Middle East Fluoropolymer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

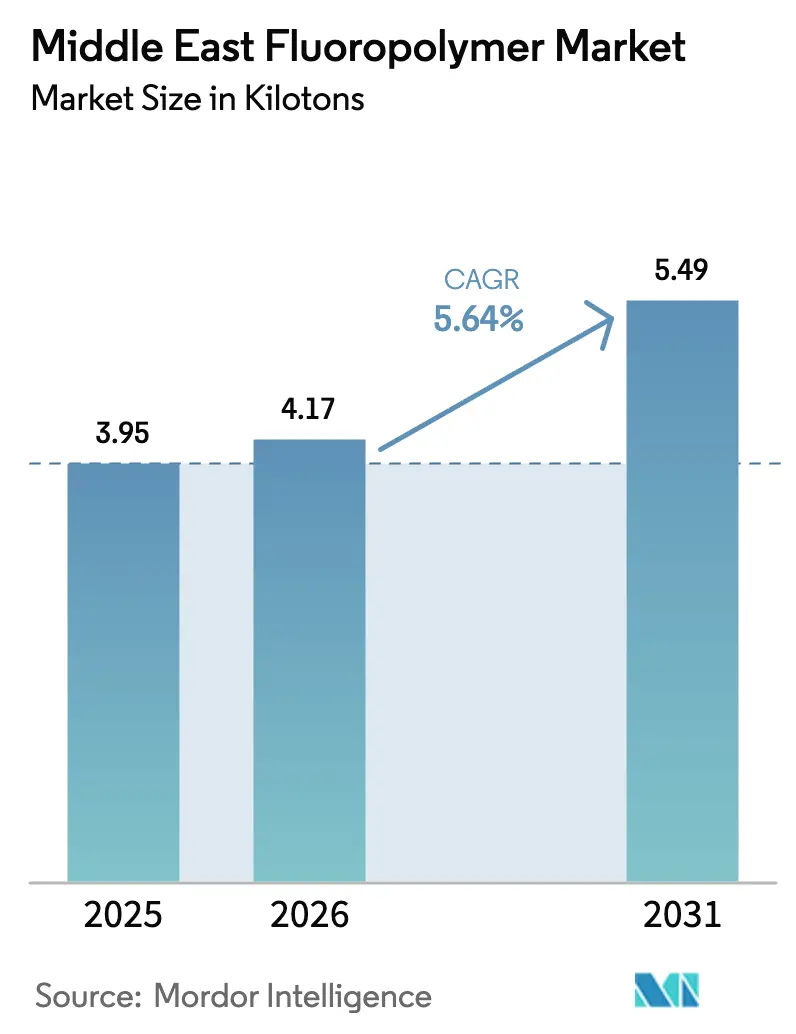

| Base Year Market Size (2025) | 3.95 kilotons |

| Market Volume (2026) | 4.17 kilotons |

| Market Volume (2031) | 5.49 kilotons |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

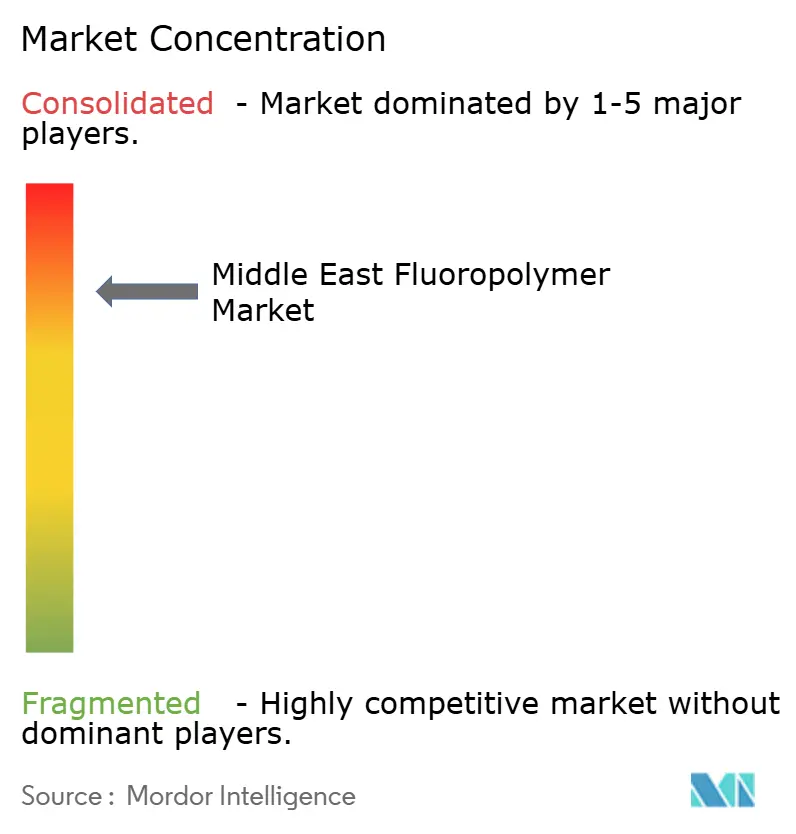

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Fluoropolymer Market Analysis by Mordor Intelligence

The Middle East Fluoropolymer Market size was valued at 3.95 kilotons in 2025 and estimated to grow from 4.17 kilotons in 2026 to reach 5.49 kilotons by 2031, at a CAGR of 5.64% during the forecast period (2026-2031). Robust petrochemical investments, large-scale power-grid upgrades, and fast-growing desalination capacity anchor demand across Saudi Arabia, the United Arab Emirates, and emerging industrial clusters in Qatar, Kuwait, and Oman. PTFE remains indispensable for high-temperature refinery and aerospace maintenance, yet FEP and PVDF volumes accelerate as the region builds electrified infrastructure, semiconductor cleanrooms and battery gigafactories. Local policymakers promote backward integration of specialty polymers into national industrial strategies, while supply-chain risks tied to PFAS regulation and Chinese PTFE tariffs nudge buyers toward regional sourcing. Strategic acquisitions, most notably ADNOC’s takeover offer for Covestro, signal more intense competition for high-value fluoropolymer applications[1]“ADNOC takeover offer for Covestro successful,” Covestro AG, covestro.com .

Key Report Takeaways

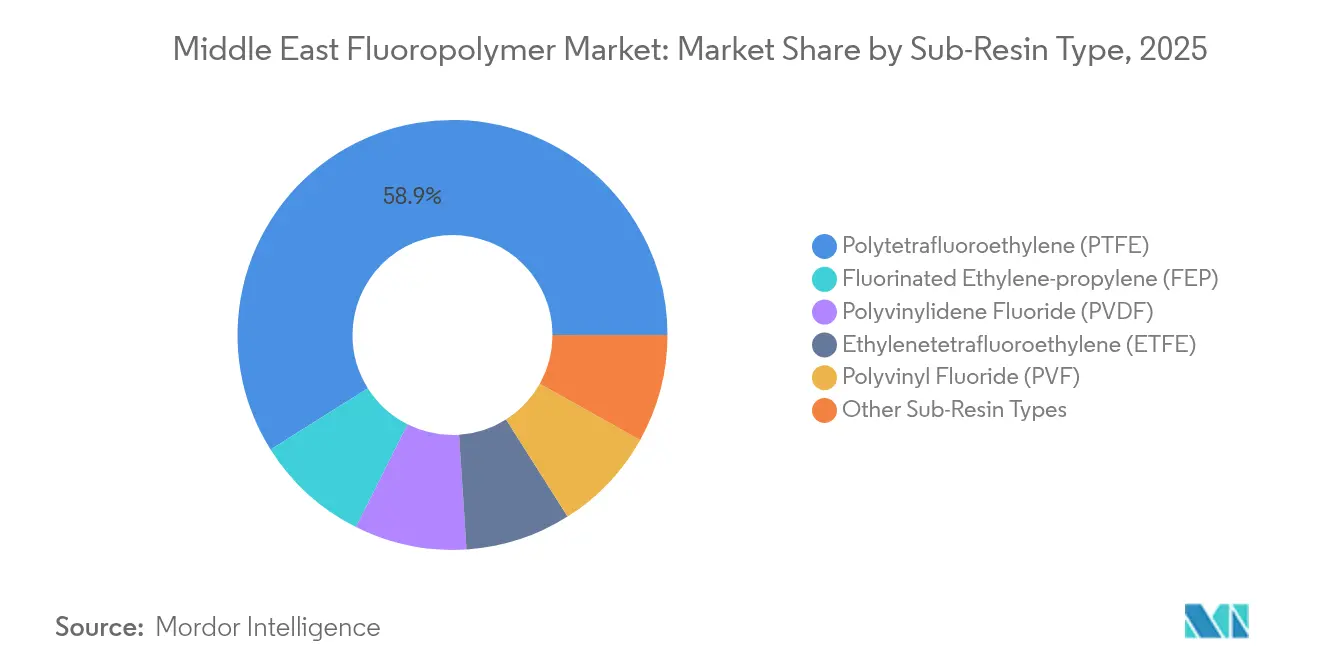

- By sub-resin, Polytetrafluoroethylene held 58.94% of the Middle East fluoropolymer market share in 2025. Fluorinated Ethylene-propylene is projected to grow at a 6.55% CAGR through 2031.

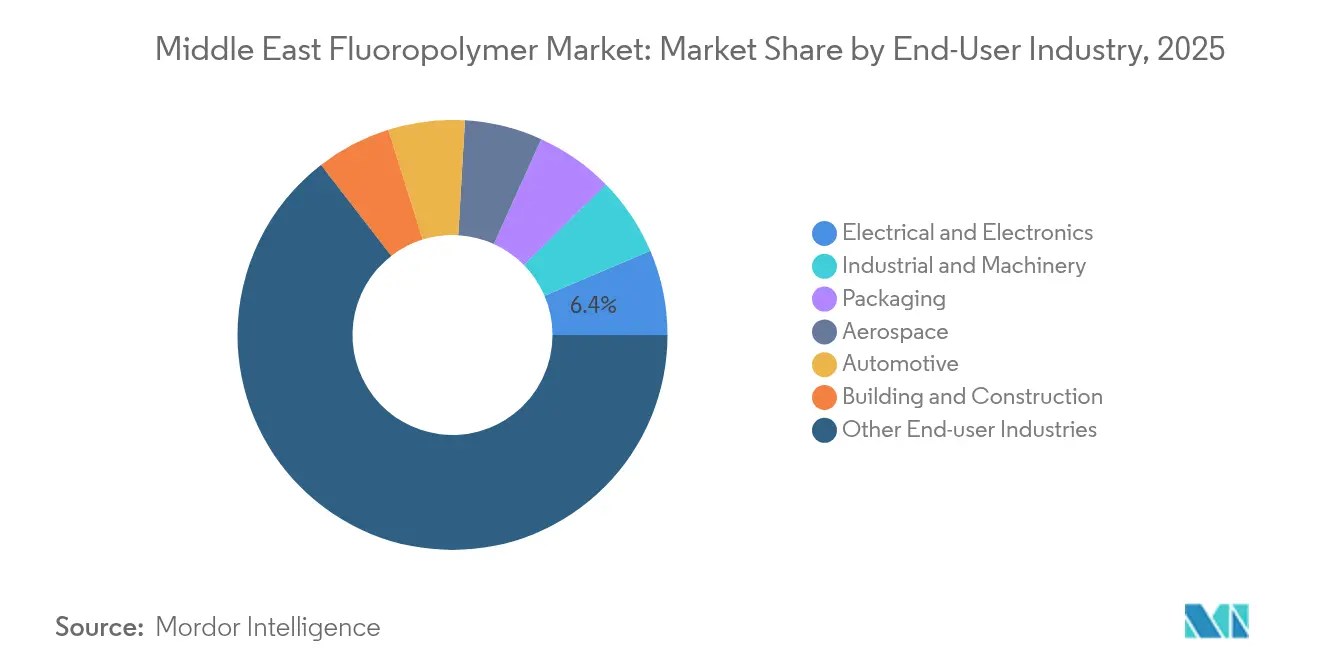

- By end-user, “Other industries” commanded a 64.52% share of the Middle East fluoropolymer market size in 2025. Electrical and Electronics is advancing at a 6.7% CAGR to 2031.

- By geography, the Rest of the Middle East captured a 56.35% share in 2025 and is progressing at a 5.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Fluoropolymer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust petrochemical project pipeline fuels specialty-polymer demand | +1.80% | Saudi Arabia, UAE, Qatar core with spillover to Kuwait | Medium term (2-4 years) |

| Electrification push in GCC drives high-performance wire-cable insulation | +1.20% | GCC-wide, concentrated in Saudi Arabia and UAE infrastructure corridors | Short term (≤ 2 years) |

| Rapid build-out of PVDF-based Li-ion battery gigafactories | +0.90% | UAE primary, with expansion potential to Saudi Arabia | Medium term (2-4 years) |

| Water-stress led desalination boom boosts PVDF membrane uptake | +0.70% | Regional, with highest intensity in Saudi Arabia and UAE coastal areas | Long term (≥ 4 years) |

| Localization incentives for aerospace MRO using ETFE & PFA | +0.50% | UAE and Saudi Arabia aviation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Petrochemical Project Pipeline Fuels Specialty-Polymer Demand

QatarEnergy, in collaboration with Chevron Phillips Chemical Company LLC, is developing a USD 6 billion integrated polymers complex in Ras Laffan Industrial City, Qatar[2]“QatarEnergy, Chevron Phillips Chemical to begin construction on integrated polymers complex in Ras Laffan Industrial City, Qatar,” Chevron Phillips Chemical Company LLC., cpchem.com. Advanced downstream units intensify chemical resistance and thermal-cycling demands, embedding long-term pull for high-grade fluoropolymers across refinery and specialty-chemical flows. Local governments link project approvals to in-region material supply, nudging distributors to hold inventory closer to plant sites. Engineering contractors are increasingly awarding framework agreements for gasket kits, pump liners, and valve seats made of fluorinated resins, thereby locking in predictable order streams that stabilize production planning for global suppliers. As Middle Eastern producers climb the value ladder, integrated complexes keep fluoropolymer demand decoupled from Western economic cycles and tied instead to domestic diversification timetables.

Electrification Push in GCC Drives High-Performance Wire-Cable Insulation

Mega-projects such as NEOM in Saudi Arabia and UAE’s solar and wind arrays need cables that retain dielectric strength above 150 °C, resist sand abrasion and meet strict fire-safety codes. FEP and ETFE jackets outperform conventional polyethylene in these harsh desert grids, while PVDF and PFA serve bus-ducts and switchgear. Borouge’s cable-grade XLPE compound and related fluoropolymer innovations support looped transmission circuits for 220 kV submarine lines that connect offshore wind farms to population centers. Procurement teams stipulate long service life to avoid costly outages during peak heat seasons, amplifying uptake of higher-cost but longer-lasting fluoropolymer insulation. Regional power utilities also embed smart-grid sensors that raise the operating temperature envelope, extending the applications where fluoropolymers are economically justified. With multiple GCC states targeting renewable penetration above 25% by 2030, cable demand forms a resilient growth spine for the Middle East fluoropolymer market.

Rapid Build-out of PVDF-Based Li-ion Battery Gigafactories

The USD 3.20 billion Statevolt facility in the UAE and announced cell plants in Saudi industrial zones consume PVDF binders at 2–4 kg per MWh of capacity, translating into steady multi-kiloton annual offtake. Morocco’s Fluoralpha HF project offers future feedstock security, reducing reliance on Chinese intermediates and shortening delivery cycles for regional cathode-active-material lines. Gigafactory developers sign multi-year offtake agreements to lock in PVDF supply, which improves visibility for polymer producers and encourages consideration of local compounding units. Banking institutions channel green-finance instruments toward domestic battery value chains, indirectly supporting the fluoropolymer consumption tied to cathode, separator and current collector components. Rising electric-vehicle assembly hubs in Jebel Ali free zone are likely to compound this pull as downstream pack integration shifts to the region.

Localization Incentives for Aerospace MRO Using ETFE & PFA

Dubai and Riyadh aviation hubs expand maintenance, repair and overhaul capabilities that rely on ETFE wire harnesses, PFA fuel-line tubing and corrosion-resistant PTFE seals. Government offsets reward airlines for sourcing parts remanufactured within free zones, granting tax incentives that indirectly lift local fluoropolymer consumption. Aircraft operating in desert climates require more frequent component replacement, further widening the maintenance market. As fleet mix evolves to next-generation wide-bodies with greater composites content, fluoropolymers remain critical for chemical-resistant bleed-air and hydraulic systems, securing multi-year replacement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS phase-out legislation uncertainty | -1.10% | Global impact with regional supply chain disruptions | Medium term (2-4 years) |

| Limited regional fluorochemical feedstock (HF) capacity | -0.80% | Regional, with highest impact in UAE and Saudi Arabia | Long term (≥ 4 years) |

| High import tariffs on Chinese PTFE since 2024 | -0.60% | Regional import-dependent markets, particularly smaller GCC states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PFAS Phase-Out Legislation Uncertainty

Evolving European and Gulf regulatory drafts blur future compliance requirements, prompting some processors to delay plant upgrades or dual-source volumes. Although PTFE, PVDF and FEP enjoy essential-use exemptions for aerospace and semiconductors, buyers still factor potential cost of substitution into capital planning. Documentation burdens rise, with downstream users demanding full material disclosure statements. Global resin majors strengthen stewardship programs, but smaller distributors struggle with traceability, causing intermittent supply gaps. The uncertainty skews purchasing toward suppliers perceived to have deeper regulatory insight, consolidating demand with larger incumbents.

High Import Tariffs on Chinese PTFE Since 2024

Regional trade authorities imposed safeguard duties on specific Chinese PTFE grades, raising landed costs for custom compounders serving niche sealing and bearing niches. Smaller GCC players with modest purchasing volume feel the brunt, passing costs to end-users who may explore non-fluorinated substitutes for marginal applications. Larger buyers leverage global contracts to mitigate, but spot availability tightens, particularly during refinery maintenance seasons. The tariff policy aims to shield future regional polymerization ventures; however, in the near term it constrains supply flexibility and adds price volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Resin Type: PTFE Retains Lead While FEP Accelerates

PTFE generated 58.94% of the Middle East fluoropolymer market share in 2025 thanks to its unmatched heat and chemical resistance in refinery, chemical and aerospace settings. Its installed base across pipe-liners and pump components ensures recurring replacement demand. FEP, however, leads growth at a 6.55% CAGR because its easier processability suits high-speed cable extrusion and semiconductor wafer carriers. Regional wire-and-cable producers retrofit lines to co-extrude FEP over copper and aluminum conductors used in solar farms and HVDC links.

PVDF volumes expand steadily on the back of desalination membranes and binder usage in battery cells. New hollow-fiber spinning units slated for Jebel Ali can localize membrane fabrication, further tying PVDF consumption to domestic water projects. Specialty grades like ETFE and PFA serve aviation and architectural film niches, with ETFE roofing films gaining traction in sports facilities planned for the FIFA Asian Cup. Niche copolymers for semiconductor wet benches and advanced filtration remain small in tonnage but deliver premium margins that attract distributors looking to diversify beyond bulk PTFE stocks.

Overall product-mix evolution nudges the Middle East fluoropolymer market toward higher-value segments. Supply partners tailor stock-keeping units to match local certification codes, reducing import delays. Training programs for compounders and fabricators spread process know-how, enabling substitution of PTFE in some gaskets with melt-processable alternatives that cut machining steps and scrap generation.

By End-User Industry: Electrical & Electronics Gains Momentum

“Other industries” collected 64.52% of the Middle East fluoropolymer market size in 2025 because the resin family permeates multiple process-industry touchpoints from acid-transfer tubing to non-stick release sheets. Petrochemical and general industrial plants remain baseline consumers even as they modernize. Electrical & Electronics, however, is projected to post the fastest 6.7% CAGR through 2031 as GCC grids digitize and data-center capacity multiplies. The segment covers high-frequency cables, PCB fabrication materials and cleanroom components.

Renewable-energy targets across the region require solar farms to link to load centers over long desert spans where peak temperatures exceed 50 °C. Fluoropolymer-insulated conductors maintain dielectric properties and suppress smoke generation, meeting new civil-defense codes. Semiconductor consortiums attracted by favorable tax regimes specify fluorinated piping for ultrapure chemicals and FEP-lined tanks, giving distributors a predictable sales channel. Aerospace MRO service bays add steady demand for heat-shrinkable PTFE sleeves that protect wiring beneath composite skins.

Packaging, building and construction and automotive remain smaller but stable consumers. PVDF architectural coatings win specifications for coastal façades facing saline spray, while battery electric buses in Riyadh trial PVDF separators and ETFE seal caps. Fluoropolymer uptake therefore spreads beyond conventional oil-and-gas uses, underscoring the region’s broader industrial pivot.

Geography Analysis

The rest of the Middle East, comprising Qatar, Kuwait, Oman, and others, accounted for 56.35% of the 2025 volume and is forecast to grow at a 5.88% CAGR, outpacing the overall Middle East fluoropolymer market. Qatar’s mega-cracker feeds downstream fluorinated intermediates while Kuwait’s refinery upgrades rely on PTFE gaskets and PVDF trays. Oman’s USD 250 million polymer complex lays the groundwork for regional compounding and R&D, shortening delivery lead times for membrane and cable producers. Logistic hubs in Doha and Duqm port connect Asian resin suppliers to GCC processors, reducing freight variability and allowing distributors to hold diversified stock closer to end-users.

Saudi Arabia boasts a substantial installed petrochemical base, ensuring a baseline PTFE consumption in corrosive process streams. Vision 2030 industrial programs and the NEOM smart-city build elevate demand for FEP and ETFE in power infrastructure and architectural elements. Desalination expansion with PVDF hollow fibers reinforces the continuous pull, while aviation maintenance clusters in Jeddah shift part sourcing toward PFA fuel hose kits. Import tariffs on Chinese PTFE, however, hit smaller fabricators in Riyadh and Dammam harder, prompting some to explore joint ventures for local sintering capacity.

The UAE retains its role as a commercial gateway. Dubai hosts the majority of regional fluoropolymer stock points, and Abu Dhabi’s in-house battery cell and composite plants provide captive demand for PVDF and PFA. Free-zone policies permit duty-free transit that smooths regional redistribution. The trading hub advantage slightly offsets the limited upstream feedstock, although Abu Dhabi’s partnership with SRF Limited to expand supply flexibility signals a gradual shift toward capacity building. Multinational resin producers establish technical service centers in Jebel Ali and Kizad to quickly troubleshoot local processing issues, thereby cementing customer loyalty.

Competitive Landscape

The Middle East fluoropolymer market remains highly consolidated, with global suppliers such as Chemours, Daikin and Arkema servicing clients through dedicated distributors and technical hubs. Contracts prioritize life-cycle support, not just raw-material price, because many applications involve long running hours under harsh conditions. Local players explore backward integration yet rely on licensing from incumbents to manage process safety and environmental compliance.

ADNOC’s acquisition of Covestro underscores a strategic pivot toward specialty polymers, potentially catalyzing regional PVDF or FEP production under new joint-venture structures. Meanwhile, AGC’s promotion of Fluon ETFE architectural film at Dubai façade conferences illustrates how value propositions increasingly hinge on durability claims relevant to desert environments. Chemours’ 2025 alliance with SRF secures extra capacity buffering against PFAS regulatory-driven disruptions and deepens supply optionality for Gulf customers.

Competition also sharpens on aftermarket services. Distributors invest in CNC machining for PTFE components tailored to refinery shutdown schedules, while membrane system integrators bundle PVDF elements with predictive maintenance analytics. Product stewardship programs differentiate suppliers as end-users scrutinize PFAS declarations. Collectively, these dynamics maintain pricing discipline and limit entry of unverified grades into critical applications.

Middle East Fluoropolymer Industry Leaders

AGC Inc.

Daikin Industries Ltd.

Dongyue Group

Syensqo

The Chemours Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Chemours Company has partnered with SRF Limited, a producer of industrial and specialty intermediates, including fluoropolymers. This agreement strengthens Chemours' global supply chain, enhances operational flexibility, and expands access to fluoropolymer capacity.

- April 2024: AGC Chemicals Europe, a subsidiary of AGC Inc., promoted its innovative Fluon ETFE FILM, a highly durable fluoropolymer film designed for architectural applications, at the Zak World of Façades conference on façade design and engineering in Dubai, United Arab Emirates.

Middle East Fluoropolymer Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Ethylenetetrafluoroethylene (ETFE), Fluorinated Ethylene-propylene (FEP), Polytetrafluoroethylene (PTFE), Polyvinylfluoride (PVF), Polyvinylidene Fluoride (PVDF) are covered as segments by Sub Resin Type. Saudi Arabia, United Arab Emirates are covered as segments by Country.| Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinyl Fluoride (PVF) |

| Polyvinylidene Fluoride (PVDF) |

| Other Sub-Resin Types |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| Saudi Arabia |

| United Arab Emirates |

| Rest of Middle East |

| By Sub-Resin Type | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinyl Fluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub-Resin Types | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the fluoropolymers market.

- Resin - Under the scope of the study, virgin fluoropolymer resins like Polytetrafluoroethylene, Polyvinylidene Fluoride, Polyvinylfluoride, Fluorinated Ethylene-propylene, Ethylenetetrafluoroethylene, etc. in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms