Laboratory Robotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

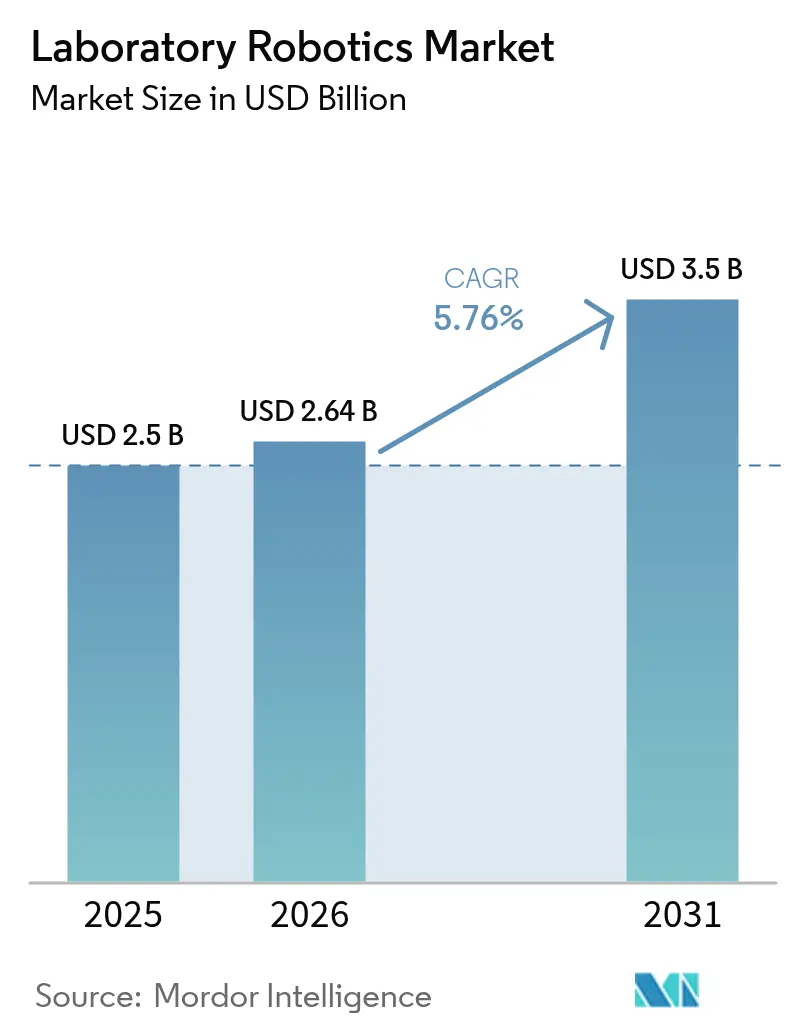

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 3.5 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

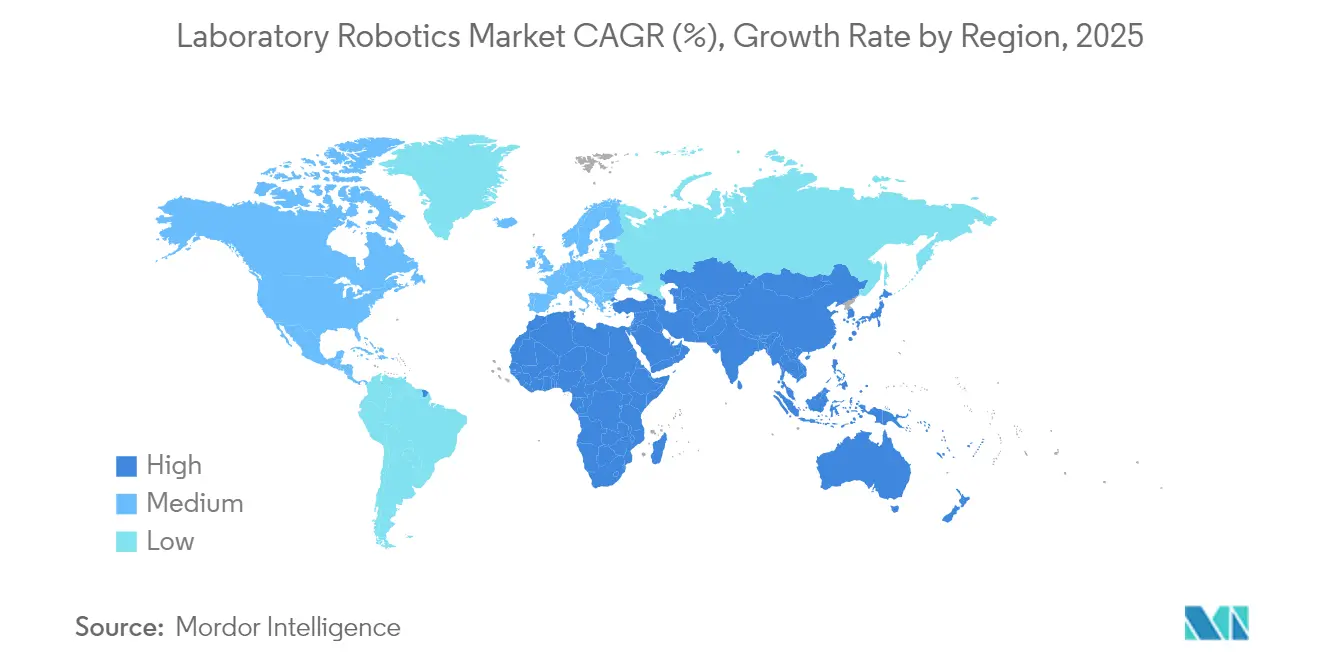

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

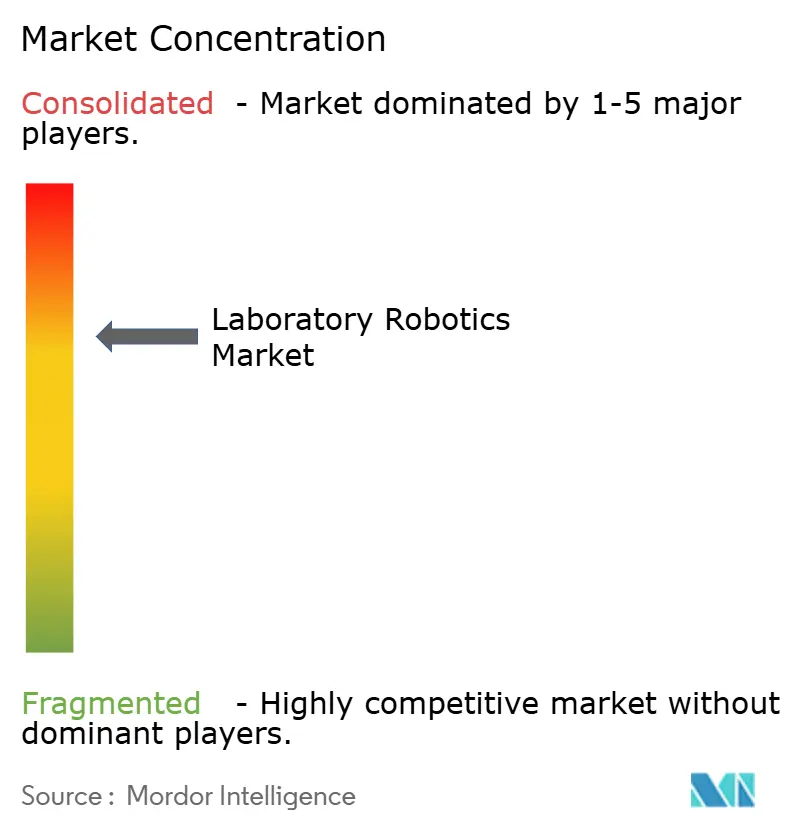

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Robotics Market Analysis by Mordor Intelligence

The laboratory robotics market size was valued at USD 2.5 billion in 2025 and estimated to grow from USD 2.64 billion in 2026 to reach USD 3.5 billion by 2031, at a CAGR of 5.76% during the forecast period (2026-2031). The measured trajectory signals a shift from emergency-driven procurement toward disciplined, long-term automation roadmaps. Demand for FDA-ready systems grows as the Laboratory Developed Tests final rule comes into force in 2025, pushing laboratories toward ISO-15189-compliant robotics. Precision medicine pipelines, sustainability mandates, and modular robotic ecosystems further reinforce investment decisions. Vendors that bundle software, instruments, and validation support continue to capture wallet share, while emerging competitors focus on acoustic dispensing, mobile manipulation, and AI integration to differentiate in the laboratory robotics market. [1]Center for Drug Evaluation and Research, “Electronic Systems, Electronic Records, and Electronic Signatures in Clinical Investigations: Questions and Answers,” U.S. Department of Health and Human Services, fda.gov

Key Report Takeaways

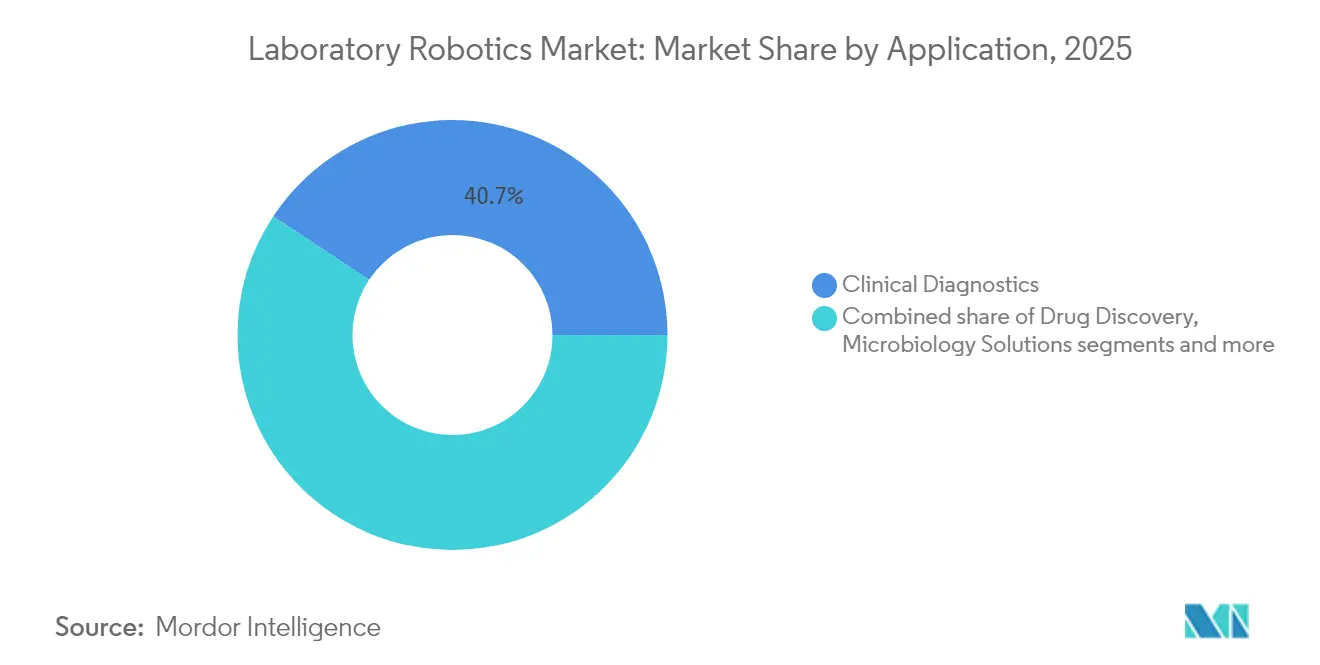

- By application, clinical diagnostics held 40.70% of the laboratory robotics market share in 2025, whereas genomics solutions are set to grow at 11.05% CAGR through 2031.

- By end-user, pharmaceutical and biotechnology companies led with 38.05% revenue share in 2025; contract research organizations will expand at a 9.67% CAGR to 2031.

- By robot type, liquid-handling platforms accounted for 54.30% of the laboratory robotics market size in 2025; collaborative mobile lab robots are projected to register 13.22% CAGR to 2031.

- By workflow stage, analytical and assay execution dominated with 46.60% share of the laboratory robotics market size in 2025, while pre-analytical sample preparation is forecast to rise at 10.25% CAGR between 2026-2031.

- By geography, North America captured 40.25% of the laboratory robotics market share in 2025; Asia-Pacific is poised for an 8.18% CAGR on the back of government-backed modernization programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laboratory Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for biosafety & error-free high-throughput screening | 1.80% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Acceleration of pandemic-preparedness programs (e.g., CEPI, BARDA funding) | 1.20% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Growth of personalized medicine requiring flexible low-volume liquid handling | 1.50% | Global, early adoption in North America & EU | Long term (≥ 4 years) |

| Adoption of AI-enabled self-optimizing "lab of the future" cells | 0.90% | APAC core, expanding to North America & EU | Long term (≥ 4 years) |

| Corporate net-zero roadmaps favouring energy-efficient cobots | 0.70% | EU & North America, emerging in APAC | Medium term (2-4 years) |

| Integration of robotic micro-factories inside CDMOs | 0.60% | Global, with early gains in North America, EU, Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Biosafety & Error-Free High-Throughput Screening

Bio-risk mitigation policies now require BSL-3 and BSL-4 facilities to eliminate manual contact with infectious samples. Automated lines at Mayo Clinic process more than 6 million assays annually while halving blood-draw volumes, demonstrating how robotics improve both safety and specimen stewardship. Integrated vision and AI modules flag pipetting anomalies in real time, satisfying data-integrity audits. Vendors add ultraviolet decontamination cycles that run between batches, allowing around-the-clock operation without compromising operator safety. These capabilities underpin steady demand within the laboratory robotics market, especially in reference labs and vaccine-testing centers.

Acceleration of Pandemic-Preparedness Programs

Public-health agencies allocate multibillion-dollar budgets that expressly call for surge-ready automation. CEPI and BARDA grants stipulate platforms that scale from research to mass testing within weeks. The University of Sheffield’s self-driving chemistry lab cut polymer discovery timelines by orders of magnitude through closed-loop AI-robot workflows. Manufacturers now design modular carts that laboratories can reconfigure for virology, serology, or vaccine potency assays on short notice. Preparedness funding thus acts as a tailwind for flexible systems across the laboratory robotics market. [2]Beckman Coulter Life Sciences, “Beckman Coulter Life Sciences Revolutionizes High-Throughput Genomic Sample Preparation with the New Biomek Echo One System,” News-Medical, news-medical.net

Growth of Personalized Medicine Requiring Flexible Low-Volume Liquid Handling

Next-generation sequencing and single-cell omics often need sub-microliter transfers that standard pipettes cannot replicate. Beckman Coulter’s Echo acoustic platform dispenses viscous or volatile reagents without tips, eliminating cross-contamination and consumable waste. As companion diagnostics gain regulatory clearance, oncology labs adopt robots that verify droplet volumes in real time, ensuring reproducibility. Such precision workflows sustain double-digit growth for genomics solutions inside the laboratory robotics market.

Adoption of AI-Enabled Self-Optimizing “Lab of the Future” Cells

Autonomous labs couple machine-learning engines with robotic arms to iterate experiments continuously. North Carolina researchers showed AI-guided systems executing hypothesis generation, experimentation, and analysis without human intervention. Commercial systems now integrate predictive-maintenance dashboards that trigger protocol rerouting when wear is detected, preserving uptime. Early deployments in materials science and drug discovery illustrate the productivity lift that persuades CFOs to fund end-to-end automation, reinforcing expansion of the laboratory robotics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity for ISO-15189 compliant installations | -1.40% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Scarcity of robotics-literate lab personnel | -0.80% | Global, with concentration in APAC & emerging markets | Medium term (2-4 years) |

| Legacy LIMS interoperability gaps | -0.60% | North America & EU primarily | Short term (≤ 2 years) |

| Cyber-security vulnerability of networked lab robots | -0.50% | Global, heightened in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity for ISO-15189 Compliant Installations

ISO 15189:2022 demands rigorous validation and documentation. A2LA accredited the first U.S. lab under the new standard in 2024, highlighting the extensive audit trail required for clinical-grade robotics. Life-science fitouts now average USD 837 per square foot, owing to redundant power, clean-room HVAC, and secure data backbones. Smaller facilities in Latin America and Africa often postpone purchases, tempering near-term uptake within the laboratory robotics market.

Scarcity of Robotics-Literate Lab Personnel

High-mix labs need staff who can script workflows, align vision systems, and troubleshoot electro-mechanical faults. Academia still teaches biology and mechanical engineering in silos, creating a pipeline gap noted by university researchers developing AI-robot testbeds. Vendors counter with drag-and-drop software and certification courses, yet talent scarcity continues to dampen broader deployment across the laboratory robotics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Genomics Solutions Drive Precision Medicine Transformation

Clinical diagnostics contributed the largest 40.70% share to the laboratory robotics market in 2025 as hospitals consolidated sample processing under high-throughput lines. Genomics solutions, however, are charted for 11.05% CAGR through 2031, outperforming all other applications. Robotic liquid handlers ensure uniform library prep, a prerequisite for reliable variant calling in oncology and rare-disease panels. Microbiology labs deploy automated pathogen-identification cells that cut turnaround to under three hours, supporting antimicrobial stewardship initiatives. Drug-discovery platforms integrate imaging stages with plate movers for phenotypic screening at scale, while proteomics workflows gain traction as robots couple with high-resolution mass-spectrometers for biomarker discovery.

The laboratory robotics market size tied to genomics workflows will grow in lockstep with falling sequencing costs and rising test volumes. Systems that combine acoustic transfer, environmental controls, and barcode-verified traceability now appear on capital-budget shortlists at national genome centers. Pharmaceutical pipelines lean on these flexible robots to accelerate clinical biomarker validation, reinforcing genomics as the fastest-advancing slice of the laboratory robotics industry.

By End-User: Contract Research Organizations Accelerate Adoption

Pharmaceutical and biotechnology companies accounted for 38.05% of laboratory robotics market revenue in 2025 because R&D spends prioritize validated, closed-loop platforms. Contract research organizations, meanwhile, are on pace for 9.67% CAGR, reflecting sponsor outsourcing trends. CROs invest in cloud-controlled labs where clients trigger robotic protocols remotely, shortening project cycles and freeing internal capacity. Academic institutes pair grants with vendor partnerships to access state-of-the-art automation without full ownership costs. Clinical labs automate to curb staffing shortages, using robots to load analysers overnight and speed patient results.

As trial designs shift toward decentralized and patient-centric formats, CROs embrace mobile robots that can redirect plates among assay stations while documenting custody in real time. The laboratory robotics market benefits because fee-for-service models spread capital expenditure across many sponsors, encouraging continued fleet expansion.

By Robot Type: Collaborative Mobile Systems Reshape Laboratory Workflows

Liquid-handling robots retained 54.30% leadership of laboratory robotics market share in 2025, anchored by entrenched microplate and tube workflows. Emerging collaborative mobile platforms, though, promise 13.22% CAGR to 2031. Mounted on autonomous carts, these systems transport plates between incubators, imagers, and freezers, eliminating conveyor belts and fixed rails. Sample-handling gantries remain vital in medium-throughput labs, while fully-integrated total automation cells—complete with de-cappers, centrifuges, and analytics—represent the pinnacle of end-to-end solutions.

The laboratory robotics market size associated with collaborative mobile units will climb as facilities retrofit existing footprints rather than build green-field suites. Energy-saving grippers based on shape-memory alloys lower operating costs by up to 90%, aligning with corporate net-zero pledges. Vendors add proximity sensors and force-limiting joints so robots can work beside technicians without cages, accelerating floor-space optimization projects.

By Workflow Stage: Pre-Analytical Automation Gains Strategic Importance

Analytical and assay execution dominated 46.60% of laboratory robotics market size in 2025, yet pre-analytical sample preparation is growing fastest at 10.25% CAGR. Barcode verification, aliquoting, and centrifugation steps contribute nearly half of all lab errors when performed manually. Robotic benches equipped with vision systems reduce mis-labelling incidents to near zero, boosting diagnostic confidence. Post-analytical data management now mate’s robot QC outputs with laboratory information systems, enabling automatic result release or reflex testing.

Regulators increasingly audit sample-handling chains under the updated ISO standard, prompting labs to extend automation upstream. Vendors respond with modular modules—tube openers, decappers, and sealers—that snap into unified control software. The laboratory robotics industry therefore broadens its scope from high-visibility pipetting islands to holistic, cradle-to-result orchestration.

Geography Analysis

North America captured 40.25% of laboratory robotics market share in 2025 due to mature biopharma pipelines and early adoption of FDA-compliant automation. Hospital networks accelerate spending to counter staff attrition, while venture-backed biotech hubs in Boston and San Diego install self-optimizing discovery cells. Federal funding via the NIH’s Advanced Research Projects Agency for Health further underwrites purchase orders for precision-medicine labs.

Asia-Pacific is projected for 8.18% CAGR through 2031, the highest worldwide. China’s Five-Year Plan directs USD 45.2 million into robotics R&D, Japan’s New Robot Strategy adds USD 440 million, and Korea earmarks USD 128 million for intelligent systems, catalysing domestic suppliers. Pharmaceutical manufacturers scale quality-control labs alongside production lines to meet ICH and PIC/S standards, driving pull-through for flexible robots. Academic mega-labs focused on population genetics install acoustic handlers and mobile robots to process large-scale biobank specimens.

Europe maintains steady momentum supported by Horizon Europe’s USD 183.5 million robotics call. Sustainability statutes nudge laboratories toward energy-efficient robots that reduce compressed-air dependence. German automation firms export modular work cells across the EU, reinforcing intra-regional supply chains. The Middle East and Africa register nascent yet accelerating demand as health-tourism hubs and vaccine-fill-finish plants modernize pathology and QC laboratories. South America benefits from technology-transfer programs paired with local reagent manufacturing, yet broader uptake hinges on credit availability and engineer training pipelines.

Competitive Landscape

The laboratory robotics market shows moderate concentration, with a core of vendors integrating hardware, software, and validation services. Thermo Fisher, Beckman Coulter Life Sciences, and Hamilton Company bundle platforms with reagent kits, creating lock-in through workflow-specific chemistries. ABB and Agilent collaborate to marry articulated arms with chromatography instruments, offering one-throat-to-choke support. Proprietary scheduling engines that adjust tasks on the fly add further differentiation.

New entrants emphasize niche strengths. Acoustic-only transfer specialists target genomics, while cloud-native orchestration firms sell subscription-based control layers compatible with multiple robot brands. Large pharmaceutical companies such as Daiichi Sankyo now develop smart labs in-house, pressuring suppliers to open APIs for seamless integration. Energy-efficiency modules that place idle robots into standby reduce power by up to 30%, aligning with ESG scorecards and becoming a deciding factor during request-for-proposal cycles.

Intellectual-property filings in force-sensing grippers and contamination-free liquid-transfer channels keep barriers to entry high. Nonetheless, open-source micro-robots attract academic users that later scale to commercial deployments, broadening the addressable base. Service contracts—predictive maintenance, software updates, and GMP re-qualification—represent growing annuity streams, reinforcing competitive moats for incumbents that can staff global support teams. [4]ABB Robotics, “ABB Robotics and Mettler-Toledo International Inc. join forces to accelerate global adoption of flexible lab automation,” new.abb.com

Laboratory Robotics Industry Leaders

Thermo Fisher Scientific Inc.

Hamilton Company

Tecan Group Ltd.

PerkinElmer Inc.

Beckman Coulter Life Sciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Epson announced development of its first collaborative robot designed for life-science cleanrooms, adding Python scripting and ISO-classified casings.

- May 2025: Persist AI secured USD 12 million Series A to expand its remotely operated formulation lab.

- April 2025: Thermo Fisher launched the Vulcan Automated Lab, integrating robotic wafers and AI for semiconductor-grade analytics.

- March 2025: Alcon agreed to acquire LENSAR for USD 356 million, adding the ALLY Robotic Cataract Laser platform.

Global Laboratory Robotics Market Report Scope

Laboratory robotics is the practice of using robots to perform or assist in various types of laboratory tasks, such as pick/place the sample and the solid additions. They can also heat/cool, mix, shake, and test the samples. While the laboratory robots have found their application in various industries and sciences, the pharmaceutical companies have been using them more than any other industry.

| Drug Discovery |

| Clinical Diagnostics |

| Microbiology Solutions |

| Genomics Solutions |

| Proteomics Solutions |

| Clinical Laboratories |

| Research and Academic Labs |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations |

| Liquid-Handling Robots |

| Sample-Handling / Plate Movers |

| Collaborative Mobile Lab Robots |

| Fully-Integrated Total Lab Automation Cells |

| Pre-analytical Sample Preparation |

| Analytical / Assay Execution |

| Post-analytical Data Management |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Bahrain | |

| United Arab Emirates | |

| Egypt | |

| Rest of Middle East and Africa |

| By Application | Drug Discovery | |

| Clinical Diagnostics | ||

| Microbiology Solutions | ||

| Genomics Solutions | ||

| Proteomics Solutions | ||

| By End-user | Clinical Laboratories | |

| Research and Academic Labs | ||

| Pharmaceutical and Biotechnology Companies | ||

| Contract Research Organizations | ||

| By Robot Type | Liquid-Handling Robots | |

| Sample-Handling / Plate Movers | ||

| Collaborative Mobile Lab Robots | ||

| Fully-Integrated Total Lab Automation Cells | ||

| By Workflow Stage | Pre-analytical Sample Preparation | |

| Analytical / Assay Execution | ||

| Post-analytical Data Management | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Bahrain | ||

| United Arab Emirates | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the laboratory robotics market?

The laboratory robotics market stands at USD 2.64 billion in 2026 and is projected to grow to USD 3.5 billion by 2031.

Which application area is expanding fastest?

Genomics solutions lead growth with an expected 11.05% CAGR as automated next-generation sequencing workflows scale in precision-medicine programs.

Why are contract research organizations investing heavily in laboratory robotics?

CROs adopt flexible, cloud-controlled robotic platforms to meet outsourced assay demand, driving a 9.67% CAGR through 2031.

What robot type is seeing the highest growth rate?

Collaborative mobile lab robots are forecast to rise at 13.22% CAGR because they retrofit existing labs and support modular workflows.

How will new ISO-15189 requirements influence market spending?

Compliance adds validation and infrastructure costs that temporarily slow adoption, particularly for smaller labs, yet ultimately favours vendors with turnkey, standards-ready systems.

Which region will contribute most to future market expansion?

Asia-Pacific will post the fastest 8.18% CAGR as government robotics grants and pharmaceutical capacity growth spur widespread automation uptake.

Page last updated on: