Middle East Feed Pigments Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

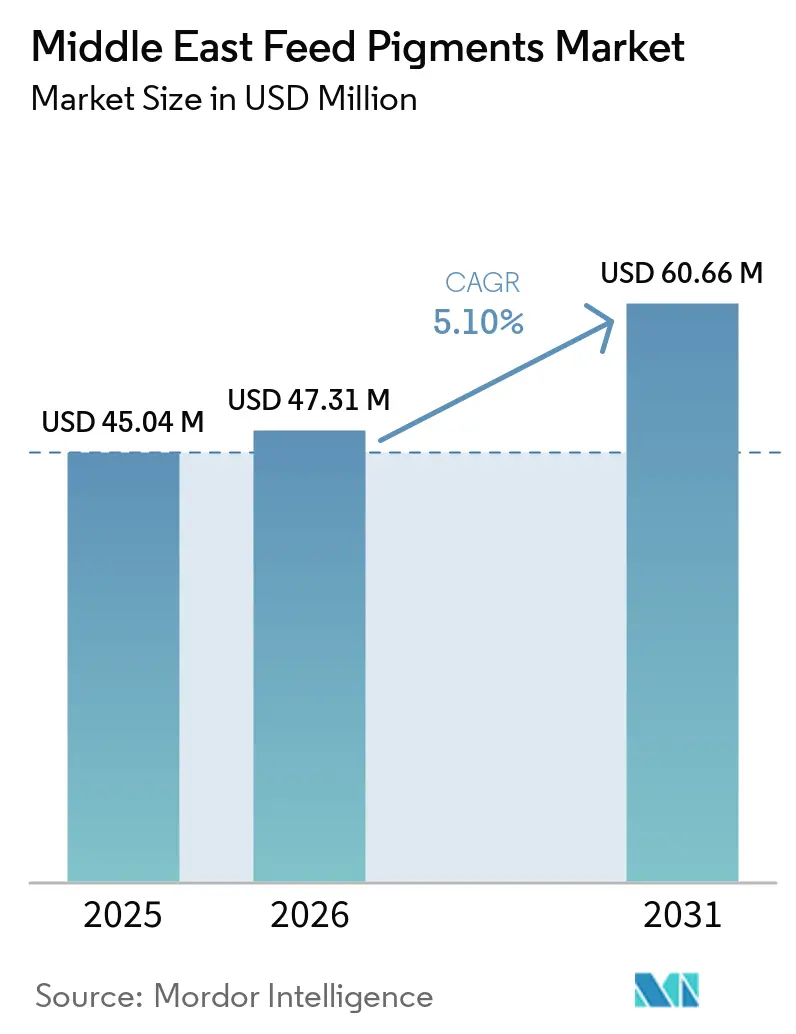

| Base Year Market Size (2025) | USD 45.04 Million |

| Market Size (2026) | USD 47.31 Million |

| Market Size (2031) | USD 60.66 Million |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Feed Pigments Market Analysis by Mordor Intelligence

The Middle East feed pigments market size is projected to expand from USD 45.04 million in 2025 and USD 47.31 million in 2026 to USD 60.66 million by 2031, registering a 5.10% CAGR between 2026 and 2031. The market is moving on the back of stronger livestock intensification, especially in poultry and aquaculture, where color performance remains tied to product acceptance and farm economics. Demand is also supported by the fact that animals cannot synthesize these pigments in sufficient amounts, which keeps feed inclusion relevant across commercial systems. The Middle East feed pigments market also benefits from having two steady demand channels, one in poultry pigmentation and the other in aquaculture flesh and shell coloration, which lowers dependence on a single end use. At the same time, supply remains exposed to imported raw materials, so companies with stable sourcing, heat-protected formulations, and strong regional distribution continue to hold an advantage. This creates opportunities for growth while emphasizing supply reliability, product stability, and performance tailored to specific applications.

Key Report Takeaways

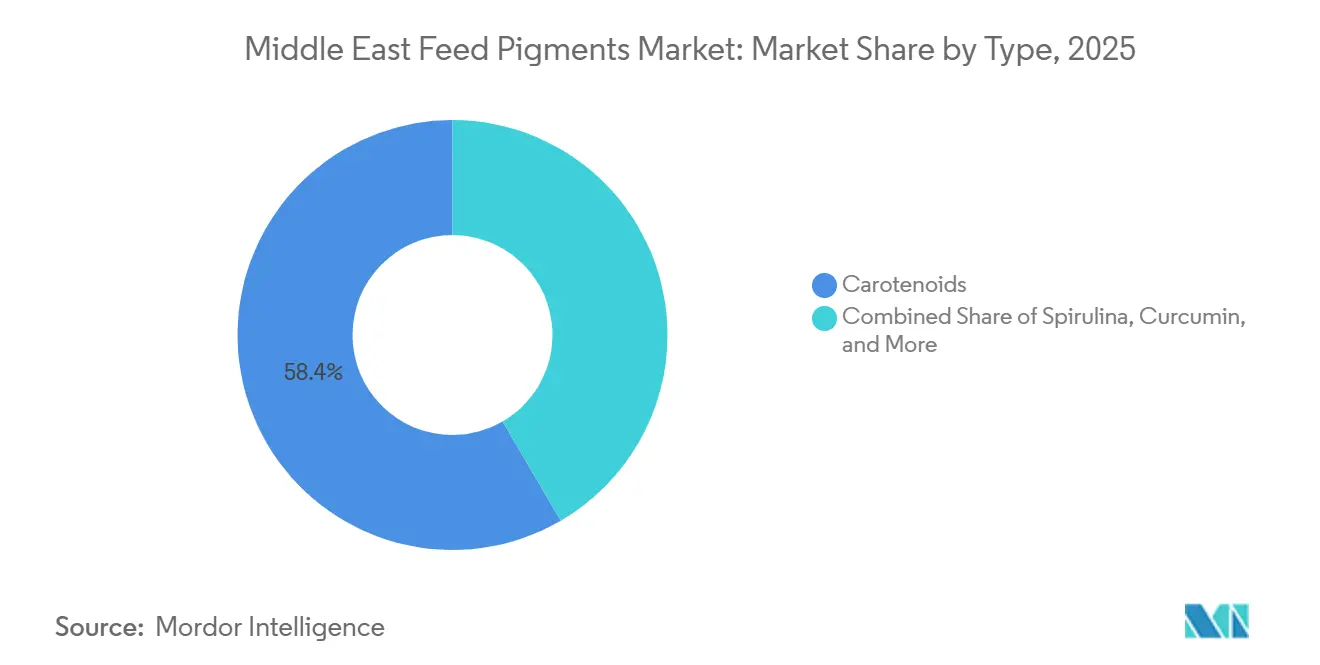

- By type, carotenoids accounted for 58.4% of the Middle East feed pigments market share in 2025, while spirulina is anticipated to expand at a 7.4% CAGR between 2026 and 2031.

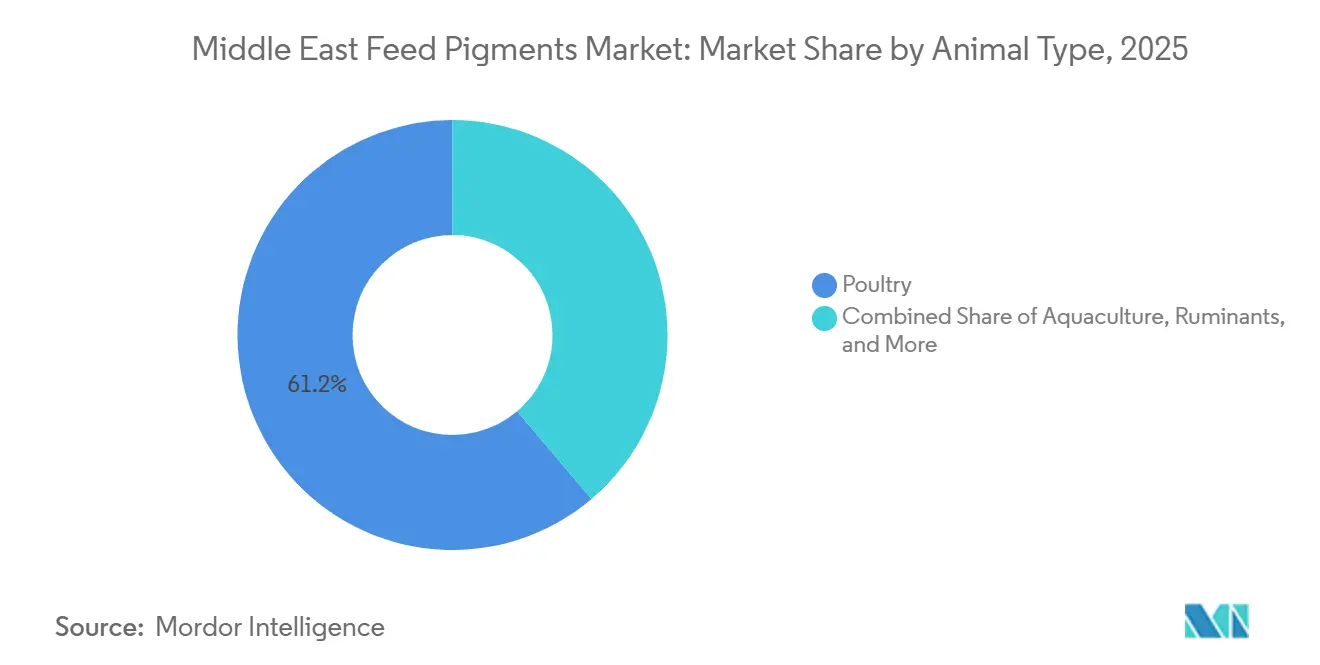

- By animal type, poultry accounted for 61.2% of the Middle East feed pigments market size in 2025, while aquaculture is anticipated to record the highest CAGR of 7.9% between 2026 and 2031.

- By geography, Saudi Arabia accounted for 36.4% of the Middle East feed pigments market share in 2025, while the United Arab Emirates is anticipated to expand at a 6.1% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Feed Pigments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry and aquaculture pigment intensity in hot-climate production systems | +1.30% | Middle East, especially Saudi Arabia, United Arab Emirates, Kuwait, and Oman | Long term (≥ 4 years) |

| Premiumization of egg yolk, broiler skin, and fish flesh color in Gulf retail channels | +0.90% | Middle East, especially Saudi Arabia, United Arab Emirates, and Qatar | Medium term (2-4 years) |

| Food security programs favoring specialized feed additives in Saudi Arabia and the United Arab Emirates | +0.80% | Saudi Arabia and United Arab Emirates | Long term (≥ 4 years) |

| Replacement of broad-spectrum synthetic colorants with species-specific carotenoid blends | +0.60% | Regional adoption with stronger concentration in Saudi Arabia and United Arab Emirates | Medium term (2-4 years) |

| Expansion of halal-positioned natural pigment demand in export-oriented poultry supply chains | +0.50% | Saudi Arabia and United Arab Emirates, with spillover into Kuwait and Qatar | Medium term (2-4 years) |

| Localization of additive manufacturing to improve regional supply reliability | +0.40% | Saudi Arabia and United Arab Emirates, supported by nearby supply hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Poultry and Aquaculture Pigment Intensity in Hot-Climate Production Systems

Poultry and aquaculture systems in the Gulf operate under persistent heat stress, which makes pigment stability a daily formulation issue rather than a cosmetic choice. Carotenoids break down more easily under thermal stress, which means feed producers often need more stable forms to protect active value before deposition in yolk, skin, or fish tissue. This raises the importance of encapsulation, controlled handling, and dependable dosing in the Middle East feed pigments market. BASF SE participates in the feed pigment market through products that help poultry and aquaculture producers achieve targeted yolk and flesh color characteristics while maintaining product quality and consistency[1]Source: BASF Animal Nutrition, “Pigmentation Solutions for Poultry and Aquaculture,” BASF Animal Nutrition, nutrition.basf.com. DSM-Firmenich has also documented the effects of storage and processing conditions on carotenoid stability, supporting the need for protected pigment delivery in warm regional conditions. The aquaculture side follows the same pattern because high ambient temperatures can reduce astaxanthin retention during feed storage and handling. This is one reason the Middle East feed pigments market continues to reward suppliers that can prove stable performance across pelleting, transport, and on-farm use. The result is steady demand for technically differentiated pigments instead of a simple shift toward low-cost imported material.

Premiumization of Egg Yolk, Broiler Skin, and Fish Flesh Color in Gulf Retail Channels

Color remains one of the clearest product signals in fresh poultry, eggs, and farmed fish across Gulf retail channels. Deep yolk color, uniform broiler skin tone, and attractive fish flesh color continue to influence how buyers judge freshness and value at the point of purchase. That keeps pigmentation programs commercially relevant even when feed budgets come under pressure. Feed pigments are widely used to help producers achieve consistent coloration, reflecting the importance of visual quality attributes for product differentiation and consumer acceptance. In the Middle East feed pigments market, this preference supports repeat use rather than occasional supplementation, especially among integrated operations serving modern retail and hospitality channels. It also strengthens the case for standardized color scoring and tighter dosing routines. Fish producers benefit similarly because appearance matters in premium sales channels and repeat purchase behavior. This keeps the Middle East feed pigments market aligned with retail presentation standards as much as with animal nutrition needs.

Food Security Programs Favoring Specialized Feed Additives in Saudi Arabia and the United Arab Emirates

Food security policy remains one of the strongest long-range supports for the Middle East feed pigments market. Saudi Arabia’s National Agricultural Strategy targets higher domestic poultry self-sufficiency, and output reached around 1 million metric tons in 2024, indicating that production expansion is already underway[2]Source: Saudi Poultry Council, “Saudi Arabia Targets 90% Poultry Self-Sufficiency Within Vision 2030,” Saudi Poultry Council, saudipoultry.net. Saudi Arabia also aims to raise seafood output to 530,000 metric tons by 2030, according to the Saudi Arabian Ministry of Environment. The United Arab Emirates follows a similar path through its National Food Security Strategy, which supports controlled food production and a broader discipline on input quality. Once production systems become more intensive and more policy-backed, additives such as feed pigments move closer to being standard inputs rather than optional enhancements. This matters in the Middle East feed pigments market because both poultry and aquaculture expansion require consistent output quality to justify capital investment. The policy push, therefore, supports not just volume growth but also greater acceptance of premium and stable pigment formats. Over time, this strengthens the role of specialized suppliers, enabling them to align product quality with national production goals.

Replacement of Broad-Spectrum Synthetic Colorants with Species-Specific Carotenoid Blends

The market is gradually moving away from simple one-size-fits-all coloring programs and toward blends designed around species, production stage, and target appearance. This shift does not always increase total pigment tonnage, but it often improves commercial value because farmers want better deposition efficiency and more reliable output. Consequently, the market is moving toward species-specific pigmentation programs that deliver more consistent, targeted coloration outcomes. Scientific work from King Abdullah University of Science and Technology has also reinforced this approach in aquaculture, where spirulina digestibility and feed response differ across species, including sobaity seabream and snubnose pompano[3]Source: Frontiers in Sustainable Food Systems, “Protein, Energy, and Amino Acids Digestibility of Spirulina (Arthrospira platensis) Fed to Snubnose Pompano Trachinotus blochii and Sobaity Seabream Sparidentex hasta,” Frontiers in Sustainable Food Systems, frontiersin.org. That matters for the Middle East feed pigments market because regional aquaculture is growing around species with different nutritional and coloration responses. As a result, buyers are less willing to depend on undifferentiated pigment inputs. They increasingly look for documented formulations with predictable performance under local production conditions. This makes the Middle East feed pigments market more specification-driven and less open to simple commodity substitution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High dependence on imported carotenoid and spirulina inputs | -0.80% | Middle East, especially Saudi Arabia, United Arab Emirates, Oman, Kuwait, and Qatar | Long term (≥ 4 years) |

| Narrow application base outside poultry and aquaculture | -0.50% | Regional, with stronger limitation in smaller livestock markets | Medium term (2-4 years) |

| Approval and registration friction across multiple Middle Eastern jurisdictions | -0.40% | Middle East, including Saudi Arabia, United Arab Emirates, Israel, Kuwait, Oman, and Qatar | Medium term (2-4 years) |

| Heat and storage sensitivity of natural pigments in regional logistics | -0.30% | Middle East, especially Saudi Arabia, United Arab Emirates, Kuwait, and Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Dependence on Imported Carotenoid and Spirulina Inputs

The Middle East feed pigments market still depends on imported carotenoids and spirulina for most of its functional supply. That leaves feed mills and integrators exposed to changes in lead times, shipping disruptions, and shifts in raw material pricing that they cannot fully control. The market has very limited local raw material depth, so any issue in upstream supply tends to quickly affect availability and cost. In September 2024, DSM-Firmenich opened a new manufacturing plant in Egypt to serve customers across the Middle East, reflecting the need for stronger local service and lower delivery risk[4]Source: DSM-Firmenich, “DSM-Firmenich Opens Animal Nutrition and Health Manufacturing Plant in Egypt,” DSM-Firmenich, dsm-firmenich.com. At the same time, aquaculture expansion in Saudi Arabia continues to drive demand for specialized pigment inputs that lack a regional supply solution. This imbalance matters because a growing market with imported dependence often sees periods of tighter customer planning and more conservative inventory decisions. Smaller buyers feel this first because they usually have less bargaining power and fewer supply alternatives. As long as import reliance stays high, the Middle East feed pigments market will remain more vulnerable to supply-side pressure than categories with stronger domestic production support.

Narrow Application Base Outside Poultry and Aquaculture

The market remains concentrated in poultry and aquaculture, limiting the scope of future expansion. Poultry is the core volume base, while aquaculture is the primary driver of growth, so the sector does not yet benefit from strong diversification across many animal categories. Saudi Arabia’s production strategy continues to support poultry and aquaculture directly, which reinforces this narrow structure rather than widening it. Saudi aquaculture targets also deepen the same pattern by adding new demand within an already important application area rather than opening a new one. Ruminant demand exists, but it stays secondary and is often linked more to nutritional support than to visible color outcomes. Swine remains a very small commercial category in the region, which removes one of the major pigment demand pools seen in some overseas markets. This means total demand in the Middle East feed pigments market remains closely linked to the pace of poultry placements and the execution of aquaculture projects. A narrow end-use base can still support growth, but it makes the market less diversified and more exposed to a smaller set of production cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carotenoids Hold the Lead While Spirulina Adds the Strongest Growth

Carotenoids accounted for 58.4% of the Middle East feed pigments market share in 2025, making them the clear leader by value. They were followed by spirulina, curcumin, and other types, which together served smaller and more specialized use cases. Carotenoids remain central because they meet both poultry yolk and skin programs and the needs of aquaculture flesh coloration. BASF SE and DSM-Firmenich continue to support this segment through dedicated carotenoid portfolios and heat-protected product formats. Their established regulatory acceptance, proven pigmentation efficiency, and compatibility with commercial feed manufacturing further strengthen demand.

Spirulina is anticipated to record the fastest growth at a 7.4% CAGR from 2026 to 2031, followed by curcumin, carotenoids, and other types. Its appeal lies in providing color support and functional nutritional value in a single ingredient, which is especially useful in aquaculture. Research conducted by the Ministry of Environment, Water and Agriculture, Riyadh, Saudi Arabia, on the Protein, Energy, and Amino Acid Digestibility of Spirulina in 2024 showed a positive feed response and strong digestibility in relevant fish species, which supports its rising adoption in the Middle East feed pigments market. It is also gaining traction in aquaculture applications due to its dual role as a natural pigment source and functional nutritional ingredient, supporting its use in premium and specialized feed formulations.

By Animal Type: Poultry Leads Current Demand While Aquaculture Drives the Fastest Expansion

Poultry accounted for 61.2% of the Middle East feed pigments market in 2025, ahead of aquaculture, ruminants, and swine. This position reflects the strong role of broiler skin and egg yolk pigmentation in regional production systems. Poultry producers rely on steady color outcomes because retail presentation and grading remain closely linked to product acceptance. The category also benefits from long-established feed inclusion practices and large integrated production bases across major countries in the region. Rising consumer preference for visually appealing poultry products continues to support consistent pigment demand.

Aquaculture is anticipated to expand at the fastest pace, with a 7.9% CAGR through 2031, followed by poultry, ruminants, and swine in that order. This is tied to aquaculture capacity plans in Saudi Arabia. The Middle East feed pigments market, therefore, sees aquaculture as its main forward demand driver, while poultry remains the largest-volume anchor, and ruminants and swine remain comparatively limited. Growing investments in intensive fish farming and premium seafood production further strengthen prospects for pigment consumption.

Geography Analysis

Saudi Arabia accounted for 36.4% of the Middle East feed pigments market in 2025, making it the largest country market in the region, as it combines scale in poultry with a fast-rising aquaculture base. The Saudi Ministry of Environment, Water, and Agriculture's expansion plans are supported by approximately USD 4.5 billion in planned sector investments under Vision 2030, with support covering capital costs for projects that use modern production technologies. This policy direction supports pigment demand indirectly because higher-intensity production systems depend on better feed control and more consistent output quality. The scale of Saudi Arabia's livestock and aquaculture sectors gives the country considerable influence over purchasing patterns, quality expectations, and supplier strategies within the Middle East feed pigments market.

The United Arab Emirates is anticipated to expand at a 6.1% CAGR between 2026 and 2031, and holds the second-largest position. Its demand profile is shaped by premium retail, controlled production systems, and food security planning. The National Food Security Strategy supports quality-certified inputs and stronger oversight across local food production systems. This creates a favorable setting for pigment products that offer documented quality and stable technical performance. Israel also stands out as a technically advanced market where feed input standards and product quality expectations remain comparatively strong. Qatar and Kuwait are smaller in livestock base, but their poultry operations continue to favor reliable pigmentation programs tied to premium end-market presentation.

Oman remains an emerging geography in the Middle East feed pigments market because aquaculture development is gradually improving its downstream demand profile. The Rest of Middle East category, including Iraq, Jordan, Lebanon, Yemen, and Bahrain, is more fragmented and more dependent on distributor-led supply. These smaller markets still contribute incremental volume, especially through conventional poultry pigmentation programs, but they lack the scale of Saudi Arabia and the United Arab Emirates. As a result, regional growth continues to center on the countries that can combine large feed demand with policy-backed livestock and aquaculture expansion.

Competitive Landscape

The Middle East feed pigments market is moderately concentrated, with several established multinational companies accounting for a significant share of total market revenue in 2025. Key participants include DSM-Firmenich, BASF SE, Kemin Industries, Inc., EW Nutrition, and Synthite Industries Ltd., alongside a broader group of regional specialists, distributors, and niche suppliers. The market structure favors companies that can provide formulation stability, quality assurance, regulatory compliance, and consistent product availability. It also makes technical service an important competitive tool, as buyers in the region often require support with handling practices, dosing optimization, and minimizing heat-related pigment degradation during feed processing.

DSM-Firmenich remains especially important because it combines a broad carotenoid position with visible regional investment and portfolio restructuring. BASF SE is also sharpening its focus on carotenoids and vitamins. In November 2025, BASF SE announced an agreement to sell its global glycinate business to Biochemm, reinforcing a tighter portfolio orientation around its core animal nutrition lines. These actions show that the largest suppliers are not only competing on products, but also on how clearly they define their strategic priorities.

Regional servicing has also become a more visible source of advantage in the Middle East feed pigments market. DSM-Firmenich’s plant opened in Egypt in September 2024 strengthened near-regional supply support for customers across the Middle East. BASF SE continues to compete through established pigmentation brands and technical positioning in poultry and aquaculture. Kemin Industries, Inc. and EW Nutrition, remain relevant because the market still values dependable supply and species-specific application support. Smaller players can still win business, but they usually need a clear advantage in pricing, service speed, or natural product positioning. The competitive picture therefore remains concentrated, but not closed, because technical credibility and distribution strength still create room for selective share gains.

Middle East Feed Pigments Industry Leaders

DSM-Firmenich

BASF SE

Kemin Industries, Inc.

EW Nutrition

Synthite Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DSM-Firmenich has agreed to sell its Animal Nutrition and Health business to CVC Capital Partners for USD 2.6 billion. As part of the transaction, the Vitamins, Carotenoids, and Aroma Ingredients portfolio will be established as a standalone entity named Essential Products Company. The deal, anticipated to close by the end of 2026, will significantly restructure the carotenoid supply chain for distributors in the Middle East.

- November 2025: BASF SE and feed additive specialist Biochem have entered into a binding agreement for Biochem's acquisition of BASF's global glycinate business. BASF SE has reaffirmed its strategic focus on vitamins and carotenoids as the core of its animal nutrition portfolio. This decision allows BASF to allocate resources toward key pigment and vitamin segments, addressing the increasing demand from the Middle East's poultry and aquaculture industries.

- September 2024: DSM-Firmenich has officially inaugurated its 10,000 sq. m. Animal Nutrition and Health manufacturing facility in Sadat City, Egypt. This marks the company's 50th global facility, with an annual production capacity of 10,000 tons of feed additives aimed at serving the Middle East market.

Middle East Feed Pigments Market Report Scope

Feed pigments are feed additives used to enhance the coloration of animal products, particularly egg yolks, poultry skin, fish flesh, and crustacean shells, through the inclusion of natural or synthetic pigment compounds in animal diets. The Middle East feed pigments market report is segmented by type (carotenoids, curcumin, spirulina, and other types), by animal type (aquaculture, poultry, ruminants, swine, and other animal types), and by geography (Saudi Arabia, United Arab Emirates, Israel, Qatar, Kuwait, Oman, and rest of Middle East). The market forecasts are provided in terms of value (USD) and volume (Metric Tons).

| Carotenoids |

| Curcumin |

| Spirulina |

| Other Types |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| Saudi Arabia |

| United Arab Emirates |

| Israel |

| Qatar |

| Kuwait |

| Oman |

| Rest of Middle East |

| By Type | Carotenoids | |

| Curcumin | ||

| Spirulina | ||

| Other Types | ||

| By Animal Type | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Israel | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the size outlook for the Middle East feed pigments space through 2031?

The Middle East feed pigments market size is projected to reach USD 60.66 million by 2031, growing at a 5.1% CAGR over 2026 to 2031.

Which animal category generates the most demand for feed pigments in the region?

Poultry is the leading category, holding 61.2% of Middle East feed pigments market size in 2025, because broiler skin and egg yolk coloration remain important in regional retail channels.

Which type of feed pigment is growing the fastest in the region?

Spirulina is the fastest-growing type, with an anticipated 7.4% CAGR between 2026 and 2031, supported by its dual role in color enhancement and functional nutrition in aquaculture feed.

Why is aquaculture becoming important for pigment suppliers in the Middle East?

Aquaculture is the fastest-growing animal segment at a 7.9% CAGR, and Saudi Arabia alone targets an increase in output to reach 530,000 metric tons by 2030.

Page last updated on: