Middle East Polycarbonate (PC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

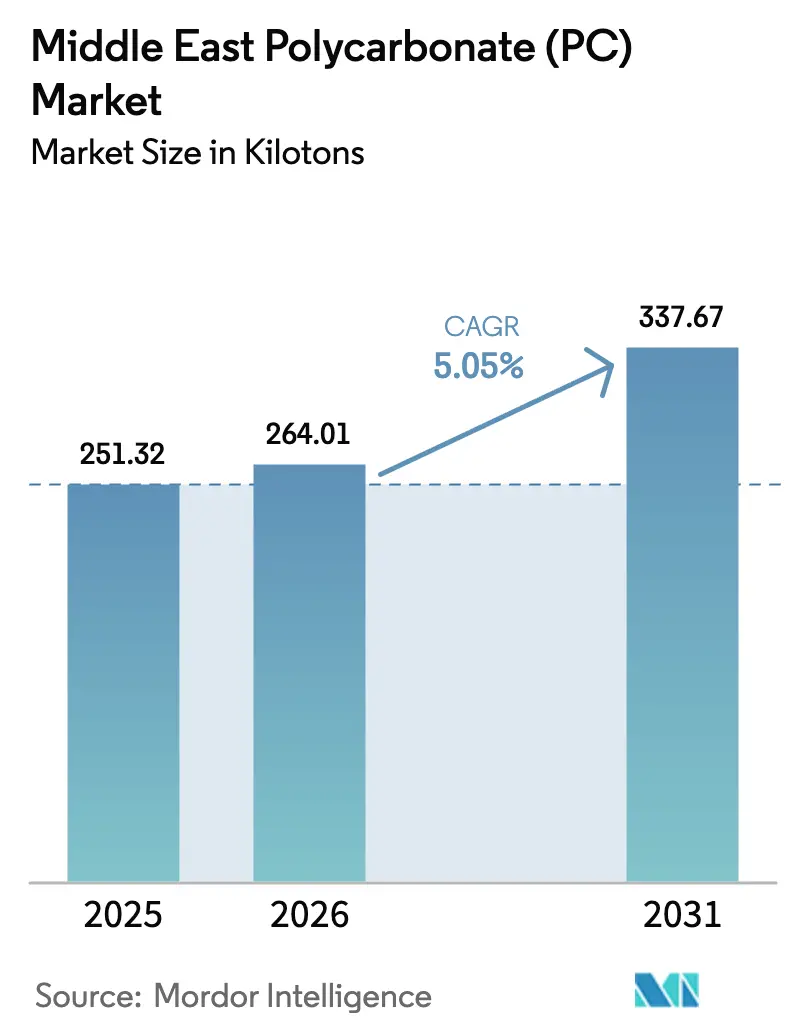

| Base Year Market Size (2025) | 251.32 kilotons |

| Market Volume (2026) | 264.01 kilotons |

| Market Volume (2031) | 337.67 kilotons |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Polycarbonate (PC) Market Analysis by Mordor Intelligence

The Middle East Polycarbonate Market size in 2026 is estimated at 264.01 kilotons, growing from 2025 value of 251.32 kilotons with 2031 projections showing 337.67 kilotons, growing at 5.05% CAGR over 2026-2031. Strong demand from construction glazing in Vision 2030 megaprojects, the build-out of UAE manufacturing free zones, and lightweighting initiatives in regional vehicle assembly anchor this growth. Defense against BPA feedstock volatility is improving through Saudi feedstock integration, while tighter Gulf Standards Organization (GSO) fire-safety rules favor high-performance grades. Local converters also gain from proximity to African and South-Asian export corridors, creating a balanced opportunity landscape for both incumbents and new entrants. Competitive intensity is dominated by SABIC’s backward-integrated capacity, yet international suppliers strengthen their foothold through technical service centers and distributor alliances.

Key Report Takeaways

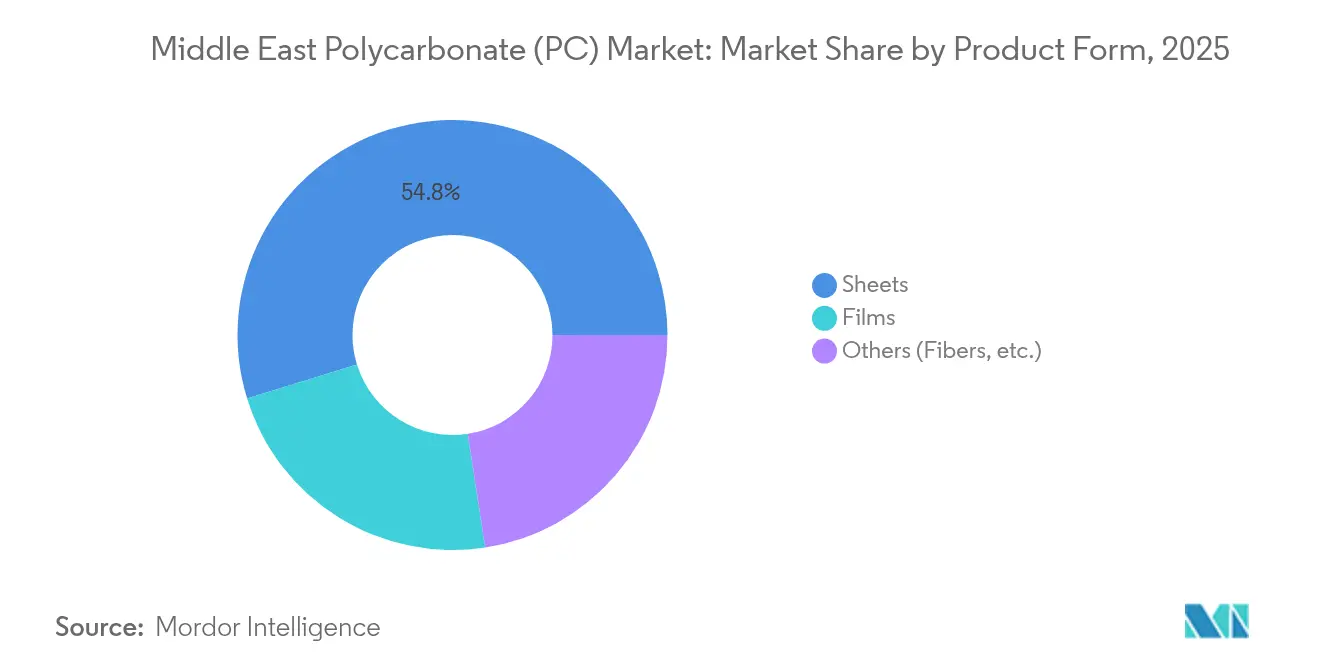

- By product form, sheets captured 54.78% of the Middle East polycarbonate market share in 2025, while films are projected to advance at a 6.05% CAGR through 2031.

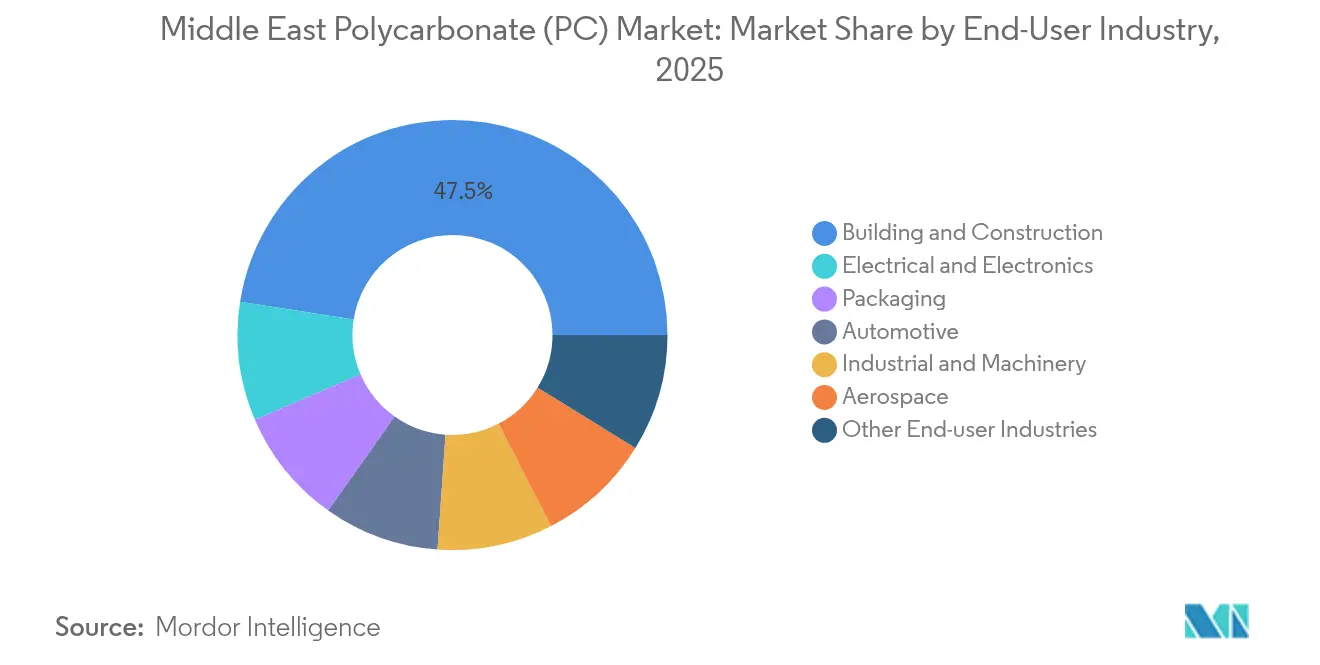

- By end-user industry, building and construction accounted for a 47.52% share of the Middle East polycarbonate market size in 2025, whereas electrical and electronics is set to expand at an 8.32% CAGR to 2031.

- By geography, the United Arab Emirates led with 41.22% revenue share in 2025, whereas Saudi Arabia is forecast to post the fastest-growth CAGR of 5.86% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Polycarbonate (PC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom under Saudi Vision 2030 megaprojects | +1.50% | Saudi Arabia, spillover to UAE and Qatar | Long term (≥ 4 years) |

| Automotive manufacturing clusters embracing lightweighting | +1.20% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Expansion of regional electronics assembly free-zones | +0.90% | UAE core, Saudi Arabia & Bahrain | Medium term (2-4 years) |

| Desert agriculture’s shift to polycarbonate greenhouses | +0.80% | GCC-wide, focused in UAE & Saudi Arabia | Long term (≥ 4 years) |

| MRO-led demand for aerospace cabin & transparencies | +0.60% | UAE aviation hubs, Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction Boom Under Saudi Vision 2030 Megaprojects

Saudi Vision 2030 commits more than USD 186 billion to building materials and infrastructure, pushing polycarbonate into façade, skylight, and transportation glazing across NEOM and Red Sea projects. Fire-safety rules under GSO EN 13501-1:2024 require materials that pass stringent flame-spread and smoke-density tests, reinforcing the appeal of engineered polycarbonate grades. Developers also prioritize circular solutions to meet the kingdom’s sustainability objectives, accelerating demand for recyclable polycarbonate sheets formulated with lower carbon footprints. Supply chains benefit from SABIC’s local feedstock integration, which cushions converters from import-linked BPA volatility. As a result, the Middle East polycarbonate market gains a stable anchor for long-cycle construction demand that extends well beyond the forecast horizon.

Automotive Manufacturing Clusters Embracing Lightweighting

UAE and Saudi Arabia are rolling out automotive cluster programs that target 50,000-100,000 vehicles annually by 2030. Polycarbonate headlamp lenses, instrument panels, and battery housings reduce component mass by 40% versus glass while meeting tough impact standards. Special flame-retardant grades introduced by SABIC simplify EV battery-pack design and thermal shielding. Turkey’s established vehicle platforms source parts across Gulf assembly lines, creating cross-border pull on specialty polycarbonate. Regional capacity additions also shrink lead times to under four weeks, positioning the Middle East polycarbonate market as a responsive partner for OEM model launches through 2030.

Expansion of Regional Electronics Assembly Free-Zones

Dubai’s Jebel Ali Free Zone and the NEOM Industrial City plan anchor large-scale smartphone, LED, and telecom equipment production that relies on high-precision polycarbonate for housings and optical films[1]Dubai Investment Development Agency, “Jebel Ali Free Zone,” DDA, dda.gov.ae . Jebel Ali’s throughput tops USD 104 billion in re-exports, giving converters a direct pipeline to African and European buyers. Specialty films engineered for flexible displays see rapid uptake alongside 5G base-station components that require UV-stable, flame-retardant plastics. As a result, free-zone manufacturing adds a consistent mid-single-digit volumetric lift to the Middle East polycarbonate market each year of the forecast.

Desert Agriculture’s Shift to Polycarbonate Greenhouses

GCC countries pursue food security by backing climate-controlled agriculture that replaces glass roofs with twin-wall polycarbonate panels, attaining 15-20% higher energy efficiency under desert climates[2]Agricultural Technology Research Institute, “Energy Efficiency in Polycarbonate Greenhouses,” atri.gov . UAE targets 70% domestic produce self-sufficiency by 2030, while Saudi Arabia monetizes carbon credits through circular carbon initiatives. Polycarbonate panels withstand sandstorms and 50 °C daytime peaks without yellowing, lowering life-cycle costs versus glass. Joint-venture greenhouses near Riyadh and Al Ain already specify multi-wall sheets with 10-year UV warranties, bolstering recurring demand across replacement cycles that average eight years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BPA feedstock price volatility | -0.70% | Region-wide, acute on imports | Short term (≤ 2 years) |

| Cost-driven substitution by acrylic & glass | -0.50% | All GCC markets | Medium term (2-4 years) |

| Limited PCR-PC recycling infrastructure | -0.30% | GCC-wide, most acute in Saudi Arabia and smaller emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BPA Feedstock Price Volatility

Red Sea shipping disruptions pushed container rates from Asia up 200-300% in 2024, inflating delivered BPA costs by 15-20% for non-integrated converters. While SABIC’s backward-integration shields some regional buyers, smaller processors endure margin squeeze that discourages speculative inventory builds. Spot BPA prices swung 22% inside one quarter, complicating pricing for monthly polycarbonate supply contracts. Producers respond by indexing quotes to a rolling BPA cost-plus formula, but downstream buyers still face budgeting uncertainty. This dampens immediate uptake in price-sensitive segments, trimming Middle East polycarbonate market momentum during volatile windows.

Cost-driven Substitution by Acrylic & Glass

Tempered glass maintains a cost advantage of 30-40% in basic glazing, prompting architects to revert to glass where impact loading is mild and regulatory flame-spread ratings are lenient. In aftermarket automotive parts, acrylic substitutes undercut polycarbonate on price when scratch resistance is non-critical. GCC public-sector budgets in housing and education projects remain tightly managed, encouraging spec revisions that switch to lower-cost materials unless GSO fire-safety rules mandate otherwise. Continuous technical education by polycarbonate suppliers is therefore essential to protect share in entry-level applications across the Middle East polycarbonate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Sheets Dominate While Films Accelerate

Sheets generated 54.78% of the Middle East polycarbonate market share in 2025. SABIC’s UV-stabilized sheet grades enable ten-year façade warranties under Gulf solar exposure. Energy-efficient architecture in Riyadh and Dubai further cements sheet relevance as developers pursue LEED and Estidama credits. In parallel, films are outpacing at a 6.05% CAGR, driven by flexible printed circuit protection and greenhouse cladding. Tight thickness tolerance, optical clarity, and chemical resistance make films integral to regional electronics hubs, positioning the segment as a consistent growth engine inside the Middle East polycarbonate market. Other forms, such as fibers and specialty extrusions, continue to serve medical devices and filtration, but together account for small share of aggregate volume.

Second-order dynamics favor segment diversification over the forecast horizon. Converters expand co-extrusion lines in Sharjah and Dammam to integrate anti-fog and anti-scratch layers onto sheets, enabling premium pricing. Film processors in Ras Al Khaimah commission tenter-frame units capable of less than10 µm thickness variance, unlocking supply for foldable handset covers. As local capacity deepens, import reliance drops, enhancing self-sufficiency and adding resilience to the Middle East polycarbonate market size outlook.

By End User Industry: Construction Leads Electronics Growth

Building and construction commanded 47.52% of 2025 demand, through skylights, canopies, and safety partitions across megaprojects. GSO fire-resistant categories push specifiers toward multi-wall sheets that deliver both insulation and compliance. The segment benefits from forward spending visibility tied to Vision 2030, Etihad Rail corridors, and Expo City Dubai retrofits, providing a robust baseline of projects locked into tender pipelines. Electrical and electronics is advancing fastest at an 8.32% CAGR, reflecting the rise of smartphone-assembly plants in Dubai, LED fabs in Abu Dhabi, and 5G tower rollouts in Saudi Arabia. Polycarbonate’s high dielectric strength and dimensional stability position it as the default solution for circuit breakers, router housings, and photovoltaic junction boxes.

Automotive retains a steady foothold as regional OEM launches such as Ceer and W Motors consume headlamp lenses and glazing that cut weight for fuel economy compliance. Aerospace relies on recurring MRO cycles, absorbing high-margin cabin interior panels despite modest tonnage. Packaging and industrial machinery tap twin-wall and glass-fiber-reinforced grades where impact forces or chemical exposures are high. Collectively, these applications broaden the Middle East polycarbonate market, tempering cyclicality tied to any single sector.

Geography Analysis

The United Arab Emirates retained a 41.22% share in 2025. Jebel Ali Free Zone supports electronics molding that ships finished goods across 180 countries, while Abu Dhabi’s chemical cluster supplies aromatic feedstocks that shorten delivery cycles. Borouge’s polyolefin expansion to 6.4 million tpa by 2025 anchors resin logistics in Ruwais, even as local extruders continue importing specialized polycarbonate grades. Regulatory predictability—zero import duties under GCC common external tariff—helps UAE processors capture export orders previously routed through Singapore and Rotterdam.

Saudi Arabia is the fastest-growing region, with a 5.86% CAGR. Vision 2030 projects like NEOM demand transparent cladding and energy-saving roof lights that withstand desert sandstorms. SABIC’s integrated complex at Jubail secures BPA supply, reducing cost swings tied to maritime chokepoints. GSO fire-safety mandates tighten specification, funneling demand toward premium flame-retardant and UV-stable polycarbonate. Public-sector procurement frameworks increasingly reward circular content, incentivizing converters to adopt post-consumer recycled grades that carry ISCC+ tags.

Qatar, Kuwait, Bahrain, and Oman collectively form the “Rest of Middle East” corridor, together representing smaller share of 2025 market volume. Qatar’s National Food Security Programme subsidizes greenhouse retrofits that specify twin-wall polycarbonate. Kuwait’s Al-Zour petrochemical complex brings new downstream processors online, providing ready buyers for sheet and film grades. Bahrain’s electronics assembly incubators and Oman’s tourism infrastructure create targeted pull, ensuring balanced geographical demand distribution across the Middle East polycarbonate market.

Competitive Landscape

The Middle East polycarbonate (PC) market is highly consolidated. SABIC leads through fully integrated feedstocks, in-house compounding, and multi-industry qualification programs that embed its grades into automotive and aerospace specifications. Recent launches of LNP ELCRIN resins containing up to 75% recycled content position SABIC to benefit from ESG-driven procurement criteria. Covestro leverages a strategic cooperation framework with ADNOC to evaluate local phosgene routes, potentially localizing carbonate intermediates. LG Chem and Mitsubishi Chemical bolster presence via regional distribution hubs in Dubai and Dammam, offering fast-response technical support that accelerates design-in for electronics and medical customers.

Middle-tier converters focus on niche plays such as optical-grade films and flame-retardant sheet lamination, differentiating via short production runs and rapid prototyping for architectural façades. The rise of on-site 3D-printing for form-fit cabin panels opens adjacency for filament-grade polycarbonate, stimulating collaboration between material suppliers and regional aviation MRO centers. Potential consolidation looms, as local investors eye bolt-on acquisitions to scale distribution networks and capture synergies in storage and compounding. The resulting equilibrium maintains robust but disciplined rivalry, ensuring steady innovation flow without destructive price competition across the Middle East polycarbonate market.

Middle East Polycarbonate (PC) Industry Leaders

Covestro AG

LG Chem

SABIC

Sumitomo Chemical Co., Ltd.

Teijin Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: SABIC has introduced its new LNP ELCRES CXL polycarbonate (PC) copolymer resins, which offer exceptional chemical resistance. These advanced materials are designed to serve customers in the mobility, electronics, industrial, and infrastructure sectors.

- October 2023: SABIC has introduced 10 new LNP ELCRIN polycarbonate copolymer resins, incorporating up to 75% certified post-consumer recycled content. This development is expected to strengthen the adoption of sustainable polycarbonate solutions in the Middle East market, particularly within consumer electronics and the automotive industry.

Middle East Polycarbonate (PC) Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Saudi Arabia, United Arab Emirates are covered as segments by Country.| Sheets |

| Films |

| Others (Fibers, etc.) |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| Saudi Arabia |

| United Arab Emirates |

| Rest of Middle East |

| By Product Form | Sheets |

| Films | |

| Others (Fibers, etc.) | |

| By End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East |

Market Definition

- End-user Industry - Building & Construction, Automotive, Electrical & Electronics, Industrial & Machinery, and Others are the end-user industries considered under the polycarbonate market.

- Resin - Under the scope of the study, consumption of virgin polycarbonate resin in its primary forms such as powder, granule, etc. are considered. Recycling has been provided separately under its individual chapter.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms