Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

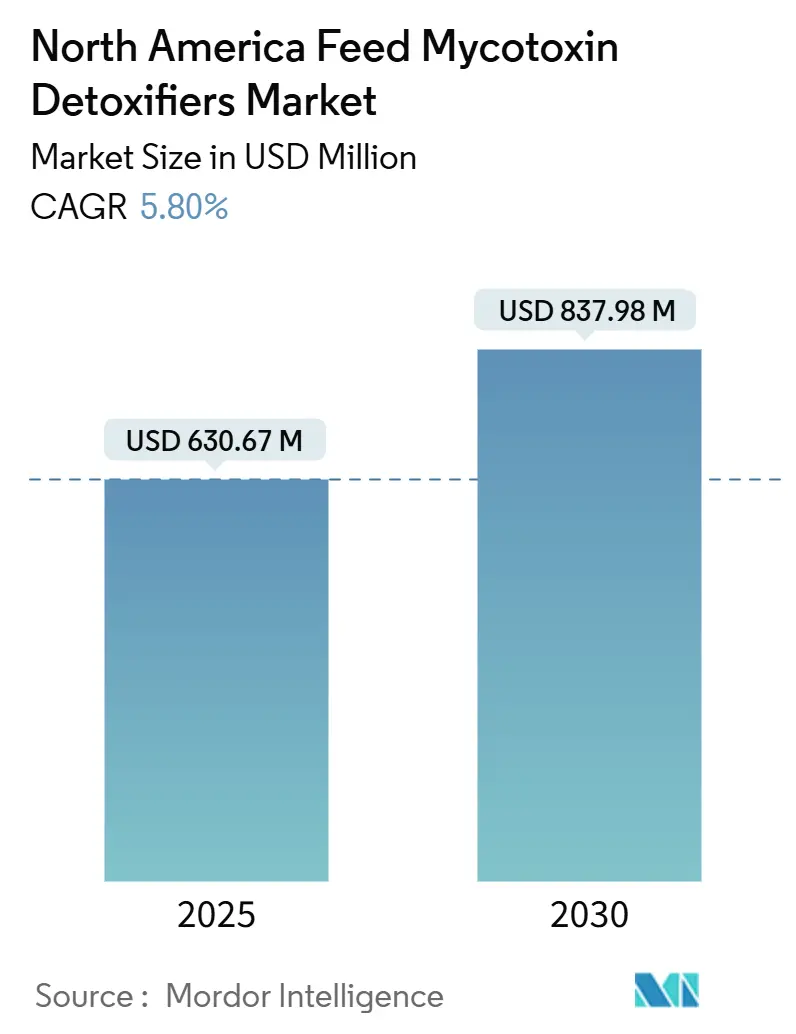

| Market Size (2025) | USD 630.67 Million |

| Market Size (2030) | USD 837.98 Million |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Feed Mycotoxin Detoxifiers Market Analysis by Mordor Intelligence

The North America Feed Mycotoxin Detoxifiers market size stands at USD 630.67 million in 2025 and is forecast to reach USD 837.98 million by 2030, advancing at a 5.8% CAGR through the period. This growth outlook reflects intensifying multi-mycotoxin pressure, stricter Food and Drug Administration (FDA) limits for aflatoxin M1 in milk, and livestock producers’ pivot toward antibiotic-free programs. The expansion reflects the region's escalating battle against climate-amplified mycotoxin contamination, where warmer and wetter harvest seasons are heightening simultaneous aflatoxin-fumonisin outbreaks across primary corn-producing states[1]Source: David Hennessy, “Climate Change Prompts Rise in Toxic Corn Fungus,” Iowa State University Department of Economics, econ.iastate.edu. Expanded vertical integration among United States poultry and dairy integrators accelerates product uptake, while artificial-intelligence (AI) sensors enable precision dosing that improves cost efficiency. On the supply side, fragmented competition allows innovative biotransformer suppliers to gain visibility despite raw-material price swings. Overall, climate amplification of fungal risks, combined with data-driven feed safety management, underpins a robust demand trajectory for the region’s detoxifier suppliers.

Key Report Takeaways

- By Sub Additive, the Binders held 68.4% of the North America Feed Mycotoxin Detoxifiers market share in 2024; biotransformers are poised to grow at a 6.0% CAGR to 2030.

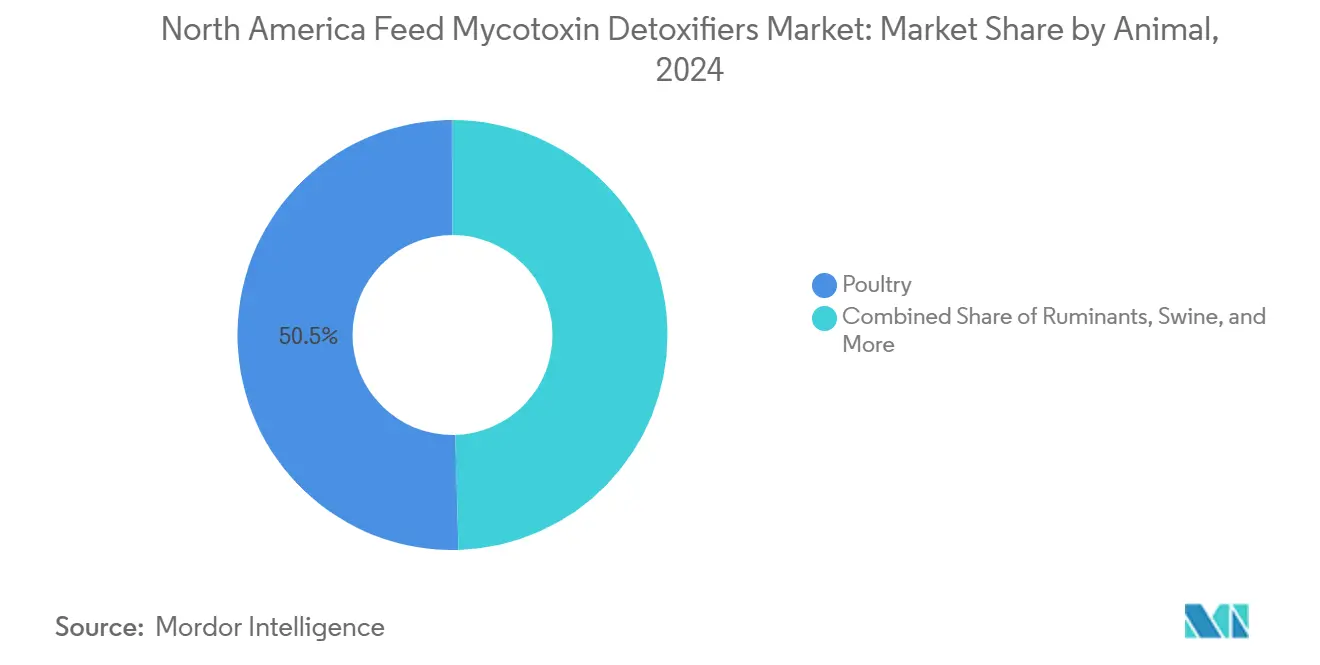

- By Animal, Poultry accounted for a 50.5% share of the North America Feed Mycotoxin Detoxifiers market size in 2024, while ruminants are set to expand at a 5.9% CAGR through 2030.

- By Geography, the United States captured 70.6% of regional revenue in 2024 and is projected to advance at a 7.5% CAGR over the forecast horizon.

North America Feed Mycotoxin Detoxifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-Driven Spike In Multi-Mycotoxin Co-Contamination | +1.8% | United States Corn Belt; Eastern Canada | Long term (≥ 4 years) |

| FDA Enforcement Of 0.5 Ppb AFM1 In Milk Driving On-Farm Detoxifier Uptake | +1.2% | United States dairy basins; Canada | Medium term (2-4 years) |

| Shift To Antibiotic-Free Livestock Increasing Reliance On Detoxifiers | +1.0% | North America; Mexico emerging | Medium term (2-4 years) |

| Rising Adoption Of AI-Based Feed-Safety Sensors Enabling Dynamic Dosing | +0.8% | United States; Canada | Short term (≤ 2 years) |

| Expansion Of United States Poultry Integrators Vertical Feed Mills | +0.6% | United States Southeast; Arkansas | Medium term (2-4 years) |

| Growth In Premium Clean-Label Meat And Dairy Channels | +0.4% | United States; Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Driven Spike In Multi-Mycotoxin Co-Contamination

Rising temperatures and erratic rainfall extend the geographic reach of Aspergillus and Fusarium fungi, pushing simultaneous aflatoxin–fumonisin outbreaks deeper into the Corn Belt. Michigan State University modeling predicts materially higher aflatoxin risk for United States maize between 2031 and 2040. Alltech’s 2024 harvest survey showed the average number of mycotoxins per corn-silage sample climbing to 8.3 from 5.3 year-earlier levels. Escalating co-occurrence forces feed mills to deploy broad-spectrum solutions that adsorb aflatoxins while enzymatically degrading Fusarium metabolites. Because climate is a structural rather than cyclical variable, demand for North America Feed Mycotoxin Detoxifiers market offerings remains resilient over the long term.

FDA Enforcement Of 0.5 Ppb AFM1 In Milk Driving On-Farm Detoxifier Uptake

The Food and Drug Administration's (FDA) rigorous enforcement of aflatoxin M1 limits at 0.5 ppb in milk is compelling dairy operations to implement preventive mycotoxin management rather than reactive contamination response[2]Source: U.S. Food and Drug Administration, “Aflatoxins, Total,” FDA Chemical Contaminants Transparency Tool, fda.gov. With aflatoxin carryover rates of 1-3% from feed to milk and detection occurring within hours of ingestion, dairy producers face immediate supply chain disruption when contaminated feed enters rations. The FDA's updated Mycotoxins in Domestic and Imported Foods Compliance Program now employs multi-mycotoxin analytical methods, expanding monitoring beyond aflatoxins to include T-2/HT-2 toxins and zearalenone. This regulatory intensification is driving proactive adoption of clay-based binders in dairy rations, with inclusion rates of 20-100 grams per head per day becoming standard practice in high-risk regions.

Shift To Antibiotic-Free Livestock Increasing Reliance On Detoxifiers

The shift toward "No Antibiotics Ever" production systems has changed livestock health management approaches, with mycotoxin detoxifiers becoming essential for maintaining animal health without antibiotics. Following the European Union's 2006 ban on antibiotic growth promoters, mycotoxin management became crucial as animals no longer had pharmaceutical protection against gut health issues and weakened immune systems, while studies show that mycotoxin exposure decreases vaccine effectiveness and makes animals more vulnerable to infections. Consumer demand for antibiotic-free meat and dairy products has expanded from premium to mainstream markets, creating a divided market where producers need advanced detoxification methods and bioprotection compounds, representing a lasting transformation driven by consumer preferences and regulations that discourage routine antibiotic use.

Rising Adoption Of AI-Based Feed-Safety Sensors Enabling Dynamic Dosing

AI-powered mycotoxin detection systems enhance feed safety management through real-time contamination assessment and precise detoxifier application. ImagoAI's Galaxy Mycotoxins Test received AOAC Performance Tested Methods certification for detecting four major mycotoxins in wheat, DDGS, and Corn Gluten Meal within 30 seconds, reducing testing time by 95% compared to traditional methods. Electronic nose technology integrated with machine learning algorithms has shown 90.1% accuracy in classifying zearalenone contamination in pet food samples, enabling non-invasive screening across various feed materials. The technology implementation is primarily in the United States and Canada, where feed operations possess the necessary capital infrastructure and technical expertise for AI-enhanced quality control systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pending Generally Recognized As Safe (GRAS) Approvals Slowing New Product Launches | -0.9% | United States regulatory bottleneck | Medium term (2-4 years) |

| Volatility in Bentonite and Zeolite Mining Costs | -0.7% | North America and Mexico supply chains | Short term (≤ 2 years) |

| Variable Field Efficacy Across Diverse Feed Matrices | -0.5% | Global; smallholder operations | Long term (≥ 4 years) |

| Price-Sensitivity Among Small and Mid-Size Producers | -0.4% | United States; Canada; Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pending Generally Recognized As Safe (GRAS) Approvals Slowing New Product Launches

The United States regulatory framework for mycotoxin detoxifiers faces challenges through the Generally Recognized As Safe (GRAS) approval process, with the Department of Health and Human Services directing the FDA to examine rulemaking that may eliminate GRAS self-determination. The FDA's Center for Veterinary Medicine requires extensive safety and efficacy data for mycotoxin binders, with food additive petitions requiring approximately 9 technical sections and review cycles lasting up to 180 days each. The FDA's position that no feed additives have received specific approval for mycotoxin binding has led suppliers to market products as anti-caking or free-flow agents instead of making direct detoxification claims. While the Animal Feed Ingredient Consultation (AFIC) program offers an alternative pathway, its temporary nature and the European Union's requirement for three independent in vivo studies create barriers for companies developing enzymatic and microbial detoxification technologies.

Volatility in Bentonite and Zeolite Mining Costs

The North American mycotoxin binder market faces cost pressures due to raw material price variations, with industrial-grade bentonite ranging from USD 80-120 per metric ton and feed-grade material costing USD 200-350 per metric ton. China's 35% share in global montmorillonite production presents supply chain risks for North American feed additive manufacturers dependent on clay mineral imports. Mining companies incur substantial environmental compliance expenses related to open-pit extraction, water-intensive purification, and calcination processes requiring temperatures of 400-700°C for activated products. The cost structure is influenced by transportation expenses and specific material requirements, particularly affecting small-scale feed mills and producers who cannot secure favorable long-term supply agreements.[3]Source: ScienceDirect, “Bentonite – an Overview,” sciencedirect.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Biotransformers Gain Ground Against Binders Dominance

Binders controlled 68.4% of the North America Feed Mycotoxin Detoxifiers market in 2024, as aluminum-silicate clays remain the default defense against aflatoxins and ergot alkaloids. The biotransformers are registering a 6.0% CAGR to 2030, supported by European Union authorizations that validate enzymatic degradation of fumonisins and zearalenone. Hybrid products such as DSM-Firmenich’s Mycofix Select 5.0 integrate adsorption, biotransformation, and bioprotection, steering procurement managers toward multi-modal formulations.

As climate change shifts contamination toward Fusarium metabolites that resist clay adsorption, demand for enzymatic solutions escalates. Competitive differentiation now centers on proprietary gene-edited enzymes like FUMzyme, which hydrolyzes fumonisins within the animal’s upper gastrointestinal tract. This technology advantage, combined with digital risk-monitoring apps, allows biotransformer suppliers to displace traditional clay volumes in integrated feed operations.

By Animal: Ruminant Applications Accelerate Despite Poultry Dominance

Poultry retained 50.5% of the North America Feed Mycotoxin Detoxifiers market size in 2024, reflecting the sector’s scale and mycotoxin sensitivity. Modern broiler genetics exhibit reduced gut barrier tolerance, making detoxifiers a standard part of premixes. Ruminants are expanding at a 5.9% CAGR, as high-energy total mixed rations shorten rumen retention time and diminish microbial detoxification, increasing systemic toxin load.

Dairy producers face direct economic penalties because aflatoxins transfer to milk at documented rates, compelling year-round binder inclusion. Research showing zearalenone conversion to more estrogenic α-zearalenol in the rumen further underscores the need for enzymatic solutions. Swine and aquaculture remain important but smaller revenue contributors, with emerging opportunities in premium companion-animal diets.

Geography Analysis

The United States holds 70.6% of the North America feed mycotoxin detoxifiers market in 2024 and maintains regional growth at 7.5% CAGR through 2030. This growth stems from climate-induced mycotoxin migration northward into the Corn Belt and stricter regulatory enforcement of contamination limits. The United States' market dominance reflects its status as the world's largest corn producer, requiring comprehensive mycotoxin management across integrated livestock operations. Regional contamination patterns show significant variation, with the Eastern Corn Belt recording mold counts averaging 450,000 colony-forming units per gram and frequent samples exceeding 1,000,000 CFU/g, while the Upper Midwest maintains contamination levels below 100,000 CFU/g. The FDA's enforcement of 0.5 ppb aflatoxin M1 limits in milk and 20 ppb aflatoxin thresholds in dairy cattle feed creates strict compliance requirements that make detoxifier adoption necessary.

Canada maintains its position as the second-largest national market, with growth driven by dairy operations expansion in Ontario and Quebec provinces and beef cattle production in Alberta and Saskatchewan. The country's regulations align with United States standards, enabling consistent mycotoxin management requirements and efficient technology transfer across borders. Canadian feed mills utilize their proximity to United States grain supplies while operating under the Canadian Food Inspection Agency's oversight, which implements mycotoxin limits similar to FDA standards.

Mexico represents the smallest but significant market, where livestock intensification and feed quality improvements increase mycotoxin management adoption beyond traditional farming operations. The country's tropical and subtropical climate creates constant aflatoxin pressure in local and imported feed ingredients, requiring continuous detoxification protocols. The United States-Mexico-Canada Agreement supports technology transfer and product distribution, allowing North American suppliers to benefit from integrated regional markets.

Competitive Landscape

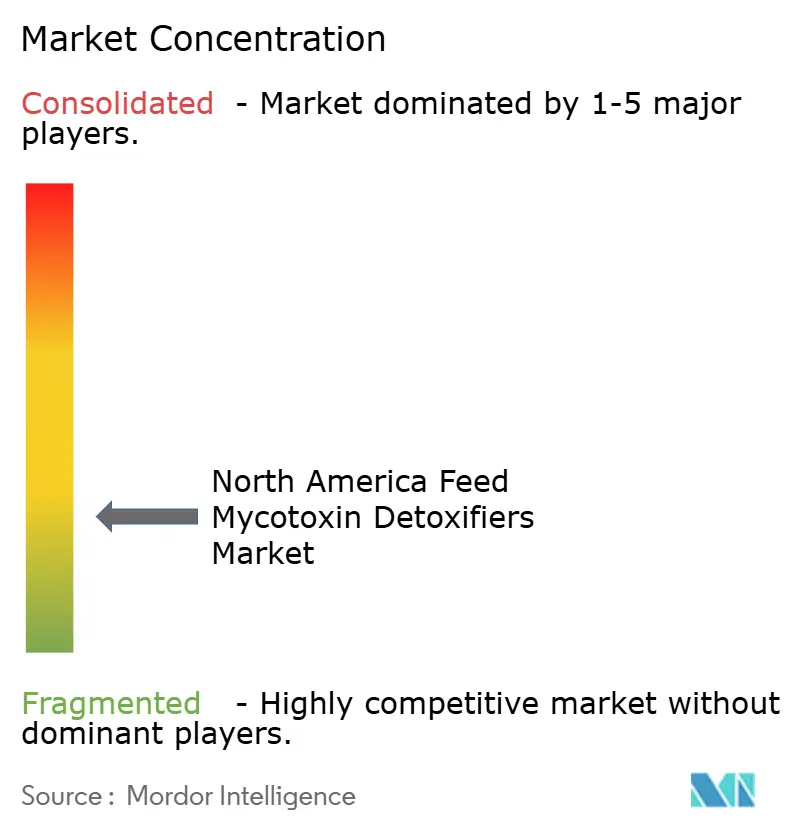

The North America feed mycotoxin detoxifiers market exhibits fragmented competition, with the market leaders collectively holding a significant market share, creating opportunities for technological differentiation and specialized positioning strategies. DSM-Firmenich maintains market leadership through its Mycofix portfolio, supported by 7 European Union authorizations for mycotoxin deactivation. Brenntag SE has established a strong presence through its distribution network and supply chain integration across North American feed markets. Companies that combine biotransformation technologies with data-driven services gain competitive advantages, as demonstrated by Adisseo's collaboration with Syngenta to develop predictive mycotoxin models, achieving 93% accuracy for deoxynivalenol contamination.

The market demonstrates significant growth potential through product innovation and strategic partnerships. Companies are investing in research and development to enhance detoxifier efficacy and develop novel application methods. The integration of digital technologies enables real-time monitoring and adjustment of detoxification processes, improving overall feed safety management. Market players are also expanding their distribution networks and technical support services to strengthen their competitive positions.

New market entrants are developing advanced materials science and biotechnology solutions to compete with traditional clay-based products. Magnetic nanocomposites demonstrate over 99% aflatoxin removal and 69% deoxynivalenol reduction in feed matrices while offering magnetic recovery capabilities. The FDA's Generally Recognized As Safe (GRAS) approval process requires extensive safety and efficacy data, creating market entry barriers. The potential elimination of GRAS self-determination may further consolidate regulatory pathways. Companies like DSM-Firmenich gain competitive advantages through integrated service offerings, including mycotoxin prediction services, analytical testing, and risk management applications. The market's fragmented structure indicates potential for consolidation as smaller companies seek economies of scale and larger firms pursue technological capabilities through acquisitions.

North America Feed Mycotoxin Detoxifiers Industry Leaders

Alltech, Inc.

Brenntag SE

Adisseo France S.A.S

DSM-Firmenich

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Alltech has launched Mycosorb A+ Evo and Mycosorb Evo, expanding its Mycosorb® range of mycotoxin management solutions. These products aim to protect livestock health and performance against multi-mycotoxin threats. The Mycosorb Evo range offers mycotoxin-binding capabilities and broad-spectrum coverage. The products provide protection against toxins including deoxynivalenol (DON), fusaric acid (FA), and Penicillium-derived toxins, as well as other common mycotoxins found in livestock feed.

- March 2025: ImagoAI's Galaxy Mycotoxins Test achieved Association of Official Analytical Chemists (AOAC) Performance Tested Methods certification for detecting aflatoxins, deoxynivalenol, fumonisins, and zearalenone in wheat, Dried Distillers Grains with Solubles, and Corn Gluten Meal, expanding beyond its original corn certification.

- February 2025: DSM-Firmenich launched its Mycotoxin Risk Management App for iOS and Android platforms, providing real-time regional contamination data, species-specific risk indicators, and mycotoxicosis troubleshooting guides linked to the company's World Mycotoxin Survey database.

North America Feed Mycotoxin Detoxifiers Market Report Scope

The North America Feed Mycotoxin Detoxifiers Market Report is Segmented by Sub Additive (Binders, Biotransformers), Animal (Aquaculture, Poultry, Ruminants, Swine, Other Animals), and Geography (Canada, Mexico, United States, Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume.

Sub Additive

| Binders |

| Biotransformers |

Animal

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| fish | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

Geography

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Sub Additive | Binders | ||

| Biotransformers | |||

| Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| fish | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| Geography | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms