Cocoa And Chocolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

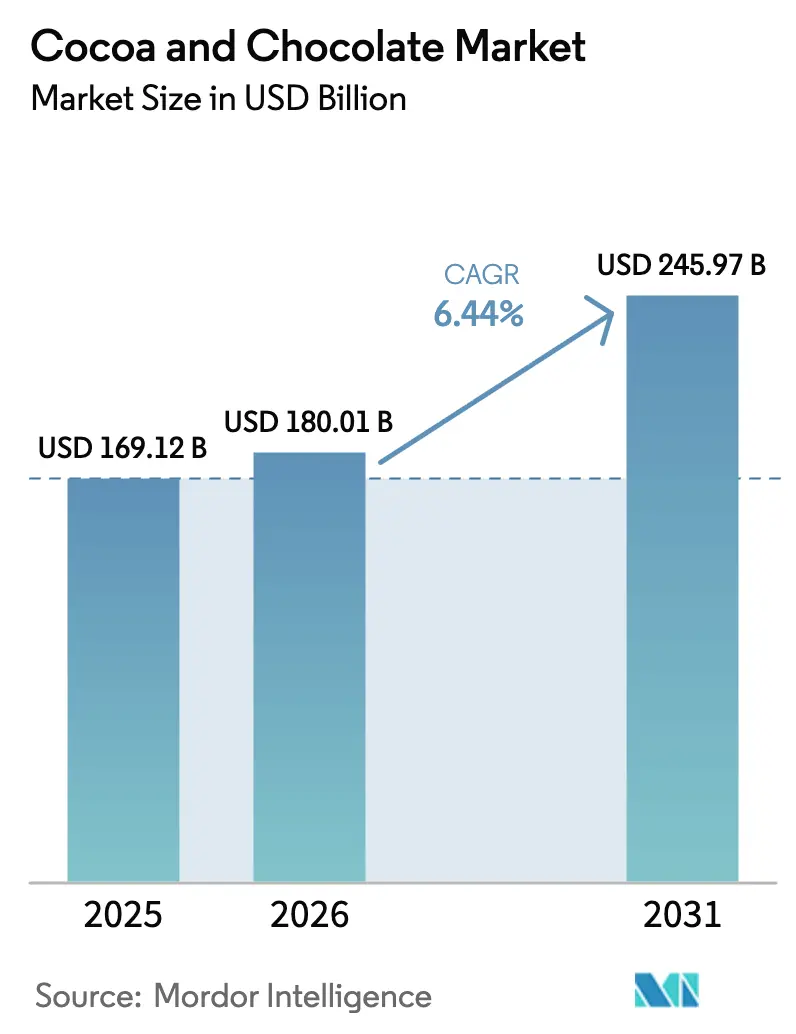

| Market Size (2026) | USD 180.01 Billion |

| Market Size (2031) | USD 245.97 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

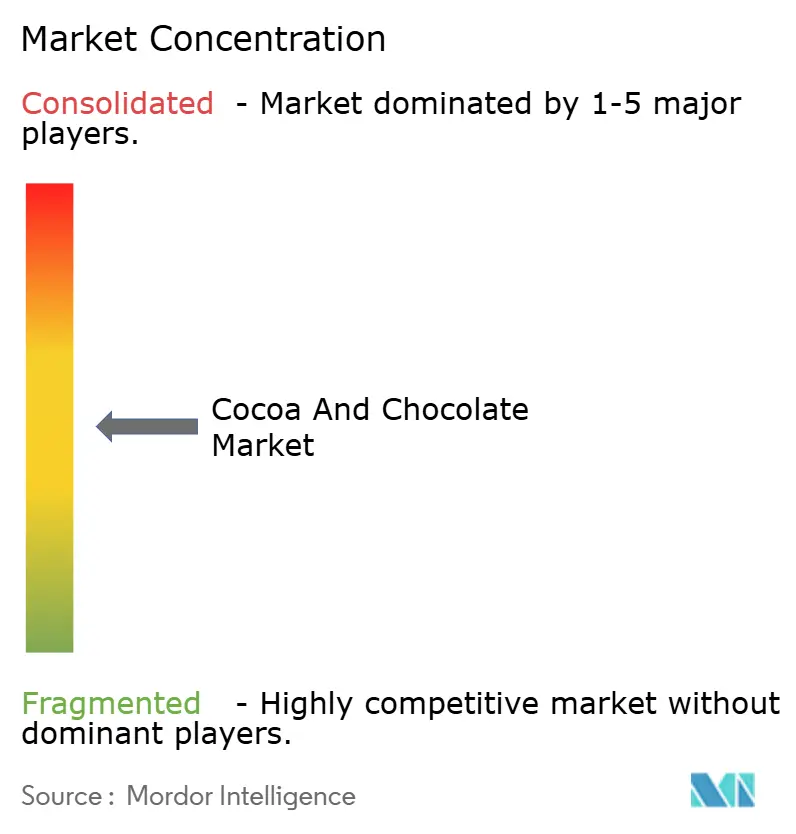

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cocoa And Chocolate Market Analysis by Mordor Intelligence

The cocoa and chocolate market size was valued at USD 169.12 billion in 2025 and estimated to grow from USD 180.01 billion in 2026 to reach USD 245.97 billion by 2031, at a CAGR of 6.44% during the forecast period (2026-2031). The growth reflects consumers’ willingness to trade up to premium products, expanding health-oriented dark chocolate demand, and fast-rising online sales. Record-high cocoa prices in early 2025 underscore supply-side pressure but have not derailed spending because manufacturers pass costs through selective price increases, shrinkflation, and product mix shifts. Besides, Europe remains the single largest regional buyer, yet Asia-Pacific delivers the strongest volume momentum as local grinding capacity comes onstream and incomes rise. Meanwhile, the EU Deforestation Regulation (EUDR) forces sweeping changes in sourcing, traceability, and compliance investments, prompting origin diversification and agroforestry programs.

Key Report Takeaways

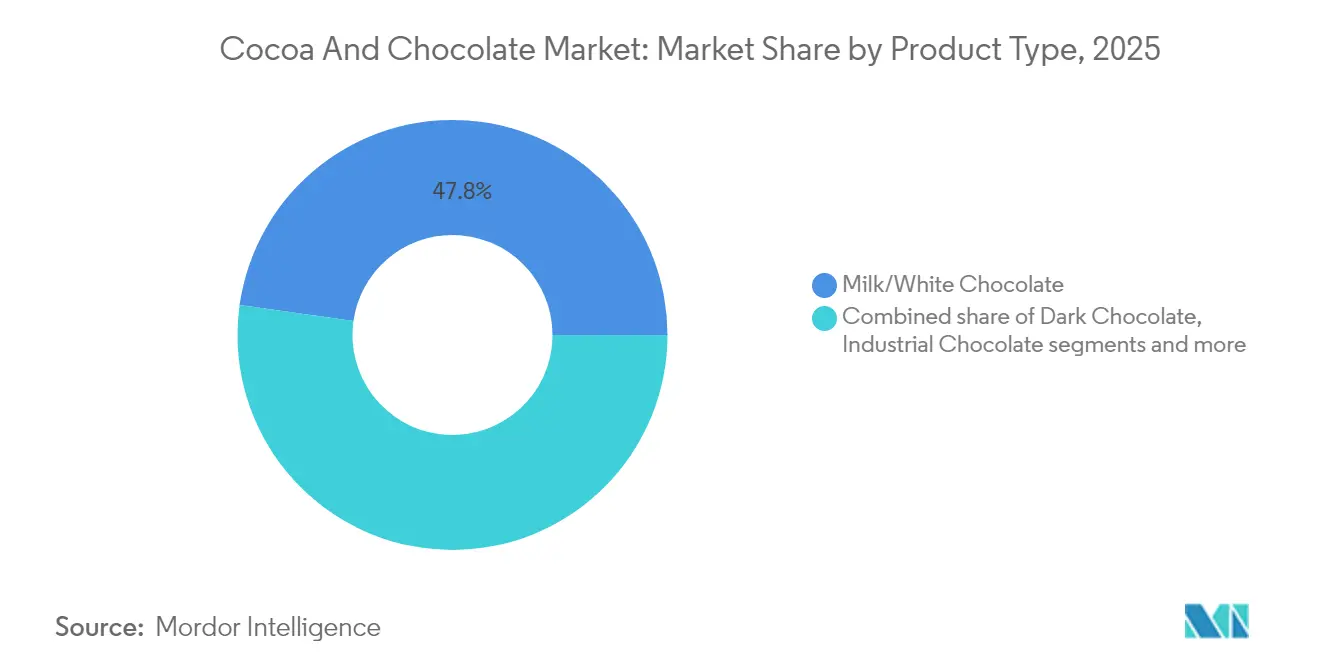

- By product type, milk/white chocolate led with 47.78% of cocoa and chocolate market share in 2025; dark chocolate is projected to expand at a 7.74% CAGR through 2031.

- By end user, the retail channel accounted for 61.42% share of the 2025 cocoa and chocolate market size, while industrial applications recorded the highest growth at 7.48% CAGR to 2031.

- By nature, conventional chocolate captured 90.45% share of the cocoa and chocolate market size in 2025; organic chocolate is advancing at an 7.78% CAGR over 2026-2031.

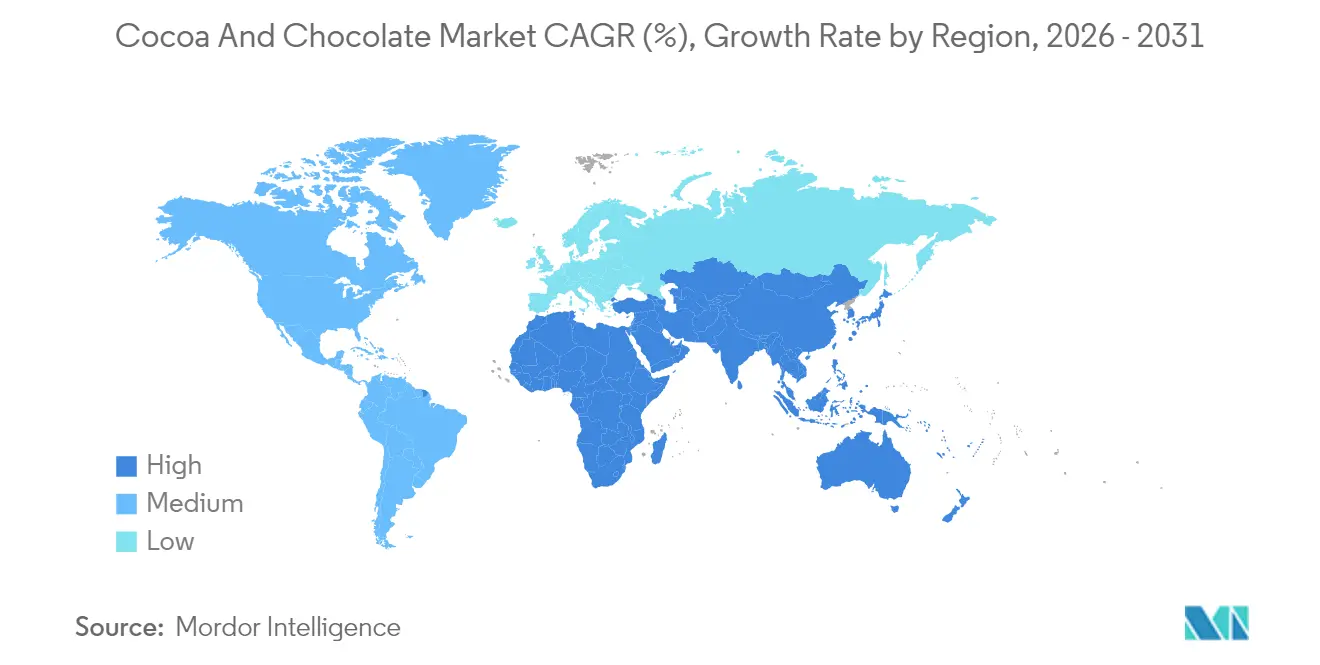

- By geography, Europe commanded 35.12% of the cocoa and chocolate market share in 2025, whereas Asia-Pacific is poised for a 7.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cocoa And Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium and indulgent chocolates | +1.2% | Global – North America and Europe hot-spots | Medium term (2-4 years) |

| Growing health awareness boosting dark chocolate intake | +0.9% | Global – led by developed markets | Long term (≥ 4 years) |

| Rapid expansion of cocoa grinding capacity in Asia-Pacific | +0.8% | Asia-Pacific core; Middle East and Africa spill-over | Medium term (2-4 years) |

| E-commerce acceleration in chocolate retail | +0.7% | Global – early gains in North America, Europe, China | Short term (≤ 2 years) |

| Functional-food use of cocoa bioactives in nutraceuticals | +0.5% | North America and European Union; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Vertical integration by bean-to-bar micro-producers | +0.3% | Global – artisanal clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium and Indulgent Chocolates

Consumer preferences in cocoa and chocolate products continue shifting toward premium and specialty offerings over mass-produced alternatives. This shift reflects a demand for higher quality, authenticity, and distinctive taste experiences. For instance, Lindt & Sprüngli's EXCELLENCE COCOA PURE, made exclusively from cocoa fruit without refined sugar, demonstrates this market evolution. Similarly, the introduction of innovative products like Angel Hair Chocolate, which combines Turkish cotton candy with Belgian chocolate, has gained significant social media attention and highlights the market's interest in artisanal and culturally-inspired offerings. Moreover, consumers demonstrate a willingness to pay 20-40% more for chocolates they perceive as authentic, ethical, and of superior quality. This trend creates opportunities for boutique chocolate manufacturers, particularly as demand grows for limited-edition, single-origin, and handcrafted products with authentic brand narratives. The expansion of urban middle classes in emerging markets has increased the demand for refined chocolate experiences, establishing premiumization as a key factor in the cocoa and chocolate industry's development.

Growing Health Awareness Boosting Dark Chocolate Intake

Dark chocolate products, particularly varieties with 70% or higher cocoa content, are experiencing increased demand driven by growing health consciousness among consumers. Scientific research supporting the benefits of cocoa flavonoids for cardiovascular and cognitive health has repositioned dark chocolate from a confectionery item to a functional food product. This trend is evident in new product launches, such as Nebula Snacks' non-glycemic chocolate bites introduced in August 2024, which feature 73% organic dark chocolate without added sugar or dairy, meeting consumer demand for clean-label products. Moreover, the health positioning has enabled chocolate manufacturers to expand into wellness-focused retail channels, previously limited to nutraceuticals and supplements. With ongoing medical research validating cocoa's health benefits and potential regulatory changes allowing more explicit health claims on packaging, dark chocolate's market presence is expanding beyond traditional confectionery categories. This market development demonstrates the integration of nutritional benefits with conventional chocolate indulgence.

Rapid Expansion of Cocoa Grinding Capacity in Asia-Pacific

The Asia-Pacific region is transitioning from a consumption-focused market to a manufacturing and processing hub through investments in local cocoa grinding operations. Major cocoa processors such as Cargill, Barry Callebaut, and Olam International expanded their operations in Asia-Pacific, as evidenced by Cargill's new cocoa production facilities in Indonesia, which were scheduled to begin operations in October 2024. The localization of processing operations reduces dependence on European and North American facilities while enabling better adaptation to regional preferences and regulatory requirements. This expansion aligns with expected growth in chocolate consumption across China, India, and Southeast Asia, where current per capita consumption remains low. Moreover, the increased local grinding capacity offers operational benefits through reduced transportation costs and improved currency risk management. These developments position the Asia-Pacific region to become a key center for cocoa processing and innovation, complementing established global processing hubs.

E-commerce Acceleration in Chocolate Retail

E-commerce has become a vital channel for consumer engagement and product distribution in cocoa and chocolate operations. Major chocolate manufacturers are implementing omnichannel strategies, as demonstrated by Ghirardelli's 2024 partnership with Salsify to manage over 650 SKUs across Walmart, Target, and Amazon platforms. This industry transformation extends beyond consumer sales to include B2B platforms serving foodservice and industrial segments. Moreover, companies are leveraging seasonal promotions and data analytics to enhance online visibility and sales conversion, responding to increased online purchasing, especially among younger consumers. The expansion of internet accessibility—91% in Europe, 87% in the Americas, and 66% in Asia-Pacific, according to the International Telecommunication Union in 2024—continues to broaden the e-commerce market [1]Source: International Telecommunication Union, "Measuring Digital Development – Facts and Figures 2024", oitu.int. Thus, success in the chocolate industry now requires effective digital marketing, inventory management, and fulfillment operations as online retail transforms global distribution networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cocoa-bean price volatility amid climate shocks | -1.8% | Global – acute in West Africa | Short term (≤ 2 years) |

| Tightening human-rights and traceability regulations | -0.9% | European Union and North America; expanding globally | Medium term (2-4 years) |

| Stricter cadmium limits in key importing regions | -0.6% | European Union; spill-over to developed markets | Long term (≥ 4 years) |

| Aging cocoa trees and disease lowering farm yields | -1.1% | West Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cocoa-Bean Price Volatility Amid Climate Shocks

Cocoa-bean prices reached unprecedented levels, with futures prices increasing by over 400% between late 2023 and early 2025. This surge primarily resulted from climate-related crop failures in Ivory Coast and Ghana, which together account for more than 60% of global cocoa production. The International Cocoa Organization documented the largest global supply deficit in over 60 years, with arrival volumes declining by 28% in Ivory Coast and 35% in Ghana during the 2023-2024 season [2]Source: International Cocoa Organization (ICCO), "Cocoa Market Report for February 2024", icco.org. These reductions stemmed from erratic rainfall patterns, higher temperatures, and increased instances of crop diseases, particularly the swollen shoot virus. Besides, the significant price increases have compelled chocolate manufacturers to implement hedging strategies and transfer higher costs to consumers. Hershey's, for example, projected flat earnings growth primarily due to increased cocoa expenses. The supply chain constraints have accelerated the development of cocoa substitutes, including Planet A Foods' ChoViva, which combines fermented oats and sunflower seeds to replicate chocolate's characteristics. Climate models indicate continued disruptions in major production regions, suggesting sustained market volatility. This outlook has intensified industry demands for comprehensive changes in sourcing approaches, supply chain operations, and product composition throughout the global chocolate industry.

Tightening Human-Rights and Traceability Regulations

Cocoa producers and chocolate manufacturers face increased regulatory oversight through new frameworks requiring human rights due diligence and supply chain traceability. The EU Deforestation Regulation (EUDR), beginning implementation in December 2025, requires all cocoa and chocolate products in the EU market to demonstrate deforestation-free and legal production status through detailed documentation, including geolocation data and risk assessments. Non-compliance penalties can reach 4% of EU turnover, requiring manufacturers and traders to transform their sourcing and documentation processes. Additional regulations, including Fairtrade's 2022 Cocoa Standard, emphasize shared responsibility in addressing child labor and deforestation. The World Cocoa Foundation notes that supply chain participants must support cocoa-farming communities and implement enhanced due diligence measures [3]Source: World Cocoa Foundation, "Fairtrade’s New Cocoa Standard: Striking a balance between robust requirements and fairness for farmers", worldcocoafoundation.org. These regulations incorporate human rights and environmental standards throughout the supply chain, but increase operational costs. Small-scale farmers may face exclusion if unable to meet traceability requirements, potentially leading to supply disruptions and market concentration. The regulatory shift extends beyond the EU, with other major chocolate-consuming nations considering similar legislation. This indicates a broader industry transition toward required transparency and ethical sourcing, necessitating global adaptation and fundamental changes across cocoa supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Drives Health-Conscious Growth

Dark chocolate demonstrates the highest growth rate with a 7.74% CAGR from 2026-2031, while milk/white chocolate maintains the largest market share at 47.78% in 2025. This trend indicates a market segmentation between health-conscious consumers seeking premium options and those preferring traditional chocolate varieties. The growth in dark chocolate consumption corresponds with research confirming the cardiovascular benefits of cocoa flavonoids, particularly in products with 70% or higher cocoa content. The industrial chocolate segment, including cocoa butter, powder, liquor, and nibs, continues to grow due to increased foodservice demand and incorporation into nutritional products. Similarly, filled and compound chocolate serves price-sensitive markets in developing regions.

Rising cocoa prices influence manufacturers to adjust their product strategies, including increased use of cocoa butter alternatives and compound chocolate formulations to protect profit margins. Research institutions like ETH Zurich demonstrate sustainable innovation through developments such as chocolate made with cocoa fruit jelly as a sugar substitute, which improves nutritional value and reduces waste. The industrial chocolate segment expands beyond food applications into cosmetics and personal care products, where cocoa butter commands higher prices for its moisturizing properties. Manufacturers focus on developing functional chocolate products containing probiotics, prebiotics, and plant extracts, transforming chocolate from a confectionery item into a vehicle for nutritional benefits.

By Nature: Organic Segment Surges Despite Conventional Dominance

The organic chocolate market is projected to grow at 7.78% CAGR from 2026-2031, emerging as the fastest-growing segment, while conventional chocolate retains 90.45% market share in 2025. This growth reflects increased consumer awareness of sustainable agriculture and the health benefits of pesticide-free cocoa production. Millennial and Gen Z consumers, particularly parents seeking healthier options for children, are the primary drivers of organic chocolate demand due to its clean-label attributes.

Conventional chocolate manufacturers face reduced margins due to increasing cocoa prices and regulatory compliance costs. In contrast, organic producers maintain profitability through premium positioning, with consumers accepting 20-40% higher prices for certified sustainable products. The African Regional Standard for Sustainable Cocoa (ARS-1000), implemented by Ghana and Côte d'Ivoire, aims to enhance cocoa sector professionalization and ensure compliance with EU deforestation regulations. This framework may reduce the operational differences between conventional and organic production methods. As organic certification requirements align with stricter regulatory demands for traceability and environmental compliance, the organic segment is positioned to gain market share, particularly as supply chain transparency becomes a regulatory requirement rather than an optional practice.

By End User: Industrial Applications Accelerate Beyond Traditional Retail

Industrial end users show the highest growth rate at 7.48% CAGR through 2031, while retail channels hold a dominant 61.42% market share in 2025. The industrial segment's expansion spans confectionery, bakery, dairy, and beverage applications, with additional opportunities emerging in pharmaceuticals and nutraceuticals as research validates cocoa's therapeutic properties. Besides, foodservice demand increases as restaurants and cafes integrate premium chocolate into desserts and specialty beverages. In retail distribution, supermarkets/hypermarkets remain dominant, with online retail channels showing significant growth.

Moreover, consumer purchasing patterns influence convenience stores and specialty retailers to emphasize impulse purchases and seasonal promotions to increase customer visits and sales frequency. Additionally, cocoa's applications now extend beyond food products, with cocoa butter becoming important in premium skincare products due to its moisturizing and antioxidant qualities. The pharmaceutical and nutraceutical sectors increasingly utilize cocoa's documented anti-inflammatory and cardiovascular benefits, creating new distribution channels. This expansion across multiple industries strengthens cocoa's market position in both lifestyle and health segments.

Geography Analysis

The European chocolate market represents a 35.12% share in 2025, driven by established consumption patterns, premium product preferences, and regulatory leadership in sustainability standards. Market growth is slowing due to market maturity and increasing health consciousness among consumers. The EU Deforestation Regulation, effective December 2024, requires deforestation-free cocoa sourcing, necessitating supply chain transparency and potentially raising costs by 10-15% according to the European Commission. Germany, the United Kingdom, and France are the primary consumption markets, while Belgium and Switzerland maintain their premium market position through heritage brands and artisanal production. The region's strict cadmium regulations for chocolate products (0.10 mg/kg for milk chocolate to 0.80 mg/kg for dark chocolate with 50% or higher cocoa content) impact global sourcing strategies and product development. European manufacturers are strengthening direct farmer relationships and implementing agroforestry programs to ensure compliance with regulations while securing their supply chains.

The Asia-Pacific region leads the global cocoa and chocolate market growth with a CAGR of 7.02% from 2026 to 2031. This growth stems from changing consumer demographics and lifestyles. Rising disposable incomes, urbanization, and middle-class expansion in China, India, and Southeast Asia have transformed chocolate from a luxury item to a common choice for gifts and daily consumption. The market expansion is driven by younger consumers and urban populations seeking premium and healthier chocolate options, affecting both mainstream and specialty segments. Digital commerce growth and targeted regional marketing have improved product accessibility. The Asia-Pacific region has established itself as a significant influence on global cocoa and chocolate market dynamics.

North America holds a dominant market share, driven by the United States' advancements in functional chocolate and premium artisanal products. The region benefits from Canada and Mexico's cost-effective manufacturing capabilities and strategic market access. In South America, Ecuador, Peru, and Colombia leverage their cocoa production advantages to establish bean-to-bar operations and expand their manufacturing facilities. The Middle East and Africa market shows expansion opportunities through demographic advantages and urban development, although market growth remains limited by regional instability and underdeveloped infrastructure. Brazil's strategic initiatives to increase cocoa production capacity by 2030, supported by agricultural technology and disease control measures, establish the country as a key supply chain component.

Competitive Landscape

The global chocolate market demonstrates moderate fragmentation, with multinational corporations including Mars, Mondelez, Ferrero, Nestlé, and Barry Callebaut maintaining substantial market shares despite the entry of regional and artisanal brands. These major companies establish industry standards through capital allocation in product development, brand building, and distribution network expansion, enabling rapid response to market demand and consumer preferences. The market's mid-tier segment comprises regional specialists and premium craft chocolate manufacturers who target specific market segments through product differentiation, limited editions, and ethical sourcing initiatives. This market structure facilitates both operational efficiency and product innovation, although market consolidation and cost pressures may increase the market share of dominant firms in the coming decade.

Market dynamics reflect shifting consumer preferences, with increased demand for premium and specialty chocolates, health-focused products like dark and sugar-free varieties, and sustainably sourced ingredients. Companies that address these market requirements through functional benefits, clean label ingredients, or product innovation capture increased market share. Regional market variations persist, with North America's established consumer base maintaining market leadership, while Europe and Asia-Pacific demonstrate strong growth due to health consciousness and diversified consumption patterns. This market segmentation creates entry opportunities for new manufacturers while established companies focus on market share retention.

The global chocolate market faces operational challenges affecting competitive dynamics, including raw material price volatility, regulatory requirements for traceability and sustainability, and supply chain complexity. These factors necessitate supply chain optimization, operational efficiency improvements, and transparent procurement processes. The market's competitive landscape is expected to intensify as it grows, particularly in premium, functional, and ethical product segments. This competitive environment presents both opportunities and risks within the moderately concentrated market structure.

Cocoa And Chocolate Industry Leaders

-

Barry Callebaut AG

-

Mars Incorporated

-

Nestlé S.A.

-

Ferrero Group

-

Mondelēz International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cadbury and Lotus Bakeries introduced the Cadbury Dairy Milk Biscoff bar, their first collaborative product, following their partnership announcement in July 2024. The product combined Cadbury Dairy Milk chocolate with Lotus Biscoff biscuit pieces and was available in three variants: a 95g price-marked pack at GBP 1.69, a standard 95g bar, and a 105g bar.

- October 2024: Cargill established a new cocoa production line at its processing plant in Gresik, Indonesia, to address the increasing demand for food and beverages across Asia. The expansion enhanced the company's position in bakery, ice cream, chocolate confectionery, and foodservice café beverages. The launch incorporated two new dark Gerkens cocoa powders and a range of Cargill Craft cocoa liquors, which featured distinct color profiles and flavors.

- June 2024: Blommer Chocolate launched its new product line, Elevate. The product provided chocolatiers and confectioners with a cost-effective alternative to traditional cocoa butter while maintaining quality standards. Elevate coatings that used Cocoa Butter Equivalent (CBE) technology integrated with cocoa butter and provided bloom resistance, which extended shelf life and preserved product appearance.

Global Cocoa And Chocolate Market Report Scope

| Dark Chocolate | |

| Milk/White Chocolate | |

| Industrial Chocolate | Cocoa Butter |

| Cocoa Powder | |

| Cocoa Liquor | |

| Cocoa Nibs | |

| Filled/Compound Chocolate |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Specialty Stores | |

| Others | |

| Industrial | Confectionery |

| Bakery | |

| Dairy and Beverages | |

| Cosmetics and Personal Care | |

| Pharmaceuticals and Nutraceuticals |

| Conventional |

| Organic |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Dark Chocolate | |

| Milk/White Chocolate | ||

| Industrial Chocolate | Cocoa Butter | |

| Cocoa Powder | ||

| Cocoa Liquor | ||

| Cocoa Nibs | ||

| Filled/Compound Chocolate | ||

| By End User | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Specialty Stores | ||

| Others | ||

| Industrial | Confectionery | |

| Bakery | ||

| Dairy and Beverages | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals and Nutraceuticals | ||

| By Nature | Conventional | |

| Organic | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the cocoa and chocolate market?

The cocoa and chocolate market size stands at USD 180.01 billion in 2026 and is projected to reach USD 245.97 billion by 2031.

Which region is growing the fastest in cocoa and chocolate sales?

Asia-Pacific shows the strongest momentum with a 7.02% CAGR driven by rising incomes and new grinding capacity.

Which product segment leads growth in the market?

Dark chocolate is the fastest-growing product segment with a 7.74% CAGR as health-conscious consumers favor 70%-plus cocoa bars.

What regulations most influence chocolate sourcing today?

The EU Deforestation Regulation, effective December 2024, requires proof of deforestation-free cocoa and is reshaping global supply chains.

Page last updated on: