Middle East and North Africa Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

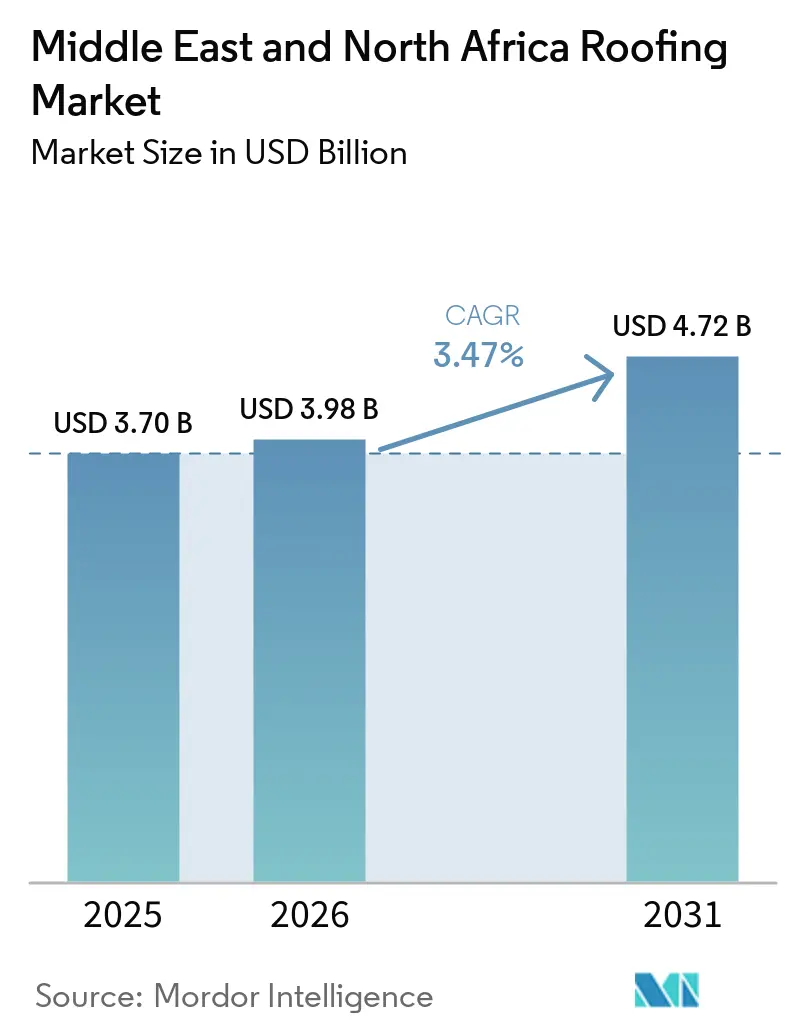

| Base Year Market Size (2025) | USD 3.70 Billion |

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 4.72 Billion |

| Growth Rate (2026 - 2031) | 3.47% CAGR |

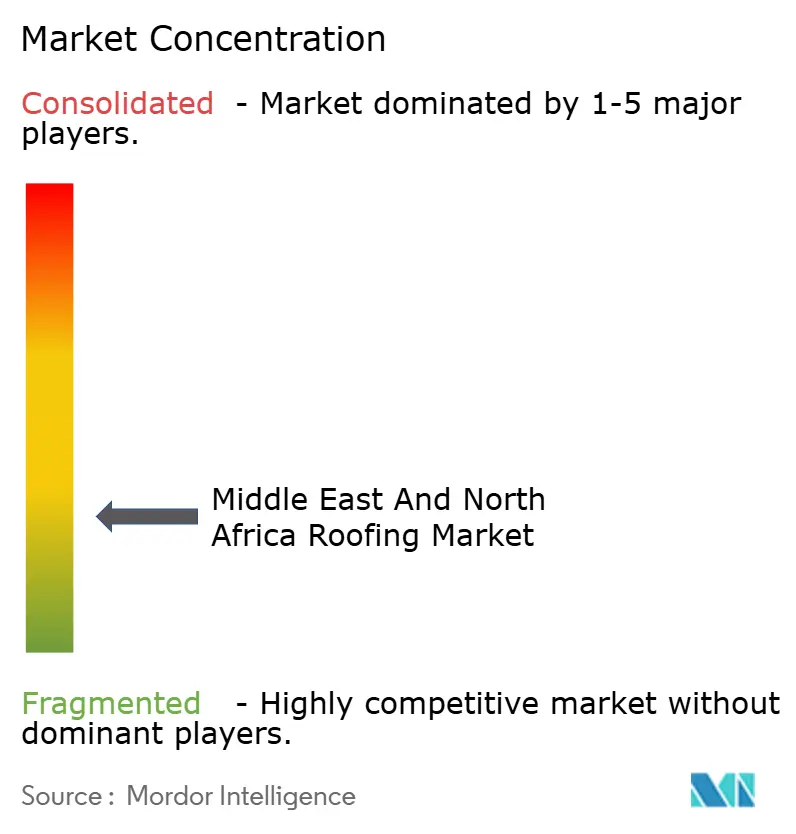

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and North Africa Roofing Market Analysis by Mordor Intelligence

The Middle East And North Africa Roofing Market size is projected to expand from USD 3.70 billion in 2025 and USD 3.98 billion in 2026 to USD 4.72 billion by 2031, registering a CAGR of 3.47% between 2026 to 2031.

The Middle East and North Africa roofing market is being shaped by a long pipeline of housing, tourism, and industrial projects in Saudi Arabia and the Gulf Cooperation Council (GCC), which is keeping demand steady even without a broad regional construction surge. Energy codes in the United Arab Emirates and Qatar are pushing new projects toward insulated and reflective roof systems, steadily boosting the value of each installation. The April 2024 flood event in the United Arab Emirates and Oman also raised the importance of waterproofing and retrofit quality, especially for flat roofs on commercial and institutional buildings. The spread of rooftop solar programs and stricter building performance standards is increasing demand for roof systems that support photovoltaic integration, lower heat gain, and longer service life. Competition in the Middle East and North Africa roofing market remains balanced between global waterproofing and insulation specialists and a wide base of regional fabricators, which supports technical upgrades but keeps pricing pressure on standard projects.

Key Report Takeaways

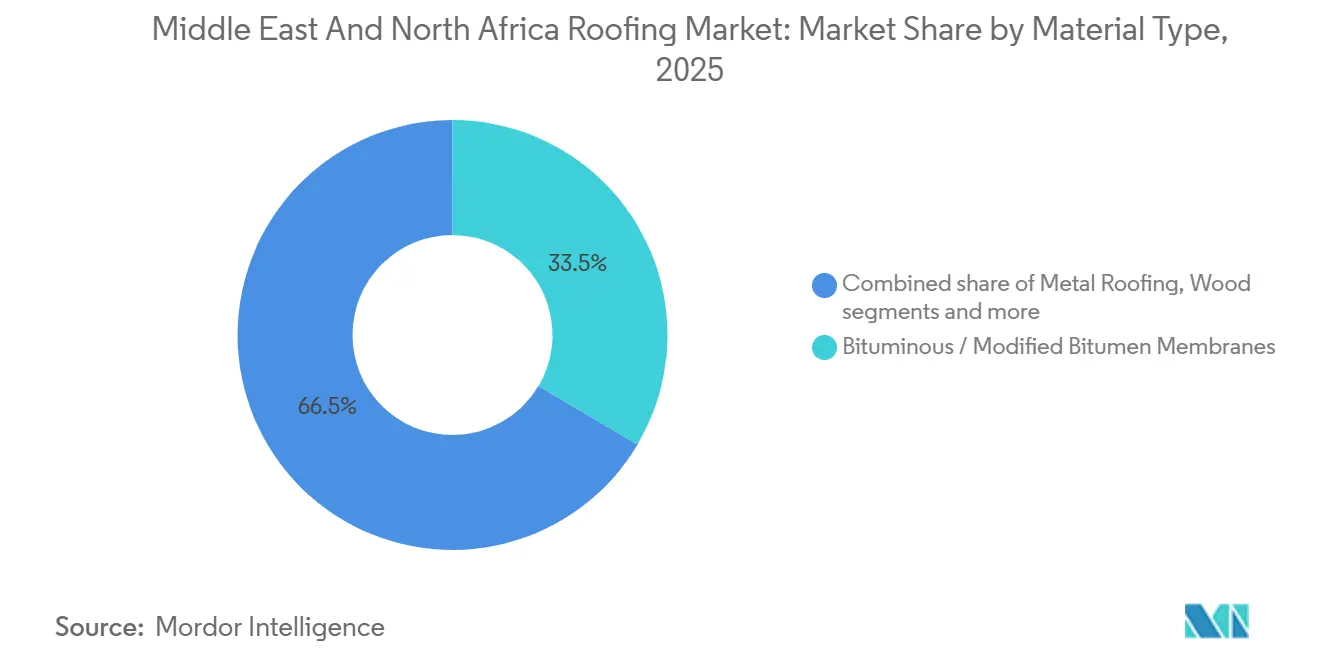

- By material type, bituminous / modified bitumen membranes led with a 33.5% revenue share in 2025, while single-ply membranes are forecast to expand at a 5.8% CAGR through 2031.

- By construction type, new construction accounted for 61% of total demand in 2025, while reroofing and replacement posted the highest projected CAGR of 5.1% through 2031.

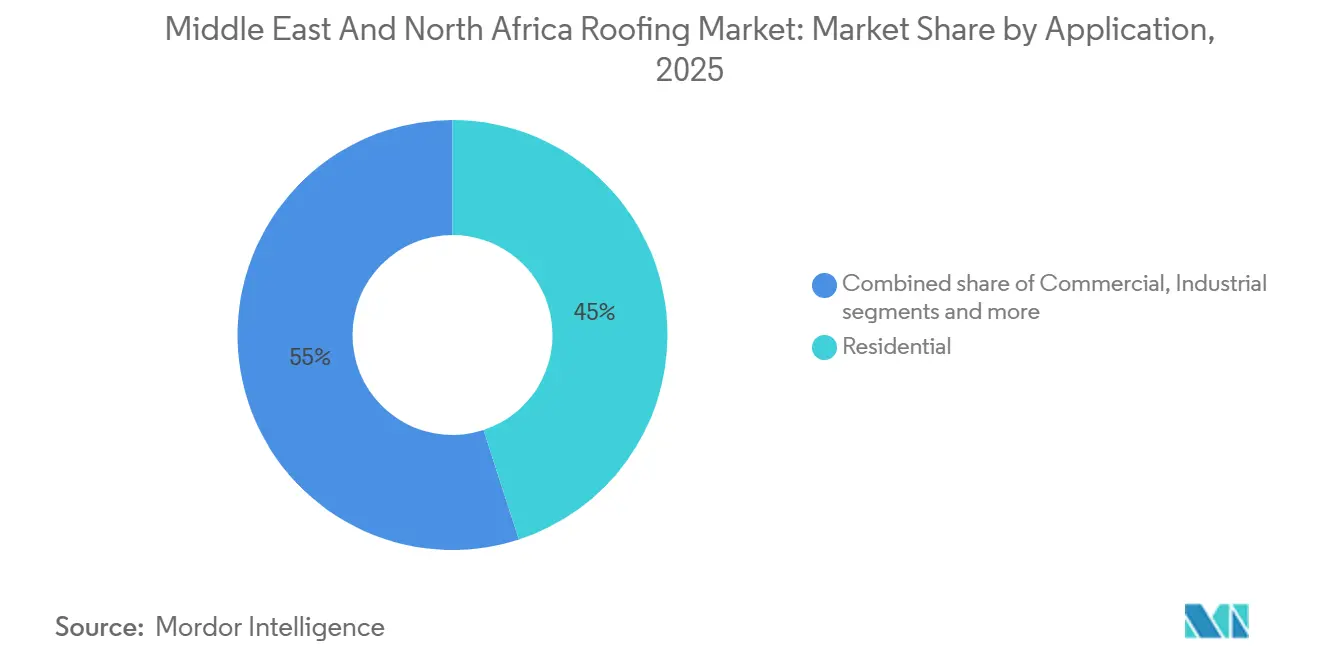

- By application, residential accounted for a 45% share of the Middle East and North Africa roofing market size in 2025, while commercial is advancing at a 4.8% CAGR through 2031.

- By geography, Saudi Arabia held 31% of the Middle East and North Africa roofing market share in 2025, while it is also the fastest-growing country at a 4.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and North Africa Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saudi Giga-Projects, Housing Expansion, and Tourism-Led Roof Demand | +1.20% | Saudi Arabia, Spillover to the United Arab Emirates and Qatar | Medium Term (2–4 Years) |

| Mandatory Energy Codes Increasing Roof Insulation and Reflective Roof Adoption | +0.60% | The United Arab Emirates and Qatar, Extending to Saudi Arabia and Morocco | Long Term (≥ 4 Years) |

| Industrial, Logistics, and Warehouse Build-Out Supporting Insulated Metal Roof Panels | +0.50% | United Arab Emirates and Saudi Arabia, with Spillover to Egypt | Medium Term (2–4 Years) |

| Waterproofing Upgrade Cycle for Flat Roofs in Hot-Climate Commercial Assets | +0.40% | GCC-Wide, with Higher Intensity in the United Arab Emirates and Saudi Arabia | Short Term (≤ 2 Years) |

| Solar-Ready Rooftop Specifications Increasing Demand for Photovoltaic-Compatible Roofing Systems | +0.30% | United Arab Emirates, Saudi Arabia, Morocco, and Egypt | Long Term (≥ 4 Years) |

| Extreme Rain and Flood Resilience Retrofits Accelerating Waterproofing-Led Reroofing | +0.30% | United Arab Emirates, Qatar, and Coastal Saudi Arabia | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Saudi Giga-Projects, Housing Expansion, and Tourism-Led Roof Demand

Saudi Arabia remains the clearest demand engine for the Middle East and North Africa roofing market, as housing expansion and large destination projects are advancing simultaneously. Housing programs are increasing baseline roof demand, while tourism and mixed-use developments are pushing projects toward higher-performing systems with stronger thermal, acoustic, and solar integration requirements[1]Saudi Building Code National Committee, “Saudi Building Code,” Saudi Building Code, sbc.gov.sa. This mix is changing the value profile of the roof package, as more projects now require specification-led systems rather than basic commodity materials. Suppliers that meet project approval standards, warranty expectations, and system certification requirements are in a stronger position than those that compete only on output volume. As a result, the Middle East and North Africa roofing market is benefiting from both high volume and richer technical content.

Mandatory Energy Codes Increasing Roof Insulation and Reflective Roof Adoption

Energy regulation is now a direct specification force in the Middle East and North Africa roofing market because compliance is built into permit and design approval processes[2]Gulf Organization for Research & Development, “GSAS Framework,” GORD, gord.qa. Dubai Municipality requires a minimum Solar Reflectance Index (SRI) of 78 for flat and low-sloped roofs in new construction, and comparable building performance systems are active in Abu Dhabi and Qatar. In Saudi Arabia, the Saudi Building Code sets limits on roof assembly thermal transmittance, and published research shows that insulation can reduce building energy use across the country’s climate zones[3]Saudi Building Code National Committee, “Saudi Building Code,” Saudi Building Code, sbc.gov.sa. The practical effect is that reflective finishes alone are losing ground to roof assemblies that combine membrane performance with insulation and longer-term energy compliance. This is raising the average material bill per project and supporting a higher-value product mix across the roofing market in the Middle East and North Africa.

Industrial, Logistics, and Warehouse Build-Out Supporting Insulated Metal Roof Panels

Industrial and logistics construction is broadening the Middle East and North Africa roofing market beyond its traditional residential base. Warehouses, fulfillment centers, cold storage buildings, and factories often use pre-engineered buildings (PEBs), which favor insulated metal roof systems and standing seam assemblies supplied by specialist manufacturers. The February 2025 ground-breaking for a new Kirby Building Systems manufacturing facility in Saudi Arabia reflects this shift toward localized supply for engineered steel and industrial roof solutions. Qualification standards such as Factory Mutual (FM) Global approval and Underwriters Laboratories (UL) listing are also becoming increasingly important in major industrial tenders, raising the barrier for smaller local suppliers. This favors companies that can combine factory capacity, tested systems, and project documentation as industrial demand expands across the roofing market in the Middle East and North Africa.

Waterproofing Upgrade Cycle for Flat Roofs in Hot-Climate Commercial Assets

A replacement cycle is opening in the Middle East and North Africa roofing market as a large stock of flat roofs moves deeper into its first major waterproofing renewal phase. This demand is strongest in commercial buildings across the GCC, where high temperatures, ultraviolet exposure, and heavy air-conditioning loads constantly stress membrane systems. The April 2024 floods in the United Arab Emirates and Oman heightened urgency by exposing weaknesses in drainage detailing, waterproofing continuity, and maintenance standards across many assets. Replacement work is usually less price-sensitive than volume new-build work because owners are paying to avoid disruption, leakage, and asset damage. That shift is helping premium membranes and better roof detailing gain share in the Middle East and North Africa roofing market, even as overall regional growth remains measured.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel, Bitumen, Polymer, and Import-Linked Input Costs | -0.50% | Global Exposure, Acute in Egypt, Morocco, and Import-Reliant GCC States | Medium Term (2–4 Years) |

| Price-Led Specification Behavior Slowing Premium Membrane Conversion | -0.40% | Egypt, Morocco, and Tier-2 and Tier-3 GCC Project Segments | Long Term (≥ 4 Years) |

| Shortage of Certified Installers for Advanced Roof Systems | -0.30% | GCC-Wide, Particularly Acute in Saudi Arabia and the United Arab Emirates | Medium Term (2–4 Years) |

| Summer Heat and Hot-Work Restrictions Narrowing Installation Windows | -0.20% | GCC-Wide, Concentrated in Riyadh, Abu Dhabi, and Doha | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Volatile Steel, Bitumen, Polymer, and Import-Linked Input Costs

Input cost volatility remains one of the clearest limits on margin expansion in the Middle East and North Africa roofing market. A 2025 study in Buildings found that construction price adjustment mechanisms in Qatar do not fully protect contractors when reliable local pricing benchmarks are weak or delayed. Metal roofing suppliers also remain exposed to movements in global steel pricing, freight, and import parity, even when local prices soften for short periods. The risk is more pronounced in North Africa because imported raw materials can be affected by currency fluctuations and commodity price movements. This cost instability makes specification upgrades harder to sell and can delay the conversion of projects into higher-value products across the Middle East and North Africa roofing market.

Price-Led Specification Behavior Slowing Premium Membrane Conversion

Lowest-cost procurement is still slowing material upgrades in parts of the Middle East and North Africa roofing market. In Egypt and Morocco, familiar bituminous systems and locally available steel products remain the default choice on many residential and smaller commercial jobs because upfront cost still outweighs lifecycle performance in many tenders. This creates a two-speed regional pattern in which premium membranes gain traction in Gulf megaprojects, while value-focused projects maintain older material preferences. The result is slower volume conversion for imported or technically advanced systems, even when regulatory trends support them. Until consultants, project managers, and owners place more weight on lifetime roof performance, pricing discipline will continue to hold back parts of the Middle East and North Africa roofing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bituminous / Modified Bitumen Membranes Dominance Faces Single-Ply Disruption

Bituminous / modified bitumen membranes accounted for 33.5% of total demand in 2025, making them the largest material group in the Middle East and North Africa roofing market. Their lead still rests on proven heat resistance, wide contractor familiarity, and localized supply chains in countries such as Saudi Arabia and Egypt. These membranes are also well established across residential and standard commercial applications, where buyers still put strong weight on initial cost and known installation practices. Even with this lead, the material mix is gradually shifting toward higher-value systems as project owners request stronger waterproofing, greater reflectivity, and warranty support. That shift is boosting value growth in the Middle East and North Africa roofing industry, even as total tonnage rises at a more moderate pace.

Single-ply membranes, including thermoplastic polyolefin (TPO), ethylene propylene diene monomer (EPDM), and polyvinyl chloride (PVC), are the fastest-growing material category at a 5.8% CAGR through 2031. Their appeal lies in rooftop solar compatibility, cleaner installation on occupied buildings, and compliance with cool-roof rules in Gulf commercial projects. Dubai Electricity and Water Authority reported that 725 megawatts of rooftop solar had been connected across 8,430 buildings in Dubai by 2025, underscoring demand for roof assemblies compatible with mounting systems and meeting warranty requirements. Metal roofing also plays an important role in industrial facilities. At the same time, clay and concrete tiles remain relevant in parts of North Africa and the Middle East, and the roofing market will remain mixed rather than single-material-led.

By Construction Type: New Build Scale Contrasts with Retrofit Momentum

New construction accounted for 61% share of the Middle East and North Africa roofing market size in 2025, making it the dominant construction type across the region. This position reflects the ongoing weight of housing delivery, tourism destinations, industrial parks, and mixed-use developments, especially in Saudi Arabia and the United Arab Emirates. Saudi housing policy continues to support this base because the Sakani program targets 2 million homes by 2030 and a 70% homeownership rate, which keeps long-run roofing volume tied to residential expansion. Premium projects add a second layer because they require higher thermal performance, more advanced waterproofing, and stronger integration with renewable power systems. That combination keeps new-build activity central to the Middle East and North Africa roofing market even as retrofit work gains ground.

Reroofing and replacement are forecast to grow faster at a 5.1% CAGR through 2031. The key support for this segment comes from aging flat-roof stock, higher owner awareness after the 2024 floods, and rising attention to waterproofing failures that can disrupt operations in commercial buildings. Retrofit demand is also moving toward better slope design, improved coatings, more detailed drainage, and higher-quality membranes in exposed climates. This means the Middle East and North Africa roofing market is no longer driven only by new area creation, because replacement cycles are becoming a more meaningful source of recurring revenue.

By Application: Residential Anchors Demand While Commercial Reshapes the Mix

Residential applications accounted for 45% of the Middle East and North Africa roofing market in 2025, making housing the largest application base in the region. That lead comes from steady housing programs in Saudi Arabia and continued residential building activity in Egypt and Morocco. Residential roofing still depends heavily on cost control, durability in hot climates, and contractor familiarity, which keeps bituminous systems and steel-based solutions widely used. At the same time, this segment is not static because rising energy standards are raising the performance floor for roofs even in more volume-led projects. That keeps the Middle East and North Africa roofing market tied to housing volume while gradually improving the average value of residential roof packages.

Commercial is the fastest-growing application at a 4.8% CAGR through 2031. Hotels, retail, mixed-use projects, logistics assets, and destination developments are driving this rise because they require more complex waterproofing, insulation, and appearance standards. Rooftop solar is an added tailwind because Saudi Electricity Company guidelines allow rooftop and Building Integrated Photovoltaic (BIPV) systems for commercial premises, which shifts roof selection toward system compatibility. Industrial and institutional buildings also add meaningful volume, and the USD 30 million Metal Park storage hub launched in Abu Dhabi in March 2025 shows the scale of industrial surfaces entering the Middle East and North Africa roofing market.

Geography Analysis

Saudi Arabia held 31% of the Middle East and North Africa roofing market share in 2025 and is also the fastest-growing country with a 4.4% CAGR through 2031. This position comes from a rare overlap of housing delivery, tourism-led megaprojects, industrial diversification, and still-rising penetration of premium roof systems. Projects tied to NEOM, Red Sea Global, and other large developments are increasing the need for reflective finishes, photovoltaic-ready assemblies, and higher waterproofing standards. Saudi Building Code requirements also raise the thermal performance baseline, which supports value growth even in more cost-sensitive residential work. This makes Saudi Arabia the main volume and value center within the Middle East and North Africa roofing market.

The United Arab Emirates is the second-largest country market and has a more mature, yet premium, specification environment. Demand is shaped by Dubai’s Al Sa'fat requirements, Abu Dhabi’s Estidama framework, post-flood waterproofing requirements, and the region’s most advanced rooftop solar rollout. By 2025, Dubai Electricity and Water Authority had connected 725 megawatts of rooftop solar across 8,430 buildings, providing membrane suppliers and standing seam system providers with a clear commercial case for solar-compatible roof design. The 2024 flood event also reset owner priorities around drainage and roof integrity, which is supporting reroofing and waterproofing upgrades across commercial and institutional assets. These factors keep the United Arab Emirates central to premium demand in the Middle East and North Africa roofing market.

Egypt and Morocco are the main North African volume centers, supported by housing activity and expanding industrial construction. Egypt remains more price-sensitive and favors bituminous membranes and pre-painted steel, while Morocco is widening its project base through infrastructure and industrial development. Qatar is smaller in absolute terms but remains relevant because the Green Sustainability Assessment System requirements and post-tournament hospitality activities continue to support demand for reflective and insulated roofs. The rest of the region adds steady volume but less acceleration. Hence, growth in the Middle East and North Africa roofing market remains led by Saudi Arabia, followed by specification-driven demand in the Gulf and volume demand in North Africa.

Competitive Landscape

The Middle East and North Africa roofing market is fragmented, with competition spanning international roofing system providers, regional manufacturers, local fabricators, and installation contractors. No single company holds a dominant position across the region, as roofing demand is distributed across multiple countries, project types, and product categories. Large multinational suppliers such as Sika, SOPREMA, Kingspan, and TSSC Group maintain positions in higher-value waterproofing, insulation, and engineered roofing systems, but collectively account for only a portion of overall market activity, as a large number of regional manufacturers, local fabricators, and installation contractors continue to serve the majority of standard roofing applications across the region. This fragmented structure creates a highly competitive environment in which pricing, delivery capabilities, local relationships, and project execution remain key differentiators across the roofing market in the Middle East and North Africa.

Strategic developments since 2025 have reinforced the importance of regional manufacturing and local market presence rather than significantly increasing market concentration. Sika expanded its footprint through the acquisitions of Gulf Additive Factory in Qatar and Gulf Seal in Saudi Arabia. At the same time, Kingspan strengthened its regional position by launching a new insulation facility in Saudi Arabia. SOPREMA also expanded its presence through manufacturing investments in Dubai and the development of certified applicator networks. While these initiatives improve supplier capabilities and market reach, they have not materially altered the fragmented nature of the Middle East and North Africa roofing market, where numerous local manufacturers, regional producers, and installation contractors continue to compete across both premium and standard roofing segments.

Competition is also intensifying in integrated roofing solutions, particularly in solar-ready roofing systems, energy-efficient assemblies, and advanced waterproofing technologies. However, no supplier currently offers a fully dominant integrated roofing platform across the region. At the same time, regional steel manufacturers, domestic roofing producers, and international entrants are increasing competitive pressure, particularly in North Africa and industrial roofing applications. Maghreb Steel's strong growth trajectory and CSCEC Steel Structure's expansion into Morocco illustrate the increasing diversity of suppliers operating across the market. As a result, the Middle East and North Africa roofing market remains highly fragmented, with competition distributed across manufacturers, distributors, installers, and specialized roofing system providers rather than concentrated among a small group of market leaders.

Middle East and North Africa Roofing Industry Leaders

Sika

Soprema

Kingspan

TSSC Group

Roofings Middle East

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kingspan Group inaugurated a new insulation manufacturing plant in Saudi Arabia, strengthening its Middle East production presence and targeting growing demand for energy-efficient building envelope systems across GCC commercial and industrial projects. The facility supports Kingspan's stated strategy of expanding manufacturing capacity in high-growth international markets beyond its core European base.

- March 2026: SGTM–TGCC Consortium secured a MAD 3.2 billion (approximately USD 340 million) contract from Morocco's National Agency for Public Equipment to design and construct the roof and façade of the Hassan II Grand Stadium in Benslimane. The project features a large-scale tensioned canopy system incorporating steel structures, cable networks, and a textile-aluminum membrane, representing one of the largest roofing engineering contracts awarded in North Africa.

- January 2026: XinFeng Steel announced plans to invest USD 10 billion in an integrated industrial complex within Egypt's Suez Canal Economic Zone. Covering approximately 10 million square meters and targeting an annual output of 10 million tons, the facility will include advanced cold-rolling and tempering lines for galvanized and pre-painted steel products, significantly expanding the regional supply of key inputs used in metal roofing systems across Egypt and the broader MENA market.

Middle East and North Africa Roofing Market Report Scope

The Middle East and North Africa Roofing Market is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, and more), by Construction Type (New Construction and Reroofing and Replacement), by Application (Residential, Commercial, Industrial, Institutional, and Others), and by Geography (Saudi Arabia, United Arab Emirates, Egypt, and more). The Market Forecasts are Provided in Terms of Value (USD).

| Asphalt Shingles |

| Clay and Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Other Roofing Materials |

| New Construction |

| Reroofing and Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Other Applications |

| Saudi Arabia |

| United Arab Emirates |

| Egypt |

| Morocco |

| Qatar |

| Rest of the Middle East and North Africa |

| By Material Type | Asphalt Shingles |

| Clay and Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Other Roofing Materials | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Other Applications | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Morocco | |

| Qatar | |

| Rest of the Middle East and North Africa |

Key Questions Answered in the Report

What is the current size of the Middle East and North Africa roofing market?

The Middle East and North Africa roofing market stands at USD 3.98 billion in 2026 and is projected to reach USD 4.72 billion by 2031, growing at a 3.47% CAGR over 2026 to 2031.

Which material category leads roofing demand across the region?

Bituminous / modified bitumen membranes accounted for 33.5% of the market in 2025 because they remain cost-effective, widely available, and familiar to contractors for hot-climate applications.

Which roofing material is growing the fastest in the region?

Single-ply membranes, including TPO, EPDM, and PVC, are the fastest-growing material type with a 5.8% CAGR through 2031, supported by solar compatibility and cool-roof compliance.

Why is Saudi Arabia so important for roofing demand?

Saudi Arabia accounted for 31% of regional demand in 2025 and is also the fastest-growing country, with a 4.4% CAGR through 2031, as housing delivery, tourism projects, and industrial expansion are advancing simultaneously.

What is driving reroofing and replacement activity in Gulf countries?

Reroofing and Replacement is projected to grow at a 5.1% CAGR through 2031, supported by aging flat-roof stock, stronger owner attention to waterproofing, and the effect of the April 2024 flood event on specification decisions.

How is rooftop solar affecting roof system selection?

Rooftop solar is increasing demand for membranes and metal systems that support mounting, ensure waterproofing continuity, and meet warranty requirements, especially in the United Arab Emirates and Saudi Arabia.

Page last updated on: