Ceramic Foam Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

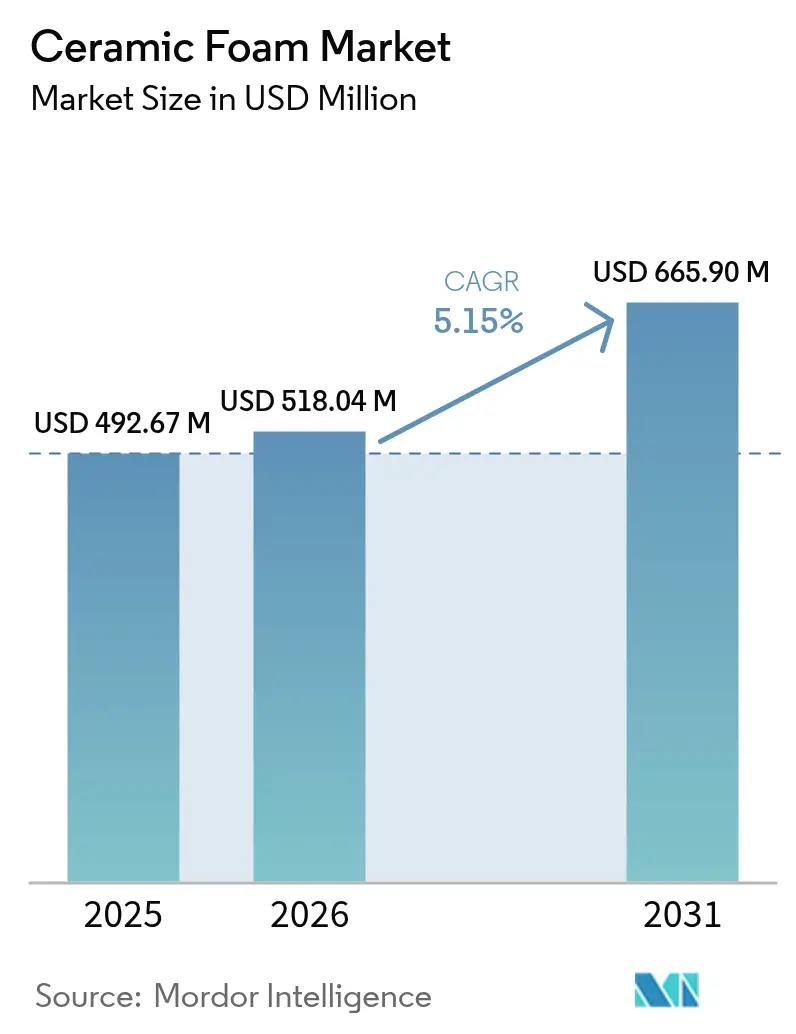

| Market Size (2026) | USD 518.04 Million |

| Market Size (2031) | USD 665.9 Million |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

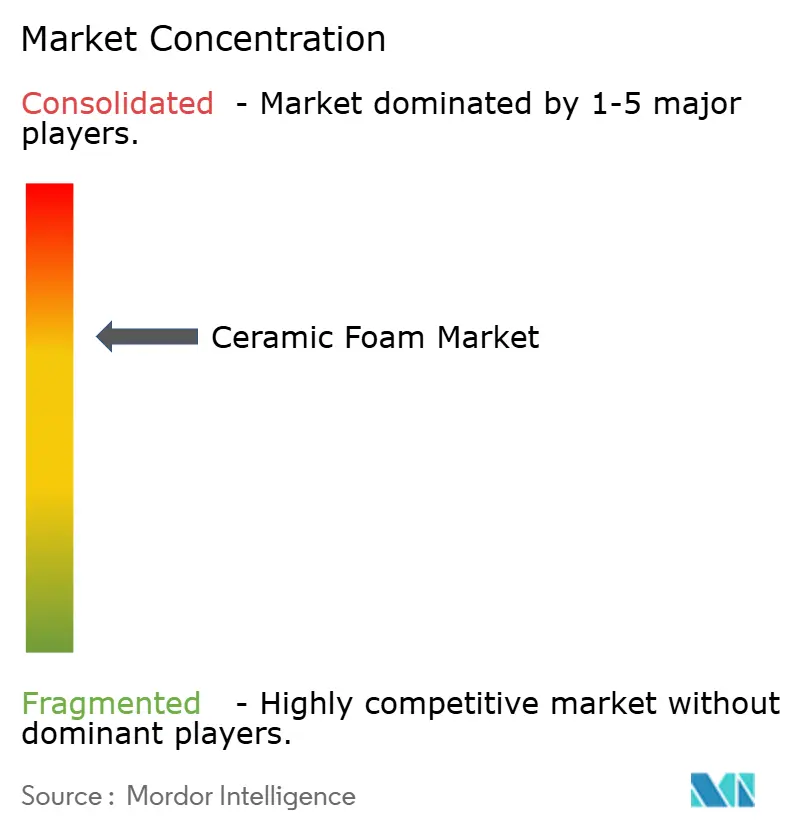

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceramic Foam Market Analysis by Mordor Intelligence

Ceramic Foam market size in 2026 is estimated at USD 518.04 million, growing from 2025 value of USD 492.67 million with 2031 projections showing USD 665.9 million, growing at 5.15% CAGR over 2026-2031. Demand is accelerating as ceramic foam delivers high-temperature stability, chemical resistance and well-controlled porosity that outperform many legacy refractory and filtration media. Rapid growth in electric-vehicle casting hubs, hydrogen production facilities and circular-economy steel mini-mills is widening the customer base. Advanced replica processes retain cost advantages in high-volume production, while additive manufacturing opens profitable niches for complex open-cell geometries. Producers also see new insulation opportunities as North American and European zero-energy building codes tighten. Meanwhile, raw-material price volatility and brittleness challenges in fully automated foundries temper near-term margins, prompting suppliers to pursue material toughening and supply-chain hedging strategies.

Key Report Takeaways

- By material type, silicon carbide held 44.74% of the ceramic foam market share in 2025, while magnesium aluminate spinel and other advanced composites are forecast to expand at a 7.41% CAGR to 2031.

- By manufacturing process, the replica/polymer sponge route led with 66.58% revenue share in 2025, whereas additive manufacturing is projected to register the highest 7.55% CAGR through 2031.

- By application, molten metal filtration accounted for 39.05% of the ceramic foam market size in 2025 and catalyst support is advancing at an 7.72% CAGR to 2031.

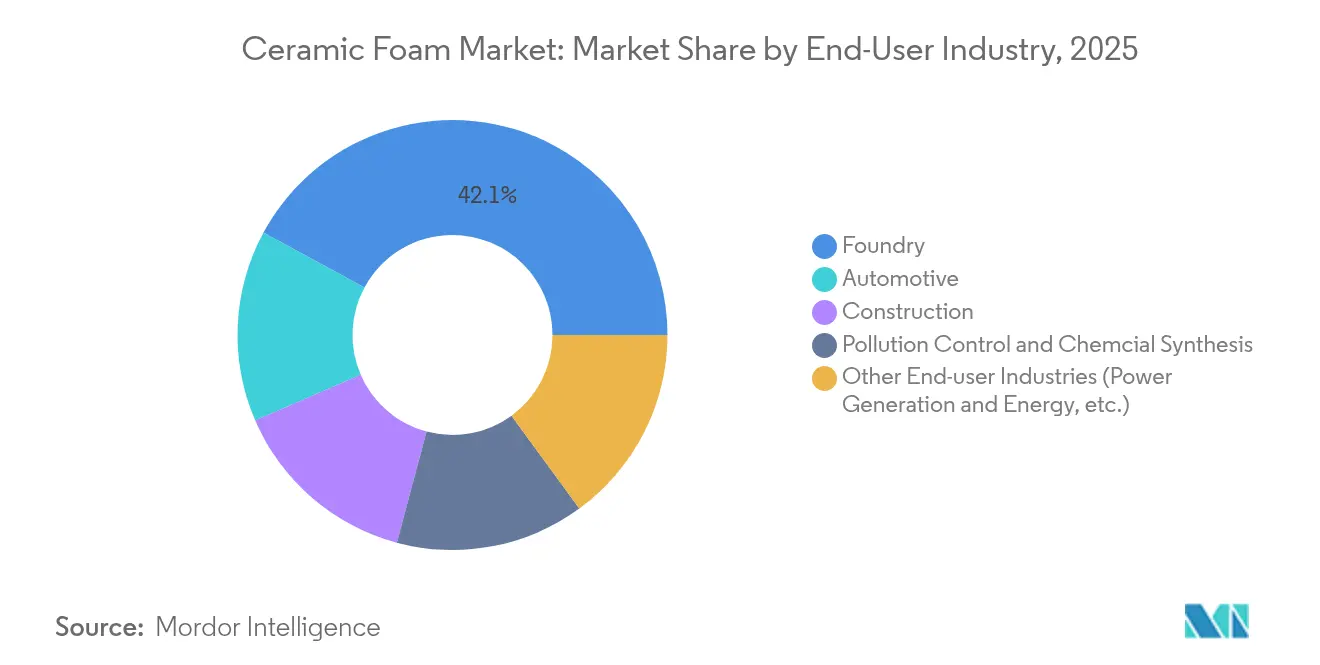

- By end-user industry, foundries dominated with 42.10% share of the ceramic foam market size in 2025; power generation and other emerging energy applications are expected to post an 7.63% CAGR between 2026 and 2031.

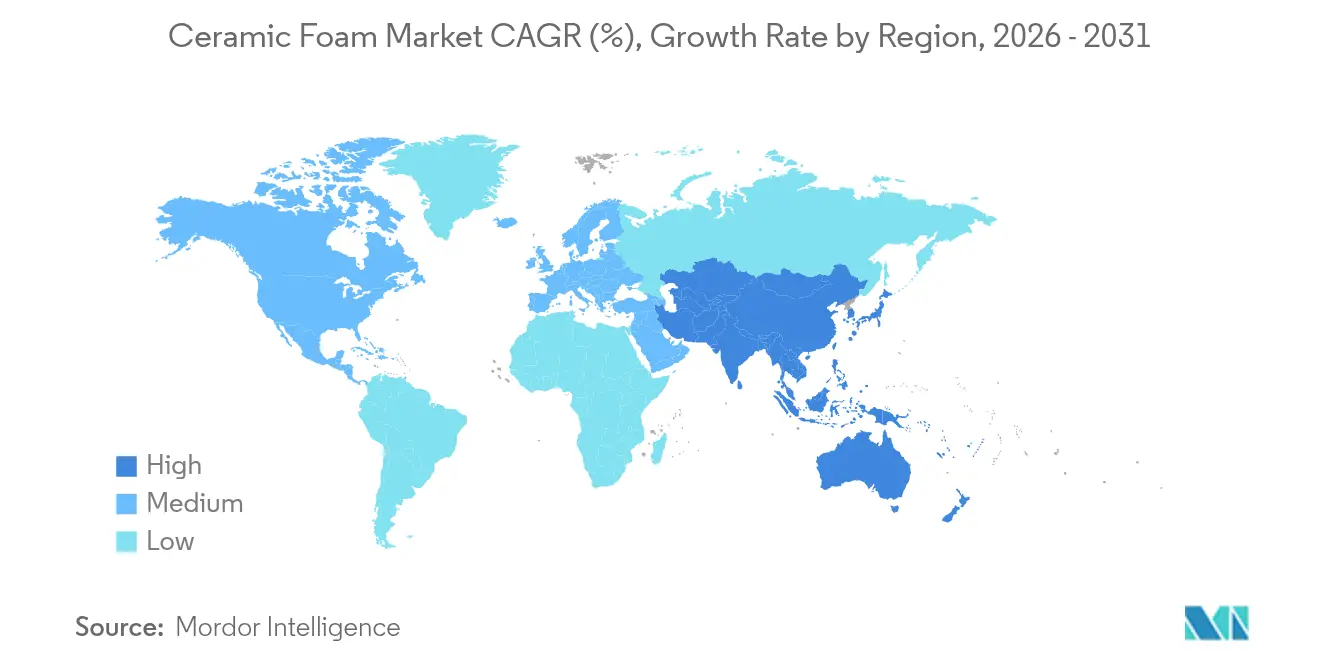

- By geography, Asia-Pacific contributed 46.25% revenue in 2025 and is set to grow at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ceramic Foam Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for low-emission molten metal filtration in EV casting hubs | +1.20% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Rapid expansion of hydrogen production requiring high-temperature catalyst supports | +0.90% | Global, early gains in Europe and North America | Long term (≥ 4 years) |

| Additive manufacturing enabling complex, cost-efficient open-cell foam geometries | +0.80% | North America and EU, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Circular-economy push for recyclable refractory linings in steel mini-mills | +0.60% | Global, concentrated in major steel regions | Medium term (2-4 years) |

| Government incentives for zero-energy buildings boosting ceramic-foam insulation panels | +0.40% | North America & EU, selective Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging demand for low-emission molten metal filtration in EV casting hubs

Electric-vehicle platforms use large aluminum structural castings that require exceptionally clean melts to meet conductivity and fatigue targets. Ceramic foam filters now enable sub-10 ppm inclusion levels in battery housings and motor casings. Vesuvius reports 40% higher uptake of SEDEX silicon-carbide filters in EV-dedicated foundries compared with conventional automotive lines[1]Vesuvius, “SEDEX Filters for Battery Casting,” vesuvius.com . Tesla’s Shanghai operations and similar Asian facilities specify silicon-carbide foams for high-pressure die casting, driving regional volume. These specifications raise throughput and repeatability criteria that favor robust open-cell geometries produced via improved replica methods. Supply-chain localization efforts in Asia-Pacific further cement regional dominance of the ceramic foam market.

Rapid expansion of hydrogen production requiring high-temperature catalyst supports

Global electrolyzer and steam-reform expansion demands refractory carriers that withstand cyclic 600-900 °C operation in corrosive atmospheres. The Ceramics UK consortium validated 100% hydrogen-fired kilns, confirming ceramic foam suitability for next-generation energy systems. Saint-Gobain is investing USD 40 million in New York to scale catalyst-carrier output, highlighting North American momentum[2]Saint-Gobain, “Saint-Gobain Invests USD 40 Million in Catalyst Carrier Plant,” saint-gobain.com . Cordierite monoliths reinforced with ceramic foam achieve optimal selectivity at 800 °C, extending service intervals for reformers and solid-oxide fuel cells. As more regions publish national hydrogen roadmaps, catalyst support orders provide a durable growth pathway for the ceramic foam market.

Additive manufacturing enabling complex, cost-efficient open-cell foam geometries

Three-dimensional printers using direct-ink writing and selective-laser-sintering now fabricate foams with graded porosity and tailored strut alignment. Parts reach 95% porosity yet retain flexural strength through strategic material deposition. These geometries improve mass-transfer coefficients in catalyst beds and raise filtration efficiency without raising pressure drop. Additive routes shorten prototyping cycles to days, suiting low-volume aerospace and research contracts. As printer throughput rises and powder costs fall, additive manufacturing is expected to capture specialized sub-segments of the ceramic foam market at premium margins.

Circular-economy push for recyclable refractory linings in steel mini-mills

Electric-arc-furnace steel capacity growth requires linings that survive rapid thermal cycling while supporting scrap-based, low-carbon operations. Studies show recycled ceramic waste can replace 70% of virgin raw materials in castables, reducing CO₂ footprint and cost. Tata Steel targets net-zero emissions in 2045 and is adding mini-mill capacity that specifies low-density spinel-calcium-aluminate foams. Such linings cut bulk density to 2.8 g/cm³ and extend service life from 18 to 31 heats, lowering refractory consumption. These gains underpin medium-term demand growth in the ceramic foam market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile alumina & zirconia prices pressuring profit margins | -1.10% | Global, with acute impact on Asian producers | Short term (≤ 2 years) |

| Brittleness leading to handling losses in automated foundries | -0.70% | North America and EU, spreading to Asia-Pacific | Medium term (2-4 years) |

| Emerging polymer-derived foams offering cheaper insulation alternatives | -0.50% | Global, concentrated in construction applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile alumina and zirconia prices pressuring profit margins

High-purity alumina and zirconia constitute a significant portion of the variable costs in ceramic foam production. Sharp price swings have forced quarterly contract renegotiations and spot purchases at elevated premiums. Zirconia toughening boosts compressive strength by 206% yet becomes less economical when raw-material indices spike. Morgan Advanced Materials noted a 4.6% revenue dip in its Thermal Ceramics unit despite stable order intake because surcharges lagged cost inflation. Smaller Asian producers, lacking long-term contracts, experienced margin compression that slowed plant upgrades and capacity additions within the ceramic foam industry.

Brittleness leading to handling losses in automated foundries

Open-cell foams fracture if robotic grippers apply uneven force or accelerated trajectories in high-throughput lines. Increased rejection rates lead to higher per-part costs and disrupt takt times. Carbon-bonded alumina filters trialed for steel casting performed well in metallurgical terms but demanded bespoke handling jigs, adding capital outlays. Continuous direct-foaming research eliminates template-burnout defects and could raise green strength, yet commercial readiness remains two to three years away. Until then, brittleness remains a mid-term adoption hurdle in automated nodes of the ceramic foam market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silicon carbide maintains leadership on thermal performance

Silicon carbide commanded 44.74% share of the ceramic foam market in 2025 due to its stability above 1,500 °C, resistance to molten aluminum and superior thermal conductivity. Rising EV casting volumes and stringent inclusion limits underpin sustained demand. Other advanced compositions such as magnesium-aluminate spinel, boride ceramics and hybrid composites form the fastest-growing cluster at a 7.41% CAGR, fulfilling aerospace, nuclear and ultra-high-temperature needs. Aluminum oxide remains attractive for general-purpose iron casting thanks to cost-efficiency, though its temperature ceiling constrains penetration into new EV and hydrogen segments. Zirconium oxide retains a niche in chemically aggressive melts, where its premium price is justified by extended service life and enhanced corrosion resistance.

Second-generation boride foams demonstrate oxidation resistance above 1,800 °C, positioning them for hypersonic vehicle thermal-protection components. Research prototypes exhibit less than 5% mass loss after 1,000 thermal cycles, a milestone that could spur future commercialization. As material scientists synthesize multiphase foams combining whisker reinforcement and oxide scales, the ceramic foam market may witness incremental displacement of legacy alumina in extreme environments.

By Manufacturing Process: Replica method faces additive manufacturing disruption

The replica or polymer-sponge process produced 66.58% of all ceramic foams shipped in 2025 owing to decades of equipment amortization, low scrap rates and familiar quality controls. It excels in producing filters with consistent pore sizes from 10 to 60 ppi, serving high-volume non-ferrous foundries. Despite its dominance, the ceramic foam market is pivoting toward additive manufacturing, the fastest-growing process at 7.55% CAGR. Laser-sintered alumina lattices and direct-ink-written cordierite carriers allow graded porosity and topology optimization unattainable with replica routes. Early adopters in catalyst support and aerospace exploit design freedom to enhance flow uniformity and mechanical resilience.

Direct foaming, which mixes gas into ceramic slurry then sinters the resulting froth, eliminates polyurethane templates and their associated burn-out emissions. Uptake is strongest in insulation panels targeting green-building credits. Gel casting endures in applications requiring near-net-shape precision, such as biomedical implants and semiconductor wafer supports, though its relatively long cycle times limit broader diffusion.

By Application: Catalyst support emerges as growth leader

Molten-metal filtration contributed 39.05% of 2025 revenue and remains the backbone of the ceramic foam market. Foundry engineers value its proven ability to cut inclusions, improve surface finish and reduce scrap. Yet catalyst support exhibits the quickest 7.72% CAGR to 2031 as hydrogen reformers, ammonia crackers and automotive exhaust after-treatment demand high void-volume, high-surface-area carriers. Ceramic foam substrates outperform honeycomb structures by boosting mass transfer and turbulence, allowing reduced precious-metal loading without sacrificing conversion efficiency.

Automotive exhaust filters are poised for moderate growth as the US EPA implements model-year 2027–2032 emissions rules that tighten particulate limits. Thermal and acoustic insulation panels gain from zero-energy building codes, delivering 42% lower heat loss than conventional walls. Furnace linings steadily expand via recyclable spinel-based foams that drop energy consumption and extend campaign life in electric arc furnaces.

By End-User Industry: Foundry leadership challenged by diversification

Foundries consumed 42.10% of ceramic foam shipments in 2025 and will retain top rank, but their share gradually erodes as power-generation and energy infrastructures accelerate. The ceramic foam market size tied to hydrogen and advanced-energy applications is forecast to grow at an 7.63% CAGR, benefiting membrane-reactor, solid-oxide fuel cell and concentrated-solar plant deployments. Automotive EV programs create dual streams of demand: filtration for aluminum mega-castings and battery thermal management pads. Construction uptake hinges on fire-resistant insulation panels favored in North American and European retrofit policies aimed at achieving net-zero operating emissions.

Pollution control and chemical synthesis maintain stable mid-single-digit growth, supported by ever-stricter industrial emission caps worldwide. Chemical processors adopt zirconia and spinel foams in corrosive hydrofluoric and hydrochloric acid environments, extending catalyst-bed life and lowering shutdown frequency.

Geography Analysis

Asia-Pacific’s 46.25% revenue share in 2025 reflects its integrated supply chain encompassing raw materials, casting facilities and downstream EV production. China’s continual steel output and Japan’s advanced ceramics research sustain baseline volumes, while South Korea’s hydrogen-economy roadmap raises future demand for catalyst foams. Forecasts indicate the region's ceramic foam market is projected to witness significant growth, supported by a robust 7.08% CAGR during the forecast period. Government grants for smart manufacturing and energy efficiency amplify adoption across foundry, automotive, and construction sectors.

North America represents a mature yet innovative arena. The region fields additive-manufacturing pioneers and benefits from federal hydrogen and battery-supply-chain funding. Saint-Gobain’s New York expansion confirms confidence in domestic catalyst-support demand. Tightening US vehicle emissions rules stimulate ceramic exhaust filter consumption. Stable iron foundry operations in the Midwest and growing aluminum casting for EV parts ensure demand resilience.

Europe prioritizes circular economy mandates and carbon-neutral steel, driving uptake of recyclable refractory foams in mini-mills. Germany, France and Italy upgrade casting lines with automated filter-handling systems, spurring research into tougher foam formulations. EU grants back additive-manufacturing pilot lines that fabricate customized pore architectures for aerospace and defense. Stringent building energy directives stimulate ceramic insulation panel deployment in renovation projects.

South America and Middle East & Africa are smaller but rising. Brazilian and Argentinian automakers adopt aluminum casting filters, while new steel capacity in Saudi Arabia’s Vision 2030 bolsters refractory demand. Foreign direct investment underpins advanced-materials institutes that enhance local competence. Infrastructure gaps and limited technical expertise slow adoption, yet localized production partnerships could unlock latent potential for the ceramic foam industry.

Competitive Landscape

The ceramic foam market is moderately consolidated, with regional specialists operating alongside global materials conglomerates. Five leading suppliers account for around 63% of global revenue, underscoring significant yet not overwhelming concentration. Vesuvius, Pyrotek and SELEE leverage decades of foundry relationships to co-engineer filter designs that fit customer gating systems. Advanced research centers on coating chemistries that boost filtration efficiency without increasing pressure drop.

Strategic investments emphasize vertical integration to secure raw materials and internalize additive-manufacturing competencies. Patent filings reveal a pivot toward hybrid processes that marry replica foaming with laser finishing, cutting total cycle time by 30%. Emerging disruptors such as Lithoz and 3DCeram specialize in ceramic-printing systems that fabricate geometrically intricate lattice foams for aerospace and biomedical clients.

Collaborations with automakers and fuel-cell developers accelerate application-specific innovation. Tier-one suppliers embed data-logging chips into filter frames, allowing foundries to track real-time melt cleanliness and predict change-out schedules. Such digital services differentiate offerings in an otherwise price-sensitive environment. Geographical expansion strategies include joint ventures in India and Vietnam to serve burgeoning EV supply chains, lowering logistics costs and customs barriers.

Ceramic Foam Industry Leaders

ERG Aerospace Corporation

LANIK s.r.o.

Pyrotek

SELEE Corp.

Vesuvius

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ERG Aerospace showcased its advanced foam-based products designed to meet the rigorous demands of aerospace and space systems at booth 634 during Space Tech USA. This initiative is expected to drive innovation and growth in the ceramic foam market by highlighting the material's potential in high-performance applications.

- March 2024: The Environmental Protection Agency (EPA) has introduced new emissions standards for light-duty and medium-duty vehicles, applicable to model years 2027-2032. These regulations are expected to drive the adoption of advanced technologies. As a result, the demand for ceramic foam in emissions control applications is anticipated to grow.

Global Ceramic Foam Market Report Scope

The global ceramic foams market report includes:

| Aluminum Oxide (Al₂O₃) |

| Silicon Carbide (SiC) |

| Zirconium Oxide (ZrO₂) |

| Others Types (Magnesium Aluminate Spinel, etc.) |

| Replica/Polymer Sponge Method |

| Direct Foaming |

| Gel Casting |

| Additive Manufacturing |

| Molten Metal Filtration |

| Automotive Exhaust Filters |

| Thermal and Acoustic Insulation |

| Catalyst Support |

| Furnace Lining |

| Other Applications (Biomedical Scaffolds, etc.) |

| Foundry |

| Automotive |

| Construction |

| Pollution Control and Chemcial Synthesis |

| Other End-user Industries (Power Generation and Energy, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Aluminum Oxide (Al₂O₃) | |

| Silicon Carbide (SiC) | ||

| Zirconium Oxide (ZrO₂) | ||

| Others Types (Magnesium Aluminate Spinel, etc.) | ||

| By Manufacturing Process | Replica/Polymer Sponge Method | |

| Direct Foaming | ||

| Gel Casting | ||

| Additive Manufacturing | ||

| By Application | Molten Metal Filtration | |

| Automotive Exhaust Filters | ||

| Thermal and Acoustic Insulation | ||

| Catalyst Support | ||

| Furnace Lining | ||

| Other Applications (Biomedical Scaffolds, etc.) | ||

| By End-User Industry | Foundry | |

| Automotive | ||

| Construction | ||

| Pollution Control and Chemcial Synthesis | ||

| Other End-user Industries (Power Generation and Energy, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the ceramic foam market?

The ceramic foam market size is USD 518.04 million in 2026.

How fast will the ceramic foam market grow through 2031?

The market is forecast to expand at a 5.15% CAGR, reaching USD 665.9 million by 2031.

Which material type leads the ceramic foam market?

Silicon carbide leads with a 44.74% share thanks to superior thermal and chemical performance in molten-metal filtration.

Why is additive manufacturing important for ceramic foam producers?

Additive techniques let manufacturers create complex graded porosity, improving filtration and catalyst functions while shortening prototyping cycles.

Which region accounts for the largest ceramic foam demand?

Asia-Pacific holds 46.25% of global revenue due to its dense foundry base, EV production and steel capacity.

What key restraint could limit short-term market growth?

Volatile alumina and zirconia prices are squeezing margins, particularly for producers without long-term supply contracts.

Page last updated on: