Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

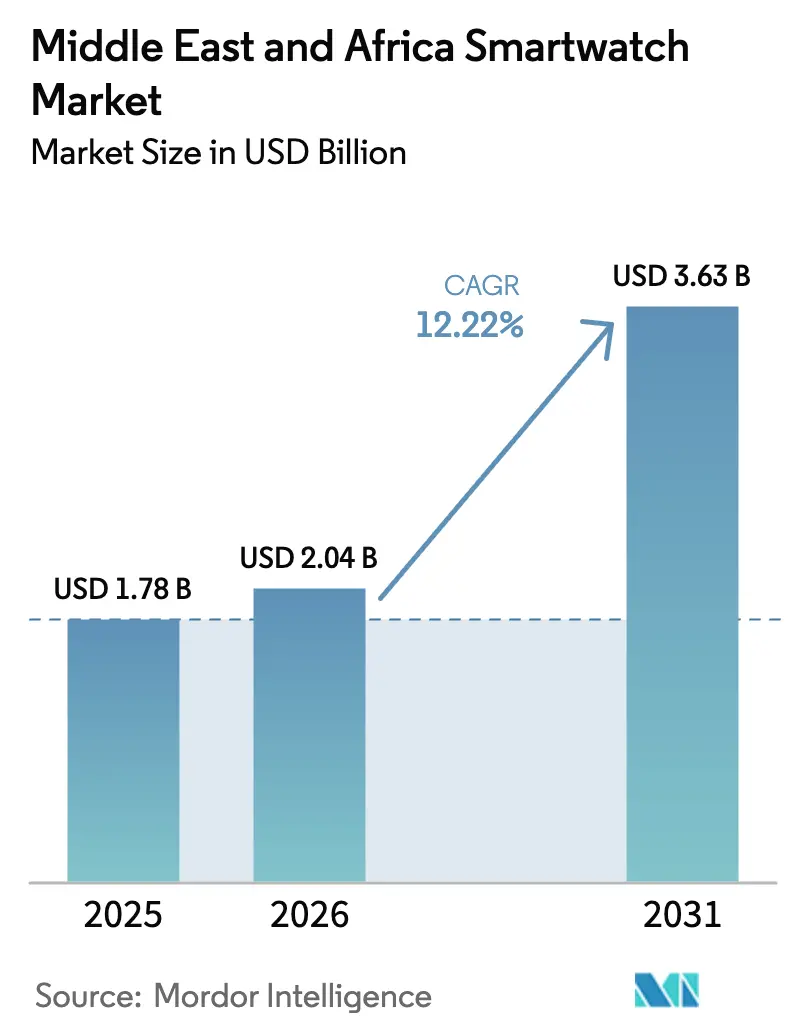

| Base Year Market Size (2025) | USD 1.78 Billion |

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 12.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Smartwatch Market Analysis by Mordor Intelligence

The Middle East And Africa Smartwatch Market size was valued at USD 1.78 billion in 2025 and is estimated to grow from USD 2.04 billion in 2026 to reach USD 3.63 billion by 2031, at a CAGR of 12.22% during the forecast period (2026-2031). This outlook is underpinned by sovereign-funded digital health mandates across the Gulf Cooperation Council (GCC), fintech partnerships that embed tap-to-pay credentials in wearables, and 5G RedCap rollouts that reduce radio module power draw by half. Cellular connectivity is redefining watches as telemedicine endpoints, while budget devices priced below USD 199 are unlocking first-time adoption in Kenya, Nigeria, and South Africa. AMOLED screens remain the dominant display owing to established supply chains, yet MicroLED prototypes already demonstrate 33% higher daylight brightness, confirming a clear premium-tier migration path. WatchOS continues to lead, but HarmonyOS is closing the gap as Huawei localizes its app store and negotiates bulk-purchase subsidies with GCC telcos. Overall, hardware shipments are shifting from Bluetooth-only accessories to independently networked devices that integrate with population health dashboards.

Key Report Takeaways

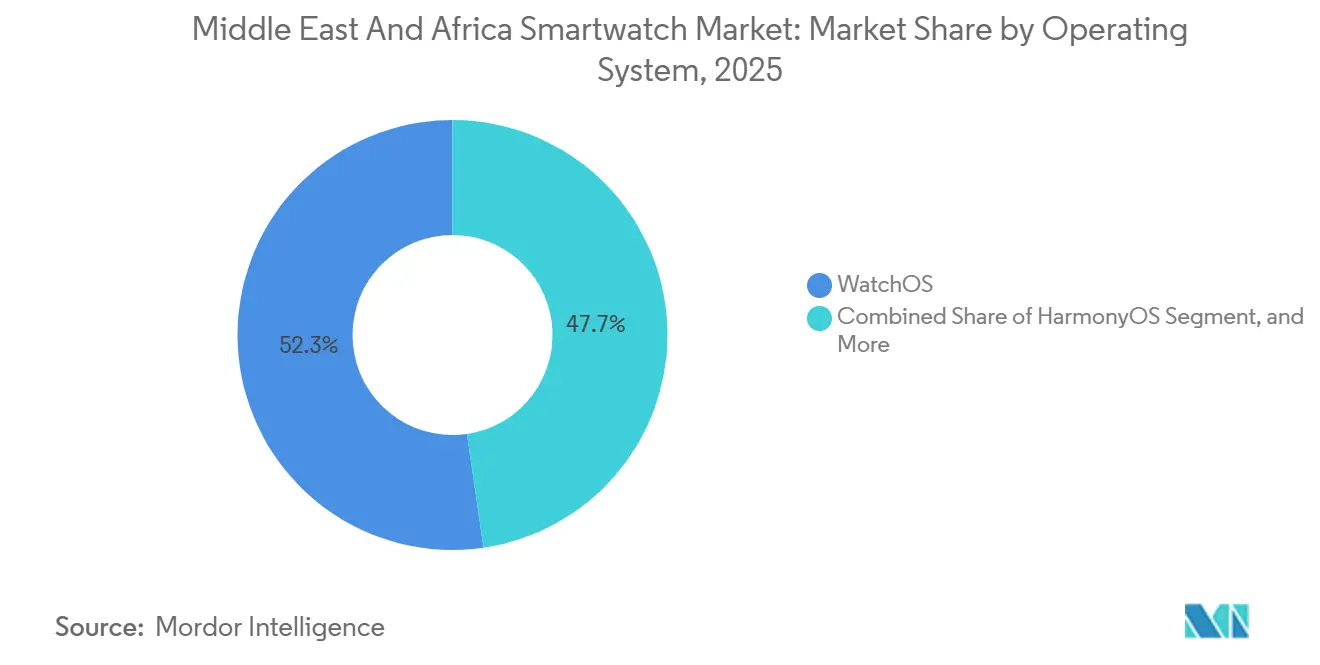

- By operating system, WatchOS accounted for 52.31% of the revenue in 2025, while HarmonyOS is forecast to post a 13.11% CAGR through 2031, representing the fastest growth in the segment.

- By display technology, AMOLED dominated with 68.19% of 2025 shipments, whereas MicroLED units are forecast to expand at a 13.24% CAGR over the same period.

- By connectivity, Bluetooth-only devices represented 59.24% of the 2025 volume; however, cellular LTE and 5G watches are projected to expand at a rate of 13.19% through 2031.

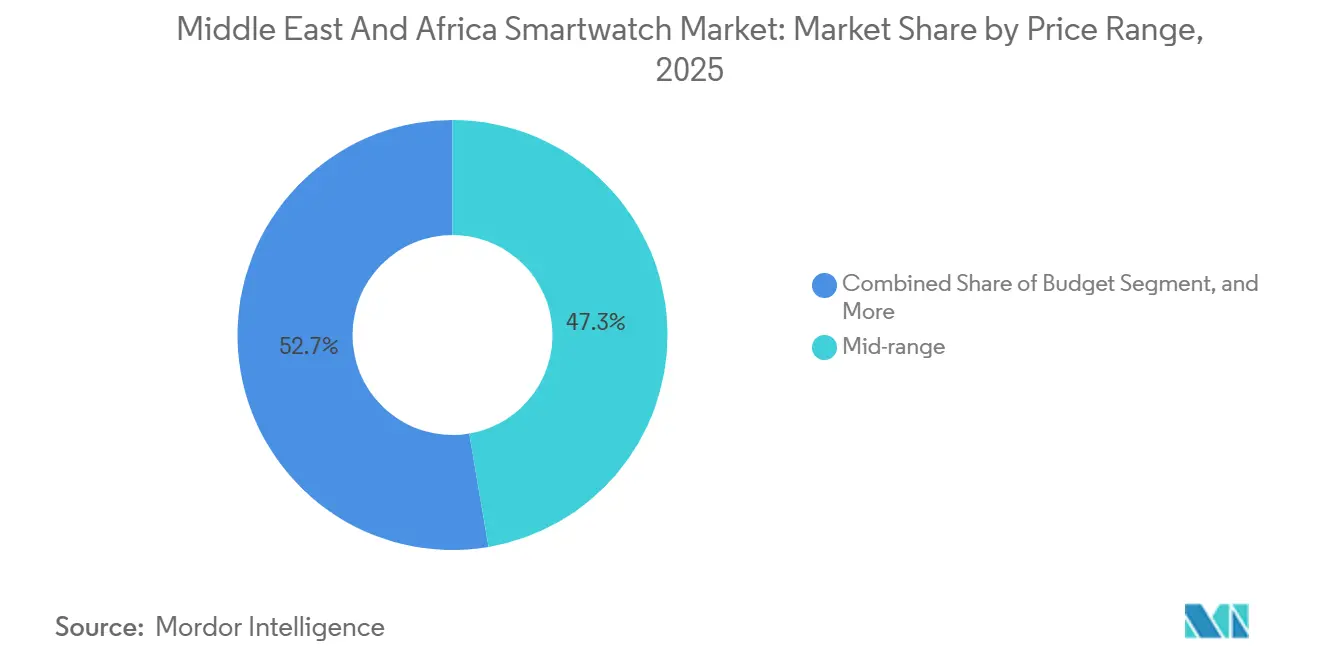

- By price band, mid-range models priced USD 200-399 captured 47.33% of sales in 2025; yet, the sub-USD 199 budget tier is predicted to grow at a 12.93% CAGR, making it the fastest-growing bracket.

- By application, sports and fitness accounted for 43.57% in 2025, while medically validated use cases are set to register a 13.07% CAGR through 2031.

- By geography, the Middle East accounted for 58.46% of 2025 revenue, while Africa is on track to post a 12.61% CAGR to 2031, the highest across subregions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Smartwatch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of eSIM-based LTE smartwatches | +2.1% | GCC core (UAE, Saudi Arabia, Kuwait, Qatar), spillover to Turkey and South Africa | Medium term (2-4 years) |

| Rapid expansion of fintech-enabled wearable payments | +1.8% | UAE, Saudi Arabia, Kuwait, Egypt, South Africa | Short term (≤ 2 years) |

| Government-led digital health initiatives in GCC | +2.3% | UAE, Saudi Arabia, Qatar, Bahrain | Medium term (2-4 years) |

| Localization incentives for consumer electronics manufacturing | +1.5% | Egypt, Saudi Arabia, UAE, Kenya | Long term (≥ 4 years) |

| Rising health consciousness and fitness club memberships | +1.9% | GCC (UAE, Saudi Arabia, Qatar), urban centers in Turkey, South Africa, Kenya | Short term (≤ 2 years) |

| Mainstream adoption of AI-driven wellness analytics | +2.2% | Global, early gains in UAE, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of eSIM-Based LTE Smartwatches

Standalone connectivity is shifting watches from companion gadgets to independent communication tools. GCC operators activate eSIM profiles in minutes and increasingly bundle 12-month data plans with every LTE device. 5G RedCap pilots in Kuwait and the UAE have cut radio costs to below USD 20 per module and reduced power consumption by roughly 50%, making mid-range cellular models viable.[1]STC Kuwait, “Commercial 5G RedCap Service,” stc.com.kw Use cases move beyond fitness, enabling fall-detection alerts routed straight to emergency dispatch and remote glucose monitoring for diabetics. Government procurement also favors LTE watches for national tele-medicine pilots, ensuring sustained demand through 2031.

Rapid Expansion of Fintech-Enabled Wearable Payments

Banks across the region now embed tokenized debit credentials directly into watch operating systems. First Abu Dhabi Bank, Emirates NBD, and Boubyan Bank rolled out watch wallets between 2024 and 2025, after which contactless watch payments became table stakes at grocery stores and metro gates. Transaction-fee sharing allows banks to subsidize hardware, trimming the effective retail price of many mid-range models by up to 20%. This creates a positive flywheel: higher watch penetration yields more payment volume, which in turn funds deeper discounts and marketing spend.

Government-Led Digital-Health Initiatives in the GCC

Health ministries in the UAE and Saudi Arabia require interoperable personal health records that can ingest wearable device data. Abu Dhabi’s Population Health Intelligence digital twin, developed in collaboration with Microsoft in 2025, already consumes resting heart rate and SpO2 feeds from commercial devices. Public insurers increasingly reimburse certified wearables for chronic-disease management, positioning devices as reimbursable medical sensors rather than discretionary electronics. Vendors that secure local regulatory clearance win access to these high-volume tenders and subscription data contracts.

Mainstream Adoption of AI-Driven Wellness Analytics

Machine-learning models trained on multi-million-hour datasets bring medical-grade predictive insights onto the wrist. Roche’s Accu-Chek SmartGuide offers two-hour hypoglycemia forecasts with 99.8% accuracy, winning payer backing in Kuwait, Qatar, and Saudi Arabia.[2]Roche Middle East, “Accu-Chek SmartGuide Launch,” roche-middleeast.com Huawei’s TruSense quadruples on-device processing to deliver real-time stress assessment without cloud latency, helping it bypass strict data-localization statutes. The WHO’s updated 2025 digital health strategy explicitly endorses AI wearables for remote care, clearing the policy runway for mass adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy regulations limiting health data monetization | -1.4% | UAE, Saudi Arabia, South Africa, Egypt, Kenya | Medium term (2-4 years) |

| High import tariffs on finished wearables in key African markets | -1.7% | Kenya, Nigeria, Tanzania, Uganda, Ghana | Short term (≤ 2 years) |

| Battery-life limitations restricting medical certifications | -0.9% | Global, acute in markets pursuing FDA/CE medical device approvals | Long term (≥ 4 years) |

| Security vulnerabilities in low-cost Android clones | -1.2% | Africa (Nigeria, Kenya, Egypt), budget segments across Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Regulations Limiting Monetization

Federal Decree-Law 45 of 2021 in the UAE and Saudi Arabia’s Personal Data Protection Law require explicit opt-in consent for every secondary use of health data, thereby squeezing ad-supported business models.[3]UAE Government, “Federal Decree-Law No. 45 of 2021,” uae.gov.ae Cloud providers must host personal health records on in-country servers, pushing up infrastructure costs. As a result, brands that rely on analytics revenue now depend more heavily on hardware margins and subscription upgrades.

High Import Tariffs on Finished Wearables in Africa

Kenya’s 25% duty, 16% VAT, and assorted levies raise landed costs by more than half. Nigeria’s layered ECOWAS schedule is similarly punitive. Budget buyers tend to gravitate toward gray-market imports that evade customs, thereby limiting the growth of official channels. To restore competitiveness, Chinese OEMs have begun assembling in Egypt under a 10-year tax holiday, reducing ex-factory prices by 20-30%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: Ecosystem Lock-In Dictates Choice

The Middle East and Africa smartwatch market size for operating-system sales highlights WatchOS with a 52.31% share in 2025; however, HarmonyOS is forecast to post a 13.11% CAGR, the fastest rate among its rivals. Apple’s closed loop of hardware, cloud services, and healthcare partnerships secures loyalty among affluent iPhone owners, but its premium pricing leaves room for Huawei and Samsung. HarmonyOS gains traction by embedding Arabic and Swahili interfaces and striking profit-sharing deals with GCC telcos that preload apps for grocery, stock trading, and ride-hailing services. Android Wear OS appeals to open-ecosystem advocates, leveraging Google Wallet and a vast library of watch faces. Over the forecast window, no single platform is likely to exceed 60% dominance, ensuring a multi-OS landscape that favors cross-platform app developers.

Growing regulatory scrutiny over data sovereignty further shapes demand. Vendors that keep processing on the device, rather than the cloud, reduce compliance friction in Saudi Arabia and South Africa. As sensor arrays become more sophisticated, adding vendors that can push real-time analytics to the edge for cuffless blood-pressure and non-invasive glucose monitoring platforms will command higher average selling prices and lower churn, thereby strengthening ecosystem lock-in.

By Display Type: AMOLED Holds Volume, MicroLED Captures Sunshine

AMOLED delivered 68.19% of 2025 shipments, confirming its cost-performance sweet spot. The Middle East and Africa smartwatch market share for AMOLED hinges on its deep blacks and thin profile, as well as the requirements for always-on faces and bezel-less industrial design. Yet, the relentless summer sun in Riyadh and Dubai exposes OLED burn-in and forces maximum-brightness modes that significantly reduce battery life. Samsung’s forthcoming 2.1-inch MicroLED panel, rated at 4,000 nits, promises 33% brighter output at roughly half the power draw, unlocking seven-day endurance even with outdoor workouts.

Yield rates remain the principal bottleneck, so MicroLED will debut in USD 500-plus models before cascading into mid-range tiers by 2028. TFT LCD and PMOLED will retreat to rugged field watches, children’s trackers, and sub-USD 50 fitness bands. Vendors that couple MicroLED with adaptive-refresh firmware and ambient-light sensors will extend run-time without user input, a critical differentiator for hikers and oil-field workers operating far from chargers.

By Connectivity: Cellular Uptake Quickens With 5G RedCap

Bluetooth-only hardware still accounts for 59.24% of the 2025 unit volume, but the Middle East and Africa smartwatch market size tied to cellular watches is expanding at the fastest rate, driven by a 13.19% CAGR through 2031. STC Kuwait’s commercial RedCap service and Etisalat’s July 2024 trial module pricing, which is below USD 20, cushions bill-of-materials escalations. Operators sweeten the proposition with bundled data plans ranging from USD 5 to USD 8 per month, shaving 15-20% off the perceived upfront cost of devices like the Apple Watch Ultra 3 LTE.

In Africa, high data costs hinder uptake; nevertheless, Nairobi’s increasingly cashless matatu network and Lagos’s planned contactless rail program are encouraging users to adopt LTE variants that support tap-to-ride payments, even when the phone remains at home. Hybrid Bluetooth-Wi-Fi SKUs fill a middle ground, syncing workouts over household routers while skipping cellular fees, but their share will erode as data tariffs fall.

By Price Range: Budget Devices Unlock Mass Adoption

Mid-range models priced USD 200-399 delivered 47.33% of sales in 2025; yet, the under-USD 199 band is forecast to climb at a 12.93% CAGR through 2031, the highest segment CAGR. The Middle East and Africa smartwatch market size for budget devices thrives on localized software, such as M-Pesa in Kenya, Arabic keyboards in Egypt, and installment plans that mirror monthly mobile-money incomes. Transsion’s Oraimo line retails for USD 50-100 ex-factory, thanks to assembly in Cairo’s tax-free zone, undercutting imported counterparts by up to 30%.

Premium SKUs above USD 400 will still command outsize profit pools, particularly in the GCC, where titanium casings and sapphire glass satisfy status signaling. Yet absolute volume growth hinges on affordability. Vendors that partner with buy-now-pay-later services, such as Tabby and Tamara, will capture mid-income buyers who lack credit cards but possess stable salaries, thereby sustaining upward migration from fitness bands to smartwatches.

By Application: Medical Monitoring Becomes Growth Catalyst

Sports and fitness retained a 43.57% revenue share in 2025; however, medically validated applications are expected to post a 13.07% CAGR through 2031, surpassing leisure use in profit contribution. GCC insurers now reimburse AI-certified continuous glucose monitors, and Saudi Arabia’s Virtual Health Guide integrates atrial-fibrillation alerts directly from wearables into electronic health records. The Middle East and Africa smartwatch market size is closely tied to clinical use; therefore, it commands premium price points and often includes subscription add-ons, such as personalized coaching or remote physician consultations.

Vendors must juggle competing battery and regulatory requirements: always-on ECG sampling depletes cells within two days, yet FDA Class II certifications require sustained sensor accuracy over 14-day wear periods. Brands exploring solid-state lithium cells and RISC-V edge AI chipsets will be the first to clear that hurdle, capturing hospital tenders and corporate wellness contracts.

Geography Analysis

The Middle East generated 58.46% of 2025 smartwatch revenue, reflecting deep smartphone penetration, high discretionary incomes, and aggressive telco subsidies. A Deloitte 2025 survey found that 89% of respondents in the GCC intended to purchase a connected device within 12 months. UAE operators now activate eSIMs in under five minutes, while Saudi Arabia’s SDAIA uses watch data to feed its Genome Program. Turkey provides a secondary hub: although eSIM went live later than in the GCC, large urban centers now match Dubai in terms of gym membership density, fueling device upgrades.

Africa is forecast to log a 12.61% CAGR to 2031, the swiftest regional pace. Smartphone shipments across the continent reached 19.2 million in Q2 2025, up 7% year-over-year, laying the prerequisite foundation for watch pairing. Egypt’s 10-year tax holiday for electronics manufacturing persuaded Transsion to assemble Oraimo watches in Cairo, thereby bypassing Kenya’s 50-plus percent landed cost tariffs and unlocking duty-free exports under the African Continental Free Trade Area. South Africa continues to punch above its weight in premium sales, thanks to robust e-commerce and Apple Store rollouts, whereas Nigeria’s macroeconomic headwinds slow official channel growth, despite its vast addressable base.

A continental policy push is adding structural tailwinds. The Smart Africa Alliance blueprint mandates HL7-FHIR compliance for national health data exchanges by 2030, explicitly calling for the integration of devices. Rwanda’s “One Citizen One Record” law already enforces local hosting of medical data, making Kigali a test bed for cloudless on-device analytics. Markets that align with these standards earlier will secure donor funding and World Bank tele-health grants, accelerating public-sector deployment of entry-level watches.

Regulatory Landscape

Smartwatches sold across the Middle East and Africa face mandatory telecom equipment type approval when they include radios such as Bluetooth, Wi-Fi, NFC, LTE, or 5G. Key authorities include Saudi Arabia's Communications, Space and Technology Commission (CST) and the UAE's Telecommunications and Digital Government Regulatory Authority (TDRA), with similar pre-market regimes in Egypt (NTRA), Nigeria (NCC), Kenya (Communications Authority of Kenya, CA), and South Africa (ICASA). This creates a multi-jurisdiction compliance workload and makes market-entry sequencing a practical concern.

Regulation also extends into data governance and product safety for health and wellness use cases. The UAE's Federal Decree-Law No. 45 of 2021 and Saudi Arabia's Personal Data Protection Law tighten consent and localization requirements for health-related data flows, shaping on-device processing and in-country hosting choices. On the device side, Kenya updated technical specifications for mobile cellular devices sold in-country in March 2026 (covering safety, electromagnetic compatibility, radiation, and environmental requirements). Markets such as Nigeria and Kenya also apply product-conformity frameworks (e.g., SONCAP and PVoC), adding electrical and EMC certification steps alongside radio approvals.

Value Chain Analysis

The MEA smartwatch value chain is anchored in imported platforms. Core chipsets, sensors, batteries, and display modules are sourced primarily from Asian manufacturing hubs, while final assembly for most branded devices remains outside the region. Regional consolidation and re-export logistics also matter, with Dubai operating as a key distribution node for inbound inventory and onward supply into GCC retail and operator channels, as well as East and West African markets. This structure makes inventory planning around port clearance, last-mile distribution capacity, and the management of multiple SKUs more complex, especially given country-by-country certification and language requirements.

Downstream, go-to-market execution depends on a three-layer network of authorized distributors, carrier partners bundling eSIM/data plans for LTE models, and multi-brand retail and e-commerce platforms. Compliance gates recur across the chain, particularly for cellular-enabled watches, where requirements such as SAR testing and local type approval can delay launches. As a result, brands need to bring regulatory testing forward in the product readiness cycle. Local assembly initiatives in parts of the region, including the Egypt-supported electronics manufacturing incentives referenced in the report context, are increasingly used to reduce landed-cost pressure in tariff-heavy African markets and to support availability for budget and mid-range tiers.

Competitive Landscape

Apple and Samsung dominate the premium segment, accounting for nearly 40% of the region’s USD 400-plus market in 2025. Apple leverages its tightly coupled ecosystem, comprising iPhone, Mac, AirPods, and iCloud, to retain affluent users, while Samsung’s Galaxy Watch 8 and upcoming Galaxy Ring position it as the go-to Android alternative. Huawei, Xiaomi, OPPO, and Honor fracture the mid-range, competing on fitness features, localized apps, and operator bundles that knock USD 40-60 off sticker prices. In Africa, Transsion’s Oraimo brand claims a double-digit share by assembling locally and packaging M-Pesa quick-pay shortcuts.

White-space opportunities cluster around medical-grade wearables. Roche’s SmartGuide launch in October 2025 signaled insurers’ willingness to reimburse AI-validated devices, and smaller players like Masimo and Biobeat are targeting the hypertension and pulse oximetry niches. African assemblers, buoyed by tariff-free component imports, are poised to build bespoke disease-management watches that meet regional language and connectivity constraints.

Technology differentiation is moving up the stack. Huawei’s TruSense quadruples on-device AI throughput to comply with strict GCC data-localization statutes, while Apple’s December 2025 hypertension notifications place it inside physicians’ clinical guidelines. Vendors that can embed FIDO2 secure-element chips and Common Criteria firmware will win enterprise and government procurement as privacy concerns escalate.

Middle East And Africa Smartwatch Industry Leaders

Apple Inc.

Samsung Electronics Co. Ltd

Garmin Ltd

Huawei Technologies Co. Ltd

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Service-led localization stands out as a near-term whitespace lever, as smartwatches move from fitness accessories toward daily-utility endpoints that bundle payments, retail, mobility, and media. Huawei's ecosystem changes in 2025-2026 show how this can translate into product momentum: Majid Al Futtaim and Huawei launched a Carrefour smartwatch app in June 2025, Huawei and Anghami launched an app for HarmonyOS 5-powered smartwatches in July 2025, and Careem launched on Huawei AppGallery in February 2026 with stated intent toward smartwatch integration. These integrations create room for OEMs and developers to prioritize locally relevant use cases (grocery, ride-hailing, commuting, and Arabic-first experiences), which in turn supports operator or bank-led subsidy models already present in the GCC.

Clinical and public-sector workflows form a second opportunity cluster, supported by digital health mandates and stricter privacy regimes that favor on-device analytics and compliant data pathways. In the GCC, programs highlighted in the report context, including Abu Dhabi's Population Health Intelligence digital twin developed with Microsoft in 2025, show how wearable metrics feed population health tooling. At the same time, reimbursement momentum around validated sensors expands the addressable tender and insurer channel for medically oriented devices. In Africa, tariff and duty pressures documented in the report context (for example, Kenya's layered levies) keep affordability and local assembly central to scaling official channels, creating openings for regionally assembled, language-optimized devices that align with national type approval and product safety requirements.

Recent Industry Developments

- June 2026: Huawei announced availability of the HUAWEI WATCH Buds 2 in the UAE, combining a smartwatch with integrated wireless earbuds in a single wearable form factor. The launch expands the category beyond conventional watches into multi-device convergence, supporting higher ASPs and tighter ecosystem lock-in for users shopping in premium retail channels.

- July 2025: Huawei and Anghami launched the Anghami app for HarmonyOS 5-powered smartwatches, enabling music streaming directly from the wrist. The move strengthens localized content utility in GCC markets and reduces dependence on phone-tethered usage, which supports longer daily wear time and subscription-driven engagement.

- July 2024: Etisalat advanced early 5G RedCap activity referenced in the report context, helping bring trial module pricing below USD 20 and improving power efficiency for wearable radios. Lower radio cost and power draw directly improve the feasibility of mid-range cellular smartwatches and reinforce operator-led bundling strategies built around eSIM activation and data plans.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is defined as the value of smartwatches sold across the Middle East and Africa, covering devices that pair with smartphones or work with their own cellular connection, and including standard device revenue captured at the point of sale.

Scope exclusions: We exclude smart bands and other wrist wearables that are not positioned and sold as smartwatches, along with accessories such as straps and charging docks.

Segmentation Overview

- By Operating System

- WatchOS

- Android Wear OS

- HarmonyOS

- Other Operating Systems

- By Display Type

- AMOLED

- PMOLED

- TFT LCD

- MicroLED

- By Connectivity

- Bluetooth Only

- Cellular (LTE/5G)

- Hybrid (Bluetooth + Wi-Fi)

- NFC-enabled

- By Price Range

- Premium (Above USD 400)

- Mid-range (USD 200-399)

- Budget (Below USD 199)

- By Application

- Personal Assistance

- Medical

- Sports and Fitness

- Other Applications

- By Geography

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean fact base on device demand, connected-user readiness, and pricing direction across the region. We used public sources such as the International Telecommunication Union (ITU) for mobile and broadband indicators, World Bank macro and income series, national statistics portals and central bank releases for consumer spending signals, and customs or trade statistics where device import flows are visible.

To ground the market in real business activity, we also reviewed company filings, investor presentations, product launch notes, and reputable press coverage that tracks retail expansion and operator bundling. Patent databases were screened to understand which health and connectivity features are being emphasized, which then helped guide interview questions. For select company financial and news checks, we additionally referenced a paid subscription database for company intelligence and timelines. These desk sources are not exhaustive, and we relied on multiple public and paid references to collect data, cross-check it, and clarify assumptions.

Primary Interviews and Surveys

Primary work focused on validating demand drivers and pricing realities that are hard to read from public data alone, especially around LTE-enabled watches, medical and fitness use cases, and channel mix shifts. We spoke with a mix of device ecosystem participants, including brands, distributors, retailers, telecom-linked channels, and informed industry experts. We then used the feedback to adjust assumptions where the public signals showed wide variance.

Coverage was balanced across the Middle East and Africa so that high-income Gulf demand patterns and more price-sensitive African demand patterns were both represented in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | |

| Mid tier: 53% | Functional/Unit leaders: 35% | |

| Smaller Players: 20% | Managers: 49% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the regional demand pool was reconstructed from connected-device readiness and wearable adoption signals, then translated into smartwatch value using price-tier mixes. To keep the totals realistic, selective bottom-up approximations were used as a cross-check, such as sampled model price points multiplied by implied volumes from channel conversations and distributor sell-through direction.

Key inputs that shaped the model included smartphone user base and mobile network readiness, the share of watches sold with cellular capability versus Bluetooth-only, the premium versus budget price split, replacement cycle expectations, and how applications like sports and fitness and medical tracking are influencing purchase intent. Where country-level information was patchy, gaps were handled by applying conservative proxy ratios from similar markets in the region, then adjusting them based on primary feedback.

For forecasting, scenario analysis was used around pricing and feature adoption (for example, NFC and LTE penetration), followed by a simple multivariate regression check using macro indicators like income trends and connectivity growth to see if the trajectory remained consistent with the observed demand signals.

Data Validation & Update Cycle

Validation was done through step-by-step checks that compare the modeled output against independent signals, then isolate any outliers before sign-off. We rechecked unusual jumps by country using follow-up calls, refreshed price assumptions when new launches changed the visible price ladder, and reviewed the logic again when channel feedback suggested mix changes.

Each report is refreshed annually, and interim updates are triggered when material events occur, such as major policy moves tied to digital health, new connectivity rollouts, or sharp currency movement that changes average selling prices. Before delivery, a final analyst pass is completed so clients receive the latest updated view aligned to the same model structure.

Mordor Intelligence's Middle East and Africa Smartwatch Market Market Size Compared With Other Published Estimates

Published values for the Middle East and Africa smartwatch market often vary because the scope lines are drawn differently, and because pricing and feature adoption are handled in different ways. In practice, the gap usually comes from what gets counted as a smartwatch sale, what year is treated as the current baseline, and how fast ASPs are assumed to move across premium and budget tiers.

Accessories and add-on services sit outside Mordor Intelligence's scope, which reduces inflation from bundles that can look like device revenue when the channel reporting is not clean. Differences also show up when some estimates lean heavily on optimistic LTE and NFC adoption in early years, or when country coverage is simplified into a single regional average without checking the mix between Gulf markets and the rest of Africa.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.04 B (2026) | |

| Global Consultancy A | USD 1.31 B (2025) | Uses a different base year and often anchors MEA as a share of global revenue, which can understate fast-growing pockets where smartwatch pricing and feature adoption are moving quicker than the global average. |

| Regional Consultancy B | USD 4.60 B (2025) | The reported figure appears to apply a broader revenue definition or category mapping, and the segmentation language suggests possible overlap with non-smartwatch rollers-style categories, which can overstate the true smartwatch-only value. |

Overall, the spread is mainly explained by base-year selection and what revenue items are counted as part of the device market. By keeping inputs tied to observable adoption signals, price-tier mixes, and country-level reality checks, the estimate stays easier to trace and repeat when the market is updated.

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa smartwatch market by 2031?

It is expected to reach USD 3.63 billion, reflecting a 12.22% CAGR between 2026 and 2031.

Which connectivity option is growing fastest across the region?

Cellular LTE and 5G models are forecast to grow at 13.19% through 2031, driven by GCC 5G RedCap deployments and bundled data plans.

Why are medical applications attracting higher margins than fitness tracking?

Regulators in the UAE and Saudi Arabia now reimburse clinically validated devices, allowing vendors to upsell subscription services for chronic-disease management.

How do import tariffs affect smartwatch pricing in Africa?

Duties in Kenya and Nigeria can exceed 50% of landed cost, driving brands toward local assembly and encouraging consumers to buy gray-market imports.

Which display technology is set to gain share in premium watches?

MicroLED panels, offering 33% higher brightness and 50% lower power draw than OLED, are slated for commercial release in 2026.

What role do data-privacy laws play in vendor strategy?

Strict consent and localization requirements in GCC and South Africa force brands to process health data on-device and pivot toward subscription revenue instead of selling anonymized analytics.

Page last updated on: