Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 240.55 Billion |

| Market Size (2026) | USD 257.63 Billion |

| Market Size (2031) | USD 363.03 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Construction Market Analysis by Mordor Intelligence

The Africa Construction Market size was valued at USD 240.55 billion in 2025 and estimated to grow from USD 257.63 billion in 2026 to reach USD 363.03 billion by 2031, at a CAGR of 7.1% during the forecast period (2026-2031). Rapid urban migration, the African Continental Free Trade Area (AfCFTA) rollout, and heightened government focus on connectivity projects are combining to lift contract backlogs across all major markets. Multilateral lenders continue to anchor funding for transnational logistics corridors, while climate-related finance mechanisms are unlocking capital for water security, renewable power, and green-building initiatives. Rising private-sector participation, particularly through public-private partnerships (PPPs), is beginning to rebalance a historically public-led ecosystem, enhancing project delivery discipline and technology uptake. Construction methods are also modernizing as modular and prefabricated solutions gain traction, addressing skilled labor bottlenecks and accelerating build times in densely populated cities.

Key Report Takeaways

- By sector, residential led with 38.02% revenue share of the Africa construction market size in 2025, while infrastructure is projected to advance at a 9.05% CAGR through 2031.

- By construction type, new builds commanded 71.05% of the Africa construction market share in 2025, whereas renovation is set to expand at a 9.2% CAGR to 2031.

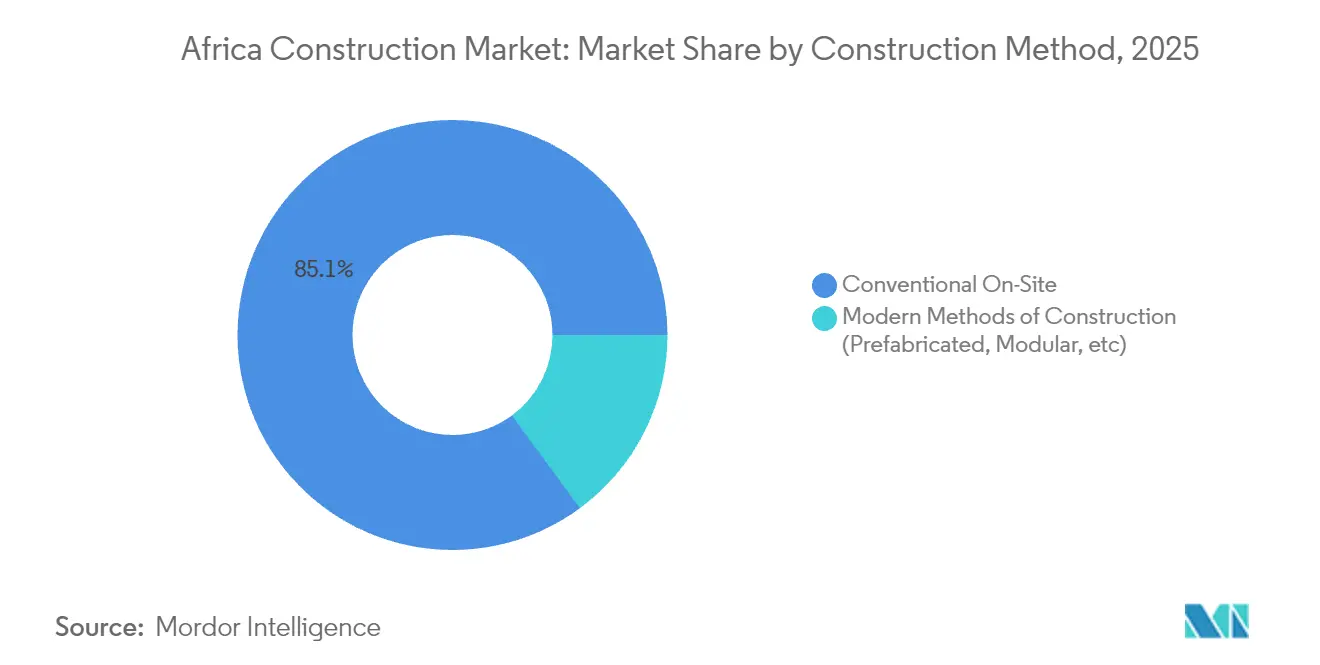

- By construction method, conventional on-site techniques retained an 85.10% share in 2025; prefabricated and modular approaches are the fastest growing at a 9.6% CAGR.

- By investment source, public spending held 75.90% of the Africa construction market size in 2025, although private funding via PPPs is forecast to climb at a 10.4% CAGR.

- By geography, Egypt captured 37.30% of the Africa construction market in 2025, whereas Kenya is the fastest-growing country at a 8.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization & housing backlog | +1.2% | Nigeria, Kenya, Ethiopia | Long term (≥ 4 years) |

| Economic diversification & GDP rebound | +0.8% | Egypt, South Africa, Morocco, Ghana | Medium term (2-4 years) |

| Government-backed infrastructure programs & PPP pipelines | +0.9% | Egypt, Kenya, Morocco | Medium term (2-4 years) |

| Expansion of pan-African logistics corridors | +0.7% | East Africa corridor, West Africa coastal routes | Long term (≥ 4 years) |

| Green-building finance inflows | +0.6% | South Africa, Morocco, Kenya, Nigeria | Medium term (2-4 years) |

| AfCFTA-linked industrial park developments | +0.5% | Ghana, Rwanda, Ethiopia, Morocco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization & Housing Backlog

Africa’s urban population is forecast to double to 1.4 billion by 2050, creating an immediate housing imperative that stretches across major capitals and secondary cities. The current deficit of 51 million affordable units puts sustained pressure on public budgets and spurs innovative financing, including mortgage-backed securities and diaspora bonds. Kenya’s two-million-unit shortfall has pushed authorities to mandate 250,000 new affordable homes annually, injecting steady volume into the Africa construction market. Nigeria’s demographic surge toward 401.31 million people by 2050 further amplifies demand for formal housing and supporting utilities. Smaller economies such as Zimbabwe are also scaling initiatives—for example, a 220,000-unit program slated for completion by 2025—highlighting region-wide momentum.

Economic Diversification & GDP Rebound

Post-pandemic fiscal strategies are channeling recovery funds into infrastructure that underpins manufacturing, services, and renewable energy goals. Morocco targets 52% renewable power in its generation mix by 2030, driving utility-scale construction and grid upgrades. Egypt’s New Administrative Capital and South Africa’s USD 54 billion infrastructure plan illustrate how megaproject pipelines can catalyze private investment and job creation. Ghana’s macro-stabilization under international support has revived flagship transport schemes, restoring contractor order books and reducing financing spreads. These diversification agendas sustain multipliers that reinforce long-run demand for civil works, commercial premises, and industrial zones across the Africa construction market[1]National Planning Commission of South Africa, “Infrastructure Investment Plan 2025–2030,” Government of South Africa, npconline.co.za.

Government-Backed Infrastructure Programs & PPP Pipelines

Seventy-eight percent of African economies now maintain PPP-specific regulations, lifting average annual infrastructure investment by USD 488 million where frameworks are robust. Ethiopia’s USD 7.8 billion Bishoftu Airport and Morocco’s USD 10 billion rail plan are emblematic of how PPP structuring enables transformative assets without unduly stretching public debt limits. Transparent risk-allocation models and standardized concession templates are shortening financial close timelines, bringing global lenders and contractors deeper into the Africa construction market. Capacity-building programs by multilateral agencies also improve contract oversight, mitigating historic cost overrun patterns and bolstering investor confidence.

Expansion of Pan-African Logistics Corridors

AfCFTA implementation has triggered parallel investments in roads, rail, ports, and dry ports that knit together regional value chains. Since 2024, over USD 15 billion has flowed into the Northern Corridor linking Kenya, Uganda, Rwanda, and South Sudan, cutting transit times by up to 40% on key trade routes. The Abidjan-Lagos coastal highway and Morocco’s new Mauritania crossing support metals, agri-business, and tourism flows, reinforcing demand for bridges, tunnels, and service centers. Corridor-led industrial nodes generate follow-on commercial and residential schemes, multiplying contract opportunities in the wider Africa construction market[2]Amani Abou-Zeid, “Status of Implementation of the AfCFTA,” African Union Commission, au.int.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political-regulatory volatility & contract risk | -0.9% | Sahel, parts of East Africa, select West Africa | Short term (≤ 2 years) |

| Skilled-labor deficits & productivity gaps | -0.8% | Most fast-growing markets | Medium term (2-4 years) |

| Hard-currency shortage & capital-controls risk | -0.6% | Nigeria, Ghana, Zambia, Malawi, Ethiopia | Short term (≤ 2 years) |

| Climatic shocks driving insurance & rebuild costs | -0.5% | Sahel, East Africa, Southern Africa drought zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Political-Regulatory Volatility & Contract Risk

Security incidents in the Sahel and sudden policy reversals elsewhere have raised political-risk premiums, pressuring contractor margins and insurance costs. Project suspensions by several global firms underscore the sensitivity of the Africa construction industry to governance instability. Retroactive rule changes, such as new localization quotas, can distort project economics and delay execution timetables. Currency volatility adds a second-order impact by inflating imported material costs and undermining debt-service capacity for foreign-currency loans. These uncertainties prompt risk-sharing mechanisms and demand contractual safeguards that lengthen negotiation cycles.

Skilled-Labor Deficits & Productivity Gaps

Demand for masons, plumbers, and BIM technicians consistently outstrips supply, leading to wage spikes and project overruns in hubs such as Johannesburg and Nairobi. Training academies lag output targets, while migration funnels skilled workers toward higher-pay Gulf markets. Limited on-site automation means productivity still relies heavily on manual processes, amplifying the impact of labor shortfalls. The adoption of digital twins and off-site fabrication is constrained by uneven broadband penetration and high equipment costs, further widening the capability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Drives Long-Term Growth

Infrastructure commands the fastest 9.05% CAGR within the Africa construction market, energized by flagship transport, energy, and water projects that enhance regional integration and climate resilience. Residential retained a 38.02% share of the Africa construction market size in 2025, buoyed by housing backlog programs and mortgage market reforms. Commercial schemes trail but remain significant, tracking the expansion of retail chains and multinational head-office relocations.

Mass-transit rail in Egypt, the USD 7.8 billion Bishoftu Airport in Ethiopia, and Morocco’s USD 40 billion water-security master plan anchor multiyear capital commitments, providing visibility to contractors and suppliers. Meanwhile, AfCFTA-enabled industrial estates stimulate warehousing and light-manufacturing structures, bridging infrastructure and commercial sub-sectors. As governments mainstream climate adaptation, infrastructure outlays increasingly cover levee upgrades, desalination plants, and smart-grid deployments, thereby diversifying contractor scope within the Africa construction market.

By Construction Type: Renovation Gains Momentum

New builds ruled with a hefty 71.05% Africa construction market share in 2025, mirroring the continent’s infrastructure gap and swelling city footprints. Renovation, however, is projected to outpace at a 9.2% CAGR, propelled by asset-life extension and energy-retrofit mandates, particularly in middle-income economies.

South Africa’s refurbishment of apartheid-era commercial towers and Ghana’s school-rehabilitation programs illustrate how aging assets pivot capital toward retrofits. Climate-resilience spending further accelerates facade upgrades, waterproofing, and insulation improvements. Contractors with diagnostic-survey and BIM reverse-engineering capabilities are positioned to capture this climbing renovation slice of the Africa construction market.

By Construction Method: Technology Adoption Accelerates

Conventional techniques still dominate 85.10% of contracts, yet modular and prefabricated systems are forecast to expand at 9.6% CAGR through 2031. Modular dormitories for mining camps in South Africa and factory-built housing shells in Lagos highlight on-site labor savings and quality gains.

Government pilot schemes in Tanzania now mandate Building Information Modeling for select public projects, signaling policy support for digital workflows. Cost-certainty, faster schedules, and reduced waste resonate with developers contending with skilled-labor shortages, thereby accelerating technology penetration across the wider Africa construction market.

By Investment Source: Private Sector Participation Surges

Public expenditure accounted for 75.90% of 2025 spending, but private inflows through PPPs are set to grow 10.4% annually as fiscal headroom narrows. China’s pivot toward equity-based PPP stakes rather than sovereign loans exemplifies changing deal structures.

The USD 350 million Tema Motorway PPP in Ghana demonstrates how shared-risk frameworks mobilize domestic pension funds and foreign institutional capital. Climate-bond issuances and blended-finance vehicles expand the investable universe further, embedding ESG metrics that attract global asset managers searching for yield in the Africa construction market.

Geography Analysis

Egypt retained 37.30% of the Africa construction market in 2025, leveraging a mature contractor base and steady mega-project flow, including the New Administrative Capital and Suez Canal upgrades. Its streamlined approvals, bonded logistics zones, and deep labor pool foster execution certainty that reassures international financiers. Simultaneously, PPP reforms are widening the door for private toll-road and urban-rail concessions, diversifying procurement channels beyond state-funded models.

Kenya is the fastest-expanding market with a 8.9% CAGR from 2026-2031, underpinned by the USD 470 billion Mombasa-Nairobi Expressway, commuter rail extensions, and renewable-power corridors. Foreign-exchange stability and judicial reforms strengthen project bankability, elevating Nairobi’s status as the gateway for East African engineering, procurement, and construction (EPC) firms.

Nigeria, South Africa, Ethiopia, and Morocco round out the second-tier heavyweights. Nigeria’s infrastructure drive aligns with oil-sector revival and housing-finance initiatives, sustaining a sizeable slice of the Africa construction market. South Africa directs capital toward grid stabilization and transport-hub refurbishments, while Ethiopia’s airport and dam programs anchor inward investment despite regional security headwinds. Morocco’s USD 10 billion rail and USD 40 billion water projects transform its northern trade corridors, signaling a climb in market share over the forecast horizon.

Competitive Landscape

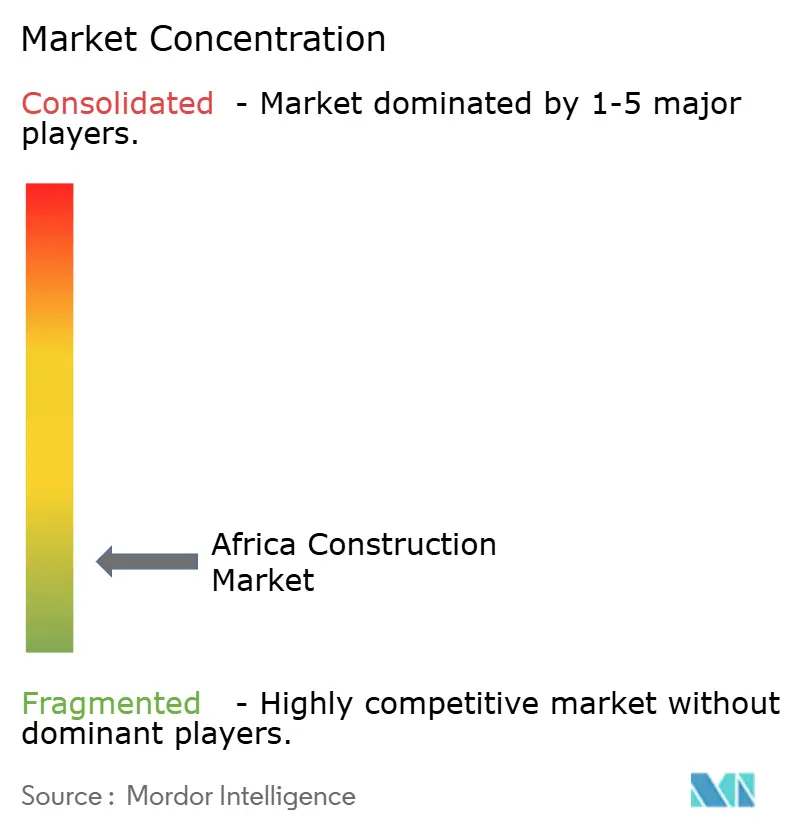

The Africa construction market exhibits high fragmentation, with no single contractor controlling more than 5% of regional turnover. Chinese state-owned enterprises such as China Communications Construction Group and China Railway Construction Corp still win large civil works packages under government-to-government frameworks, yet project awards increasingly hinge on localization clauses that favor joint ventures with domestic firms. European majors Vinci, Bouygues, and Strabag focus on high-specification rail, hydropower, and airport contracts where technical thresholds are higher.

Local champions, including Julius Berger Nigeria, Aveng, and WBHO, expand through cost-competitive bids and nuanced regulatory knowledge, helped by preference policies that award additional scoring for domestic content. As technology becomes an edge, early adopters of BIM-enabled clash detection and drone-based site monitoring are garnering productivity advantages that translate into improved bid accuracy. Prefabricated housing specialists from South Africa and Kenya are carving out niches in the affordable-housing sub-sector, highlighting fragmentation even within emerging technology arenas of the Africa construction market.

External market entrants face growing compliance hurdles around ESG, data-sharing, and workforce nationalization, impacting cost structures and partnership strategies. Supply-chain localization is intensifying, driving demand for regional cement, steel rebar, and façade systems, which in turn is elevating procurement risks tied to commodity price swings. The competitive chessboard remains fluid, offering room for strategic alliances centered on specialized equipment, digital twins, and green-material innovation.

Africa Construction Industry Leaders

China Communications Construction Group Ltd.

China Railway Construction Coro Ltd.

Vinci SA

Dangote Group

Bouygues SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Morocco approved a USD 10.3 billion rail expansion, including a high-speed link to Marrakesh, to connect 43 cities and 12 ports by 2030.

- February 2025: Morocco and Mauritania agreed to open a new Smara-Bir Moghrein border crossing to facilitate USD 1 billion in annual iron ore exports.

- August 2024: Ghana signed a USD 350 million PPP with Maripoma Limited to reconstruct the Accra-Tema Motorway, signaling West Africa’s growing appetite for private capital in highway assets.

- June 2024: Kenya inked a USD 470 billion contract for the Mombasa-Nairobi Expressway, the region’s largest transport investment to date.

Africa Construction Market Report Scope

Construction is a diverse industry that includes activities ranging from mining, quarrying, and forestry to constructing infrastructure and buildings, manufacturing and supplying products, and maintenance, operation, and disposal.

A complete background analysis of the African construction industry, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and geographical trends, and the COVID-19 pandemic’s impact, is covered in the report.

The African construction market is segmented by sector (commercial construction, residential construction, industrial construction, infrastructure (transportation) construction, and energy and utility construction), construction type (additions, demolition, and new construction), and region (Eastern Africa, Western Africa, Southern Africa, and Northern Africa). The report offers market sizes and forecasts for the African construction market in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Nigeria |

| South Africa |

| Egypt |

| Kenya |

| Ethiopia |

| Rest of Africa |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Nigeria | |

| South Africa | ||

| Egypt | ||

| Kenya | ||

| Ethiopia | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Africa construction market and its forecast CAGR?

The market is valued at USD 257.63 billion in 2026 and is projected to expand at a 7.1% CAGR through 2031.

Which country holds the largest share in African construction activity?

Egypt leads with a 37.30% share, supported by mega-projects such as the New Administrative Capital and Suez Canal upgrades.

Which segment is expected to grow fastest through 2031?

Infrastructure construction is forecast to grow at 9.05% CAGR, driven by transport, energy, and water projects.

How significant is private investment in African construction?

Private funding accounts for 24.10% of spending today and is projected to rise at 10.4% CAGR as PPP models proliferate.

Page last updated on: