Ultra-high Molecular Weight Polyethylene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

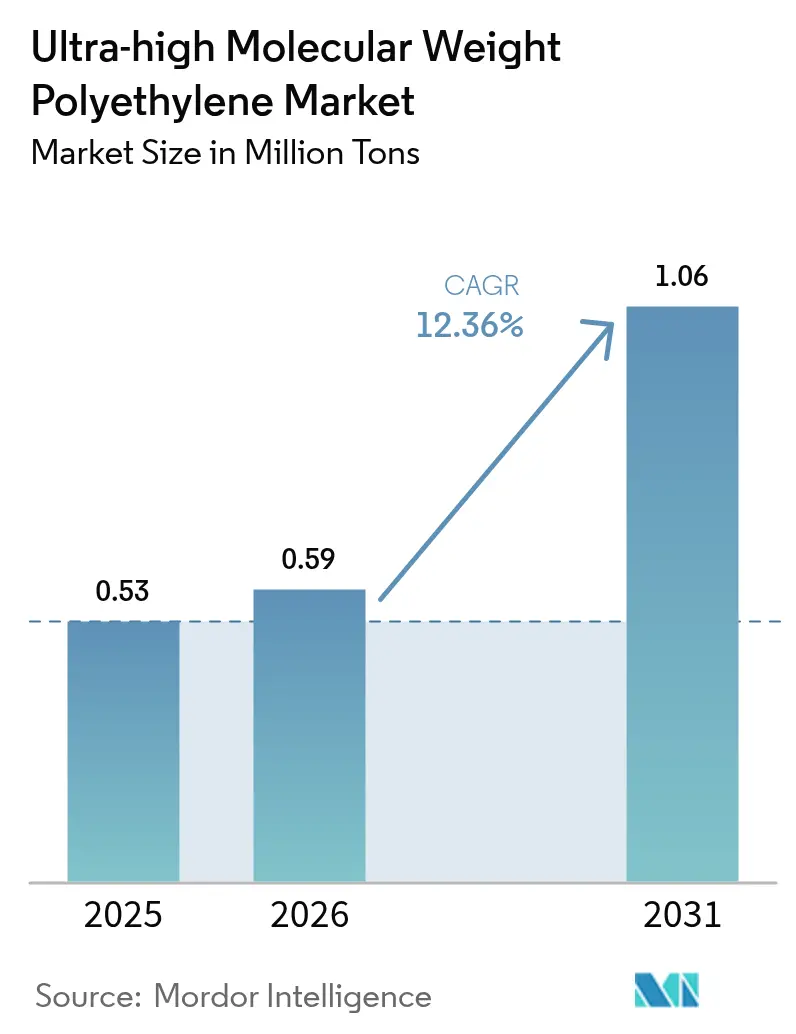

| Market Volume (2026) | 0.59 Million tons |

| Market Volume (2031) | 1.06 Million tons |

| Growth Rate (2026 - 2031) | 12.36% CAGR |

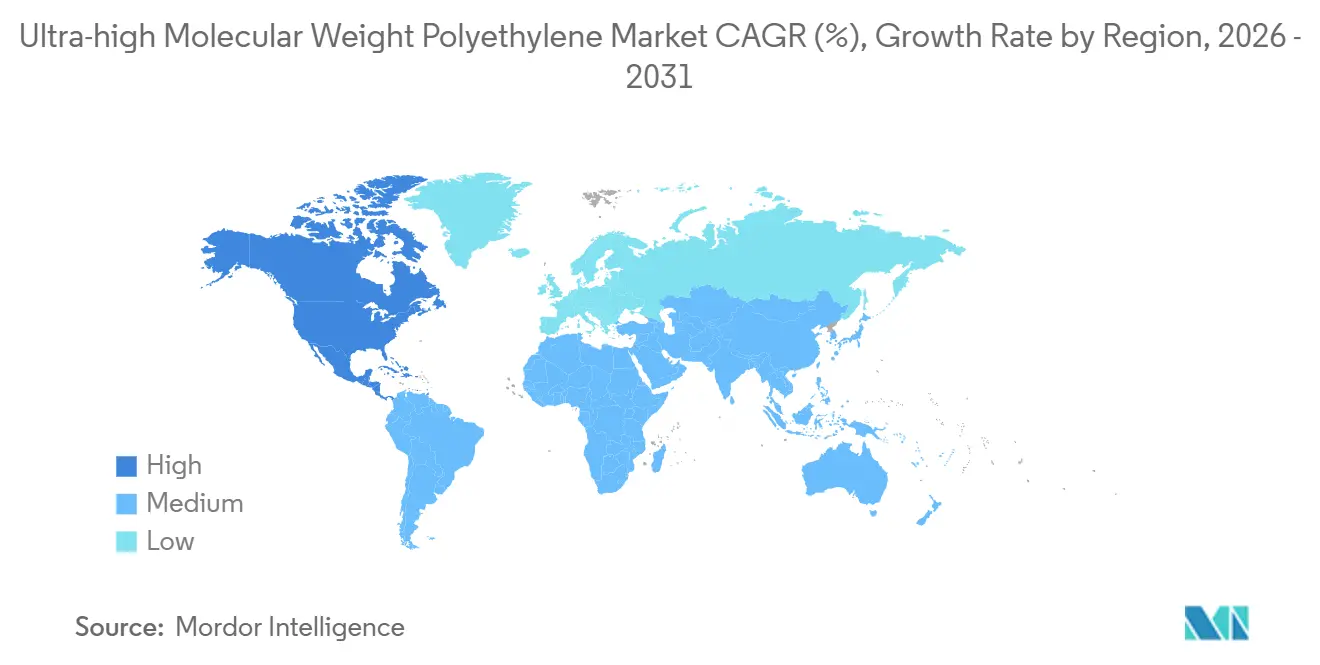

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultra-high Molecular Weight Polyethylene Market Analysis by Mordor Intelligence

The Ultra-high Molecular Weight Polyethylene Market size is projected to be 0.53 million tons in 2025, 0.59 million tons in 2026, and reach 1.06 million tons by 2031, growing at a CAGR of 12.36% from 2026 to 2031. Demand pulls come from lithium-ion battery separators for electric vehicles, offshore wind rope and mooring lines, and medical innovations such as 3D-printed orthopedic implants. Powder remains the leading form because gel-spinning lines started in China and North America convert this feedstock into high-tenacity fiber. Medicine continues to command the largest end-use volume, yet electronics now shows the fastest growth as chip packaging and advanced insulation adopt UHMWPE films to manage thermal stress. Regionally, Asia-Pacific anchors production and consumption, North America accelerates on energy-policy support, and Europe leverages strict medical-device rules to secure premium imports. Competitive intensity is moderate: Celanese, Asahi Kasei, Honeywell, DSM, and SABIC defend proprietary technology while Chinese entrants scale low-cost capacity.

Key Report Takeaways

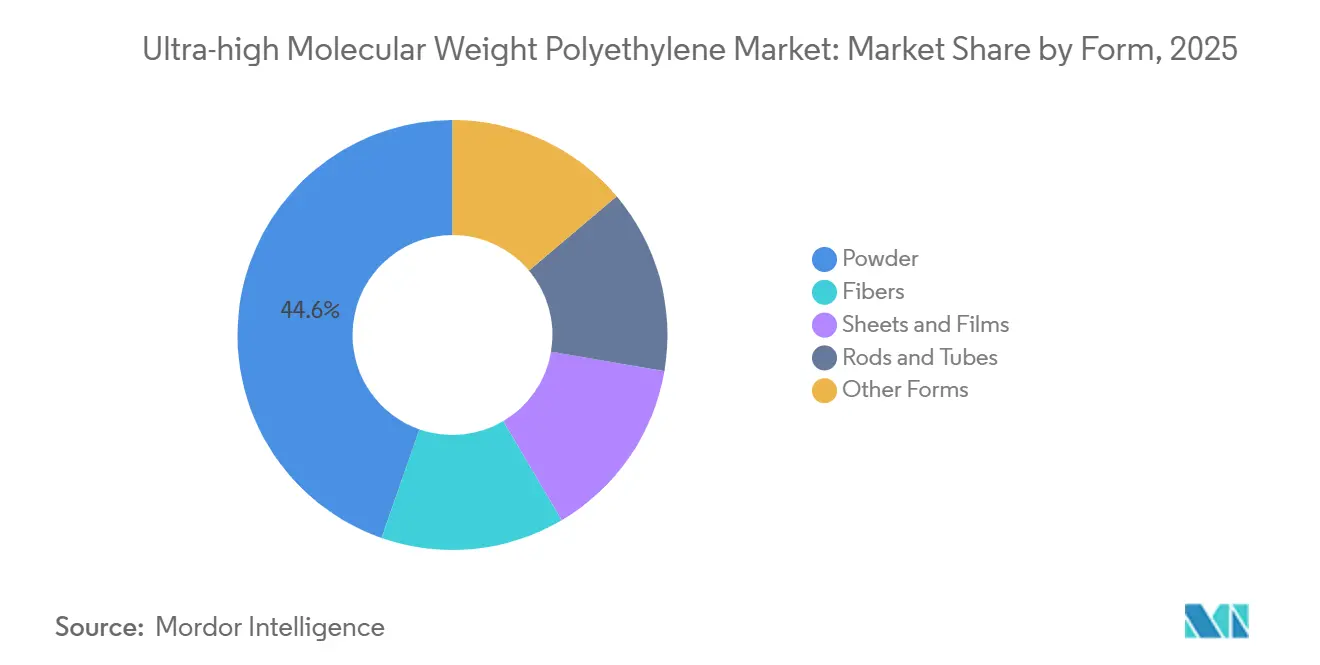

- By form, powder held 44.65% of the Ultra-high Molecular Weight Polyethylene market share in 2025 and is set to grow at a 12.64% CAGR through 2031.

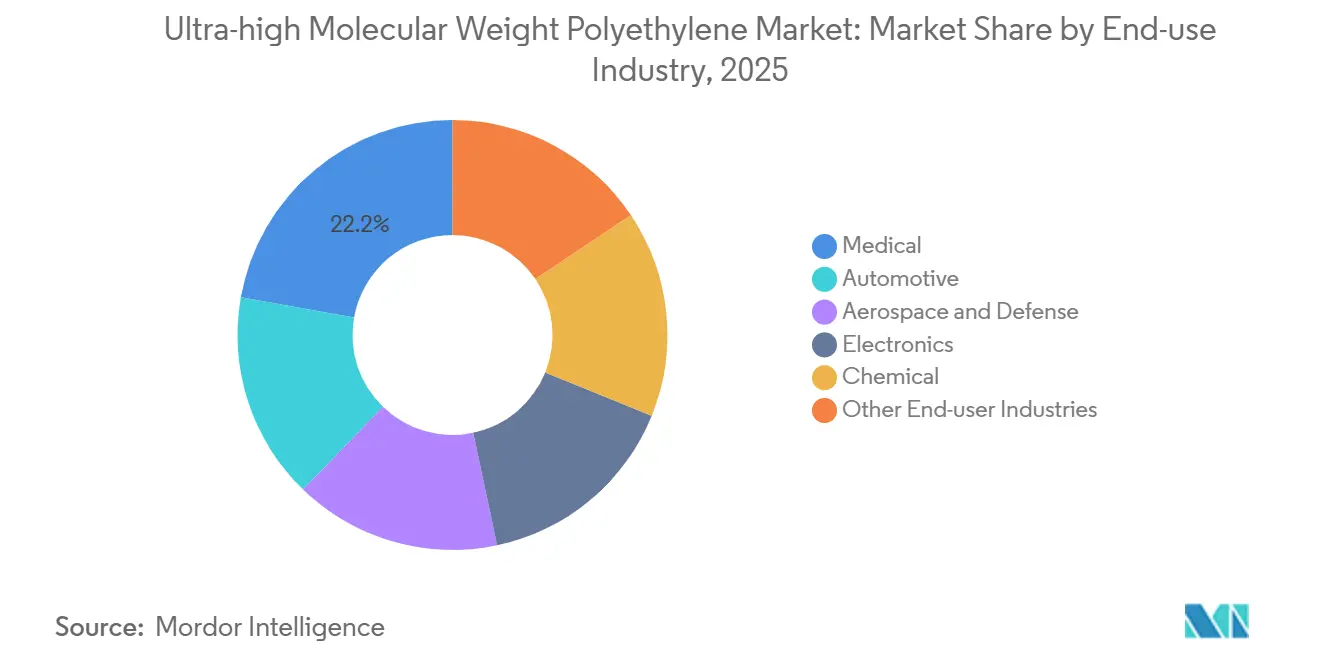

- By end-user, the medical segment led with 22.20% share in 2025, while electronics is forecast to post the fastest 13.10% CAGR to 2031.

- By geography, Asia-Pacific dominated with 44.57% volume share in 2025, and North America is poised for the highest 12.99% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Ultra-high Molecular Weight Polyethylene Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-performance polymer substitution in EV battery separators | +3.2% | Global, with concentration in China, North America, and Europe | Medium term (2-4 years) |

| Surge in APAC shipbuilding and offshore rope demand | +2.8% | APAC core, spill-over to Middle East offshore projects | Short term (≤ 2 years) |

| Growing use in medical wearables and smart textiles | +1.9% | North America, Europe, Japan | Medium term (2-4 years) |

| Growing demand for 3D-printed UHMWPE orthopedic implants | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Closed-loop, medical-grade UHMWPE recycling routes | +1.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-Performance Polymer Substitution in EV Battery Separators

Cell makers in the lithium-ion sector are increasingly opting for UHMWPE membranes, produced via thermally induced phase separation. This preference stems from the resin's high molecular weight, which ensures robust mechanical performance even at sub-20 µm thickness. In a significant move, Braskem secured an award from the Department of Energy in October 2024. This funding aims to boost separator powder capacity in Texas, fortifying domestic supply chains and creating skilled jobs. Additionally, nanoparticle-modified UHMWPE is enhancing electrolyte wettability, reducing cell impedance, and accommodating the fast-charging profiles sought by vehicle OEMs. As demand for separators surges, there's a noticeable shift of powder away from commodity sheet markets, benefiting producers who are channeling investments into clean-room extrusion and automotive quality systems.

Surge in APAC Shipbuilding and Offshore Rope Demand

In 2023, China added offshore wind capacity. Each gigawatt installation consumed UHMWPE rope, totaling fiber for the year. UHMWPE rope, derived from the polymer, boasts a weight that's significantly lighter than steel wire, yet it offers a tensile strength that's superior, making it ideal for deeper-water turbines. The substitution rate of UHMWPE has risen over the years, with projections suggesting it will continue to grow by 2030. China's new GB/T 21328-2024 standard, set to take effect in October 2024, establishes criteria for breaking-load and abrasion, further hastening regional adoption. Additionally, there's a growing demand for Korean and Japanese LNG carriers, which are now incorporating UHMWPE composite mooring lines.

Growing Use in Medical Wearables and Smart Textiles

In 2024, a study unveiled an ultrahigh-strength braided smart yarn, embedded with UHMWPE fibers, achieving a high tensile strength. This innovative yarn, housing triboelectric sensors, serves a dual purpose: providing structural support and facilitating signal transduction. Such capabilities position this polymer as the foundational element for next-gen garments, designed to monitor motion, harness energy, and endure washing cycles. In 2024, China's surgical robotics market integrated numerous units, each utilizing UHMWPE tendons, leading to incremental demand. Globally, humanoid robot platforms are increasingly opting for UHMWPE cables, aiming to optimize their payload-to-weight ratios. While wearables may not dominate in tonnage, their premium pricing and diverse electronic channels significantly boost overall margins.

Growing Demand for 3D-Printed UHMWPE Orthopedic Implants

Pilot trials on hybrid UHMWPE-PEEK lattices demonstrated additively manufactured hip and knee components that match patient bone stiffness, mitigating stress shielding and cutting revision risk. U.S. FDA guidance defines oxidation index, molecular weight distribution, and wear-debris limits that polymer suppliers must meet to qualify for orthopedic devices. As printers achieve sub-100 µm layer resolution, patient-matched liners move from prototype to clinical evaluation. An aging population in North America and Europe sustains baseline demand, while additive workflows shorten lead times between scan and surgery.

Restraints Impact Analysis of Ultra-high Molecular Weight Polyethylene Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High processing-energy intensity vs. bio-based alternatives | -1.8% | Global, with acute pressure in Europe due to carbon pricing | Medium term (2-4 years) |

| Low melting point limits high-load composite designs | -1.3% | Aerospace and automotive sectors in North America, Europe | Long term (≥ 4 years) |

| Trade-remedy duties on Asian UHMWPE powder exports | -0.7% | Import-dependent regions: Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Processing-Energy Intensity vs. Bio-Based Alternatives

Producing gel-spun materials requires significantly more energy per tonne compared to traditional polyethylene film extrusion[1]Polymer Processing Journal, “Energy Consumption in UHMWPE Gel Spinning Processes,” polymerprocessingjournal.com. This heightened energy demand arises from the necessity of dissolving the polymer in hot decalin or paraffin prior to undergoing multi-stage drawing. In 2024, Europe's carbon pricing increased the production costs of UHMWPE[2]European Commission, “EU Emissions Trading System Carbon Pricing Data,” ec.europa.eu. While bio-based polyethylene boasts a lighter carbon footprint, this advantage exerts downward pressure on the prices of commodity sheets and films. Despite the promise of super-critical CO₂ solvent trials and waste-heat recovery projects, their capital-intensive nature curtails any immediate financial relief.

Low Melting Point Limits High-Load Composite Designs

While UHMWPE melts at a temperature well below the service temperatures encountered in automotive underbody shields and aerospace structures, this limits its applicability. Although cross-linking enhances thermal stability, it simultaneously reduces elongation and heightens brittleness. As a result, design engineers are turning to PEEK or PPS, which melt at significantly higher temperatures, for applications in high-heat zones. Additionally, the growing adoption of thermoplastic composites in aircraft cabins further sidelines UHMWPE, as the polymer's limited processing window poses challenges for tape laying.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Ultra-high Molecular Weight Polyethylene Market Segment Analysis

By Form:

Powder Retains Leadership as Gel-Spinning Lines RampPowder captured 44.65% volume in 2025 and grows at a 12.64% CAGR through 2031. This growth is bolstered by the launch of large-scale gel-spinning lines, notably Jiuzhou Xingji’s facility, which came online in 2024. The market size for ultra-high molecular weight polyethylene powder is set to increase during the forecast period. Demand for fiber grades, driven by applications in ballistic armor, offshore ropes, and specialty films, is steering capital investments. Meanwhile, compression-molded sheets and ram-extruded rods are being utilized as wear-resistant liners. In a strategic move, Mitsui Chemicals boosted its HI-ZEX capacity in 2024, ensuring a robust supply of powder for battery separators.

Fibers, holding the second position in the market, are reaping benefits from defense budgets. These budgets prioritize UHMWPE laminates, which can halt rifle rounds at a weight significantly lighter than traditional aramid armor. Sheets and films find their applications in semiconductor wafer carriers, food-handling equipment, and chute liners, where attributes like low friction and chemical inertness are paramount. While rods and tubes have carved out a niche in mechanical components, experimental 3D-printing filaments are grappling with viscosity challenges, despite promising lab demonstrations for medical prototypes.

By End-Use Industry:

Electronics Challenges Medicine’s DominanceMedicine held 22.20% volume in 2025 as joint replacements continued to specify UHMWPE acetabular liners with wear rates below 0.1 mm/year. Electronics posts a 13.10% CAGR to 2031 on the back of sub-5 nm node packaging that needs low-k, moisture-resistant insulation films. Automotive, ranked third, benefits from separator adoption and polymer bearings in electric powertrains. Aerospace and defense rely on UHMWPE armor and rotor blades but face long procurement cycles tied to public budgets. Chemical processing and niche sporting goods absorb the remainder, offering steady but smaller increments.

Geography Analysis

APAC Ultra-high Molecular Weight Polyethylene Market

Asia-Pacific accounted for 44.57% volume in 2025 and remains the epicenter of the ultra-high molecular weight polyethylene market. China’s integrated chain stretches from monomer to finished rope, and its national GB/T 21328-2024 standard streamlines quality assurance for offshore wind contractors. Japan sources powder for surgical sutures and Teijin’s medical devices, while South Korea’s shipbuilders embed UHMWPE mooring lines in LNG carriers. India and ASEAN grow from a small base as local EV and food-processing sectors scale.

North America Ultra-high Molecular Weight Polyethylene Market

North America posts the fastest regional growth at a 12.99% CAGR through 2031, lifted by the Department of Energy’s funding for Braskem’s Texas separator plant and by defense spending that prioritizes domestic Spectra fiber supply. FDA regulations maintain high entry barriers, securing powder of consistent molecular weight distribution. Canada uses UHMWPE slurry liners in oil sands, and Mexican auto plants move toward in-house separator lamination. Honeywell’s plan to spin off Advanced Materials by early 2026 may unlock new capital sources for regional expansions.

EMEA and South America Ultra-high Molecular Weight Polyethylene Market

Europe trails by volume yet benefits from the strict Medical Device Regulation that favors UHMWPE’s biocompatibility. German premium EV makers pilot separators, and the United Kingdom equips security forces with UHMWPE body armor. DSM and SABIC’s recycled Dyneema trial aligns with EU circular-economy incentives. South America and Middle-East and Africa remain small importers; Brazil’s mining sector uses sheets, and Saudi Arabia tests UHMWPE pipeline liners for corrosive brine.

Value Chain Analysis

Upstream, the value chain starts with ethylene feedstock and catalyst systems that enable specialized polymerization to reach ultra-high molecular weight. Producers then convert UHMWPE resin into powder and, for higher-value outlets, run solvent-based gel-spinning and multi-stage drawing to make high-tenacity fiber for ballistic armor and offshore rope, or clean-room film and membrane routes for lithium-ion battery separators and electronics insulation.

Midstream and downstream processing is where differentiation and bottlenecks concentrate. Tight molecular-weight control, impurity management, and application-specific compounding and lamination determine access to medical, separator, and defense specifications, while commodity sheet and rod markets face stronger price pressure. Capacity additions in China and targeted projects such as CNOOC Ningbo Daxie Petrochemical’s announced 40,000 tpa UHMWPE unit underline ongoing upstream investment, but value capture increasingly shifts to integrated fiber and film converters and to qualified distribution channels serving medical and battery supply chains.

Competitive Landscape

The ultra-high molecular weight polyethylene market is concentrated. Chinese firms raise capacity rapidly and integrate through weaving and lamination, compressing margins in commodity grades. Technology advantage now hinges on oxidation inhibitors, viscosity modifiers, and molecular-weight control that enable thinner films without fisheyes. Patent filings from 2024–2025 explore cross-link chemistries that push melting points above 150 °C, opening a pathway to aerospace interiors. Standards bodies ASTM and ISO refine debris analysis and oxidation testing, creating certification costs that smaller players must absorb. Mergers and acquisitions interest centers on medical recycling, advanced separator films, and ballistic composite prepregs. Western resin suppliers protect gross margins through application engineering and long-term supply contracts tied to regulatory compliance.

Ultra-high Molecular Weight Polyethylene Industry Leaders

Celanese Corporation

Braskem

Mitsui Chemicals Inc.

LyondellBasell Industries Holdings B.V.

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Ultra-high Molecular Weight Polyethylene Market Companies Covered in this Report

- Asahi Kasei Corporation

- Avient Corporation

- Braskem

- Celanese Corporation

- dsm-firmenich

- DuPont

- Honeywell International Inc.

- Korea Petrochemical Ind. Co., LTD.

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- Röchling SE & Co. KG

- Shandong Longforce Engineering Material Co., Ltd

- TEIJIN LIMITED

Market Opportunities and Future Outlook

A visible gap exists between installed capacity and qualified output for high-end applications, particularly where adoption depends on tight resin cleanliness and consistent molecular-weight distribution, such as separator membranes and medical devices. The same pattern shows up in the push for localized supply chains in North America for battery materials, including the U.S. Department of Energy award process tied to Braskem’s La Porte, Texas, UHMWPE capacity for lithium-ion battery separators. Standards activity in offshore and medical end uses also increases the emphasis on qualification readiness, including China’s GB/T 21328-2024 for offshore rope performance and evolving FDA guidance expectations for orthopedic components.

Europe also offers a near-term opening for import substitution as new regional supply projects shorten qualification loops for converters that currently rely on premium imports. Repsol is constructing a 15,000 tpy UHMWPE plant at the Puertollano Industrial Complex in Spain, with commissioning scheduled for 2026. At the same time, project timing and capital allocation remain tied to petrochemical cycle conditions and EV demand volatility, including Braskem’s termination of the UTEC-1 LIBS retrofit and expansion project at La Porte after FEL-2 engineering in December 2025. As a result, opportunities cluster around suppliers that can redirect capacity toward higher-margin grades and secure off-take requirements.

Recent Industry Developments in Ultra-high Molecular Weight Polyethylene Market

- January 2026: Solstice Advanced Materials announced a USD 220 million expansion of its ballistic fiber production in Colonial Heights, Virginia, to increase Spectra Shield fiber output. The investment strengthens domestic availability of UHMWPE-based armor materials and raises competitive pressure on specialty fiber supply aimed at defense and security end uses.

- June 2025: Braskem entered final negotiations for a USD 50 million U.S. Department of Energy award to expand UHMWPE output at La Porte, Texas, targeted at lithium-ion battery separator applications. The move highlights policy-backed efforts to onshore critical polymer inputs for electrification supply chains and supports converter qualification activity around domestic powder sources.

- November 2024: Updated 510(k) guidance for orthopedic bone plates and screws from the U.S. FDA clarifies performance data expectations for UHMWPE components. The guidance strengthens the qualification pathway for medical-grade UHMWPE and affects supplier decisions and market entry timing for medical devices.

Ultra-high Molecular Weight Polyethylene Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the ultra-high-molecular-weight polyethylene (UHMWPE) market covers demand for UHMWPE resin and semi-finished forms used in high wear, low friction, and high strength applications across industrial and specialty end uses.

Scope exclusions: The sizing excludes downstream fabricated finished goods where UHMWPE is only one input (for example, completed devices, assemblies, or installed systems).

Segments Covered in This Report

- By Form

- Powder

- Fibers

- Sheets and Films

- Rods and Tubes

- Other Forms (3-D Printing Filament, etc.)

- By End-use Industry

- Automotive

- Aerospace and Defense

- Medical

- Electronics

- Chemical

- Other End-user Industries (Oil and Gas, Sports, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping UHMWPE supply, trade, and end-use pull so the model has real anchors before assumptions are added. Public sources were used to understand polymer demand and industrial activity, including USITC and UN Comtrade trade statistics, Eurostat industry tables, USGS materials context, and customs and port statistics published by select national agencies.

We also reviewed technical and adoption signals from ISO and ASTM-related testing references for the way performance is reported, patent databases for process and application activity, and peer-reviewed journals on items such as battery separator performance, medical wear, and fiber processing. Company annual reports, investor presentations, and reputable press were checked to confirm capacity expansions, product positioning, and regional demand commentary, with company financials and news intelligence databases used to standardize timelines and identifiers. These sources are not exhaustive, and we used additional public documents and data points for collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test what desk sources cannot fully show, especially form-level mix shifts and near-term pricing and contract behavior for UHMWPE. We spoke with participants across the resin and fiber value chain, including distributors, converters, and procurement and engineering roles across APAC, EMEA, and the Americas. The inputs were then used to close gaps and confirm adoption patterns in medical wear parts, industrial wear components, and energy storage uses.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 41% |

| Mid tier: 56% | Functional/Unit leaders: 38% | EMEA: 32% |

| Smaller Players: 18% | Managers: 49% | Americas: 27% |

Market-Sizing & Forecasting

The core model is built using a top-down reconstruction of demand in tons, where production, trade flows, and consumption signals are translated into regional apparent demand and then split across key application pools. Results are then corroborated with selective bottom-up checks, such as sampling supplier capacity additions and typical run rates, and validating implied volumes using ASP bands so totals stay realistic.

Inputs used in the model include polymer output and trade direction, capacity additions and debottlenecking timelines, typical conversion yields from powder into fiber and separator-related material, replacement and wear-driven demand in industrial parts, and the pace of EV battery separator build-outs that influence high purity demand. Where a bottom-up check has missing coverage for private operators, gap fills are handled with conservative utilization ranges that were validated in interviews, and then applied consistently by region.

Forecasting is done with scenario analysis supported by lightweight regression-style relationships between industrial output indicators, vehicle and energy storage build cycles, and historical resin price movements, followed by expert review for realism. When the year-by-year logic is finalized, volume growth and price progression are kept separate during the build, then recombined only after the drivers are reviewed for consistency.

Data Validation & Update Cycle

Checks are run at several points so totals do not drift away from real-world constraints. We compare model outputs with independent signals such as trade balance direction, announced capacity and commissioning slippage, and implied per-application intensity. Any outliers are reviewed again before sign-off.

Anomaly checks include year-over-year jumps, regional share swings, and price-to-volume mismatches, which are traced back to the driver assumptions and corrected when needed. Reports are refreshed annually, with interim updates when material events occur such as major plant outages, large expansions, or sharp feedstock-driven price moves. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Ultra High Molecular Weight Polyethylene Market Size Compared Against Other Published Estimates

Published estimates for UHMWPE often vary because the unit of measurement, what is counted as UHMWPE versus adjacent polymers, and the way pricing is applied are not always consistent. Some sources lead with revenue, while others focus on shipment volumes, and the spread widens further when regional coverage and update timing differ.

By tracking volume in tons and then cross-checking implied value using a transparent price-per-ton range, Mordor Intelligence keeps UHMWPE counted as resin demand instead of blending in downstream finished goods. Differences also come from whether fibers and battery separator related demand are treated as resin consumption or as a higher value converted product, and from whether currency timing and inflation uplifts are applied uniformly across years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.59 M (2026) | |

| Global Consultancy A | USD 2.93 B (2025) | This estimate is published in USD and likely applies a broader value chain scope, where converted forms and higher downstream pricing can be blended into the total, which lifts the value versus a resin-volume anchored view. |

| Industry Publisher B | USD 2.14 B (2024) | The stated number is revenue-led and tied to a 2024 base year, and it also references both volume and revenue, which can create mixing of measurement bases and a slower refresh of capacity timing and price changes. |

The table shows that the largest gap is not only the year, but also whether the total is built from tons and then priced, or built directly from revenue with broader product boundaries. When the same scope and unit are kept consistent, the market story becomes easier to trace back to clear drivers like capacity ramps, trade direction, and end-use pull, and we can explain each step without relying on hidden multipliers.

Key Questions Answered in the Report

How large will global demand be for ultra-high molecular weight polyethylene by 2031?

Volume is forecast to reach 1.06 million tons by 2031, reflecting a 12.36% CAGR from 0.59 million tons in 2026.

Which form contributes most to future growth?

Powder retains leadership, expanding at a 12.64% CAGR as new gel-spinning lines convert it into high-tenacity fiber.

What drives regional expansion in North America?

Department of Energy funding for battery-separator powder and defense demand for Spectra fiber lift regional CAGR to 12.99%.

Why is electronics outpacing medicine in growth rate?

Semiconductor packaging and insulation films require low-dielectric UHMWPE, pushing electronics to a 13.10% CAGR through 2031.

Page last updated on: