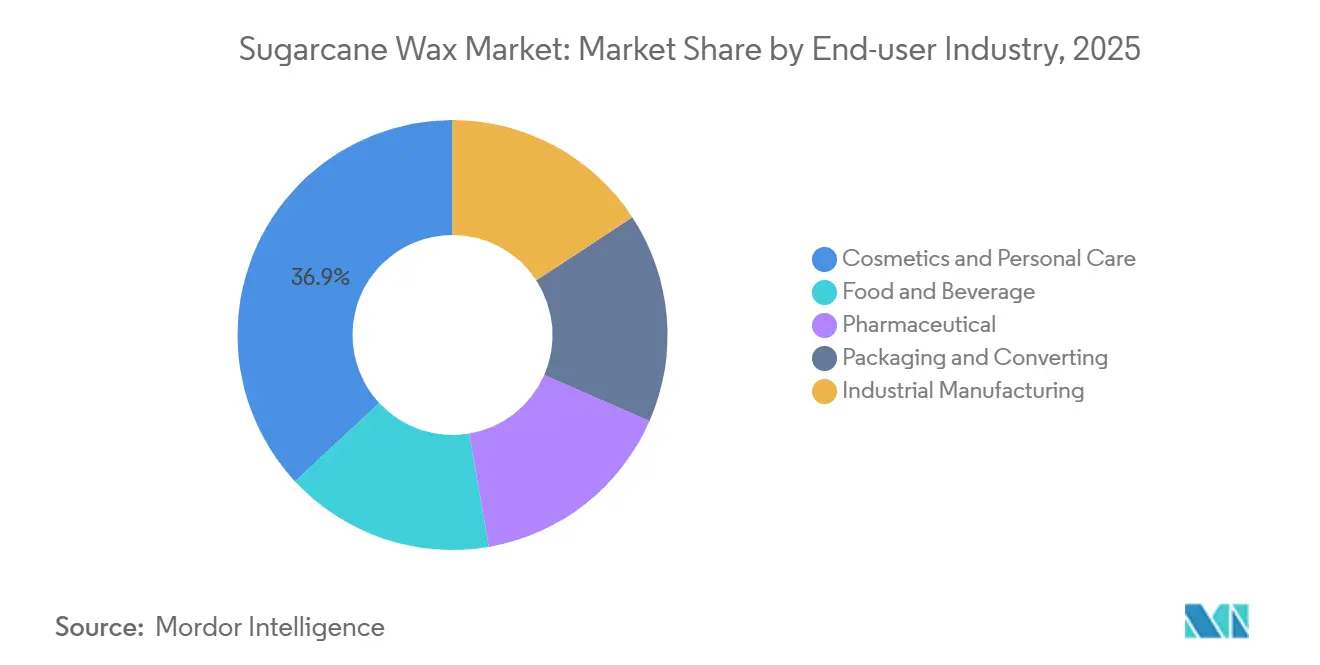

- By end-user industry, cosmetics and personal care accounted for 36.92% of the sugarcane wax market share in 2025, and the pharmaceutical industry is forecast to grow at a 4.12% CAGR through 2031.

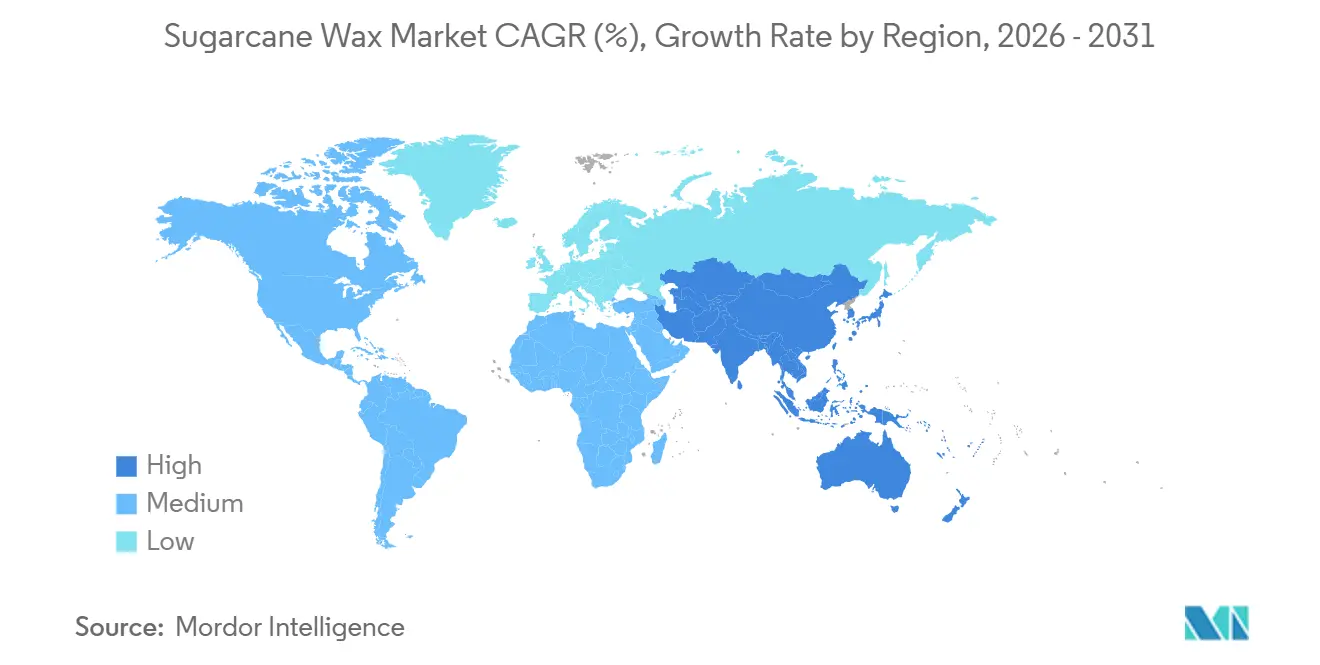

- By geography, Asia-Pacific commanded 47.73% share of the sugarcane wax market share in 2025 and is expected to register a 5.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sugarcane Wax Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural and sustainable waxes in cosmetics and food | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of sugarcane production and by-product valorization (APAC, South America) | +1.0% | APAC (India, Thailand, ASEAN), South America (Brazil, Argentina) | Long term (≥ 4 years) |

| Bio-based packaging regulations in EU and North America | +1.5% | Europe and North America, spillover to export-oriented APAC mills | Short term (≤ 2 years) |

| Super-critical CO₂ extraction breakthroughs lifting yield and lowering cost | +0.8% | Global, early adoption in Europe and advanced APAC facilities | Medium term (2-4 years) |

| Certification-driven sourcing by global CPG brands (RSB, Bonsucro) | +0.4% | Global, strongest in EU and North America procurement, APAC supply | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Natural and Sustainable Waxes in Cosmetics and Food

Global clean-beauty spending reached USD 281.0 billion in 2025, with Europe and the United States contributing nearly USD 34 billion in growth over four years. Sugarcane wax, with its 80-85% fatty-acid-ester composition, serves as a replacement for synthetic thickeners, allowing brands to simplify INCI lists and secure vegan claims. In food coatings, retailer bans on PFAS are driving fresh-produce packers toward natural waxes. Crude sugarcane wax can be fractionated into cosmetic- and food-grade products, enabling biorefineries to optimize output by value segment. Due to the seasonal and labor-intensive nature of carnauba wax production in Ceará, formulators are increasingly mitigating supply risks by incorporating sugarcane wax into their formulations.

Expansion of Sugarcane Production and By-Product Valorization

India processed 283.54 million tons of sugarcane in the 2025-26 season, producing approximately 11.4 million tons of press mud, though less than 10% is utilized for wax production. Brazilian mills exported 33.774 million tons of sugar in 2025, even while diverting cane for ethanol production, which has paradoxically stabilized filter-cake supply. Thailand’s integrated biorefineries, supported by Board of Investment incentives, now co-locate ethanol, power, and wax production lines. The International Sugar Organization forecasts the tightest global sugar stocks-to-consumption ratio in 15 years, prompting mills to monetize co-products like wax to maintain margins[1]International Sugar Organization, “World Sugar Balance 2025/26,” iso.org. Recent capital expenditure commitments by BP Bunge, Shree Renuka, and Dangote are expected to add up to 20,000 tons of annual wax capacity by 2027.

Bio-Based Packaging Regulations in EU and North America

The EU’s Packaging and Packaging Waste Regulation 2025/40 will ban PFAS linings in food-contact paper starting in August 2026, prompting converters to seek natural barrier alternatives. Similar restrictions under California’s AB 1200 and Canada’s draft Single-Use Plastics rules collectively impact over 400 million consumers. Sugarcane wax coatings, which already hold FDA GRAS status, reduce regulatory hurdles for U.S. food packers. While PFAS coatings are currently more cost-effective, potential remediation liabilities are narrowing the cost gap. Rigid paperboard can accommodate 100% wax layers, whereas flexible films require hybrid blends, segmenting the market opportunity by packaging format.

Super-critical CO₂ Extraction Breakthroughs Lifting Yield and Lowering Cost

Super-critical CO₂ extraction, operating above 73.8 bar and 31.1 °C, selectively extracts high-molecular-weight esters while leaving sugars behind, achieving peroxide values below 5 Meq/kg without secondary refining. Pilot studies indicate 15-25% higher recovery rates compared to hexane systems, with up to 30% lower energy consumption due to the closed-loop recycling of CO₂. Although the capital investment for a 500 kg/h unit ranges from USD 1.5-2.5 million, the premium pricing of cosmetic-grade wax has reduced payback periods to three to five years for early adopters. A February 2026 UK patent filing highlights ongoing R&D in agricultural-residue wax extraction, signaling competitive advancements. Early adopters in Germany and Japan are expected to bring 3,000-4,000 tons per year of high-purity capacity online by 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited large-scale commercial supply chain | -0.6% | Global, acute in North America and Europe where demand exceeds local supply | Short term (≤ 2 years) |

| Competition from incumbent natural and synthetic waxes | -0.4% | Global, most intense in cost-sensitive industrial applications | Medium term (2-4 years) |

| Filter-cake supply volatility amid ethanol-first production swings | -0.3% | APAC and South America, tied to sugar-ethanol price parity | Short term (≤ 2 years) |

| High CAPEX for cosmetic-grade refining | -0.2% | Global, limiting entry for small and mid-sized mills | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Large-Scale Commercial Supply Chain

Fewer than 20 facilities globally can consistently produce cosmetic-grade sugarcane wax with peroxide values below 5 Meq/kg. Demand is concentrated in Europe and North America, regions with minimal sugarcane processing[2]U.S. Department of Agriculture, “Domestic Sugar Production 2025,” usda.gov. Import lead times of eight to twelve weeks increase landed costs by 15-25% when refrigerated freight is included. Quality degradation during transit, due to the melting point of crude wax (81-87 °C), necessitates cold-chain logistics, which many origin ports lack. Unlike carnauba wax, sugarcane wax lacks ASTM color benchmarks, requiring batch-by-batch testing that increases transaction complexity. Investments in midstream hubs at ports such as Santos, Mumbai, and Bangkok could reduce lead times and improve quality assurance for converters.

Competition from Incumbent Natural and Synthetic Waxes

Carnauba wax dominates Brazil’s natural-wax exports due to its superior hardness, making it ideal for automotive polishes, while candelilla wax is preferred for low-dose confectionery glazes. Synthetic waxes like polyethylene and Fischer-Tropsch waxes, priced at USD 2-4 per kg, are approximately half the cost of cosmetic-grade sugarcane wax, maintaining their dominance in adhesives and rubbers. In the candle market, paraffin wax’s consistent burn profile further limits sugarcane wax adoption. Sugarcane wax is gaining traction primarily in applications where sustainability offers measurable financial benefits, such as PFAS-replacement coatings and vegan cosmetics. Hybrid blends incorporating 20-40% sugarcane wax with carnauba are emerging as a cost-effective solution for formulators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Premium Esters Command Rapid Growth

Refined sugarcane wax held a 50.67% share of the sugarcane wax market in 2025, owing to its adaptability in cosmetics, food coatings, and industrial polishes. High-purity wax ester concentrate is anticipated to grow at a 5.11% CAGR through 2031, as pharmaceutical excipient buyers prioritize peroxide values below 2 Meq/kg and policosanol levels above 20%, which support cardiovascular health claims.

Refined grades adhere to FDA food-contact standards and European pharmacopoeial requirements, providing an accessible compliance route, while crude wax remains limited to applications like textile sizing and rubber compounding. Economies of scale in secondary refining are reducing the cost disparity between refined and crude wax, driving demand for higher-specification products. Additionally, super-critical CO₂ systems are enabling ester concentrates to enter niche nutraceutical and derma-cosmetic markets, indicating a division in the sugarcane wax industry between commodity and premium value segments.

By Functionality: Barrier Coatings Catch Up to Emollients

Emollients and thickeners accounted for 47.88% of revenue in 2025, as sugarcane wax’s fatty-alcohol profile was used to replicate skin lipids. Film-forming and water-barrier functionalities are projected to grow at a 4.56% CAGR through 2031, driven by PFAS bans and advancements in natural coatings for paperboard, achieving WVTR levels comparable to low-density polyethylene for dry snacks.

Hybrid performance is emerging as a key trend, with blends offering gloss, hardness, and hydrophobicity at lower dosages, enhancing cost competitiveness against carnauba wax. Automotive and furniture polishes are incorporating 20-30% sugarcane wax to reduce formulation costs while maintaining 85 GU gloss at a 60° angle. Research into esterification with omega-3 fatty acids suggests the potential for next-generation multifunctional waxes with improved barrier properties and enhanced skin-feel.

By Application: Pharmaceuticals Emerge as Fastest-Growing Use Case

Cosmetics and personal care remained the largest application segment, holding a 33.87% share in 2025, driven by products such as stick foundations, lip balms, and hair pomades. Pharmaceutical applications are growing at a 5.03% CAGR through 2031, supported by clinical evidence that daily policosanol intake of 10-20 mg can reduce systolic blood pressure and increase HDL cholesterol levels.

In North America, dietary supplement brands have introduced sugarcane-derived policosanol softgels, while European regulators are evaluating functional-food dossiers that could expand market volumes. Food-coating applications are also increasing as vegan and allergen-free positioning gains traction among grocery retailers. However, candles and hot-melt adhesives remain dominated by lower-cost synthetic alternatives, limiting market penetration in price-sensitive niches.

By End-user Industry: Pharmaceutical Premiums Offset Cosmetics Revenue

The cosmetics and personal care industry accounted for 36.92% of the market share in 2025, encompassing finished-product manufacturers, contract manufacturers, private-label producers, and indie brands. These entities collectively purchase 12,000-15,000 tons annually of refined and high-purity sugarcane wax for stick products, emulsions, and color cosmetics. The pharmaceutical industry, growing at a 4.12% CAGR through 2031, includes nutraceutical supplement brands (e.g., NOW Foods, Nature's Plus, Solgar), pharmaceutical excipient suppliers (e.g., JRS Pharma, Roquette), and CDMOs that produce controlled-release tablets and capsule shells. High-purity wax ester concentrates command USD 15-25 per kilogram, compared to USD 6-10 per kilogram for cosmetic-grade refined wax, due to stringent quality requirements and smaller batch sizes.

The food and beverage industry, including fruit and vegetable packers, cheese producers, and confectionery manufacturers, utilizes food-grade refined wax for surface coatings that enhance shelf life and visual appeal. The packaging and converting industry, comprising paperboard mills, flexible packaging converters, and coating applicators, is experiencing growth as PFAS restrictions take effect. A single large paperboard mill can consume 500-1,000 tons annually of wax for barrier coatings on food-service packaging. Industrial manufacturing end-users, such as automotive, furniture, textiles, and rubber sectors, remain highly price-sensitive and less inclined to pay premiums for sustainability.

Geography Analysis

Asia-Pacific commanded 47.73% share of the sugarcane wax market in 2025 and is expected to register a 5.40% CAGR through 2031. India and Thailand produced over 12 million tons of filter cake in 2025, yet less than 5% was utilized for wax extraction, indicating significant untapped potential. China, a major buyer of Brazilian carnauba wax, is increasing import substitution by certifying domestic sugarcane wax feedstocks for cosmetics, reflecting heightened regulatory scrutiny over ingredient origins.

North America depends on imports due to limited local sugarcane production. However, strong clean-label demand and FDA GRAS clarity support premium pricing. To mitigate lead-time risks, buyers are exploring long-term offtake agreements with Brazilian and Thai mills. Europe’s PPWR timeline positions it as a regulatory leader, sourcing certified wax volumes from Bonsucro-audited mills in Mauritius and Nicaragua, often at a 10-15% price premium over non-certified alternatives.

South America remains a production hub, exporting up to 90% of refined output. However, freight volatility poses challenges to exporter margins. The Middle-East and Africa are emerging markets, with natural beauty imports into GCC countries showing double-digit growth from a small base. Overall, regional dynamics highlight the importance of feedstock security and certification in shaping sugarcane wax market trade flows.

Competitive Landscape

The sugarcane wax market is moderately fragmented. Paramelt’s acquisition of KAHL in February 2026 added 2,000-3,000 tons of European capacity and expanded its natural-wax product range. Godavari Biorefineries partnered with Synthomer to convert cane-derived butanol into bio-based acrylates, enhancing value extraction per ton of cane and stabilizing earnings against sugar-price fluctuations.

Smaller players like Natural Sourcing LLC differentiate themselves through Bonsucro and RSB certifications, capturing 10-15% price premiums from indie beauty brands emphasizing ingredient transparency. Process patents from Praj Industries for reflux purification demonstrate ongoing innovation aimed at reducing peroxide values without generating excessive adsorbent waste. As capacity grows, mid-tier distributors may become acquisition targets for larger conglomerates seeking to expand market share and certification capabilities, potentially leading to a more consolidated sugarcane wax industry.

Sugarcane Wax Industry Leaders

DEUREX AG

Origen Chemicals

Koster Keunen

GODAVARI BIOREFINERIES LTD.

Cerax

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BASF launched Lamesoft OP Plus, a wax-based opacifier with over 92% natural-origin content. This product utilized sugarcane-derived formulations, aligning with the growing demand in the sugarcane wax market.

- February 2025: The EU Packaging and Packaging Waste Regulation (PPWR), which came into force on February 11, 2025, and will be applied from August 12, 2026, promoted the use of sustainable materials. This regulation influenced the sugarcane wax market by driving demand for recyclable and biodegradable packaging alternatives.

Global Sugarcane Wax Market Report Scope

Sugarcane wax is a natural, plant-based wax derived from the surface of sugarcane stalks, primarily as a byproduct of sugar refining (filter cake). It is a hard wax with a high melting point, commonly used as a sustainable and vegan alternative to carnauba wax in cosmetics, lubricants, and industrial coatings.

The sugarcane wax market is segmented into grade, functionality, application, end-user industry, and geography. By grade, the market is segmented into refined sugarcane wax, crude sugarcane wax, and high-purity wax ester concentrate. By functionality, the market is segmented into emollient and thickener, film-former and water-barrier, and gloss and surface-hardness enhancer. By application, the market is segmented into cosmetics and personal care, food (coatings and glazing), pharmaceuticals, polishes and surface coatings, adhesives and sealants, candles and aromatics, and other applications. By end-user industry, the market is segmented into cosmetics and personal care, food and beverage, pharmaceutical, packaging and converting, and industrial manufacturing. The report also covers the market size and forecasts for sugarcane wax in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Refined Sugarcane Wax |

| Crude Sugarcane Wax |

| High-Purity Wax Ester Concentrate |

| Emollient and Thickener |

| Film-Former and Water-Barrier |

| Gloss and Surface-Hardness Enhancer |

| Cosmetics and Personal Care |

| Food (Coatings and Glazing) |

| Pharmaceuticals |

| Polishes and Surface Coatings |

| Adhesives and Sealants |

| Candles and Aromatics |

| Other Applications |

| Cosmetics and Personal Care |

| Food and Beverage |

| Pharmaceutical |

| Packaging and Converting |

| Industrial Manufacturing |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Refined Sugarcane Wax | |

| Crude Sugarcane Wax | ||

| High-Purity Wax Ester Concentrate | ||

| By Functionality | Emollient and Thickener | |

| Film-Former and Water-Barrier | ||

| Gloss and Surface-Hardness Enhancer | ||

| By Application | Cosmetics and Personal Care | |

| Food (Coatings and Glazing) | ||

| Pharmaceuticals | ||

| Polishes and Surface Coatings | ||

| Adhesives and Sealants | ||

| Candles and Aromatics | ||

| Other Applications | ||

| By End-user Industry | Cosmetics and Personal Care | |

| Food and Beverage | ||

| Pharmaceutical | ||

| Packaging and Converting | ||

| Industrial Manufacturing | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the sugarcane wax market?

The sugarcane wax market stands at USD 40.73 billion in 2026 and is projected to reach USD 51.79 billion by 2031.

Which region contributes the most demand?

Asia-Pacific supplies 47.73% of global revenue in 2025 and is also the fastest-growing region at a 5.40% CAGR through 2031.

What drives the surge in pharmaceutical use?

Clinical data showing policosanol’s positive impact on HDL and blood pressure is prompting nutraceutical companies to adopt high-purity sugarcane wax ester concentrates.

How are EU regulations influencing adoption in packaging?

The EU’s PFAS restrictions, effective August 2026, are forcing converters to switch to natural barriers, lifting demand for sugarcane-wax-based coatings.

Page last updated on: