Middle East Feed Mycotoxin Detoxifiers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

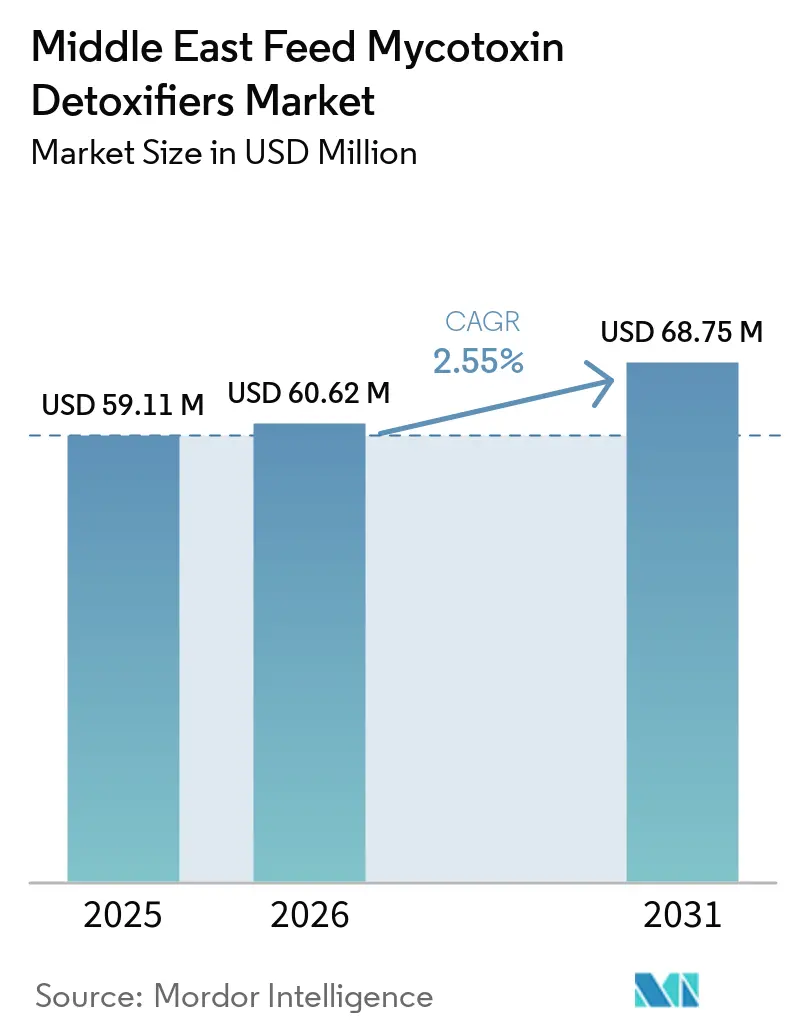

| Base Year Market Size (2025) | USD 59.11 Million |

| Market Size (2026) | USD 60.62 Million |

| Market Size (2031) | USD 68.75 Million |

| Growth Rate (2026 - 2031) | 2.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Feed Mycotoxin Detoxifiers Market Analysis by Mordor Intelligence

The Middle East feed mycotoxin detoxifiers market size is projected to expand from USD 59.11 million in 2025 and USD 60.62 million in 2026 to USD 68.75 million by 2031, registering a CAGR of 2.55% between 2026 and 2031. The Middle East feed mycotoxin detoxifiers market is driven by consistently high contamination levels in imported grains, finished feed, and feed ingredients utilized in commercial livestock systems. Saudi Arabia and Iran remain the core demand centers because both markets depend heavily on imported corn and soybean meal, and both face storage and logistics conditions that can worsen fungal pressure after cargo arrives. Feed safety oversight is also becoming more formal across Gulf Cooperation Council (GCC) markets, which raises the value of registered detoxification products and technical support for large feed mills and integrated livestock operators. Freight disruptions, uneven testing capacity, and the continued preference for low-cost, untreated feed among smaller buyers keep adoption from rising as fast as contamination risk would suggest. Even so, the Middle East feed mycotoxin detoxifiers market continues to benefit from expanding industrial feed production, tighter commercial quality protocols, and a gradual shift from single-mechanism binders toward broader detoxification programs.

Key Report Takeaways

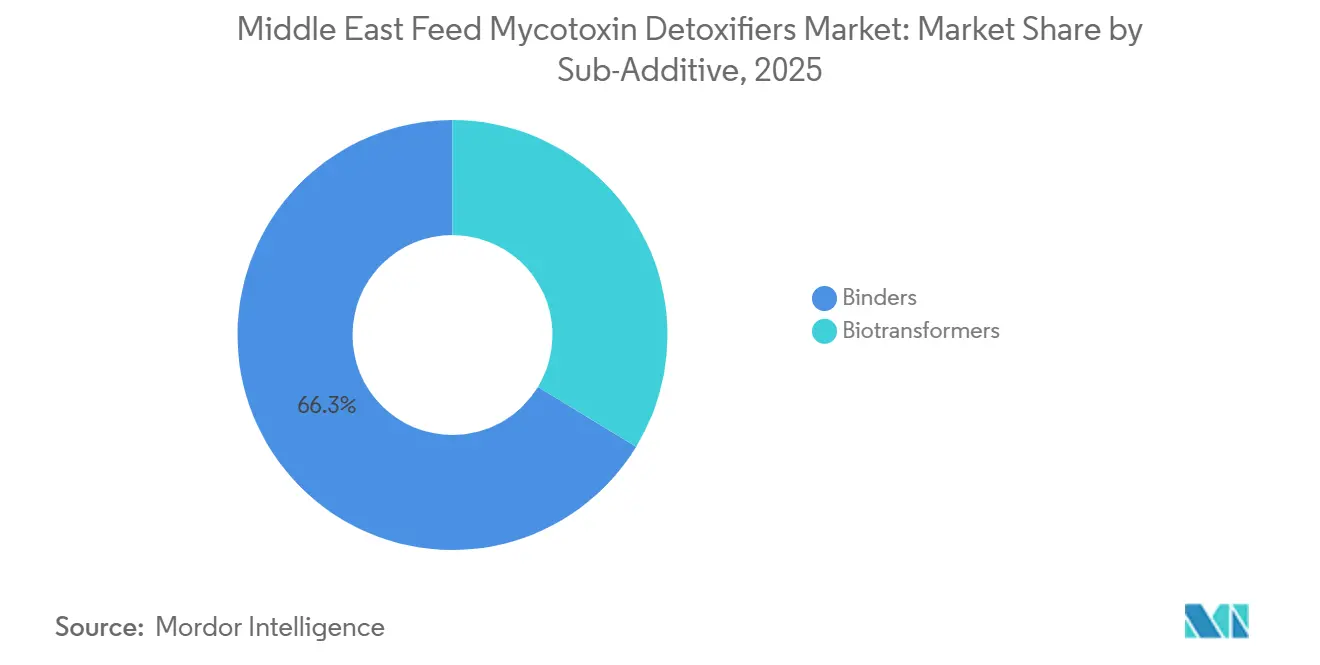

- By sub-additive, binders were the largest segment with 66.3% of the Middle East feed mycotoxin detoxifiers market share in 2025, while biotransformers were the fastest segment and are projected to grow at a 2.6% CAGR through 2031.

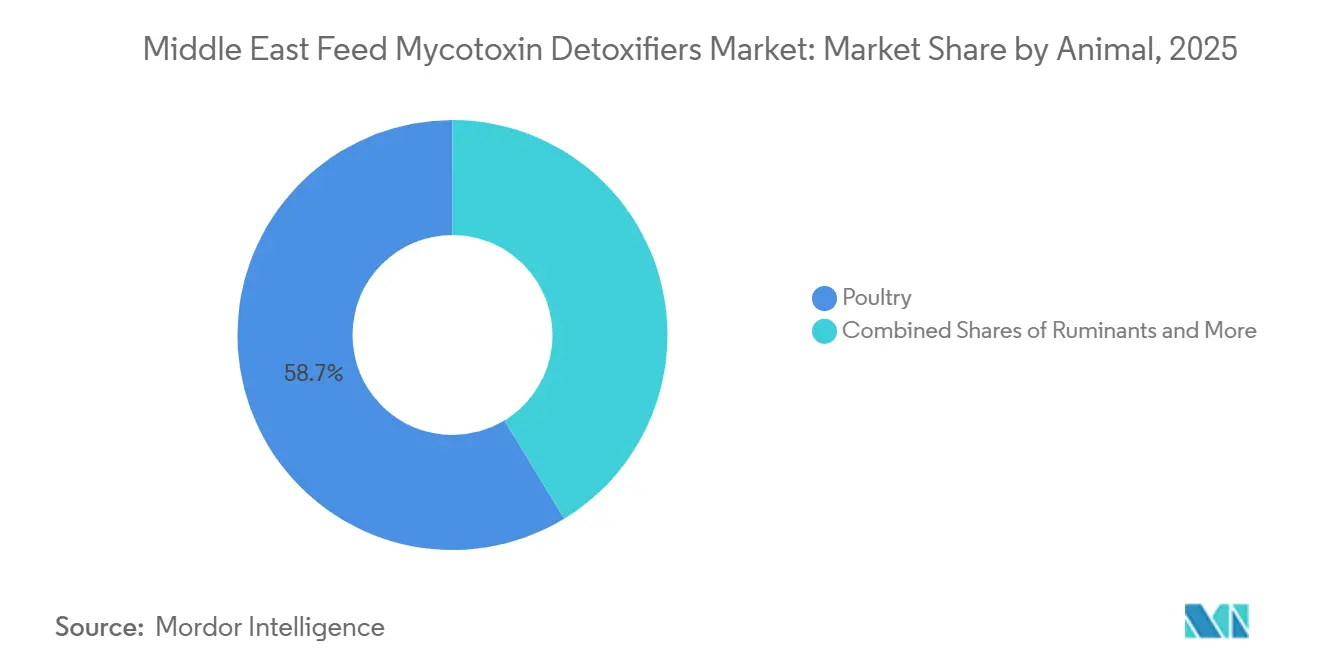

- By animal, poultry was the largest segment with 58.7% of the Middle East feed mycotoxin detoxifiers market share in 2025, and poultry is projected to remain the fastest-growing segment, expanding at a CAGR of 2.6% through 2031.

- By geography, Saudi Arabia accounted for 40.0% of the Middle East feed mycotoxin detoxifiers market share in 2025, while Iran was the fastest segment and is forecast to expand at a 2.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Feed Mycotoxin Detoxifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poultry and dairy intensification under extreme heat conditions | +0.7% | Saudi Arabia, United Arab Emirates, Oman, with spillover into Iran and Jordan | Medium term (2-4 years) |

| Hot-climate and import-driven mycotoxin exposure risk in feed supply chains | +0.6% | Regional, with the strongest effect in Saudi Arabia and Iran | Short term (≤ 2 years) |

| Stronger feed safety and residue oversight across GCC markets | +0.4% | Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Oman, Qatar, with limited spillover into Iran | Medium term (2-4 years) |

| Expansion of industrial feed milling and commercial livestock farming | +0.6% | Saudi Arabia, Iran, and the rest of the Middle East | Medium term (2-4 years) |

| Multi-mycotoxin contamination requiring broader-spectrum solutions | +0.4% | Regional, with heightened relevance in imported feed systems | Short term (≤ 2 years) |

| Use of alternative feed ingredients raising contamination risks | +0.3% | Saudi Arabia and Iran first, then wider regional adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Poultry and Dairy Intensification Under Extreme Heat Conditions

Poultry and dairy expansion is creating a steady volume base for the Middle East feed mycotoxin detoxifiers market, as high-output farms cannot absorb repeated disruptions to feed quality without measurable losses. Saudi Arabia's food security agenda continues to drive increased local poultry production. Corn usage in feed has reached a range from 4.6 to 4.9 million metric tons in the marketing year 2025/26, compared to 4.7 million metric tons in 2024/25, reflecting the rapid growth in ration demand within the kingdom[1]Source: USDA Foreign Agricultural Service, “Grain and Feed Annual, Saudi Arabia,” USDA Foreign Agricultural Service, apps.fas.usda.gov. In hot environments, grain and finished feed face a shorter safe storage window, so larger poultry and dairy operators are more willing to include detoxifiers on a preventive basis rather than wait for visible production losses. Dairy also introduces residue risk, as aflatoxin B1 in feed can be converted to aflatoxin M1 in milk, underscoring the importance of risk management. Formal testing in organized dairy chains is becoming more common. The commercial logic is stronger in vertically integrated systems, where a single contamination event can simultaneously affect feed conversion, flock health, milk quality, and the branded product's reputation. That dynamic gives the Middle East feed mycotoxin detoxifiers market a demand base that is tied not only to contamination levels but also to the operating model of modern livestock production.

Hot-Climate and Import-Driven Mycotoxin Risk in Feed Supply Chains

The Middle East mycotoxin detoxifiers market also benefits from the region’s structural dependence on imported feed materials, as contamination burdens are shaped by long transit times, repeated handling, and warm storage conditions after arrival. A January 2025 study in Toxins examined 100 poultry feedstuff samples from Riyadh, Al-Hassa, Qassim, and Jeddah and found multi-mycotoxin contamination in every sample, with aflatoxins detected in 84% and fumonisins in 56%[2]Source: Layla A. Al-Saad et al., “Detection of Mycotoxins and Aflatoxigenic Fungi Associated with Compound Poultry Feedstuffs in Saudi Arabia,” Toxins, mdpi.com. The same study reported that Aspergillus flavus was the dominant aflatoxigenic species isolated, underscoring the importance of storage conditions and handling practices, not just contamination at origin. This matters because commercial feed lots increasingly exhibit multiple toxin classes simultaneously, which undermines the usefulness of narrow, single-target solutions. As a result, buyers in the Middle East feed mycotoxin detoxifiers market are gradually moving from event-based purchases toward more routine inclusion programs for finished feed, especially in poultry-heavy systems. The shift is important because it turns detoxifier demand into a recurring operating cost instead of an occasional corrective response.

Stronger Feed Safety and Residue Oversight Across GCC Markets

More formal feed oversight across GCC markets is raising the commercial value of compliant, registered products in the Middle East feed mycotoxin detoxifiers market. Regional standard-setting activity in 2025 moved contaminants and toxins in food and feed into a more unified framework, which supports a clearer compliance environment for cross-border feed and additive trade. In Saudi Arabia, the Saudi Food and Drug Authority requires feed factories and warehouses to meet defined technical requirements, and feed products must pass a more structured registration path before entering the market. That process favors suppliers that can provide dossiers, technical validation, product consistency, and on-ground support to mills that need reliable documentation. The benefit is not limited to premium pricing, as formal oversight also helps larger buyers avoid the operational uncertainty that often accompanies low-cost generic alternatives. Over time, this shifts more value in the Middle East feed mycotoxin detoxifiers market toward suppliers that combine product efficacy with regulatory support and risk interpretation.

Expansion of Industrial Feed Milling and Commercial Livestock Farming

The rise of industrial feed milling remains one of the clearest structural supports for the Middle East feed mycotoxin detoxifiers market because large mills tend to apply detoxification products as part of standard process control. Commercial mills usually operate with tighter quality parameters, broader raw material intake, and stronger customer accountability than farm-level mixers, so they are more likely to include binders or biotransformers on a routine basis. This is especially relevant in Saudi Arabia, where poultry and dairy expansion is increasing the role of integrated feed manufacturing in the national protein supply chain. As plant scale increases, the cost of a single contaminated batch also rises, strengthening the economic case for preventive inclusion even when feed budgets are under pressure. Larger mills also tend to use more diverse raw materials, which increases the likelihood of co-contamination and heightens interest in products that can serve beyond aflatoxin control. In practical terms, every step toward industrial feed formalization expands the stable customer base for the Middle East feed mycotoxin detoxifiers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity and preference for untreated or locally sourced feed | -0.5% | Iran, rural Saudi Arabia, and smaller operators across the rest of the Middle East | Medium term (2-4 years) |

| Limited diagnostic and formulation availability in smaller markets | -0.4% | Yemen, Iraq, Oman, and smaller Iranian mills | Long term (≥ 4 years) |

| Efficacy variability under complex toxin co-contamination profiles | -0.4% | Regional, especially where multiple toxin classes occur together | Medium term (2-4 years) |

| Red Sea and Gulf shipping disruptions affecting additive supply chains | -0.3% | Saudi Arabia, United Arab Emirates, Kuwait, and Iran | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity and Preference for Untreated or Locally Sourced Feed

Price sensitivity is the primary commercial restraint in the Middle East feed mycotoxin detoxifiers market, as smaller livestock operators often view detoxifiers as non-essential. This challenge is particularly evident in Iran and among smaller-scale operations across the region, where purchasing decisions prioritize immediate feed costs over the potential to prevent downstream losses. In areas with limited rapid testing, contamination is frequently identified only after signs of reduced animal performance emerge. Even then, the issue is often attributed to other nutritional or management factors, delaying the adoption of detoxifiers. The lack of regular diagnostics and comprehensive recordkeeping makes it difficult to demonstrate the economic benefits of preventive detoxification. This creates a gap between biological risks and the commercial adoption of detoxifiers, slowing market growth beyond what contamination prevalence would suggest. Without improved testing access or more consistent regulatory enforcement, low-cost, untreated feed will continue to limit market penetration.

Red Sea and Gulf Shipping Disruptions Affecting Additive Supply Chains

Shipping disruptions across the Red Sea and Gulf corridors continue to weigh on the Middle East feed mycotoxin detoxifiers market because many higher-value additives reach the region through Europe-Asia trade routes. World Bank documentation showed that Suez Canal traffic had fallen sharply by the end of 2024, forcing rerouting around the Cape of Good Hope and adding 10 to 14 transit days plus container surcharges of as much as USD 2,100 on affected routes[3]Source: World Bank, “The Red Sea Crisis, Trade and Ecological Impacts,” World Bank, documents1.worldbank.org. For import-dependent distributors, that means higher freight costs, longer replenishment cycles, and a greater need for working capital to hold safety stock. The impact is stronger for enzyme-based products and specialized formulations that are not easily sourced from regional suppliers. At the same time, the same delays can worsen exposure in imported corn and soy cargoes held longer in warm environments, so disruption lifts both the urgency for detoxification and the cost of supplying it. This creates an uneven market in which larger suppliers are better positioned to absorb shocks, while smaller players struggle to protect margins and maintain availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Binders Lead the Market but Biotransformers Gain on Broader Risk Coverage

Binders accounted for 66.3% of the Middle East feed mycotoxin detoxifiers market share in 2025, making them the largest sub-additive segment across poultry, dairy, and ruminant feed programs. This dominance reflects a long-standing preference for clay-based solutions, which are familiar to formulators, cost-effective, and easy to incorporate into feed without significant process modifications. In many commercial systems, binders serve as the primary defense mechanism, as aflatoxin control remains a critical economic and regulatory priority. This is particularly significant in countries where buyers require low-cost solutions that can be applied across large feed volumes with minimal technical complexity. Consequently, the Middle East feed mycotoxin detoxifiers market continues to rely heavily on mineral adsorbents as the foundational approach for routine mycotoxin management.

The Middle East feed mycotoxin detoxifiers market size for biotransformers is projected to grow at a 2.6% CAGR through 2031, making them the fastest-growing sub-additive segment despite starting from a smaller base. This growth is driven by the region’s diverse contamination profile, as binders are less effective against certain Fusarium-derived toxins compared to enzymatic or biological degradation methods. A 2024 survey by DSM-Firmenich AG of finished feed in Turkey and the Middle East revealed fumonisins in 93% of sampled lots and zearalenone in 83%, highlighting the need for solutions beyond mineral adsorption. As multi-toxin exposure becomes a common challenge in commercial feed procurement, nutrition teams are increasingly adopting hybrid and multi-mechanism programs. While binders are expected to remain relevant, the growth of the Middle East feed mycotoxin detoxifiers market is increasingly influenced by products capable of addressing a broader toxin spectrum with enhanced technical precision.

By Animal: Poultry Remains the Largest User While Aquaculture Builds Strategic Relevance

Poultry accounted for 58.7% of the Middle East feed mycotoxin detoxifiers market in 2025, making it the largest animal segment and the main volume anchor for product demand. The region’s broiler, layer, and breeder systems operate with high feed throughput and narrow performance tolerances, so even subclinical contamination can carry visible economic consequences. Research published in the Journal of Applied Poultry Research in August 2025 showed that exposure of poultry to multiple mycotoxins can impair gut integrity, worsen feed conversion, and increase disease susceptibility, even when contamination remains below classic tolerance thresholds. That matters in fast-cycle broiler systems, where a short decline in intake or conversion can quickly affect profitability. Poultry is also the fastest-growing animal segment, with a 2.6% CAGR through 2031, keeping it central to the commercial outlook for the Middle East feed mycotoxin detoxifiers market.

The Middle East feed mycotoxin detoxifiers market size for aquaculture remains smaller than for poultry and ruminants, but the segment is gaining importance because plant-based aquafeed formulations introduce their own contamination pathways. Ruminants continue to provide stable demand, especially where dairy systems need reliable aflatoxin management to protect milk quality under formal residue oversight. Swine and other animals remain minor contributors due to the limited commercial swine base in the region, particularly in the GCC. However, a key takeaway for the Middle East feed mycotoxin industry is that demand is no longer restricted to poultry. An increasing number of feed categories now rely on imported or concentrated plant ingredients, which often have complex toxin profiles.

Geography Analysis

In 2025, Saudi Arabia accounted for 40% of the Middle East feed mycotoxin detoxifiers market share, making it the largest country segment by a significant margin. This position is attributed to its well-structured poultry and dairy industries, substantial dependence on imported feed materials, and a progressively formalized feed system in terms of regulation and procurement. The Saudi Food and Drug Authority has enhanced technical requirements for feed factories and warehouses, emphasizing the need for registered, documented additive products within the commercial supply chain. This combination of volume growth, reliance on imports, and stricter regulatory oversight positions Saudi Arabia as a key player in the Middle East feed mycotoxin detoxifiers market.

Iran is the fastest-growing country segment in the Middle East feed mycotoxin detoxifiers market, with a projected CAGR of 2.8% through 2031. Despite having one of the largest poultry production bases in the region, the penetration of detoxifiers in Iran remains below its risk profile due to factors such as currency pressures, import restrictions, and uneven commercial infrastructure. This gap is significant, as a substantial portion of the Iranian feed system operates under economic constraints, leading buyers to be cautious about investing in preventive additives, even when contamination risks are high. However, these conditions also present potential opportunities, as even small improvements in formal feed practices could generate new demand across the extensive production base. Iran exemplifies a market with significant growth potential through improved diagnostics, enhanced technical sales, and broader access to compliant formulations.

The rest of the Middle East segment includes the United Arab Emirates, Kuwait, Qatar, Bahrain, Oman, Jordan, Iraq, and Yemen, with demand conditions varying significantly across these countries. The United Arab Emirates and Oman benefit from more integrated poultry and aquaculture systems, whereas Iraq and Yemen face challenges such as reliance on imports, fragmented purchasing practices, and limited testing capacity. According to Cargill, Incorporated’s 2025 Global Mycotoxin Report, published in March 2026, zearalenone levels remained consistently high across feed markets in the Middle East and Africa. This is particularly relevant for operators utilizing corn-based ingredients and distillers' dried grains with solubles in several Gulf markets. As newer commercial livestock investments expand beyond Saudi Arabia, these countries are expected to adopt more structured procurement practices rather than relying on ad hoc spot purchases. Consequently, while the Middle East feed mycotoxin detoxifiers market remains concentrated in a few key countries, regional growth is gradually extending to additional markets.

Competitive Landscape

The Middle East feed mycotoxin detoxifiers market is moderately concentrated at the higher end, with key players such as DSM-Firmenich AG, BASF SE, Alltech, Inc., Kemin Industries, Inc., and Cargill, Incorporated maintaining strong positions in 2025. These companies leverage technical services, data access, and a diverse range of registered products to sustain their market presence. Their competitive advantage extends beyond pricing, focusing on integrating risk surveillance, application support, and product validation. This approach aligns with the growing demand from large feed mills and integrated poultry groups, which are increasingly reluctant to rely on unsupported efficacy claims, especially when contamination involves multiple toxin classes. Consequently, the competitive focus in the Middle East feed mycotoxin detoxifiers market is shifting toward suppliers offering feed risk management as a service rather than solely as a packaged additive.

Recent strategic initiatives by leading companies highlight the evolving competitive landscape. In March 2026, Cargill, Incorporated released its 2025 Global Mycotoxin Report, linking the dataset to its Notox product positioning and emphasizing a data-driven approach to technical selling. In August 2025, DSM-Firmenich AG inaugurated a new plant in Jadcherla, India, featuring a dedicated production line for mycotoxin risk management products, designed to enhance supply reliability for Middle East customers. Additionally, in Q1 2026, Archer Daniels Midland Company and Alltech, Inc. launched their North American feed joint venture, combining large-scale manufacturing and distribution capabilities with specialized mycotoxin management expertise. These developments underscore the increasing importance of scale, technical expertise, and supply chain control as competitive differentiators, surpassing the significance of mere product variety.

The lower-price segment of the Middle East feed mycotoxin detoxifiers market remains fragmented. Regional distributors and generic mineral binder suppliers continue to exert pricing pressure, particularly in markets with constrained feed budgets and limited testing capabilities. This dynamic prevents premium brands from dominating the entire market, even as they lead in the performance-driven segment. Opportunities still exist in underpenetrated areas such as aquaculture feed, Iran’s commercial feed base, and combination products targeting broad co-contaminants rather than individual toxins. As a result, the competitive landscape remains balanced, with clear leaders in the premium and service-oriented segment, while local and regional competition ensures significant buyer bargaining power across the market.

Middle East Feed Mycotoxin Detoxifiers Industry Leaders

DSM-Firmenich AG

Kemin Industries, Inc.

Alltech, Inc.

Cargill, Incorporated

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cargill, Incorporated, published its 2025 Global Mycotoxin Report, based on 389,926 analyses across 41 countries, identifying persistent multi-mycotoxin pressure and confirming that ZEN remained consistently elevated in Middle East and Africa feed markets. The report reinforces Cargill, Incorporated's positioning as a data-led mycotoxin risk management partner, supporting its Notox brand refresh and its technical engagement with GCC and Iranian feed producers.

- February 2026: Archer Daniels Midland Company and Alltech, Inc. have officially launched an animal feed joint venture. This collaboration integrates Archer Daniels Midland Company's manufacturing and distribution capabilities with Alltech, Inc.'s expertise in mycotoxin management and animal nutrition. By combining extensive experience in feed production and mycotoxin risk management, the venture aims to expedite the deployment of mycotoxin solutions through shared commercial channels.

- November 2025: BASF SE and Biochem have entered into a binding agreement under which Biochem will acquire BASF SE's global glycinate business. The transaction is anticipated to close in the first quarter of 2026. This agreement aligns with BASF SE's ongoing efforts to optimize its portfolio in the specialty animal nutrition segment, as the company shifts its focus to core, high-margin product lines. This development is projected to have implications for the Middle East Feed Mycotoxin Detoxifiers Market.

Middle East Feed Mycotoxin Detoxifiers Market Report Scope

Feed mycotoxin detoxifiers are specialized additives mixed into animal feed to neutralize harmful fungal toxins. They work by trapping the toxins in the digestive tract (binding) or by breaking them down into harmless compounds (biotransformation), ensuring livestock remain healthy and productive.

The Middle East feed mycotoxin detoxifiers market report is segmented by sub-additive (binders and biotransformers), by animal (aquaculture, poultry, ruminants, swine, and other animals), and by geography (Saudi Arabia, Iran, and the rest of the Middle East). The market forecasts are provided in value (USD) and volume (metric tons).

| Binders |

| Biotransformers |

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

| Saudi Arabia |

| Iran |

| Rest of Middle East |

| Sub Additive | Binders | ||

| Biotransformers | |||

| Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| Country | Saudi Arabia | ||

| Iran | |||

| Rest of Middle East | |||

Key Questions Answered in the Report

What is the current value of the Middle East feed mycotoxin detoxifiers market in 2026?

The Middle East feed mycotoxin detoxifiers market stands at USD 60.62 million in 2026 and is forecast to reach USD 68.75 million by 2031, with growth supported by imported feed exposure and tighter feed quality controls.

Which sub-additive category leads demand in this region?

Binders remain the largest sub-additive segment, holding 66.3% share in 2025, because they are familiar to feed formulators, cost-effective, and easy to apply in large-volume feed systems.

Why is poultry the main end-use area for mycotoxin detoxifiers in the Middle East?

Poultry held 58.7% share in 2025 because broiler and layer systems operate with high feed throughput and narrow performance tolerances, making contamination control more commercially important.

Which country offers the strongest growth outlook through 2031?

Iran is the fastest-growing country segment with a projected 2.8% CAGR through 2031, supported by a large poultry base and room for deeper adoption as feed practices become more formal.

What is the biggest risk factor supporting detoxifier demand across regional feed supply chains?

The main demand trigger is the combination of import dependence, hot storage conditions, and frequent multi-toxin contamination in feed materials and finished feed lots, especially in poultry-oriented systems.

Page last updated on: