Middle East Feed Yeast Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 37.91 Million |

| Market Size (2026) | USD 42.81 Million |

| Market Size (2031) | USD 48.37 Million |

| Growth Rate (2026 - 2031) | 2.47% CAGR |

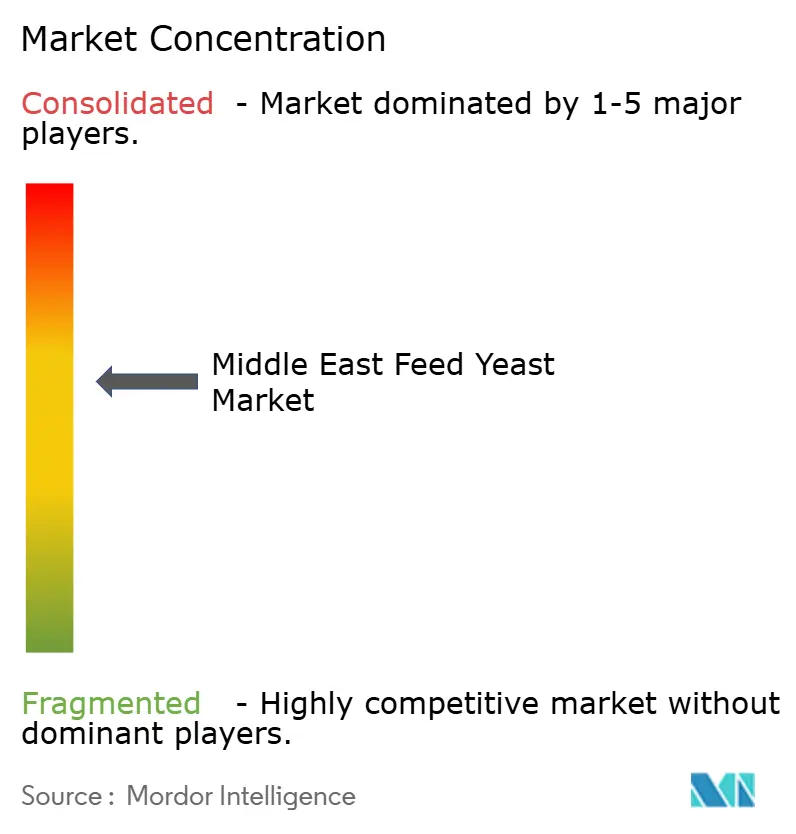

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Feed Yeast Market Analysis by Mordor Intelligence

The Middle East feed yeast market size is projected to expand from USD 37.91 million in 2025 and USD 42.81 million in 2026 to USD 48.37 million by 2031, registering a CAGR of 2.47% between 2026 and 2031. The Middle East feed yeast market is being supported by the steady expansion of industrial livestock systems and food security programs across the Gulf Cooperation Council countries, with Saudi Arabia remaining the clearest demand center for poultry feed inputs and related functional additives. The shift away from antibiotic growth promoters is also moving procurement toward yeast-based solutions that can support gut health, immune function, and feed efficiency under tighter antimicrobial resistance rules in the United Arab Emirates and Saudi Arabia. Rising mycotoxin pressure in imported feed grains is widening the use case for yeast cell wall fractions and spent yeast, especially in poultry systems where contamination risk directly affects productivity. The Middle East feed yeast market is also benefiting from demand for more specialized products in dairy and aquaculture, where heat stress control, antioxidant supplementation, and immune support matter more than simple price competition. Competition remains moderate because suppliers with strong technical service, registered product portfolios, and dependable regional distribution relationships are better placed to defend share than companies competing only on price.

Key Report Takeaways

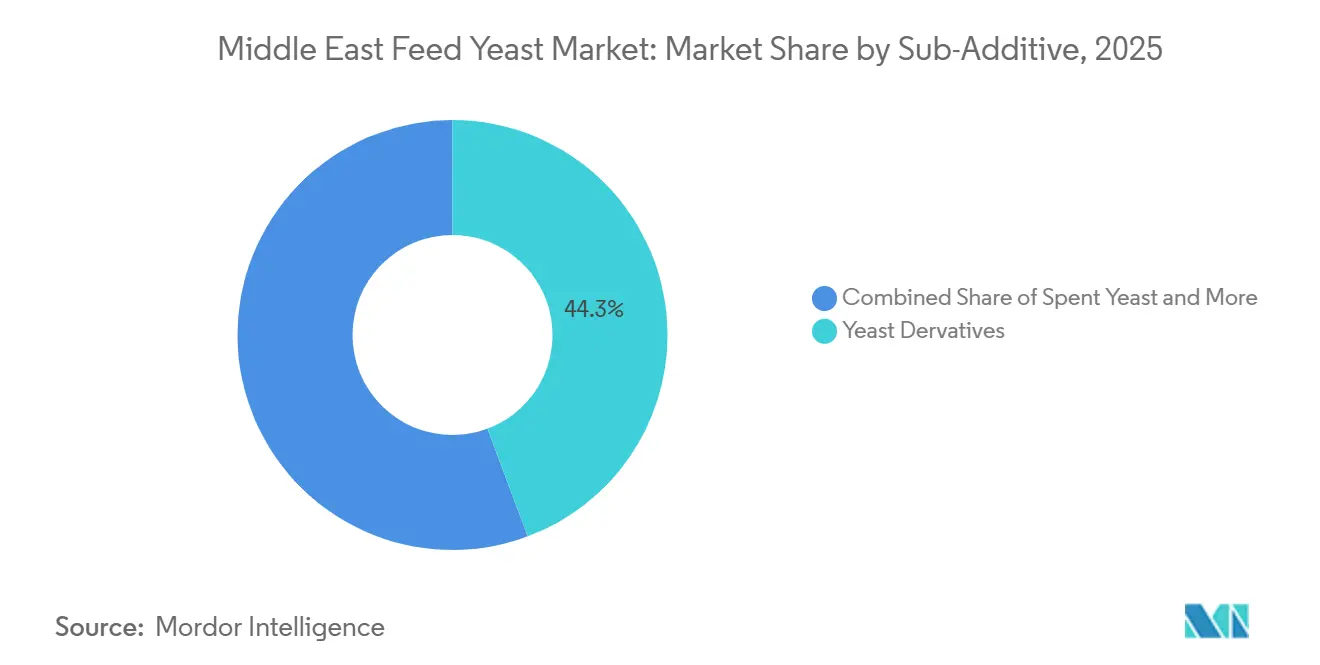

- By sub-additive, yeast dervatives was the largest segment, accounted for 44.3% of the Middle East feed yeast market share in 2025, and spent yeast is the fastest-growing segment, with a projected 2.7% CAGR through 2031.

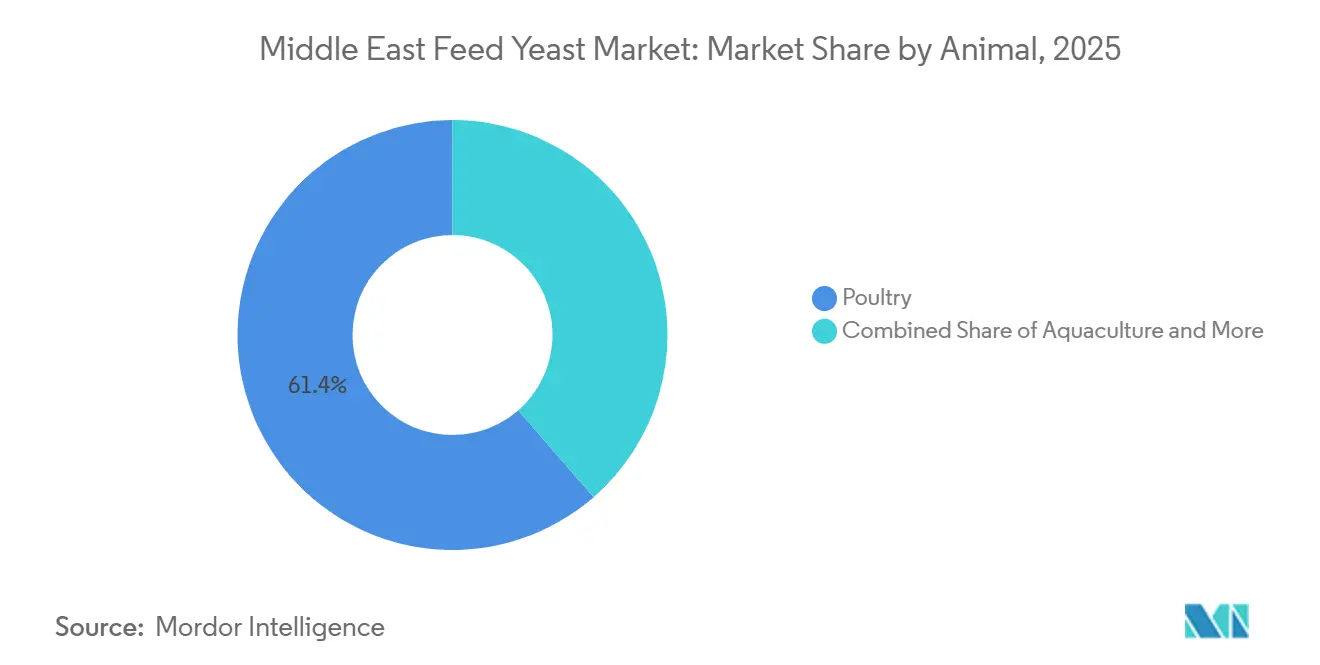

- By animal, poultry was the largest segment with a 61.4% of the Middle East feed yeast market size in 2025, and it is also the fastest-growing segment with a 2.6% CAGR through 2031.

- By geography, Saudi Arabia was the largest country segment with a 40.1% share in 2025, while Iran was the fastest-growing country segment with a projected 2.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Feed Yeast Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saudi poultry self-sufficiency expansion | +0.8% | Saudi Arabia | Short term (≤ 2 years) |

| Antibiotic-reduction shift toward functional yeast additives | +0.6% | United Arab Emirates, Saudi Arabia, Gulf Cooperation Council | Short term (≤ 2 years) |

| Dairy yield optimization across Saudi Arabia and Gulf Cooperation Council | +0.4% | Saudi Arabia, Gulf Cooperation Council | Medium term (2-4 years) |

| United Arab Emirates aquaculture capacity build-out | +0.3% | United Arab Emirates, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Heat-stress mitigation demand for gut-stable yeast products | +0.3% | Core Gulf Cooperation Council markets, spillover to Iran | Short term (≤ 2 years) |

| Mycotoxin pressure in imported feed grains | +0.2% | Region wide, concentrated in Saudi Arabia and Iran | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Saudi Poultry Self-Sufficiency Expansion

Saudi Arabia’s broiler meat production reached 1.2 million metric tons in 2024, and the country’s self-sufficiency rate stood at 72%, keeping domestic livestock expansion closely tied to the Vision 2030 food security target of 90%, as per General Authority for Statistics (GASTAT). This production push is raising the need for more consistent feed performance across large integrated poultry operations in the Middle East feed yeast market. Bigger farms usually rely on standardized feed programs, which favor additives that support immunity and improve feed conversion without disrupting existing formulations. The same expansion is also tightening quality expectations for supplier service, registration readiness, and product stability in commercial rations. As Saudi producers scale output, the Middle East feed yeast market is seeing stronger demand for yeast-based products that fit both productivity goals and export-oriented production standards.

Antibiotic-Reduction Shift Toward Functional Yeast Additives

The United Arab Emirates National Action Plan on Antimicrobial Resistance 2025 to 2031 and Saudi Arabia’s comparable framework are pushing livestock systems toward lower reliance on antibiotic growth promoters under the World Health Organization One Health approach. In the Middle East feed yeast market, that change is most visible in broiler and shrimp production, where gut health support and feed efficiency remain critical after antibiotic withdrawal. A 2025 review in Veterinary Science found that yeast-derived products and probiotics can help maintain productivity during early growth stages in poultry after antibiotic growth promoters are removed. That evidence matters because it gives buyers a scientific basis for replacing older synthetic pathways with functional yeast inputs. The Middle East feed yeast market is therefore gaining support from a demand stream driven by compliance pressure rather than short-term cost shifts.

Dairy Yield Optimization Across Saudi Arabia and Gulf Cooperation Council

The dairy side of the Middle East feed yeast market is gaining support from higher milk yield targets in Saudi Arabia and other Gulf Cooperation Council countries, where herd productivity is increasingly tied to precision nutrition and animal resilience. Heat stress remains a major operational problem in these systems, making rumen-stabilizing additives more relevant in commercial dairy feed. A 2025 study in Animals demonstrated that live yeast supplementation in heat-stressed dairy cows increased dry matter intake by 0.3 kg/day and milk yield by 0.7 kg/day[1]Source: MDPI Editorial Office, “A Meta-Analysis of the Association Between Live Yeast Supplementation and Lactation Performance in Dairy Cows Under Heat Stress,” Animals, mdpi.com. Those results support the use of live yeast where producers want measurable output gains rather than low-cost filler ingredients. This has created a growing demand in the Middle East feed yeast market, where specialized live yeast and selenium yeast products have the potential to grow independently of poultry production cycles.

United Arab Emirates Aquaculture Capacity Build-Out

Aquaculture is still smaller than poultry in the Middle East feed yeast market, but its demand profile is growing as the United Arab Emirates builds domestic fish and shrimp capacity through large capital projects. In December 2024, ADQ announced plans to establish a land-based shrimp farm in Abu Dhabi as part of the country's initiative to reduce reliance on imported seafood[2]Source: AGBI Staff, “ADQ Plans Abu Dhabi Shrimp Farm With Korean Startup,” AGBI, agbi.com. The same policy direction is also visible in Abu Dhabi’s state-linked aquaculture development plans, which are projected to lift demand for quality-controlled aquafeed inputs over time. Aquaculture uses yeast differently from poultry because immune support, palatability, and antioxidant function matter alongside protein contribution. This has created a growing demand in the Middle East feed yeast market, where specialized live yeast and selenium yeast products have the potential to grow independently of poultry production cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependence and freight volatility | -0.3% | Iran, Gulf Cooperation Council | Short term (≤ 2 years) |

| Feed additive registration and Arabic labeling burden | -0.2% | Saudi Arabia, Gulf Cooperation Council | Medium term (2-4 years) |

| Halal and substrate traceability scrutiny | -0.2% | Core Gulf Cooperation Council markets | Medium term (2-4 years) |

| Field-level efficacy variability in hot-climate pelleting | -0.1% | Core Gulf Cooperation Council markets, spillover to wider Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Dependence and Freight Volatility

The region’s feed sector depends heavily on imported corn, soybean meal, and fermentation-linked inputs, leaving the Middle East feed yeast market exposed to freight volatility, port disruptions, and geopolitical routing risks. Iran experiences significant challenges in this area due to reduced food affordability, driven by currency depreciation and a decline in domestic grain production. Additionally, feed availability and producer margins continued to face significant pressure, according to the Statistical Center of Iran (SCI). Live yeast products are especially vulnerable because shelf life and temperature sensitivity limit how much stock importers can safely hold. That makes the Middle East feed yeast market more sensitive to external supply shocks than categories that can be warehoused with fewer performance risks.

Feed Additive Registration and Arabic Labeling Burden

Saudi Arabia requires prior registration of feed additives before commercial sale, and imported products must also have Arabic labeling that meets formal clearance requirements. In the Middle East feed yeast market, which adds time and cost to product launches, especially for newer yeast derivatives and selenium yeast products that may not already have precedent approvals. Companies with strong global portfolios still face separate regulatory paths across different Middle Eastern countries, which slows regional rollout. This matters because product innovation loses speed when translation work, dossiers, and approval cycles stretch over many months. The burden is not enough to stop growth, but it does favor established suppliers with registered products and local regulatory support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Spent Yeast Anchors Cost-Effective Feed Formulations

Yeast Derivatives held the largest market share at 44.3% in 2025, making it the anchor product in commercial poultry and ruminant rations across the Middle East feed yeast market. Its leading position stems from practical value rather than narrow specialization, as it can serve as a protein contributor, an immunostimulant, and a mycotoxin-binding support ingredient in a single formulation. The product mix is significant in a region where feed cost pressures are high, and buyers typically favor products with multiple functional roles. Selenium yeast is gaining relevance in dairy and ruminant applications where selenium deficiency in arid conditions supports demand for organic selenium sources. Live yeast, torula dried yeast, whey yeast, and yeast derivatives each remain present in more targeted niches where performance claims are easier to defend than simple price points.

Within the Middle East feed yeast market size, spent yeast is projected to be the fastest-growing sub-additive segment, with a 2.7% CAGR from 2026 to 2031, indicating that mainstream demand will remain durable even as premium formats expand. A 2024 Frontiers in Veterinary Science study found that hydrolyzed yeast supplementation in heat-stressed broilers improved intestinal redox balance and reduced mortality, supporting the move toward more standardized yeast fractions with clearer performance claims. This creates opportunities for higher-margin formulations within the Middle East feed yeast market, particularly for suppliers capable of transitioning from bulk spent yeast to validated derivative products. The same sub-additive landscape also gives pre-registered products an advantage because Saudi regulatory compliance applies across all functional categories. As a result, the segment is broad enough to support both volume growth and selective premiumization.

By Animal: Poultry Leads by Volume as Aquaculture Opens New Demand Channels

Poultry held the largest market share at 61.4% in 2025, keeping it the clear center of demand in the Middle East feed yeast market. Poultry is also the fastest-growing animal segment, with a projected 2.6% CAGR through 2031, supported by integrated broiler and layer systems that require better gut health, toxin control, and heat-stress management. Broiler production drives most of this volume because reductions in antibiotic use, risks associated with imported grain, and dense production systems all increase the value of multifunctional yeast additives. Layer farms have a somewhat different demand profile, with stronger interest in selenium yeast where eggshell quality and yolk appearance affect commercial value. Ruminants remain important as dairy and beef systems seek more precise feed support under hot conditions, while swine remains limited because of regional dietary constraints.

Within the Middle East feed yeast market, poultry remains the segment with the most scalable demand growth, as the commercial feed base is already large and technically managed. Aquaculture, however, is becoming more relevant as the United Arab Emirates expands fish and shrimp production and places more emphasis on domestic food supply. The Sharjah Executive Council’s 2026 decision on aquaculture farm management also supports a more formal feed-quality environment, favoring certified yeast ingredients over unverified inputs. That gives the Middle East feed yeast industry a second growth channel outside poultry, even if its present volume remains much smaller. Other animals, including horses and companion animals, in Gulf urban markets continue to represent niche demand, with buyers willing to pay higher unit prices for specialized derivative products.

Geography Analysis

Saudi Arabia held the largest share, 40.1%, in 2025, maintaining its position as the main demand base in the Middle East feed yeast market. The country’s food security agenda continues to support poultry expansion, underscoring the need for a reliable supply of feed additives across commercial broiler systems. Saudi Arabia also matters because the Saudi Food and Drug Authority requires pre-market registration and Arabic labeling, which favors suppliers that are already regulatory-ready. The same structure makes Saudi Arabia the most commercially important country in the Middle East feed yeast market, not only because of current demand but also because it sets a higher compliance standard for participation.

Iran is the fastest-growing country segment, with a projected 2.7% CAGR through 2031, though that outlook comes amid difficult near-term operating conditions. Currency weakness has limited the purchasing power of poultry and livestock producers, and trade reporting in 2026 showed that premium additive buying was under clear pressure. Even so, Iran still has a large livestock base, which keeps its long-run demand potential meaningful in the Middle East feed yeast market. Iran’s dependence on imported feed grains also exposes it to aflatoxin and fumonisin risks, which supports the future role of yeast cell wall products once budget conditions stabilize.

The rest of Middle East segment encompasses the United Arab Emirates, Kuwait, Qatar, Bahrain, Oman, Jordan, Iraq, and other markets, each with unique livestock and aquaculture characteristics. Among these, the United Arab Emirates stands out as a key growth area, driven by antimicrobial resistance policies and increased aquaculture investments, which are boosting the demand for functional feed ingredients. In Kuwait and Qatar, there is a more specific demand for selenium yeast and live yeast, particularly in dairy systems where summer heat stress impacts productivity. Oman contributes to market growth due to documented mycotoxin exposure in cereal grains, which underscores the need for yeast-based binders in feed formulations. Across the Gulf Cooperation Council (GCC), the implementation of GSO 2578:2021 provides a unified regulatory framework, creating a more standardized yet stringent environment for the Middle East feed yeast market.

Competitive Landscape

The Middle East feed yeast market is moderately fragmented, with global fermentation specialists and broader animal nutrition suppliers competing on product quality, technical support, regulatory compliance, and distribution depth. Lesaffre et Compagnie, Lallemand Inc., and Angel Yeast Co., Ltd. remain the most visible yeast-focused participants, while Alltech, Inc., Archer Daniels Midland Company, and DSM-Firmenich AG compete through wider nutrition portfolios that include yeast-based offerings. This structure means no single company dominates every application or country in the Middle East feed yeast market. Suppliers that can combine registered products with practical field support are in the strongest position to defend customer relationships.

Corporate restructuring and portfolio expansion are shaping competition more than simple price cuts. In June 2025, Lesaffre et Compagnie completed the acquisition of a 70% stake in Biorigin, strengthening its access to yeast derivatives for animal nutrition and aquaculture. In July 2025, Lallemand Inc. acquired Solyve through its Lallemand Bio-Ingredients business, a move aimed at reinforcing its microbial solutions portfolio[3]Source: Lallemand Inc., “Lallemand Bio-Ingredients Acquires Solyve,” Lallemand Inc., lallemand.com. In February 2026, CVC Capital Partners agreed to acquire 80% of DSM-Firmenich AG’s Animal Nutrition and Health business for EUR 2.2 billion (USD 2.4 billion), with the division split into 2 standalone companies if the deal closes as planned. These moves could change product priorities and channel relationships across the region.

Technology and application support are also becoming more important in the Middle East feed yeast market, especially in poultry and aquaculture. In April 2026, DSM-Firmenich AG launched SciTell Microbiome Analytics, a DNA sequencing tool designed to translate poultry gut microbiome data into nutrition decisions. This type of service can help suppliers justify premium positioning when buyers want clearer proof of feed response. Companies such as Phibro Animal Health Corporation and Nutreco N.V. also benefit from offering mycotoxin management programs that can be paired with yeast cell wall fractions. That broader service model supports retention in a market where feed mills increasingly want fewer suppliers and more complete technical packages.

Middle East Feed Yeast Industry Leaders

BASF SE

DSM-Firmenich AG

Kemin Industries, Inc.

Alltech, Inc.

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Alltech, Inc. and Archer Daniels Midland Company have officially launched their North American Animal Feed Joint Venture. This collaboration integrates 33 Alltech mills and 11 ADM United States feed mills into a network of 44 mills. Alltech's specialty portfolio, including Yea-Sacc yeast culture products, will remain with Alltech as a supplier to the joint venture, ensuring continued supply to Middle Eastern markets where these products have existing regulatory approvals.

- April 2026: Angel Yeast Co., Ltd. introduced its yeast-based bio-feed product range under the Fubon brand in 2026. This range includes live yeast, spent yeast, and yeast cell wall preparations, developed to improve animal nutrition and health while addressing the growing demand for sustainable, efficient feed solutions. The company is actively expanding into neighboring Middle Eastern markets to strengthen its presence and serve a wider customer base.

- October 2025: Lallemand Inc. has expanded the availability of LEVUCELL Trivantage, combining LEVUCELL SC, PROTERNATIVE live yeasts, and AGRIMOS yeast postbiotic, in standard and TITAN micro-encapsulated formats. Its TITAN technology ensures live yeast viability during pelleting at up to 85°C, addressing efficacy challenges in GCC and Middle Eastern high-temperature feed mills.

Middle East Feed Yeast Market Report Scope

Yeast additives are nutritional supplements or ingredients (such as nitrogen, vitamins, and amino acids) added to a yeast culture to stimulate growth and optimize fermentation. They are widely used in baking, brewing, and livestock feed to ensure efficient metabolic performance and consistent final products.

The Middle East feed yeast market report is segmented by sub-additive (live yeast, selenium yeast, spent yeast, torula dried yeast, whey yeast, and yeast derivatives), by animal (aquaculture, poultry, ruminants, swine, and other animals), and by geography (Saudi Arabia, Iran, and the rest of Middle East). The market forecasts are provided in terms of value (USD) and volume (Metric Tons).

| Live Yeast |

| Selenium Yeast |

| Spent Yeast |

| Torula Dried Yeast |

| Whey Yeast |

| Yeast Derivatives |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| Saudi Arabia |

| Iran |

| Rest of Middle East |

| By Sub Additive | Live Yeast | |

| Selenium Yeast | ||

| Spent Yeast | ||

| Torula Dried Yeast | ||

| Whey Yeast | ||

| Yeast Derivatives | ||

| By Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Country | Saudi Arabia | |

| Iran | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the outlook for Middle East feed yeast through 2031?

The Middle East feed yeast market is projected to rise from USD 42.81 million in 2026 to USD 48.37 million by 2031, at a 2.47% CAGR. Growth is being supported by poultry expansion, antimicrobial resistance policy, and wider use of functional feed inputs.

Which animal segment generates the most demand for yeast feed additives in the Middle East?

Poultry is the largest animal segment, with 61.4% share in 2025. Large broiler systems are the main reason for this lead.

Which sub-additive category leads demand in the region?

Yeast dervatives is the largest sub-additive segment, with 44.3% share in 2025. Its role as a protein support ingredient, immunostimulant, and mycotoxin binder supports that position.

Why are yeast-based feed additives gaining traction in Gulf Cooperation Council countries?

Demand is rising because livestock systems are reducing antibiotic growth promoter use and dealing with more heat stress and mycotoxin risk. These conditions make live yeast, spent yeast, and yeast derivatives more useful in commercial feed programs.

Which country is the largest market in the region?

Saudi Arabia is the largest country segment, with 40.1% share in 2025. Its poultry self-sufficiency drive and stricter feed additive registration framework make it the main commercial anchor in the region.

What are the main barriers facing suppliers in this space?

The main barriers are import dependence, freight volatility, feed additive registration rules, Arabic labeling, Halal traceability, and performance variability during hot-climate pelleting. These factors favor companies with strong regulatory support and technically stable products.

Page last updated on: