Encoder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

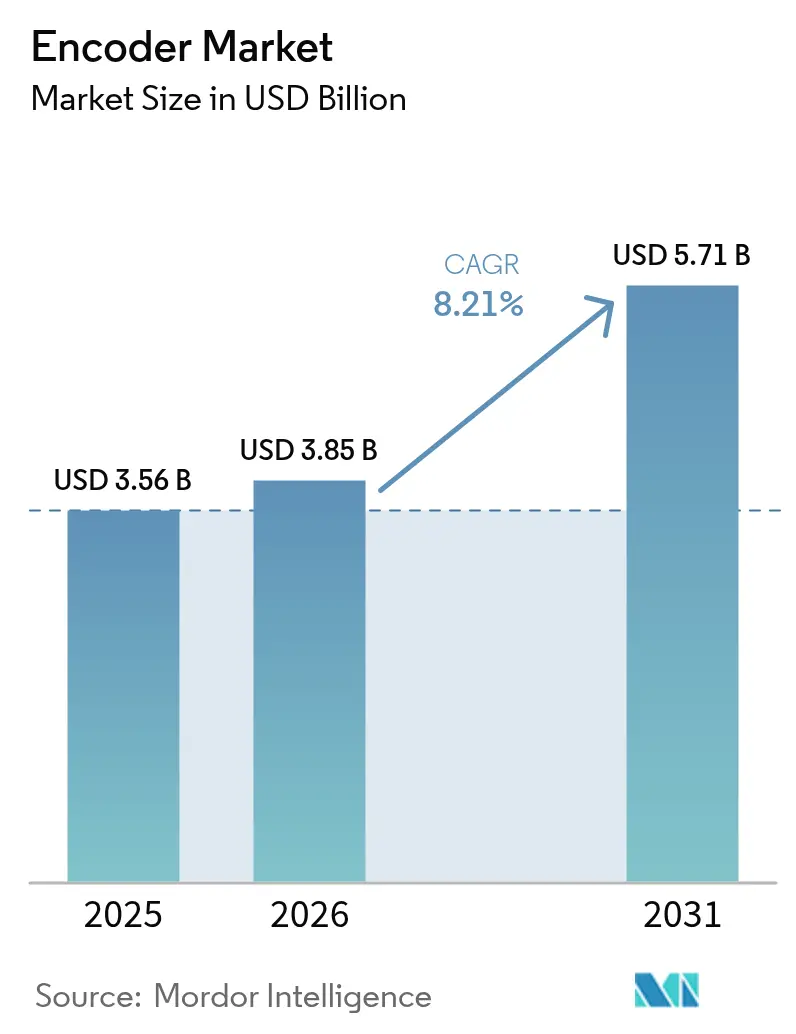

| Market Size (2026) | USD 3.85 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

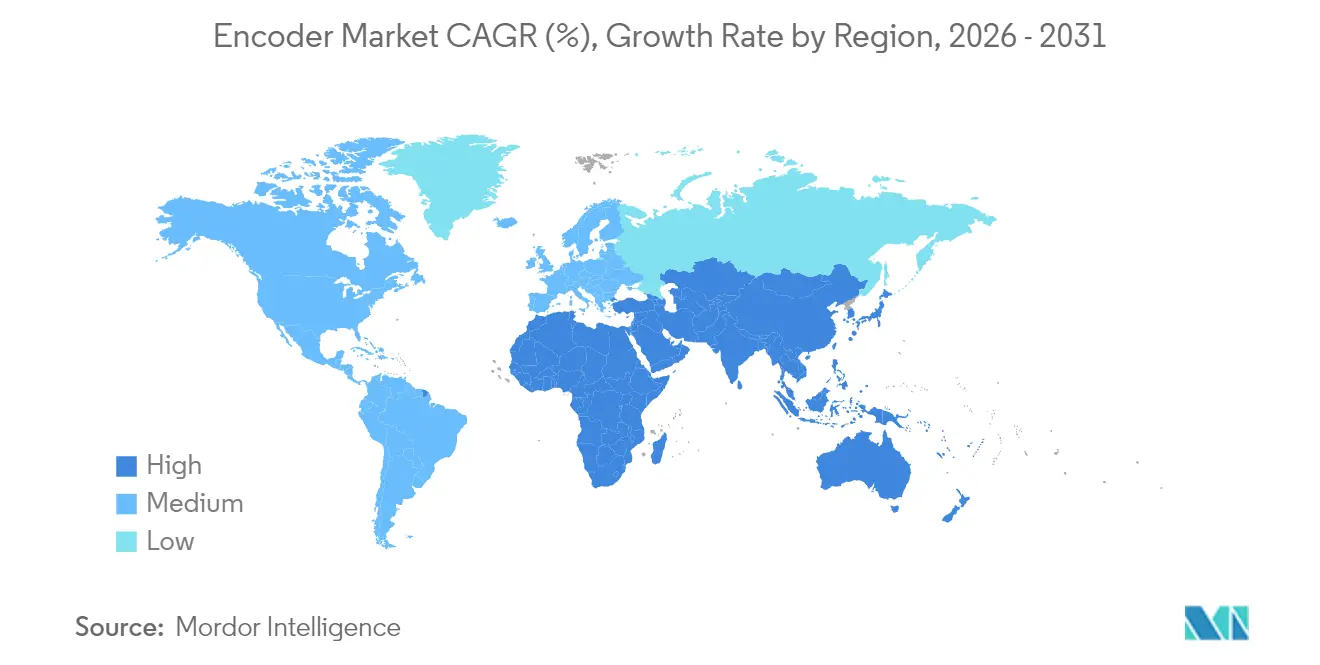

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Encoder Market Analysis by Mordor Intelligence

The encoder market size in 2026 is estimated at USD 3.85 billion, growing from 2025 value of USD 3.56 billion with 2031 projections showing USD 5.71 billion, growing at 8.21% CAGR over 2026-2031. Sustained factory-floor automation, the spread of collaborative robots, and tightening functional-safety rules are the main forces propelling this expansion. Pent-up demand for higher‐resolution feedback is accelerating the migration from incremental to absolute designs, while integrated motor-encoder modules shorten assembly time and improve mean time between failures. Asia-Pacific, led by China, Japan, and India, contributes the largest volume of shipments and also captures the fastest growth rate as regional manufacturers scale precision packaging, electronics, and machine-tool lines. Established European vendors retain leadership in sub-micron optical products, yet rapidly improving magnetic IC solutions from Suzhou and Shenzhen have widened global price competition and nudged many buyers toward hybrid or inductive alternatives.

Key Report Takeaways

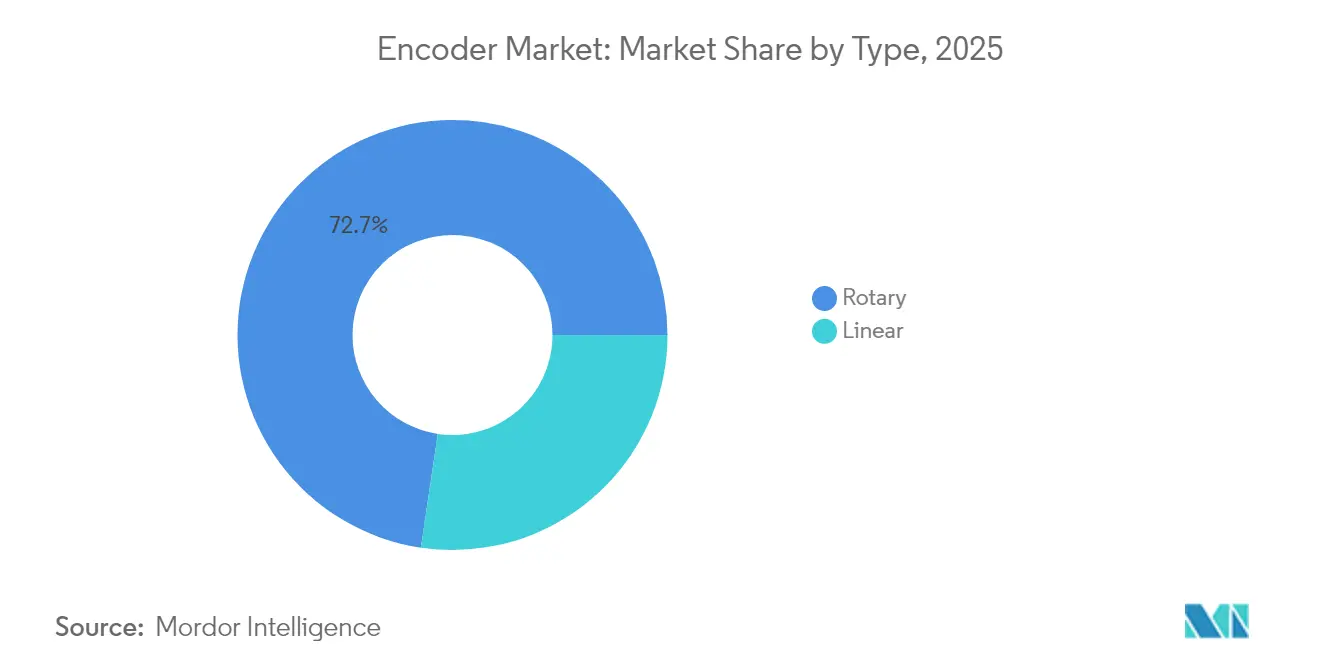

- By product type, rotary devices held 72.65% of encoder market share in 2025; linear encoders record the fastest 7.28% CAGR to 2031.

- By technology, optical systems led with 51.85% revenue in 2025, while magnetic designs post the highest 8.17% growth through 2031.

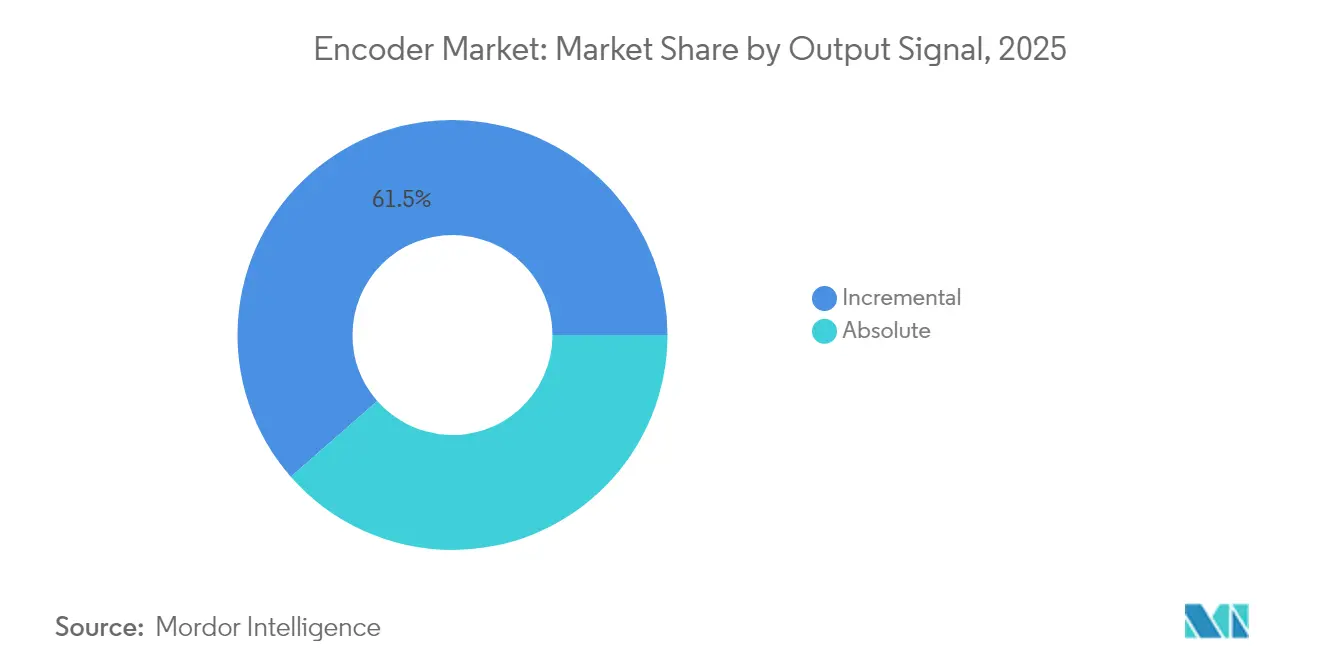

- By output signal, incremental units controlled 61.45% of the encoder market size in 2025, yet absolute encoders expand at 8.62% annually.

- By end-user industry, industrial automation accounted for 38.55% of 2025 revenue; medical devices represent the fastest-growing application at 9.11% CAGR.

- By geography, Asia-Pacific commanded 35.25% of global sales in 2025 and maintains a 9.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Encoder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU collaborative-robot adoption | +0.6% | Western & Northern Europe | Medium term (2-4 years) |

| China smart packaging lines | +0.8% | China, Taiwan | Short term (≤2 years) |

| Japanese SIL 2/3 safety rules | +0.5% | Japan | Long term (≥4 years) |

| India PLI-driven CNC expansion | +0.4% | India | Medium term (2-4 years) |

| US medical-robotics shift to integrated motor-encoder modules | +0.5% | United States | Short term (≤2 years) |

| Semiconductor lithography demand for sub-nanometer feedback | +0.7% | Global tier-1 fabs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EU adoption of collaborative robots

Wider use of cobots in German, French, and Nordic plants requires sub-micron feedback to guarantee safe human-robot interaction. OEMs now specify encoders with 1 nm resolution and ±4 µm system accuracy to meet force-limiting norms, enabling robots to detect the slightest contact and halt within milliseconds. High-resolution absolute optics such as Renishaw’s RESOLUTE line meet these thresholds and support speeds up to 100 m/s, letting automation suppliers increase throughput without compromising worker protection. Broader deployment of ISO / TS 15066-compliant systems is therefore lifting average selling prices across the encoder market even as unit volumes climb [1]Renishaw plc, “RESOLUTE Absolute Encoder System,” renishaw.com .

China’s smart packaging lines

Electronics and pharmaceutical packagers in China run lines that position parts at sub-100 nm tolerances while cycling hundreds of units per minute. Vibration, thermal fluctuation, and airborne particulates force line builders to blend optical scales with rugged housings or shift to inductive formats that still deliver nanometer-grade precision. Each expansion project typically specifies multiple axes of feedback, so growth in this vertical materially raises encoder shipments. Provincial subsidies for fully automated factories amplify demand by lowering capital hurdles for mid-tier manufacturers.

Functional-safety (SIL 2/3) rules in Japanese process industries

Chemical and pharmaceutical sites in Japan must now prove compliance with SIL 2/3 mandates that ensure safe shutdown if any single component fails. Encoders with redundant tracks and built-in diagnostics gain share because they acquire absolute position on power-up and validate signal integrity in real time. The rule set spurs early replacement of legacy incremental units, lengthening the average revenue per installation and bolstering the encoder market in a country already known for high automation density.

PLI-backed CNC machine-tool growth in India

India’s Production Linked Incentive program has mobilized USD 19.3 billion (₹1.61 lakh crore) of committed capital and created over 1.15 million jobs across electronics, medical devices, and automotive lines. CNC builders responding to fresh domestic orders are equipping new spindles and linear motors with high-precision rotary encoders to hold micron-level part tolerances. The resulting uplift in unit demand supports local assembly of encoder subcomponents and entices foreign vendors to increase Indian sourcing [2]Press Information Bureau, “PLI Scheme Generates ₹14 Lakh Crore Production Across 14 Sectors,” pib.gov.in .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dust-induced optical-encoder failures | -0.3% | ASEAN steel & cement corridors | Short term (≤2 years) |

| Low-cost magnetic IC price erosion | -0.4% | Global mid-tier automation | Medium term (2-4 years) |

| US-EU export controls on ultra-precision encoders | -0.2% | Mainland China | Short term (≤2 years) |

| Remaining price premium of absolute encoders | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Optical contamination failures in dust-intensive ASEAN steel mills

Particulate fallout in blast-furnace bays obstructs traditional code discs, leading to sudden position loss and unscheduled outages. Facility managers now pivot toward magnetic or inductive sensing that tolerates debris without sacrificing uptime, curbing replacement demand for optical models and marginally slowing encoder market revenue in heavy-industry niches [3]Baumer Group, “Bearingless Encoders for Harsh Industrial Environments,” baumer.com .

Suzhou & Shenzhen low-cost magnetic IC encoders driving price erosion

Foundry-level advances let Chinese fabless firms offer 10-bit to 12-bit single-chip encoders at fraction-of-legacy prices. General automation customers adopt these parts for conveyors and pick-and-place arms where ultimate resolution is less critical. Greater supply exerts downward pressure on average selling prices worldwide, shrinking gross margins and limiting near-term revenue expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Rotary dominance reinforced by linear acceleration

Rotary devices generated 72.65% of encoder market revenue in 2025 as virtually every servo motor and robot joint needs angular feedback. Their entrenched base, wide shaft-size offerings, and direct compatibility with off-the-shelf drives keep demand buoyant. Linear encoders, however, post a 7.28% CAGR to 2031 as semiconductor steppers, lithography stages, and direct-drive tables prioritise friction-free translation. The encoder market size for linear solutions is set to climb from USD 973.66 million in 2025 to USD 1.48 billion in 2031, propelled by machine-tool builders replacing ball-screw rigs with air-bearing or magnetic levitation slides. Growth in additive manufacturing also favours linear scales that provide closed-loop z-axis control at sub-micron granularity.

Emerging use of enclosed designs such as Renishaw’s FORTiS reduces downtime in coolant-rich machining centres, while ultra-high-vacuum variants capture share in EUV lithography chambers. Although retrofits sustain rotary volumes, new-build capital equipment increasingly incorporates dual sensors—rotary for spindle position and linear for carriage motion raising overall encoder market shipments without cannibalising either sub-category.

By Technology: Optical precision versus magnetic resilience

Optical encoders retained 51.85% revenue in 2025, driven by 1 nm resolution models required in wafer steppers, coordinate-measuring machines, and high-end cobots. The encoder market share for optical units may slip marginally by 2031 as magnetic options cut the historical resolution gap. Magnetic devices expand at an 8.17% CAGR because they withstand oil mist, dust, and wide temperature swings, lowering total cost of ownership in steel, mining, and wind-turbine applications. Battery-free absolute magnetics recently launched by Nidec further widen use cases by eliminating supercapacitors and maintenance cycles .

Capacitive and inductive platforms occupy well-defined niches: capacitive encoders resist electromagnetic interference for MRI beds and semiconductor ion implanters, whereas inductive solutions thrive in food-grade or wash-down zones thanks to fully sealed housings. Suppliers devote R&D dollars to hybrid stacks that blend optical code strips with magnetic reference tracks, handling high axial misalignment without loss of nanometric repeatability. This convergence should keep encoder market differentiation centred on firmware, diagnostics, and connectivity rather than pure sensing physics.

By Output Signal: Absolute gaining momentum over incremental

Incremental encoders led unit shipments in 2025 because PLCs and variable-frequency drives already support quadrature inputs and because the devices cost 15%–20% less. Yet absolute formats record an 8.62% CAGR—outpacing every other category—since users cannot afford post-power-loss homing in lights-out warehouses or surgical theatres. The encoder market size for absolute models is projected to rise from USD 1.37 billion in 2025 to USD 2.25 billion in 2031. Price premiums are falling as single-turn magnetic ASICs integrate multiturn counting through energy harvesting, while high-end optical discs now share photodiode arrays across two tracks to conserve bill of materials.

Next-generation inductive scanning from Heidenhain delivers 22-bit output in a 35 mm flange package, suiting collaborative robots and delta pickers where envelope constraints are strict. As capital equipment budgets increasingly factor downtime into life-cycle cost models, absolute encoders’ ability to start from rest with full positional awareness often justifies the extra upfront expense.

By End-user Industry: Industrial backbone meets medical innovation

Discrete manufacturing captured 38.55% of 2025 revenue, underpinned by automotive, white-goods, and electronics production lines that deploy hundreds of axes per site. Growth remains linked to tightening takt-time targets and higher first-pass yield, both of which benefit from real-time position feedback. The encoder industry finds incremental opportunity in medical devices where surgical robots, CT gantries, and infusion pumps must track movement within sub-millimetre bands. Medical adoption posts a 9.11% CAGR as hospitals in the United States and Western Europe expedite digitised operating suites.

Electric-vehicle drivetrains sustain steady unit pull-through for resolvers and motor-shaft encoders, especially in China where local OEMs ship millions of e-motors annually. Semiconductor manufacturers represent a smaller but high-margin pool because each lithography scanner can embed more than 120 linear and rotary encoders, many priced far above commodity levels. Across these verticals, integration with industrial Ethernet protocols and predictive-maintenance firmware emerges as a key differentiator.

Geography Analysis

Asia-Pacific led with 35.25% of global revenue in 2025 and sustains a 9.45% CAGR through 2031. Chinese policy backing for smart factories and compound-semiconductor fabs continues to funnel encoder orders into coastal provinces. Japan’s installed robot base exceeds 420 units per 10,000 workers, keeping demand resilient for SIL-rated feedback components that fit legacy servo footprints. India’s PLI tranche drives the fastest incremental gains, with encoder call-offs attaching to new CNC, PCB, and medical-device lines financed under the scheme. The encoder market size in Asia-Pacific therefore moves from USD 1.26 billion in 2025 toward USD 2.16 billion in 2031.

North America and Europe together represent roughly half of 2025 turnover, powered by aerospace, medical robotics, and precision machining. The United States anchors clinical-grade demand: Johnson & Johnson MedTech’s OTTAVA™ surgical platform integrates ultra-compact optical encoders on every robotic arm to secure sub-millimetre repeatability. German and Swiss suppliers export high-accuracy scales worldwide, cementing Europe’s role as an innovation hub even as unit volumes migrate East. EU subsidies for collaborative-robot deployment channel revenue toward 1 nm-class feedback solutions, lifting average selling price across the region.

Latin America and the Middle East & Africa remain smaller contributor regions yet post steady single-digit growth as brownfield plants retrofit automated conveyors, palletisers, and bottling lines. Brazilian auto assemblers and Mexican Tier-1 suppliers now add magnetic encoders to motor drives as part of broader Industry 4.0 overhauls. Gulf-state oil producers specify ruggedised inductive and magnetic designs rated to 125 °C ambient and certified for Class 1 Div 2 zones. This uptake diversifies the global encoder market and cushions suppliers against cyclical slowdowns in any one geography.

Competitive Landscape

The battle for share remains open, with no single firm exceeding 15% of global revenue. European leaders such as Renishaw, Heidenhain, and Baumer protect high-precision niches by rolling out multi-protocol digital outputs, functional-safety variants, and self-monitoring firmware. Japanese conglomerates Omron and Panasonic focus on mechatronic integration that shortens commissioning time for OEM clients. Meanwhile, Chinese challengers including Shanghai SICK, HONTKO, and several Suzhou IC houses flood the mid-tier automation space with 12-bit magnetic SoC products that cut bill-of-materials costs by 30% compared with traditional optical units.

Strategic moves increasingly hinge on ecosystem partnerships. Heidenhain co-develops inductive scanning arrays with drive-maker Siemens to embed high-bandwidth position feedback directly inside servo housings. Renishaw collaborates with metal-3D-printing firms to feed real-time stage data into melt-pool control loops, raising build quality and opening a lucrative after-market calibration service. Nidec aligns its new battery-free magnetic encoder with in-house servo motors, pitching a unified motion stack that eliminates backup power modules.

White-space opportunities centre on predictive-maintenance analytics. Vendors that harvest error signal statistics, vibration signatures, and temperature drift can warn plant engineers of impending encoder failure several weeks in advance. Adding this layer of insight lets suppliers sell software subscriptions that compound revenue and differentiate hardware that is otherwise at risk of commoditisation. The encoder market therefore shifts from mere component supply toward integrated motion-intelligence platforms.

Encoder Industry Leaders

Omron Corporation

Dr. Johannes Heidenhain GmbH

Rockwell Automation Inc.

Honeywell International

Pepperl+Fuchs SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- undefinedApr 2025: Nidec introduced battery-free magnetic encoders for its servo motors, eliminating backup power while retaining absolute position information .

- undefinedNov 2024: Johnson & Johnson MedTech received FDA clearance for the OTTAVA™ robotic surgical system that embeds high-precision encoders to enhance surgical workflow.

- February 2024: Heidenhain unveiled next-generation inductive scanning technology that lowers signal noise and boosts resolution for factory-automation tasks.

- January 2024: Renishaw expanded the RESOLUTE family with Functional-Safety variants certified for SIL 2/3 applications

Global Encoder Market Report Scope

Encoders are components added to a direct current motor to convert the mechanical motion into digital pulses that integrated control electronics can interpret. The main purpose of encoders is to transform information from one format to another for standardization, speed adjustment, or safety control.

The encoder market is segmented by type (rotary and linear), technology (optical, magnetic, and photoelectric), end-user industry (automotive, electronics, textile, printing machinery, industrial, and medical), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Rotary |

| Linear |

| Optical |

| Magnetic |

| Capacitive |

| Inductive |

| Other Technologies |

| Incremental |

| Absolute |

| Automotive |

| Electronics and Semiconductor |

| Industrial |

| Textile |

| Printing Machinery |

| Medical Devices |

| Energy and Power |

| Aerospace and Defense |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Rotary | |

| Linear | ||

| By Technology | Optical | |

| Magnetic | ||

| Capacitive | ||

| Inductive | ||

| Other Technologies | ||

| By Output Signal | Incremental | |

| Absolute | ||

| By End-user Industry | Automotive | |

| Electronics and Semiconductor | ||

| Industrial | ||

| Textile | ||

| Printing Machinery | ||

| Medical Devices | ||

| Energy and Power | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Encoder Market?

The Encoder Market size is expected to reach USD 3.85 billion in 2026 and grow at a CAGR of 8.21% to reach USD 5.71 billion by 2031.

What is the current Encoder Market size?

In 2026, the Encoder Market size is expected to reach USD 3.85 billion.

Who are the key players in Encoder Market?

Omron Corporation, Honeywell International, Schneider Electric, Rockwell Automation Inc. and Panasonic Corporation are the major companies operating in the Encoder Market.

Which is the fastest growing region in Encoder Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What years does this Encoder Market cover, and what was the market size in 2025?

In 2025, the Encoder Market size was estimated at USD 3.85 billion. The report covers the Encoder Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Encoder Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: