Rice Syrup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

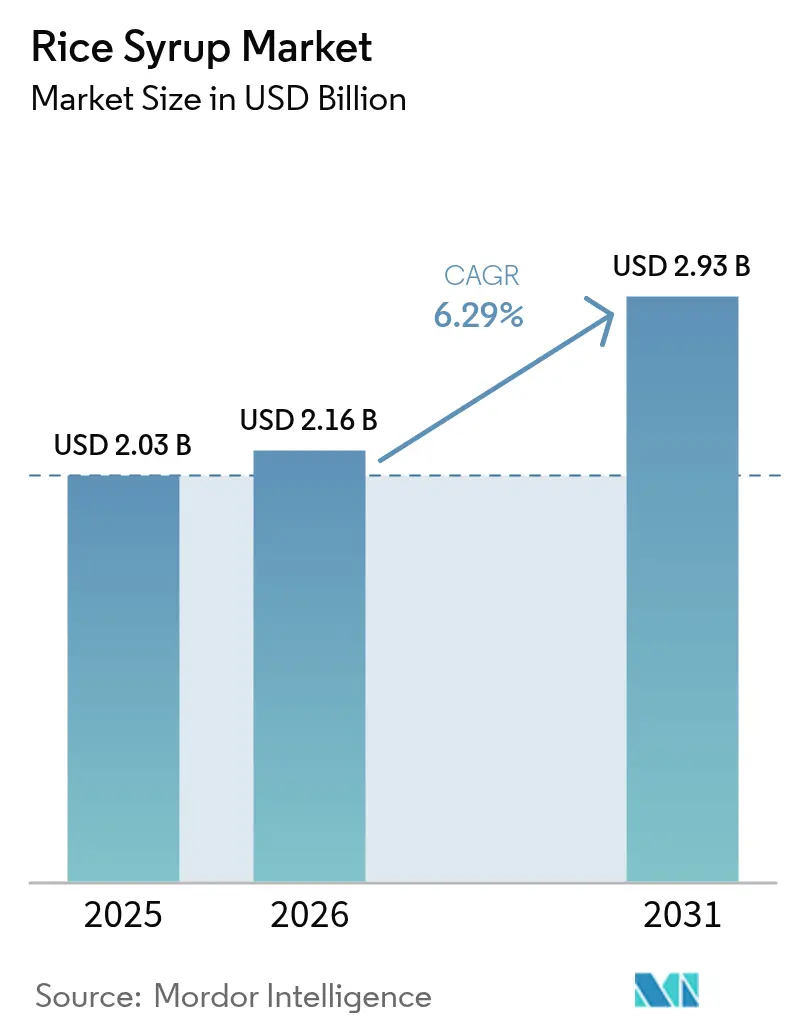

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.93 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rice Syrup Market Analysis by Mordor Intelligence

The rice syrup market size is expected to grow from USD 2.03 billion in 2025 to USD 2.16 billion in 2026 and is forecast to reach USD 2.93 billion by 2031 at 6.29% CAGR over 2026-2031. Rising regulatory scrutiny of synthetic sweeteners, stronger clean-label rules, and consumer preference for ingredients perceived as natural are widening the addressable base for rice-derived sweeteners in beverages, baked goods, infant nutrition, and plant-based dairy. Europe remains the largest regional demand center, reflecting the region’s tight additive regulations and premium organic consumption, while North America is recording the fastest growth as reform of the Food and Drug Administration (FDA) definitions for “healthy” claims pushes formulators toward non-artificial options. Brown rice syrup continues to dominate formulation share because its bran layer delivers trace minerals, antioxidants, and a lower glycemic response than corn-based syrups. The conventional category commands volume leadership due to cost advantages, yet certified-organic variants are scaling rapidly after the United States Department of Agriculture (USDA)’s Strengthening Organic Enforcement rule added digital traceability for imported organic inputs. Supply-side inflation persists amid volatile paddy prices, but advances in non-thermal bran stabilization and high-efficiency enzyme hydrolysis are trimming conversion losses and improving solids yield, thereby softening raw-material risk for processors.

Key Report Takeaways

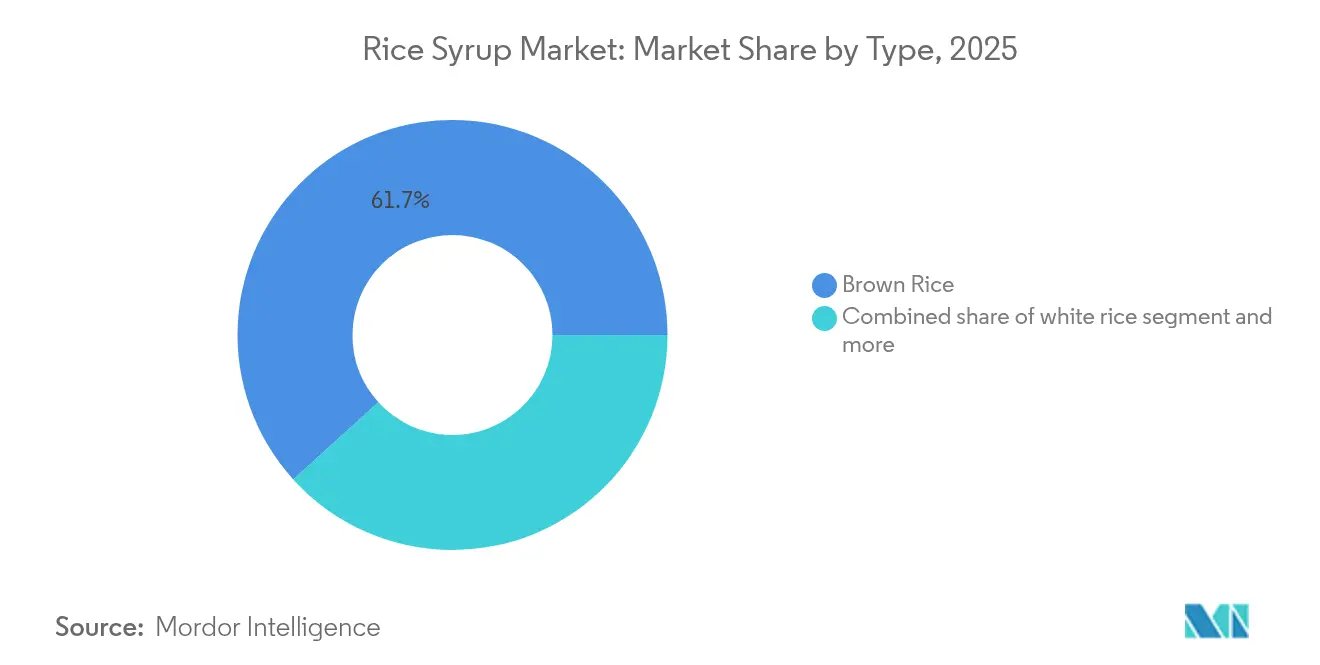

- By rice type, brown rice held 61.72% of the rice syrup market share in 2025; brown rice is projected to post the quickest segment CAGR of 8.45% through 2031.

- By category, the conventional segment led with 56.58% revenue share in 2025, while organic variants are forecast to expand at 7.08% CAGR between 2026-2031.

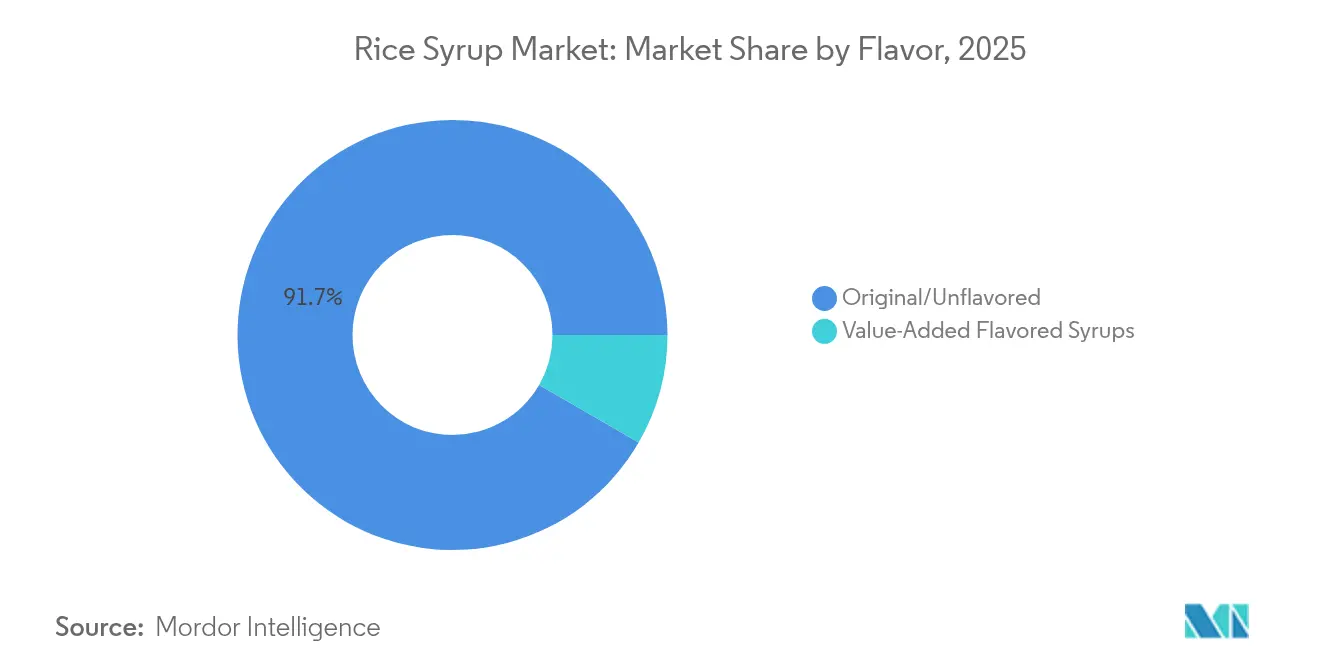

- By flavor, original/unflavored formulations accounted for 91.66% of the rice syrup market size in 2025; value-added flavored syrups will register an 8.01% CAGR to 2031.

- By application, bakery and confectionery represented 37.86% of the rice syrup market size in 2025; infant formula and baby foods are expected to grow at 7.02% CAGR through 2031.

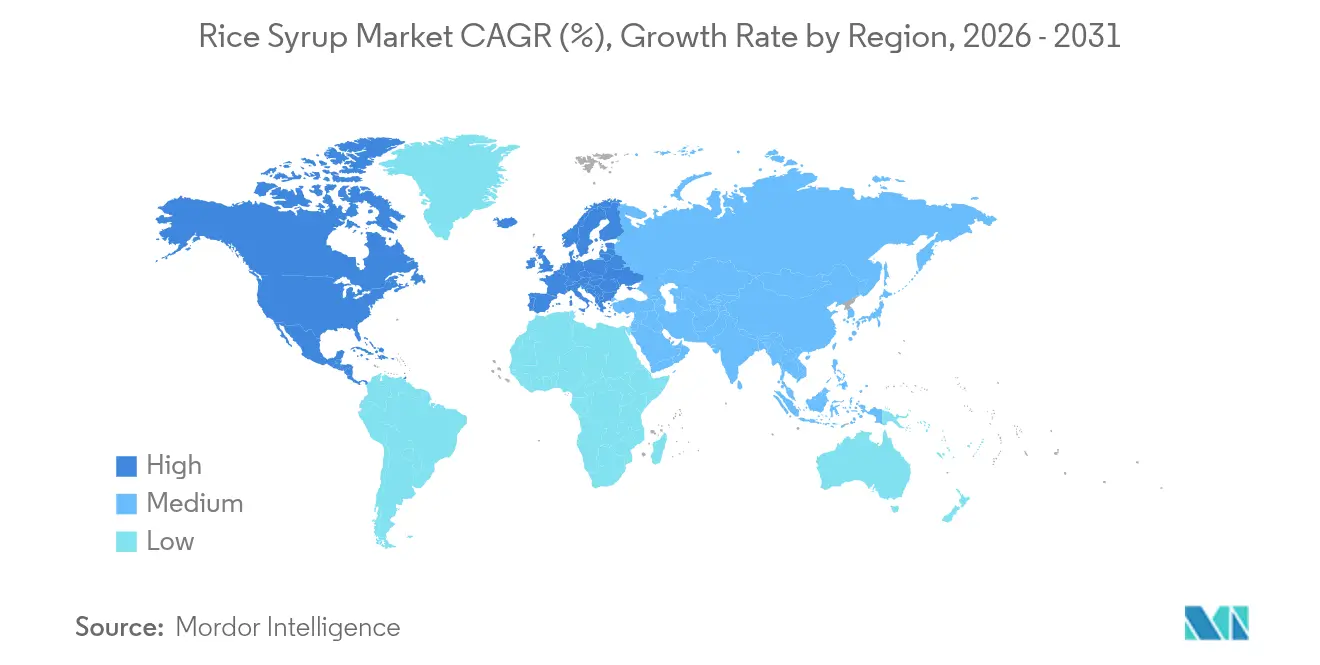

- By geography, Europe dominated with 34.12% value share in 2025; North America is projected to post the highest regional CAGR of 8.21% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rice Syrup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural sweeteners in beverage formulations | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing use in organic baby food products worldwide | +1.2% | North America and Europe core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Expanding demand for allergen-free sweeteners | +1.40% | Global, particularly strong in developed markets | Short term (≤ 2 years) |

| Growth in plant-based dairy alternatives using rice syrup | +0.9% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Wide application in clean-label baked goods and snacks | +1.1% | Global | Short term (≤ 2 years) |

| Rising use in confectionery as a non-GMO sweetening solution | +0.8% | Global, with premium segment focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural Sweeteners in Beverage Formulations

Brand owners are reformulating ready-to-drink teas, flavored waters, and functional beverages ahead of the 2025 Food and Drug Administration (FDA) “healthy” claim overhaul that lowers added-sugar thresholds, prompting substitution of high-fructose corn syrup with enzymatically produced rice syrup[1]Source: Federal Register, " FDA's Revised "Healthy" Claim Guidelines Impact Sugar Content Requirements", www.federalregister.gov. Germany, France, and the United Kingdom collectively raised imports of HS 1702.30 rice-based sweeteners from USD 631 million in 2022 to USD 677 million in 2023, underscoring momentum in craft beverage channels according to CBI (Centre for the Promotion of Imports from developing countries)[2]Source: CBI (Centre for the Promotion of Imports from developing countries), "Imports of rice-based sweeteners", www.cbi.eu. Cargill's SimPure soluble rice flour, honored with a 2023 Edison Award, illustrates how ingredient suppliers are offering one-for-one maltodextrin replacements that carry a clean-label halo. The neutral flavor of rice syrup enables formulators to achieve consistent sweetness without masking botanicals, and its relatively high dextrose-equivalent range supports rapid fermentability in low-alcohol applications. The growing consumer preference for natural and clean-label ingredients has positioned rice syrup as a preferred alternative in beverage formulations. Additionally, the versatility of rice syrup in various applications, from sports drinks to kombucha, has expanded its market potential across different beverage categories.

Increasing Use in Organic Baby Food Products Worldwide

Parents prioritizing traceable ingredient origins are gravitating to baby purées and infant cereals sweetened with rice syrup that comply with United States Department of Agriculture (USDA) organic and European Union Regulation 2023/476 standards [3]Source: U.S Department of Agriculture, "Rice syrup that complies with USDA organic and EU Regulation", www.ams.usda.gov. Electronic NOP import certificates introduced in March 2024 raised entry barriers for synthetic or ambiguously sourced sweeteners, concentrating share among certified rice syrup suppliers with transparent chain-of-custody documentation. Food and Drug Administration (FDA) rules under 21 CFR 106 require formula makers to validate carbohydrate quality and allergen control, and rice syrup's single-crop provenance simplifies compliance auditing. WIC nutrition-package revisions that emphasize culturally relevant produce and flexible sweetening sources further underpin demand for organic, hypoallergenic sugars in early-childhood SKUs. The implementation of these stringent regulations has led to increased adoption of rice syrup in infant formula manufacturing, particularly in developed markets. Additionally, the growing consumer preference for clean-label products has strengthened rice syrup's position as a natural sweetening alternative in the food and beverage industry.

Expanding Demand for Allergen-Free Sweeteners

Under European Union Regulation (EU) 2024/1033, the expansion of eight-allergen labeling has intensified manufacturers' focus on gluten-free carbohydrates. This shift positions rice syrup as a compliant solution for multiple allergens. In June 2025, Axiom Foods clinched the inaugural Food and Drug Administration (FDA) Generally Recognized as Safe (GRAS) notice for rice protein (GRN 1073), bolstering trust in rice-derived macronutrients. This move also paves the way for syrup variants in medical nutrition. Healthcare providers and K-12 foodservice operators are ramping up rice syrup usage, especially where avoiding cross-contamination with soy, dairy, or wheat is crucial. These regulatory nods have spurred food manufacturers to adopt rice syrup as a primary sweetener in their reformulations. Furthermore, heightened consumer awareness about allergen-free products has unveiled fresh avenues for rice syrup in niche dietary markets. The adaptability of rice syrup due to clean-label appeal is viable, across food applications, from beverages to confections, underscores rice syrup's burgeoning potential in diverse industry segments. The increasing demand for plant-based and vegan-friendly ingredients further supports the growth of rice syrup in the food industry. Additionally, the rising trend of clean eating and transparency in food labeling has amplified the preference for rice syrup as a natural sweetener.

Growth in Plant-Based Dairy Alternatives Using Rice Syrup

Oat, almond, and pea-based "milks" leverage rice syrup for balanced sweetness and mouthfeel that supports foam stability in barista formats. Cargill invested EUR 38 million in soluble-fiber lines that help brand owners meet 30% sugar-reduction targets while maintaining label simplicity, pairing fibers with low-DE rice syrup for bulking. USDA organic processing rules under 7 CFR 205.270 accept enzymatic hydrolysis, allowing certified-organic rice syrup to serve as the primary carbohydrate in dairy-free yogurt bases. The versatility of rice syrup in plant-based applications has led manufacturers to increase their production capacity to meet rising demand. Food manufacturers are increasingly incorporating rice syrup as a natural sweetener alternative in response to consumer preferences for clean-label products. The compatibility of rice syrup with organic certification requirements has positioned it as a preferred ingredient in the expanding organic food segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from other natural sweeteners | -1.3% | Global, particularly in price-sensitive segments | Short term (≤ 2 years) |

| Higher production costs compared to synthetic sweeteners | -0.9% | Global, with greater impact in developing markets | Medium term (2-4 years) |

| Vulnerability to rice price fluctuations in global markets | -0.9% | Global, with acute impact in Asia-Pacific rice-dependent regions | Short term (≤ 2 years) |

| Limited sweetness compared to high fructose corn syrup | -0.8% | Global, most pronounced in cost-sensitive beverage applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Other Natural Sweeteners

The rice syrup market faces growing constraints due to competition from various natural sweeteners, as manufacturers and end-users seek affordable ingredients that align with consumer preferences. Tate & Lyle completed its USD 1.8 billion acquisition of CP Kelco in June 2024, augmenting its stevia, allulose, and pectin capabilities and escalating price-performance pressure on rice syrup solutions. AGRANA simultaneously expanded isoglucose capacity in Europe, enabling customers to switch to lower-cost glucose syrups where the functional contribution of rice syrup is marginal. These moves are eroding negotiating leverage for smaller rice syrup specialists that cannot match the bundled ingredient portfolios of diversified sweetener suppliers. The consolidation trend has intensified competition in the rice syrup segment, particularly affecting regional manufacturers with limited product portfolios. Market participants are increasingly focusing on developing specialized rice syrup formulations to maintain their competitive edge. The shifting landscape has prompted rice syrup manufacturers to explore strategic partnerships and value-added product development to sustain their market position. The emergence of alternative sweeteners and increasing price sensitivity among end-users has further challenged rice syrup manufacturers' market share. Small and medium-sized rice syrup producers face mounting pressure to differentiate their offerings through unique formulations and applications. Regional players are experiencing margin compression due to the expanding presence of global sweetener manufacturers in local markets.

Higher Production Costs Compared to Synthetic Sweeteners

The production costs of rice syrup remain higher than synthetic sweeteners due to raw material price fluctuations, complex processing requirements, and supply chain challenges, affecting its market competitiveness. A January 2024 El Niño-linked supply squeeze lifted Japanese rice prices by 80%, forcing Tokyo to release emergency stocks and demonstrating the volatility embedded in agricultural feedstocks. Rabobank projects stocks-to-use ratios for the global rice balance sheet to keep tightening through 2033/34, underscoring persistent cost pressure for syrup processors reliant on imported paddy. Synthetic corn syrups, derived from relatively abundant U.S. dent corn, continue to undercut rice syrup on delivered-solids cost, a gap that widens in freight-inflated emerging markets. The increasing frequency of extreme weather events threatens rice cultivation patterns and yield stability across major producing regions. Limited processing capacity and specialized equipment requirements create barriers to entry for new manufacturers in the rice syrup segment. Regional trade restrictions and protectionist policies further compound supply chain uncertainties for international rice syrup producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rice Type: Brown Rice Dominance Drives Premium Positioning

Brown rice syrup accounted for 61.72% of 2025 volume as bakers and infant-food formulators embraced its intact bran-layer micronutrient profile. The high nutritional content and natural composition make it particularly appealing for health-conscious consumers seeking clean-label alternatives. That breakthrough allows producers to extend storage life and press toward cost parity with white rice while preserving flavor neutrality. White rice syrup remains a mainstay in legacy confectionery lines due to mature supply chains and lower unit costs but trails in growth because marketing teams prioritize the more "whole-grain" proposition of brown variants. The established processing infrastructure and economies of scale continue to make white rice syrup an economically viable option for traditional applications. Specialty pigmented cultivars such as black and red rice are beginning to seed hyper-niche launches in sports gels and antioxidant-rich spreads, yet their cumulative share of the rice syrup market is below 2% in 2025. These specialty variants command premium pricing due to limited availability and specialized processing requirements.

In the forward window, projected 8.45% CAGR for brown rice reflects alignment with wellness framing in developed markets and extended-shelf-life wins in emerging ASEAN bakeries adopting clean-label dough conditioners. The growing consumer preference for natural ingredients has accelerated the adoption of brown rice syrup in premium food applications. Producers are broadening raw-material origination to Vietnam and Thailand where mechanized harvesting is lowering foreign-matter counts and moisture variability. The implementation of advanced harvesting technologies has significantly improved quality consistency and reduced processing costs. This diversification reduces overdependence on Japanese and Korean crop cycles that historically dictated spot-price spikes. The expanded sourcing network has enhanced supply chain resilience and stabilized pricing throughout the year.

By Category: Organic Growth Accelerates Despite Conventional Leadership

The conventional stream delivered 56.58% of 2025 global volume but ceded incremental share to certified-organic syrups that earned a 7.08% forecast CAGR after the United States Department of Agriculture (USDA)'s March 2024 digital traceability directive strengthened label integrity. The shift towards organic certification has reshaped market dynamics, particularly in developed regions where regulatory compliance is stringent. Consumer awareness regarding food safety and clean-label products has further accelerated this transition. Organic up-trading is particularly evident in baby foods and premium granola clusters, where consumers tolerate 20-30 bps price lifts for pesticide-free claims. The demand for organic variants in these premium segments continues to grow as manufacturers emphasize health and wellness positioning. While organic rice trades at premia of USD 110-135/ton over conventionally grown paddy, downstream processors recover margin through recipe optimization—cutting dosage by 2-3 g per 100 g due to the higher maltose ratio typical of organic enzymatic profiles.

Global processors are investing in vertically integrated organic estates in Thailand's Northeast Corridor that offer dual cropping for rice and mung beans, thereby diluting fixed overhead per hectare and lowering per-ton carbon intensity. These investments demonstrate the industry's commitment to sustainable agriculture and supply chain optimization. The integration of dual-cropping systems has emerged as a key strategy for cost management and environmental sustainability. The rice syrup industry is also piloting blockchain-anchored audit trails that link paddy lot IDs to finished-goods batches, creating digital provenance records that satisfy EU Regulation (EU) 2023/1542 on deforestation-free supply chains. The implementation of blockchain technology has enhanced transparency and traceability throughout the supply chain. This digital transformation has strengthened consumer trust and regulatory compliance in the market.

By Flavor: Value-Added Innovation Challenges Traditional Dominance

Original/unflavored solutions still supplied 91.66% of output in 2025 because their neutral taste profile carries over into sauces, nutritional bars, and RTD coffees without sensory interference. The versatility of unflavored rice syrups makes them a preferred choice for manufacturers seeking clean-label sweetening solutions. Their ability to maintain product stability across various applications has established them as a cornerstone ingredient in food processing. The value-added flavored rice syrup segment is projected to grow at a CAGR of 8.01% through 2031. This growth is attributed to increasing consumer demand for distinctive flavor profiles and natural botanical infusions, including ginger, matcha, and cacao nib macerates. The growing consumer interest in unique flavor experiences has accelerated the development of botanical-infused variants. The natural extraction methods ensure product authenticity while meeting clean-label requirements. Manufacturers are extracting essential oils via super-critical CO₂ and integrating them at dosing rates below 0.2%, thus preserving organic certification under National List 205.605.

Flavored-syrup marketers emphasize provenance storytelling—such as Yunnan jasmine or Sri Lankan cinnamon—to justify retail pricing that can exceed conventional rice syrup by 60%. The premium positioning strategy has successfully captured the attention of quality-conscious consumers. The emphasis on geographical origin has created a new value perception in the specialty sweetener segment. Formulators of specialty pancake syrups, kombucha bases, and artisanal gelato are early adopters, although scale remains modest because compatibility testing must verify that flavor compounds do not precipitate during high-temperature pasteurization. Over the outlook period, co-creation partnerships with craft chocolatiers and micro-breweries will likely unlock new demand pockets for value-added variants.

By Application: Infant Formula Emergence Reshapes Growth Dynamics

Bakery and confectionery dominated with 37.86% market value share in 2025, as rice syrup's humectant properties maintain soft crumb structures and extend ambient shelf life. The ingredient's natural preservation capabilities make it particularly valuable for artisanal bakeries seeking clean-label solutions. Its ability to enhance texture while providing consistent moisture retention has made it indispensable in premium confectionery manufacturing. Infant formula and baby food manufacturers are projected to achieve a 7.02% CAGR as the Food and Drug Administration (FDA) strengthens transparency requirements under 21 CFR 105.65, compelling brands to list unambiguous carbohydrate sources. The implementation of these regulations has accelerated the adoption of rice syrup as a trusted ingredient in infant nutrition.

Asia-Pacific multinationals are reformulating traditional maltodextrin-based weaning snacks using low-DE rice syrup to address increasing cross-border ecommerce scrutiny of additive content. This shift reflects a broader industry trend toward cleaner labels and natural ingredients. Secondary applications in nutraceutical chews and gummy vitamins are expanding as formulators leverage rice syrup's low viscosity to achieve rapid depositor throughput without added glycerol. The versatility of rice syrup has made it an attractive option for manufacturers seeking to optimize production efficiency. Pharmaceutical excipient producers are evaluating rice syrup as a hypoallergenic binder for orally dissolving films. The growing demand for allergen-free medications has positioned rice syrup as a viable alternative in pharmaceutical formulations.

Geography Analysis

Europe retained a 34.12% revenue lead in 2025 by virtue of conservative additive approvals and the region’s USD 54 billion organic packaged-food spend, locking in a loyal base for plant-based sweeteners. European Food Safety Authority (EFSA)’s layered risk-assessment pipeline often spans six years, so incumbent natural sweeteners such as rice syrup enjoy a moat while synthetic rivals await dossier reviews. Germany, France, and the United Kingdom collectively imported 149,000 metric tons of rice-derived glucose under HS 1702.30 in 2024, reflecting robust demand in bakery centers clustered around Hamburg, Paris, and Manchester. Mid-sized European private-label chocolatiers are installing vacuum-cooker lines optimized for rice syrup, citing 3-point moisture reductions versus corn syrup for the same Brix level, thus enabling cleaner tempering curves.

North America recorded the fastest expansion, with the rice syrup market expected to post an 8.21% CAGR through 2031. Food and Drug Administration (FDA) plans to phase out petroleum-based artificial colors by 2026, and the agency’s rebasing of Generally Recognized As Safe (GRAS) self-affirmations is steering formulators toward proven botanical sweeteners. U.S. rice imports climbed to a record 47.0 million hundredweight in 2025, indicating wider adoption of jasmine and basmati types favored in premium syrup conversions. Ingredient majors such as ADM and Cargill are repurposing Midwest corn-wet-milling tanks for rice substrate enzymolysis, cutting trucking miles and shrinking CO₂ footprints.

Asia-Pacific presents latent upside given abundant paddy supply but still accounts for less than 18% of global turnover because quality-assurance systems are uneven. Thailand’s Office of Agricultural Economics projects a 5% rebound in 2025/26 paddy output as El Niño recedes, offering processors an opportunity to secure competitively priced feedstock provided they invest in post-harvest drying infrastructure. South American bakeries, led by Brazil, are exploring rice syrup as an egg-free sponge cake humectant to sidestep volatile shell-egg pricing, while Middle East and Africa demand is concentrated among Dubai-based confectioners supplying travel retail. Across emerging regions, adoption will hinge on technical assistance that equips small and mid-sized food plants to manage higher-viscosity syrup streams without fouling legacy pumps.

Competitive Landscape

The rice syrup market sits at a moderate concentration level. Global agrifood majors such as Archer-Daniels-Midland Company, Austrade Inc., Wuhu Deli Foods Co., Ltd., and Gulshan Polyols Ltd., Gulshan Polyols Ltd. among others, control advantaged origination networks and enzyme expertise, enabling them to undercut regional independents on delivered-solids cost. Vertical integration strategies include direct rice-paddy contract farming and in-house maltogenic amylase development, giving leaders pricing agility during commodity spikes.

Mid-tier specialists—California Natural Products, Lundberg Family Farms, and Nature’s Crops—concentrate on certified-organic or whole-grain derivatives that fetch premiums in infant nutrition and keto granola niches. Many lack the scale to shoulder volatile freight or currency swings, so they hedge exposure through multi-origin sourcing from Arkansas, Pakistan, and Cambodia.

Technological differentiation is accelerating. Japanese processors are rolling out electron-beam irradiation tunnels that deactivate residual lipase without elevating Maillard compounds, improving flavor stability in brown rice syrup destined for ready-to-drink coffee. Chinese equipment vendors are showcasing continuous-vacuum evaporators capable of achieving 83° Brix at 40 °C, minimizing hydrolytic browning and preserving the light color demanded by beverage formulators. Strategically, incumbents are acquiring micro-startups with IP in flavor-infused syrups to secure early access to proprietary maceration techniques.

Rice Syrup Industry Leaders

-

Archer-Daniels-Midland Company

-

Austrade Inc.

-

Wuhu Deli Foods Co., Ltd.

-

Gulshan Polyols Ltd.

-

Pioneer Industries Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2023: LT Foods' subsidiary Nature Bio Foods has established an organic rice processing facility in Uganda, its first plant in Africa. The facility enables direct sourcing from East African farmers, enhancing supply chain traceability and supporting local agricultural communities. The plant processes and exports organic rice to European and US markets, supporting LT Foods' expansion of its organic product portfolio.

- October 2022: Austrade Inc. launched organic rice sweeteners to address the demand for clean-label, non-GMO, and allergen-friendly sweetening solutions. The company's new product line includes organic brown rice syrup, clarified rice syrup, and high-maltose rice syrup for use in snacks, beverages, bakery items, and nutritional products. The rice sweeteners enhance texture and moisture retention while providing a mild, neutral taste.

- September 2021: Nature Bio Foods BV, a subsidiary of LT Foods, has opened an organic food processing plant in Rotterdam, Netherlands. The facility processes organic rice, rice-based products including syrups, and other foods through cleaning, grading, and packaging operations. The plant strengthens the company's European market presence and supply chain capabilities by providing traceable organic products near customer locations.

Global Rice Syrup Market Report Scope

Rice syrup is made by fermenting the rice and subjecting it to natural enzymes, which turns the starch present in the rice into sugar. The liquid produced through this procedure is then heated and turned into syrup.

The scope of the market is segmented by rice type, origin, application, and geography. For each segment, the market sizing and forecast have been done on the basis of value (in USD million).

| Brown Rice |

| White Rice |

| Others |

| Conventional |

| Organic |

| Original/Unflavored |

| Value-Added Flavored Syrups |

| Bakery and Confectionery |

| Beverages |

| Dairy and Dessert Products |

| Infant Formula and Baby Foods |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Rice Type | Brown Rice | |

| White Rice | ||

| Others | ||

| By Category | Conventional | |

| Organic | ||

| By Flavor | Original/Unflavored | |

| Value-Added Flavored Syrups | ||

| By Application | Bakery and Confectionery | |

| Beverages | ||

| Dairy and Dessert Products | ||

| Infant Formula and Baby Foods | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the rice syrup market?

The global rice syrup market is valued at USD 2.16 billion in 2026 and is projected to reach USD 2.93 billion by 2031, reflecting a 6.29% CAGR.

Which region leads the rice syrup market?

Europe holds the largest regional share at 34.12% in 2025, driven by stringent additive regulations and high organic-food consumption.

Why is brown rice syrup gaining share?

Brown rice syrup retains bran micronutrients and antioxidants, enabling premium positioning and supporting an expected 8.45% CAGR through 2031.

What is driving organic rice syrup growth?

The USDA’s Strengthening Organic Enforcement rule improves supply-chain transparency, boosting consumer trust and propelling a 7.08% CAGR for organic variants.

What production technologies are improving cost efficiency?

Cold-plasma bran stabilization and continuous-vacuum low-temperature evaporation cut enzymatic degradation and energy use, trimming unit costs for processors.

Page last updated on: