Middle East Polyethylene Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.23 Billion |

| Market Size (2026) | USD 13.77 Billion |

| Market Size (2031) | USD 16.79 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

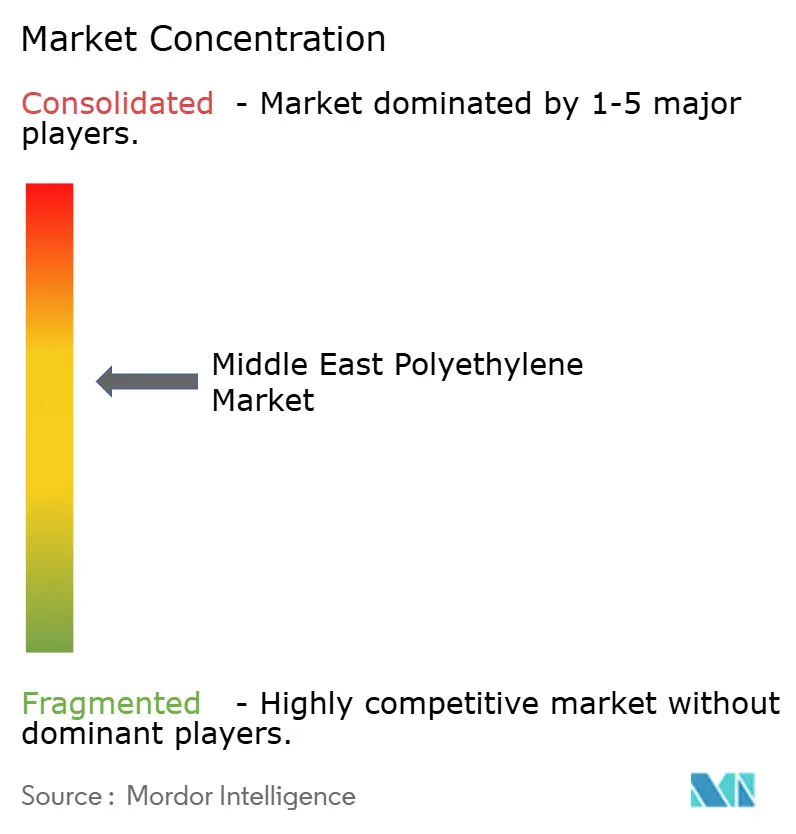

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Polyethylene Market Analysis by Mordor Intelligence

The Middle East Polyethylene Market size was valued at USD 13.23 billion in 2025 and estimated to grow from USD 13.77 billion in 2026 to reach USD 16.79 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031). Maturing regional supply, strong state-backed investments, and resilient packaging demand keep growth on a steady trajectory. Saudi Arabia, anchored by SABIC’s 4.01 million-tonne annual output, remains the largest producer and exporter, while the United Arab Emirates delivers the fastest capacity expansion as Borouge’s fourth phase at Ruwais comes onstream. Petrochemical diversification strategies under Saudi Arabia’s National Industrial Strategy and the UAE’s AED 294 billion program aim to reinforce regional self-sufficiency, mitigate feedstock risk, and open up export opportunities to Africa and South Asia. Infrastructure megaprojects—including district cooling networks, desalination pipelines, and renewable-energy interconnectors—add a countercyclical cushion for pipe and cable-grade consumption. Consolidation moves, such as ADNOC’s planned merger of Borouge, Borealis, and Nova Chemicals, signal a tightening of pricing discipline and greater bargaining power with converters.

Key Report Takeaways

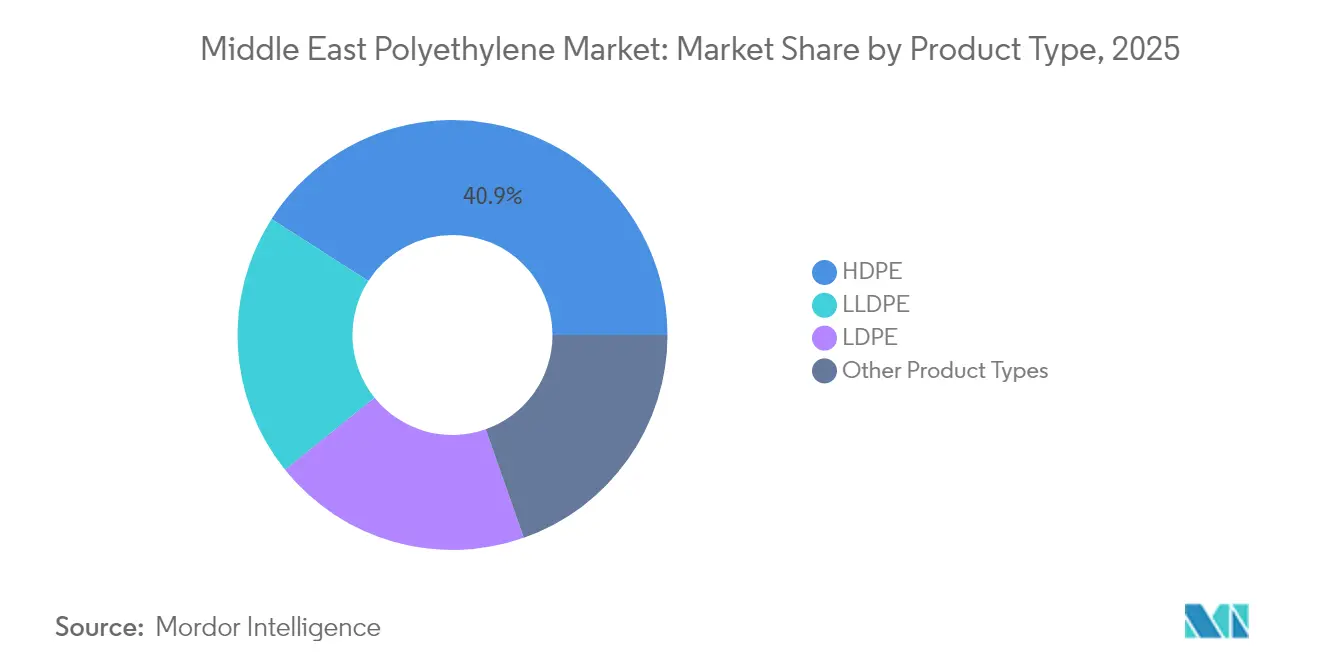

- By product type, high-density polyethylene led with 40.92% of the 2025 Middle East polyethylene market share, whereas linear low-density polyethylene is forecast to advance at a 5.05% CAGR through 2031.

- By application, films and sheets accounted for 46.05% of the Middle East polyethylene market size in 2025, and wires and cables are projected to grow at a 5.12% CAGR to 2031.

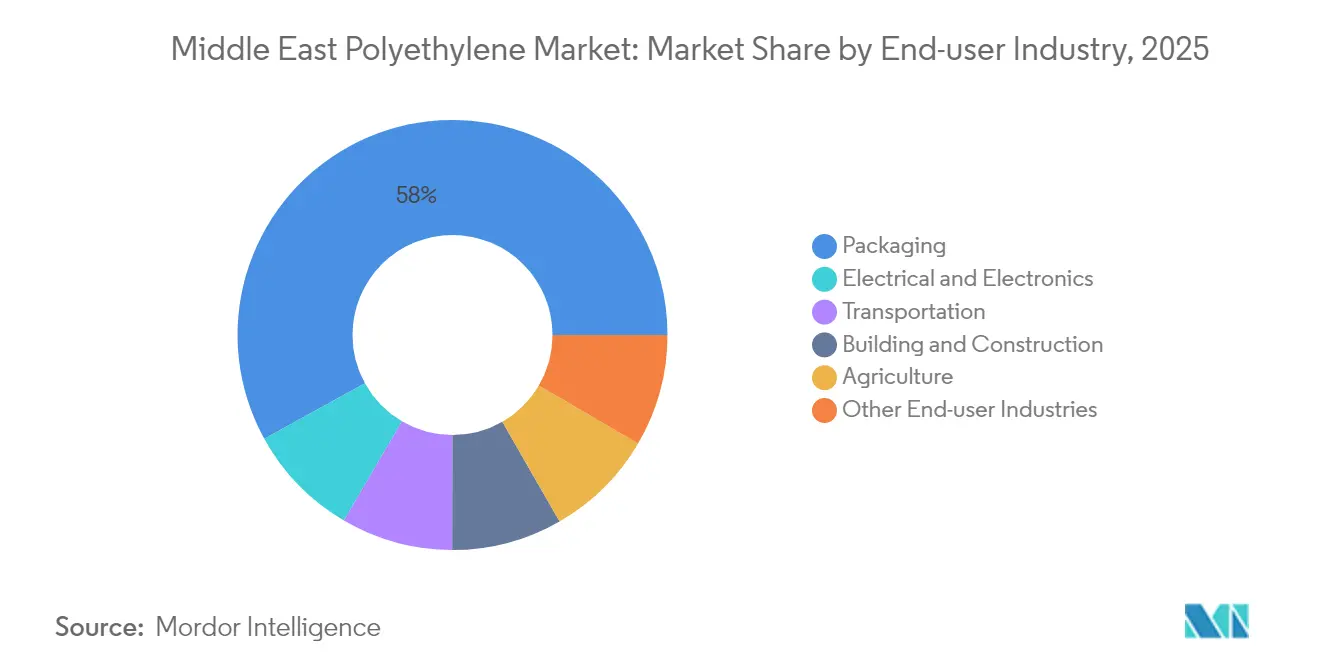

- By end-user, packaging captured a 58.02% revenue share in 2025; the electrical and electronics sector is the fastest-growing demand center, tracking a 4.99% CAGR through 2031.

- By geography, Saudi Arabia held 39.35% of the 2025 market share, while the United Arab Emirates recorded the highest regional CAGR of 4.84% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Polyethylene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaging demand growth in FMCG and e-commerce | +1.2% | Saudi Arabia, UAE, Qatar, spillover to Egypt and Jordan | Medium term (2-4 years) |

| Automotive and electronics uptake for replacement parts | +0.8% | UAE free zones, Saudi Arabia industrial clusters | Medium term (2-4 years) |

| State-led GCC petrochemical diversification | +1.5% | Saudi Arabia, UAE, Qatar, Kuwait | Long term (≥ 4 years) |

| Surge in PE pipe demand for district cooling networks | +0.9% | Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Mandatory recyclate-content rules | +0.6% | Saudi Arabia, UAE, pilot projects in Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Rigid and Flexible Packaging Demand in FMCG and E-Commerce

The regional flexible-packaging market reached USD 10 billion in 2024, with Saudi Arabia leading adoption of recyclable mono-material films that simplify post-consumer sorting under SASO’s 2021 regulations[1]Standards Department, “Technical Regulation for Packaging and Waste Management,” Saudi Standards, Metrology and Quality Organization, saso.gov.sa. Fast-growing e-commerce platforms such as Amazon.ae and Noon rely on polyethylene mailers, bubble wrap, and air pillows, driving annual protective packaging growth into the high teens. Brand owners shifting to linear low-density polyethylene films meet recyclability targets and benefit from downgauging that cuts material use by up to 15%. These dynamics underpin LLDPE’s 5.12% CAGR outlook while cementing films as the single largest application throughout the forecast window.

Industrial Uptake for Automotive and E&E Replacement Parts

Electric-vehicle assembly zones in Abu Dhabi, Dubai, and Saudi Arabia’s NEOM project specify polyethylene grades for battery housings, cable insulation, and under-hood components. Borouge’s 100,000 tpa cross-linked polyethylene unit at Ruwais supplies specialty compounds for subsea power cables that link expanding solar farms to national grids. Data-center construction tied to sovereign artificial-intelligence programs accelerates consumption of flame-retardant HDPE conduits, supporting a 5.08% CAGR in the electrical and electronics segment.

State-Led Diversification into Petrochemicals Across GCC

Saudi Arabia earmarked USD 600 billion for manufacturing, aiming to lift plastics production to 115.7 million tonnes by 2035[2]Editorial Desk, “National Industrial Strategy Targets Manufacturing Expansion,” Ministry of Investment Saudi Arabia, misa.gov.sa. The UAE’s Ta’ziz hub awarded AED 7.34 billion in EPC contracts for a chemicals port, storage, and pipelines that will export 4.7 million tonnes of methanol, ammonia, and polyolefins by 2028. Qatar’s 1.68 million-tonne HDPE line at Ras Laffan is expected to come online in 2026, with swing capability to serve either Asia or Europe. Meanwhile, Iran aims to roll out an 8.6 million-tonne capacity under its Seventh National Development Plan, despite a 42% gas shortage, as reported by NPC.IR. These investments deepen the Middle East polyethylene market’s export reach and intensify inter-regional competition.

Surge in PE Pipe Demand for District Cooling and Water-Saving Networks

Saudi Arabia’s district cooling capacity is slated to exceed 1.5 million refrigeration tonnes by 2030, with polyethylene pipes chosen for their corrosion resistance and trenchless installation advantages. Abu Dhabi and Dubai mandate HDPE conduits for new commercial districts, while precision irrigation mandates a 30% reduction in agricultural water use when polyethylene drip lines replace flood irrigation. Pipe demand thus offers a stable outlet that cushions the Middle East polyethylene market during packaging-cycle downturns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution by polypropylene and PET | –0.7% | Saudi Arabia, UAE, Egypt | Medium term (2-4 years) |

| Feedstock price volatility | –1.1% | Ethane-rich Saudi Arabia, UAE; naphtha-exposed Iran, Egypt | Short term (≤ 2 years) |

| Import tariffs and compliance hurdles in Africa | –0.5% | GCC exporters serving Egypt, Kenya, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Readily Available Substitutes Such as PP and PET

Polypropylene and polyethylene terephthalate gain market share in hot-fill containers, beverage bottles, and automotive trim, where thermal resistance outperforms that of polyethylene. Borouge’s polypropylene capacity expansion to 720,000 tpa and SABIC’s PP5707N grade development diversify portfolios and hedge against polyethylene substitution pressure. Price spreads can swing 20–30% within a quarter during crude oil volatility, prompting converters to switch resins when cost advantages emerge.

Feedstock Price Volatility and Import Tariffs in African Outlets

A 42% gas-feedstock shortfall reported by Iran’s National Petrochemical Company shaved cracker utilization and forced curtailments in 2024. Naphtha-based sites in Egypt track Brent crude swings; margins tighten sharply once oil exceeds USD 85 per barrel. Egypt’s GOEIC registration now requires ISO 9001 credentials and Arabic-language dossiers, adding up to 12 weeks of lead time and approximately 6% to landed costs for Gulf exporters. Red Sea disruptions halved Suez Canal throughput, prompting many Middle East polyethylene market players to reroute via the Cape of Good Hope, which quadrupled container costs and eroded Gulf cost advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: HDPE Dominates, LLDPE Gains in Specialty Films

High-density polyethylene retained 40.92% of the 2025 Middle East polyethylene market share, buoyed by demand for blow-molded drums, IBCs, and large-diameter pressure pipes. Tasnee’s 400,000 tpa HDPE train at Jubail supplies raffia, injection molding, and pipe resins that meet ISO 4427 standards. Low-density polyethylene performs well in shrink films and lamination layers, while linear low-density polyethylene experiences the strongest growth, aided by Borstar Enhanced grades that enable 15–20% downgauging without compromising mechanical properties.

Down-gauged e-commerce mailers, puncture-resistant stretch films, and clarity-enhanced greenhouse covers drive LLDPE’s forecast CAGR to 5.05%, narrowing its contribution to the Middle East polyethylene market size to approximately one-third by 2031. Ultra-high-molecular-weight polyethylene and EVA copolymers occupy niche medical, conveyor, and photovoltaic applications, although they collectively account for a share below mid-single digits.

By Application: Films Lead, Wires and Cables Accelerate

Films and sheets captured 46.05% of the 2025 demand, mirroring a significant value in the flexible packaging sector that supplies FMCG and e-commerce customers. Government-backed producer-responsibility frameworks drive the adoption of mono-materials, reinforcing polyethylene’s role as a recyclable-friendly substrate.

Cross-linked polyethylene insulation for subsea interconnectors and data-center cabling fuels a 5.12% CAGR in wires and cables. Borouge’s 100,000 tpa plant operates using peroxide cross-linking to produce cable grades certified for continuous service at 90°C. Injection-molded automotive parts and blow-molded fuel tanks round out demand, with rotomolding and extrusion coating accounting for residual volumes.

By End-User Industry: Packaging Prevails, Electrical Surges

Packaging end-users consumed 58.02% of all resin in 2025, driven by demographic tailwinds and urbanization rates above 80% in Saudi Arabia and the UAE. Protective-packaging formats—air pillows, foam, bubble wrap—scale with e-commerce parcel flows that surpassed several hundred million transactions in 2024.

Electrical and electronics demand expands at a 4.99% CAGR as utility-scale renewables, EV charging corridors, and hyperscale data centers multiply cable-grade purchases. ADNOC’s Ta’ziz complex will localize the production of vinyl chloride monomer and caustic soda, securing upstream inputs for wire-and-cable jackets and further solidifying polyethylene’s role in the segment. Building, agriculture, and consumer-goods categories together account for the remaining balance.

Geography Analysis

Saudi Arabia held 39.35% of 2025 Middle East polyethylene market share owing to 4.01 million tonnes of SABIC capacity, Tasnee’s dual HDPE/LDPE trains, and generous ethane allocations that keep integrated cracker margins near 88%. District-cooling installations in Riyadh and Jeddah and SASO recyclability mandates sustain domestic demand, while Jubail and Yanbu industrial cities provide a hub for export logistics under the High Commission for Industrial Security.

The United Arab Emirates records the top regional growth pace of 4.84% CAGR as Borouge lifts Ruwais nameplate to 6.4 million tonnes by 2025, underpinning the country’s rise as the leading polyethylene exporter after the planned Borouge–Borealis–Nova merger. Ta’ziz infrastructure investments worth AED 7.34 billion add a chemicals port and storage facilities that streamline outbound volumes toward Africa and South Asia.

Qatar brings a 1.68 million-tonne HDPE project online at Ras Laffan in 2026, while Kuwait and Oman contribute incremental swing output. Iran aims for 8.6 million tonnes under its Seventh Plan but faces gas shortfalls that limit near-term utilization. Rest-of-Middle-East nations, led by Egypt’s 7 million-tonne build-out and cross-border projects under the Integrated Industrial Partnership, round out the regional landscape.

Competitive Landscape

The Middle East Polyethylene Market is moderately consolidated. ADNOC’s USD 9.7 billion deal to merge Borouge with Borealis and acquire Nova Chemicals establishes a USD 60 billion polyolefins champion that will operate with a combined polyethylene and polypropylene capacity of 13.6 million tonnes upon completion in 2026. Strategic thrusts center on feedstock integration, specialty-grade development, and circular economy positioning. SABIC’s TRUCIRCLE mechanical-recycling initiative secures offtake agreements with global FMCG companies seeking certified circular resins. Borouge’s Borstar Enhanced PE delivers downgauging advantages prized by film converters wrestling with volatile feedstock costs.

Middle East Polyethylene Industry Leaders

Dow

Exxon Mobil Corporation

SABIC

Qatar Petrochemical Company (QAPCO)

Borouge

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SABIC teamed up with Iyris, a pioneer in sustainable agricultural climate technology, and Napco National. Together, they've developed a new greenhouse roof, featuring certified circular polyethylene (PE) sourced from SABIC’s Trucircle portfolio, which is already being utilized in Saudi Arabia’s National Food Production Initiative (NFPI).

- February 2025: Saudi Arabia's Ministry of Energy allocated the necessary feedstock for establishing industrial complexes by the National Industrialization Company (Tasnee) and the Sahara International Petrochemical Company (Sipchem) in Jubail Industrial City. The project will have a production capacity of nearly 3.3 million metric tonnes of polyethylene and methyl tert-butyl ether (HDPE, LLDPE, MTBE).

Middle East Polyethylene Market Report Scope

Polyethylene (PE) is a light, flexible synthetic resin created by polymerizing ethylene. Polyethylene is a member of the essential polyolefin resin family. It is the most commonly used plastic in the world, found in everything from clear food wraps and shopping bags to detergent bottles and automotive fuel tanks. It can also be split or spun into synthetic fibers or made to have rubber-like elastic characteristics.

The Middle Eastern polyethylene market is segmented into product type, application, end-user industry, and geography. By product type, the market is segmented into HDPE, LDPE, LLDPE, and other product types. By application, the market is segmented into blow molding, films and sheets, injection molding, pipes and conduits, wires and cables, and other applications. By end-user industry, the market is segmented into packaging, transportation, electrical and electronics, building and construction, agriculture, and other end-user industries. The report covers the market size and forecast for the Middle Eastern polyethylene market in 6 countries across the Middle East. For each segment, the market sizing and forecasts have been done based on volume in tons.

| HDPE |

| LDPE |

| LLDPE |

| Other Product Types |

| Blow Molding |

| Films and Sheets |

| Injection Molding |

| Pipes and Conduits |

| Wires and Cables |

| Other Applications |

| Packaging |

| Transportation |

| Electrical and Electronics |

| Building and Construction |

| Agriculture |

| Other End-user Industries |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Iran |

| Rest of Middle East |

| By Product Type | HDPE |

| LDPE | |

| LLDPE | |

| Other Product Types | |

| By Application | Blow Molding |

| Films and Sheets | |

| Injection Molding | |

| Pipes and Conduits | |

| Wires and Cables | |

| Other Applications | |

| By End-user Industry | Packaging |

| Transportation | |

| Electrical and Electronics | |

| Building and Construction | |

| Agriculture | |

| Other End-user Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Iran | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current value of the Middle East polyethylene market?

The market is valued at USD 13.77 billion in 2026 and is projected to reach USD 16.79 billion by 2031.

Which country leads regional polyethylene production?

Saudi Arabia contributes 39.35% of 2025 output, backed by SABIC’s 4.01 million-tonne integrated capacity.

Which segment grows fastest through 2031?

Wires and cables, supported by cross-linked polyethylene grades, show a 5.12% CAGR through 2031.

How will recyclate-content mandates affect resin demand?

Regulations in Saudi Arabia and the UAE push converters toward virgin–recycle blends, lifting demand for certified circular polyethylene.

What are the key risks to Middle East exporters?

Feedstock price swings, logistics disruptions in the Red Sea, and rising import tariffs in African markets can erode cost advantages.

Page last updated on: