Advanced Ceramics Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 105.12 Billion |

| Market Size (2031) | USD 146.13 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Ceramics Market Analysis by Mordor Intelligence

The Advanced Ceramics Market size is estimated at USD 105.12 billion in 2026, and is expected to reach USD 146.13 billion by 2031, at a CAGR of 6.81% during the forecast period (2026-2031). This steady ascent stems from the electrification of vehicles, demand for high-frequency power electronics, and sovereign-manufacturing directives that localize substrate output in the United States, the European Union, and China. Supply-chain realignment favors materials able to handle temperatures above 1,200 °C, extend component life, and enable miniaturization in AI servers and 5G infrastructure. Manufacturers are widening portfolios to include piezoelectric titanates, aluminum nitride substrates, and zirconia-based bioceramics that win faster regulatory approvals. At the same time, capital-intensive sintering processes and limited recycling options temper near-term profitability, prompting incumbents to pursue efficiency gains and strategic partnerships.

Key Report Takeaways

- By material type, alumina captured 41.26% of the 2025 share; titanate ceramics hold the highest 7.82% CAGR outlook.

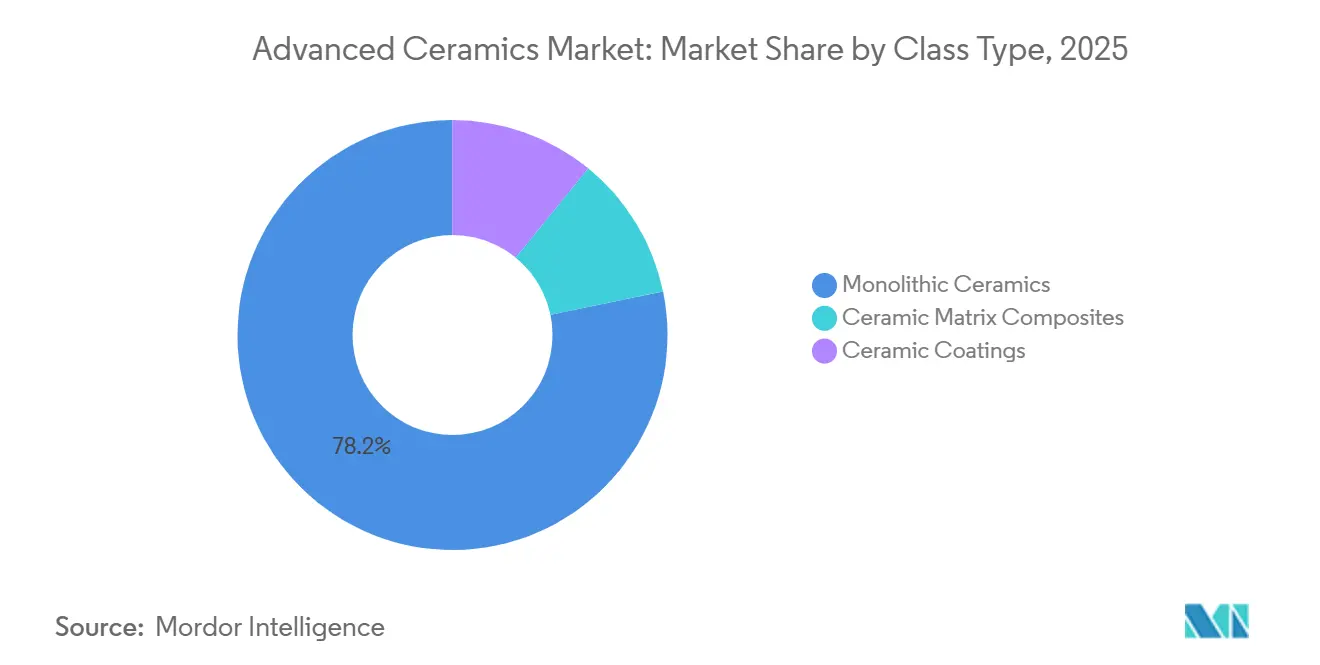

- By class type, monolithic products commanded 78.24% of 2025 revenue; ceramic matrix composites are pacing at an 8.17% CAGR.

- By application, electroceramics led with 45.31% of 2025 revenue, while bioceramics is advancing at an 8.79% CAGR through 2031.

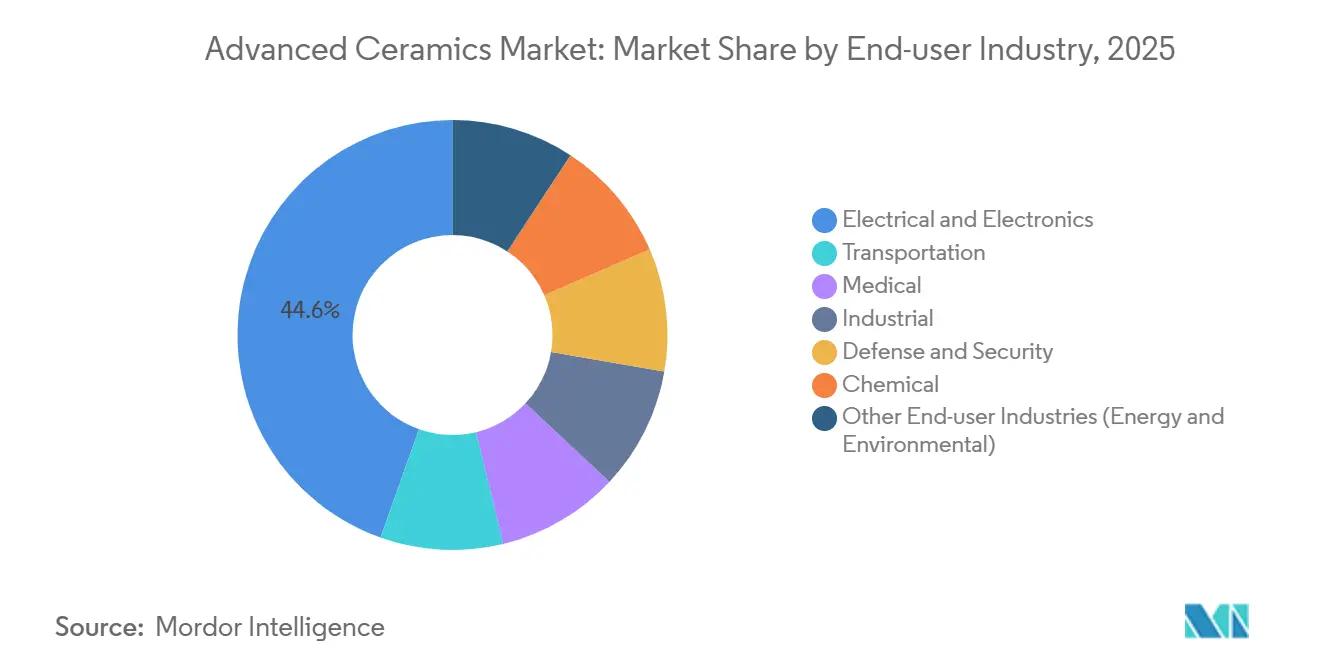

- By end-user industry, electronics accounted for 44.56% of sales in 2025, whereas the medical segment is anticipated to post the fastest 11.87% CAGR to 2031.

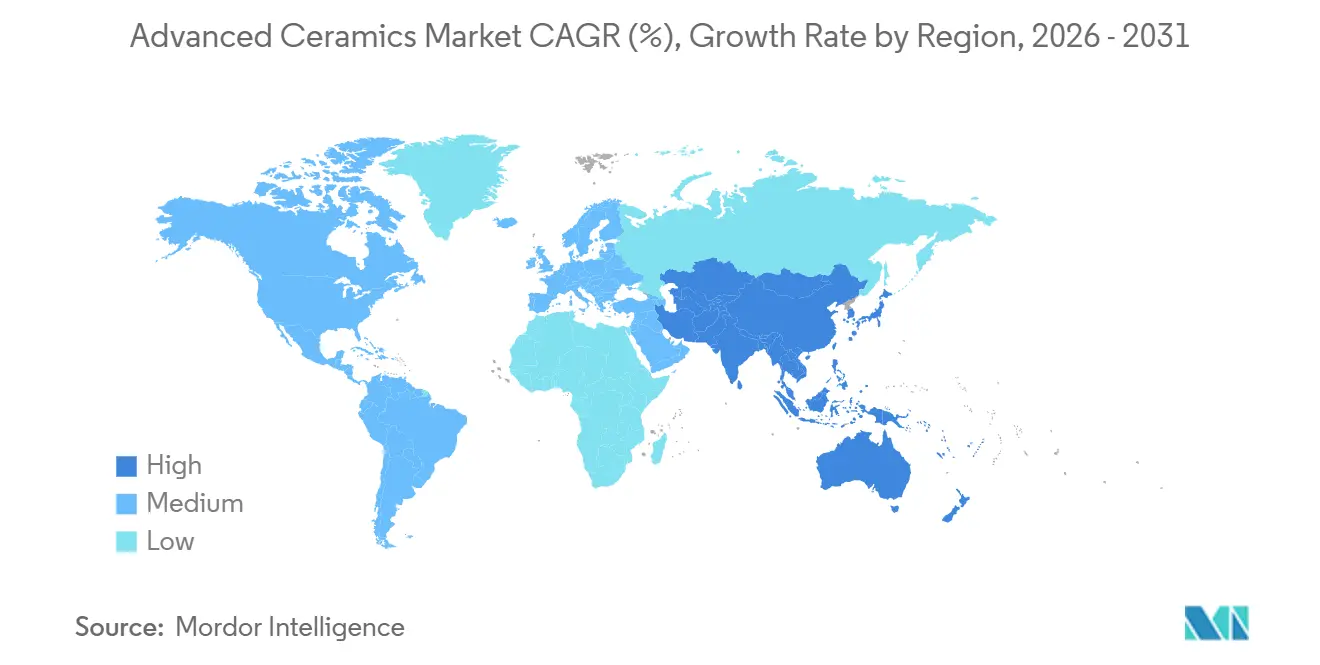

- By geography, Asia-Pacific controlled 54.22% of 2025 turnover and is expanding at a 7.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Advanced Ceramics Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from metals and high-performance plastics | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Expanding use in medical implants and devices | +1.8% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Demand in high-frequency power electronics | +1.5% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Rising aerospace and defense thermal needs | +1.1% | North America, Europe | Long term (≥ 4 years) |

| Solid-state batteries and SOFC adoption | +1.0% | Global, early traction in Japan, Germany, California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift From Metals And High-Performance Plastics

Automotive and aerospace weight-reduction rules accelerate the swap from steel and aluminum to silicon nitride and silicon carbide. Hyundai-Transys showed ceramic bearings cut parasitic losses by 12% versus steel in 2024 tests[1]Hyundai-Transys Research Center, “Ceramic Bearing Efficiency Study,” hyundai-transys.com. NASA’s 2025 work proved silicon-nitride turbine blades endure 1,400 °C, 200 °C hotter than nickel superalloys, while lowering mass by 40%[2]NASA Glenn Research Center, “High-Temperature Silicon Nitride Turbine Blades,” nasa.gov. Yet NSK’s 2024 filing revealed that ceramic-ball costs above USD 15 each keep some suppliers on hybrid designs. Overall, OEMs continue to qualify all-ceramic parts for EV gearboxes and hypersonic propulsion despite cost gaps.

Expanding Use In Medical Implants And Devices

Zirconia-toughened alumina and yttria-stabilized zirconia are replacing cobalt-chromium in joint arthroplasty because of low ion release and high wear resistance. Zimmer Biomet won FDA 510(k) clearance in March 2025 for its Persona IQ femoral component featuring a zirconia head that lowers polyethylene wear by 60% over 15 years. Stryker’s 2025 investor deck said its Mako platform with ceramic liners cut revision surgeries below 2% at 10 years. Although Europe’s stricter Medical Device Regulation extends launch timelines 18-24 months, the added rigor consolidates share for ISO 13485-certified plants.

Demand In High-Frequency Power Electronics

Gallium-nitride and silicon-carbide transistors need aluminum nitride and silicon-carbide substrates with thermal conductivity above 150 W/m-K. Kyocera expanded Kagoshima AlN output by 30% in January 2025 to serve 800-V EV platforms. Maruwa noted 45% shipment growth to 5G customers with ASPs above USD 8/cm² during fiscal 2024. An IEEE 2025 study found SiC substrates slash inverter cooling mass 25%, letting automakers delete liquid loops. These advantages support rapid substrate uptake through 2027.

Rising Aerospace And Defense Thermal Needs

Ceramic matrix composites now appear in high-pressure turbine sections. GE Aviation disclosed over 200 kg of SiC–SiC CMC parts per LEAP engine, trimming fuel burn by 1.5%. Rolls-Royce’s June 2025 data showed UltraFan CMC blades run at 1,500 °C, 100 °C hotter than metal Trent XWB parts, boosting thermal efficiency 2%. Oerlikon Surface Solutions landed a USD 42 million U.S. Air Force contract in September 2024 for yttria-stabilized zirconia coatings rated 1,650 °C. Defense programs, therefore, lock in long-term demand for ultra-high-temperature ceramics.

Restraints Impact Analysis of Advanced Ceramics Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs | -0.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Complex, capital-intensive manufacturing | -0.7% | Global, barriers highest in emerging markets | Medium term (2-4 years) |

| Limited end-of-life recycling infrastructure | -0.4% | Global, most pronounced in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Costs

Kiln temperatures above 1,600 °C and post-machining inflate ceramic prices 3-5× molded polymers. CoorsTek’s 2024 deck showed alumina substrates need 12 MWh per ton, with volatile European gas adding USD 0.80-1.20/kg. CeramTec’s 2025 sustainability report projected EUR 18 million (USD 19.4 million) to electrify kilns, raising unit cost by 6% until power prices stabilize. Small-batch niches like pyrolytic boron nitride exceed USD 500/kg, deterring wider uptake.

Complex, Capital-Intensive Manufacturing

Greenfield plants require USD 50-150 million for powder synthesis, isostatic presses, and metrology. Morgan Advanced Materials invested USD 12 million with Penn State to pilot SiC fibers that will not be commercialized before 2027. ISO 17025 accreditation adds 8-12 weeks to aerospace and medical qualification. Emerging-market suppliers struggle to recruit ceramics engineers, paying 40% salary premiums for expatriates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Advanced Ceramics Market Segment Analysis

By Material Type:

Alumina Anchors Electronics, Titanate Gains in SensorsAlumina captured 41.26% of the advanced ceramics market share in 2025, reflecting its entrenched use as the dielectric in multilayer ceramic capacitors that ship in the trillions every year. That dominance equated to the largest slice of the advanced ceramics market size for any individual material during the base year. Titanate ceramics, led by barium titanate and lead zirconate titanate, are projected to clock a 7.82% CAGR through 2031, the fastest rate among material categories. Together, alumina and titanate therefore set the tone for how the advanced ceramics market will evolve in electronic components and sensing technologies. Demand for alumina MLCC dielectrics intensified after Murata expanded Izumo capacity by 20% to satisfy AI-server boards that need up to 2,000 capacitors each.

Beyond MLCCs, zirconia commands a share in dental crowns and femoral heads because yttria-stabilized grades deliver fracture toughness above 10 MPa√m, double alumina. Silicon carbide and silicon nitride remain staples for high-temperature hardware, with SiC substrates already embedded in 800-volt electric-vehicle inverters. Aluminum nitride sells at premium prices—USD 8–12 per cm²—because 170 W/m-K thermal conductivity keeps gallium-nitride radio-frequency amplifiers within safe operating limits. Magnesium silicate catalyst supports and pyrolytic boron nitride crucibles fill smaller but profitable niches as the advanced ceramics market diversifies into petrochemical reforming and semiconductor crystal growth. Collectively, these materials define the next phase of functional specialization across the advanced ceramics market.

By Class Type:

Monolithic Dominance Faces CMC DisruptionMonolithic products generated 78.24% of revenue in 2025, giving them the largest position in the overall advanced ceramics market. That commanding presence translated into the single biggest contribution to the advanced ceramics market size for any class type. Yet ceramic matrix composites are forecast to expand at an 8.17% CAGR, almost two percentage points above the market average, as aerospace primes qualify CMC turbine components capable of running 100 °C hotter than nickel alloys. Powder-to-part vertical integration at Kyocera, CoorsTek, and TDK allows monolithic substrates to meet tight AI-server impedance tolerances, thereby reinforcing short-term volume advantages.

Momentum nonetheless is shifting. Safran reported that CMC shrouds trim fuel burn by 1.2% on LEAP-equipped aircraft. Praxair Surface Technologies documented yttria-stabilized zirconia coatings that stretch overhaul intervals from 15,000 to 22,000 flight hours, a USD 3.2 million benefit per engine. These gains illustrate how coatings and composites erode the incumbent lead of monolithics. The advanced ceramics market, therefore, stands at a crossroads where volume remains in monolithic formats while value migrates to engineered CMC and coating architectures that lengthen service life in demanding thermal profiles.

By Application:

Electroceramics Lead, Bioceramics SurgeElectroceramics delivered 45.31% of application revenue in 2025, marking the single biggest vertical inside the advanced ceramics market. Multilayer ceramic capacitors dominate this slice, and Samsung Electro-Mechanics is adding 10 billion units per month of MLCC capacity by Q2 2026, underscoring strong unit intensity in AI accelerators. Bioceramics, led by zirconia-toughened alumina implants, will grow at an 8.79% CAGR through 2031, the highest among application groups. That pace positions medical devices to add the most absolute dollars to the advanced ceramics market size after electronics.

Structural ceramics such as silicon-nitride cutting inserts and alumina armor plates continue to find traction in transportation and defense. Wear and corrosion components protect pump seals and valve seats in chemical processing, while thermal-barrier ceramics like hafnium diboride guard scramjet leading edges at 2,000 °C. Cordierite diesel-particulate filters capture 95% of soot to help heavy-duty trucks meet Euro VI targets, reflecting environmental pull on the advanced ceramics market. Catalyst supports and high-temperature filters, therefore, remain indispensable even as new medical and electronic uses proliferate.

By End-User Industry:

Electronics Dominate, Medical AcceleratesElectrical and electronics accounted for 44.56% of the advanced ceramics market size in 2025, yielding the largest slice of any customer vertical in the market. Persistent double-digit data-center growth and vehicle digitization keep MLCC demand elevated, and UBS reported distributor inventory dipped to only 45 days of supply in late 2024. The medical segment, however, is slated for an 11.87% CAGR through 2031, the fastest trajectory across end users, driven by more than 2.5 million annual joint-replacement procedures in mature economies. That expansion propels medical devices toward a bigger share of the advanced ceramics market size by decade-end.

Transportation, spanning automotive and aerospace, relies on silicon-carbide substrates and ceramic matrix composites to meet lightweighting mandates. Industrial sectors use alumina and silicon carbide tooling to machine nickel-based superalloys, while the chemical industry needs cordierite honeycomb supports to oxidize volatile organic compounds at 98% efficiency. Defense agencies obligated USD 1.8 billion in fiscal 2025 for advanced materials under the U.S. Defense Production Act, highlighting a sovereign push that reverberates across the advanced ceramics market. Collectively, these diverse customer sets ensure that no single industry can dictate future growth paths, preserving balanced demand dynamics.

Geography Analysis

APAC Advanced Ceramics Market

Asia-Pacific generated 54.22% of revenue in 2025, making it the largest regional slice of the advanced ceramics market. That lead is projected to widen as the region posts a 7.11% CAGR through 2031, well ahead of North America and Europe. Japan’s Ministry of Economy, Trade and Industry indicated domestic shipments hit JPY 1.2 trillion in 2024 (USD 8.1 billion) and still grew exports 18% despite geopolitical frictions. Vertical integration at Kyocera, Murata, and TDK—spanning powder synthesis to electrical testing—compresses cycle times and safeguards proprietary know-how, cementing Asia-Pacific’s dominance in the advanced ceramics market.

East Asia and India Advanced Ceramics Market

South Korea accelerates capacity via Samsung Electro-Mechanics and LG Innotek, whose combined 2024 capital outlays topped KRW 800 billion (USD 610 million) for new MLCC and substrate lines. China’s Made in China 2025 incentives subsidize alumina-powder expansion at Sinocera’s Yixing plant, now producing 15,000 metric tons per year. India remains import-dependent for 70% of its needs, yet its Production-Linked Incentive scheme for electronics foresees localized substrate assembly by 2028, potentially adding fresh momentum to the regional advanced ceramics market.

North America Advanced Ceramics Market

The advanced ceramics demand in North America is anchored by aerospace and defense programs that favor U.S. suppliers such as CoorsTek, 3M, and Corning. The Inflation Reduction Act’s domestic-content clauses prompted General Motors to commit to U.S. aluminum-nitride substrates in Ultium battery packs from 2026 onward. Pratt & Whitney Canada is deploying ceramic-matrix-composite turbine components in PW800 engines to improve fuel economy for Gulfstream business jets, demonstrating the technology’s northward diffusion. Mexico’s Querétaro automotive hub hosts substrate assembly lines that supply U.S. EV plants, capitalizing on regional-value-content rules under USMCA.

Europe Advanced Ceramics Market

Europe represented a considerable market share in 2025, with Germany, France, and the United Kingdom leading production and consumption. CeramTec and Morgan Advanced Materials operate ISO 13485-certified plants producing zirconia femoral heads and alumina acetabular liners. While the European Medical Device Regulation lengthens approval cycles, it also filters out non-compliant importers, funneling demand toward established brands. Germany’s Fraunhofer IKTS collaborates with Siemens Energy to achieve 65% electrical efficiency in hydrogen-fueled SOFC stacks by 2027. EU Horizon Europe grants are channeling EUR 120 million into ultra-high-temperature ceramics for hypersonic vehicles, ensuring the region remains relevant in the advanced ceramics market.

South America and MEA Advanced Ceramics Market

South America and the Middle East and Africa are witnessing rising demand for advanced ceramics. Brazil’s EMBRAER is testing silicon-nitride flap-track rollers to shave aircraft maintenance costs, while Saudi Aramco finances pyrolytic boron nitride crucibles for in-house semiconductor pilot lines. Both regions, however, depend on imported powders, limiting value capture within the advanced ceramics market. Long-term upside hinges on knowledge transfer and the maturation of local ceramic-engineering curricula.

Mordor Intelligence provides coverage of the advanced ceramics market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Value Chain Analysis

The advanced ceramics value chain starts with high-purity oxide and non-oxide inputs (alumina, zirconia, titanate, SiC/Si3N4, AlN) and critical additives such as rare-earth stabilizers, where yttrium cost volatility is a recurring risk for zirconia grades. Material conversion covers powder synthesis and granulation through forming (tape casting, injection molding, isostatic pressing), then debinding, sintering/hot pressing/HIP, and precision post-machining plus metallization or joining for substrates and hermetic packages. Qualification cycles also shape delivery, with high-purity grades taking 12-24 months to approve and new hot isostatic pressing capacity facing equipment lead times exceeding 18 months, so throughput and yield management remain central to competitiveness.

On the downstream side, parts and semi-finished components move through specialized distributors and direct OEM channels into electronics (MLCCs, power modules, RF, semiconductor equipment), medical implants, and aerospace/defense coatings and CMC hardware. Vertical integration and capability consolidation show up in 2026 actions, including Kyocera International, Inc. expanding its Hendersonville, North Carolina fine ceramics plant with a 30,000-psi cold isostatic press and 16,000 square feet of added space, along with deals that pull adjacent technologies under one roof (McDanel Advanced Materials and Richland Glass strategic merger; HEICO via Exxelia acquiring 90% of CalRamic Technologies for high-voltage ceramic capacitors). Bosch Advanced Ceramics rebranded to Sinto Advanced Ceramics Europe GmbH after integration into the Sintokogio Group, reflecting how production know-how, equipment access, and end-market certifications are increasingly managed within larger industrial groups.

Competitive Landscape

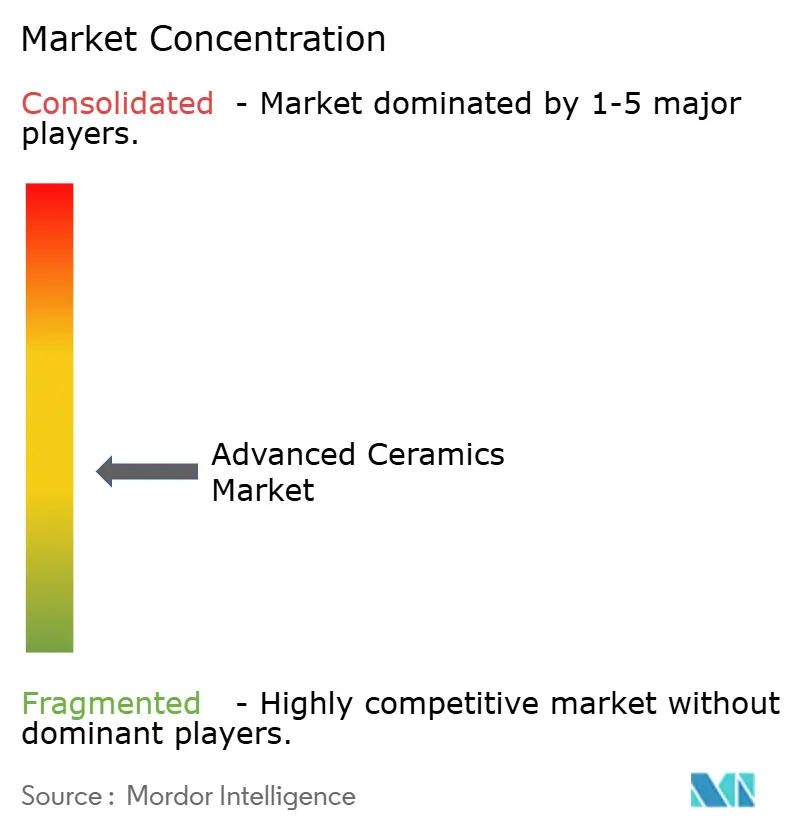

The advanced ceramics market is moderately fragmented. Japanese incumbents maintain powder-to-module vertical integration, giving them tight control of dielectric formulations and multilayer stacking accuracy. Murata’s 2025 roll-out of 0402-size capacitors with 100 V ratings for AI accelerator boards illustrates the edge gained from in-house material science. Kyocera expanded Kagoshima AlN capacity by 30% in 2025 to protect its share in EV inverter substrates.

Advanced Ceramics Industry Leaders

KYOCERA Corporation

CoorsTek Inc.

CeramTec GmbH

Morgan Advanced Materials

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Advanced Ceramics Market Companies Covered in this Report

- 3M

- AGC Inc.

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek Inc.

- Corning Incorporated

- Elan Technology

- International Syalons (Newcastle) Limited

- KYOCERA Corporation

- MARUWA Co., Ltd.

- Materion Corporation

- McDanel Advanced Material Technologies LLC

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Rauschert Heinersdorf-Pressig GmbH

- Saint-Gobain

- SPT-Group

- Vesuvius

- Wonik QnC Corporation

Market Opportunities and Future Outlook

Electronics and semiconductor manufacturing equipment continue to create whitespace for higher-performance ceramic substrates and precision components as power density and thermal-management requirements tighten in AI servers, RF, and power electronics. Capacity commitments point to where suppliers are directing capital, including Kyocera’s Hendersonville, North Carolina cold isostatic pressing capability and plant floor-space expansion (April 2026) and NGK’s JPY 70.0 billion investment in a new ceramic production site in Nomi City, Ishikawa Prefecture for semiconductor manufacturing equipment, with mass production scheduled for October 2029. On the demand side, Samsung Electro-Mechanics disclosed a facilities investment plan across Busan, Sejong, and Thailand through 2040 to expand MLCC and FC-BGA substrate capacity, reinforcing the premium on scale, defect control, and materials know-how in electroceramics.

Aerospace and defense programs offer a second opportunity lane, where public funding and OEM qualification requirements reward suppliers that can industrialize CMC and ultra-high-temperature processing. AeroVironment received a USD 20 million Ceramics Advanced Materials and Processes (CAMP) contract from the Air Force Research Laboratory (May 2026) to advance next-generation ceramic matrix composites, supporting process maturation and downstream adoption in flight hardware supply chains. At the same time, the market continues to show a sustainability and supply-risk gap around end-of-life recycling and rare-earth stabilizer exposure, which opens room for powder recovery, lower-energy firing routes, and material substitutions that reduce dependence on constrained inputs such as yttrium while maintaining qualification requirements in medical and aerospace programs.

Recent Industry Developments in Advanced Ceramics Market

- June 2026: HEICO Corporation, through its Exxelia business, acquired a 90% ownership stake in CalRamic Technologies, a manufacturer of high-voltage ceramic capacitors. The acquisition strengthens Exxelia’s position in ceramic capacitor supply for demanding electronics applications where reliability and voltage performance drive specification, and it tightens control over a specialized component segment within electroceramics.

- January 2025: Kyocera boosted aluminum-nitride substrate capacity by 30% at Kagoshima to serve 800-V EV battery systems, supported by an investment of JPY 8 billion (USD 54 million). The expansion targets a key bottleneck in power electronics thermal management, where AlN’s high thermal conductivity supports higher switching power densities.

- May 2024: Morgan Advanced Materials entered a USD 12 million collaboration with Pennsylvania State University to develop silicon carbide fibers for ceramic matrix composites aimed at aerospace turbine applications. The partnership includes establishing a chemical vapor infiltration reactor at Penn State’s Materials Research Institute, building a pathway from materials R&D to pilot-scale capability for CMC supply chains.

Advanced Ceramics Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers engineered ceramic materials and parts that are designed for high-performance use. Adoption is driven by performance characteristics such as heat resistance, wear resistance, electrical behavior, and chemical stability.

Scope exclusions: Traditional clay-based structural ceramics and glass-ceramics are excluded from the market totals.

Segments Covered in This Report

- By Material Type

- Alumina

- Zirconia

- Titanate

- Silicon Carbide

- Silicon Nitride

- Aluminum Nitride

- Magnesium Silicate

- Pyrolytic Boron Nitride

- Others

- By Class Type

- Monolithic Ceramics

- Ceramic Matrix Composites

- Ceramic Coatings

- By Application

- Structural Ceramics

- Bioceramics

- Electroceramics

- Wear and Corrosion Components

- Thermal Barrier and UHTC Components

- Catalyst Supports and Filters

- Others (Environmental and Energy Systems)

- By End-user Industry

- Electrical and Electronics

- Transportation

- Medical

- Industrial

- Defense and Security

- Chemical

- Other End-user Industries (Energy and Environmental)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by pinning down the demand and supply signals that can be checked in public data before we build the model. We refer to sources such as the USGS for minerals and industrial materials context, US Census Bureau trade statistics for import and export patterns tied to ceramic materials, and OECD macro indicators to anchor manufacturing cycles by region. For end-use pull signals, we also review sources such as the International Energy Agency for energy transition equipment trends, along with FDA and NIH publications to understand activity in medical devices that use advanced ceramic components.

After that, we use company annual reports, investor presentations, and credible press coverage to extract capacity expansions, application focus, and regional mix statements that help shape assumptions. Select paid database subscriptions are used for company financials and intelligence, patent activity screening, and shipment-level import and export checks when public reporting is not detailed enough. The sources named here are illustrative only, and additional public and paid references were used for data collection, cross-checking, and clarification during the study.

Primary Interviews and Surveys

Primary work was used to test what we saw in desk research and to fill gaps around real pricing, adoption timing, and which applications are counted as advanced ceramics versus adjacent materials. Interviews and survey responses came from a mix of material suppliers, component makers, distributors, and procurement or engineering stakeholders in key end-use industries. Findings were then checked across the main consuming regions so outlier views did not steer the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 45% |

| Mid tier: 46% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 20% | Managers: 51% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic. The top-down view is constructed from end-use demand pools and production and trade signals that help reconstruct likely consumption by region. The model is then corroborated with selective bottom-up approximations, such as sampling average selling prices for common component categories and combining them with approximate shipment or usage volumes shared by interviewees.

Practical inputs that shape the totals include trends in electronics manufacturing output, medical device production signals, automotive and industrial production cycles, and the mix shift toward higher-value engineered parts, which can change average prices even when volumes move slowly. Material-side indicators, such as availability and pricing direction for key raw materials, are used to sanity-check whether revenue growth is coming from real demand or from cost pass-through. When a bottom-up view is incomplete for smaller applications, we bridge gaps using penetration-style assumptions that are validated in interviews and then constrained by trade and macro reality checks.

For forecasting, scenario analysis is used. It is guided by how end-user order patterns, capacity additions, and pricing expectations are described by industry participants. This keeps the forward view explainable, since drivers like utilization, replacement cycles, and qualification timelines tend to matter more than purely statistical extrapolation in this market.

Data Validation & Update Cycle

Validation is handled through triangulation across desk signals, primary feedback, and internal math checks inside the model. Outputs are compared against independent indicators such as trade direction, manufacturing growth rates, and known capacity or expansion announcements, and then variances are investigated before sign-off. When a number looks too high or too low, assumptions are revisited, and follow-up calls are triggered with respondents who have direct pricing or volume visibility.

The work goes through multi-step analyst reviews, including consistency checks between regions and end uses so growth patterns remain realistic. Reports are refreshed annually, and interim updates are made when material events occur, such as major plant expansions, demand shocks in key end uses, or meaningful price swings. Before delivery, a final refresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Advanced Ceramics Market Size Measured Against Other Published Estimates

Published market numbers for advanced ceramics can vary a lot, even when the titles look similar, because product boundaries and the value basis are not always aligned. Differences also come from whether a source sizes the full value of end products or only the ceramic material and component portion that is directly attributable to advanced ceramics.

The table shows a wide spread between sources. In Mordor Intelligence's model, the totals are limited to advanced (engineered) ceramics while explicitly excluding traditional clay-based structural products and glass-ceramics, which can shift totals when other studies blend adjacent categories. Gaps can also show up when forecasts assume different price progression paths, use different currency conversion timing, or apply aggressive adoption curves in electronics and industrial uses without strong cross-checks against trade and capacity signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 105.12 B (2026) | |

| Global Consultancy A | USD 119.44 B (2025) | Uses an earlier base year and can include a broader revenue stack across downstream products, which inflates totals when ceramic content is not isolated consistently by application. |

| Industry Publisher B | USD 12.07 B (2024) | Likely reflects a narrower slice of the market (often limited to select materials or specialty components), and the smaller base year and scope selection reduce the reported value versus full-market accounting. |

Taken together, the comparison suggests that scope boundaries and what gets counted as revenue are the main reasons the market sizes do not line up. By tying assumptions to observable end-use signals, checking pricing logic, and keeping inclusions and exclusions explicit, the final estimate stays traceable and repeatable for planning discussions.

Key Questions Answered in the Report

What is the current value of the advanced ceramics market?

The advanced ceramics market size is estimated at USD 105.12 billion in 2026 and is on track for USD 146.13 billion by 2031.

Which application accounts for the largest revenue?

Electroceramics, led by multilayer ceramic capacitors, generated 45.31% of 2025 revenue.

Which end-user industry is growing fastest?

The medical industry segment is projected to post an 11.87% CAGR through 2031 due to wider adoption of zirconia-based orthopedic implants.

Why is Asia-Pacific so dominant in advanced ceramics?

The region hosts vertically integrated giants like Kyocera and Murata and benefits from concentrated MLCC and EV-inverter supply chains.

What hinders wider adoption of advanced ceramics?

High production costs above 1,600 °C sintering, complex capital-intensive processes, and limited recycling infrastructure restrain growth.

Are ceramic matrix composites gaining share?

Yes, CMCs are forecast to expand at an 8.17% CAGR through 2031 as aerospace and defense programs qualify hotter-running turbine components.

Page last updated on: