Africa Feed Mycotoxin Detoxifiers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

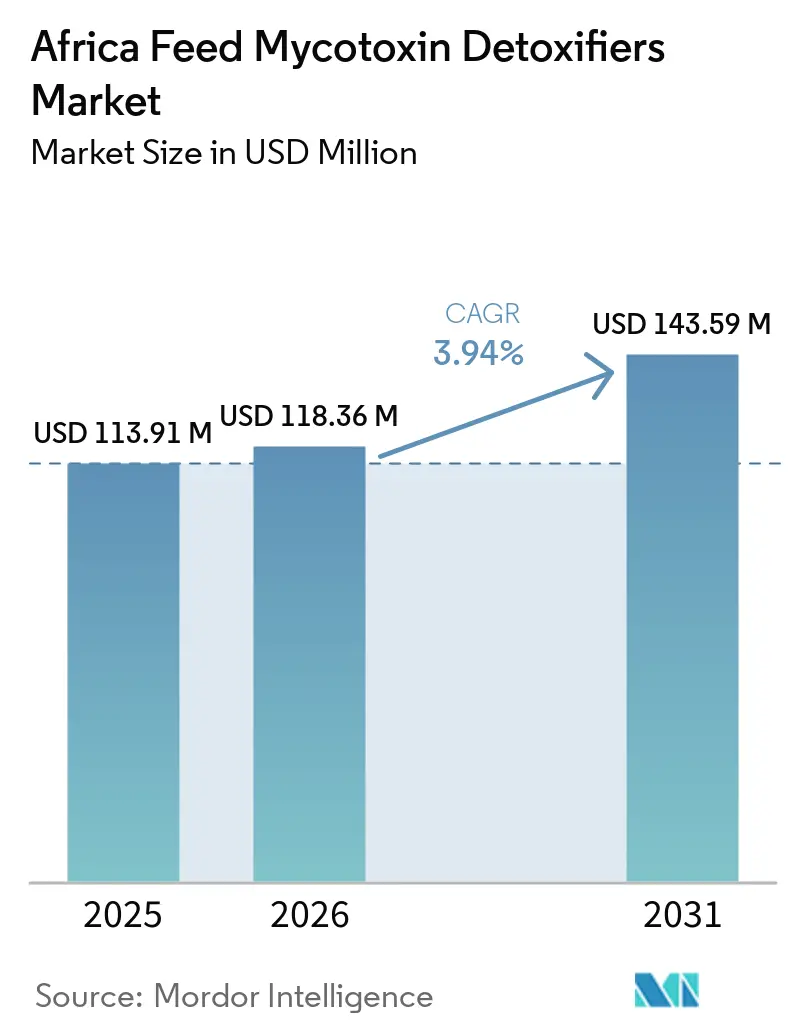

| Base Year Market Size (2025) | USD 113.91 Million |

| Market Size (2026) | USD 118.36 Million |

| Market Size (2031) | USD 143.59 Million |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

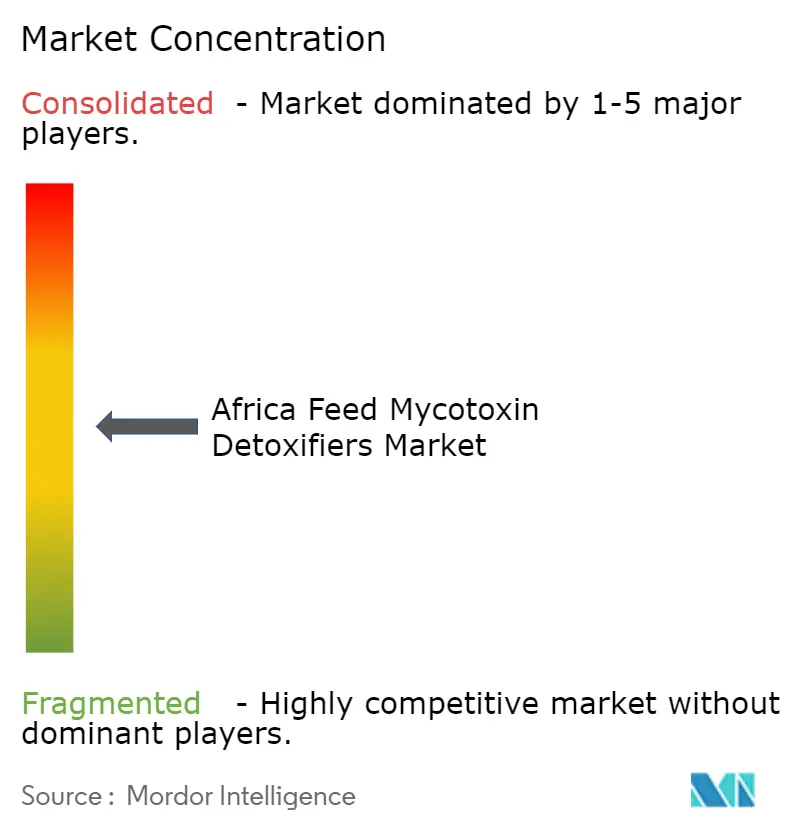

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Mycotoxin Detoxifiers Market Analysis by Mordor Intelligence

The Africa feed mycotoxin detoxifiers market was valued at USD 113.91 million in 2025 and is projected to grow from USD 118.36 million in 2026 to USD 143.59 million by 2031, registering a CAGR of 3.94% during the forecast period of 2026-2031. This growth is driven by the increasing focus on feed safety and livestock productivity across the region. Awareness of the negative impact of mycotoxin contamination on animal health, feed efficiency, and production performance is prompting feed manufacturers and livestock producers to adopt detoxification solutions. The warm and humid climatic conditions prevalent in many African countries heighten the risk of fungal growth and toxin formation in feed ingredients, emphasizing the need for effective toxin management strategies. Furthermore, the gradual modernization of commercial feed production, the adoption of quality assurance practices, and the strengthening of food and feed safety regulations are supporting market expansion. There is also a growing demand for advanced detoxification products that provide broader-spectrum protection and enhanced efficacy, as feed producers aim to maintain feed quality, ensure animal welfare, and comply with evolving industry standards.

Key Report Takeaways

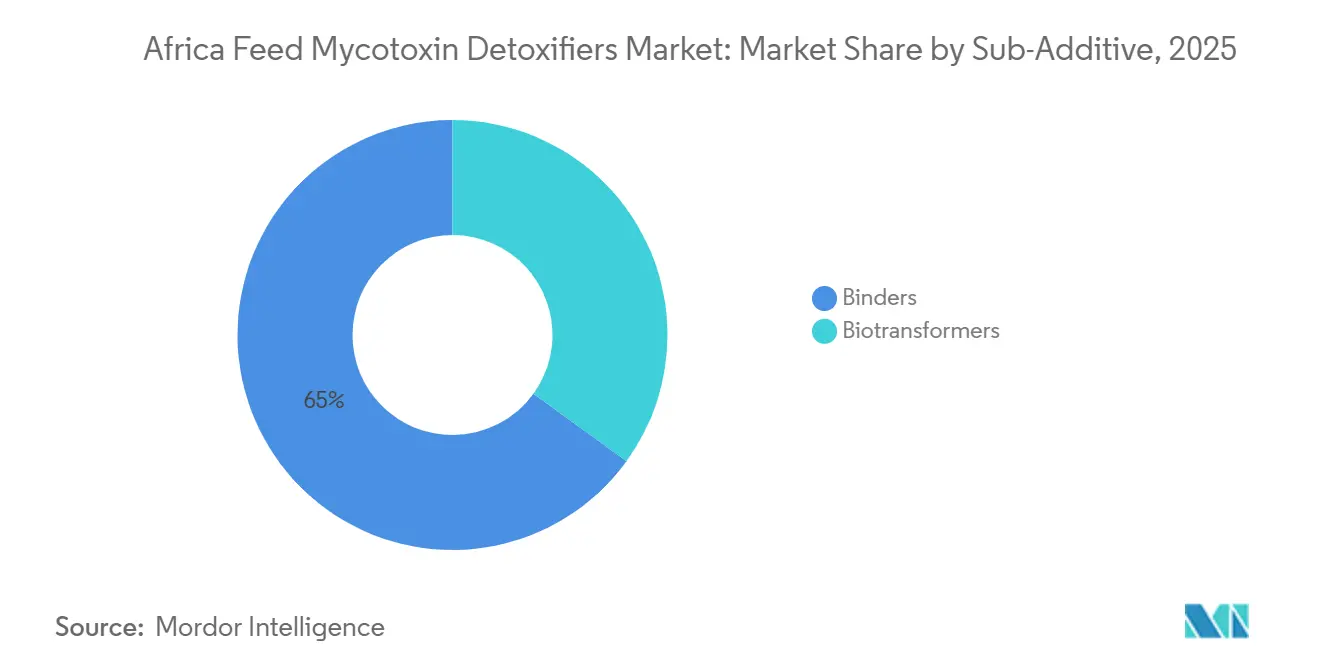

- By sub-additive, the Africa feed mycotoxin detoxifiers market share for binders accounted for the largest 65.0% in 2025, while the Africa feed mycotoxin detoxifiers market size for biotransformers is projected to record the fastest growth at 3.9% CAGR from 2026 to 2031.

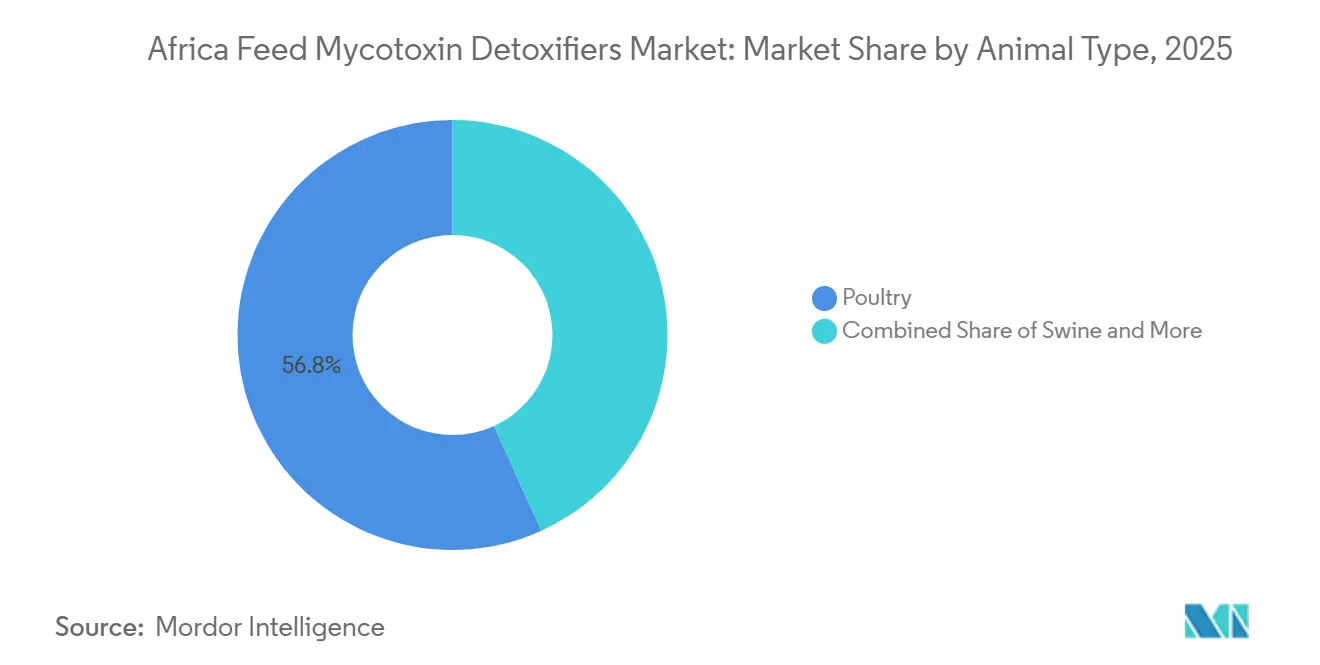

- By animal type, poultry held the largest 56.8% share in 2025, while swine is forecast to grow at the fastest CAGR of 4.7% from 2026 to 2031.

- By geography, South Africa captured the largest 48.4% share in 2025, and it is also projected to grow at the fastest CAGR of 4.6% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Mycotoxin Detoxifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High aflatoxin and fumonisin load in African feed grains | +1.2% | Sub-Saharan Africa, East Africa, and Egypt | Long term (≥ 4 years) |

| Expansion of commercial compound feed capacity | +0.8% | Uganda, Kenya, Côte d'Ivoire, Egypt, and Ghana | Short term (≤ 2 years) |

| Poultry sector intensification and food-safety scrutiny | +0.9% | South Africa, Egypt, and Nigeria | Medium term (2-4 years) |

| African Union and national aflatoxin control programs | +0.6% | Pan-African, with early gains in East Africa and West Africa | Long term (≥ 4 years) |

| Rapid uptake of low-infrastructure aflatoxin testing | +0.5% | Kenya, Nigeria, and Ghana | Short term (≤ 2 years) |

| Rising use of variable by-products and distressed grains in feed | +0.7% | Egypt, West Africa, and Southern Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Aflatoxin and Fumonisin Load in African Feed Grains

The Africa feed mycotoxin detoxifiers market is driven by the ongoing risk of mycotoxin contamination in feed grains, particularly in maize-based feed systems, which are predominant in livestock production across the region. The DSM-Firmenich World Mycotoxin Survey (January–December 2025) identified Sub-Saharan Africa as an extreme-risk region for mycotoxin contamination, with aflatoxins and fumonisins being the primary toxins impacting feed safety[1]Source: DSM-Firmenich Animal Nutrition & Health, “dsm-firmenich World Mycotoxin Survey: January–December 2025,” dsm-firmenich.com.. The survey also noted that mycotoxin contamination often occurs as co-contamination rather than isolated toxin events, complicating feed quality management for commercial feed manufacturers and livestock producers. This contamination pattern is increasing the demand for advanced mycotoxin detoxifiers capable of addressing multiple toxins simultaneously, thereby supporting animal health, productivity, and feed safety standards in the African feed industry.

Expansion of Commercial Compound Feed Capacity

The Africa feed mycotoxin detoxifiers market is experiencing growth due to the rapid expansion of formal compound feed manufacturing in the region. According to the Alltech Agri-Food Outlook 2025, Africa produced 64.2 million metric tons of compound feed in 2025, marking an 11.5% increase from 2024[2]Source: Alltech, “Alltech Agri-Food Outlook 2025,” alltech.com.. This growth positioned Africa as the fastest-growing feed-producing region globally for the second consecutive year. As feed production becomes more commercialized, manufacturers are prioritizing feed quality, consistency, and risk management. Larger feed mills, which procure grain in bulk and adhere to stricter quality assurance standards, are driving the demand for mycotoxin detoxifiers to address contamination risks and ensure optimal animal performance. As a result, the continued growth of industrial feed production is sustaining the demand for mycotoxin management solutions in the African feed market.

Poultry Sector Intensification and Food-Safety Scrutiny

The Africa feed mycotoxin detoxifiers market is driven by the ongoing growth of commercial poultry production, which is a significant consumer of compound feed in the region. According to the Alltech Agri-Food Outlook, in 2025, Egypt's broiler feed production grew by 21.9% comapred to 2024, highlighting the rapid expansion of organized poultry operations and the increased use of professionally manufactured feed. With poultry producers facing stricter performance and food safety standards, ensuring feed quality has become a priority. This has led to rising demand for mycotoxin detoxifiers, which help mitigate contamination risks, promote animal health, and support consistent production outcomes in commercial poultry systems.

African Union and National Aflatoxin Control Programs

The Africa feed mycotoxin detoxifiers market is experiencing growth due to the development of a more robust regulatory framework for food and feed safety across the continent. In February 2025, the African Union Assembly adopted the Statute of the Africa Food Safety Agency (AFSA), creating a continental body to enhance food safety coordination, regulatory harmonization, and alignment with international standards among member states. As regulatory oversight becomes more organized, commercial feed manufacturers are likely to focus more on preventive feed safety measures, including mycotoxin risk management. This regulatory progression is driving the integration of mycotoxin detoxifiers into standardized feed quality assurance programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus low-cost clay alternatives | -0.4% | Pan-African, with the strongest effect in West Africa and East Africa smallholder markets | Medium term (2-4 years) |

| Low awareness among smallholders and on-farm mixers | -0.2% | Sub-Saharan Africa outside the South Africa formal sector | Long term (≥ 4 years) |

| Sparse in-country efficacy validation for local toxin profiles | -0.1% | West Africa and East Africa outside Kenya | Medium term (2-4 years) |

| Fragmented enforcement outside formal feed channels | -0.1% | Nigeria, Tanzania, and much of Rest of Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Low-Cost Clay Alternatives

The market is constrained by the relatively high cost of advanced detoxification solutions compared to conventional clay-based binders. Cost-sensitive livestock producers and feed mixers, particularly in informal and small-scale production systems, often prioritize affordability when choosing feed additives. This issue was highlighted in a November 2024 mission by the ECOWAS Regional Agency for Agriculture and Food (RAAF/ARAA), which identified the high cost of reagents for rapid aflatoxin tests as a significant challenge to feed safety management in the region[3]Source: ECOWAS Regional Agency for Agriculture and Food (RAAF/ARAA), “Public Health: ECOWAS Commits to Quality Livestock Feed Production through Aflatoxin Control,” araa.org.. These cost-related barriers hinder investment in comprehensive mycotoxin control measures and slow the adoption of premium detoxifiers in price-sensitive segments of the African feed industry.

Fragmented Enforcement Outside Formal Feed Channels

Fragmented enforcement continues to hinder the growth of the Africa feed mycotoxin detoxifiers market, particularly beyond the formal mill segment. Regulatory oversight remains inconsistent across many livestock-producing regions, especially in areas where feed is mixed, traded, or distributed through informal channels. This inconsistency weakens the effectiveness of feed safety requirements, as compliance monitoring often does not extend reliably beyond registered commercial operators. For instance, the African Union's adoption of the Statute establishing the Continental Food Safety Agency in March 2025 underscores that continent-wide food safety governance structures are still in the early stages of development. Consequently, many small and mid-sized feed operators fall outside systematic monitoring frameworks, reducing their incentives to invest in routine testing and mycotoxin detoxification solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Biotransformer Uptake Reshaping a Binder-Dominated Market

The Africa feed mycotoxin detoxifiers market share for binders held the largest 65.0% in 2025. Binders remain a cornerstone of demand due to their established role in commercial feed production and their effectiveness in managing mycotoxin risks. Their widespread availability, familiarity among feed manufacturers, and compatibility with existing feed formulations contribute to their continued adoption across various livestock sectors. Demand is particularly robust in maize-based feed systems, where contamination concerns significantly influence purchasing decisions. Additionally, their cost efficiency and ease of integration into feed manufacturing processes further solidify their role in routine feed safety programs.

The Africa feed mycotoxin detoxifiers market size for biotransformers is forecast to grow at the fastest CAGR of 3.9% from 2026 to 2031. This growth is driven by increasing recognition of the need for solutions that address complex contamination profiles beyond traditional adsorption methods. Biotransformers are gaining traction due to their ability to target a broader range of mycotoxins through biological conversion processes, complementing conventional detoxification strategies. Their adoption is particularly significant in advanced feed operations aiming for enhanced feed safety and improved performance outcomes. As quality standards become more stringent, interest in multifunctional detoxification technologies is expanding across commercial production systems.

By Animal Type: Poultry as Volume Anchor, Swine as the Growth Vector

Poultry accounted for the largest 56.8% share in 2025. Poultry remains the dominant consumer of feed mycotoxin detoxifiers due to its dependence on compound feed and the direct impact of feed quality on productivity, flock performance, and profitability. Commercial broiler and layer operations generally maintain stricter feed management practices than many other livestock sectors, supporting consistent demand for toxin mitigation solutions. Producers are increasingly focused on maintaining animal health, feed efficiency, and production consistency, which strengthens the role of detoxifiers within feed programs. Continued expansion of organized poultry production further reinforces the segment’s leading position.

Swine is projected to grow at the fastest CAGR of 4.7% from 2026 to 2031. The segment is benefiting from the gradual modernization of pork production systems and increasing emphasis on feed quality management. Swine producers are becoming more aware of the performance and health implications associated with mycotoxin exposure, encouraging greater adoption of preventive feed safety measures. As commercial production practices expand, demand for consistent feed formulations and improved nutritional management is increasing. The growing integration of feed quality controls into swine production systems is supporting wider acceptance of mycotoxin detoxifiers as part of routine feeding strategies.

Geography Analysis

South Africa accounted for the largest market share of 48.4% in 2025 and is projected to grow at the fastest CAGR of 4.6% from 2026 to 2031. This market leadership is attributed to the country's well-established commercial feed industry, advanced livestock production systems, and higher adoption of feed quality management practices compared to many other African markets. Large-scale poultry, dairy, and livestock producers in South Africa typically operate within structured supply chains, where maintaining feed consistency and controlling contamination are critical operational priorities. Additionally, the presence of organized feed manufacturers and industry-led quality assurance programs has increased awareness of mycotoxin-related risks. These factors have created a more conducive environment for the adoption of feed mycotoxin detoxifiers compared to less formalized regional markets.

Egypt remains a significant demand center due to its highly commercialized poultry and aquaculture sectors, both of which rely heavily on compound feed. The country benefits from a relatively organized feed manufacturing base compared to many regional markets, fostering favorable conditions for routine feed safety practices. Demand is further driven by increasing awareness of contamination risks and the need to sustain animal performance in intensive production systems. Feed manufacturers in Egypt are increasingly adopting preventive quality management strategies, enhancing the role of mycotoxin mitigation solutions in commercial livestock and aquaculture operations.

Kenya is emerging as a key growth market due to the expansion of commercial livestock production and a growing emphasis on feed quality management. Feed manufacturers are prioritizing contamination control as production systems become more structured. A study published in the European Journal of Nutrition and Food Safety in February 2025 revealed that 34.1% of analyzed cereal and animal feed samples in Bomet County, Kenya, tested positive for aflatoxins, underscoring the persistent contamination risks faced by livestock producers. This highlights the importance of preventive feed safety measures and supports the adoption of mycotoxin management solutions across Kenya's feed value chain.

Competitive Landscape

The market is moderately fragmented, comprising multinational feed additive manufacturers and regional distributors competing across both formal and informal feed channels. Key players include DSM-Firmenich AG, Kemin Industries, Inc., Nutreco N.V. (SHV Holdings N.V.), Alltech, Inc., and Bluestar Adisseo Company (China National BlueStar (Group) Co., Ltd.). These companies maintain a strong presence through established distribution networks, technical expertise, and diverse feed additive portfolios. Competition is most intense in organized feed manufacturing sectors, where factors such as product performance, regulatory compliance, and technical support significantly influence purchasing decisions.

Value-added technical services are playing a growing role in shaping competition, particularly in the detoxifier segment. In February 2025, Alltech expanded its Alltech RAPIREAD mycotoxin testing program through a collaboration with Waters | VICAM, enhancing its capabilities to include complete feed analysis at a global level. This development highlights an industry-wide shift toward data-driven feed safety management, where suppliers provide customers with both contamination monitoring and mitigation strategies. As commercial feed producers prioritize quality assurance, companies offering a combination of testing services, technical expertise, and high-performing products are strengthening their competitive positions within formal livestock production systems.

Product differentiation is becoming increasingly critical as feed manufacturers seek solutions to address complex contamination challenges. Biological and enzyme-based technologies are gaining traction, particularly in commercial operations focused on managing a broader spectrum of mycotoxins. Suppliers are investing more in research and development to improve the efficacy of detoxification solutions targeting multiple mycotoxin classes while also supporting animal health and feed performance. This trend underscores the growing importance of innovation and technical specialization as feed producers respond to evolving contamination risks and stricter feed safety regulations.

Africa Feed Mycotoxin Detoxifiers Industry Leaders

DSM-Firmenich AG

Kemin Industries, Inc.

Nutreco N.V. (SHV Holdings N.V.)

Alltech, Inc.

Bluestar Adisseo Company (China National BlueStar (Group) Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DSM-Firmenich AG has opened a new office and application center in Nairobi, Kenya, to enhance animal nutrition innovation and provide technical support across East Africa. This facility aims to improve customer collaboration and provide quality solutions while supporting mycotoxin risk management and feed safety initiatives in the regional livestock market.

- January 2025: Alltech, Inc. expanded its Alltech RAPIREAD mycotoxin management testing program through a collaboration with Waters | VICAM. This partnership enhances global mycotoxin detection capabilities, including in Africa, and supports more accurate contamination assessments, aiding in the selection and application of mycotoxin detoxifiers and improving feed risk management practices.

- January 2024: Novozymes A/S and Chr. Hansen Holding A/S have merged to form Novonesis A/S, establishing a global biosolutions company specializing in enzymes and microbial technologies. This merger enhances the company's ability to develop advanced biosolutions, such as mycotoxin detoxification solutions, aimed at improving feed safety within Africa's livestock industry.

Africa Feed Mycotoxin Detoxifiers Market Report Scope

Mycotoxin detoxifiers include feed additives designed to reduce, bind, or neutralize mycotoxins in animal feed. These additives enhance feed safety, promote animal health and productivity, and mitigate losses resulting from fungal toxin contamination in livestock and aquaculture production. The Africa Feed Mycotoxin Detoxifiers Market Report is Segmented by Sub-Additive (Binders and Biotransformers), by Animal Type (Poultry, Ruminants, Swine, Aquaculture, and Other Animals), and by Geography (Egypt, Kenya, South Africa, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Binders |

| Biotransformers |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| Egypt |

| Kenya |

| South Africa |

| Rest of Africa |

| By Sub-Additive | Binders | |

| Biotransformers | ||

| By Animal Type | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | Egypt | |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for Africa feed mycotoxin detoxifiers demand?

The Africa feed mycotoxin detoxifiers market is forecast to reach USD 143.59 million by 2031.

Which sub-additive category leads current revenue in Africa?

Binders led the market in 2025 with the largest 65.0% of value, supported by lower cost, broad availability, and established use in formal feed mills.

Which animal segment drives the highest demand for detoxifiers in Africa?

Poultry is the largest demand center, accounting for the largest 56.8% of market value in 2025.

Why does South Africa remain the key country in this space?

South Africa held the largest 48.3% of market value in 2025 and is projected to grow at the fastest 4.6% CAGR from 2026 to 2031.

Page last updated on: