Middle East and Africa Feed Antioxidants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

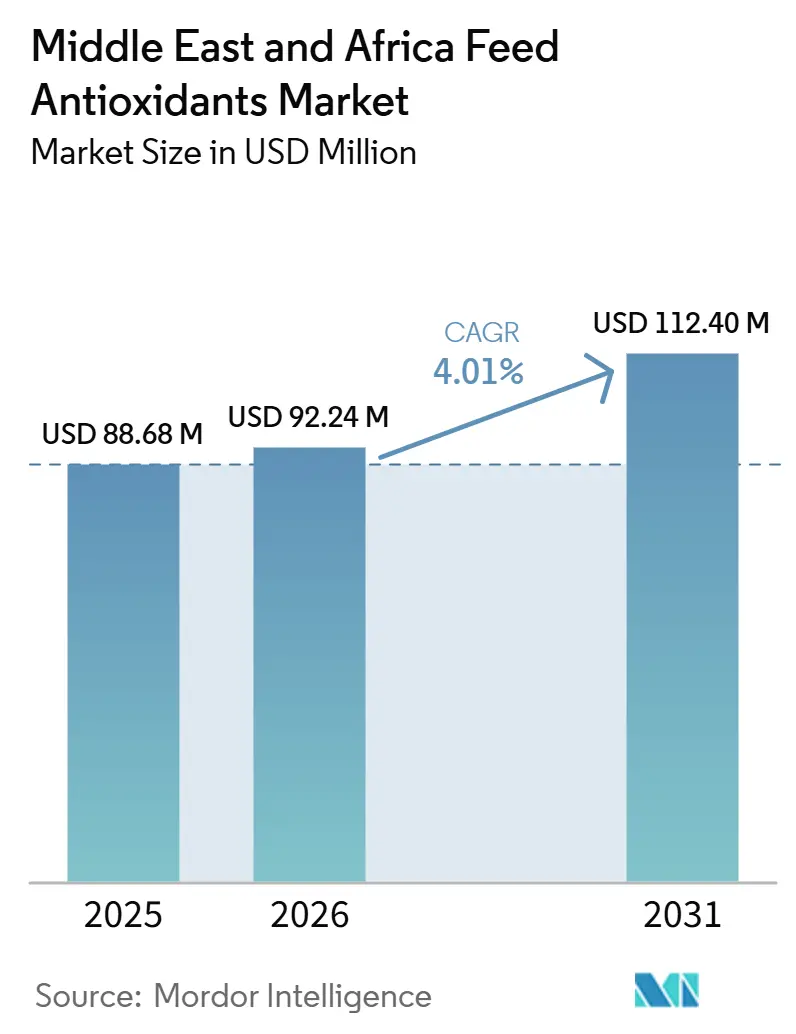

| Base Year Market Size (2025) | USD 88.68 Million |

| Market Size (2026) | USD 92.24 Million |

| Market Size (2031) | USD 112.40 Million |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Africa |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Feed Antioxidants Market Analysis by Mordor Intelligence

The Middle East and Africa feed antioxidants market size is projected to grow from USD 88.68 million in 2025 and USD 92.24 million in 2026 to USD 112.40 million by 2031, registering a CAGR of 4.01% between 2026 and 2031. The market is advancing as commercial feed demand continues to rise in poultry, aquaculture, and organized livestock systems, while hot storage and transport conditions make oxidation control essential. The region's reliance on imported feed ingredients increases transit time and storage exposure, supporting steady antioxidant inclusion across commercial feed formulations. The market is also shaped by a divide between cost-focused buyers that prefer synthetic products and larger integrators that require standardized additive programs with tighter quality control. Mycotoxin pressure in compound feed is expanding the role of antioxidants beyond basic shelf-life protection, as mills increasingly need consistent feed quality under harsher operating conditions. The result is a market where volume growth remains steady, product choice stays highly price sensitive, and suppliers that combine product performance with technical support hold a clearer advantage.

Key Report Takeaways

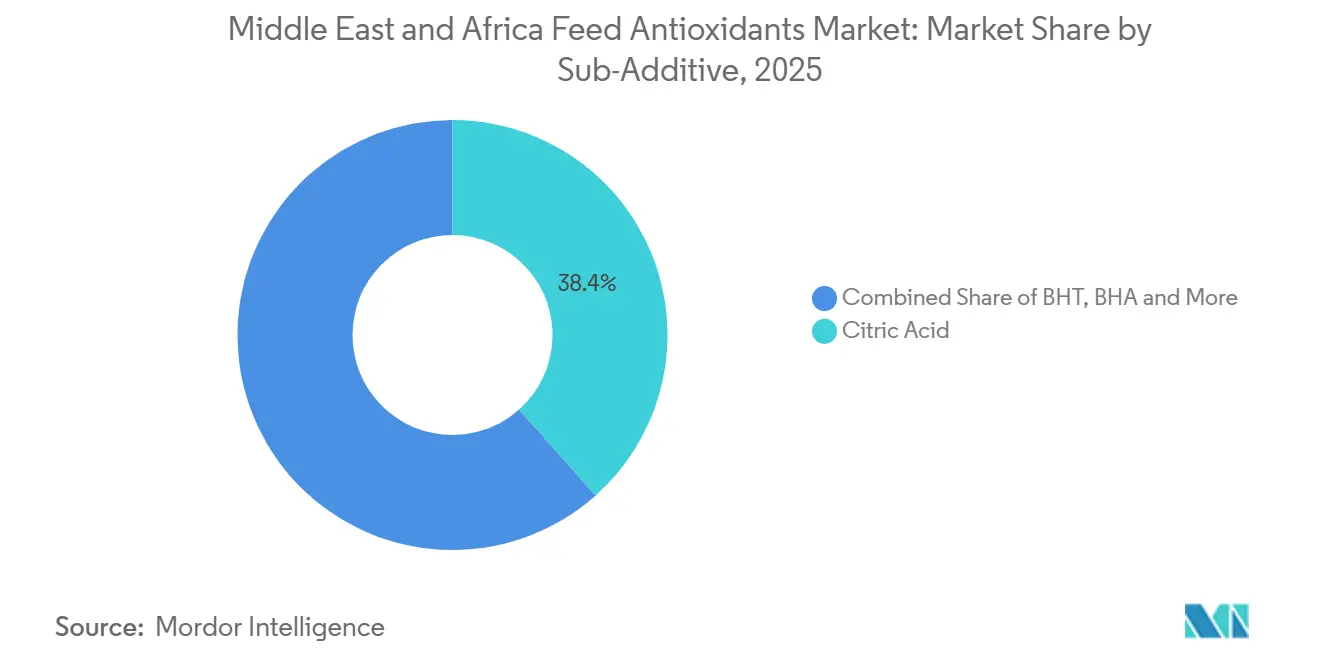

- By sub-additive, citric acid is the largest segment, accounting for 38.4% of the market share in 2025, while tocopherols are the fastest-growing segment and are anticipated to expand at a 4.1% CAGR between 2026 and 2031.

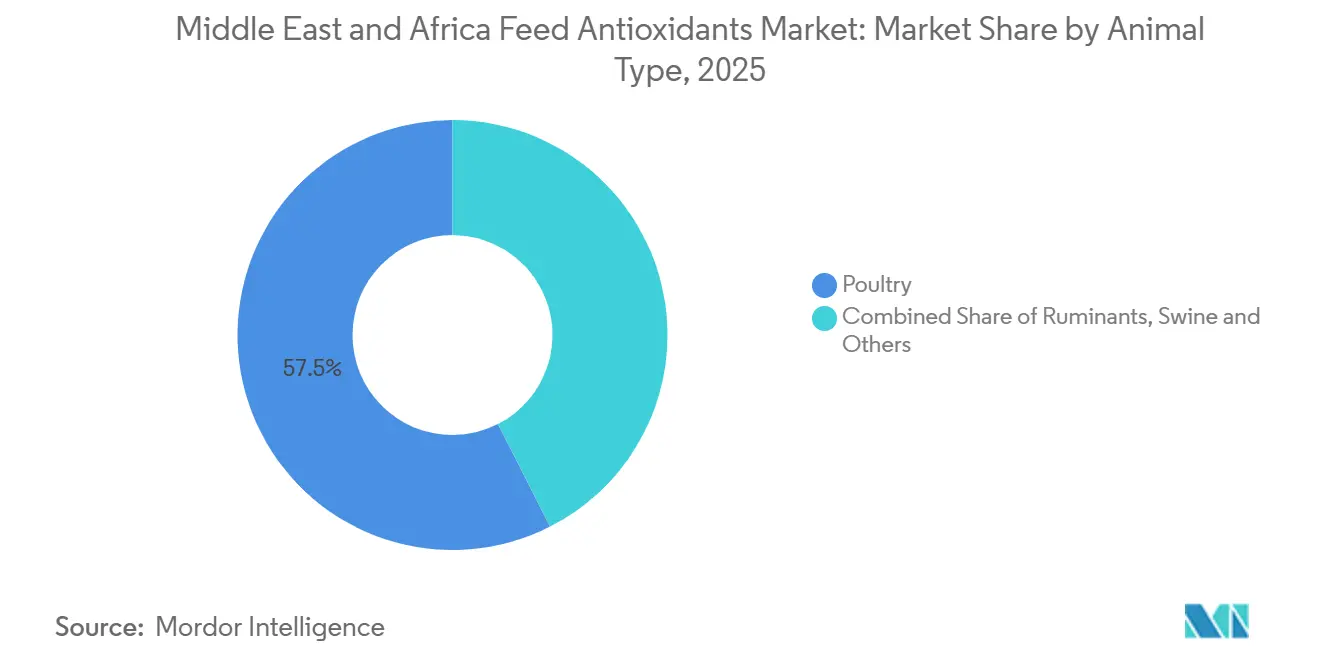

- By animal, poultry is the largest segment and held 57.5% of the market share in 2025, while swine is the fastest-growing segment and is projected to grow at an 4.3% CAGR between 2026 and 2031.

- By geography, Africa is the largest segment, accounting for 63.0% of the market share in 2025, and it is also the fastest-growing segment, anticipated to expand at a 3.9% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Feed Antioxidants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising commercial poultry and broiler output | +0.9% | Middle East and Africa core, Saudi Arabia, Egypt, UAE | Short term (≤ 2 years) |

| Feed shelf-life pressure in hot storage and transport conditions | +1.0% | Pan-regional, most acute in the Middle East and North Africa | Short term (≤ 2 years) |

| Shift toward high-performance synthetic antioxidants in cost-sensitive feed mills | +0.7% | North Africa and sub-Saharan Africa | Medium term (2-4 years) |

| Expanding feed premix standardization among large integrators | +0.7% | Saudi Arabia, UAE, Egypt | Medium term (2-4 years) |

| Mycotoxin risk management increasing oxidation control in compound feed | +0.6% | Middle East and Africa, Egypt, Nigeria, Kenya core | Medium term (2-4 years) |

| Export-oriented meat supply chains raising feed quality requirements | +0.5% | South Africa, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Commercial Poultry and Broiler Output

According to the Ministry of Statistics data, Saudi Arabia produced 1.3 million metric tons of broiler meat in 2024, reflecting the country's large commercial poultry sector and substantial feed consumption requirements[1]Source: General Authority for Statistics, “The Ministry of Statistics: Broiler chicken production in the Kingdom will increase to 1.3 million tons during 2024” stats.gov.sa. USDA report said Egypt remained a major poultry producer, with nearly 1.99 billion birds processed and poultry meat output of approximately 2.5 million metric tons in 2024[2]Source: Foreign Agricultural Services, “FAIRS Country Report Annual” fas.usda.gov. These production systems require large feed batches, tighter inventory management, and greater finished-feed stability, which keeps antioxidant use closely tied to commercial scale. The Middle East and Africa feed antioxidants market benefits from this pattern, as organized poultry growth generates consistent additive demand rather than sporadic purchasing. Government-backed food security programs further support this demand, since feed consumption rises in line with supported production targets rather than short-term retail demand alone. As poultry systems become more intensive, the need to protect feed fats during storage and transportation will continue to support the Middle East and Africa feed antioxidants market.

Feed Shelf-Life Pressure in Hot Storage and Transport Conditions

High ambient temperatures across the region increase the risk of lipid oxidation in fat-containing feed ingredients, particularly when feed moves through open yards, ports, and non-climate-controlled storage facilities. This operating environment makes oxidation control a standard formulation requirement for commercial mills, especially in the Gulf and North Africa. The problem is more pronounced when feed relies on imported grains, oils, and protein meals that spend extended periods in transit before milling. These physical constraints are difficult to address through handling changes alone, providing consistent support for the Middle East and Africa feed antioxidants market. Mills that reduce antioxidant use still face the commercial costs of rancidity, reduced feed quality, and shorter storage windows. As a result, climate and logistics conditions continue to sustain a steady base of demand across the Middle East and Africa feed antioxidants market.

Shift Toward High-Performance Synthetic Antioxidants in Cost-Sensitive Feed Mills

Synthetic antioxidants remain dominant because many feed mills in the region purchase additives primarily based on delivered cost per ton of feed. BHA, BHT, and ethoxyquin continue to meet this requirement due to their ease of dosing and long-established performance records in commercial feed applications. The Middle East and Africa feed antioxidants market continues to favor these products, as a large portion of buyers operate within narrow formulation budgets with limited capacity for input experimentation. This preference is reinforced in fragmented African milling systems, where procurement teams tend to favor reliable compounds that can be adopted without specialized technical support. Ethoxyquin also retains relevance in aquafeed applications, where oxidative pressure in fishmeal and high-fat formulations is more difficult to manage with lower-cost alternatives. Over time, differentiation in the Middle East and Africa feed antioxidants market is likely to depend less on core chemistry alone and more on supply reliability, dosing guidance, and premix integration.

Expanding Feed Premix Standardization Among Large Integrators

Larger poultry and aquaculture operators are shifting toward centralized purchasing and standardized feed specifications across their internal networks. This shift supports antioxidant inclusion through premix systems, where dosing is controlled more consistently than in decentralized farm-level procurement. Integrators typically seek fewer formulation changes, fewer quality failures, and clearer traceability across production sites, which benefits the Middle East and Africa feed antioxidants market. Standardization also favors suppliers that can support repeat formulations and technical audits, increasing the value of service alongside product supply. Export-facing operations have an additional reason to standardize, as consistent additive use strengthens feed quality documentation and product acceptance in customer markets. As integrator-led feed programs expand, a larger share of demand in the Middle East and Africa feed antioxidants market is likely to move through structured premix channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty around synthetic antioxidant usage | -0.4% | Global, with early compliance pressure in Saudi Arabia, UAE, Egypt | Medium term (2-4 years) |

| Price volatility in key feed additive inputs | -0.3% | Pan-regional | Short term (≤ 2 years) |

| Fragmented feed mill base limiting premium antioxidant penetration | -0.4% | Sub-Saharan Africa and Rest of Middle East | Long term (≥ 4 years) |

| Low technical awareness among smallholder feed users | -0.3% | Rest of Africa and Rest of Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty Around Synthetic Antioxidant Usage

The EU's denial of authorization for ethoxyquin has altered the broader regulatory context around feed antioxidant use, even though rules are not uniform across the Middle East and Africa region. Nigeria's regulatory directive banning ethoxyquin in 2025 in feed for food-producing animals adds market-specific compliance pressure. Morocco also formalized animal feed quality, safety, and labeling standards in 2024, indicating that feed additive governance is tightening in parts of the region. These changes do not remove synthetic antioxidants from the Middle East and Africa feed antioxidants market, but they do increase registration, reformulation, and portfolio planning costs for suppliers. Buyers serving export-linked channels may also respond ahead of regulatory changes, shifting demand away from some legacy products before local rules are updated. The restraint facing the Middle East and Africa feed antioxidants market therefore stems less from an immediate regional ban and more from uneven compliance risk across markets.

Price Volatility in Key Feed Additive Inputs

Many synthetic antioxidants are linked to petrochemical value chains, meaning their cost base can move with oil and benzene-related raw material prices. Natural antioxidant systems face a different risk, as their inputs depend on agricultural supply conditions and concentrated sourcing patterns. The Middle East and Africa feed antioxidants market is sensitive to both pressures, as end users typically resist additive price increases when feed margins are already under strain. During cost-stressed periods, mills can delay purchases, reduce dose rates, or switch to cheaper alternatives if their formulation flexibility allows. This makes pricing power difficult to sustain even when underlying feed production continues to expand. As a result, raw material volatility can slow revenue growth in the Middle East and Africa feed antioxidants market even when volume demand remains stable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Citric Acid held the largest Share While Tocopherols Record the Highest Growth Rate

Citric acid was the largest sub-additive in the market in 2025, with 38.4% share. Its position is attributed to its widespread use as a multifunctional additive that enhances antioxidant performance by chelating metal ions, improving feed stability, and extending shelf life across poultry, ruminant, aquaculture, and compound feed applications. Its broad compatibility with both synthetic and natural antioxidant systems, coupled with its cost-effectiveness and regulatory acceptance, has supported its extensive adoption across commercial feed manufacturing. BHA, BHT, and ethoxyquin continued to represent the major antioxidant segment, with BHT frequently used alongside BHA to improve oxidative stability while maintaining cost-efficient feed formulations. Ethoxyquin also remained important in preserving high-polyunsaturated fishmeal used in aquaculture feed, while other antioxidants, including TBHQ (tert-butylhydroquinone) and specialty blends, continued to serve niche formulation requirements.

Tocopherols were the fastest-growing sub-additive and are anticipated to expand at a 4.1% CAGR between 2026 and 2031. Growth is being supported by compliance-driven demand as export-oriented producers in South Africa and Egypt shift toward ethoxyquin-free formulations for European Union and premium GCC (Gulf Cooperation Council) channels. This shift is turning tocopherols from a premium choice into a more regular procurement requirement in some feed programs. Propyl gallate, supported by wider use in blended aquafeed formulations and improved availability from Asian suppliers. Research published in Animal Nutrition in 2025 further supported the case for tocopherols by demonstrating antioxidant, anti-inflammatory, and growth-related benefits beyond basic lipid preservation [3]Source: Review Article, “Biological functions and applications of rosemary extracts in animal production” sciencedirect.com.

By Animal: Poultry Commands Volume While Swine Advances Faster

Poultry was the largest market segment in 2025, with a 57.5% share. This position reflects the scale and intensity of broiler and layer farming across Saudi Arabia, the UAE, and Egypt, where hot storage conditions and rapid feed turnover make antioxidant use routine. Broilers remained the main volume base in the region. Saudi Arabia produced 1.3 million metric tons of broilers in 2024, while Egypt processed nearly 1.99 billion birds in the same year. These production systems are also supported by food security programs, which help sustain stable feed demand. Layer operations added another consistent source of antioxidant demand, particularly in Egypt and South Africa, while other poultry categories remained smaller but are becoming more structured as processing standards improve. Outside poultry, ruminants demand is shaped by beef feedlot expansion in South Africa and East Africa and by commercial dairy production in the Gulf. Aquaculture, with fish leading demand and shrimp requiring more specialized antioxidant support due to the sensitivity of high-PUFA diets.

Swine was the fastest-growing animal segment and is anticipated to expand at a 4.3% CAGR between 2026 and 2031. This growth is driven by the gradual formalization of commercial pork production in non-Muslim majority sub-Saharan African countries such as Ethiopia, Uganda, the Democratic Republic of the Congo, and other parts of East Africa. As urbanization broadens protein demand, more organized swine operations are adopting feed quality practices that many smallholder systems had previously not followed. The expansion of commercial swine feed milling in urban and peri-urban areas is also creating a more substantial antioxidant demand base than the region had a decade ago. Suppliers can support this category efficiently by extending the same distribution networks already used for poultry. Companies that build swine and aquaculture support on top of their poultry business are likely to capture a larger share of the region's growth.

Geography Analysis

Africa was the largest and fastest-growing geographic subregion in the market in 2025, accounting for 63.0% of total regional demand. The subregion is anticipated to expand at a 3.9% CAGR between 2026 and 2031, supported by the steady formalization of commercial feed milling, rising aquaculture investment, and improved logistics across major trade corridors. South Africa remains one of the region's most structured markets, with organized feed production, export-linked quality systems, and procurement practices that favor established antioxidant suppliers. Its beef exports rose 30% in 2024 to 38,657 metric tons, while the South African Certified Red Meat Scheme received ISO 9001 certification in 2025, both of which reinforce stricter feed quality expectations. Egypt also remains central to regional demand, as the continent's largest poultry producer with 2.5 million metric tons of output in 2024 and one of the fastest-expanding aquafeed markets, where domestic demand rose 36% in 2025. DSM-Firmenich AG's Sadat City facility, operational since September 2024 with 10,000 metric tons of annual capacity, further strengthened Egypt's position as a regional feed additive hub.

The Middle East, with Saudi Arabia remaining the dominant country market due to direct production subsidies and poultry self-sufficiency goals under Saudi Vision 2030. New capacity additions are reinforcing that demand base. Alwadi Poultry Farms' new 90-TPH (tons per hour) feed mill became operational in 2026, while Tanmiah Food Company's 100-farm expansion program is set to begin commercial production in January 2027. The UAE also plays an important role as a premium, import-dependent feed hub, where heat exposure and rapid distribution cycles increase antioxidant use across poultry and dairy feed. Across the rest of the Middle East, adoption is progressing more gradually as feed infrastructure develops at varying speeds.

The rest of Africa, including Nigeria, Kenya, Ethiopia, Tanzania, and other sub-Saharan markets, represents a high-potential but more complex growth area. Demand remains concentrated in formal urban feed mill clusters rather than smallholder systems, which keeps expansion uneven across markets. Nigeria's catfish sector is growing at 10% annually, while Kenya's expanding poultry and livestock feed sectors are generating new antioxidant demand. At the same time, price sensitivity continues to limit the uptake of premium formulations in many markets. Regulatory frameworks are also evolving, as demonstrated by Tanzania's 2025 standard for compounded poultry feed concentrates. Consolidation toward larger mills remains gradual, keeping this part of the region more of a volume growth opportunity than a premium value opportunity in the near term.

Competitive Landscape

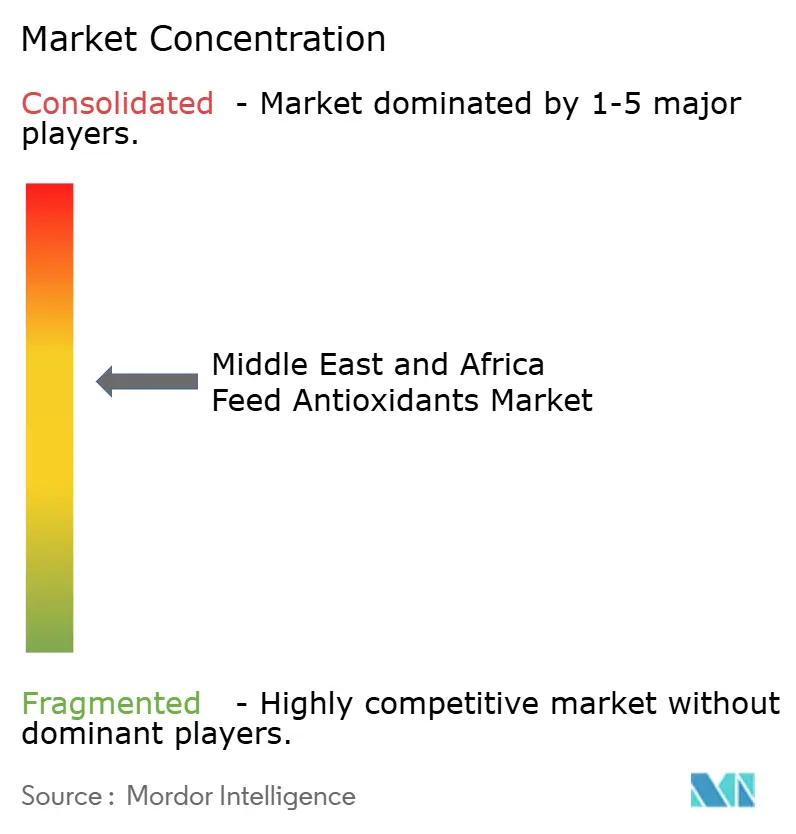

The Middle East and Africa feed antioxidants market remained moderately concentrated in 2025, with the top five companies accounting for a significant share of regional sales. Large multinational suppliers maintained their competitive advantage through established brands, broad product portfolios, technical expertise, and reliable distribution networks. However, the market remained competitive as regional suppliers and generic manufacturers continued to exert pricing pressure, particularly in conventional synthetic antioxidant categories. As a result, feed manufacturers retained multiple sourcing options, preventing excessive market concentration despite the scale advantages enjoyed by leading participants.

Leading companies continued to strengthen their competitive positions through portfolio optimization and supply chain investments. In November 2025, BASF and Biochem entered a binding agreement for Biochem's acquisition of BASF's global glycinate business, reflecting an increased focus on strategic portfolio specialization within animal nutrition. Although these investments occurred outside the region, they remain relevant to the Middle East and Africa feed antioxidants market, where import dependence makes supply continuity, technical support, and product availability key purchasing considerations for commercial feed manufacturers.

Competition is anticipated to remain active across both multinational and regional suppliers. While price competition is likely to remain strongest , smaller companies continue to differentiate themselves through natural antioxidant solutions, customized formulation support, and specialized technical services. Higher-value applications, particularly in aquaculture and premium livestock feed, provide greater opportunities for product differentiation as feed stability and oxidative protection become increasingly important. Consequently, the Middle East and Africa feed antioxidants market is anticipated to remain moderately concentrated over the forecast period, with established global suppliers leveraging scale and integrated supply networks while specialized companies expand through application expertise and customer-focused technical support.

Middle East and Africa Feed Antioxidants Industry Leaders

BASF SE

Kemin Industries, Inc.

Cargill, Incorporated

Alltech Inc.

Novus International, Inc. (Mitsui & Co., Ltd. and Nippon Soda Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Elsewedy Industrial Development and New Hope Egypt, part of China's New Hope Liuhe Group, signed a land agreement on March 12, 2026, to establish a new 400,000 metric ton annual capacity poultry and aquaculture feed manufacturing plant in 10th of Ramadan City, Egypt. The facility will be New Hope's fifth plant in Egypt, with approximately 50,000 metric tons of output designated for export, reinforcing Egypt's role as a regional feed hub and expanding the antioxidant-inclusive formulated feed volume in North Africa.

- February 2026: De Heus Animal Nutrition opened one of Africa's largest feed mills in Kenya with an initial production capacity of 240,000 metric tons per year. The expansion strengthens the company's position in the Middle East and Africa feed antioxidants market by increasing compound feed production, thereby supporting higher demand for feed antioxidants to enhance feed stability and shelf life.

- March 2026: Balady Poultry Company in Saudi Arabia commissioned a new feed mill developed with Famsun, comprising 3 production lines with a total capacity of 60 metric tons per hour, representing an investment of USD 7 million. The facility targets improved formulation control and reduced reliance on external feed suppliers, with financial impact anticipated from Q2 2026, expanding the commercially managed antioxidant demand base within Saudi Arabia's vertically integrated poultry sector.

Middle East and Africa Feed Antioxidants Market Report Scope

Feed antioxidants are substances used in animal feeds to increase the shelf life of feed by preventing undesirable oxidation in finished feeds and the guts of animals. They are known to keep the nutritional and energy value of the feed intact and also prevent rancid oxidation of fats.

The Middle East and Africa Feed Antioxidants Market is Segmented by Sub-Additives (BHA, BHT, Ethoxyquin, and More), by Animal Type (Ruminant, Poultry, Swine, and More), and by Geography (Saudi Arabia, United Arab Emirates). The Market Size and Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Butylated Hydroxyanisole (BHA) |

| Butylated Hydroxytoluene (BHT) |

| Citric Acid |

| Ethoxyquin |

| Propyl Gallate |

| Tocopherols |

| Other Antioxidants |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Swine | |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Other Animals |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Sub-Additive | Butylated Hydroxyanisole (BHA) | |

| Butylated Hydroxytoluene (BHT) | ||

| Citric Acid | ||

| Ethoxyquin | ||

| Propyl Gallate | ||

| Tocopherols | ||

| Other Antioxidants | ||

| By Animal | Ruminants | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Swine | ||

| Aquaculture | Fish | |

| Shrimp | ||

| Other Aquaculture Species | ||

| Other Animals | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa feed antioxidants market by 2031?

The Middle East and Africa feed antioxidants market is forecasted to reach USD 112.40 million by 2031, rising from USD 92.24 million in 2026 at a 4.01% CAGR

Why does poultry lead demand in the MEA feed antioxidants market?

Poultry leads demand because broiler and layer farming is highly commercialized across key countries such as Saudi Arabia, the UAE, and Egypt, where large feed volumes and hot storage conditions make antioxidant use essential.

What is the main factor supporting steady antioxidant use in feed?

Hot storage and transport conditions, along with long exposure times for imported feed ingredients, keep oxidation control necessary across commercial feed operations.

Why does Africa lead the MEA feed antioxidants market?

Africa leads because it has the largest demand base in the region, supported by expanding commercial feed milling, rising aquaculture activity, and improving logistics.

Page last updated on: