Piezoelectric Ceramics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Piezoelectric Ceramics Market Analysis by Mordor Intelligence

The Piezoelectric Ceramics Market size is projected to expand from USD 1.55 billion in 2025 and USD 1.63 billion in 2026 to USD 2.07 billion by 2031, registering a CAGR of 4.92% between 2026 to 2031. Lead-based composition still dominated in 2025 with an 81.11% share, yet regulatory pressure under the European Commission’s RoHS Directive is steering investments toward lead-free alternatives, which are expected to exceed the 30% threshold by 2032. Asia-Pacific accounted for 52.22% of revenue in 2025 and is growing at a 5.78% CAGR, driven by large-scale production in China and high-precision engineering in Japan. Sensors contributed 34.45% of the 2025 revenue, but energy harvesters and nanogenerators are on the fastest growth trajectory with a 6.17% CAGR, supported by the increasing adoption of IoT and wearable devices. Competitive intensity is rising as established players enhance PZT technology while investing in lead-free research, and newer Chinese firms focus on high-temperature ceramics for specialized applications.

Key Report Takeaways

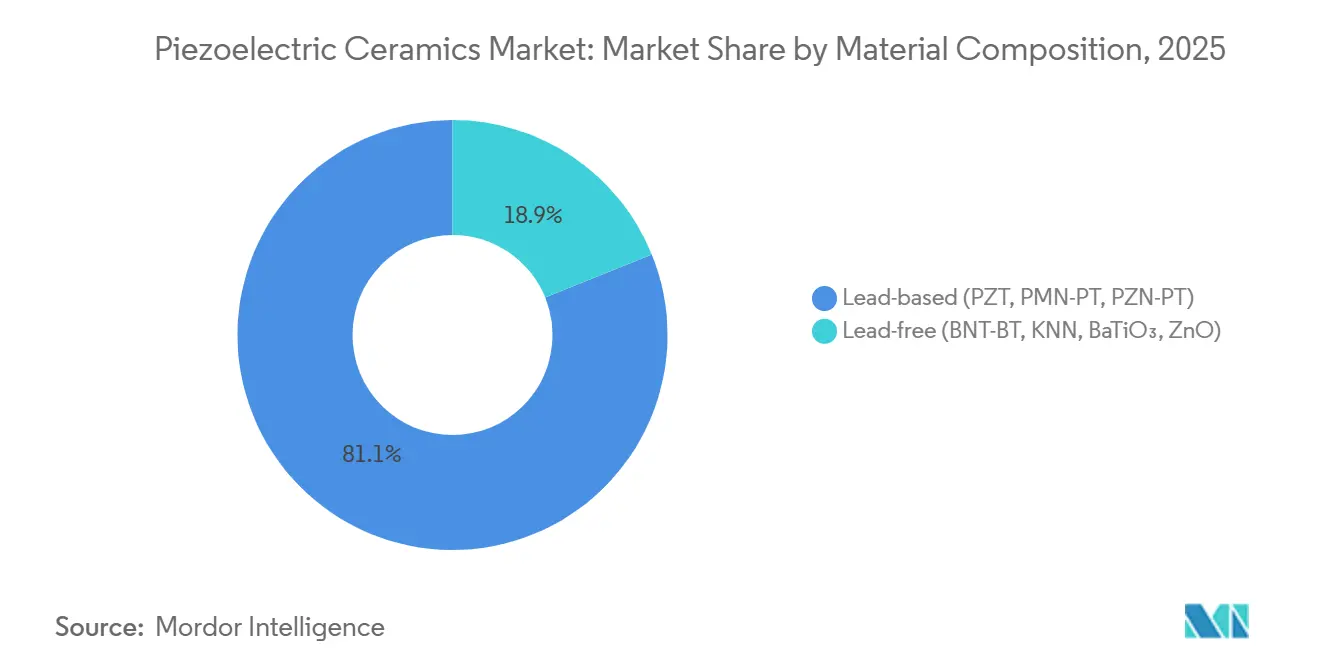

- By material composition, lead-based (PZT, PMN-PT, PZN-PT) composition held 81.11% of the piezoelectric ceramics market share in 2025 and is forecast to expand at a 5.14% CAGR through 2031.

- By application, sensors led with a 34.45% of the piezoelectric ceramics market share in 2025, while energy harvesters and nanogenerators are set to record the fastest 6.17% CAGR through 2031.

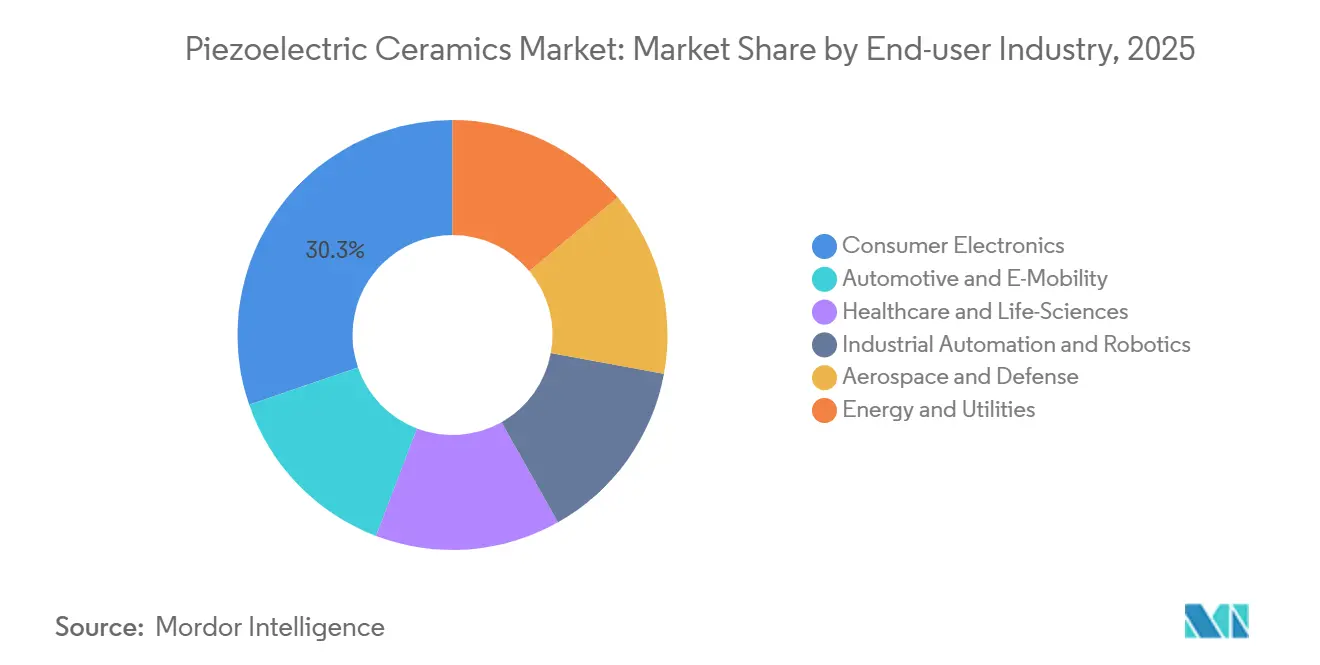

- By end-user industry, consumer electronics commanded 30.26% of the piezoelectric ceramics market share in 2025, and automotive and e-mobility are advancing at a 5.56% CAGR through 2031.

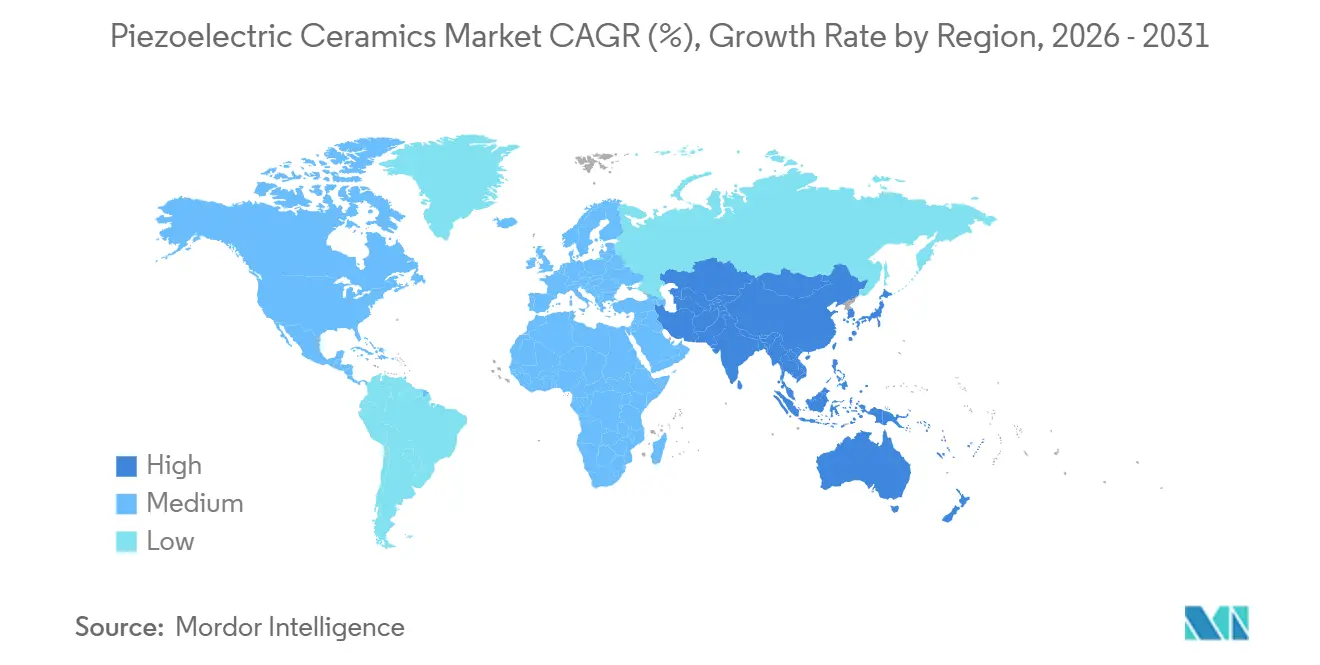

- By geography, Asia-Pacific held 52.22% of the piezoelectric ceramics market share in 2025 and is forecast to expand at a 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Piezoelectric Ceramics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption in medical imaging and therapeutic devices | + 1.2% | Global, with concentration in North America and EU for regulatory-approved devices; APAC for manufacturing scale | Medium term (2-4 years) |

| 5G/6G RF-filter miniaturisation needs high-k piezoceramics | + 1.5% | Global, led by APAC (China, South Korea, Japan) for 5G infrastructure; North America and EU for 6G RandD | Short term (≤ 2 years) |

| Government incentives for local MLCC capacity using PZT dielectrics | + 0.8% | APAC core (China, Japan, South Korea); spillover to North America (CHIPS Act beneficiaries) | Medium term (2-4 years) |

| Quantum transducer RandD drives cryogenic piezoceramic demand | + 0.3% | North America and EU (quantum computing hubs); select APAC research centers | Long term (≥ 4 years) |

| Additive manufacturing enables complex aerospace piezo meta-structures | + 0.6% | North America and EU (aerospace/defense primes); emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption in Medical Imaging and Therapeutic Devices

Piezoelectric ceramics are increasingly replacing older transducer materials in compact ultrasound equipment as hospitals demand portable solutions. Lead-free KNN ceramics have achieved a d33 of 630 pC/N in wearable ultrasound patches, addressing toxicity concerns while maintaining sensitivity. pMUTs manufactured on CMOS lines reduce production costs and simplify signal integration in point-of-care scanners. High-intensity focused ultrasound systems now utilize CeramTec hemispherical discs larger than 150 mm, meeting power-density requirements for tumor ablation. Biocompatibility regulations in the United States and EU are accelerating the transition to lead-free BNT-BT composites, which match PZT power output at lower drive temperatures. As a result, device manufacturers are achieving both performance and compliance benefits, strengthening the piezoelectric ceramics market.

5G/6G RF-Filter Miniaturization Needs High-k Piezoceramics

Millimeter-wave rollouts require AlScN and LiNbO₃ thin films for high-Q BAW and SAW filters that fit inside smartphone modules under 1 mm². AlScN’s kt² exceeding 10% provides a sharper roll-off that handset OEMs need for crowded spectrum allocations. LiNbO₃ LLSAW filters are optimized for sub-6 GHz bands, offering superior power handling compared to quartz. FUJIFILM’s 2025 patent on niobium-doped PZT multilayers achieves a d31 of 389 pC/V below 7 V, aligning with the requirements of low-voltage mobile electronics[1]FUJIFILM Corporation, “Multilayer Piezoelectric Element Patent,” fujifilm.com. The rapid multiplication of frequency bands in 6G R&D ensures sustained demand, supporting long-term growth in the piezoelectric ceramics market.

Government Incentives for Local MLCC Capacity Using PZT Dielectrics

Japan’s METI funding, China’s Made in China 2025 program, and the U.S. CHIPS and Science Act all support domestic MLCC production, indirectly driving investments in PZT powder. The 2025 TDK-Nippon Chemical Industrial joint venture is accelerating barium titanate development to localize upstream materials[2]TDK Corporation, “Corporate News Releases,” tdk.com . PI Ceramic’s EUR 1 million multilayer tape production line has halved sample lead times, demonstrating how subsidy-supported infrastructure accelerates commercialization cycles and expands the piezoelectric ceramics market.

Quantum Transducer R&D Drives Cryogenic Piezoceramic Demand

Superconducting qubits require interfaces with photonics at millikelvin temperatures, increasing interest in LiNbO₃ and SrTiO₃ piezoceramics for low-loss transduction. PI Ceramic supplies actuators qualified to 4 K for UHV labs, providing researchers with ready-to-use components that withstand cryogenic cycling. Although current volumes are limited, government quantum budgets mitigate early procurement risks, embedding piezoelectric ceramics into quantum technology supply chains and paving the way for future market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from PVDF-based piezopolymers | -0.7% | Global, with higher impact in wearable medical devices (North America and EU) and flexible electronics (APAC) | Short term (≤ 2 years) |

| Supply-chain volatility of Nb₂O₅ and Ta₂O₅ for lead-free KNN systems | -0.9% | Global, acute in regions transitioning to lead-free (EU, North America); APAC less affected due to PZT dominance | Medium term (2-4 years) |

| High scrap rates in additive-manufactured piezoceramics scale-up | -0.4% | North America and EU (early adopters of AM for aerospace/defense); emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from PVDF-Based Piezopolymers

PVDF’s flexibility, lightweight properties, and FDA clearance are driving its adoption in wearables, soft robotics, and implantable sensors, challenging rigid ceramics. While its d33 of 20–30 pC/N is significantly lower than PZT, it is sufficient for low-force applications. Cost-effective production methods such as solution casting and electrospinning are encouraging consumer brands to adopt polymer films. This shift toward entry-level applications intensifies price competition, exerting pressure on margins across the piezoelectric ceramics market.

Supply-Chain Volatility of Nb₂O₅ and Ta₂O₅ for Lead-Free KNN Systems

Brazil controls approximately 85% of the global niobium supply, while tantalum is subject to conflict-mineral compliance costs. Spot-price fluctuations exceeding 50% disrupt forward pricing for lead-free producers. Reformulating to alternatives like BaTiO₃ or BLSF variants requires significant time and capital, delaying substitution efforts. While strategic stockpiles benefit large OEMs, smaller firms face cash-flow challenges, limiting the broader adoption of lead-free products in the piezoelectric ceramics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Composition: Lead-Based Formulations Retain Dominance Despite Regulatory Headwinds

Lead-based systems accounted for 81.11% of the piezoelectric ceramics market share in 2025, with this share projected to grow at a 5.14% CAGR through 2031. The market size for lead-based variants is expanding faster than the overall market due to PZT's benchmark-setting d33 values exceeding 600 pC/N. Manufacturers are enhancing performance through dopants like niobium, as demonstrated by FUJIFILM's sub-7 V multilayer actuator patent. Parallel lead-free programs are being developed to mitigate future compliance risks but have yet to challenge PZT's dominance in high-performance applications such as medical imaging and sonar.

BNT-BT discs have shown equivalent acoustic power to PZT in 40 kHz ultrasonic cleaners with reduced heat generation, while KNN soft grades are targeting underwater receivers. Bismuth-layered ferroelectrics, with Curie points above 650 °C, are enabling extreme-temperature applications like oil-well logging. However, each substitution requires requalification in terms of geometry, voltage, and lifetime, which slows adoption but supports a multi-year growth trajectory within the piezoelectric ceramics market.

By Application: Sensors Command Largest Share While Energy Harvesters Accelerate

Sensors contributed 34.45% of the market revenue in 2025, driven by applications such as automotive TPMS, ultrasonic parking modules, and MEMS microphones. The KiVibe triaxial accelerometer, launched in July 2025, enhanced sensitivity to 50 mV/g in a 0.9-gram package, boosting demand in aerospace health monitoring. Although commoditization in smartphones has reduced unit prices, high volumes have sustained sensors as a key segment in the piezoelectric ceramics market.

Energy harvesters and nanogenerators are expected to grow at a 6.17% CAGR through 2031, making them the fastest-growing application segment. Vibration harvesters installed on factory machines and footstep tiles in smart buildings provide a microwatt power supply, eliminating battery maintenance costs. Other applications, including actuators, ultrasonic imaging, and frequency-control devices, leverage specific piezoelectric properties to maintain a diverse application portfolio.

By End-user Industry: Consumer Electronics Lead but Automotive Gains Momentum

Consumer electronics accounted for 30.26% of the market value in 2025, encompassing haptic drivers, autofocus actuators, and ultrasonic fingerprint sensors. TDK's decision in March 2026 to manufacture Apple sensors in the United States highlights onshore production trends, diversifying supply chains and expanding the North American piezoelectric ceramics market.

The automotive and e-mobility segment is projected to grow at a 5.56% CAGR through 2031. Piezoelectric fuel injectors enable nanoliter metering in GDI engines, while battery-monitor sensors track the state of charge in EV packs. The transition to 48-volt architecture supports higher-power actuators for active suspension systems, broadening demand. Other industries, including medical devices, industrial automation, aerospace, and energy, contribute to a multi-industry ecosystem that rewards rapid customization in the piezoelectric ceramics market.

Geography Analysis

Asia-Pacific generated 52.22% of global revenue in 2025 and is projected to grow at a 5.78% CAGR through 2031. China dominates in high-volume powder and low-cost disc production, Japan specializes in multilayer and thin-film precision parts, and South Korea and Taiwan integrate components into smartphones and 5G modules. Murata's USD 233 million Fukui R&D facility, completed in February 2026, focuses on barium titanate and PZT advancements, reinforcing the region's leadership. Indian companies like Sparkler Ceramics are scaling industrial sensor production, while Australian miners drive demand for ruggedized sensors in challenging environments.

North America's demand is driven by aerospace, defense, and medical ultrasound applications. The CHIPS Act's fabrication incentives have indirectly benefited piezoelectric ceramics by sharing cleanroom facilities with semiconductor production. TDK's new U.S. production line for Apple products underscores the appeal of local sourcing amid geopolitical uncertainties. Canada and Mexico contribute through aerospace tooling and automotive sensor assembly, supporting the regional piezoelectric ceramics market.

Europe is led by Germany's automotive and industrial automation sectors and the United Kingdom's aerospace industry. CeramTec is scaling up production of large-format PZT discs for sonar applications, while PI Ceramic's April 2025 advancements in BNT and KNN materials have spurred collaborative projects. Strict EU RoHS regulations are accelerating the adoption of lead-free alternatives faster than in other regions. Additionally, Brazil's offshore energy projects and Saudi Arabia's smart-city initiatives contribute smaller but strategically significant volumes to the global piezoelectric ceramics market.

Competitive Landscape

The market is moderately fragmented. The top five suppliers include Murata, TDK, Kyocera, CeramTec, and CTS Corporation. These companies are pursuing dual strategies to enhance PZT performance while investing in lead-free R&D. TDK's November 2025 joint venture with Nippon Chemical Industrial aims to integrate raw materials and reduce prototyping cycles. PI Ceramic's automated multilayer production line now delivers custom actuators within four weeks, highlighting agility as a competitive advantage in the piezoelectric ceramics market.

Additive manufacturing is emerging as a growth area. Aerospace OEMs are collaborating with niche players to develop 3D-printed lattices for structural health monitoring. Jiangci Electronics has utilized texturing techniques to triple high-temperature performance, targeting oil-well and aerospace applications that command premium pricing.

Future growth opportunities include cryogenic transducers for quantum networks, sensors capable of operating above 250 °C for downhole applications, and implant-grade lead-free materials. FUJIFILM's low-voltage multilayer stack is designed for battery-constrained consumer devices, while CTS's high-Curie BLSF ceramics target extreme environments. The piezoelectric ceramics market is increasingly shifting toward specialization, where application expertise and vertical collaboration are key differentiators.

Piezoelectric Ceramics Industry Leaders

KYOCERA Corporation

Murata Manufacturing Co., Ltd.

TDK Corporation

CTS Corporation

CeramTec GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: PI Ceramic GmbH achieved a significant breakthrough in the production of lead-free piezoceramic components. The bismuth sodium titanate (BNT) and potassium sodium niobate (KNN) material systems provided performance comparable to the traditional lead zirconate titanate (PZT) system in certain applications.

- July 2024: CTS Corporation launched a portfolio of nine lead-free piezoceramic materials, including four new formulations under the LF Series, designed to improve environmental sustainability in electronics. These materials, based on KNN and NBT-BT, provided high-performance, RoHS-compliant alternatives to lead-based (PZT) ceramics for applications in industries such as medical devices, automotive, and industrial sensors.

Global Piezoelectric Ceramics Market Report Scope

Piezoelectric ceramics are engineered ferroelectric materials designed to convert mechanical stress into electrical energy (direct effect) and electrical energy into mechanical stress (inverse effect). These materials are commonly utilized in sensors, actuators, and transducers. Prominent examples include Lead Zirconate Titanate (PZT) and Barium Titanate, which are extensively used in applications such as ultrasonic cleaning, medical imaging, and precision motor controls.

The Piezoelectric Ceramics market is segmented into material composition, application, end-user industry, and geography. By material composition, the market is segmented into lead-based (PZT, PMN-PT, PZN-PT) and lead-free (BNT-BT, KNN, BaTiO₃, ZnO). By application, the market is segmented into sensors (pressure, ultrasonic, MEMS microphones), actuators (fuel injectors, micro-positioners), energy harvesters and nanogenerators, ultrasonic imaging and cleaning, and frequency control and timing (SAW/BAW resonators). By end-user industry, the market is segmented into consumer electronics, automotive and e-mobility, healthcare and life sciences, industrial automation and robotics, aerospace and defense, and energy and utilities. The report also covers the market size and forecasts for piezoelectric ceramics in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Lead-based (PZT, PMN-PT, PZN-PT) |

| Lead-free (BNT-BT, KNN, BaTiO₃, ZnO) |

| Sensors (pressure, ultrasonic, MEMS mics) |

| Actuators (fuel injectors, micro-positioners) |

| Energy Harvesters and Nanogenerators |

| Ultrasonic Imaging and Cleaning |

| Frequency Control and Timing (SAW/BAW resonators) |

| Consumer Electronics |

| Automotive and E-Mobility |

| Healthcare and Life-Sciences |

| Industrial Automation and Robotics |

| Aerospace and Defense |

| Energy and Utilities |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| NORDIC Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Composition | Lead-based (PZT, PMN-PT, PZN-PT) | |

| Lead-free (BNT-BT, KNN, BaTiO₃, ZnO) | ||

| By Application | Sensors (pressure, ultrasonic, MEMS mics) | |

| Actuators (fuel injectors, micro-positioners) | ||

| Energy Harvesters and Nanogenerators | ||

| Ultrasonic Imaging and Cleaning | ||

| Frequency Control and Timing (SAW/BAW resonators) | ||

| By End-user Industry | Consumer Electronics | |

| Automotive and E-Mobility | ||

| Healthcare and Life-Sciences | ||

| Industrial Automation and Robotics | ||

| Aerospace and Defense | ||

| Energy and Utilities | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Australia | ||

| NORDIC Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the piezoelectric ceramics market?

The piezoelectric ceramics market stands at USD 1.63 million in 2026 and is projected to reach USD 2.07 million by 2031.

Which material composition leads revenue in 2025?

Lead-based composition held 81.11% of revenue in 2025.

What application segment is growing the fastest through 2031?

Energy harvesters and nanogenerators are projected to grow at a 6.17% CAGR through 2031 as battery-free IoT nodes scale.

Which region contributes the most revenue?

Asia-Pacific generated 52.22% of global sales in 2025 and remains the growth engine with a 5.78% CAGR through 2031.

Page last updated on: