Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.47 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Mycotoxin Detoxifiers Market Analysis by Mordor Intelligence

The feed mycotoxin detoxifiers market size is valued at USD 2.36 billion in 2025 and is estimated to grow from USD 2.47 billion in 2026 to USD 3.02 billion by 2031, at a CAGR of 4.10% during the forecast period (2026-2031). Heightened enforcement of aflatoxin and deoxynivalenol thresholds in the European Union and China, the broad phase-out of in-feed antibiotics, and the rising incidence of multi-mycotoxin contamination in corn and soybean meal are sustaining double-digit expansion across the feed mycotoxin detoxifiers market. Commercial integrators in Denmark, the Netherlands, and Brazil are switching from clay binders to enzyme-based biotransformers that preserve nutrient digestibility and align with antibiotic-free labeling, an important competitive differentiator in the feed mycotoxin detoxifiers market. Climate-driven Fusarium migration into temperate wheat and barley belts is enlarging the addressable base in Canada and northern Europe, converting seasonal purchases into year-round demand.

Key Report Takeaways

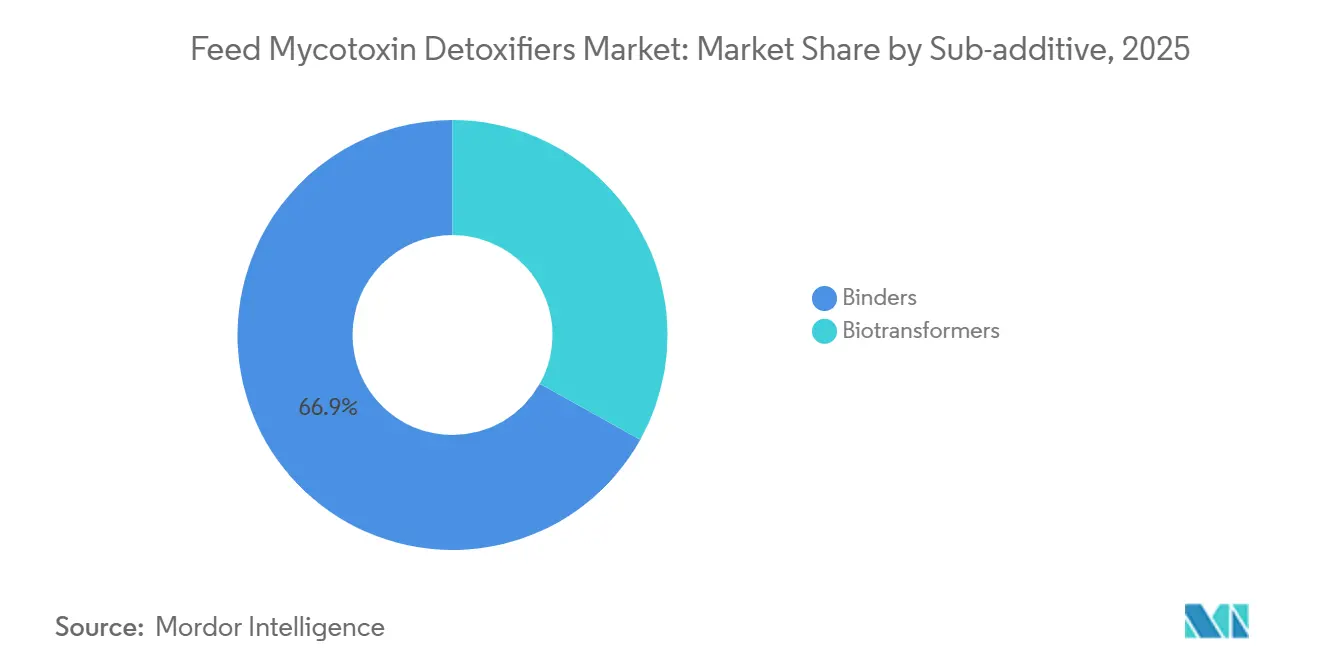

- By sub-additive, binders were the largest segment, holding 66.9% of the feed mycotoxin detoxifiers market share in 2025, whereas biotransformers are the fastest growing segment, advancing at a 4.1% CAGR through 2031.

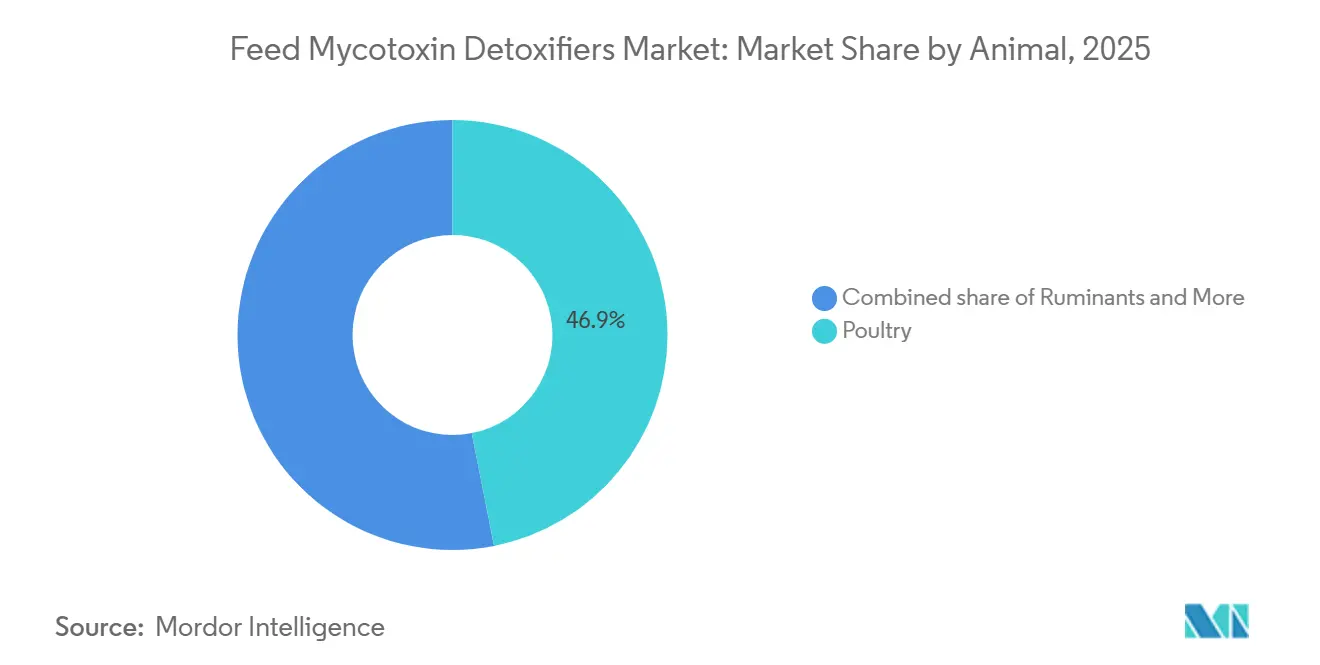

- By animal, poultry was the largest segment, commanding 46.9% of the feed mycotoxin detoxifiers market size in 2025. It is also the fastest-growing segment, projected to grow at a 4.3% CAGR to 2031.

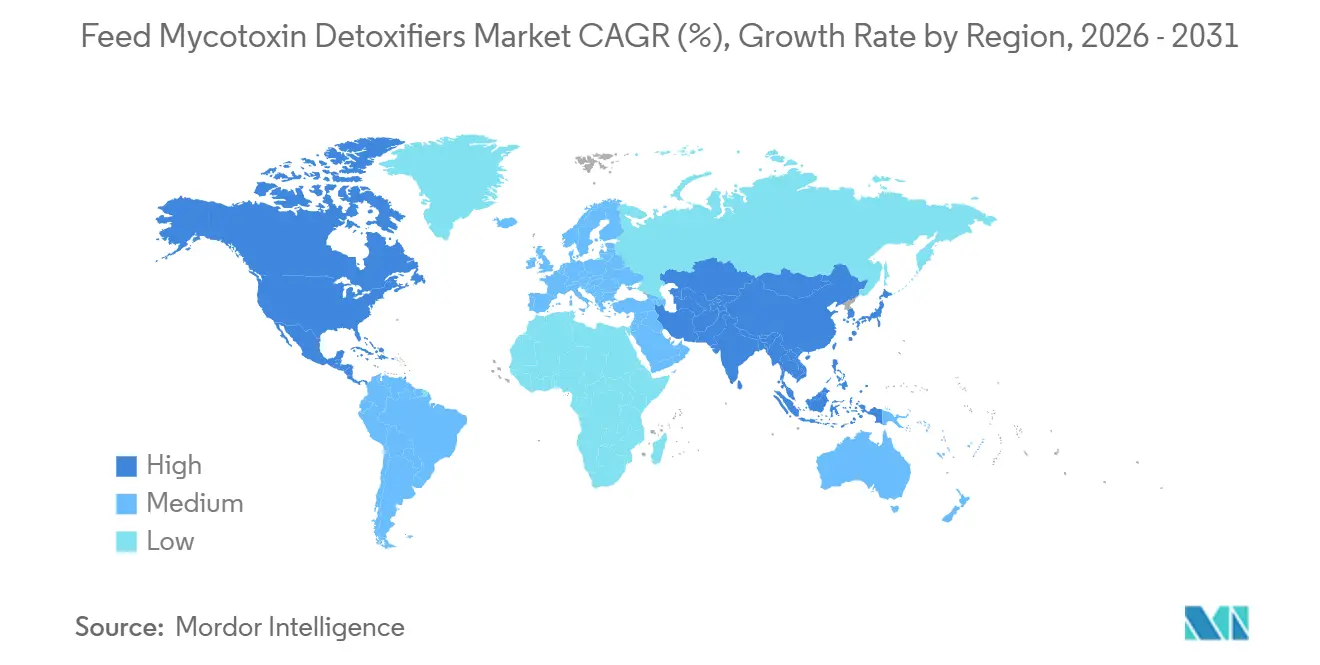

- By geography, Asia-Pacific is the largest region, contributing 31.2% of the feed mycotoxin detoxifiers market share in 2025. North America is the fastest-growing segment, forecast to post the fastest 4.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Mycotoxin Detoxifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of mycotoxin contamination in corn and oilseed meals | +2.3% | Global, with acute pressure in North America, South America, and the Asia-Pacific | Medium term (2-4 years) |

| Stricter maximum-limit legislation in the European Union, China, and Southeast Asia | +1.9% | Europe, China, Vietnam, Thailand, and Indonesia | Short term (≤ 2 years) |

| Growth of commercial compound-feed capacity in emerging economies | +1.7% | Asia-Pacific, South America, and Africa | Long term (≥ 4 years) |

| Climate-change-driven shift in Fusarium and Aspergillus geographies | +1.4% | North America, Europe, and Russia | Medium term (2-4 years) |

| Biotransformer demand boosted by antibiotic growth-promoter phase-outs | +1.6% | Europe, North America, and select Asia-Pacific markets | Short term (≤ 2 years) |

| Rapid adoption of multi-species precision-feeding programs | +1.2% | North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Mycotoxin Contamination in Corn and Oilseed Meals

The increasing prevalence of mycotoxins such as aflatoxins, fumonisins, deoxynivalenol (DON), ochratoxin, and zearalenone in corn, wheat, and oilseed meals is a key driver for the demand for detoxifiers. Erratic rainfall and inadequate post-harvest drying intensified aflatoxin and deoxynivalenol loads in 2024-2025 corn and soybean harvests across Iowa, Illinois, and key Brazilian states, forcing mills to elevate detoxifier inclusion rates or pay premiums for tested grain[1]Source: U.S. Department of Agriculture, “Corn Mycotoxin Screening Results 2024 Harvest,” usda.gov. Similar contamination in European maize imports increased fumonisin exposure, prompting integrators to adopt multi-toxin binders that protect poultry liver health and swine feed efficiency. Continuous confined housing has erased seasonal purchasing spikes, turning detoxifiers into a core year-round ingredient within the feed mycotoxin detoxifiers market.

Stricter Maximum-Limit Legislation in the European Union, China, and Southeast Asia

Governments in regions such as the European Union, China, and Southeast Asia are tightening allowable limits on mycotoxins in animal feed to enhance food safety and ensure export compliance. This has compelled feed mills and integrators to proactively use detoxifiers as a risk mitigation strategy. The European Commission Regulation (EC) No 1881/2006 and related guidance values set strict limits for aflatoxins, fumonisins, and zearalenone. Similarly, China’s GB (Guobiao) standards regulate aflatoxin B1 levels in feed ingredients. Non-compliance can result in penalties and restricted exports. Harmonization efforts under Codex Alimentarius are encouraging countries to align safety standards, raising compliance expectations in emerging markets.

Growth of Commercial Compound-Feed Capacity in Emerging Economies

The expansion of industrial livestock farming in regions such as Asia-Pacific, South America, and Africa is driving growth in compound feed production, thereby increasing the addressable market for detoxifiers. Larger operations require consistent feed safety to maintain predictable performance. According to the Alltech Global Feed Survey, global compound feed production exceeds 1.3 billion metric tons annually, with Asia-Pacific leading in output[2]Source: Alltech, “Special Nutrients Acquisition,” alltech.com . Rapid growth in countries such as Vietnam, India, Indonesia, and Brazil has driven demand for feed additives, including detoxifiers. Vertical integration trends in the poultry and swine sectors have led integrators to control their own feed mills. This centralized decision-making facilitates the standardized inclusion of detoxifiers across large feed volumes. As industrial feed usage deepens in emerging markets, detoxifiers are transitioning from optional to essential feed safety solutions.

Climate-Change-Driven Shift in Fusarium and Aspergillus Geographies

Rising temperatures and irregular rainfall are altering fungal ecology, increasing contamination risks in both traditional and new geographies. Warmer climates favor Aspergillus (aflatoxins), while shifts in humidity favor Fusarium species (fumonisins). The European Food Safety Authority (EFSA) has noted that Southern and Central Europe may face heightened aflatoxin risks due to warming climates. Climate-driven crop stress, such as drought followed by humidity, increases fungal susceptibility both pre- and post-harvest. This unpredictability reduces reliance on historical contamination patterns, prompting feed producers to adopt year-round preventive detoxifier use rather than on a seasonal basis.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus traditional binders for cost-sensitive farmers | -1.8% | Africa, South America, South Asia, and Middle East | Short term (≤ 2 years) |

| Low awareness among small and backyard livestock producers | -1.3% | Sub-Saharan Africa, Southeast Asia, and South America | Medium term (2-4 years) |

| Efficacy variability under multi-toxin challenges | -0.9% | Global, with an acute impact in regions with co-contamination | Medium term (2-4 years) |

| Regulatory gray area for enzyme-based biotransformers in the Americas | -0.7% | United States, Canada, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Awareness Among Small and Backyard Livestock Producers

In developing regions, inadequate testing infrastructure limits awareness of subclinical contamination. Many farmers depend on visual inspection rather than laboratory testing for quality assessment. According to the Food and Beverage Organisation, feed safety assessments and structured monitoring systems are insufficient in parts of Sub-Saharan Africa and Southeast Asia, which contributes to lower use of feed additives. Fragmented distribution networks and inadequate technical advisory services hinder product education. In the absence of extension programs or integrator support, adoption among small-scale producers remains limited.

Regulatory Gray Area for Enzyme-Based Biotransformers in the Americas

The United States Food and Drug Administration has no specific category for mycotoxin-degrading enzymes, which delays commercial entry and adds toxicology costs. Canada applies case-by-case reviews, while Brazil offers only provisional clearances, dampening capital investment in domestic production. Enzyme-based detoxifiers are subject to extensive safety and efficacy evaluations before approval, particularly within the European Union regulatory framework. Under Regulation (EC) No 1831/2003, feed additives must obtain Feed additives Environmental Risk Assessment (FERA) authorization, which involves complex data submission requirements[3]Source: European Commission, “Commission Regulation (EU) 2023/915 on Maximum Levels for Certain Contaminants in Food,” Official Journal, eur-lex.europa.eu. These approval processes can extend commercialization timelines, especially for innovative microbial or enzymatic technologies. In contrast, traditional binders face fewer regulatory barriers, allowing for quicker market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Biotransformer Momentum Builds

Binders were the largest segment, holding 66.9% of the feed mycotoxin detoxifiers market share in 2025, anchored by bentonite and zeolite products priced below USD 2 kg. Yeast-cell-wall glucans widened zearalenone and T-2 coverage and helped binders hold ground in the feed mycotoxin detoxifiers market. This segment benefits from straightforward registration processes and an ample supply of raw materials. Binders, in particular, are preferred for their ability to trap toxins in the animal's gastrointestinal tract, forming a binder-mycotoxin complex that is safely excreted. Their lower cost compared to other detoxifier types and ease of use have significantly contributed to their market dominance, especially in monogastric animals, where they are predominantly utilized.

Biotransformers are the fastest-growing segment, advancing at a 4.1% CAGR through 2031, as European and North American integrators adopt enzymatic solutions that degrade toxins and support gut integrity. Biotransformers are experiencing the fastest growth trajectory among sub-additives. These products are gaining prominence in regions with advanced agricultural practices, as farmers increasingly acknowledge their effectiveness in enhancing animal health and feed efficiency. The segment's growth is further supported by heightened concerns about feed safety and the growing demand for innovative solutions in mycotoxin management. Significant advancements are projected in the feed mycotoxin binders and modifiers market within this context.

By Animal: Aquaculture Surges

Poultry was the largest segment, accounting for 46.9% of the feed mycotoxin detoxifiers market in 2025, and is the fastest growing segment, projected to grow at a 4.3% CAGR to 2031. Aflatoxin impairs liver function and egg quality. Ruminants account for a significant share, mostly dairy cattle, and protecting milk against aflatoxin M1 limits. Swine adoption focuses on sows and nursery pigs that are vulnerable to zearalenone-related reproductive issues. The significant market presence is mainly driven by the growing global population and rising consumer demand for poultry products. The Asia-Pacific region, especially countries such as China and India, plays a major role in this market segment due to extensive commercial poultry operations and an increasing emphasis on feed quality and safety standards.

Aquaculture is hold significat share, the fastest among all species. Shrimp exporters in Thailand and Ecuador now face zero-tolerance aflatoxin rules, driving the mandatory inclusion of aflatoxin binders in shrimp feeds. The feed mycotoxin detoxifiers market size for aquaculture formulations is projected to rise in tandem with recirculating systems and premium salmon exports from Chile.

Geography Analysis

Asia-Pacific is the largest region, contributing 31.2% of the feed mycotoxin detoxifiers market share in 2025, driven by the rapid expansion of industrial feed production and hot, humid climates that promote fungal growth. China’s mega-feed mills pursue Hazard Analysis and Critical Control Point System (HACCP) and International Organization for Standardization (ISO) certification, embedding detoxifiers in every formula. Vietnam and Indonesia’s new mills integrate modular dosing systems that adjust binder and enzyme blends according to rapid immunoassay results, reflecting the precision-feeding trend. India’s consolidation from backyard to commercial production enlarges the customer base willing to pay for proven toxin control. Southeast Asian shrimp and tilapia exporters are particularly sensitive to European rejection risk, accelerating adoption.

North America is the fastest-growing segment, forecast to post the fastest 4.8% CAGR through 2031. United States integrators such as Tyson Foods synchronously roll out detoxifier programs across thousands of contract growers, generating consistent large-lot orders that favor suppliers with strong technical service teams. Canada’s Prairie Provinces, once marginal buyers, now integrate detoxifiers into dairy and swine rations following elevated deoxynivalenol in spring wheat, underscoring how climate change enlarges the feed mycotoxin detoxifiers market. Mexico lifts imports via cross-border distributors to support its expanding poultry hubs in Jalisco and Veracruz.

Europe held significant position of the feed mycotoxin detoxifiers market share in 2025, of mills in Germany, the Netherlands, and Denmark applying standardized inclusion under ISO 22000 feed-safety systems. Premium biotransformers enjoy traction because integrators vie for antibiotic-free and animal-welfare labels that command retail premiums. Russia broadened deployment after Aspergillus outbreaks in its southern grain belt lifted aflatoxin detections. The regional feed mycotoxin detoxifiers market benefits from robust laboratory infrastructure that verifies efficacy claims and supports continuous improvement.

Competitive Landscape

The market is moderately consolidated, with the top players including Cargill, Incorporated, Biomin Holding GmbH (DSM-Firmenich AG), Kemin Industries, Inc., Alltech, Inc., and Bluestar Adisseo Company. These leaders leverage global distribution, proprietary enzyme portfolios, and bundled gut-health solutions, but none wields price-setting power. Competitive focus has shifted toward multi-toxin efficacy and software-enabled dosing. Emerging disruptors include biotechnology startups engineering broad-spectrum esterases, and regional specialists offering yeast-fraction binders tailored to local grain matrices.

Global distributors, such as Brenntag, facilitate market access for mid-tier specialists, proprietary technical support remains a significant differentiator at scale. Combination products that integrate adsorbent clays with degradative enzymes are gaining attention for joint ventures, combining formulation expertise with supply chain capabilities. The regulatory landscape favors companies with comprehensive safety dossiers, offering accelerated returns for early adopters while creating barriers to entry for latecomers.

New entrants and smaller players are capturing market share by focusing on niche segments and developing specialized products tailored to specific animal species or regional requirements. Their success relies on building strong local partnerships, investing in technical expertise, and implementing competitive pricing strategies. These companies actively address potential regulatory changes and environmental concerns while meeting the growing demand for natural and sustainable solutions.

Feed Mycotoxin Detoxifiers Industry Leaders

Cargill, Incorporated

Biomin Holding GmbH (DSM-Firmenich AG)

Kemin Industries, Inc.

Alltech, Inc.

Bluestar Adisseo Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cargill, Incorporated, introduced its new Notox brand of advanced mycotoxin management tools, which leverages cutting-edge technology for superior binding efficiency. The company is emphasizing a data-driven approach, utilizing its extensive mycotoxin database to track global contamination risks in real-time and provide customers with risk assessment tools such as the Mycotoxin Impact Calculator (MIC).

- October 2025: Alltech, Inc., launched its next-generation Mycosorb Evo range of mycotoxin binders, designed for enhanced efficacy against a wider spectrum of mycotoxins, including fusaric acid, and Penicillium-derived toxins.

- September 2024: CABI (Centre for Agriculture and Bioscience International) research validated the industrial feasibility of their Aflasafe biocontrol products, confirming a four-year shelf stability that is resilient to variations in storage temperature and packaging material.

Global Feed Mycotoxin Detoxifiers Market Report Scope

Feed mycotoxin detoxifier modifiers are additives included in animal feed to reduce the harmful effects of mycotoxins. These substances function by binding toxins, degrading them, or preventing their absorption in the animal's digestive system. The Feed Mycotoxin Detoxifiers Market Report is Segmented by Sub-Additive (Binders and Biotransformers), Animal (Aquaculture, Poultry, Ruminants, Swine, and Other Animals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (metric Tons).

Sub Additive

| Binders |

| Biotransformers |

Animal

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

Region

| Africa | By Country | Egypt |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | By Country | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Country | France |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Country | Iran |

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | By Country | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Country | Argentina |

| Brazil | ||

| Chile | ||

| Rest of South America |

| Sub Additive | Binders | ||

| Biotransformers | |||

| Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| Region | Africa | By Country | Egypt |

| Kenya | |||

| South Africa | |||

| Rest of Africa | |||

| Asia-Pacific | By Country | Australia | |

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Philippines | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | By Country | France | |

| Germany | |||

| Italy | |||

| Netherlands | |||

| Russia | |||

| Spain | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Country | Iran | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| North America | By Country | Canada | |

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Country | Argentina | |

| Brazil | |||

| Chile | |||

| Rest of South America | |||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms