Transparent Ceramics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

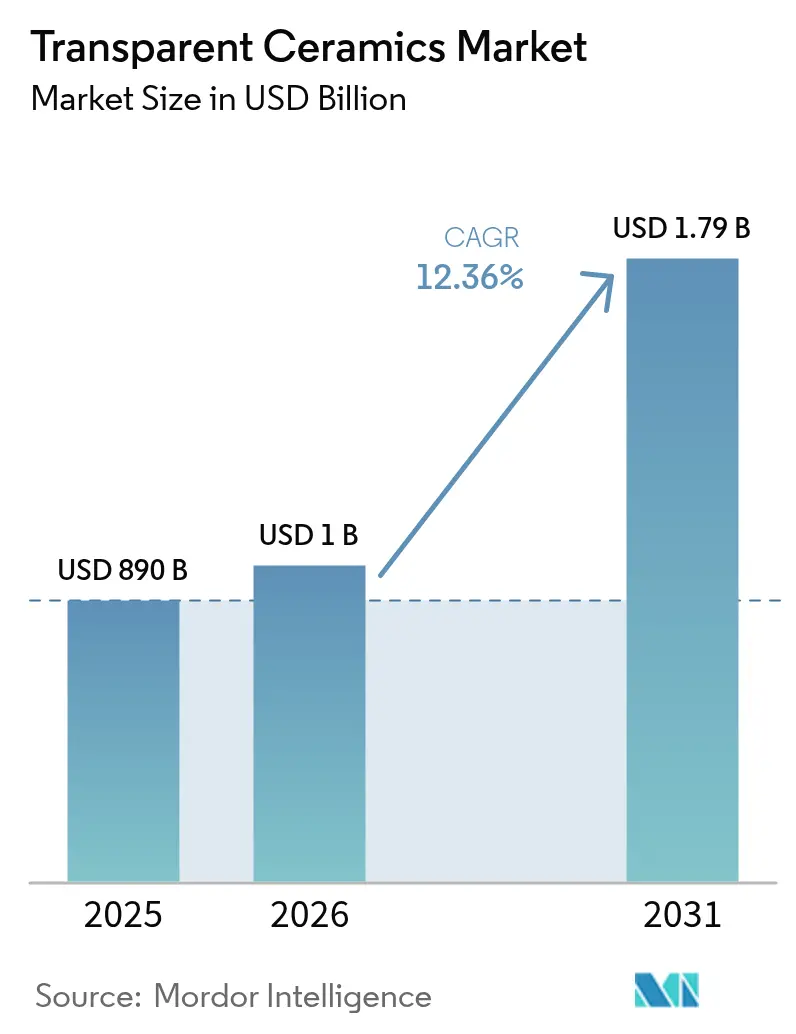

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 12.36% CAGR |

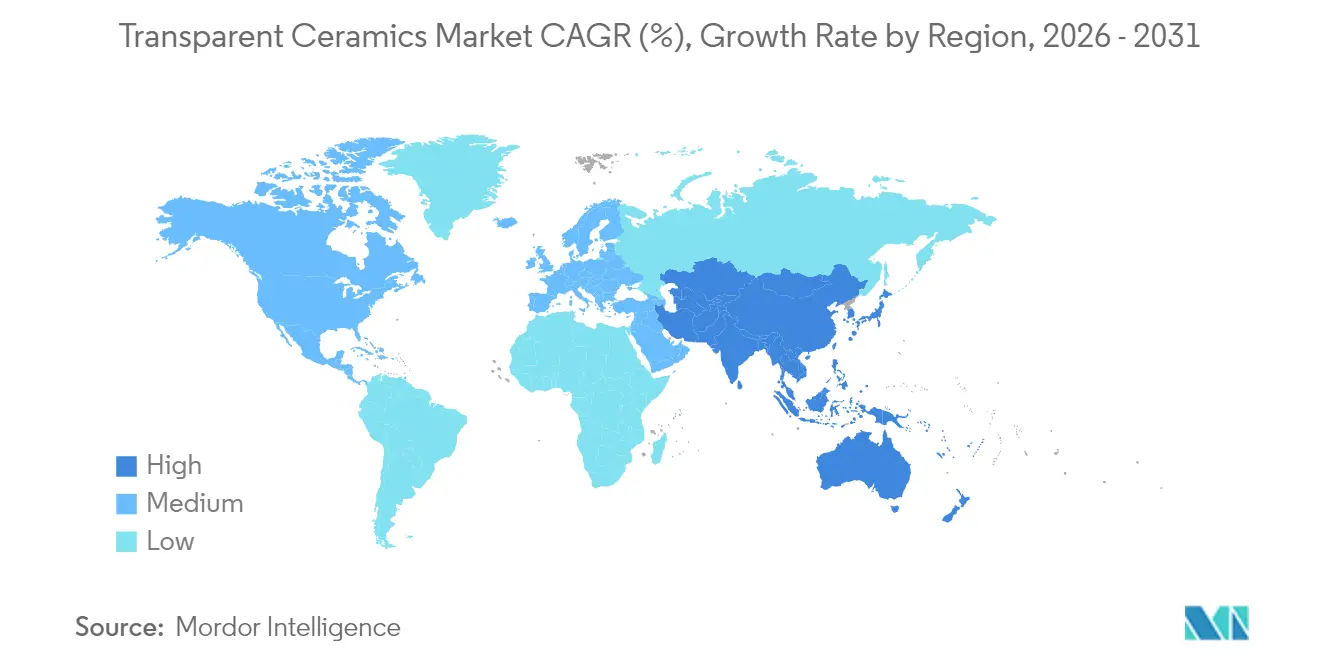

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transparent Ceramics Market Analysis by Mordor Intelligence

The Transparent Ceramics Market size was valued at USD 890 million in 2025 and estimated to grow from USD 1 billion in 2026 to reach USD 1.79 billion by 2031, at a CAGR of 12.36% during the forecast period (2026-2031). Demand for fusion-grade laser optics, hypersonic vehicle domes, and next-generation optoelectronic components continues to redefine performance baselines, spurring investment in manufacturing technologies that shrink defect rates and expand throughput. Asia Pacific, supported by semiconductor and aerospace buildouts in China and Japan, contributes the largest revenue block and simultaneously registers the fastest regional growth, reflecting scale economics and coordinated industrial policy. Crystalline-structure ceramics dominate current shipments, especially in military optics, yet cost-advantaged glass-ceramic variants are closing ground as consumer electronics brands pivot to scratch-resistant, high-clarity covers. Material leadership resides with sapphire, but aluminum oxynitride’s ballistic performance is allowing it to seize design-in wins for next-generation infrared (IR) windows on hypersonic platforms. The competitive field, while moderately consolidated, is tilting toward vertical integration as players race to secure rare-earth inputs and proprietary sintering know-how, lowering unit costs and unlocking capacity for high-volume sectors such as dental implants and LED lighting.

Key Report Takeaways

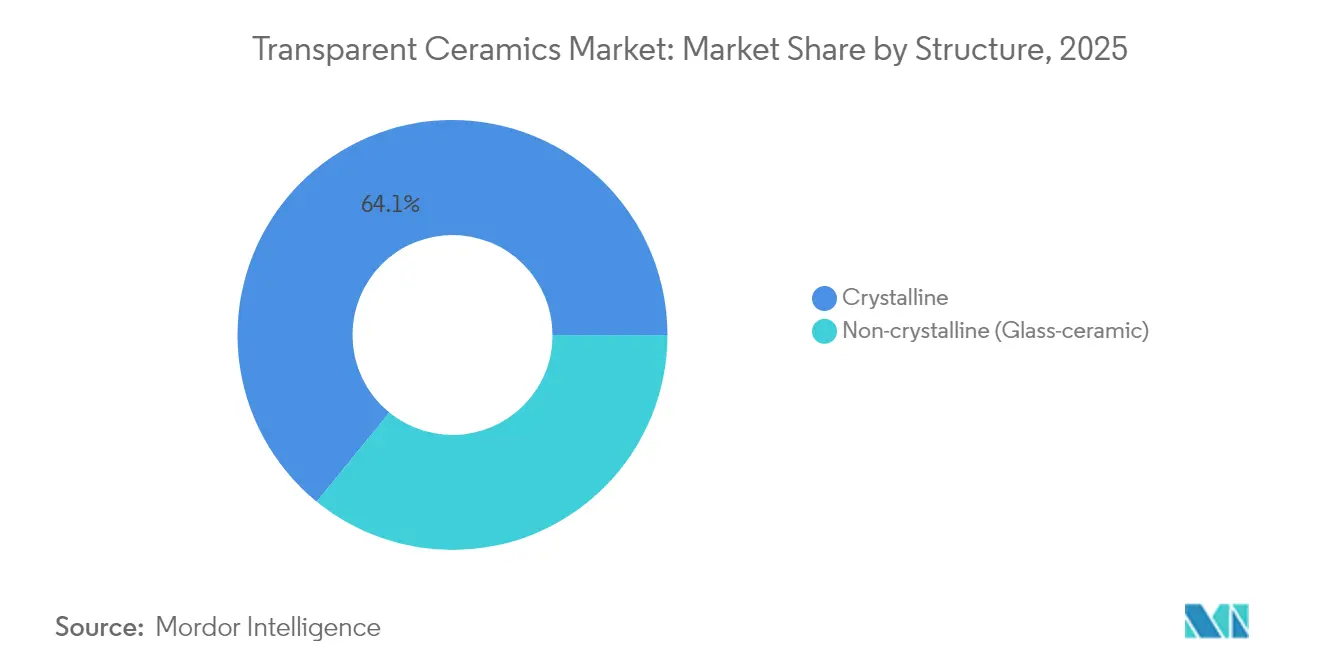

- By structure, crystalline ceramics held 64.12% of the 2025 transparent ceramics market share, whereas non-crystalline formats are forecast to expand at a 12.58% CAGR through 2031.

- By material, sapphire captured 42.74% share of the transparent ceramics market size in 2025; aluminum oxynitride is set to grow at 12.66% CAGR to 2031.

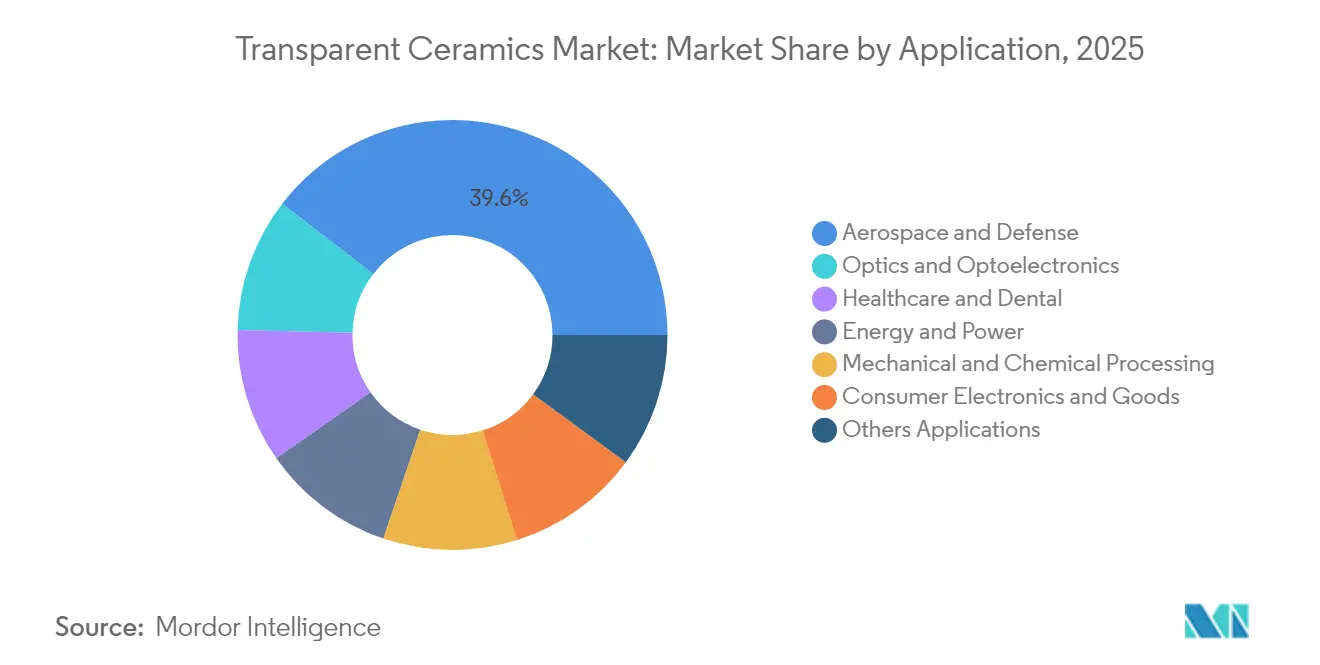

- By application, aerospace & defense accounted for 39.55% of the transparent ceramics market share in 2025, while healthcare and dental are advancing at 13.28% CAGR to 2031.

- By region, Asia Pacific led with 56.12% revenue share in 2025; the same region is forecast to accelerate at a 13.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transparent Ceramics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating usage in optics & optoelectronics | +3.20% | Global, with concentration in Asia Pacific and North America | Medium term (2-4 years) |

| Growing demand from aerospace & defense | +2.80% | North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| Advanced Ceramics Increasingly Replacing Plastics and Metals | +2.10% | Global | Medium term (2-4 years) |

| Fusion-grade high-power ceramic lasers | +1.90% | North America, Europe | Long term (≥ 4 years) |

| Rising use of transparent ceramics in IR domes for hypersonic vehicles | +1.60% | North America, Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Usage in Optics & Optoelectronics

Laser-driven manufacturing, lidar, and photonic-integrated circuits are fueling record off-take for high-purity, low-defect transparent ceramics. Titanium:sapphire-on-insulator prototypes have delivered compact layouts that cut system footprints while boosting power density, signaling commercial feasibility for wafer-level laser arrays. Ce-doped garnet ceramics now demonstrate luminance saturation thresholds of 65 W mm-2, offering durable, thermally stable alternatives to single-crystal gain media in LED backlights and industrial lasers. The transparent ceramics market is, therefore, intertwined with broadband communications, where miniaturization pressures amplify the value of materials that can survive intense photon flux and elevated junction temperatures.

Growing Demand from Aerospace & Defense

Transparent ceramics meet the dual mandate of optical transmission and high-temperature resilience imposed by supersonic aircraft, missile seekers, and satellite sensor windows. Porous Si₃N₄ radomes have reached 56% porosity while preserving mechanical integrity, trimming overall weight for long-range interceptors[1]Tsinghua University Press, “Porous Si₃N₄ Radomes,” tup.tsinghua.edu.cn . Transparent domes on hypersonic glide bodies must tolerate 2,000 °C skin temperatures; AlON and spinel exceed such thresholds while resisting thermal shock. U.S. federal roadmaps name these ceramics as cornerstone materials for resilient energy weapon optics and directed-energy systems[2]U.S. Department of Energy, “Harsh Environment Materials Roadmap,” energy.gov . Substitution away from germanium windows further elevates the transparent ceramics market, alleviating strategic mineral supply risk through chalcogenide glass derivatives that match sensor bandwidth needs.

Advanced Ceramics Increasingly Replacing Plastics and Metals

Automakers, consumer-electronics brands, and industrial OEMs are phasing in ceramic parts where polymers warp or metals corrode. Transparent ceramics resist thermal cycling, harsh chemicals, and abrasion, making them suitable for EV battery seals, smartphone camera covers, and high-visibility machinery guards. Experiments with titania-based nano screens promise wall-scale displays at one-tenth of OLED cost, translating to large-volume glass-ceramic substrates in next-generation public information panels. Additive-manufactured alumina parts cut tool-change downtime in semiconductor etchers, replacing coated metals that suffer plasma erosion.

Fusion-Grade High-Power Ceramic Lasers

Commercial-fusion timelines are compressing, pivoting the transparent ceramics industry toward specialty optics that endure megajoule pulse regimes. Laser World of Photonics 2025 showcased supply-chain gaps in diode pump arrays and beam-combiner windows, with ceramic slabs offering higher damage thresholds than glass lenslets. Fluoride-based transparent ceramics have achieved visible lasing at 605 nm under room temperature, hinting at cost-effective beamline components for inertial-confinement reactors. Research into ultra-high-temperature ceramics processed via laser melting has yielded compositions that withstand 4,000 °C, positioning them for first-wall panels and diagnostic ports in tokamak environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost | -2.40% | Global | Short term (≤ 2 years) |

| Manufacturing complexity & yield losses | -1.80% | Asia Pacific, North America | Medium term (2-4 years) |

| Sustainability issues in rare-earth mining | -1.20% | Global, particularly China and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost

Transparent ceramics require high-purity feedstocks and multi-stage sintering profiles that push furnace dwell times and electricity usage well above standard tile or structural ceramics. Two-step sintering raises density but demands precision thermal ramps, while diamond-wheel finishing of sapphire parts adds capex for high-RPM spindles and coolant systems. Industry carbon-footprint scrutiny is accelerating shifts to green hydrogen kilns, but near-term conversion expenses weigh on margins.

Manufacturing Complexity & Yield Losses

Yield attrition stems from micro-porosity, inclusions, and residual stress. Spark plasma sintering can collapse these defects, yet the technique calls for bespoke dies and tight vacuum control that inflate maintenance overheads. Laser additive routes sometimes cause cellular-solid microstructures harboring dislocations that undermine optical throughput[3]Journal of the American Ceramic Society, “Microstructures in Laser-Sintered Alumina,” ceramics.org . Oxygen-vacancy management in indium gallium zinc oxide electrodes illustrates the broader hurdle: unmitigated vacancies shift carrier mobility, compromising electro-optic response. Thermal gradients during laser polishing of quartz pieces can spike to 940 °C in milliseconds, necessitating intricate scan-path algorithms to stave off craze lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Structure: Crystalline Dominance Drives Defense Applications

Crystalline variants secured 64.12% transparent ceramics market share in 2025, validated by consistently higher transmission in the 0.3–5 μm band and compressive strengths above 2 GPa. Fine-grain sapphire domes and YAG laser slabs illustrate the segment’s versatility across radomes and solid-state lasers. Non-crystalline glass-ceramics, conversely, capitalized on agile melt-casting lines and lower scrap rates, capturing handset lens covers and smart-watch backplates. Their 12.58% CAGR underscores demand elasticity in price-sensitive consumer channels.

Cordierite glass-ceramics that combine 82.3% transmittance with sub-2.6 ppm °C-1 thermal expansion pave the way for monolithic mobile screens that forego polymer lamination. Meanwhile, advanced nucleant systems—P₂O₅ + ZrO₂ + TiO₂—shift crystallization to the bulk, enhancing mechanical tensile strength without sacrificing clarity. Spark plasma sintering reduces processing windows from hours to minutes, halving energy input and shrinking grain boundaries to suppress scattering.

By Material: Sapphire Leadership Challenged by AlON Innovation

Sapphire’s 42.74% grip on revenues owes to mature Kyropoulos and edge-defined film-fed growth furnaces that scale boules up to 300 kg, lowering per-substrate cost for LED wafers and smartphone optics. Aluminum oxynitride, however, is registering 12.66% CAGR as missile OEMs specify lighter, tougher IR windows. Surmet’s ALON blanks show flexural strengths near 400 MPa, a substantial margin over spinel. Yttrium aluminum garnet still anchors DPSS laser cavities, while spinel (MgAl₂O₄) wins ballistic-window programs.

Alpha HPA’s commissioning of 5N-purity sapphire growth units signals the ongoing expansion of legacy material supply. At the same time, exploratory transparent AlN ceramics emerge from plasma-assisted deposition, offering 320 W m-1 K-1 thermal conductivity, which could disrupt high-flux lidar arrays. Yttria-stabilized zirconia is surging in zirconia-based dental crowns, blending translucency with load-bearing capacity. Rare-earth-doped garnets are penetrating micro-LED displays, where pulse width modulation demands rapid phosphor decay.

By Application: Healthcare Growth Accelerates Beyond Aerospace Dominance

Aerospace & defense contributed 39.55% of sector turnover in 2025, valued at more than USD 352 million, anchored by seeker windows, armor-grade viewports, and laser weapon optics. The transparent ceramics market size addressed by aerospace is set for high-single-digit CAGR as hypersonic and counter-UAS programs proliferate. Healthcare and dental, however, outpace all segments at 13.28% CAGR; transparent zirconia implants cut peri-implantitis risk while meeting aesthetic expectations.

Ceramic femoral heads exhibit 1439 ± 62 HV1 hardness, translating to reduced wear debris and longer prosthesis lifespans. Intraoral scanners now integrate optical blocks cast from spinel to withstand autoclave cycles. Consumer electronics absorb volumes of scratch-immune sapphire lenses, with multi-camera phone architectures magnifying unit demand. Energy applications are taking shape, where spectral-conversion ceramic layers up-shift photons, enhancing c-Si solar output by 7–9%.

Geography Analysis

Asia Pacific controlled 56.12% of 2025 sales, buoyed by entrenched sapphire boules in Hunan and wide-aperture AlON plates in Nagoya. Government stimulus for local semiconductor etching and display fabs furnishes anchor demand, while export-oriented defense conglomerates in China adopt spinel domes for next-generation ISR drones. By 2031, the region is poised to generate significant incremental revenue, growing at a rate of 13.95% CAGR. South Korea’s nano transparent screen initiative cuts per-inch costs to one-tenth of OLED, broadening addressable display footprints and deepening local supply chains.

North America remains the technology vanguard, leveraging DARPA and DoE grants to demonstrate directed-energy laser couplers and fusion-grade optics. LightPath Technologies is substituting BDNL4 chalcogenide glass for germanium, insulating the defense base from geopolitical risk. Mexico’s electronics maquiladoras integrate glass-ceramic heat spreaders into power modules, signaling outward regional diffusion of advanced materials.

Europe positions itself on value-added, low-carbon production. SCHOTT’s EUR 450 million capital program includes a hydrogen-fired float line that delivered its first CO₂-neutral glass in 2024, validating feasibility for ceramic sintering kilns. Germany’s Ceramic Composites network targets a doubling of oxide-fiber throughput by 2025, critical for ceramic-matrix composites in aerospace turbines. The Middle East and Africa record nascent but strategic uptake, especially in concentrated solar power fields where dust-resistant, IR-transparent shields elongate heliostat lifetimes.

Competitive Landscape

The transparent ceramics market features a moderate degree of consolidation: the top five producers—SCHOTT AG, CoorsTek Inc., Surmet Corporation, CeramTec GmbH, and AGC Inc.—collectively hold roughly 53% of global turnover. These incumbents intensify vertical integration, acquiring powder-feedstock firms and kiln-component suppliers to lock in price stability and proprietary grain-growth modifiers. CoorsTek has paired spark plasma sintering with high-purity alumina feed to lift yields by 18%, while Surmet scales 40-inch ALON blanks for next-generation airborne sensors.

New entrants in China and South Korea exploit scale economies and domestic rare-earth deposits, narrowing cost gaps in sapphire wafers and glass-ceramic lens covers. IP portfolios, rather than capacity alone, are becoming decisive: SCHOTT’s zero-lead alumino-silicate filed patents on hydrogen-assisted melt pools, granting an ecological differentiator. Strategic alliances abound; Kyocera’s 2024 accord with Kyoto Sangyo University transfers cordierite mirror recipes into telescope OEMs, ensuring application-focused feedback loops.

Competitive intensity also rises from cross-industry incursions. LED epitaxy giants begin backward integration into sapphire growth, while defense primes establish joint ventures for in-house AlON finishing. Supply security for yttrium and terbium oxides influences procurement decisions, giving miners with ESG-compliant extraction an upstream bargaining chip.

Transparent Ceramics Industry Leaders

Surmet Corporation

CoorsTek Inc.

SCHOTT AG

CeramTec GmbH

AGC Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Fraunhofer IKTS has opened Europe’s first R&D center for transparent ceramics in Hermsdorf, Thuringia. The institute aims to collaborate with industrial partners to develop innovative and cost-effective applications.

- November 2024: CeramTech showcased its advanced portfolio of "high-performance ceramics" at electronica 2024, emphasizing its applications in transparent ceramics. This focus is expected to drive innovation and growth in the transparent ceramic market by fostering technological advancements and expanding its industrial applications.

Global Transparent Ceramics Market Report Scope

The transparent ceramics market report includes:

| Crystalline |

| Non-crystalline (Glass-ceramic) |

| Sapphire (Al₂O₃) |

| Yttrium Aluminum Garnet (YAG) |

| Aluminum Oxynitride (AlON) |

| Spinel (MgAl₂O₄) |

| Yttria-stabilized Zirconia (YSZ) |

| Other Advanced Materials |

| Optics and Optoelectronics |

| Aerospace and Defense |

| Mechanical and Chemical Processing |

| Healthcare and Dental |

| Consumer Electronics and Goods |

| Energy and Power |

| Others Applications |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| ASEAN countries | |

| Rest of Asia Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| UAE | |

| South Africa | |

| Egypyt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Structure | Crystalline | |

| Non-crystalline (Glass-ceramic) | ||

| By Material | Sapphire (Al₂O₃) | |

| Yttrium Aluminum Garnet (YAG) | ||

| Aluminum Oxynitride (AlON) | ||

| Spinel (MgAl₂O₄) | ||

| Yttria-stabilized Zirconia (YSZ) | ||

| Other Advanced Materials | ||

| By Application | Optics and Optoelectronics | |

| Aerospace and Defense | ||

| Mechanical and Chemical Processing | ||

| Healthcare and Dental | ||

| Consumer Electronics and Goods | ||

| Energy and Power | ||

| Others Applications | ||

| By Geography | Asia Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN countries | ||

| Rest of Asia Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| UAE | ||

| South Africa | ||

| Egypyt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current transparent ceramics market size and growth outlook?

The transparent ceramics market size stands at USD 1 billion in 2026 and is projected to reach USD 1.79 billion by 2031, advancing at a 12.36% CAGR driven by aerospace, defense, and optoelectronics demand.

Which region dominates transparent ceramics demand?

Asia Pacific leads with 56.12% revenue share in 2025 and is also the fastest-growing region, expanding at 13.95% CAGR through 2031 on the back of semiconductor and aerospace investments.

Why is aluminum oxynitride attracting attention?

Aluminum oxynitride combines optical transparency with ballistic resistance, enabling lighter IR domes for hypersonic vehicles and achieving the fastest material-segment CAGR of 12.66%.

How are transparent ceramics penetrating healthcare?

Transparent zirconia implants and dental crowns exhibit high hardness and biocompatibility, propelling healthcare applications at a 13.28% CAGR, the quickest among end-use segments.

Which companies hold key positions in the transparent ceramics industry?

SCHOTT AG, CoorsTek Inc., Surmet Corporation, CeramTec GmbH, and AGC Inc. constitute the core leadership group, jointly accounting for about 53% of global revenue.

Page last updated on: