Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.64 Billion |

| Market Size (2026) | USD 30.07 Billion |

| Market Size (2031) | USD 37.93 Billion |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

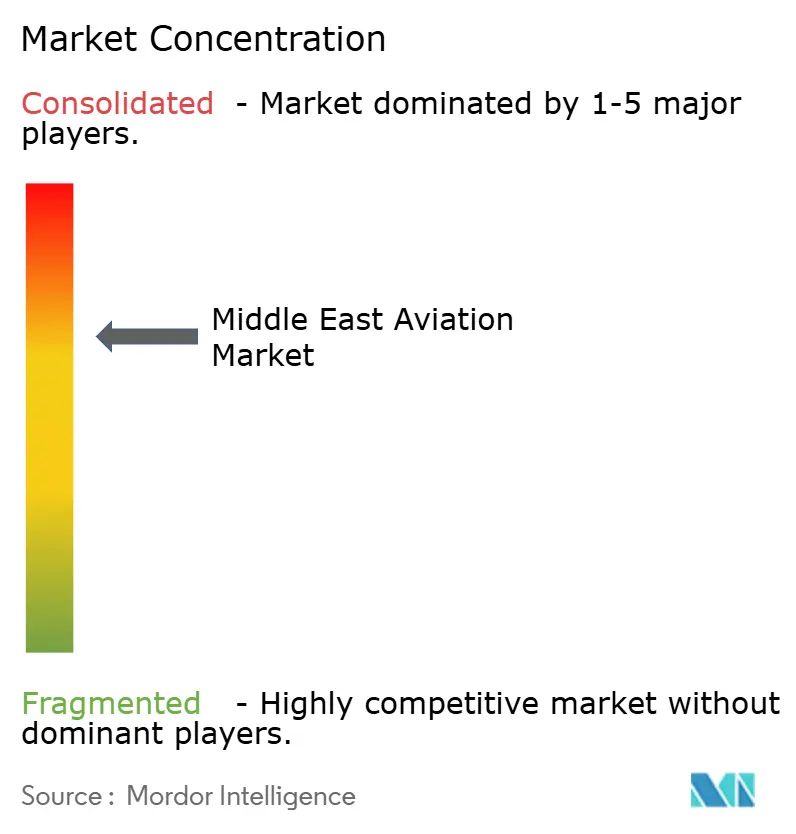

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Aviation Market Analysis by Mordor Intelligence

The Middle East aviation market size is expected to grow from USD 28.64 billion in 2025 to USD 30.07 billion in 2026 and is forecasted to reach USD 37.93 billion by 2031 at a 4.75% CAGR over 2026-2031. The modest growth rate, compared with the 9.4% leap in passenger traffic in 2024, signals a shift in value creation from sheer volume to higher-yield fleets, expanding cargo yields, and premium ancillary revenue streams. Elevated fleet renewal activity, rapid expansion of sixth-freedom hubs, and accelerated low-cost carrier (LCC) penetration continue to shape competitive intensity. Sovereign commitments to sustainable aviation fuel (SAF) production and next-generation airport infrastructure are solidifying the Middle East aviation market’s role as a bridge for connectivity while also cushioning carriers against future carbon-pricing regimes. Yet, geopolitical risk premiums, skilled labor shortages, and uneven air service liberalization remain significant brakes on margin expansion. Cargo monetization, especially time-sensitive e-commerce flows, offers short-cycle upside but also exposes yields to rapid capacity additions.

Key Report Takeaways

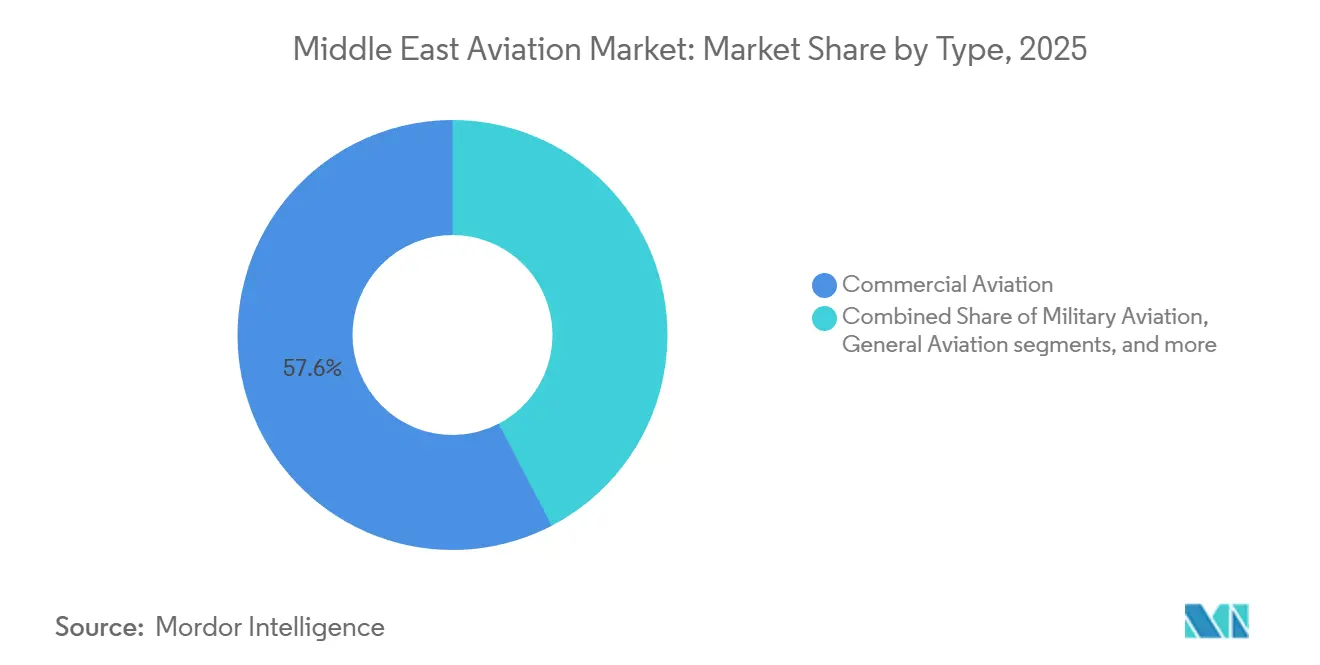

- By type, commercial aviation led with a 57.64% share of the Middle East aviation market in 2025. Advanced air mobility is forecast to grow at an 8.45% CAGR through 2031.

- By propulsion, turbofan engines accounted for 66.42% of the Middle East aviation market size in 2025, whereas hybrid-electric systems are projected to grow at a 7.21% CAGR through 2031.

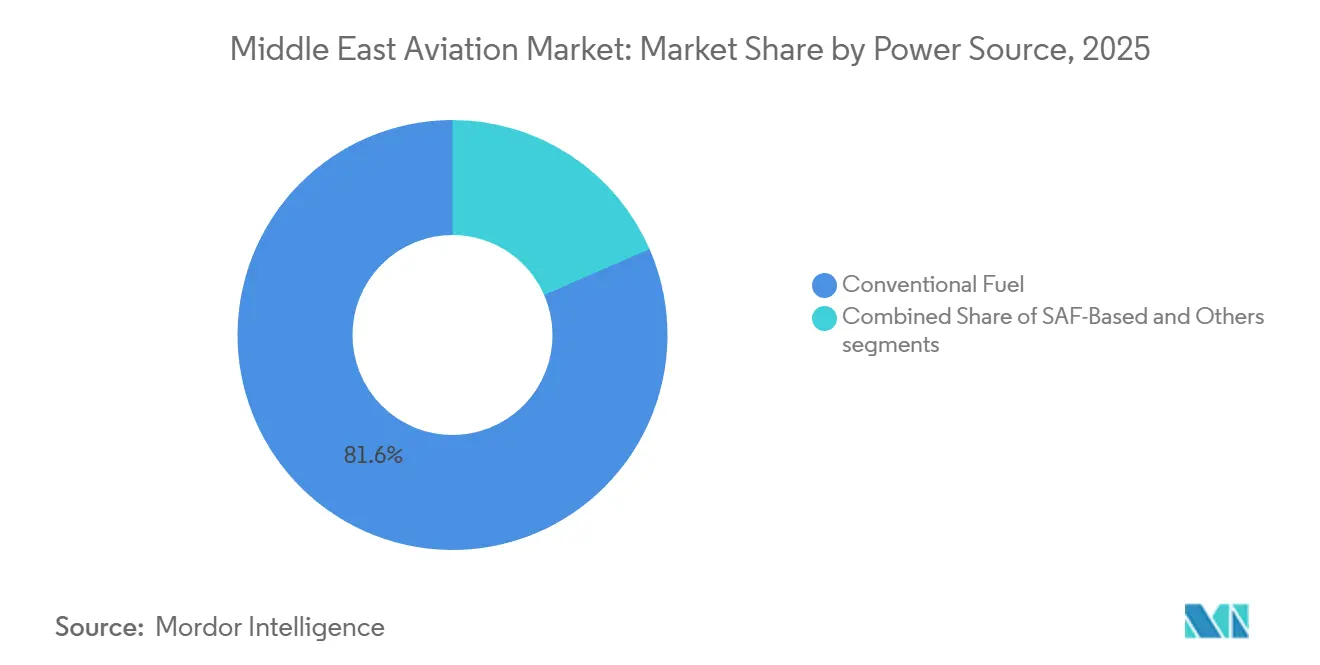

- By power source, conventional jet fuel retained an 81.55% share in 2025; SAF-based solutions are projected to grow at an 8.12% CAGR through 2031.

- By fit, linefit accounted for 67.32% market share in 2025; retrofit is projected to grow at a 6.56% CAGR through 2031.

- By geography, Saudi Arabia accounted for 27.22% of the Middle East aviation market in 2025, while Qatar is forecast to grow at a 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resilient recovery in international passenger traffic supporting regional demand | +1.2% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| Fleet renewal strategies focused on fuel efficiency and emissions optimization | +0.9% | UAE, Qatar, Saudi Arabia | Medium term (2-4 years) |

| Strategic expansion of sixth-freedom hubs by Gulf mega-carriers | +0.8% | UAE, Qatar, Oman, Kuwait | Long term (≥ 4 years) |

| Accelerated adoption of low-cost carrier business models | +0.7% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| State-backed investment in next-generation airport infrastructure | +1.0% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Air cargo growth driven by regional e-commerce and logistics integration | +0.6% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Resilient Recovery in International Passenger Traffic Supporting Regional Demand

Load factors reached 80.8% in 2024, surpassing the 78.2% global average as international routes recovered above 2019 benchmarks. Hub carriers benefit from sixth-freedom flows that reroute travelers between Europe, Asia, and Africa. A unified GCC visa, set to begin in 2026, is expected to unlock 12 million additional leisure and business trips, easing the planning of multi-country itineraries.[1]Gulf Cooperation Council Secretariat, “Unified Visa Initiative,” gcc-sg.org Revenue per passenger must still rise by 3-4% each year to match the 4.75% CAGR, as traffic momentum alone is insufficient. Geopolitical disruptions, such as Red Sea maritime incidents, temporarily divert cargo to air; however, the demand spike dissipates once sea lanes return to normal. Carriers therefore emphasize premium cabins and ancillary services to sustain yield expansion.

Fleet Renewal Strategies Focused on Fuel Efficiency and Emissions Optimization

Emirates bolstered its B777-9 backlog to 270 units in December 2025, aiming to achieve 20–25% fuel-burn savings over legacy widebodies.[2]Boeing, “Emirates 777-9 Contract Increase,” boeing.com Etihad allocated USD 1 billion to retrofit A320 and B787 fleets, paring fuel use by 15% per seat-kilometer. These moves align with CORSIA’s carbon-neutral growth requirement from 2027, ICAO. Regional reliance on conventional jet fuel, however, exposes operators to Brent crude volatility that averaged USD 95–105 per barrel in 2024. SAF costs two to four times as much as Jet A-1, so mandated blending targets and sovereign production incentives are pivotal to closing the price gap.

Strategic Expansion of Sixth Freedom Hubs by Gulf Mega-Carriers

Dubai’s USD 35 billion Al Maktoum International expansion will increase annual capacity to 260 million passengers by 2033, across five runways and 400 gates. Flydubai’s 150-unit A321neo deal diversifies its narrowbody platform, targeting thinner intra-Asia sectors. Qatar Airways plans to serve 190 cities by 2030, backed by 188 widebody aircraft in its order book. Liberal bilateral pacts within the GCC support this scale, but protectionist regimes in Egypt, Jordan, and Iraq curb fifth-freedom reach and cap the potential for transfer traffic. Infrastructure, therefore, outpaces regulatory openness in adjacent markets.

Accelerated Adoption of Low-Cost Carrier Business Models

Low-cost operators accounted for 29% of regional seat capacity in April 2025, representing an 8.1% year-over-year increase in market share. Flynas has expanded its fleet to 80 aircraft and aims to reach 105 by 2027, capitalizing on domestic demand tied to Vision 2030 tourism objectives. Air Arabia’s foray into Central Asia shows that LCCs are winning fares 30-50% below full-service tariffs. Profitability depends on daily utilization that tops 11 hours and ancillary revenue approaching 22% of total income. Slot constraints at Riyadh and Jeddah still favor the national carrier, limiting LCC peak-season expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated geopolitical risk premiums increasing operational insurance burdens | -0.6% | Iraq, Yemen, Iran-adjacent airspace | Short term (≤ 2 years) |

| Regional shortage of skilled pilots and certified maintenance personnel | -0.5% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Limited bilateral air liberalization beyond intra-GCC agreements | -0.3% | Egypt, Jordan, Iraq, Lebanon | Long term (≥ 4 years) |

| Jet fuel price volatility and restricted access to effective hedging instruments | -0.4% | Regional, smaller carriers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Geopolitical Risk Premiums Increasing Operational Insurance Burdens

War-risk premiums increased by 150-200% in 2024 after tensions in the Red Sea and between Iran and Israel led to detours, adding USD 200-400 per flight hour.[3]Lloyd’s of London, “War Risk Report 2024,” lloyds.com Hull and liability policies span 12-18 months, compelling mid-size airlines to renegotiate rates twice as often. Insurers demand collateral equal to 20-30% of the hull value for older fleets, squeezing working capital for carriers such as Iraqi Airways and Mahan Air. Higher premiums translate into ticket surcharges, but price-sensitive leisure demand limits pass-through, compressing margins.

Regional Shortage of Skilled Pilots and Certified Maintenance Personnel

Boeing projects that 60,000 pilots will be required in the region by 2042, yet academies produced only 1,200 graduates in 2024.[4]Boeing, “Pilot and Technician Outlook 2025-2044,” boeing.com Emirates and Qatar training centers expand capacity, but simulator and instructor shortages persist. Maintenance vacancies in avionics and powerplant trades approach 20%, despite Lufthansa Technik’s 200-technician expansion in Abu Dhabi. Smaller airlines poach crews at 20–30% wage premiums, undermining LCC cost advantages and slowing fleet growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Commercial Aviation Anchors Revenue, Advanced Air Mobility Gains Momentum

Commercial services accounted for 57.64% of 2025 revenue, supported by Gulf mega-carriers operating high-capacity widebodies. This represents the largest share of the Middle East aviation market. Growth moderates as mature long-haul flows face yield pressure from LCC encroachment and volatile fuel costs. Nevertheless, premium-cabin retrofits and cargo belly monetization sustain profitability.

Advanced air mobility (AAM), growing at an 8.45% CAGR, is redefining urban trips under 100 kilometers. Saudi Arabia’s Hajj trial transported 12,000 pilgrims via EHang EH216-S eVTOLs at USD 80-100 for a 50-kilometer hop, confirming the commercial potential of the technology. NEOM’s EUR 175 million (USD 204.52 million) stake in Volocopter and Archer’s Saudi JV plan creates domestic manufacturing ecosystems. These initiatives elevate connected-city connectivity and diversify the future Middle East aviation market.

By Propulsion Technology: Turbofan Leads, Hybrid-Electric Retrofits Accelerate

Turbofan engines accounted for 66.42% of the Middle East aviation market in 2025, thanks to Pratt & Whitney GTF and CFM LEAP platforms that cut fuel consumption by 15-20% compared with earlier models. This dominance anchors the Middle East aviation market share in propulsion. Rolls-Royce and Saudia will test hybrid-electric systems on 10 B787s by 2027, aiming for a 10-12% fuel savings on medium-range missions. Hybrid-electric technology’s 7.21% CAGR is driven by retrofit economics and stricter carbon targets.

Turboprops still serve 22% of sub-100-seat fleets, especially in Oman’s secondary airports. Turboshafts dominate offshore and medical helicopters, while turbojets persist in older business jets. Piston engines equip training aircraft across Saudi academies. Full-electric propulsion remains experimental, although the EH216-S taxi shows early niche feasibility. Certification standards unveiled by ICAO in 2024 mandate 10,000-hour endurance tests, which will delay the entry of hybrid-electric narrowbodies to 2028-2030.

By Power Source: Conventional Fuel Prevails, SAF Scaling Requires Cost Relief

Conventional fuel held an 81.55% share in 2025, underpinned by mature refining supply and Brent-linked pricing near USD 2.80-3.20 per gallon. SAF grew 8.12% annually, spurred by Emirates’ 3 million-gallon Neste offtake blended at 30% and Qatar Airways’ 25 million-gallon Gevo deal starting 2028. The UAE aims to achieve an annual output of 700 million liters by 2030, targeting a supply of 8-10% of national demand.

SAF’s 60-90% price premium deters voluntary uptake; adoption therefore hinges on mandates or carbon pricing. Hydrogen and synthetic fuels remain in development, with Airbus expecting no commercial hydrogen-powered jet before 2035. NEOM’s USD 5 billion green-hydrogen plant aspires to produce aviation fuel by 2030, yet distribution and certification hurdles persist.

By Fit: Linefit Dominates, Retrofit Extends Asset Life amid Delivery Delays

Linefit options accounted for 67.32% of revenue in 2025, as OEMs delivered new aircraft equipped with GE9X engines, composite wings, and lightweight cabins. This category captures the lion’s share of the Middle East aviation market size at the installation stage. Retrofit demand grows at 6.56% annually because narrowbody delivery queues typically stretch six to eight years. Etihad’s program installs Sharklet winglets on A320 jets, trimming fuel by 4% and extending range by 100 nautical miles.

Retrofit economics work well on 12-year-old A320s, which cost significantly less for upgrades compared to a new A320neo. Compliance mandates also spur upgrades; 450 regional aircraft are expected to add ADS-B Out equipment by 2025 under EASA requirements. Lufthansa Technik’s Abu Dhabi site handles 120 heavy checks a year, up from 80, capitalizing on this backlog. Still, new-build fuel efficiency stays superior, keeping linefit in demand once supply bottlenecks ease.

Geography Analysis

Saudi Arabia contributed 27.22% of 2025 revenue, the largest national share in the Middle East aviation market. Vision 2030 aims to attract 150 million visitors by 2030, supported by a 121-aircraft order from Saudia and Flynas' expansion. Regulatory slot preferences for Saudia at key airports, however, restrict LCC peak growth.

The United Arab Emirates relies on the USD 35 billion Al Maktoum expansion and Abu Dhabi's Midfield Terminal to reinforce hub status. Emirates holds a 270-unit B777X backlog while Etihad adds 32 widebodies, together injecting 18 million incremental seats by 2028. Qatar has the fastest forecasted CAGR at 6.74%, leveraging Hamad International's 53-million-passenger capacity and an 188-widebody order pipeline. A 25-million-gallon SAF agreement and a new training center address fuel and labor constraints simultaneously. Israel maintains its defense posture through its F-35 fleet expansion despite elevated insurance premiums. Kuwait, Oman, and the broader Rest of the Middle East collectively supply 28% of revenue, with new narrowbody orders and turboprop routes filling secondary-city gaps, even as sanctions hinder some operators.

Regulatory Landscape

Civil aviation oversight in the Middle East is anchored in national regulators that align closely to ICAO Standards and Recommended Practices (SARPs). In the UAE, the General Civil Aviation Authority (GCAA) operates through Civil Aviation Regulations (CARs), Saudi Arabia’s General Authority of Civil Aviation (GACA) administers GACARs, and Qatar Civil Aviation Authority (QCAA) governs national certification and operations. Regionally, ICAO’s Middle East Regional Aviation Safety Plan (MID-RASP 2023-2025) provides a common safety enhancement framework that supports convergence in oversight priorities, while licensing, approvals, and day-to-day operational requirements stay state-specific.

Recent UAE rulemaking highlights how quickly compliance requirements can shift through Safety Decisions and circulars. In February 2026, the GCAA issued Safety Decision 2026-03 to temporarily suspend unmanned aircraft systems (drones) and light sport aircraft operations in UAE airspace due to national security concerns, affecting civil UAS activity. The GCAA also issued Safety Decision 2026-06 with airworthiness flexibility provisions (through 4 May 2026) for stranded aircraft and related audit and procedural changes impacting AMOs and CAMOs. In April 2026, guidance clarified that AI-based pseudo-pilots used in ATC simulation can be adopted within existing safety and training governance without a new, bespoke regulatory approval.

Value Chain Analysis

The Middle East aviation value chain runs from aircraft and engine OEMs through tier suppliers, component distribution and logistics, line maintenance and heavy MRO, and airport and air navigation services, ending with end users that include airlines, defense operators, business aviation, and emerging UAS and AAM operators. Regional demand continues to lean on imported aircraft, engines, and high-value rotables, while localization efforts progress through free-zone clusters and industrial participation programs. Dubai South’s Mohammed bin Rashid Aerospace Hub (MBRAH) has developed an Aerospace Supply Chain zone (1.29 million square feet) to co-locate MRO, training, and manufacturing, and Saudi industrial developers have launched aviation clusters such as MODON’s 1.2 million square meter Modon Oasis aviation hub in Jeddah near King Abdulaziz International Airport.

Downstream economics are shaped by parts availability and repair throughput, especially for carriers and independent MROs. In early 2026, aftermarket procurement cycles lengthened as parts manufacturers prioritized OEM production over spares, leading regional MROs to broaden sourcing beyond traditional OEM channels and to use digital inventory platforms to locate constrained avionics and tooling. Localization is also moving into defense and missionized platforms through named work packages. This includes the Tawazun Council and Airbus agreement to manufacture C295 cargo compartment removable tanks in the UAE (with EPI/EDGE Group as sole-source supplier), as well as Airbus-Mubadala collaboration frameworks for A400M industrial work packages that build local aerostructure and sustainment capability.

Competitive Landscape

Airbus SE and The Boeing Company collectively secure a significant number of commercial aircraft orders. Still, the duopoly’s pricing power erodes as Emirates negotiated 40-45% discounts on its B777-9 deal, a level usually reserved for launch customers. In business aviation, Bombardier, Dassault, and Textron share deliveries to ultra-high-net-worth buyers, although no regional manufacturer has yet cracked the segment, despite their industrial ambitions under Vision 2030.

Defense competition diverges. Lockheed Martin and Boeing dominate high-value fighter contracts, but regional firms such as Turkey’s Baykar and the UAE’s EDGE Group now control 30-35% of unmanned, trainer, and light-attack procurement. Baykar’s 60% global UCAV share is built on proven TB2 deployments across conflict zones, and its Kizilelma unmanned fighter achieved the first beyond-visual-range missile intercept by a UCAV in November 2025. EDGE integrates precision weapons onto imported platforms, signaling a desire to move up the value chain through technology transfer.

White-space opportunities exist for 100-150-seat regional jets optimized for 2,000-3,000 km sectors, hybrid-electric propulsion for sub-100-seat aircraft, and autonomous cargo drones capable of handling 500-1,000 km missions. Engine suppliers GE Aerospace, Rolls-Royce plc, and Pratt & Whitney may differentiate themselves on 100% SAF-ready architectures, even as OEMs focus on composite airframes to reduce fuel burn. Overall, the Middle East aviation market fosters a bifurcated competitive field: concentrated in commercial OEMs yet increasingly contested in defense and emerging technologies.

Middle East Aviation Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Bombardier Inc.

Israel Aerospace Industries Ltd.

Airbus SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is large-scale MRO capacity and engine-repair localization as Gulf fleets expand, delivery delays extend aircraft time-in-service, and utilization increases shop-visit intensity. In May 2026, Emirates broke ground on a USD 5.1 billion engineering complex at Dubai South. Sanad also announced an AED 480 million (USD 130 million) aircraft engine Repair Center of Excellence in Al Ain, reinforcing the push toward in-region heavy maintenance and engine capability for widebody and next-generation engine families. Together, these investments create room for component repair, test-cell capacity, tooling, and licensed capability that can reduce turnaround times and limit reliance on non-regional repair networks.

Opportunities also sit in operational digitization and next-generation infrastructure buildouts. Air traffic management modernization using AI and data-driven tools is being pursued to raise airspace capacity and reduce delay costs at major hubs. AAM infrastructure planning is becoming more structured as well, including LYNEports publishing a GCC-focused AAM Concept of Operations in June 2026 to support vertiport and operational readiness workstreams. Sustainability-linked demand is increasingly showing up in contracts, including May 2026 when DHL Express signed a 10-year offtake for 250,000 tonnes of SAF from a planned SAF One facility in Bahrain (deliveries from 2028). This creates a clearer pathway for SAF supply-chain services, blending logistics, and book-and-claim offerings tied to aviation and express logistics users.

Recent Industry Developments

- June 2026: Boeing delivered the first two 787-9 Dreamliner passenger airplanes to Riyadh Air. The handover advances Saudi Arabia’s airline buildout and adds near-term widebody capacity with fuel-efficient aircraft that can support long-haul network expansion and hub connectivity.

- May 2026: Emirates broke ground on a USD 5.1 billion engineering complex at Dubai South. The project expands regional heavy maintenance capacity and supports faster turnaround and deeper in-house capabilities for large commercial fleets as utilization and retrofit activity increase.

- July 2024: Saudi Arabia ordered four additional Airbus A330 Multi Role Tanker Transport (MRTT) aircraft for the Royal Saudi Air Force, with conversion work scheduled to start in 2026. The order strengthens the defense aviation pipeline and supports sustainment and mission-system integration demand alongside commercial fleet modernization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Middle East aviation market is defined as the value of aircraft and aircraft-related technology sales in the region, covering fixed-wing and rotary-wing platforms, plus unmanned aerial systems and advanced air mobility aircraft.

Scope exclusions: It excludes airport infrastructure buildouts, airline service revenues, and MRO and other aviation services that sit outside aircraft and onboard technology sales.

Segmentation Overview

- By Type

- Commercial Aviation

- Narrowbody

- Widebody

- Regional Jets

- Military Aviation

- Combat

- Transport

- Special Mission

- Helicopters

- General Aviation

- Business Jets

- Commercial Helicopters

- Unmanned Aerial Systems

- Civil and Commercial

- Defense and Government

- Advanced Air Mobility (AAM)

- eVTOL

- Urban Air Mobility (UAM)

- Commercial Aviation

- By Propulsion Technology

- Turboprop

- Turbofan

- Piston Engine

- Turboshaft

- Turbojet

- Hybrid-Electric

- Electric

- By Power Source

- Conventional Fuel

- SAF-Based

- Others

- By Fit

- Linefit

- Retrofit

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Israel

- Kuwait

- Oman

- Rest of Middle East

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public data that explains how much flying activity exists, how fleets are changing, and what the policy direction looks like across the Middle East. We referred to sources such as ICAO and IATA publications, national civil aviation authority releases, airport operator traffic statistics, and fleet and order disclosures from airline annual reports and investor presentations.

To turn those signals into model inputs, older time series were cleaned and aligned so the same definitions were used year over year, and then they were checked against credible media and association updates. Where available, patent databases were reviewed to understand propulsion and power-source shifts, and an import and export shipment-level database was used selectively to sanity-check aircraft and major subsystem movements by country. These desk research sources are illustrative only, and many other public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the scope boundary and the pricing and delivery assumptions that desk sources rarely disclose clearly. We spoke with airline and leasing stakeholders, defense-facing buyers, and suppliers across the aircraft and onboard technology chain. Input was balanced across key Middle East demand centers before final inputs were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 15% | |

| Mid tier: 56% | Functional/Unit leaders: 39% | |

| Smaller Players: 15% | Managers: 46% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where fleet additions, replacement cycles, and delivery pipelines are converted into value using region-relevant average pricing and mix assumptions, then adjusted for the share of fixed-wing, rotary-wing, UAS, and AAM that is actually procured in the Middle East. Totals were corroborated with selective bottom-up checks, such as sampled aircraft program pricing, supplier and channel checks, and a simple volume-times-ASP roll-up for a limited set of platform categories.

Key inputs that shaped the model included airline capacity and traffic direction, active fleet size and age profile, firm order backlogs and delivery schedules, defense procurement cadence, and propulsion and power-source mix shifts (including the pace of SAF-based adoption where it affects retrofit and line-fit content). When a bottom-up checkpoint had gaps, we filled them with conservative mix assumptions and then re-tested them in follow-up calls until the range tightened.

Forecasts were developed using scenario analysis, since aircraft delivery timing and procurement decisions can shift with policy and financing conditions. Scenario weights were guided by expert consensus on near-term delivery realism, with sensitivity runs on ASP progression, platform mix, and retrofit rates.

Data Validation & Update Cycle

Outputs were validated through multiple checks, starting with country-level and type-level splits that must reconcile back to the regional total. Large variances triggered a second pass on the underlying drivers, followed by a targeted re-check with selected interviewees when assumptions could not be supported by public signals.

Before sign-off, the model is reviewed by another analyst to catch inconsistent definitions, currency timing issues, and step-change errors in trend lines. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the most current view available.

Mordor Intelligence's Middle East Aviation Market Size Compared Against Other Published Estimates

Published market sizes for Middle East aviation often do not match because each source draws the market boundary in its own way, and then uses different timing and pricing assumptions. Differences usually show up around what is counted as aviation value, how adjacent services are treated, and which year is used for currency and inflation alignment.

By tracking delivery pipelines, fleet replacement timing, and platform mix at the country level, Mordor Intelligence keeps the estimate tied to aircraft and onboard technology sales, while some sources blend in airport or airline service value or use a wider aviation services definition.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.51 B (2025) | |

| Regional Consultancy A | USD 23.70 B (2025) | Uses a narrower demand build that can undercount defense and emerging segments like UAS and AAM, and it may apply more conservative delivery realization assumptions for the year. |

| Industry Publisher B | USD 26.73 B (2025) | Often follows a broader aviation framing that can shift value between aircraft sales and services, and it can differ on ASP progression and the base-year currency timing used for conversion. |

Taken together, the spread is mainly explained by scope boundaries and by how delivery timing and average pricing are carried into the base year. Our approach stays repeatable because each total can be traced back to clear volume drivers, mix assumptions, and a small set of validation checks that are practical to re-run as new data comes in.

Key Questions Answered in the Report

How large is the Middle East aviation market in 2026?

The Middle East aviation market stands at USD 30.07 billion in 2026 and is projected to reach USD 37.93 billion by 2031, registering a 4.75% CAGR.

Which segment is expanding the fastest in Middle Eastern skies?

Advanced air mobility (AAM) exhibits the highest CAGR, at 8.45% through 2031, as Saudi Arabia scales autonomous air taxis.

What share of regional revenue does conventional jet fuel still command?

Conventional fuel accounts for 81.55% of the 2025 power-source mix despite SAF gains.

Why are hybrid-electric retrofits gaining attention?

The hybrid-electric offers 10-12% fuel savings and support CORSIA compliance while mitigating new-aircraft delivery delays.

Which country is the fastest-growing aviation market in the region?

Qatar is forecasted to post a 6.74% CAGR to 2031, propelled by Hamad International expansion and a 188-widebody order pipeline.

Page last updated on: