Monolithic Ceramics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

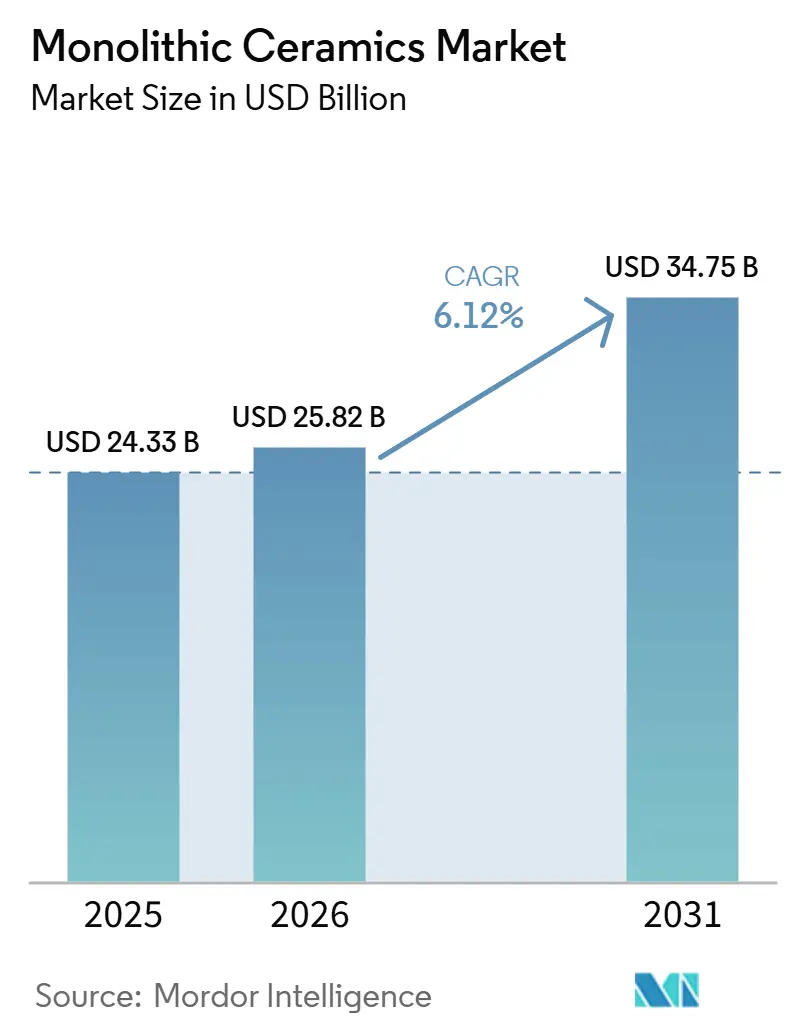

| Market Size (2026) | USD 25.82 Billion |

| Market Size (2031) | USD 34.75 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Monolithic Ceramics Market Analysis by Mordor Intelligence

The Monolithic Ceramics Market size is expected to increase from USD 24.33 billion in 2025 to USD 25.82 billion in 2026 and reach USD 34.75 billion by 2031, growing at a CAGR of 6.12% over 2026-2031. Shifts toward electrified drivetrains, miniaturized electronics, and extreme-environment hardware continue to reshape demand, driving growth in precision substrates and transparent armor over traditional refractory applications. Supply chains are increasingly adopting powder-to-package vertical integration, providing established players opportunities for margin recovery despite rare-earth constraints causing input volatility. Simultaneously, additive manufacturing is enabling the creation of complex lattices for heat exchangers and porous implants, expanding the design possibilities. Regional investments remain uneven: Asia-Pacific dominates wafer-carrier and power-module orders, while Europe focuses on solid-oxide electrolyzer stacks aligned with its green-hydrogen mandates. Together, these factors support a resilient Monolithic ceramics market narrative despite short-term cost challenges.

Key Report Takeaways

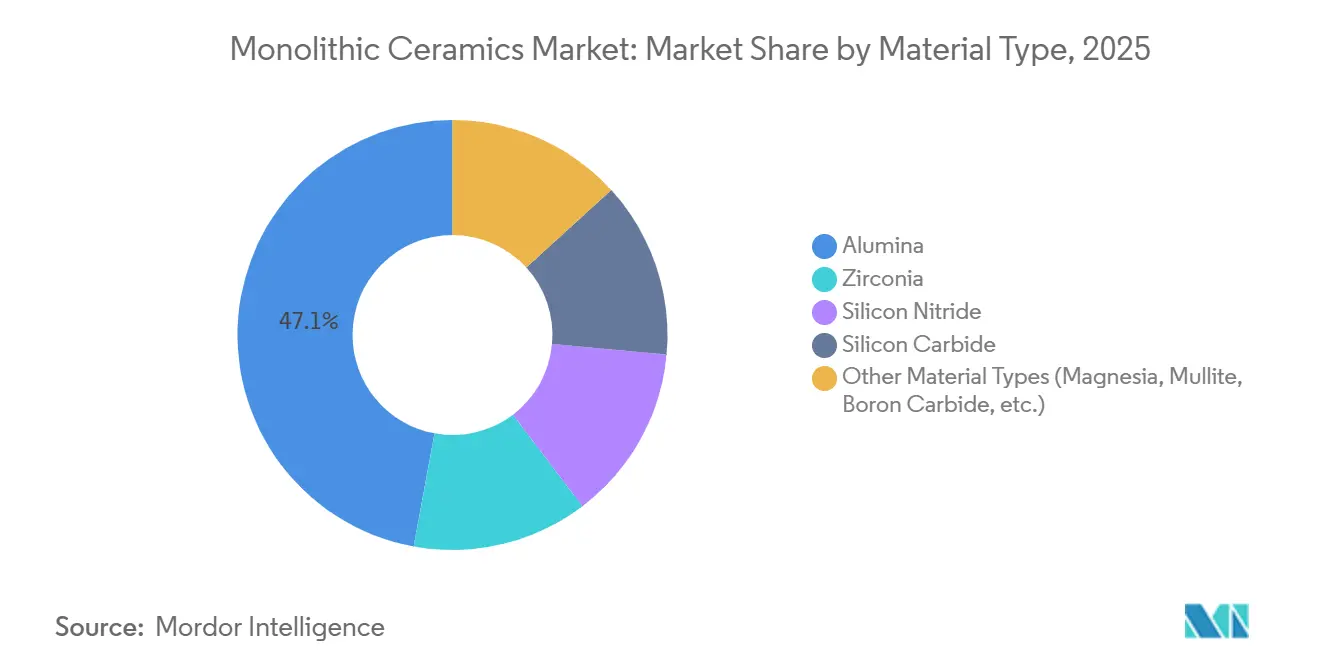

- By material type, alumina led with 47.12% of the monolithic ceramics market share in 2025; silicon carbide is forest to record the fastest 6.58% CAGR through 2031.

- By structure, opaque captured 57.22% of the monolithic ceramics market share in 2025, whereas transparent is on track for a 6.44% CAGR through 2031.

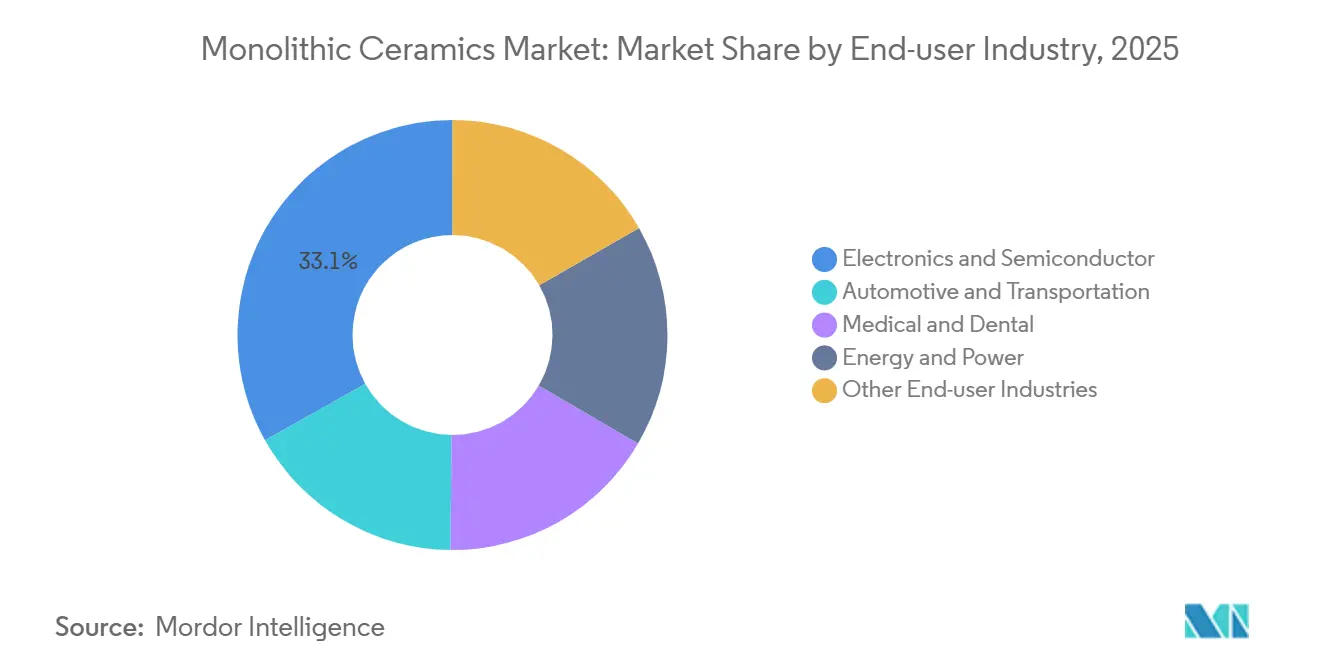

- By end-user industry, electronics and semiconductors generated 33.14% of the monolithic ceramics market share in 2025, while energy and power is advancing at a 6.99% CAGR through 2031.

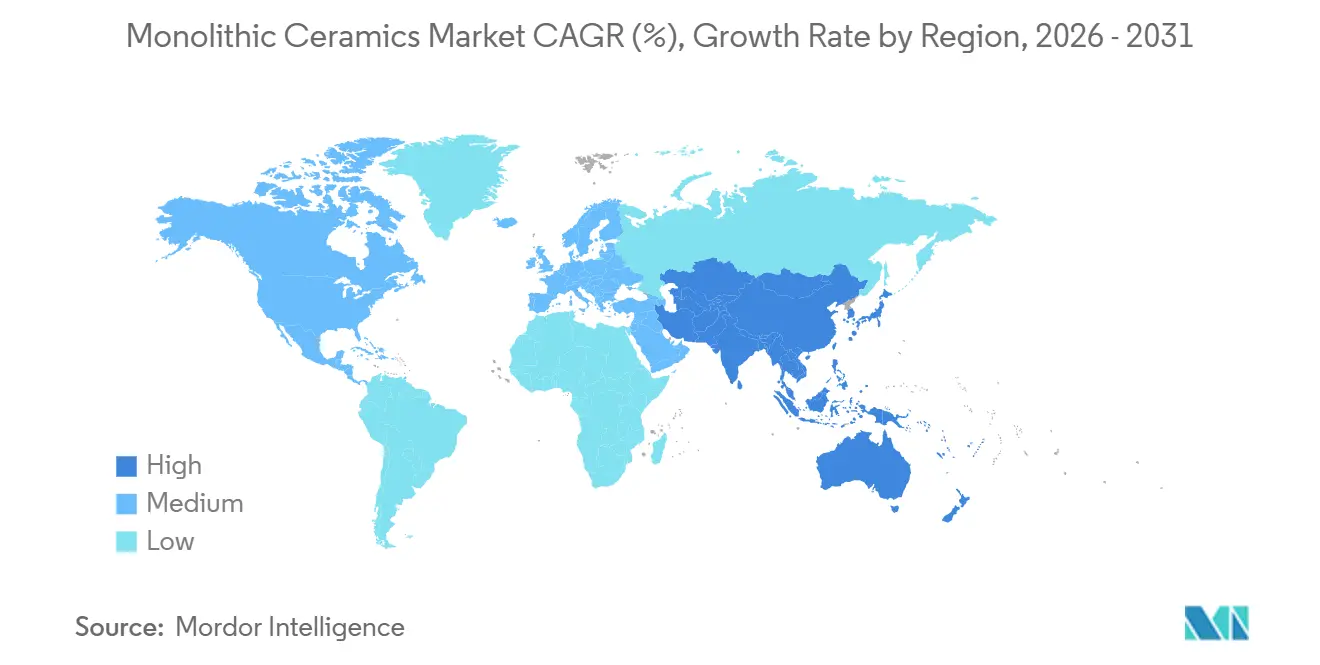

- By geography, Asia-Pacific commanded 44.22% of the monolithic ceramics market share in 2025 and is projected to maintain the quickest 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Monolithic Ceramics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV power-train thermal management | +1.4% | Global, with concentration in China, Germany, United States | Medium term (2-4 years) |

| Demand for semiconductor etch and CMP fixtures | +1.6% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Medical and dental implant adoption boom | +0.9% | North America, Europe, Japan | Long term (≥ 4 years) |

| Green-hydrogen solid-oxide electrolyzer stacks | +1.2% | Europe, North America, Australia | Medium term (2-4 years) |

| Space economy (re-usable launchers, hypersonics) | +0.7% | United States, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Power-Train Thermal Management

Wide-bandgap silicon-carbide inverters now achieve over 99% efficiency, reducing heat loads by half compared to silicon IGBTs and increasing vehicle range by approximately 7% per charge. Mass production by ROHM–Schaeffler, STMicroelectronics, and Infineon on 200 mm wafers is lowering die costs and driving higher ceramic substrate volumes. Alumina and aluminum-nitride direct-bonded copper substrates are essential for dissipating these heat losses, while ISO 26262 compliance remains critical to mitigate delamination risks for inverter developers. The Monolithic ceramics market is well-aligned with the growth of 800-V e-mobility platforms. Back-end suppliers are already reporting nine-month lead times for AIN sheets, highlighting sustained pricing power.

Demand for Semiconductor Etch and CMP Fixtures

TSMC’s USD 56 billion capital expenditure plan for 2026 and Intel’s 18A ramp are expected to add thousands of alumina wafer carriers, yttria-coated chamber liners, and silicon-carbide susceptors per fab. CHIPS Act grants are projected to increase the U.S. share of advanced logic production to nearly 15% by the end of 2025, boosting local demand for semiconductor fixtures. NGK Insulators is tripling its HICERAM capacity to achieve JPY 20 billion in sales by 2030, emphasizing the integration of component manufacturing with semiconductor fabs. However, labor shortages are delaying tool installations, extending order backlogs for specialty carriers. The monolithic ceramics market remains closely tied to semiconductor capital expenditure cycles, ensuring volume visibility through 2028.

Medical and Dental Implant Adoption Boom

Two-year clinical trials have demonstrated a 100% survival rate for monolithic zirconia crowns, outperforming metal-ceramic restorations, which are more prone to chipping. A 10-year study further validated this performance, attributing it to the elimination of veneer-core interfaces. CoorsTek’s Cerasurf alumina composite hips address wear concerns for younger patients, while regulatory differences between FDA 510(k) and EU MDR are tightening post-market evidence requirements. However, challenges in design-for-manufacturability persist, as two-piece screw-retained zirconia implants have shown only a 60.9% survival rate at 12 months, prompting a shift toward one-piece solutions. Despite these challenges, increasing implant adoption among aging OECD populations is driving growth in the monolithic ceramics market within the healthcare sector.

Green-Hydrogen Solid-Oxide Electrolyzer Stacks

Topsoe has opened a 500 MW cell factory in Denmark with support from the EU Innovation Fund, securing orders from First Ammonia and Forestal Oriental. Solid-oxide electrolyzer units offer 20-30% greater electrical efficiency by recycling process heat, making them a preferred choice for industrial decarbonization. Yttria-stabilized zirconia membranes remain the leading electrolyte material; however, China’s April 2025 export curbs caused a 95% drop in U.S. yttrium imports, leading to significant price spikes[1]U.S. Geological Survey, “Rare Earths 2026 Summary,” usgs.gov. While Western miners are expected to address ore shortages, bottlenecks in solvent extraction and high-purity calcination are likely to delay relief until the late 2020s. As a result, the Monolithic ceramics market is experiencing elevated price pass-throughs, though long-term demand for solid-oxide stacks remains robust.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intrinsic brittleness and design limits | -0.8% | Global | Long term (≥ 4 years) |

| Dopant-grade alumina and yttria supply squeeze | -1.1% | North America, Europe, Japan | Short term (≤ 2 years) |

| Carbon-neutral furnace regulations | -0.6% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intrinsic Brittleness and Design Limits

The fracture toughness of ceramics, ranging from 3-6 MPa√m, is significantly lower than that of metals, limiting their use in tensile or impact applications. For example, silicon-nitride EV motor bearings require surface roughness of ≤14 nm, increasing machining costs by four times compared to steel. Over-dimensioning to handle stress adds weight, while additive manufacturing introduces anisotropic flaws despite offering geometric flexibility. Standards such as ASTM C1161 and C1239 provide guidelines for flexural and Weibull testing, but no unified certification pathway exists for safety-critical additive-manufactured parts. These challenges constrain the broader adoption of ceramics, narrowing the addressable market until design standards evolve.

Carbon-Neutral Furnace Regulations

EU ETS Phase IV is reducing free allowances, and from 2026, the Carbon Border Adjustment Mechanism (CBAM) will impose duties on imports from regions with less stringent carbon policies[2]European Commission, “Carbon Border Adjustment Mechanism,” europa.eu. Sintering ceramics at 1,400-1,600 °C emits approximately 0.8-1.2 tons of CO₂ per ton of ceramic, adding GBP 80-120 per ton under the U.K.’s GBP 100 per ton CO₂ price. Fully electric kilns face challenges with thermal uniformity, while retrofitting hybrid lines costs EUR 5-10 million each. Although Germany and Spain are piloting hydrogen burners, large-scale hydrogen pipeline infrastructure is not expected until the late 2020s, creating medium-term challenges for the monolithic ceramics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Silicon Carbide Gains on Electrification Wave

Alumina held 47.12% of revenue dominance in 2025, but silicon carbide is anticipated to achieve a 6.58% CAGR through 2031, marking the fastest growth among materials. This is attributed to the shift towards wide-bandgap devices in EV inverters and renewable energy converters. Alumina's affordability ensures its continued use in CMP rings and implant abutments, while zirconia's transformation toughening enhances its application in solid-oxide electrolyzer electrolytes. Infineon's transition to 200 mm silicon carbide wafers has reduced epitaxy costs by 30%, supporting efforts to achieve price parity.

The monolithic ceramics market size for silicon carbide substrates is expected to grow significantly once ST-Sanan's 480,000-wafer production line reaches full capacity in 2028. Alumina, however, continues to dominate the monolithic ceramics market for fixtures. Silicon nitride and niche oxides, though smaller in scale, are strategically important for applications such as bearings and armor. Kyocera's BIOCERAM AZUL hybrid blend, with a flexural strength of 1,400 MPa, highlights incremental material innovations beyond the primary materials.

By Structure: Transparent Ceramics Accelerate in Defense Optics

Opaque ceramics accounted for 57.22% of revenue in 2025, but transparent ceramics are projected to grow at a 6.44% CAGR through 2031. This growth is driven by applications such as AlON windows and sapphire domes. AlON transmits 80% of light across the 350-4,900 nm range and resists 12.7 mm armor-piercing rounds while being 30% lighter than glass laminates, making it suitable for armored vehicle retrofits.

Transparent ceramics require impurity levels of ≤50 ppm and hot-isostatic pressing at 1,800 °C, limiting production to a few licensed manufacturers. While the market size for transparent ceramics remains modest, it is expected to scale rapidly as weight reduction becomes a priority in military applications. Opaque alumina and zirconia continue to dominate high-volume applications such as wafer carriers and implants, while porous scaffolds are gaining traction in regenerative medicine, albeit from a small base.

By End-user Industry: Energy and Power Segment Leads Growth

Electronics and semiconductors contributed 33.14% of revenue in 2025, but the energy and power segment is expected to grow at the fastest rate, with a 6.99% CAGR through 2031. This growth is driven by the scaling up of solid-oxide electrolyzers and solid-state batteries. QuantumScape's 24-layer LLZO cells, which achieved 800 cycles with 95% capacity retention, underscore the relevance of oxide separators.

The monolithic ceramics market size for energy applications is expanding from a smaller base, while electronics maintain their leading market share through continuous fab expansions. Applications such as automotive turbochargers and medical implants contribute to market diversity, ensuring a balanced risk profile for the sector.

Geography Analysis

Asia-Pacific captured 44.22% of revenue in 2025 and is projected to grow at a 6.88% CAGR through 2031, driven by China's advanced ceramics production. Industrial clusters in Zibo and Foshan have a combined turnover exceeding CNY 100 billion, while Japanese manufacturers are investing JPY 55 billion in capacity and R&D between 2024 and 2026. ASEAN assembly hubs are also emerging as labor costs rise along China's coastal regions.

North America benefits from CHIPS Act incentives. Defense-driven demand for space ceramics is also contributing to growth. NGK's USD 58 million Arizona plant, set to become operational in 2027, will localize wafer-carrier supply. Canada and Mexico remain niche players, focusing on oil-field sensors and traditional tiles, respectively.

Europe interlinks ceramics with hydrogen goals. Topsoe's Danish electrolyzer plant, supported by EUR 94 million in funding, positions Scandinavia as a leader in green hydrogen. Germany's machinery sector and the U.K.'s Morgan Advanced Materials are key suppliers of aerospace composites. However, rising CBAM costs are prompting kiln electrification across southern Europe. Sanctions on Russia's advanced powder exports are redirecting demand within the CIS to domestic mills.

Competitive Landscape

The monolithic ceramics market is moderately concentrated, with the top five companies accounting for approximately 41% of revenue in 2025. Kyocera, NGK Insulators, and Murata leverage powder-to-package integration, ensuring traceability and rapid design iterations for semiconductor and automotive applications. Opportunities remain in areas such as bio-resorbable scaffolds and ultrahigh-temperature hypersonic edges, where scale offers limited advantages.

Capacity expansions are concentrated near logic-fab build-outs. Murata's JPY 35 billion R&D hub in Fukui focuses on capacitor and inductor innovation for 5G and ADAS modules. NGK's expanded HICERAM line supports TSMC, Samsung, and Intel with flatness specifications within 50 µm for 300-mm carriers, a standard few competitors can meet. Intellectual property filings in functionally graded SiC-AIN substrates suggest emerging competition in next-generation heat spreaders.

Chinese companies such as Sinocera and CCTC are leveraging subsidies under the Made-in-China 2025 initiative to compete in mid-tier substrates. However, high-purity alumina and medical-grade zirconia remain dominated by Japanese and European firms. Additive manufacturing is creating a competitive edge, as demonstrated by Kyocera's 3D-printed silicon carbide heat exchangers, which improve convective transfer by 40% and reduce tooling lead times from months to weeks, a challenge for traditional pressed-part producers to replicate.

Monolithic Ceramics Industry Leaders

CoorsTek Inc.

Kyocera Corporation

Morgan Advanced Materials

Saint-Gobain

CeramTec GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hufschmied Zerspanungssysteme introduced a new class of tools, the PCD torus milling cutters, designed for machining monolithic ceramics and carbide. The initial model, designated as P150M, featured 25 cutting edges and a diameter of 3 mm.

- November 2024: Vesuvius inaugurated two new manufacturing plants in Visakhapatnam, India, specializing in Alumina-Silica (AlSi) and Basic Monolithic refractories. These facilities supported the Make in India initiative, enhancing production capacity to meet the demands of the growing Indian iron and steel industries with high-performance refractory products.

Global Monolithic Ceramics Market Report Scope

Monolithic ceramics are single-structure, inorganic, non-metallic materials, primarily composed of oxide or non-oxide compounds. They are recognized for their high strength, hardness, and thermal resistance. Typically produced through the sintering of powdered materials, these ceramics are generally brittle. However, advancements in engineering have led to the development of fibrous monoliths, enhancing their fracture toughness for use in aerospace, industrial, and dental applications.

The Monolithic Ceramics Market is segmented into material type, structure, end-user industry, and geography. By material type, the market is segmented into alumina, zirconia, silicon nitride, silicon carbide, and other material types (magnesia, mullite, boron carbide, etc.). By structure, the market is segmented into transparent, opaque, and porous. By end-user industry, the market is segmented into electronics and semiconductor, automotive and transportation, medical and dental, energy and power, and other end-user industries (industrial equipment, chemical, metallurgy, etc.). The report also covers the market size and forecasts for monolithic ceramics in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Alumina |

| Zirconia |

| Silicon Nitride |

| Silicon Carbide |

| Other Material Types (Magnesia, Mullite, Boron Carbide, etc.) |

| Transparent |

| Opaque |

| Porous |

| Electronics and Semiconductor |

| Automotive and Transportation |

| Medical and Dental |

| Energy and Power |

| Other End-user Industries (Industrial Equipment, Chemical, Metallurgy, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Alumina | |

| Zirconia | ||

| Silicon Nitride | ||

| Silicon Carbide | ||

| Other Material Types (Magnesia, Mullite, Boron Carbide, etc.) | ||

| By Structure | Transparent | |

| Opaque | ||

| Porous | ||

| By End-user Industry | Electronics and Semiconductor | |

| Automotive and Transportation | ||

| Medical and Dental | ||

| Energy and Power | ||

| Other End-user Industries (Industrial Equipment, Chemical, Metallurgy, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the monolithic ceramics market?

The monolithic ceramics market stands at USD 25.82 billion in 2026 and is forecast to reach USD 34.75 billion by 2031.

Which material type is growing fastest through 2031?

Silicon carbide is projected to rise at a 6.58% CAGR through 2031 on EV and renewable-power adoption.

Why is Asia-Pacific the largest regional contributor?

Concentrated semiconductor investment and China’s expanding advanced-ceramics base deliver 44.22% of 2025 revenue and a 6.88% CAGR through 2031.

How are yttrium export controls affecting supply?

China’s 2025 restrictions cut U.S. imports 95%, sending high-purity yttria prices soaring and pressuring electrolyzer membrane costs.

Page last updated on: