Modular Robotics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 14.26 Billion |

| Market Size (2030) | USD 27.92 Billion |

| Growth Rate (2025 - 2030) | 14.38% CAGR |

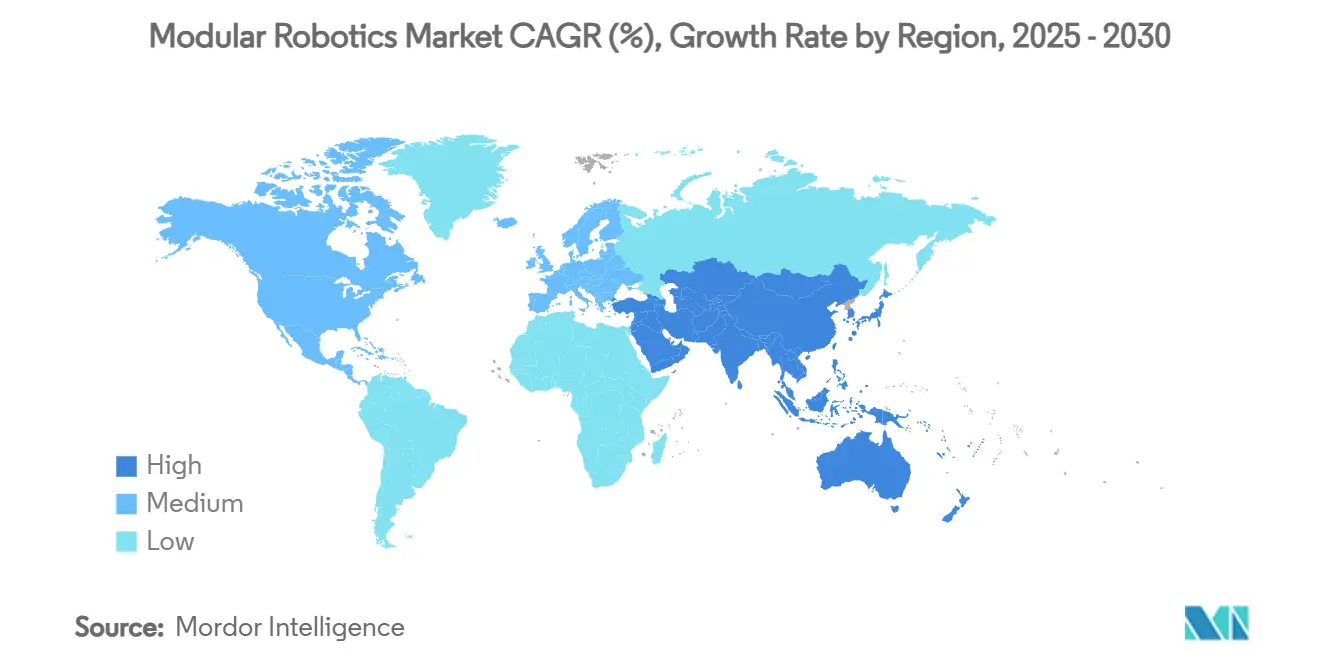

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

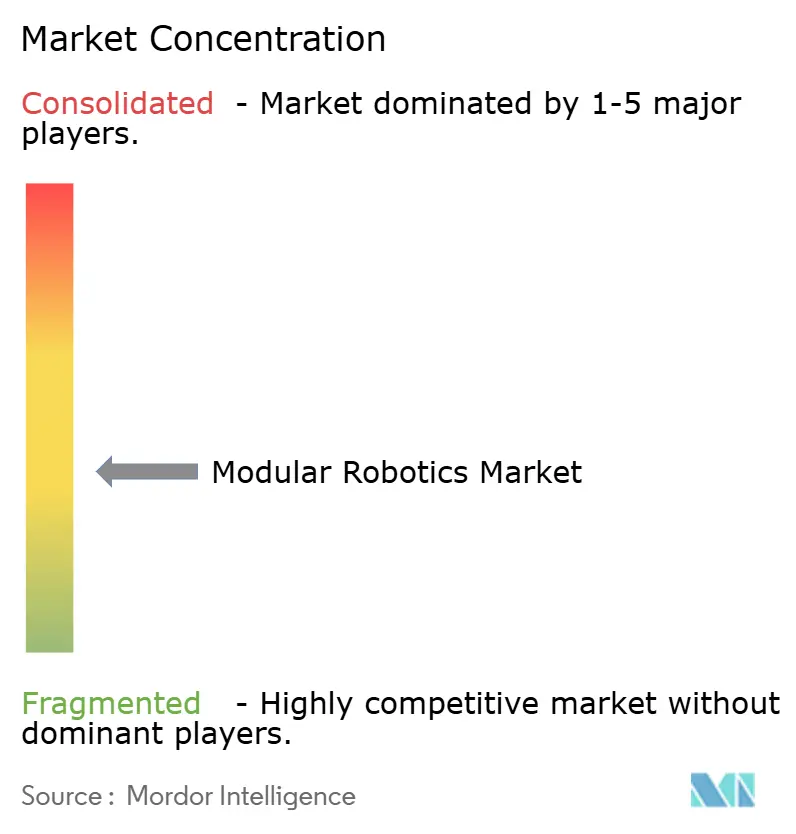

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modular Robotics Market Analysis by Mordor Intelligence

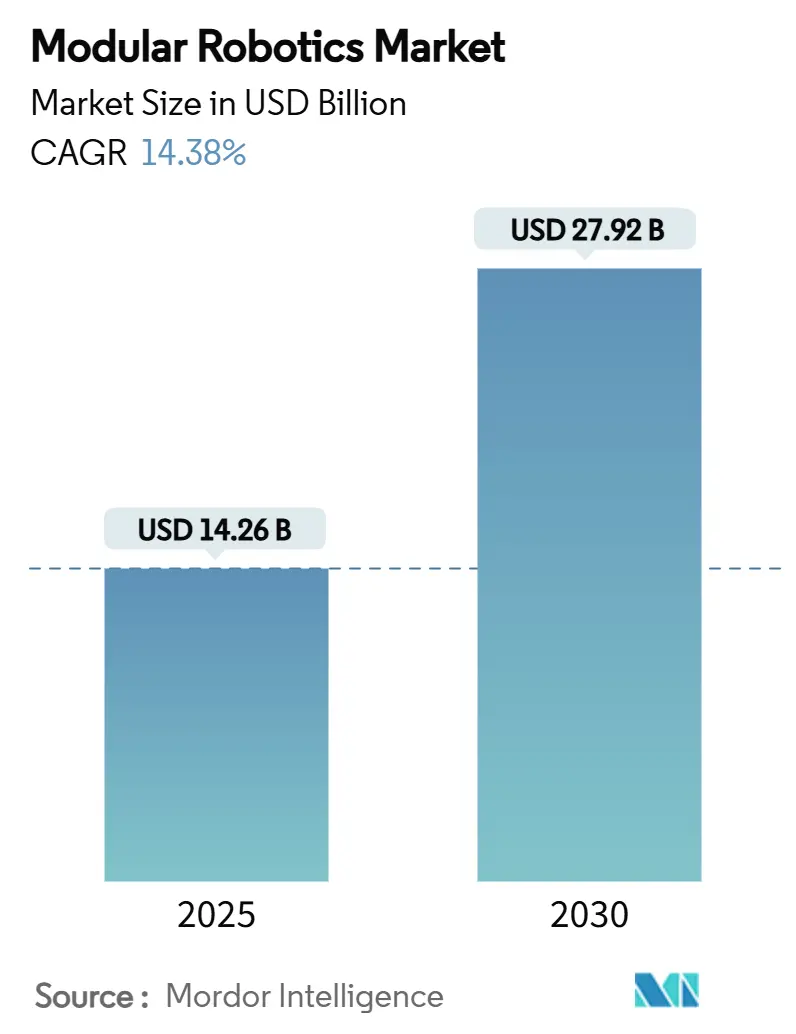

The modular robotics market size is USD 14.26 billion in 2025 and is forecast to climb to USD 27.92 billion by 2030, reflecting a 14.38% CAGR over the period. This momentum stems from the transition away from fixed-architecture robots toward flexible, plug-and-play modules that lower change-over time and reduce lifetime cost of ownership. Automotive original equipment manufacturers adopting lights-out plants, such as Tesla’s unboxed flow that targets 50% cost cuts with 40% fewer operators, are setting the pace. Asia-Pacific holds sway thanks to China’s 276,000 new industrial robot installations in 2023 and the country’s deep patent pool covering two-thirds of global humanoid robotics filings. Collaborative modules are scaling fastest as safety-rated joints and integrated vision shrink deployment barriers for mixed human–robot workcells. Across end-user verticals, healthcare facilities eager to expand surgical capacity and electronics producers racing toward sub-10 nm geometries view reconfigurable platforms as a hedge against rapid product change.

Key Report Takeaways

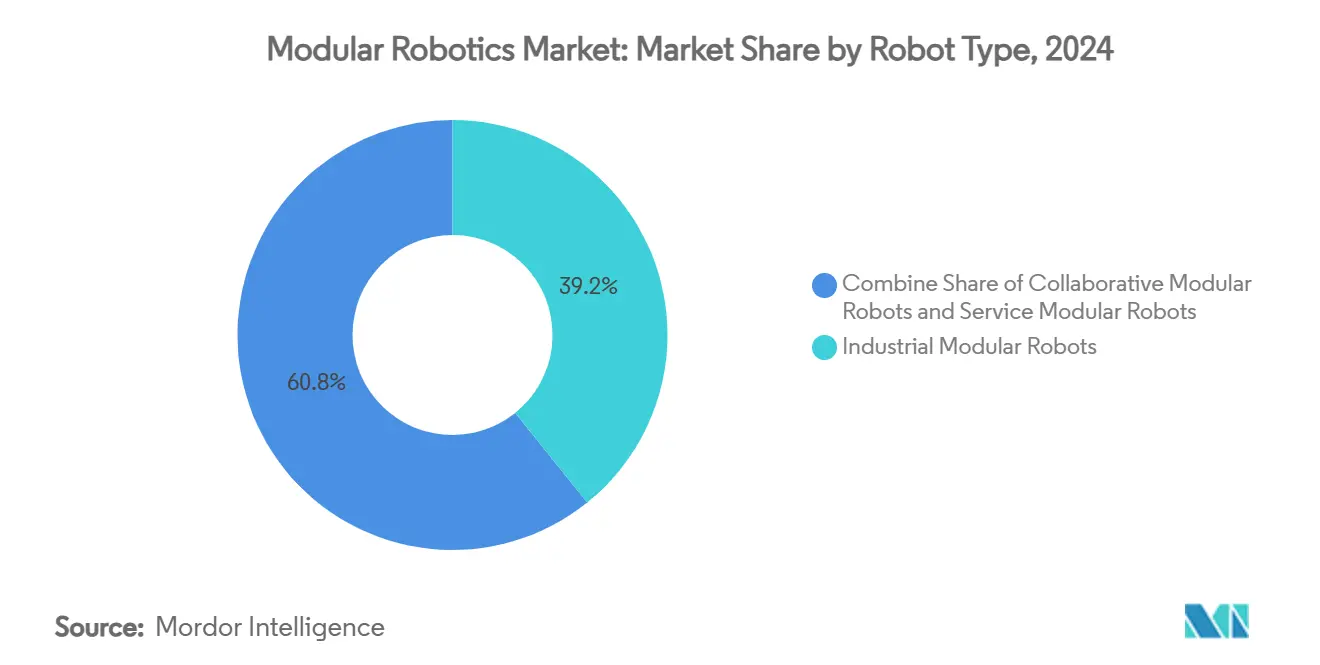

- By robot type, industrial modules led with 39.21% share in 2024, while collaborative modules posted the highest 16.02% CAGR outlook through 2030.

- By payload, systems handling up to 15 kg are projected to expand at 17.21% CAGR, yet the 16–60 kg bracket retained 34.55% of 2024 revenue.

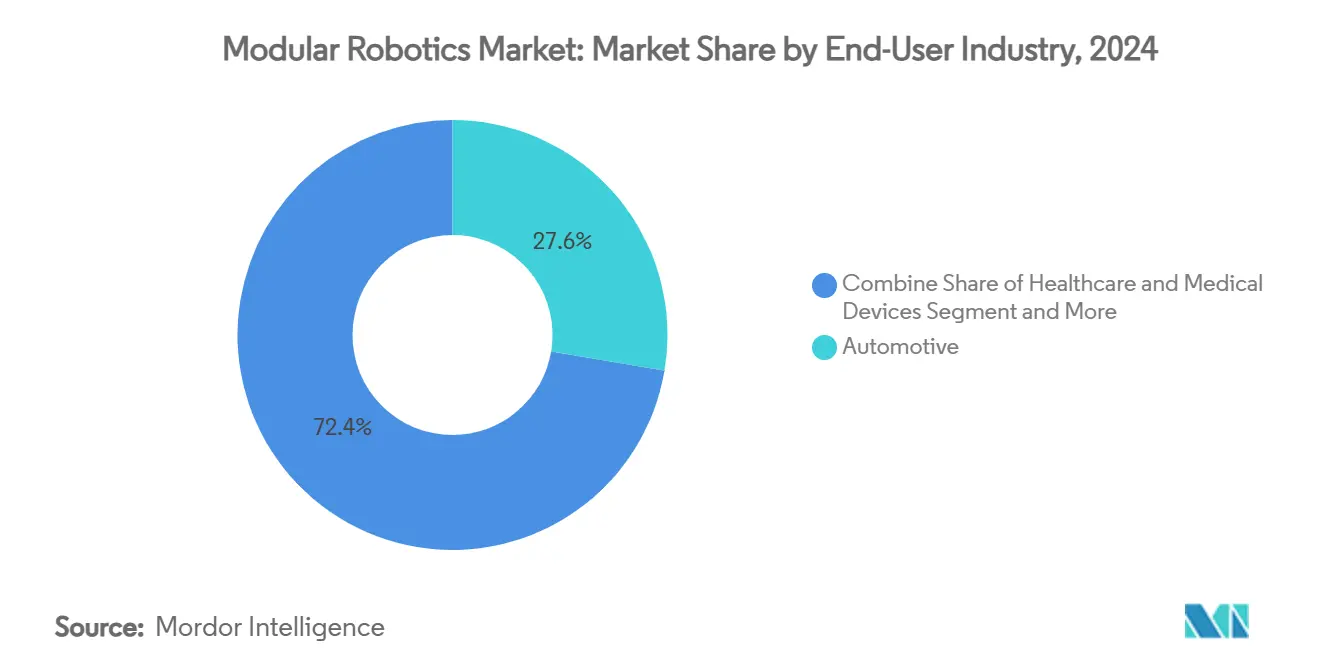

- By end-user, automotive lines captured 27.64% of 2024 revenue, whereas healthcare solutions are forecast to grow at 18.44% CAGR.

- By application, assembly dominated with 31.34% share in 2024, but inspection and testing activities are on track for a 17.34% CAGR.

- By geography, Asia-Pacific controlled 34.56% of 2024 revenue and is expected to post an 18.21% CAGR through 2030.

Global Modular Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid miniaturization and cost-down of servo-modules | +2.1% | Global, with Asia-Pacific manufacturing leadership | Medium term (2-4 years) |

| Automotive OEM shift to flexible, lights-out factories | +3.2% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Plug-and-play software ecosystems and ROS 2 integration | +1.8% | Global, led by North America and EU | Medium term (2-4 years) |

| Surge in e-commerce micro-fulfillment sites | +2.4% | Global, with highest impact in North America | Short term (≤ 2 years) |

| Government "re-shoring" incentives for adaptive automation | +1.9% | North America primarily, spillover to EU | Long term (≥ 4 years) |

| AI-powered self-reconfiguring swarm platforms | +1.4% | Global, early adoption in aerospace and defense | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Miniaturization and Cost-Down of Servo-Modules

Shrinking integrated drives now deliver the same torque in half the volume, unlocking compact joints that streamline arm architecture and lower bill-of-materials cost. Maxon’s micro integrated motion controller, FAULHABER’s high-density miniature motors, and Copley’s nano drives exemplify this advance. [1]FAULHABER, “Drive Systems,” faulhaber.com Lighter joints enable cobots handling 3–16 kg workloads to be redeployed without overhead cranes, so factories refresh lines overnight instead of during shutdowns. Healthcare, semiconductor, and laboratory customers benefit from sterile, cleanroom-rated modules that tuck electronics inside sealed casings. The cumulative effect is accelerating adoption in precision markets where a kilogram saved per axis frees valuable workspace for sensors and vision. As component prices fall and volumes rise, cost parity with traditional articulated arms approaches, expanding the modular robotics market footprint further.

Automotive OEM Shift to Flexible, Lights-Out Factories

Vehicle makers are dismantling fixed conveyors and installing reconfigurable framing cells that accept multiple body variants. BMW extended automated in-plant driving to 90% of Leipzig production, trimming idle time and supporting mixed model runs. [2]BMW Group, “High-Tech in Production,” bmwgroup.com Mercedes-Benz lowered energy use 20% at Rastatt after introducing AI-directed modular stations that build hybrid and battery vehicles on one line. Magna’s framing system and Comau’s rapid model-switching cells allow contract assemblers to chase niche electric vehicle programs without dedicated tooling. The outcome is a step-change in takt flexibility that favors robots capable of fast axis exchange, quick fixture swaps, and software-defined motion sequencing. Automotive leadership accelerates downstream suppliers’ investments, reinforcing scale economies for module vendors.

Plug-and-Play Software Ecosystems and ROS 2 Integration

Industrial maturity of ROS 2 is washing away proprietary programming silos. Neobotix bundles ROS 2 simulation and Nav 2 autonomous navigation, giving integrators validated libraries for path planning and multi-goal behaviours. Apex.AI’s Grace middleware injects deterministic memory handling and safety certification pathways, easing the leap from lab prototype to volume production. [3]NIST, “Measurement Science for Manufacturing Robotics,” nist.govConsultancy roadmaps warn that ROS 1 reaches end-of-life in May 2025, prompting urgent migration among brownfield fleets. The Swedish Defence Research Agency likens the situation to the PC standardisation wave that crushed hardware cost by unifying software stacks. As APIs converge and safety stacks mature, fleets blend hardware from several vendors yet share a single software pipeline, lifting demand for vendor-agnostic modular kits.

Surge in E-Commerce Micro-Fulfillment Sites

Online retail growth fuels small-footprint automation inside existing retail real estate. AutoStore placed 140 cube-based robots at CJ Logistics in Incheon, tripling order throughput per square metre. Amazon piloted Project Juniper, embedding AutoStore and Fulfil technology to push goods directly from store backrooms to local consumers in under two hours. Brightpick’s Giraffe picker raises storage density up to threefold and processes 5,200 parcels per hour, while Tompkins’ tSort converts idle retail space into parcel hubs with minimal floor anchors. Reconfigurable cells let operators adjust bin counts and bot fleets to seasonal peaks without structural works. The modular robotics market rides this wave because fulfilment providers value rapid deployment and scalability over long life cycles typical of distribution centre conveyors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for industrial-grade modular joints | -2.8% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| IP fragmentation slowing standards harmonization | -1.6% | Global, particularly affecting cross-border deployments | Medium term (2-4 years) |

| Worker-safety certification gaps for dynamic reconfiguration | -1.2% | North America and EU regulatory focus | Medium term (2-4 years) |

| Rare-earth magnet supply-chain volatility | -2.1% | Global, highest impact on humanoid robotics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Industrial-Grade Modular Joints

Precision reducers and safety-rated controllers stretch payback periods for small plants. RobCo offers ISO 10218-1 compliant arms that teach by demonstration, yet ownership still requires a multi-year depreciation window. Japanese harmonic reducer suppliers set pricing power, leaving emerging-market buyers exposed to foreign-exchange swings. Formic’s robotics-as-a-service contracts lower the entry hurdle, but the National Institute of Standards and Technology notes that lack of internal expertise remains a parallel obstacle to capital access. [4]Apex.AI, “From ROS 2 Prototype to Production,” apex.ai Overall, front-loaded investment slows penetration into high-mix, low-volume workshops even though total cost of ownership falls over the asset life.

IP Fragmentation Slowing Standards Harmonization

Modular interfaces vary by supplier, and patent thickets covering tool-changer couplings and hot-swap axis drives generate licensing costs and legal uncertainty. Cross-border integrators juggle overlapping claims when exporting systems into multiple jurisdictions. Divergent safety protocols compound complexity, forcing repeat validation. While consortia promote open mechanical standards, resolution will take several release cycles, moderating global roll-outs until late decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Industrial Leadership Faces Collaborative Challenge

Industrial modules retained 39.21% of 2024 revenue as manufacturers rely on proven six-axis arms for 24 / 7 throughput. The modular robotics market size contribution of this cohort remains significant despite slower growth. Collaborative modules, however, project a 16.02% CAGR that outpaces all other types as safety scanners, force-limiting joints, and intuitive programming make deployment attractive on existing lines. Universal Robots installed cobot cells at Marelli Slovakia that lifted electronics assembly speed 25% while eliminating quality escapes. CES 2025 demonstrations by Elephant Robotics highlight how one base can morph from education to light industrial roles, underscoring convergence between industrial and service classes. Over the forecast, hybrid architectures blending high payload capability with cobot ergonomics are likely, reinforcing modularity’s appeal.

The service-robot slice stays modest yet strategic, largely in healthcare, hospitality, and inspection. Hospitals value sterile-compliant frames where surgical manipulators detach for autoclave without dismantling the entire arm. Hotels test concierge carts that swap drink modules for linen-delivery bins during off-peak hours. As non-industrial demand scales, module suppliers diversify catalogue offerings, incrementally lowering unit costs for all markets.

By Payload Capacity: Mid-Range Dominance Yields to Lightweight Innovation

Arms lifting 16–60 kg anchored 34.55% of 2024 spending, reflecting automotive and general-fabrication staples. Module kits in this range balance reach, stiffness, and affordability, suiting engine block handling and palletising tasks. Yet lightweight units below 15 kg are slated for the fastest 17.21% CAGR, propelled by touch-safe cobots and desktop assembly labs. Maxon and Pollen Robotics collaborated on the Reachy 2 humanoid, showing how 6 kg-class modular joints can drive natural motions.

Heavier segments serve specialist niches. Payloads above 225 kg load aircraft fuselages and wind-turbine sections, while 61–225 kg cells dominate automotive under-body framing. Although these categories enjoy steady replacement revenue, their share will erode as lightweight and mid-range segments absorb growth, reshaping the modular robotics market share profile across payload brackets.

By End-User Industry: Automotive Leads While Healthcare Accelerates

Automotive lines captured 27.64% of 2024 revenue by weaving reconfigurable frames into mixed model plants shifting toward electric platforms. Lights-out press shops and gigacasting cells leverage modular arms to adjust gripper sets between sedan and SUV panels in minutes. Healthcare trails in size but commands an 18.44% CAGR as surgical suites adopt systems like the Carina platform that cut unit cost through shared master controllers.

Electronics and semiconductor plants rank third due to escalating wafer fabrication complexity. KUKA supplied 13,000 ESD-rated arms to the sector, many in modular kits that support tool retrofits as node sizes shrink. Food and beverage bottlers turn to Sidel’s label-applying cobot, which swaps reel modules without stopping the line, trimming change-over to 45 seconds. Logistics firms such as GXO sign multi-year humanoid deployments to meet rising e-commerce peaks. These cross-vertical wins reinforce the modular robotics industry thesis that a single hardware platform can traverse markets by swapping end-effectors and software.

By Application: Assembly Dominance Challenged by Inspection Innovation

Assembly retained 31.34% of 2024 revenue as module kits excel at fastening, pressing, and seating operations. Integrated vision lets the same cell handle multiple SKUs with zero manual recalibration. Inspection and testing lines, however, will climb at 17.34% CAGR because AI vision paired with dexterous arms can validate ever-smaller tolerances in electronics and medical devices. Scientific Reports highlighted modular arms validating urological instrument alignment, cutting rework and surgeon setup time.

Material handling, pick-and-place, and welding remain durable pillars, yet growth moderates as those segments saturate. Painting and dispensing benefit from modular extension axes that reach complex contours. The expanding inspection share indicates manufacturers now view quality assurance as equal to throughput, prompting procurement of versatile robots able to switch from assembly to metrology during off-shifts, enhancing utilisation rates across the modular robotics market.

Geography Analysis

Asia-Pacific held 34.56% of 2024 revenue and projects an 18.21% CAGR through 2030, buoyed by China’s 276,000 new industrial installs and national roadmaps that subsidise high-end servos. Government clusters in Shenzhen and Suzhou anchor component ecosystems, cutting lead time for domestic brands.

North America leverages the CHIPS and Inflation Reduction Acts to funnel tax credits into fabs and battery plants, lifting demand for adaptive production pods. Apple has located a Detroit manufacturing academy to widen the workforce for smart-factory roll-outs. Europe, focused on precision mid-volume goods, sees Munich-based RobCo scale new facilities to become a regional modular leader.

South America, the Middle East, and Africa start from a smaller installed base but show double-digit ordering as labour costs rise and energy-exporting economies diversify. Regional integrators partner with global OEMs to localise gripper fabrication, easing import duties. Over the horizon, Asia-Pacific will still top volume, yet aggregated growth from the other four regions narrows the modular robotics market size gap, diversifying revenue streams for multinational suppliers.

Competitive Landscape

The field counts 24 material participants yet none surpasses a 10% share, yielding moderate fragmentation. ABB, FANUC, and KUKA exploit service networks and vertical integration, while challengers like Flexiv, Neura Robotics, and Agile Robots centre on AI-first control stacks and variable-stiffness joints. ABB injected USD 170 million into the OmniCore platform that cuts cycle time 25% and energy 20%, positioning a hardware-agnostic controller at portfolio core.

Competitive archetypes divide into horizontal platform builders and vertical specialists. Horizontal players package generic motion modules plus application libraries, courting integrators who tailor cells. Vertical specialists lock in deep domain know-how: Neura targets human-cobot interaction, whereas RobCo standardises European brownfield retrofits. Patent analytics reveal Alphabet, Hyundai, and ABB hold the most claims on dexterous manipulation outside China, suggesting looming license negotiations as humanoids reach pilot scale.

White-space sits in mid-market plants where conventional six-axis rigs overshoot capability and entry-level cobots underperform. Vendors promoting scalable torque modules configurable from 10 kg to 60 kg without new controllers can tap this underserved zone. Strategic partnerships, including ABB’s tie-up with Molg on e-waste micro-factories, point to an ecosystem model in which hardware OEMs join niche system builders to accelerate adoption.

Modular Robotics Industry Leaders

ABB Ltd.

Yaskawa Electric Corporation

FANUC Corporation

KUKA Aktiengesellschaft

Universal Robots A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SoftBank committed USD 500 million to Skild AI to accelerate AI-native robotics platforms.

- January 2025: 1X purchased Kind Humanoid, aligning large-language models with bipedal robots.

- January 2025: AutoStore opened a robot plant in Rayong, Thailand, halving global lead times.

- December 2024: Apptronik partnered with Google DeepMind to improve humanoid intelligence.

- December 2024: Sojo Industries and Blue Chip Beverage adopted the Sojo Flight modular line for flexible packaging.

Global Modular Robotics Market Report Scope

| Industrial Modular Robots |

| Service Modular Robots |

| Collaborative Modular Robots |

| Up to 15 kg |

| 16-60 kg |

| 61-225 kg |

| Above 225 kg |

| Automotive |

| Electronics and Semiconductor |

| Healthcare and Medical Devices |

| Food and Beverage |

| Logistics and Warehousing |

| Aerospace and Defense |

| Other End-User Industry |

| Assembly |

| Material Handling |

| Pick and Place |

| Welding and Soldering |

| Painting and Dispensing |

| Inspection and Testing |

| Other Application |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Robot Type | Industrial Modular Robots | ||

| Service Modular Robots | |||

| Collaborative Modular Robots | |||

| By Payload Capacity | Up to 15 kg | ||

| 16-60 kg | |||

| 61-225 kg | |||

| Above 225 kg | |||

| By End-User Industry | Automotive | ||

| Electronics and Semiconductor | |||

| Healthcare and Medical Devices | |||

| Food and Beverage | |||

| Logistics and Warehousing | |||

| Aerospace and Defense | |||

| Other End-User Industry | |||

| By Application | Assembly | ||

| Material Handling | |||

| Pick and Place | |||

| Welding and Soldering | |||

| Painting and Dispensing | |||

| Inspection and Testing | |||

| Other Application | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current valuation of the modular robotics market?

The modular robotics market size stands at USD 14.26 billion in 2025 and is projected to reach USD 27.92 billion by 2030.

Which end-user segment is expanding the fastest?

Healthcare applications are growing at an 18.44% CAGR as hospitals adopt surgical and rehabilitation modules.

How much of global revenue does Asia-Pacific generate?

Asia-Pacific commands 34.56% of 2024 revenue and is forecast to maintain leadership through 2030.

What key factor constrains adoption among small manufacturers?

High upfront capex for precision modular joints remains the chief barrier, particularly in emerging markets.

Which application will outpace others over the forecast?

Inspection and testing modules are projected to register a 17.34% CAGR thanks to AI-enabled quality demands.

Page last updated on: