Technical Ceramics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

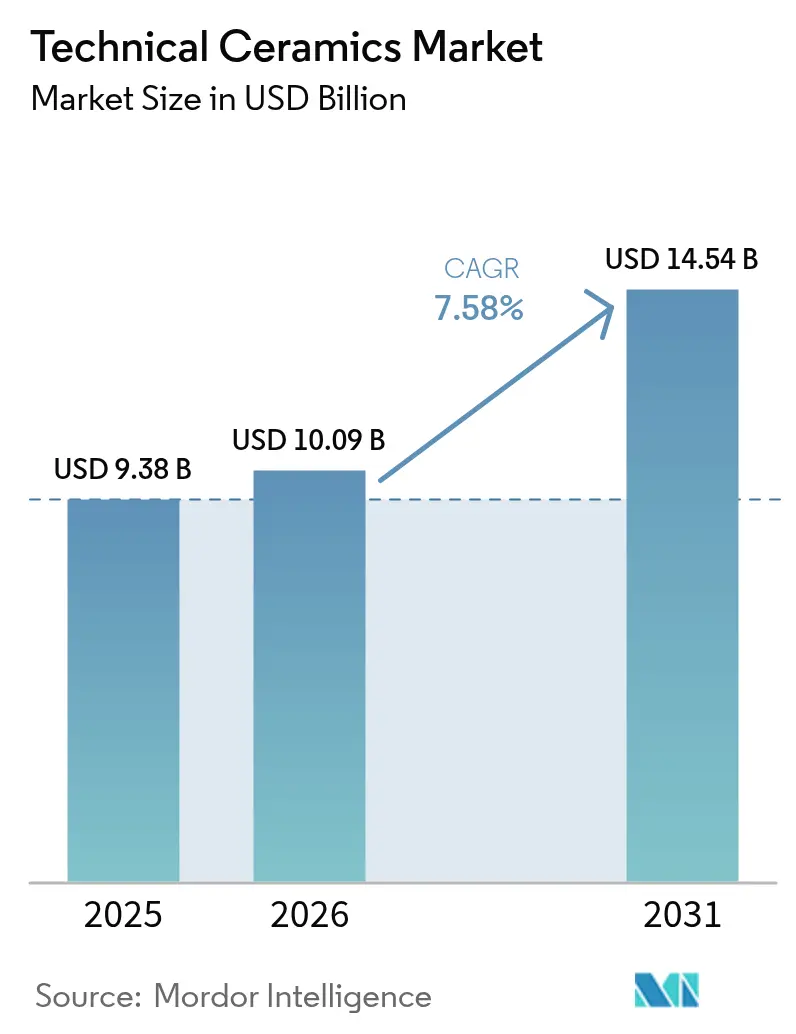

| Market Size (2026) | USD 10.09 Billion |

| Market Size (2031) | USD 14.54 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Technical Ceramics Market Analysis by Mordor Intelligence

Technical Ceramics Market size in 2026 is estimated at USD 10.09 billion, growing from 2025 value of USD 9.38 billion with 2031 projections showing USD 14.54 billion, growing at 7.58% CAGR over 2026-2031. Demand is clustering around semiconductor substrates, electric-vehicle (EV) thermal control parts, and biocompatible implants, where failure tolerance is virtually zero and material science is a strategic differentiator. Rising fab construction across China, Japan, and South Korea is lifting consumption of aluminum nitride and silicon carbide packages, while 800 V EV drive-train architectures force automakers to specify ceramic heat spreaders that can dissipate more than 200 W/mK without compromising electrical insulation. Supply chains remain vulnerable to critical-mineral concentration, yet leading producers are countering with capacity additions in lower-risk jurisdictions and tighter recycling loops that reduce virgin material exposure. Monolithic formulations still dominate volume, but ceramic-matrix composites are accelerating fastest as aerospace and defense primes pay premiums for lighter, hotter-capable components that cut mass and raise fuel efficiency.

Key Report Takeaways

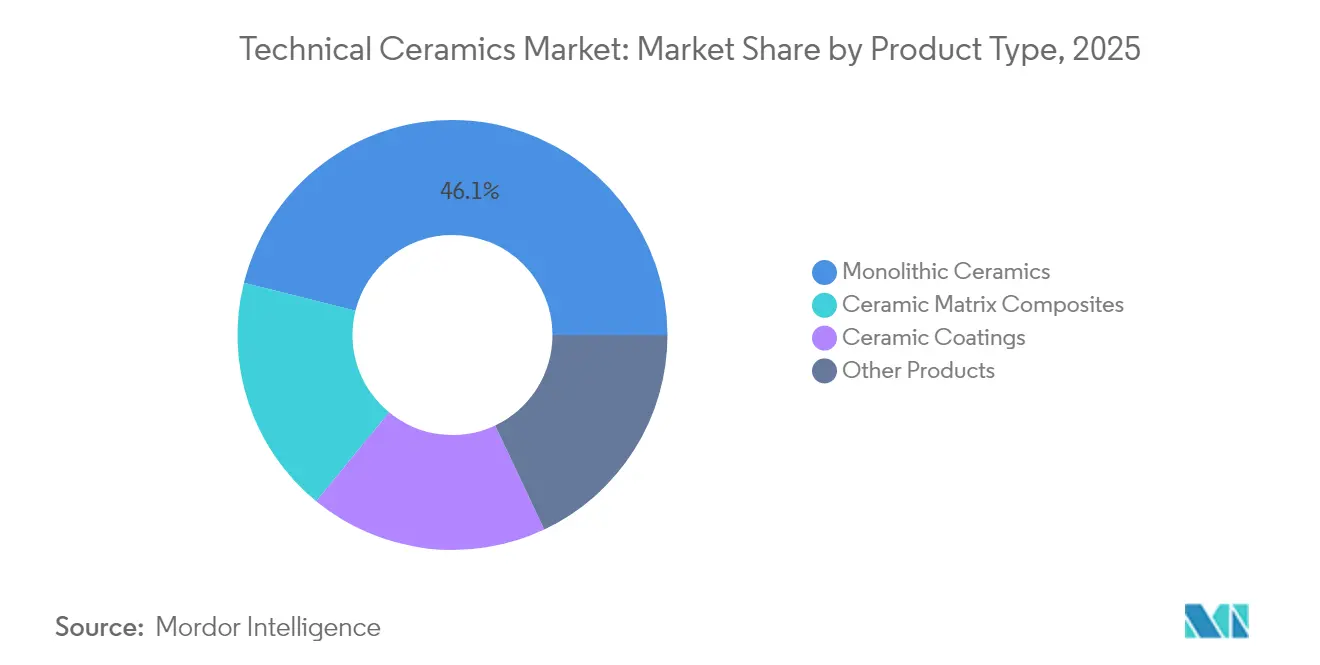

- By product type, monolithic ceramics held 46.10% of the technical ceramics market share in 2025, while ceramic matrix composites are poised for the quickest expansion at an 8.72% CAGR through 2031.

- By material class, oxide ceramics captured 62.80% revenue in 2025; non-oxide variants are projected to register a 7.76% CAGR during 2026-2031.

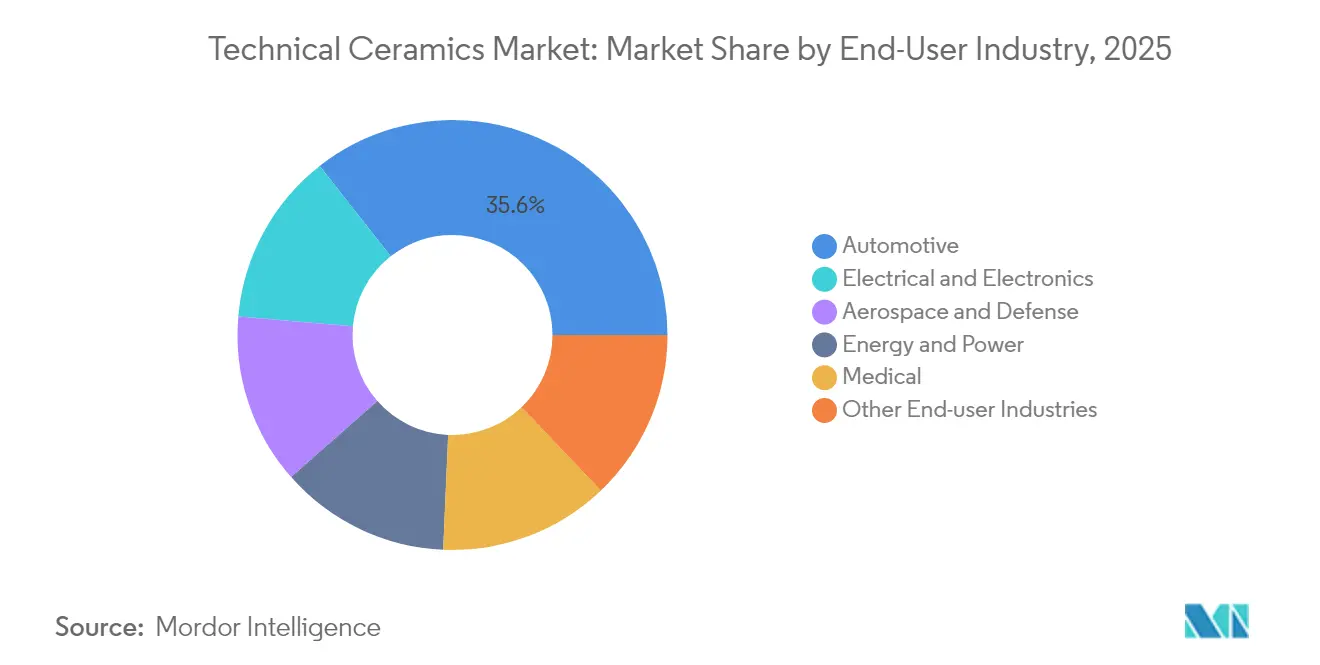

- By end-user industry, automotive accounted for 35.60% of the technical ceramics market size in 2025, whereas electrical and electronics is slated to grow fastest at 9.29% annually to 2031.

- By key application, insulators and substrates secured 54.20% share of the technical ceramics market size in 2025; wear-resistant parts and bearings should climb at an 8.11% CAGR over the forecast window.

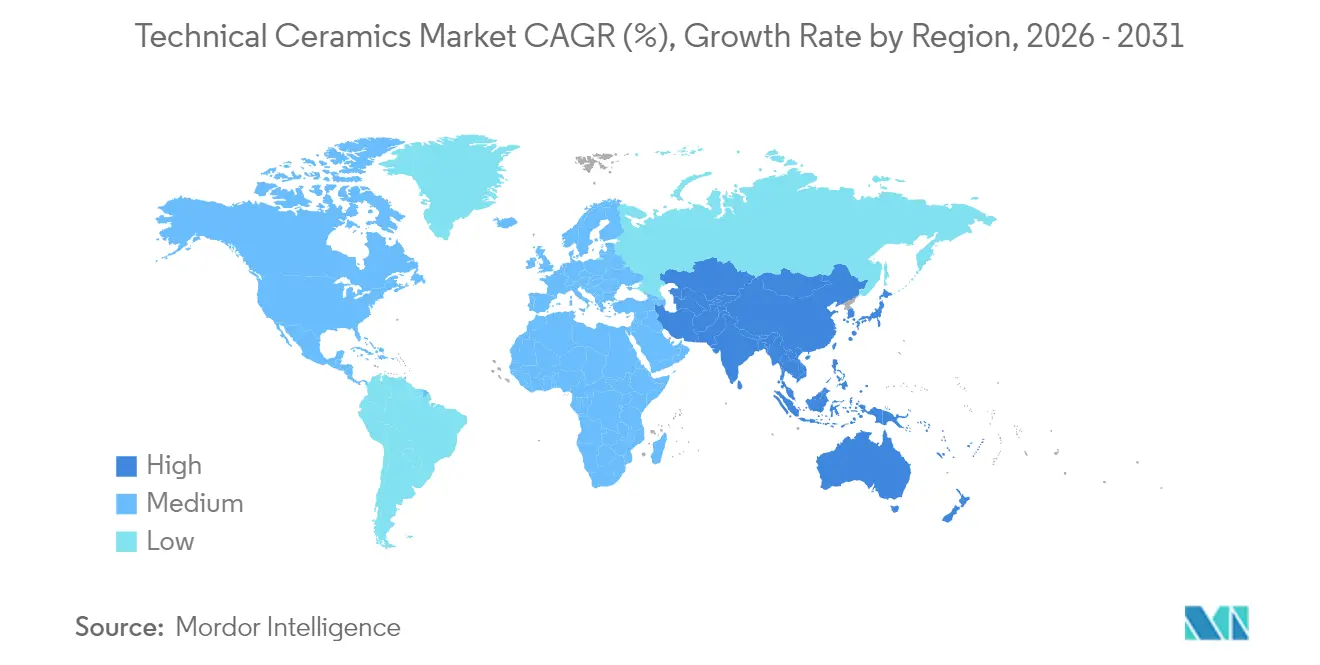

- By region, Asia Pacific dominated with 43.40% of the 2025 total and is forecast to compound at 7.84% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Technical Ceramics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding semiconductor & consumer-electronics output in Asia Pacific | +2.10% | Asia Pacific core, spill-over to North America | Medium term (2-4 years) |

| EV power-train thermal-management needs | +1.80% | Global, with concentration in China, Europe, North America | Short term (≤ 2 years) |

| Rising use in high-value medical implants & devices | +1.40% | North America & EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Hydrogen-electrolyser stack components | +1.20% | Europe core, expanding globally | Long term (≥ 4 years) |

| In-space manufacturing & satellite hardware | +0.90% | North America & Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Semiconductor & Consumer-Electronics Output in Asia Pacific

Fab build-outs across Taiwan, mainland China, Japan, and South Korea are resetting the demand baseline for aluminum nitride and silicon carbide substrates that can survive peak junction temperatures exceeding 1,000 °C while ensuring dielectric integrity. Chip designers pursuing gallium nitride architectures are widening thermal budgets faster than legacy metal lead-frames can handle, making ceramic packages an essential throughput enabler. Kyocera is funneling USD 470 million into a dedicated Japanese line to synchronize ceramic substrate availability with next-generation processor nodes. Synchronizing substrate growth cycles with lithography ramp-ups remains difficult because kilns require longer validation loops than semiconductor clean-rooms, but tier-one device makers are now signing multi-year offtake agreements to lock in supply. Regional governments are simultaneously underwriting advanced-materials clusters to reduce reliance on overseas feedstocks, a policy move that could compress lead times and moderate pricing volatility.

EV Power-Train Thermal-Management Needs

Global EV shipments surpassed 15 million units in 2024, and nearly every platform upgrade now targets 800 V electrical architectures that squeeze more power through smaller inverters. Silicon carbide power modules dissipate heat at triple the rate of silicon devices, yet the allowable junction temperature band remains tight, creating a design window ideally served by ceramic heat spreaders boasting greater than 200 W/mK conductivity. CeramTec’s chip-on-heatsink solution lowers thermal resistance while maintaining dielectric separation, a combination that lengthens module life in high-vibration automotive environments. Automakers are price-sensitive, but warranty liabilities linked to thermal failures tip purchasing decisions toward high-reliability ceramics despite higher unit costs. As fleet electrification accelerates in China, Europe, and the United States, demand for ceramic substrates, busbars, and gel-coated cooling plates is scaling in parallel.

Rising Use in High-Value Medical Implants & Devices

Orthopedic and dental surgeons are migrating toward zirconia and hydroxyapatite implants because these materials integrate with bone and resist infection better than metal alloys. Patient-specific 3D-printed lattices streamline operating-room fitment times and reduce revision surgeries. United States regulators cleared several trabecular ceramic spinal cages in 2024, a milestone that shortened the historical approval cycle and signaled growing FDA confidence in ceramic bio-compatibility. Margins in the medical device channel exceed those in volume automotive parts, encouraging producers to dedicate clean-room space and traceability protocols that satisfy stringent sterilization rules. These factors lock in established suppliers while tempering rapid capacity additions, meaning revenue growth stems from premium pricing rather than large tonnage.

Hydrogen-Electrolyzer Stack Components

Europe’s green-hydrogen roadmap calls for 134 GW of electrolyzer capacity by 2030, much of it favoring solid-oxide technology that operates near 800 °C. Such temperatures rule out metallic separators, elevating demand for ceramic interconnects that maintain ionic conductivity without warping under redox cycling. Topsoe has committed EUR 94 million to Europe’s largest SOEC plant, with initial stacks incorporating alumina-based gas diffusion layers. Scaling ceramic plates remains challenging because sintering furnaces become the bottleneck once stack assemblies exceed pilot volumes. Even so, hydrogen OEMs project tenfold demand by 2028, positioning ceramics as a secondary growth engine alongside semiconductors and EVs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & processing cost | -1.90% | Global, particularly acute in North America & Europe | Short term (≤ 2 years) |

| Intrinsic brittleness & machining losses | -1.30% | Global, with higher impact in precision applications | Medium term (2-4 years) |

| Critical-minerals supply-chain exposure | -1.10% | Global, with Asia Pacific dependencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intrinsic Brittleness & Machining Losses

Hardness that delivers heat and wear resistance simultaneously increases fracture risk during post-sinter grinding. Yield losses of 20-30% inflate unit costs and lengthen lead times. Fiber-reinforced ceramic-matrix composites mitigate crack propagation but add layer-up and infiltration steps that offset durability gains with higher process complexity. Additive manufacturing offers near-net-shape alternatives, yet material palettes and throughput still lag conventional presses, limiting adoption outside prototyping.

Critical-Minerals Supply-Chain Exposure

Ceramic bodies often blend yttria, scandia, and other rare-earth oxides that are 80% processed in China. Any export curbs would ripple through global delivery schedules. The 2025 U.S. Geological Survey summary warned of intensifying competition for dysprosium and terbium used in high-temperature sintering aids[1]United States Geological Survey, “Critical Mineral Risk Outlook 2025,” usgs.gov . Producers are testing substitute chemistries, but performance deltas persist, particularly in thermal conductivity. Larger firms are stockpiling feedstock, yet carrying costs tie up working capital and complicate inventory turns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Monolithic Reliability versus Composite Agility

Monolithic ceramics retained 46.10% technical ceramics market share in 2025 due to mature press-and-sinter lines that deliver uniform quality at scale. The segment should still post mid-single-digit gains as industrial OEMs retrofit pumps, nozzles, and insulators with alumina bodies that outlast steel equivalents. Composite grades, however, will lift the overall technical ceramics market as their 8.72% CAGR attracts aerospace and defense budgets chasing weight savings above 30% alongside thermal ceilings beyond 1,500 °C. In 2026, the engine hot-section segment alone accounts for a USD 1.18 billion slice of the technical ceramics market size. Processing breakthroughs such as rapid forced-air sintering are collapsing densification steps from hours to minutes, trimming energy cost curves, and narrowing price spreads with monolithics. As these efficiencies propagate, composites are expected to erode monolithic share, but not displace them outright, because automotive and industrial plants still prize predictable shrinkage and low scrap rates.

The coatings niche serves as a transitional pathway: OEMs can spray zirconia or silicon carbide onto legacy metal parts, achieving incremental heat-flux gains without redesigning the entire assembly. This retrofit approach is popular in petrochemical burners and diesel particulate filters where shutdown budgets are tight. Ceramic fibers remain small in tonnage yet influential in insulation markets; aerogel-filled fiber quilts rated to 1,100 °C are seeing uptake in LNG ship cargo holds, another indicator that specialized performance credentials sustain premium pricing in smaller sub-segments.

By Material Class: Oxide Dominance Faces a Non-Oxide Challenge

Oxide families such as alumina, zirconia, and mullite delivered 62.80% of 2025 revenue owing to abundant raw material availability and well-documented process controls. These grades form the baseline for capacitor dielectrics and wear plates across multiple industries. Yet silicon carbide, silicon nitride, and emerging boron carbide non-oxide formulations are booking faster order growth because they combine lower density with thermal conductivities approaching copper. The non-oxide cohort is on a 7.76% trajectory through 2031, expanding the technical ceramics market by servicing frontier devices where oxide glass phases cannot survive. Cost barriers persist, but as fab line yields improve and reject rates fall below 5%, non-oxide price premiums are narrowing. Regulatory fuel-economy mandates and data-center heat-flux escalation both point to sustained long-run tailwinds for these higher-performance grades.

Composite or hybrid material classes merge oxide matrices with non-oxide whiskers or fibers, delivering synergistic toughness and conductivity. Interest is building in lanthanum-doped alumina blends that resist dielectric breakdown at elevated voltages, a property valued by grid-scale solid-state transformer projects. These cross-over formulations validate the thesis that future share battles will not be oxide versus non-oxide but hybrid versus single-phase, adding complexity yet widening solution space.

By End-User Industry: Automotive Anchors, Electronics Accelerates

Automotive OEMs represented 35.60% of 2025 revenue, leveraging bulk purchasing of substrates, sensors, and exhaust after-treatment carriers. Component count per battery-electric vehicle already exceeds 200 ceramic parts, including heaters, fuses, and pressure sensors. Volume scaling in China and Germany shores up this baseline and keeps unit costs competitive. Still, the electrical and electronics vertical will expand at 9.29% annually, lifting its slice of the technical ceramics market size. Semiconductor demand alone would exhaust planned capacity for aluminum nitride boards by 2027 if announced furnaces slip the schedule. Medical devices, though a smaller pocket, yield the highest EBITDA margins at more than 30% because biocompatibility and traceability place natural moats around approved product codes. Energy and power grids round out the portfolio with high-voltage insulator strings and hermetic seal rings for gas-insulated switchgear that must endure lightning impulse tests without flashover.

Aerospace and defense customers, historically dominant in research funding, are pivoting from radomes to turbine shrouds as next-generation propulsion concepts call for service temperatures beyond nickel superalloy limits. Even so, airframe procurement cycles hover near a decade, tempering the near-term volume impact. That said, the single-use defense segment is positioning ceramic armor plates to protect vehicles without weight penalties, bolstering composite throughput.

By Key Application: Insulators Command, Wear Parts Outpace

Insulators and substrates formed 54.20% of applications revenue in 2025, driven by multi-layer ceramic capacitors and printed circuit boards in consumer electronics. Intense miniaturization trends translate into thinner dielectric layers, forcing tighter impurity control and favoring suppliers with high-purity kiln atmospheres. At the same time, industrial automation is elevating cycle rates, inflating abrasive wear on pumps and robots. Consequently, bearings and wear parts are projected to jump at 8.11% CAGR, underpinned by alumina sleeves and silicon carbide mechanical seals capable of lasting 50,000 hours between overhauls.

Thermal management modules remain the linchpin in EV, data-center, and renewable energy hardware, where failure often cascades into system downtime penalties. Ceramic-embedded heat pipes are replacing copper in some radar modules to halve weight while keeping transistor junctions below 125 °C. Meanwhile, bio-implants and dental abutments constitute a lucrative micro-segment where unit prices can exceed USD 4,000 per piece, more than 100 times the average electronic substrate, highlighting the profit diversity across the application spectrum.

Geography Analysis

Asia Pacific dominated the technical ceramics market with 43.40% share in 2025 and is tracking a 7.84% CAGR to 2031. Mainland China hosts the majority of alumina powder calcination and offers cost arbitrage in labor-intensive finishing steps, yet rising electricity tariffs and environmental compliance fees are eroding the historic savings gap. Japan is repositioning toward ultra-clean, high-value substrates that align with national semiconductor revival incentives; Kyocera’s Nagasaki site will lift domestic fine-ceramic output by 10% upon its 2026 start-up. South Korea’s memory-chip epicenter drives demand for low-defect silicon nitride boards, while India is luring EV supply-chain investors with tax holidays in Gujarat and Tamil Nadu. Regional governments are also mapping recycling corridors to capture scrap zirconia and yttria, an initiative that may dilute raw-material import dependencies over the long term.

North America is mature yet innovation-heavy, claiming nearly 30% of global R&D outlays tied to ceramic matrix composites. The United States accounts for the bulk of aerospace turbine and medical implant orders, justifying ISO-class kilns and USP Class VI clean-room protocols that less regulated regions bypass. Saint-Gobain’s USD 40 million catalyst-carrier plant in New York will add 100 jobs and shorten delivery cycles for East-Coast petro-refiners. Canadian mining houses supply bauxite and rare-earth concentrates, but still send most feedstock to Asian refineries. Mexico is emerging as an assembly hub for EV inverters, prompting substrate suppliers to weigh near-shoring steps that sidestep USMCA rules-of-origin tariffs.

Europe claims roughly one-fifth of global revenue and aligns commercial success with sustainability mandates. Germany’s machine-tool builders specify wear-resistant alumina guides that cut lubrication demand by 60%, dovetailing with EU eco-design standards. France and Spain are piloting hydrogen hubs that will soon require thousands of square meters of solid-oxide electrolyzer plates. The region’s REACH chemical-safety framework compels tight traceability, a compliance cost that props up incumbents but slows new venture launches. Post-Brexit United Kingdom policy leans toward advanced materials catapults, aiming to translate university lab breakthroughs into pilot lines within three years, yet significant scale will hinge on export markets, given limited domestic demand.

Competitive Landscape

The industry’s technical barriers and protracted customer qualification cycles establish low competitive intensity. The top five suppliers hold roughly 28% combined revenue, underscoring fragmentation even as scale confers cost leverage. Kyocera, CeramTec, and Saint-Gobain field vertically integrated value chains spanning powder preparation through precision grinding, enabling rapid iteration of customer-specific compositions. Medium-tier players focus on narrow application lanes such as aerospace carbon-silicon-carbon composites or dental zirconia blanks, relying on intellectual-property portfolios and exclusive supply contracts to secure margins. Contract lengths often exceed five years in semiconductor and medical segments because design audits and regulatory filings are expensive and time-consuming.

Strategically, companies are tilting toward forward integration, embedding design-for-manufacture engineers within customer R&D teams to lock in early-stage specifications. Patent filings in flash sintering, additive manufacturing, and oxide-dispersion-strengthened composites rose 12% year over year in 2025, signaling above-average innovation momentum in processing technology. Mergers remain selective; large conglomerates prefer minority stakes in start-ups working on printable ceramic pastes rather than full acquisitions, minimizing integration risk while retaining optionality. Cost inflation in rare-earth feedstocks is also accelerating off-take agreements with mining companies, ensuring direct access to yttria and scandia flows outside Chinese jurisdiction.

Government policy is shaping competition as subsidies for domestic semiconductor supply chains now tie chip-fabrication grants to local substrate sourcing. This stipulation benefits Japan, the United States, and Germany, where established ceramic furnaces can meet purity benchmarks without months of cross-border shipping delays. Conversely, producers heavily exposed to commodity monolithics face margin compression as metal-based substitutes close the cost-performance gap in non-critical applications. Overall, the technical ceramics market rewards sustained R&D outlays and intimate customer partnerships over scale alone.

Technical Ceramics Industry Leaders

3M

CeramTec GmbH

CoorsTek Inc.

Kyocera Corporation

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saint-Gobain Ceramics has announced plans to invest over USD 40 million in a new manufacturing facility in Wheatfield, New York, to enhance ceramic catalyst carrier production. Construction is scheduled to commence later this year, with the project expected to be fully completed by 2028.

- August 2024: Kyocera Corporation has initiated the construction of a new production facility in Nagasaki, Japan. With an investment of approximately USD 469 million, the facility is designed to enhance the manufacturing capacity for fine ceramic components and semiconductor packages. Operations are expected to begin in 2026.

Global Technical Ceramics Market Report Scope

Technical ceramics are robust, heat-resistant, and electrically and thermally insulating. They are synthetic materials created utilizing advanced manufacturing methods to accomplish specialized functions in difficult conditions. Technical ceramics can be monolithic, coated, or composite, formed from oxides, carbides, nitrides, and borides. Technical ceramics are used in cutting tools, wear-resistant parts, electrical insulators, high-temperature furnace components, and biomedical implants.

The market is segmented on the basis of product, end-user industry, and geography. By product, the market is segmented into monolithic ceramics, ceramic matrix composites, ceramic coatings, and other products. By end-user industry, the market is segmented into automotive, electrical and electronics, energy and power, medical, defense and aerospace, and other end-user industries. The report also covers the market size and forecasts for the technical ceramics market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Monolithic Ceramics |

| Ceramic Matrix Composites |

| Ceramic Coatings |

| Other Products |

| Oxide Ceramics |

| Non-Oxide Ceramics |

| Others |

| Electrical and Electronics |

| Automotive |

| Energy and Power |

| Medical |

| Aerospace and Defense |

| Other End-user Industries |

| Insulators and Substrates |

| Thermal Management Components |

| Wear-resistant Parts and Bearings |

| Bio-implants and Dental |

| Armor and Protection |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Monolithic Ceramics | |

| Ceramic Matrix Composites | ||

| Ceramic Coatings | ||

| Other Products | ||

| By Material Class | Oxide Ceramics | |

| Non-Oxide Ceramics | ||

| Others | ||

| By End-user Industry | Electrical and Electronics | |

| Automotive | ||

| Energy and Power | ||

| Medical | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Key Application | Insulators and Substrates | |

| Thermal Management Components | ||

| Wear-resistant Parts and Bearings | ||

| Bio-implants and Dental | ||

| Armor and Protection | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the technical ceramics market in 2026?

The technical ceramics market stands at USD 10.09 billion in 2026 and is projected to reach USD 14.54 billion by 2031, growing at a 7.58% CAGR.

Which segment holds the highest technical ceramics market share?

Monolithic ceramics lead with a 46.10% technical ceramics market share in 2025, thanks to established reliability and scale economies.

What is driving demand in the Asia Pacific region?

Rapid semiconductor fab expansion, surging EV production, and sustained consumer-electronics output underpin Asia Pacific’s 43.40% revenue share and 7.84% growth outlook.

Why are technical ceramics critical for electric vehicles?

Ceramic substrates and heat spreaders manage high thermal loads in 800 V power-train architectures, ensuring silicon carbide modules maintain safe junction temperatures and prolong vehicle life.

Which application is growing fastest through 2031?

Wear-resistant parts and bearings are expected to outpace other uses at an 8.11% CAGR as industrial automation raises component duty cycles and precision requirements.

Page last updated on: