Middle East Polyamide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

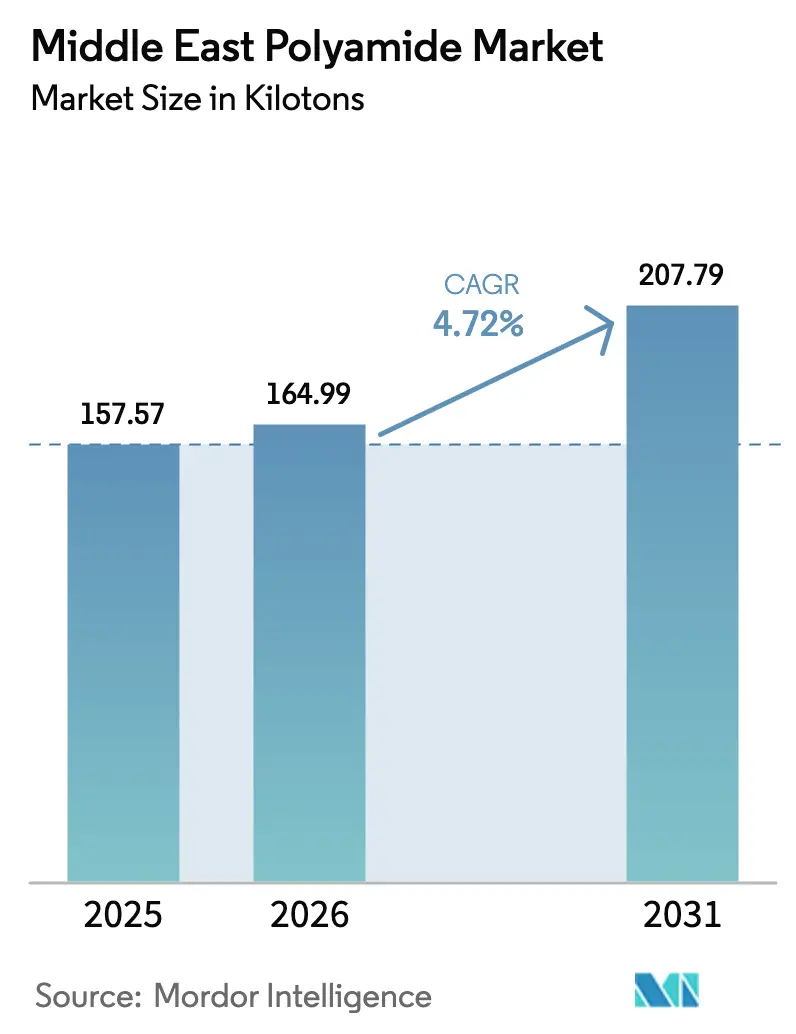

| Base Year Market Size (2025) | 157.57 kilotons |

| Market Volume (2026) | 164.99 kilotons |

| Market Volume (2031) | 207.79 kilotons |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Polyamide Market Analysis by Mordor Intelligence

Middle East Polyamide Market size in 2026 is estimated at 164.99 kilotons, growing from 2025 value of 157.57 kilotons with 2031 projections showing 207.79 kilotons, growing at 4.72% CAGR over 2026-2031. Abundant, competitively priced feedstocks underpinned by integrated petrochemical complexes keep production costs low while Vision 2030 and similar diversification agendas funnel capital into downstream polymer processing. Rapid growth in automotive, electronics, and advanced packaging accelerates demand for higher-value grades, prompting producers to expand compounding capacity near end-use hubs. Vertical integration by national champions such as Saudi Aramco shields margins from crude-oil volatility, and sustained foreign direct investment creates collaborative ecosystems that shorten supply chains and stimulate technology transfer. The Middle East Polyamide market continues to benefit from intra-GCC trade agreements that harmonize technical standards and lower tariff barriers for specialty polymers.

Key Report Takeaways

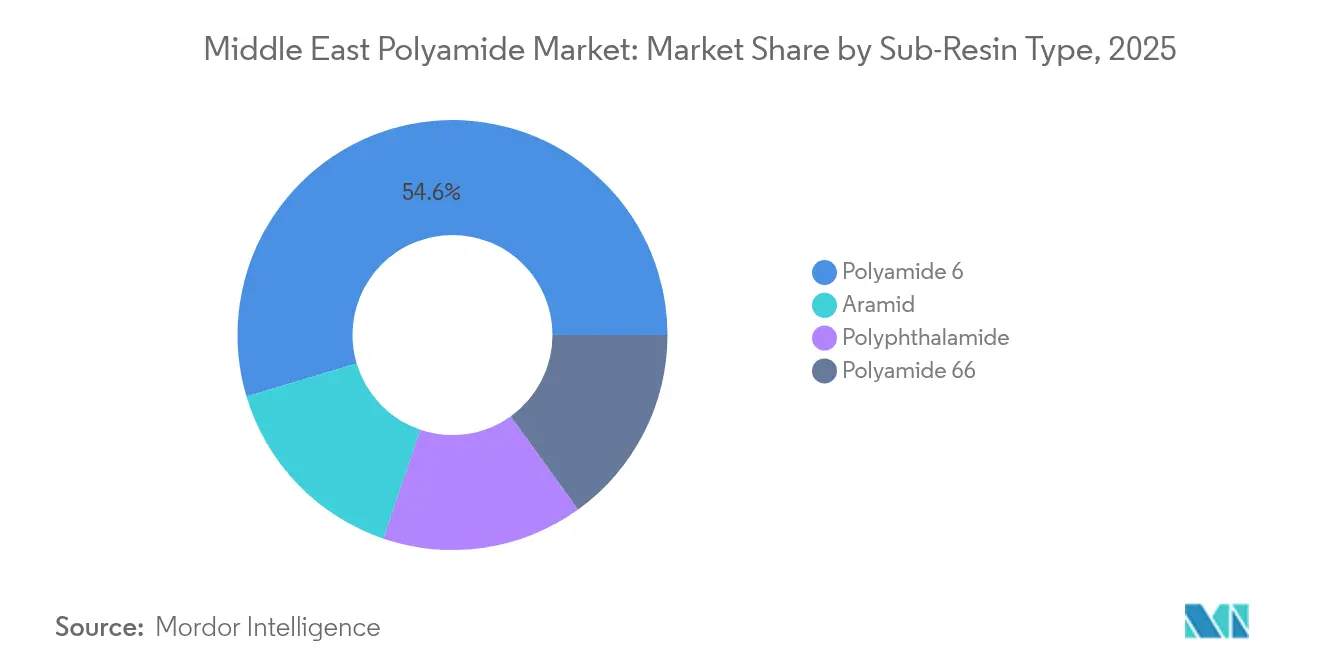

- By sub-resin, polyamide 6 led with a 54.62% Middle East Polyamide market share in 2025; aramid is forecast to expand at a 6.89% CAGR through 2031.

- By end-user, electrical and electronics accounted for 30.78% of the Middle East Polyamide market size in 2025 and is advancing at a 7.18% CAGR through 2031.

- By geography, the Rest of Middle East held 39.88% market share in 2025, while the UAE is projected to grow at a 5.82% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Polyamide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting initiatives | +1.2% | Saudi Arabia, UAE, spillover to Qatar | Medium term (2-4 years) |

| Electrical and electronics manufacturing boom | +0.8% | UAE core, expanding to Saudi Arabia and Kuwait | Short term (≤ 2 years) |

| High-barrier packaging demand | +0.7% | UAE and Saudi Arabia with regional coverage | Medium term (2-4 years) |

| Infrastructure-led engineering plastics | +0.6% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| E-mobility battery component requirements | +0.5% | UAE and Saudi Arabia EV hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Automotive Lightweighting Initiatives

Regional vehicle assembly programs are scaling rapidly as OEMs locate near low-cost resin supply, and weight reduction targets place polyamide-rich components at the forefront of design changes. Imports of electric and hybrid vehicles reached USD 2.7 billion and USD 3.6 billion respectively in 2024, underscoring the speed at which electrified drivetrains penetrate local fleets[1]United Nations ESCWA, “Arab Trade in 2023: Trends and Highlights,” unescwa.org. Under-hood parts, battery casings, and high-voltage connectors all favor temperature-stable, mechanically robust grades such as PA6 and PA66. Producers respond by tailoring automotive compounds that meet ISO 26262 and OEM-specific flammability standards while incorporating recycled content to satisfy sustainability benchmarks. LyondellBasell’s July 2024 debut of Schulamid ET100 signals growing emphasis on circular formulations for interior applications, though the Middle East Polyamide market still relies on imported masterbatch for specialized colors and UV packages in the short term. As local extrusion and injection facilities come online, supply chain lead times shorten, amplifying the competitive appeal of regionally blended automotive polyamides.

Growing Electrical and Electronics Manufacturing Investments

National industrial strategies fast-track semiconductor back-end, consumer-device assembly, and data-center construction, propelling consumption of flame-retardant polyamides in connectors, sockets, and chassis components. Dubai’s free-zone incentives attracted multiple PCB assemblers during 2024, and planned wafer-level packaging plants will demand tight-tolerance resins with low warpage at solder-reflow temperatures. The 5G rollout across GCC countries adds volume in antenna housings and fiber-optic components requiring hydrolysis-resistant PA6. Manufacturers leverage local compounding houses to customize glass-reinforced grades that balance CTI performance and surface finish, a shift that keeps more value inside the Middle East Polyamide market. Bilateral trade pacts such as the UAE-Indonesia CEPA slash duties on specialty polymers and spur joint ventures that lock in long-term resin offtake, reinforcing growth momentum.

Packaging Sector Demand for High-Barrier Materials

Food-security programs and the region’s hot climate intensify need for multilayer films where polyamide serves as an oxygen and aroma barrier. Pharmaceutical exports from Saudi Arabia grew 14% in 2024, leading blister-pack converters to specify coextruded PA layers that safeguard drug potency during trans-desert transport. Regional flex-pack makers install nine-layer blown film lines capable of incorporating bio-based PA resins, meeting rising brand-owner targets for recyclable structures. High-barrier industrial sacks for petrochemicals and fertilizers also migrate to PA-reinforced designs for puncture resistance. As chemical recycling pilots mature, processors will tap post-consumer PA waste streams to close the loop, a strategy aligned with Gulf sustainability frameworks and likely to raise demand for compatibilizer blends inside the Middle East Polyamide market.

Infrastructure Boom Driving Construction-Grade Engineering Plastics

Mega-projects such as Saudi Arabia’s NEOM and the UAE’s Etihad Rail require piping, cable conduits, and desalination components that withstand sand abrasion, UV radiation, and chlorinated water. DOMO’s TECHNYL SAFE has gained traction in potable-water applications due to excellent hydrolytic stability and compliance with WRAS and NSF standards. Contractors specify PA11 and PA12 for flexible gas pipes and pressure-rated fittings where corrosion-free life cycles offset higher upfront cost versus metal. Material substitution policies in public works tenders recognize total cost of ownership, expanding polyamide penetration into bridge bearings and HVAC systems. Long-term durability needs secure a steady pull for engineering-grade volumes that will account for a growing slice of the Middle East Polyamide market by the end of the decade.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil-derived feedstock prices | -0.9% | Regional, with highest impact in Saudi Arabia and UAE | Short term (≤ 2 years) |

| Limited high-temperature-grade production capacities in-region | -0.6% | Regional, particularly affecting specialized applications | Medium term (2-4 years) |

| Trade barriers and antidumping duties on Asian imports | -0.4% | UAE and Saudi Arabia import-dependent segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil-Derived Feedstock Prices

Turbulence in crude benchmarks translates swiftly into naphtha and benzene costs, compressing polyamide spreads during pricing down-cycles. Average oil prices were USD 83 per barrel in 2024, 10% lower than 2022, while regional petrochemical export values dropped 18%, highlighting margin pressure. Producers with long-haul arbitrage exposure face amplified risk as shipping rates fluctuate alongside geopolitical tensions in the Red Sea corridor. Currency depreciation in non-GCC importing markets adds complexity, raising dollar-denominated additive and catalyst costs. Nevertheless, the Middle East Polyamide market mitigates part of this volatility through feedstock transfer pricing within vertically integrated giants such as SABIC, protecting local converters from extreme swings that global spot buyers encounter.

Limited High-Temperature-Grade Production Capacities In-Region

Demand for polyphthalamide, aramid fiber, and other more than or equal to 150 °C service-temperature grades outstrips local extrusion and polymerization capacity. Aerospace assembly lines in Dubai South outsource PPA intake manifolds from Europe, incurring six-week lead times that hamper just-in-time production. Qualification protocols set by international airworthiness agencies restrict rapid supplier substitution, reinforcing the dominance of established Western producers. Capex requirements for aramid are high, with para-amid polymerization and spinning plants costing upward of USD 300 million, a hurdle that delays indigenous build-out. Technology-licensing talks proceed, yet multi-year timelines mean the Middle East Polyamide market will continue importing critical heat-resistant grades through at least 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Resin Type: PA6 Retains Scale as Aramid Accelerates

Polyamide 6 captured 54.62% of the Middle East Polyamide market share in 2025 on the strength of mature caprolactam loops integrated with refinery aromatics streams. Unit costs remain favorable, making PA6 the workhorse resin for cable ties, engine covers, and consumer-durable housings. Downstream compounders in Jubail and Ruwais expand glass-fiber and mineral-filled lines that push PA6 volumes deeper into structural uses once dominated by PA66, improving the Middle East Polyamide market size for commodity-plus grades. Aramid, though accounting for a smaller absolute tonnage, posts a 6.89% CAGR as aerospace, defense, and energy-service operators adopt para-amid ropes, ballistic panels, and high-pressure hoses. Regional offsets in military procurement packages encourage technology transfer of aramid prepreg fabrication to Saudi industrial cities, hinting at a modest reduction in import reliance after 2027.

Innovation clusters in UAE’s KEZAD and Saudi Arabia’s SPARK foster cooperative research and development on bio-based PA610 and recycled PA6/66 blends, reflecting broader ESG priorities within the Middle East Polyamide industry. Polyphthalamide secures design wins in EV power electronics but remains hindered by limited local HMDA and isophthalic-acid streams. Resin majors evaluate debottlenecking adipic-acid assets, potentially easing PA66 supply constraints by 2026 and stabilizing prices for automotive intake manifolds. The overall competitive landscape therefore balances high-volume PA6 corridors with fast-growing but capital-intense aramid pockets, creating a nuanced trajectory for the Middle East Polyamide market.

By End-User Industry: Electronics Anchor Demand Upside

Electrical and electronics accounted for 30.78% of the Middle East Polyamide market size in 2025, reflecting the dense cluster of mobile-device, telecom-equipment, and data-center investments. Flame-retardant PA6/66 and glass-reinforced PA46 dominate fine-pitch connector housings, while laser-transparent PA6 grades enable over-molding of optical sensors critical to 5G infrastructure. The region’s sovereign wealth funds back semiconductor OSAT facilities, locking in resin offtake agreements that reduce exposure to container-freight delays from Asia. Automotive holds the second-largest share as OEM knock-down kits evolve into full assembly lines, increasing under-hood polyamide uptake in turbo-air ducts and thermal-management components. Battery-electric models intensify the need for aramid separators and PA6-based cell spacers, enlarging the Middle East Polyamide market by linking polymer demand to the e-mobility curve.

Continuous megaproject construction secures baseline volume through polyamide-based water systems and reinforced building products, while packaging converters leapfrog to seven-layer lines that incorporate bio-based PA for consumer goods. Machinery manufacturers tied to oil and gas place specialty orders for PA12 umbilicals and PPA pump parts that resist sour-gas environments, demonstrating the varied application toolkit within the Middle East Polyamide industry. Though aerospace volumes are relatively small, they influence material innovation disproportionately, pushing suppliers to qualify high-temperature and low-FST grades that elevate profit margins. This diversified end-use matrix insulates the Middle East Polyamide market from shocks in any single downstream segment.

Geography Analysis

The Rest of Middle East retained 39.88% Middle East Polyamide market share in 2025, driven by Qatar, Oman, and Kuwait leveraging integrated condensate splitters and strategic ports that funnel feedstocks into value-added manufacturing. QatarEnergy’s USD 6 billion Ras Laffan complex proceeds with a mixed-xylene unit that frees benzene for domestic caprolactam lines, supporting PA6 pellet exports to regional compounders. Oman’s Duqm zone courts Chinese and Indian investors seeking tariff-free access to GCC markets, translating into incremental Middle East Polyamide market demand for electrical conduit and industrial machinery parts. Kuwait signs long-term ethane supply contracts that underpin PA66 fiber applications in filtration and industrial fabrics, demonstrating how niche strategies across smaller Gulf states collectively impact regional polymer flows.

The UAE posts the fastest trajectory with a 5.82% CAGR through 2031 as Abu Dhabi’s advanced manufacturing agenda co-locates resin plants and high-precision molding parks. Dubai’s Jebel Ali Port processes more than 75,000 TEU of engineering plastics annually, enabling Just-In-Sequence deliveries to OEMs across MENASA. Free-trade pacts such as the CEPA with Indonesia eliminate duties on caprolactam and specialty additives, ensuring cost-competitive feedstock importation. Sustainable development policies mandate recycled-content targets in packaging and automotive components, spurring adoption of chemically recycled PA6 in logistics pallets and interior trims, which lifts total Middle East Polyamide market size.

Saudi Arabia remains a pivotal node owing to feedstock scale and Vision 2030 manufacturing diversification. SABIC debottlenecks its Yanpet PA6 lines, while Petro Rabigh integrates captive adipic-acid output to hedge PA66 supply. The kingdom’s YANBU-based Ravago compounding site triples capacity in 2025 to supply glass-reinforced PA6 to appliance makers across Africa.

Competitive Landscape

The Middle East Polyamide market demonstrates moderate fragmentation. SABIC maintains a commodity-grade stronghold, yet invests in recycled-feedstock trials to align with circular-economy regulations. International players like BASF, Arkema, and LANXESS carve niches in high-heat, low-warpage compounds, leveraging global application-development centers to win aerospace and EV battery business. Strategic alliances proliferate as specialty know-how meets low-cost monomers. Huntsman anchors Arabian Amines Company in Jubail, ensuring local supply of hexamethylenediamine essential for PA66 and PPA.

Middle East Polyamide Industry Leaders

Arkema

BASF

Koch IP Holdings, LLC

Petro Rabigh

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Saudi Aramco acquired an additional 22.5% stake in Petro Rabigh for USD 702 million, raising ownership to 60%. This vertical integration move strengthens feedstock security and downstream polymer production capabilities.

- July 2024: Syensqo introduced recycled-content polyamide grades containing up to 50% post-consumer material for packaging and automotive uses.

Middle East Polyamide Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Aramid, Polyamide (PA) 6, Polyamide (PA) 66, Polyphthalamide are covered as segments by Sub Resin Type. Saudi Arabia, United Arab Emirates are covered as segments by Country.| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-User Industries |

| Aramid |

| Polyamide 6 |

| Polyamide 66 |

| Polyphthalamide |

| Saudi Arabia |

| United Arab Emirates |

| Rest of Middle East |

| End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-User Industries | |

| By Sub-Resin Type | Aramid |

| Polyamide 6 | |

| Polyamide 66 | |

| Polyphthalamide | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyamide market.

- Resin - Under the scope of the study, virgin polyamide resins like Polyamide 6, Polyamide 66, Polyphthalamide, and Aramid in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms