Liquor Chocolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

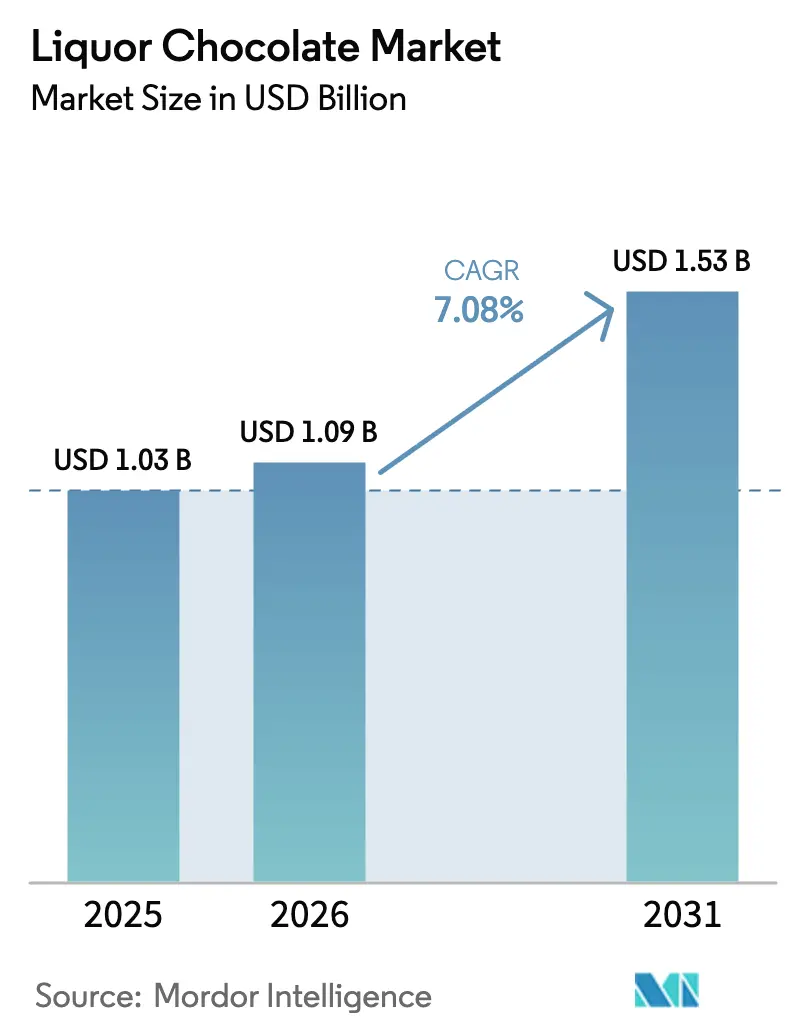

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquor Chocolate Market Analysis by Mordor Intelligence

The liquor chocolate market size was valued at USD 1.03 billion in 2025 and is estimated to grow from USD 1.09 billion in 2026 to reach USD 1.53 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031). Premium gifting, cross-branding with spirits, and duty-free expansion are driving the liquor chocolate market's growth, despite challenges posed by increasing cocoa prices and alcohol regulations. Collaborations with spirit brands position these products as experiential offerings, supporting significant price premiums. Electronic commerce (e-commerce) platforms and specialty stores are expanding consumer access, even with shipping restrictions. Travel-retail outlets benefit from recovering passenger traffic, capturing impulse purchases, and delivering strong profit margins that help mitigate ingredient cost fluctuations. Additionally, sustainability initiatives and halal-compliant product innovations are creating new demand opportunities while maintaining the luxury appeal of the market.

Key Report Takeaways

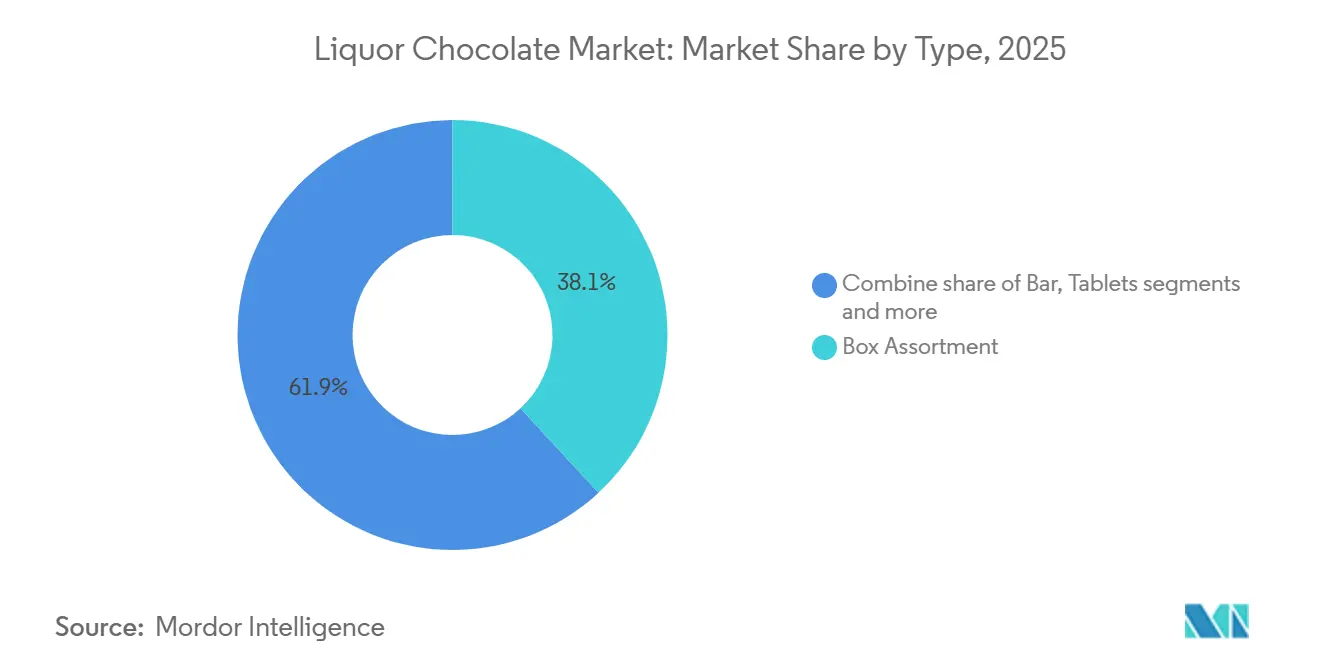

- By type, box assortments led with 38.11% share of the liquor chocolate market in 2025, while bars are projected to expand at an 8.28% CAGR through 2031.

- By nature, conventional products captured 78.21% share in 2025, whereas organic variants are forecast to grow at an 8.02% CAGR to 2031.

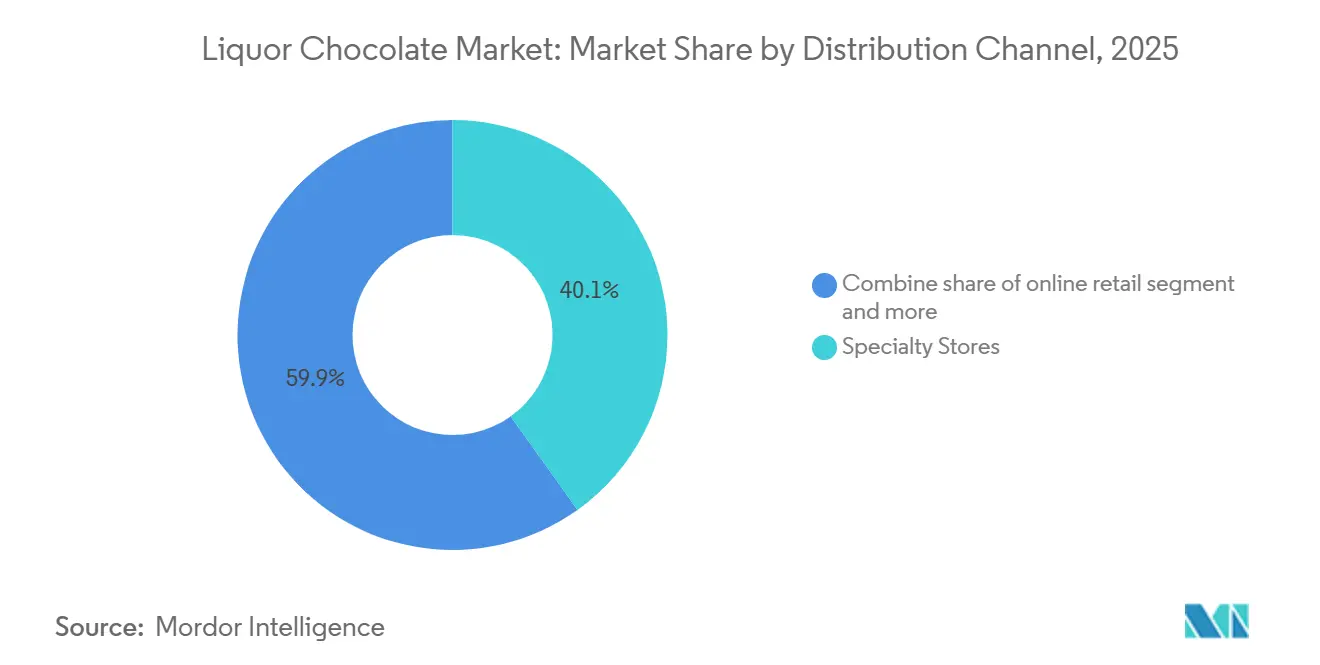

- By distribution channel, specialty stores held 40.12% share in 2025, but online retail is set to increase at an 8.49% CAGR during 2026-2031.

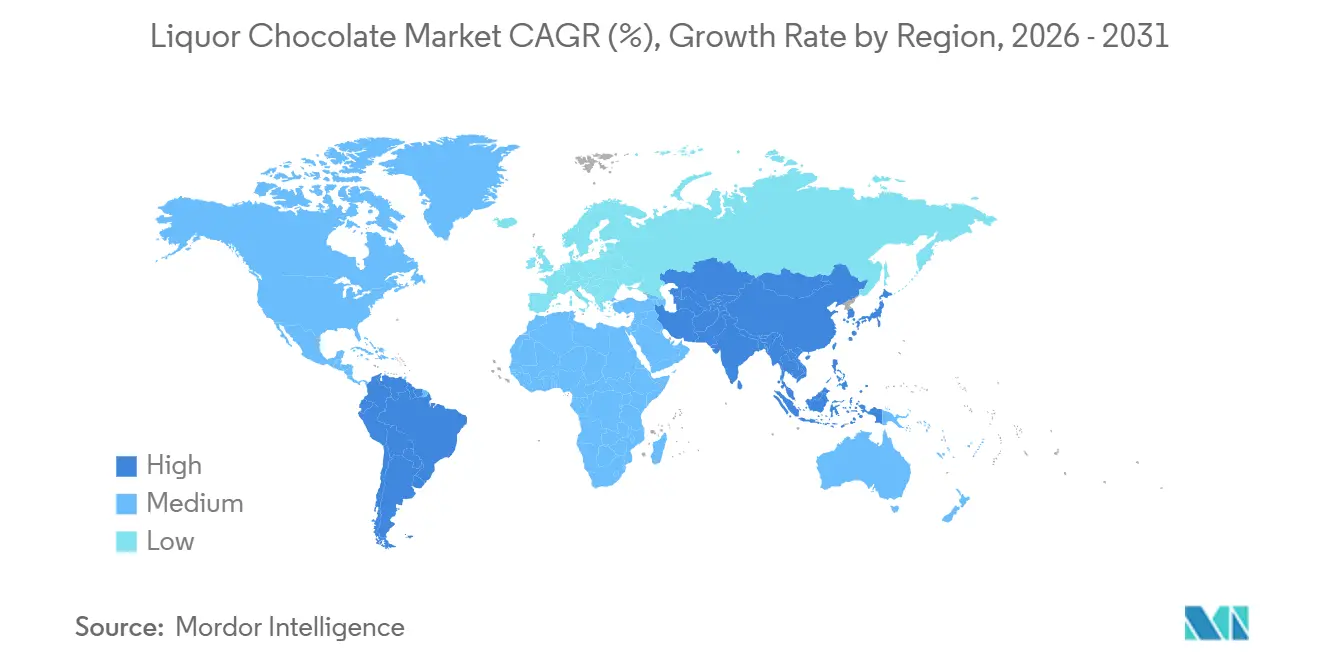

- By geography, Europe commanded 45.32% share in 2025, while Asia-Pacific is poised to register the fastest regional CAGR of 7.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquor Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Collaborations between chocolate makers and spirit brands | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing preference for experiential and gourmet food products | +1.5% | Global, led by North America, Europe, and urban Asia-Pacific | Long term (≥4 years) |

| Demand for sustainable, organic, and fair-trade liquor chocolates | +0.9% | Europe and North America core, spillover to Asia-Pacific | Long term (≥4 years) |

| Growing gifting culture for special occasions | +1.3% | Global, particularly strong in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Airport duty-free sales targeting travelers | +1.1% | Global, concentrated in Middle East, Asia-Pacific, and European hubs | Short term (≤2 years) |

| Rise in specialty stores offering expert-curated selections | +0.8% | North America and Europe, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Collaborations between chocolate makers and spirit brands

Collaborations between confectionery companies and distilleries are opening new opportunities for co-branding and market expansion by combining the premium appeal of craft spirits with artisan chocolate. For example, Woodford Reserve has extended its partnership with Compartés, introducing limited-edition bourbon-infused chocolate bars that capitalize on the distillery's heritage and command a premium price compared to standard chocolate bars. Similarly, LOTTE Corporation launched Rummy x Bacchus, a product that blends rum-flavored chocolate with its well-known Bacchus candy brand, targeting nostalgic consumers and encouraging trial purchases through convenience store channels. Whitman's collaborated with Boulevard Brewing to develop beer-infused truffles, which are sold exclusively through specialty retailers. This partnership highlights how regional craft brewers can gain access to national confectionery distribution networks. Additionally, Heritage Distilling's Cocoa Bomb Chocolate Whiskey earned the title of "Best Flavored Whiskey" at the American Distilling Institute competition, showcasing the category's appeal to spirits judges and indicating potential for premium placements in on-premise locations. These collaborations help reduce customer acquisition costs by leveraging shared brand audiences and creating limited-edition products that drive impulse purchases. However, they require careful alignment on alcohol-content thresholds to avoid triggering federal excise taxes in the United States.

Increasing preference for experiential and gourmet food products

Consumers are increasingly viewing food as a way to share stories and express themselves socially. This shift has led to a change in spending patterns, moving away from basic commodity staples toward curated, visually appealing indulgences that convey sophistication. According to Barry Callebaut's February 2026 trend report, "Minorstones" was identified as one of the top five consumer behaviors, with a significant majority of respondents celebrating smaller personal milestones rather than waiting for major holidays. This trend has created consistent demand throughout the year for premium gifting formats. The report also highlighted that a large proportion of consumers actively avoid ultra-processed foods, with most preferring ingredient lists containing fewer than five components. As a result, manufacturers are reformulating products to include recognizable ingredients, such as single-malt whiskey or aged rum, instead of artificial flavorings. Additionally, Lindt reported that premium chocolate sales among users of glucagon-like peptide-1 (GLP-1) receptor agonist medications grew at a faster rate compared to non-users. This indicates that individuals using weight-management drugs are opting for higher-quality, lower-volume indulgences rather than eliminating treats entirely. This trend has positively impacted liquor chocolates, which are priced significantly higher than standard assortments. These products align with the "treat yourself" mindset while offering indulgence in smaller portion sizes.

Demand for sustainable, organic, and fair-trade liquor chocolates

Sustainability credentials have shifted from being niche differentiators to becoming standard consumer expectations. More consumers are now willing to pay higher prices for products with certifications such as Fairtrade, organic, and Rainforest Alliance, which reflect ethical sourcing and environmental responsibility. Many major chocolate brands have committed to sourcing fully certified sustainable cocoa within the next few years. This establishes a baseline that organic liquor-chocolate producers must exceed through efforts like third-party verification and blockchain-based traceability. The Chocolate Scorecard evaluated companies across various regions, including several in Asia, on factors such as traceability, living income, child labor, deforestation, agroforestry, and pesticide management. The scoring system ranks performance from "Leading" to "Lagging," providing a public benchmark that encourages underperforming companies to improve or face reputational risks. Chocolate and Love offers a single-origin Panama dark chocolate bar with high cocoa content that is both organic and Fairtrade certified. The cocoa is sourced directly from cooperatives such as Cocabo in Panama and Acopagro in Peru. Additionally, the packaging is made from Forest Stewardship Council-certified paper and compostable wood-pulp film, meeting European Standard EN13432 and American Society for Testing and Materials D6400 biodegradability standards [1]Source: European Bioplastics, “Certified Bioplastics Performance in Industrial Composting,” european-bioplastics.org. The primary challenge lies in expanding organic and fair-trade liquor chocolates beyond specialty markets while maintaining sustainability commitments and addressing potential price resistance from mainstream consumers.

Growing gifting culture for special occasions

Liquor chocolates occupy a unique niche in the gifting market, blending the elegance of wine or spirits with the appeal of confectionery. This combination makes them ideal for corporate thank-you gifts, host presents, and milestone celebrations. In Southeast Asia and the Middle East, Muslim consumers are increasingly favoring halal-certified, alcohol-free options for events such as Eid, Ramadan, and weddings. Indonesia's mandatory halal certification deadline of October 17, 2026, under Government Regulation Number 42 of 2024, mandates that all food and beverage manufacturers either obtain certification from the Halal Product Assurance Agency or the Halal Certification Agency or label their products as "Non-Halal." This regulation effectively divides the market into compliant and non-compliant categories [2]Source: American Halal Foundation, “Mandatory Halal Certification Now Enforced,” halalfoundation.org. In Western markets, 2BAR Spirits launched a Whiskey and Chocolate gift pack in November 2024. This package, featuring a 750-milliliter bottle and artisan truffles, is aimed at the premium corporate gifting segment during the holiday season. Marketing data from Ramadan 2026 indicated notable growth in the occasions and gifts categories, with a significant year-over-year increase in Vietnam and Malaysia. These trends underscore the importance of culturally tailored packaging and messaging in these markets.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent alcohol regulations varying by jurisdiction | -1.4% | Global, acute in United States, Middle East, and select Asia-Pacific markets | Long term (≥4 years) |

| Health concerns over alcohol consumption and calorie content | -0.9% | Global, particularly North America and Europe | Medium term (2-4 years) |

| High production costs from quality ingredients and spirits | -0.7% | Global, with margin pressure most severe in emerging markets | Short term (≤2 years) |

| Cultural taboos against alcohol in certain regions | -0.6% | Middle East, North Africa, and Muslim-majority Asia-Pacific countries | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent alcohol regulations varying by jurisdiction

Liquor chocolates operate within a complex regulatory framework where confectionery and alcohol-beverage regulations overlap. Manufacturers must navigate dual oversight, state-specific licensing, and labeling requirements, which complicate distribution and increase compliance costs. In the United States, the Food and Drug Administration (FDA) regulates chocolate standards under Title 21 of the Code of Federal Regulations (CFR) Part 163, which defines chocolate liquor as the solid or semi-plastic mass derived from roasted cacao nibs containing a significant percentage of cacao fat [3]Source: Code of Federal Regulation, “Chocolate liquor,” ecfr.gov. At the same time, the Alcohol and Tobacco Tax and Trade Bureau (TTB) assumes jurisdiction when the alcohol content reaches or exceeds a specific threshold by volume, imposing federal excise taxes, age-verification requirements, and state-specific distribution licenses. Lindt has stated that it does not import liqueur-filled chocolates into the United States due to the complexity of federal and state alcohol regulations, leaving this market segment to smaller domestic producers willing to bear the compliance costs. In Ireland, mandatory alcohol health-warning labels have been postponed until a later year, offering a temporary competitive advantage to European producers exporting to non-European Union (EU) markets without requiring packaging modifications. In Indonesia, a halal certification deadline set for a specific date under Government Regulation Number 42 of 2024, requires all food and beverage products to display either BPJPH (Halal Product Assurance Organizing Agency) halal certification or explicit "Non-Halal" labeling. Non-compliance will result in fines, market withdrawal, and public notices. This regulation effectively excludes alcohol-infused chocolates from the world's fourth most populous country unless reformulated to be alcohol-free.

Health concerns over alcohol consumption and calorie content

Rising health consciousness and the increasing use of weight-management medications are influencing chocolate consumption patterns. Consumers are now seeking lower-calorie, functional alternatives that align with their wellness goals while still offering indulgence. By the year 2025, glucagon-like peptide-1 (GLP-1) drugs such as Ozempic are expected to reach a significant portion of U.S. households. Users of these medications are projected to account for a notable share of chocolate sales, despite reducing overall grocery spending. These consumers tend to trade up to premium, lower-volume options rather than eliminating treats entirely. For instance, Lindt reported a substantial growth in premium chocolate sales among GLP-1 users in 2025, compared to a moderate increase among non-users. This indicates that liquor chocolates could appeal to this group if marketed as sophisticated, portion-controlled indulgences. However, the inclusion of alcohol adds empty calories, with a typical liqueur-filled praline containing a considerable amount of calories and sugar, which conflicts with clean-eating trends. The key challenge lies in balancing indulgence with health claims, as regulatory bodies closely monitor functional-food marketing, and consumers remain skeptical of products that overpromise wellness benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Single-Serve Bars Reshape Impulse Occasions

Bars are projected to grow at an annual rate of 8.28% from 2026 to 2031, outperforming other formats due to their convenience, portion control, and suitability for travel-retail distribution. These individually wrapped, on-the-go options cater to consumer preferences for portability. In 2024, Woodford Reserve and Compartés introduced a bourbon-infused chocolate bar and extended their partnership through 2026. This product is positioned as a portable alternative to boxed assortments, particularly for male-oriented gifting occasions. The bar format also streamlines production compared to filled pralines, as processes like enrobing and molding require fewer manual steps than shell-forming and liqueur injection. This enables higher throughput on automated production lines.

Boxed assortments accounted for 38.11% of the market share in 2025, supported by their popularity in corporate gifting, seasonal holidays, and premium retail displays. Their presentation and variety justify higher price points, appealing to consumers seeking premium options. Neuhaus, the inventor of the praline in 1912, launched a Chocolate Cocktails collection in collaboration with Belgian mixologist Noa Van Ongevalle. This collection features spirit-infused pralines designed to replicate cocktail flavor profiles, targeting consumers interested in experiential products.

By Nature: Organic Certification Commands Loyalty Premium

Organic liquor chocolates are expected to grow at an annual rate of 8.02% from 2026 to 2031. This growth is driven by consumers who increasingly prioritize products made with fair-trade cocoa, pesticide-free ingredients, and transparent supply chains. These preferences reflect a growing awareness of ethical and sustainable practices in the food industry. Despite this trend, conventional products retained a significant 78.21% market share in 2025. This dominance is primarily due to their lower price points and widespread availability, making them more accessible to a broader consumer base.

Chocolate and Love, a prominent brand in the organic chocolate market, offers an 80% single-origin Panama dark chocolate bar that is certified organic and Fairtrade. The cocoa used in this product is sourced directly from cooperatives such as Cocabo in Panama and Acopagro in Peru, ensuring traceability and support for local farmers. Furthermore, the packaging is designed with sustainability in mind, utilizing Forest Stewardship Council (FSC)-certified paper and compostable wood-pulp film. These materials meet the EN13432 and ASTM D6400 biodegradability standards, aligning with environmentally friendly practices.

By Distribution Channel: E-Commerce Bypasses Licensing Friction

Online retail is expected to grow at an annual rate of 8.49% from 2026 to 2031, making it the fastest-growing distribution channel. This growth is driven by direct-to-consumer models that facilitate personalized gifting, subscription boxes, and broader geographic reach while bypassing state-specific alcohol licensing restrictions. Specialty stores accounted for 40.12% of the market share in 2025, benefiting from expert curation, in-store tastings, and consumer education on pairing recommendations. However, these stores face challenges such as rising urban rental costs and competition from e-commerce platforms offering broader assortments and home delivery options. André's Confiserie Suisse has partnered with J. Rieger and Company distillery since 2015 to sell spirit-infused chocolates. These products are available both at its Kansas City retail location and through an online storefront that ships to 48 states. By formulating chocolates with alcohol content below the 0.5% threshold that triggers federal excise taxes, the company has successfully implemented a dual-channel strategy. This approach demonstrates how specialty retailers can use e-commerce to expand their market reach while maintaining the brand equity established through physical retail experiences.

Supermarkets and hypermarkets provide access to mass-market consumers and capitalize on impulse purchases, particularly during holiday seasons. End-cap displays and checkout lanes encourage unplanned additions to shopping carts. However, these channels require slotting fees, promotional allowances, and competitive pricing, which can compress margins for premium liquor chocolates. Other distribution channels, such as hotel minibars, airline duty-free carts, and corporate gift services, cater to niche markets. While these channels offer high per-unit margins, their volume potential remains limited.

Geography Analysis

In 2025, Europe accounted for 45.32% of the global market share, driven by Belgium's annual chocolate production, Switzerland's luxury chocolate heritage, and a dense network of artisan chocolatiers specializing in liqueur-filled pralines. Belgium hosts thousands of chocolatiers, with Neuhaus credited for inventing the praline in 1912. Leonidas offers pure liqueur boxes containing 5% liqueur content and 28% chocolate by weight, while Godiva markets a chocolate liqueur with 15% alcohol by volume, positioning it as a dessert spirit competing with cream liqueurs such as Baileys Irish Cream. Tchelo, a Belgian liqueur brand launched in 2024, introduced a Praline flavor. Germany, the United Kingdom, the Netherlands, Poland, and Spain contribute significant volumes through supermarket and discount-channel distribution. However, premiumization remains concentrated in Switzerland, Belgium, and France, where artisan margins of 48% support reinvestment in innovation and sustainability.

The Asia-Pacific region is forecasted to grow at an annual rate of 7.93% from 2026 to 2031, making it the fastest-growing regional market. This growth is fueled by rising middle-class incomes in China, India, and Southeast Asia, urbanization that increases exposure to Western confectionery formats, and the expansion of airport duty-free retail targeting affluent travelers. China and India recorded approximately 18% annual growth in chocolate confectionery consumption, while Japan and South Korea lead in premium adoption through department-store concessions and a strong gift-set culture. However, cultural and regulatory barriers fragment the region. For example, Indonesia's halal certification deadline in October 2026, under Government Regulation Number 42 of 2024, requires all food and beverage products to display Badan Penyelenggara Jaminan Produk Halal (BPJPH) halal approval or "Non-Halal" labeling, effectively excluding alcohol-infused chocolates unless reformulated. Mondelez expanded its partnership with Evirth, a cakes and pastries manufacturer in China, to leverage brands and create premium offerings in the rapidly growing Chinese bakery segment, showcasing how multinational confectioners adapt to local preferences.

North America, South America, and the Middle East and Africa collectively represent the remaining market share. In the United States, fragmented state-by-state alcohol regulations deter multinational players like Lindt from importing liqueur-filled chocolates. Canada and Mexico have more streamlined federal oversight, but lower per capita chocolate consumption and price sensitivity limit the penetration of the premium segment. In South America, Brazil's Cacau Show dominates domestic distribution through a franchise model emphasizing affordability and local flavors. Meanwhile, Argentina, Colombia, Chile, and Peru remain underpenetrated due to economic volatility and import tariffs on premium spirits.

Competitive Landscape

The liquor chocolate market shows moderate concentration, with established confectionery multinationals, specialist artisans, and regional players coexisting. While no single entity dominates the market, each leverages unique competitive strengths. Companies such as Mars, Lindt, Ferrero, and Mondelez International benefit from global distribution networks, decades of brand equity, and procurement scale, which help mitigate cocoa-price volatility. However, they face challenges such as regulatory complexities and margin pressures in alcohol-infused product lines, which represent a small portion of their overall portfolios.

In December 2025, Mars completed a USD 36 billion acquisition of Kellanova, creating a combined snacking business that spans salty, sweet, and alcohol-adjacent categories. Similarly, Mondelez International explored a potential takeover of Hershey in late 2024, a move that could consolidate nearly half of the global chocolate market under three major players. This consolidation is expected to influence duty-free assortments, co-branding strategies, and sustainability initiatives.

Specialist players, including Anthon Berg, Abtey, Neuhaus, and Godiva, maintain their artisan positioning through limited-edition collaborations with distilleries, premium retail placements, and storytelling that emphasizes heritage and craftsmanship. White-space opportunities in the market include alcohol-free "mocktail" chocolates, which replicate spirit flavor profiles without regulatory challenges. These products enable entry into Muslim-majority countries and appeal to health-conscious consumers participating in trends such as Dry January or reducing alcohol consumption.

Liquor Chocolate Industry Leaders

Mars Incorporated

Chocoladefabriken Lindt & Sprüngli AG

Ferrero International S.A.

Abtey Chocolaterie

Savencia Fromage & Dairy Suisse SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mondelez International inaugurated a CHF 65 million Toblerone Center of Excellence in Bern, Switzerland, with Swiss President Guy Parmelin attending the ceremony. The facility includes a new production line and expanded chocolate, nougat, and mass-production capabilities to enhance capacity and support innovation efforts.

- January 2026: LOTTE Corporation launches "Rakkus," marking the first collaboration between its top-selling liquor chocolates, "Rummy" and "Bacchus," combining their unique flavors into a single product for the first time.

- December 2025: Mars Incorporated finalized its USD 36 billion acquisition of Kellanova, forming a combined snacking business that encompasses salty, sweet, and alcohol-adjacent categories. This acquisition strengthens Mars' position as a key player in global confectionery and snack distribution.

Global Liquor Chocolate Market Report Scope

Liquor chocolates are produced using cocoa bean nibs, which contribute to their unique taste and texture. The market is categorized based on type, nature, distribution channel, and geography. By type, the market is divided into bars, tablets, box assortments, and others. By nature, it is segmented into organic and conventional. Distribution channels include supermarkets/hypermarkets, specialty stores, online retail stores, and other channels. Geographically, the study covers key regions such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD and volume in tonnes for all the abovementioned segments.

| Bar |

| Tablets |

| Box Assortment |

| Other Types |

| Organic |

| Conventional |

| Supermarkets and Hypermarkets |

| Speciality Stores |

| Online Retail |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Bar | |

| Tablets | ||

| Box Assortment | ||

| Other Types | ||

| By Nature | Organic | |

| Conventional | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Speciality Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global sales value for liquor chocolates by 2031?

Sales are expected to reach USD 1.53 billion in 2031, reflecting a 7.08% CAGR from 2026.

Which product format is expanding the quickest?

Single-serve bars are forecast to post the fastest growth, advancing at an 8.28% CAGR between 2026 and 2031.

Do alcohol regulations limit cross-border e-commerce?

Yes, many brands keep alcohol content below 0.5% by volume so they can ship direct-to-consumer without triggering federal excise tax or state-level liquor licensing.

Why are liquor-chocolate bars popular with travelers?

Bars fit hand-luggage rules, deliver portion control, and command premium duty-free margins, making them attractive impulse purchases in airports.

How does halal certification shape demand in Asia-Pacific?

Indonesia and Malaysia require halal approval or “Non-Halal” labeling, so brands develop alcohol-free “mocktail” chocolates to stay accessible during Ramadan and other gifting seasons.

Page last updated on: