Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

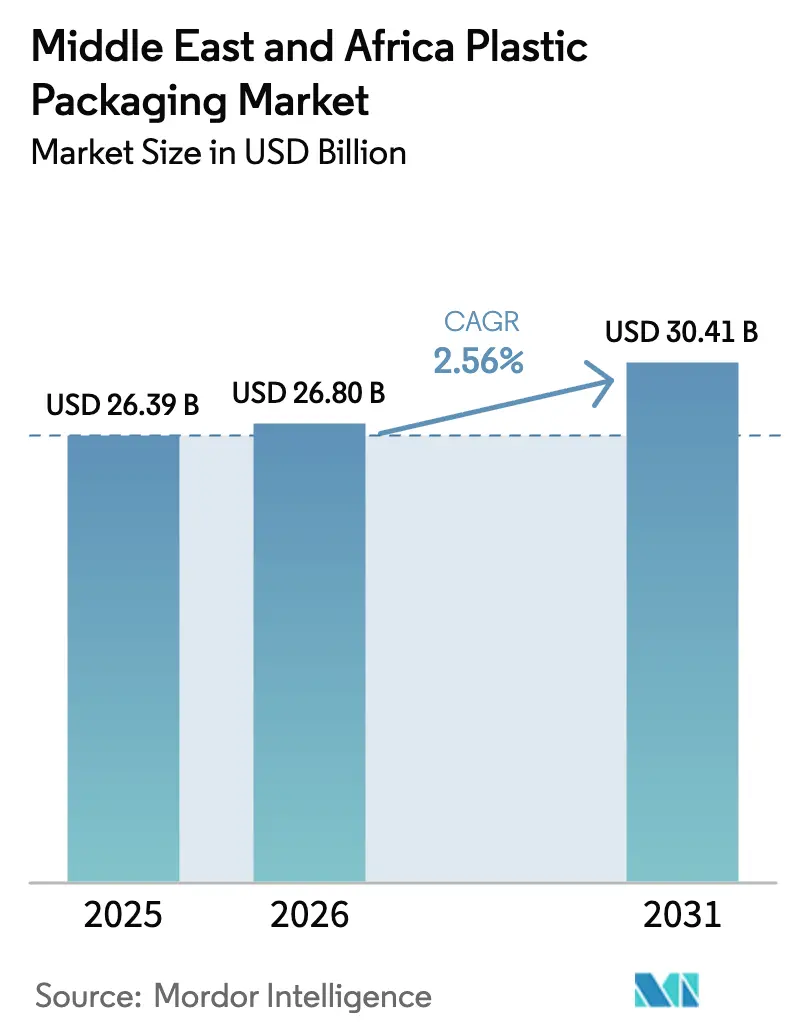

| Base Year Market Size (2025) | USD 26.39 Billion |

| Market Size (2026) | USD 26.80 Billion |

| Market Size (2031) | USD 30.41 Billion |

| Growth Rate (2026 - 2031) | 2.56% CAGR |

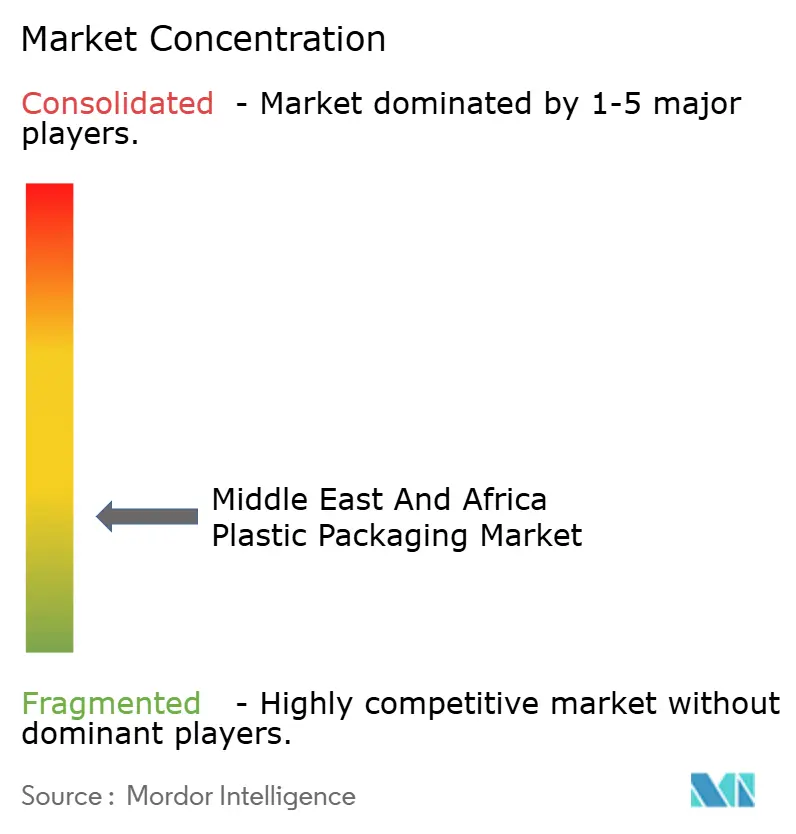

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Plastic Packaging Market Analysis by Mordor Intelligence

The Middle East and Africa plastic packaging market size is projected to expand from USD 26.39 billion in 2025 and USD 26.80 billion in 2026 to USD 30.41 billion by 2031, registering a CAGR of 2.56% between 2026 to 2031. Demand pivots toward lightweight formats for e-commerce, sovereign wealth funds finance large-scale recycling hubs, and Gulf regulators phase out single-use items, reshaping every link in the supply chain. Hot-fill beverages, premium cosmetics, and specialist healthcare lines favor polyethylene terephthalate (PET) due to its superior barrier properties, while polyethylene maintains volume leadership thanks to price advantages and converter familiarity. Flexible films, pouches, and flow-wrap formats gain ground at the expense of rigid bottles and jars as brand owners seek freight savings and lower carbon intensity. Multilayer coextrusion and digital printing enable converters to differentiate on the shelf without increasing material usage, and food-safety regulations in Saudi Arabia and the United Arab Emirates drive the adoption of high-barrier films.

Key Report Takeaways

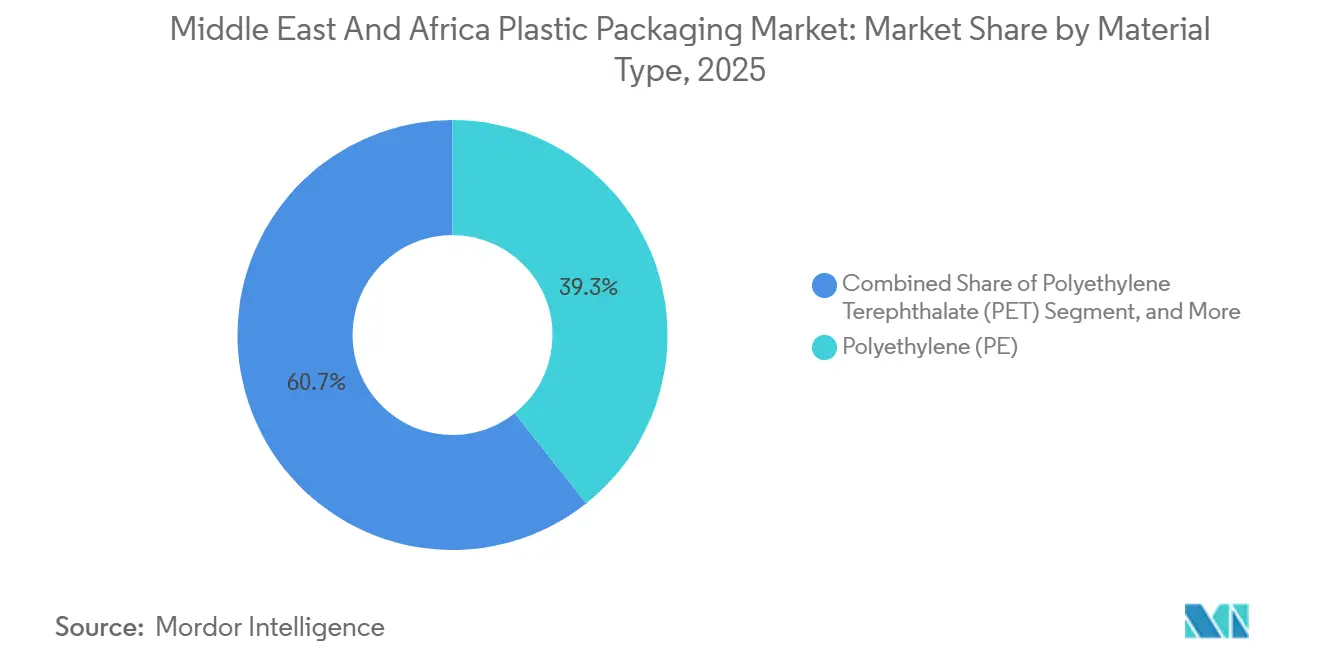

- By material, polyethylene captured 39.32% of Middle East and Africa plastic packaging market share in 2025, while PET is set to grow at a 3.56% CAGR through 2031.

- By packaging type, flexible formats accounted for 55.62% of Middle East and Africa plastic packaging market and are forecast to expand at a 3.87% CAGR through 2031.

- By product form, pouches and sachets accounted for 31.32% of demand in 2025, whereas films and wraps are poised to grow at the fastest rate, with a 4.22% CAGR to 2031.

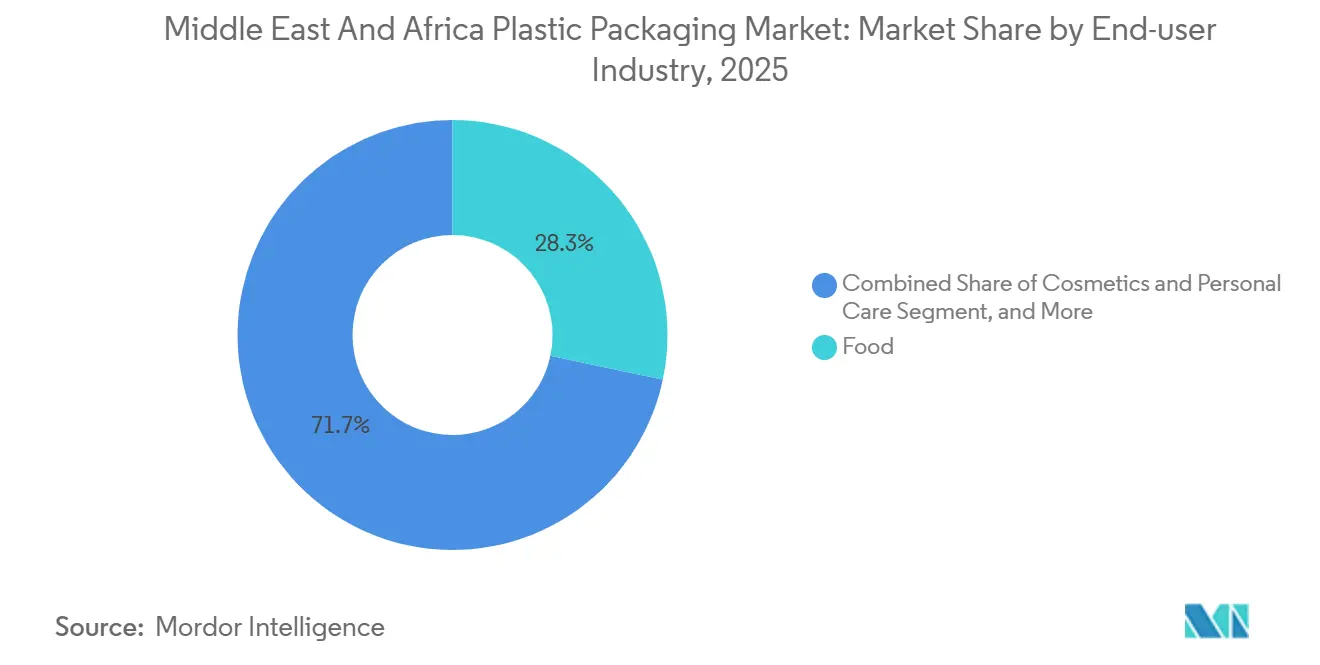

- By end-user industry, food retained 28.32% of the Middle East and Africa plastic packaging market in 2025, yet cosmetics and personal care are projected to accelerate at a 4.32% CAGR through 2031.

- By manufacturing process, extrusion represented 28.14% of activity in 2025 and is expected to rise at a 3.67% CAGR through 2031.

- By geography, the Middle East commanded 68.32% of 2025 sales and Africa is predicted to register a 3.45% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Oxo-Degradable Plastics | +0.3% | Gulf Cooperation Council states, South Africa | Medium term (2-4 years) |

| Steady Rise in Demand for Processed Food | +0.6% | Saudi Arabia, United Arab Emirates, Egypt, Nigeria, South Africa | Long term (≥ 4 years) |

| Accelerating Growth of E-Commerce Fulfilment Packaging | +0.7% | United Arab Emirates, Saudi Arabia, Egypt, Nigeria, Kenya | Short term (≤ 2 years) |

| Expanding Regional Healthcare Infrastructure | +0.4% | Saudi Arabia, United Arab Emirates, Egypt, Nigeria | Medium term (2-4 years) |

| Sovereign Wealth-Fund Backing for Recycling Capacity | +0.5% | Saudi Arabia, United Arab Emirates, Qatar, Kuwait | Long term (≥ 4 years) |

| Adoption of High-Barrier Films for Hot-Fill Beverages | +0.4% | Saudi Arabia, United Arab Emirates, Egypt, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Steady Rise in Demand for Processed Food

Urban migration, rising dual-income households, and climate-driven food-safety concerns lift demand for hermetically sealed, portion-controlled grocery lines across the region. Supermarket chains shift shelf space from loose staples to pre-packed meats, dairy, and snacks, pulling through multilayer barrier films that extend shelf life under 40 °C ambient temperatures.[1]Food and Agriculture Organization, “Food Outlook 2024,” fao.org Saudi Arabia already approaches Western European packaged-food consumption benchmarks, while Nigeria’s penetration lags below 15%, indicating significant headroom for new capacity. Converters respond with modified-atmosphere sachets and vacuum-skin trays that curb spoilage and shrink in-store waste. As distribution networks reach second-tier cities, small-format pouches allow retailers to balance affordability with hygiene, reinforcing adoption of flexible plastic solutions within the Middle East and Africa plastic packaging market.

Accelerating Growth of E-Commerce Fulfilment Packaging

Online retail expanded at 30% in 2024 and continues to outpace other channels, driven by consumers under 35 who dominate the Gulf workforce. Fragile supply routes that involve bumpy roads or multiple hand-offs increase breakage risk, pushing logistics operators to over-specify cushioning layers. Lightweight flow-wraps, air pillows, and stretch films safeguard orders without unduly raising freight costs, deepening penetration of plastics in last-mile distribution. Nigerian e-commerce alone is expected to add USD 5.71 billion in sales between 2023 and 2028, translating into millions of additional parcels that demand protective films and bubble mailers. Quick-commerce platforms in Dubai and Riyadh introduce a parallel stream for temperature-controlled shipments, spurring uptake of expanded polystyrene liners and vacuum panels. These dynamics collectively underpin above-average volume growth for the Middle East and Africa plastic packaging market.

Sovereign Wealth-Fund Backing for Recycling Capacity

Saudi Arabia’s Public Investment Fund created Saudi Investment Recycling Company to divert 82% of waste from landfills by 2035, allocating SAR 37 billion to new plants and collection systems. Development financiers reinforce the trend; the International Finance Corporation provided USD 37 million to the Mohinani Group for PET reprocessing sites in Ghana and Nigeria, demonstrating that circular-economy assets meet commercial hurdle rates.[2]Graphic Online, “Mohinani Group and IFC Sign Agreement to Recycle Plastic Waste,” graphic.com.gh Brand owners pay price premiums for recycled content to meet voluntary pledges and comply with emerging quotas, improving project economics. As sorting and washing capacity scales, mechanically recycled pellets feed back into bottles, films, and strapping, gradually closing material loops within the Middle East and Africa plastic packaging market.

Expanding Regional Healthcare Infrastructure

Vision 2030 reforms target 3.2 hospital beds per 1,000 residents in Saudi Arabia by 2030, triggering construction of clinics and specialized centers that utilize sterile blisters, surgical drapes, and diagnostic pouches. The United Arab Emirates upgrades oncology facilities that need gamma-stable polyethylene and polypropylene films validated under ISO 11607. Borouge commercialized a medical-grade low-density polyethylene in 2024 that withstands irradiation without discoloration, offering local substitutes for imported resins. Nigeria’s push for local drug manufacturing adds filling lines that depend on high-clarity PET vials and foil-laminated blister webs. The healthcare boom, therefore, channels steady, specification-sensitive demand into the Middle East and Africa plastic packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Concerns Over Recycling and Safe Disposal | -0.4% | Global pressure, acute in Gulf states and South Africa | Medium term (2-4 years) |

| High Raw-Material Costs and Limited Recycling Infrastructure | -0.5% | Sub-Saharan Africa, Egypt, smaller Gulf states | Short term (≤ 2 years) |

| Emerging Gulf Single-Use Plastic Bans | -0.6% | United Arab Emirates, Saudi Arabia, Qatar, Bahrain | Short term (≤ 2 years) |

| Currency Volatility Impacting Polymer Resin Imports | -0.3% | Egypt, Nigeria, Kenya, Ghana | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emerging Gulf Single-Use Plastic Bans

The United Arab Emirates enforces Federal Decree-Law 36 of 2024, prohibiting single-use bags, cutlery, and straws from January 2026, with escalating fines through 2028. Saudi Arabia signals similar intent under its Green Initiative, though timelines remain fluid, generating investment uncertainty for converters. Compostable resin supply is nascent and priced 40% above conventional polyethylene, raising cost barriers for smaller firms. The possibility of asset write-offs on extrusion and injection lines tuned for single-use products threatens margins. Nonetheless, bans catalyze portfolio pivots toward reusable or certified-recyclable formats, ultimately embedding higher specification standards across the Middle East and Africa plastic packaging market.

High Raw-Material Costs and Limited Recycling Infrastructure

Currency depreciation magnifies feedstock price swings; Egypt’s pound slide in 2024 lifted imported polyethylene costs by nearly 30% in local terms, squeezing converter profitability. Sub-Saharan African converters pay a premium of up to 20% for resins compared to their integrated Gulf peers, reflecting smaller order volumes and inland freight surcharges. The food-grade recycled PET capacity stands at below 5% of regional demand, forcing brand owners to import or downcycle the material. The resulting supply deficit limits the adoption of recycled-content mandates and raises compliance risk. Volatile inputs foster hand-to-mouth purchasing, undermining scale efficiencies and capping investment appetites within the Middle East and Africa plastic packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: PET Gains on Barrier and Recyclability Mandates

Polyethylene holds a 39.32% market share in the Middle East and Africa plastic packaging market in 2025, driven by its cost advantages and versatility across blown-film, injection, and rotational molding operations. Linear low-density polyethylene dominates the stretch-wrap and shrink-film segments that secure pallets traveling on dusty highways, while high-density polyethylene leads the way in detergent and lubricant bottles, which require chemical resistance. Polypropylene remains attractive for closures and woven sacks, particularly as tethered-cap regulations gain traction, although its recycling pathways lag behind those of PET. PET is forecast to expand at a 3.56% CAGR, surpassing the overall Middle East and Africa plastic packaging market. Indorama Ventures launched a lightweight PET bottle in 2024 that reduces preform mass by 15% while maintaining top-load strength, thereby lowering resin use and freight emissions. Hot-fill beverage lines prefer PET because it withstands 85 °C pasteurization without warping, unlike polyethylene. Extended producer responsibility schemes in South Africa and Kenya impose steeper fees on non-recyclable formats, prompting brand owners to shift toward PET.

Polyethylene’s resilience rests on local feedstock from Saudi petrochemical giants, ensuring timely supply and price leverage. Polypropylene benefits from growing demand for injection-molded reclosable lids in dairy and coffee. Polystyrene’s niche covers insulated food containers and protective cushioning, yet regulators scrutinize its micro-fragmentation tendencies. Meanwhile, mono-material PET lidding films enter ready-meal trays to improve recyclability. As recycled-content quotas tighten, converters weigh the security of captive polyethylene supply against end-market preference for PET circularity. This competitive interplay keeps both polymers central to the Middle East and Africa plastic packaging market, even as PET captures incremental growth.

By Packaging Type: Flexible Formats Capture E-Commerce and Portion-Control Demand

Flexible packaging commanded 55.62% share in 2025 and is projected to record a 3.87% CAGR, reflecting its weight efficiency and low shipping footprint. Stand-up pouches reduce landfill volumes and cut transportation emissions in half compared to glass jars, an attribute that retailers' marketing eco-scores leverage heavily. Huhtamaki rationalized its United Arab Emirates sites in 2024 to pool five-layer coextrusion assets, signaling a race toward higher throughput and thinner gauges.[3]Huhtamaki, “Flexible Packaging Operations and Capabilities,” huhtamaki.com Rigid containers maintain relevance in sauces, spreads, and household cleansers where controlled dispensing and tactile branding influence purchase decisions. Nonetheless, the rising demand for courier shipments of cosmetics sachets, nutraceutical powders, and meal kits amplifies the need for flow-wraps and mailer films. The Middle East and Africa plastic packaging market size for flexible formats will, therefore, remain on an expansion path relative to rigid counterparts.

Rigid solutions still dominate beverages, yogurts, and vitamins, where shelf impact and tamper evidence are critical. Injection stretch blow moulding of PET bottles ensures clarity and crack resistance, particularly important for premium juices sold across the Gulf’s travel retail channel. Blow-molded high-density polyethylene jerrycans secure agrochemicals and motor oils that require UN-certification for hazardous goods. Hybrid designs blur boundaries; paperboard sleeves bonded to thin polyethylene liners give brand owners improved stiffness and printability without compromising recyclability. The dual strategy allows converters to safeguard margins while meeting opposing pressures of regulatory compliance and consumer convenience.

By Product Form: Films and Wraps Accelerate on Logistics and Sustainability Pressures

Pouches and sachets are projected to hold a 31.32% stake in 2025, targeting condiments, beverages, and shampoo dose packs aimed at low-income consumers. Yet, small-format litter concerns trigger retailer mandates for recyclable mono-material films, which constrain growth. Bottles and jars retain their dominance in carbonated soft drinks because aluminum and glass still outperform plastics in terms of barrier criteria. Trays and containers service chilled meats and ready meals, though some lines switch to vacuum pouches to pare material weights by up to 70%. Films and wraps are expected to register a 4.22% CAGR through 2031, emerging as the pace-setting product form. Stretch-film formulations utilize metallocene catalysts to achieve 20-micron gauges without tearing, allowing for pallet stability with minimal resin usage. High-clarity flow-wrap encloses bakery goods, extending freshness during interstate distribution from Riyadh to Jeddah.

The Middle East and Africa plastic packaging market size for films and wraps is projected to widen as automated palletization gains ground in Egyptian and South African distribution centers. Retailers demand thinner stretch hoods compatible with high-speed lines to prevent bottlenecks. Conversely, multilayer pouches fight for regulatory breathing space; most waste-management systems lack sorting technology for metallized laminates. Converters experiment with high-barrier polyethylene films that forgo aluminum, but shelf-life sacrifices limit adoption in long-haul export SKUs. Bottles leverage deposit-return systems in South Africa to sustain high recovery rates, proving recyclability advantages against sachets. Ultimately, films and wraps rise fastest because they supply efficiency gains without requiring wholesale changes to consumer use behavior.

By End-User Industry: Cosmetics and Personal Care Lead Growth on Premiumization

Food retains the largest revenue share at 28.32% in 2025, encompassing snacks, dairy, and ambient sauces; however, growth moderates as Gulf markets mature. Beverage packaging is migrating from glass to PET, driven by the lightweight benefits and shatter resistance, particularly on pilgrimage routes with strict safety protocols. The demand for cosmetics and personal care is forecast to grow at 4.32% through 2031, driven by young, affluent Gulf consumers who associate sophisticated packaging with product efficacy. Airless pumps, metallized closures, and velvet-surface films command price premiums that brands pass through to shoppers eager for curated aesthetics. McKinsey projects that the Middle East and North Africa beauty sector will reach over USD 60 billion by 2030, with Saudi Arabia contributing nearly USD 13.4 billion. Such momentum tilts converter portfolios toward injection-molded compacts, PETG bottles, and ultraviolet-blocking labels.

Pharmaceutical uptake tracks hospital investment; blister packs, IV solution bags, and sterile barrier pouches rely on ISO-certified cleanrooms that many African converters are now building with European technical partners. Industrial use cases, including lubricants and fertilisers, demand blow-molded drums that must endure 1.2-meter drop tests, a segment insulated from single-use bans. Agriculture absorbs woven polypropylene sacks for grain, while electronics importers deploy anti-static films for semiconductor boards transiting Jebel Ali free-zone. The diversity of end-use keeps the Middle East and Africa plastic packaging market resilient against cyclical swings in any single vertical.

By Manufacturing Process: Extrusion Dominates on Versatility and Capital Efficiency

Extrusion accounted for 28.14% of activity in 2025 and is predicted to rise at a 3.67% CAGR. A single blown-film line can toggle between die configurations to produce shrink sleeves during the day and stretch hoods at night, maximizing utilization. Huhtamaki’s South African five-layer line pushes 900 kilograms per hour, matching European benchmarks and confirming that capital, not capability, is the gating factor. Injection molding advances with all-electric presses that reduce cycle times for closures built to meet tether-cap legislation. Blow molding is divided into extrusion blow molding for commodity bottles and injection stretch blow molding for premium PET applications that require optical clarity. Thermoforming services produce trays and cups at lower mold costs, making them appealing to new entrants seeking rapid payback.

Energy tariffs shape geography; Egyptian converters pay double the Gulf average per kilowatt-hour, eroding competitiveness in extrusion and blow molding of heavy formats. West African operators compensate with lower wages but face grid instability, prompting firms to install diesel generators that add to their overhead. Automation is gaining traction as Saudi plants adopt automated material-feed systems, which trim labor and resin losses. Digital twin software enters maintenance schedules, predicting screw wear and preventing downtime. These process-level changes underpin productivity gains that help the Middle East and Africa plastic packaging market absorb input-cost volatility without wholesale price inflation.

Geography Analysis

Saudi Arabia, the United Arab Emirates, and Qatar together controlled 68.32% of 2025 regional revenue, underpinned by abundant feedstock and state-led downstream diversification. Saudi Arabia’s Public Investment Fund has earmarked SAR 37 billion for recycling infrastructure, spanning material recovery facilities and chemical depolymerization units. Hotpack Packaging Industries pledged SAR 1 billion for a mega complex in Riyadh and AED 250 million for a PET plant in Dubai, illustrating how family-owned groups match multinational investments to secure local supply. The United Arab Emirates’ single-use prohibition starting 2026 compels converters to diversify into reusable and compostable offerings, compressing product-development timelines. Smaller Gulf states benefit from customs unions and duty-free re-export networks that funnel raw materials and finished goods through Jebel Ali and Hamad ports, sustaining economies of scale in regional converting hubs.

Africa, forecast to post a 3.45% CAGR through 2031, offers the higher growth runway. Egypt attracted USD 200 million from UFlex for PET resin and aseptic packaging lines, targeting a 12 billion pack capex, positioning the Suez Canal Economic Zone as a gateway to European customers. Nigeria’s e-commerce boom lifts demand for bubble mailers and stretch wraps, yet imported resin premiums curb competitiveness. Coca-Cola Nigeria opened a 13,000-tonne PET collection hub, demonstrating brand owner willingness to seed recycling ecosystems. South Africa leads mechanical recycling with Alpla’s 35,000-tonne food-grade PET plant feeding both domestic and export markets.

Sub-Saharan markets face power outages, poor road links, and currency swings that discourage high-spec installations, tilting demand toward ambient-stable sachets and woven sacks. Still, demographic dividends attract converters willing to absorb risk for first-mover advantage. Gulf petrochemical cost leadership will preserve the Middle East’s numeric dominance, yet Africa’s consumption expansion should deliver a growing portion of incremental Middle East and Africa plastic packaging market revenue over the forecast horizon.

Competitive Landscape

The Middle East and Africa plastic packaging market exhibits fragmentation. Alpla deepened its footprint by fully acquiring its Egyptian plant in December 2024 and purchasing a stake in Taba Plastic Industries in January 2025, prioritizing density over greenfield investment. Huhtamaki consolidated its United Arab Emirates sites to sharpen asset utilization amid intensifying flexible-pack competition, underscoring the premium on scale economies. Local champions counter through vertical integration; Hotpack’s twin projects in Riyadh and Dubai secure PET preform and film capacity, sheltering it from feedstock fluctuations. Certification to BRC, ISO 22000, and HACCP remains a gatekeeper for multinational fast-moving consumer goods contracts, and smaller converters struggle to fund audits, hindering entry.

Recycled resin supply is a white-space opportunity. International Finance Corporation financing for Ghana and Nigeria PET plants adds 30,000 tonnes but covers less than 5% of demand, leaving room for new entrants. Technology differentiators emerge in multilayer film recipes and digital print runs that reduce minimum order quantities, appealing to direct-to-consumer beauty labels searching for bespoke packaging.

Saudi petrochemical producers such as SABIC and Borouge provide home-field advantage through cost-plus resin deals, anchoring their captive converters in the low quartile of the global cost curve. Currency controls and import tariffs protect fledgling African firms, yet the absence of scale leaves them vulnerable when domestic demand softens, reinforcing consolidation trends within the Middle East and Africa plastic packaging market.

Middle East And Africa Plastic Packaging Industry Leaders

Zamil Plastic Industries Co.

Huhtamaki South Africa (Pty) Ltd

Takween Advanced Industries

Napco National

Constantia Flexibles Afripack

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Beyti inaugurated an EGP 1 billion (USD 240 million) expansion, unveiling Egypt’s first ultra-high-temperature milk line in PET bottles.

- October 2025: OQ’s Ladayn Programme in Oman received USD 220 million in commitments across 26 agreements, with nine advanced polymer firms starting production.

- October 2025: Egypt launched a national beverage-carton recycling campaign alongside Tetra Pak and Uniboard, backed by a EUR 2.5 million (USD 2.8 million) line rated at 8,000 tonnes per annum.

- May 2025: Saudi Investment Recycling Company and EIG Management Company signed a memorandum of understanding to deploy USD 375 million in refuse-derived fuel plants and USD 250 million in tire-pyrolysis units.

Middle East And Africa Plastic Packaging Market Report Scope

Plastic packaging is an integral part of the multifaceted system for providing products, from manufacture to consumption. Its principal purpose is to ensure the safe and secure delivery of the product in flawless and perfect condition to the end user (either the manufacturer of the product or the consumer). Its role in a circular economy is to sustain the value of a product for as long as required and to help remove product waste.

The Middle East and Africa Plastic Packaging Market Report is Segmented by Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene and EPS, and Other Material Types), Packaging Type (Flexible, and Rigid), Product Form (Bottles and Jars, Trays and Containers, Pouches and Sachets, Bags and Sacks, Films and Wraps, and Other Product Forms), End-User Industry (Food, Beverage, Pharmaceuticals and Healthcare, Cosmetics and Personal Care, Industrial, and Other End-user Industries), Manufacturing Process (Extrusion, Injection Molding, Blow Molding, Thermoforming, and Other Manufacturing Processes), and Country. The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Other Manufacturing Processes |

By Region

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Material Type | Polyethylene (PE) | |

| Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | ||

| Polystyrene and EPS | ||

| Other Material Types | ||

| By Packaging Type | Flexible Plastic Packaging | |

| Rigid Plastic Packaging | ||

| By Product Form | Bottles and Jars | |

| Trays and Containers | ||

| Pouches and Sachets | ||

| Bags and Sacks | ||

| Films and Wraps | ||

| Other Product Forms | ||

| By End-User Industry | Food | |

| Beverage | ||

| Pharmaceuticals and Healthcare | ||

| Cosmetics and Personal Care | ||

| Industrial | ||

| Other End-user Industries | ||

| By Manufacturing Process | Extrusion | |

| Injection Molding | ||

| Blow Molding | ||

| Thermoforming | ||

| Other Manufacturing Processes | ||

| By Region | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa plastic packaging market in 2031?

The market is forecast to reach USD 30.41 billion by 2031, growing at a 2.56% CAGR.

Which packaging type is expected to expand the quickest through 2031?

Flexible formats, including pouches and flow-wrap films, are projected to advance at a 3.87% CAGR, outpacing rigid alternatives.

Why is PET gaining share within regional material demand?

PET combines hot-fill compatibility, high clarity, and established recycling streams, enabling brand owners to meet performance needs and recycled-content pledges.

How will Gulf single-use plastic bans affect converters?

The bans compel a pivot toward reusable, recyclable, or compostable designs, pressuring firms to invest in new materials and retool existing lines before 2028.

What growth opportunities exist for investors in the sector?

Food-grade recycled PET capacity, multilayer high-barrier film production, and e-commerce fulfilment packaging all present under-served niches with attractive demand trajectories.

How concentrated is the supplier landscape?

With the top five converters holding roughly 35% of revenue, the market remains moderately fragmented, allowing room for consolidation plays and specialist entrants.

Page last updated on: