Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Paper Packaging Market Analysis by Mordor Intelligence

Egypt paper packaging market size in 2026 is estimated at USD 2.06 billion, growing from 2025 value of USD 1.98 billion with 2031 projections showing USD 2.52 billion, growing at 4.05% CAGR over 2026-2031. Expansion stems from Egypt’s role as a regional manufacturing hub, the rising importance of cost-effective paper solutions in the total cost of goods sold, and the government’s growing incentives for export-oriented, recyclable fiber packaging.[1]Interpack Magazine, “The Resilient Rise of the Egyptian Packaging Sector in Challenging Times,” interpack.com Rapid e-commerce adoption accelerates demand for corrugated formats, while sustainability regulations and record electricity tariffs prompt manufacturers to shift toward energy-efficient, fiber-based alternatives. Supply-chain shocks linked to Red Sea disruptions have increased freight costs, yet strategic port modernization and rebate programs continue to attract new investments in molded fiber and recycling capacity.

Key Report Takeaways

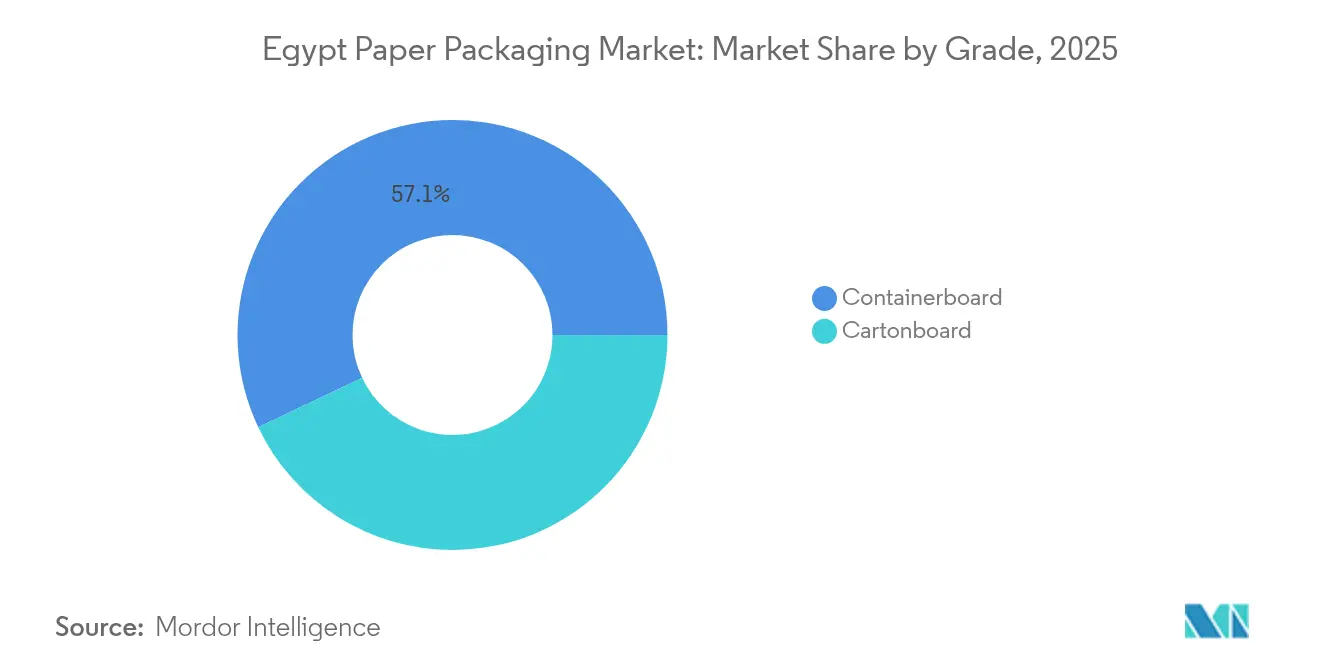

- By grade, containerboard held 57.05% of the Egypt paper packaging market share in 2025, while cartonboard is advancing at a 6.03% CAGR between 2026 and 2031.

- By product, corrugated boxes accounted for 30.10% share of the Egypt paper packaging market size in 2025; folding cartons are projected to grow at 5.86% CAGR between 2026 and 2031.

- By end-user, the food sector led with a 42.20% share of the Egypt paper packaging market in 2025, while the healthcare packaging sector is expected to expand at a 5.72% CAGR between 2026 and 2031.

- By packaging format, rigid solutions captured a 51.55% Egypt paper packaging market share in 2025; molded fiber and pulp are forecast to record a 5.78% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for sustainable packaging | +1.2% | National – major early gains in Cairo, Alexandria, Giza | Medium term (2-4 years) |

| Growth of Egypt’s food and beverage processing sector | +1.8% | National – Delta region, Upper Egypt | Long term (≥4 years) |

| Expansion of e-commerce driving corrugated demand | +0.9% | Urban centers, secondary cities | Short term (≤2 years) |

| Government export incentives for recyclable fiber packs | +0.7% | Export corridors – Red Sea, Mediterranean ports | Medium term (2-4 years) |

| Beverage-carton recycling capacity coming on-stream | +0.3% | Sadat City hub, national roll-out | Long term (≥4 years) |

| Smart, trace-and-trace paper packs for pharma exports | +0.4% | Cairo pharmaceutical cluster, export pathways | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Sustainable Packaging

Egypt’s first domestic cardboard recycling line commenced operations in December 2024, providing essential circular-economy infrastructure and signaling strong government backing for greener materials. Hypermarket chains distributed 4,500 reusable bags to phase out single-use plastics, amplifying public awareness and accelerating retailer commitment to fiber-based options. Extended Producer Responsibility rules under Law 202 of 2020 oblige packaging suppliers to finance collection and recycling, creating cost-advantage opportunities for local mills that leverage agricultural waste such as sugarcane bagasse. Research confirms that plates molded from bagasse meet stringent food-contact guidelines, increasing confidence among quick-service restaurants seeking compostable alternatives. The target of raising national waste-collection rates to 95% by 2025 further expands fiber recovery volumes and encourages fresh investments in molded-pulp capacity.

Growth of Egypt’s Food and Beverage Processing Sector

Egypt’s packaged-food spending increased by 35% in 2024 to EGP 4 trillion (USD 89.5 billion) and is forecast to reach USD 125.4 billion by 2028, underpinning sustained demand for corrugated and folding cartons. Fresh produce exports worth USD 1.7 billion a year require rigid crates and humidity-resistant liners to protect citrus and grapes on maritime routes to the United Kingdom, Netherlands and Saudi Arabia. Tax exemptions for new processing lines foster domestic manufacturing, while African Continental Free Trade Area tariff cuts of up to 90% open new regional markets for Egypt-sourced packaged snacks and juices. Mobile-commerce platforms boost single-serve orders, prompting brand owners to shift toward portion-controlled folding cartons that withstand rapid-cycle logistics. Collectively, these factors accelerate the expansion of carton and kraftliner capacity across Delta industrial zones and Upper Egypt's agrarian belts.

Expansion of E-commerce Driving Corrugated Demand

Egypt’s online retail user base has surged on the back of a USD 25 billion Middle East and Africa e-commerce pipeline expected by 2027, placing immediate stress on last-mile delivery and packaging. A Damietta-Trieste Ro-Ro service now cuts Mediterranean shipping days from six to 2.5 and slashes port fees by 88%, enabling e-commerce merchants to shorten replenishment cycles and standardize corrugated dimensions for automated sortation. Demand has shifted toward lightweight, tamper-evident shippers featuring tear strips and QR codes that streamline returns and enhance traceability. Quick print-run digital presses have gained prominence in Cairo fulfillment centers, promoting brand personalization while maintaining tight turnaround times. The net result is an escalating consumption of B-flute and E-flute board grades, which are tailored for direct-to-consumer delivery boxes.

Government Export Incentives for Recyclable Fiber Packs

The EGP 45 billion export rebate program, launched in June 2025, accelerates investment in recyclable paper packaging by guaranteeing 90-day reimbursement and linking payouts to energy-efficiency metrics. Projects in Upper Egypt receive an extra five-year tax holiday, catalyzing mill expansions that utilize local straw fiber and reduce import dependency. The Export Development Support Fund increases incentives by 2% for small converters that achieve 40% local value-added thresholds, driving equipment upgrades in folding-carton and corrugated plants. Improved customs digitization at Port Said and Sokhna ports has shortened clearance times, prompting global brand owners to source printed cartons locally. The collective effect bolsters Egypt's paper packaging market growth by reducing export friction and incentivizing the adoption of sustainable fibers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile global pulp and paper raw-material prices | -1.4% | Import-dependent regions nationwide | Short term (≤2 years) |

| Low-cost plastic substitutes intensifying competition | -0.8% | Urban, price-sensitive segments | Medium term (2-4 years) |

| Red Sea shipping disruptions raising freight costs | -0.6% | Export corridors – Suez Canal, Port Said, Sokhna | Short term (≤2 years) |

| Higher industrial electricity tariffs after subsidy removal | -0.5% | Nationwide – energy-intensive mills | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Global Pulp and Paper Raw-Material Prices

Packaging costs rose 45% year-on-year in 2024 as Northern Bleached Softwood Kraft pulp prices spiked 11% and freight surcharges climbed 256% following Red Sea shipping disruptions. Egypt imports 78% of its paper needs, exposing converters to currency swings and congested container lanes. Electricity tariffs now stand at 160-194 piastres per kWh after the removal of subsidies, adding up to 12% to mill operating expenses. The state further spent USD 3 billion on gas imports in the first half of 2025, pushing grid costs higher and pressuring energy-intensive kraftliner production in MANASSA. Smaller box makers with thin margins struggle to hedge pulp volatility, which slows capacity additions and stalls the expansion of the Egyptian paper packaging market.

Low-cost Plastic Substitutes Intensifying Competition

Plastic alternatives are projected to reach USD 226.2 million by 2026, growing at a 10% annual rate and undercutting paper solutions in price for snacks, beverages, and personal-care sachets. Life-cycle assessments reveal that paper packs often lag behind plastics in eutrophication and water-use metrics, unless reuse rates climb above four times, challenging the sustainability marketing of fiber formats. Limited municipal recycling at 15.9% of waste collected dampens circularity claims for paper, while plastics makers introduce bio-based resins and mono-material laminates that enhance their environmental positioning. Consequently, brand owners in cost-sensitive categories retain low-density polyethylene pouches, restricting substitution potential for Egyptian paper packaging industry suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Containerboard Holds the Lead on Industrial Backbones

Containerboard generated over half of Egypt's paper packaging market revenue in 2025, its 57.05% share driven by corrugated case requirements for cement, fertilizers, and fruit exports. Within this grade, Kraftliner caters to heavy-duty export crates, while Testliner serves domestic FMCG boxes where cost efficiency prevails. White-top variants command higher margins among appliance brands seeking bright print surfaces in Cairo hypermarkets. Cartonboard is the fastest-rising grade and is projected to log a 6.03% CAGR, driven by the demand for folding boxboard with precise color fidelity in pharmaceutical blister cartons and premium confectionery packs. Solid Bleached Sulfate boards also gain traction due to stringent child-resistant packaging rules for syrups and ointments bound for European pharmacies.

Cartonboard’s ascendancy reflects Egypt’s pivot toward value-added exports. Healthcare firms in 6th of October City require tamper-verifiable cartons complete with data-matrix codes and braille embossing. Foodservice operators migrating to sustainable clamshells accelerate the adoption of poly-coated cartonboard, although stakeholders anticipate a gradual shift to aqueous barriers to align with recyclability guidelines. Coupled with Mondi’s 180 million-bag capacity expansion in industrial sacks, the grade mix reaffirms the dominance of containerboard yet underscores a premium-segment opportunity for cartonboard converters equipped with UV-offset presses.

By Product: Corrugated Solutions Dominate Shipping Ecosystems

Corrugated boxes accounted for 30.10% of the Egypt paper packaging market size in 2025 as exporters rely on RSC and die-cut formats to safeguard horticultural and textile consignments. Customized board grades ranging from 125 gsm to 220 gsm balance stiffness and cost, targeting long-haul maritime routes via Sokhna and Damietta ports. Folding cartons, although smaller in tonnage, outpace overall growth at a 5.86% CAGR through 2031, driven by brand-driven shelf visibility in pharmacy and beauty aisles. Digital embellishment enables small-batch SKUs for e-commerce flash sales, enhancing consumer perception and permitting just-in-time inventory.

Growth prospects in other specialty formats include honeycomb partitions for white goods and electronics that require edge crush protection, and paper mailers that combine kraft outer plies with padded fiber inserts for apparel shipping. Converters investing in multi-point gluers and rotary die-cutters can flexibly transition between bulk shipments and retail-ready cartons, supporting profitability across economic cycles.

By End-User Industry: Food Reigns, Healthcare Accelerates

The food sector anchored 42.20% of 2025 revenues, leveraging robust agricultural output and rising demand for packaged staples in urban households. Citrus exporters specify ventilated, wax-coated corrugated trays to mitigate mold during voyages to Rotterdam, whereas snack makers adopt high-graphic folding cartons to attract millennial buyers. Beverage cartons gain momentum through aseptic packs that preserve shelf-stable milk and juices without refrigeration, aligning with Egypt’s energy-conservation policies.

Healthcare packaging, forecast at a 5.72% CAGR, benefits from Egypt’s ambition to triple pharmaceutical exports by 2030. Serialization mandates drive the adoption of track-and-trace labels integrated into folding cartons, while cold-chain biologics require multi-wall corrugated shippers lined with molded pulp components. Complementary growth in the personal-care and home-care categories stimulates demand for laminated cartonboard in detergent capsules and hair-color kits, thereby widening the product-mix scope for Egypt's paper packaging market stakeholders.

By Packaging Format: Rigid Boards Retain the Edge

Rigid configurations controlled 51.55% of the 2025 value, underscoring Egypt’s export-heavy economy, which prioritizes load-bearing performance. Triple-wall corrugated solutions service sugar and fertilizer bulk bags, while solid board crates support fresh fish shipments through Mediterranean routes. The surge in molded fiber is set for a 5.78% CAGR, reflecting rising investments in banana-fiber trays and bagasse-based cup carriers that satisfy the sustainability pledges of quick-service restaurants.

Semi-rigid folding cartons remain crucial in channels where point-of-sale aesthetics sway consumer choice. Hybrid packs, which integrate litho-laminated corrugated with specialty liners, address the electronics and footwear niches that require cushioning and premium graphics. Flexible paper wraps, though less prevalent, target portion-controlled spice sachets and confectionery twist-wraps, provided manufacturers overcome moisture-barrier limitations through fluorine-free coatings.

Geography Analysis

Egypt’s strategic location between Africa, the Middle East, and Europe cements its stature as a transcontinental packaging hub. Industrial clusters in 6th of October City, 10th of Ramadan City, and Sadat City host large corrugators and folding-carton plants, leveraging export rebate corridors that connect directly to Sokhna and Port Said gateways. Cairo and Alexandria together account for an estimated 48% of domestic consumption due to their dense retail footprints and concentration of FMCG factories. Upper Egypt regions, notably Minya and Qena, supply cane bagasse feedstock to molded-fiber lines, linking agrarian economies with circular packaging value chains. The Red Sea shipping disruptions that cut Suez Canal revenues by 40% in early 2024 exposed logistic vulnerabilities yet also prompted accelerated investment in the 10th of Ramadan dry port, aimed at easing container backlogs and lowering dwell times. Government efforts to localize 23 industries have fostered additional in-country demand, encouraging converters to build satellite plants near automotive, electronics, and pharmaceutical zones. Egypt’s packaging exports increased by 65% year-over-year in 2022, reaching USD 198 million, with Sudan, Libya, and Italy as key destinations. This growth is projected to continue at a double-digit rate as free-trade agreements mature.

Across the Delta, integrated board mills benefit from access to imported recovered fiber via Damietta, facilitating cost-competitive supply into EU markets under duty-free concessions. Meanwhile, Sinai and Red Sea governorates increasingly position themselves as eco-tourism hotspots adopting plastic-free mandates, stimulating localized demand for compostable molded-pulp tableware. Collectively, these geographic shifts reinforce a diversified demand base for the Egypt paper packaging market and mitigate overreliance on any single trade lane.

Regulatory Landscape

Paper packaging placed on the Egyptian market is shaped by standards and labeling rules administered through the Egyptian General Organization for Standards and Quality (EOS), including Egyptian Standard ES 4630:2022 on packaging and packaging waste (aligned to EN 13427:2004) and ES 2289:2022 on mandatory labeling requirements for prepackaged goods. For importers and converters bringing in board, recovered fiber, inks, or packaging machinery, the Customs Law executive regulations (Ministerial Decree No. 430 of 2021, as amended) govern inspection and conformity checks prior to release, with clearance tied to compliance with applicable standards.

In May 2026, the Ministry of Finance issued Decree No. 362 of 2026, streamlining import documentation by removing the need for a separate packing list when the commercial invoice includes detailed package-level information. This procedural change reduces administrative friction for converters that import grades, chemicals, and equipment, and it sits alongside customs mechanisms such as duty installment options for machinery and equipment imported for production facilities, subject to the conditions in the customs executive regulations.

Competitive Landscape

The Egyptian paper packaging market exhibits moderate concentration, characterized by the presence of global multinationals and agile local players. Mondi’s acquisition of Egypt Sack and National Bag converted an extra 180 million industrial bags annually, deepening its dominance in cement and fertilizer applications.

Tetra Pak and Uniboard invested EUR 2.5 million (USD 2.75 million) to establish an 8,000-tonne beverage carton recycling facility, generating closed-loop feedstock that secures cartonboard supply for liquid food processors.[3]Uniboard, “Joint Project to Recycle Used Beverage Cartons,” uniboard-egypt.com International Paper and Huhtamaki cultivate premium folding carton niches for the beauty and pharmaceutical segments, banking on high-gloss UV lacquers and anti-counterfeit features. Local mid-caps such as UNIPAKNILE and El-Ahram Co. leverage cost leadership and geographical proximity to agricultural clients, swiftly converting 3-ply trays for citrus exporters.

Technology partnerships play a prominent role: SIG collaborates with Plastic Bank and TileGreen to introduce a blockchain-enabled carton collection system, converting waste fiber into cement blocks for the construction market. The competitive arena is therefore split between scale efficiencies in industrial sacks and differentiated sustainability propositions in molded pulp and beverage cartons, allowing for diverse market entries and fostering healthy rivalry.

Egypt Paper Packaging Industry Leaders

Tetra Pak Egypt Ltd

Huhtamaki Egypt L.L.C.

Mondi plc

INDEVCO Group SAL

Masr International Paper (MIP)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large, export-oriented capacity additions and licensing facilitation programs create whitespace across corrugated, cartonboard conversion, and molded fiber. The Suez Canal Economic Zone (SCZone) agreement with Eroglu Global Holding for a USD 175 million cardboard and packaging factory in Qantara West (announced January 2026) underscores demand for locally made cartons, boxes, and corrugated sheets that connect to industrial-zone infrastructure and export corridors. At the same time, the Egyptian Cabinet granting a Golden License to Huhtamaki Egypt for a molded fiber packaging facility in the CPC Industrial Zone in Sadat City (Menoufia) points to an enabling route for scaled fiber-based formats that substitute plastic in foodservice and expand access to molded-pulp components for protective packaging.

Opportunities also cluster around localization of containerboard and higher-spec corrugated conversion that supports e-commerce and export logistics. Commissioning of Greenliner’s containerboard machine at 10th of Ramadan City (November 2025) and Cepack Group’s agreement with BHS Germany to install a new corrugated line (December 2025, capacity uplift cited at about 70%) indicate active investment in domestic supply and faster technology upgrade cycles for converters. With Egypt’s EGP 45 billion export rebate program (launched June 2025) tying rebates to sustainability and energy-efficiency metrics, converters that can document recycled content, improve energy intensity, and satisfy labeling and standards requirements have a clearer path to compete for export-oriented FMCG and industrial demand.

Recent Industry Developments

- April 2026: UNIPAKNILE launched the RHINOPAK brand for heavy-duty paper packaging aimed at agriculture, appliances, and automotive applications. The launch expands the company’s positioning in higher-performance corrugated and protective packaging niches, where specification-led demand supports value-added converting and print capabilities.

- May 2025: Huhtamaki confirmed plans for a new molded fiber packaging facility in the CPC Industrial Zone in Sadat City, with operations targeted for August 2026. This investment improves local availability of fiber-based alternatives for foodservice and protective packaging, and it aligns with Egypt’s push for recyclable packaging formats within industrial zones.

- December 2024: Tetra Pak and Uniboard inaugurated Egypt’s first used beverage carton recycling facility in Sadat City, backed by a EUR 2.5 million joint investment and designed for 8,000 tonnes per year. The facility adds domestic recycling infrastructure for carton-based packaging, supporting circular feedstock creation and reducing reliance on imported recovered fiber for cartonboard-related applications.

Research Methodology Framework and Report Scope

Segmentation Overview

- By Grade

- Cartonboard

- Solid Bleached Sulphate (SBS)

- Solid Unbleached Sulphate (SUS)

- Folding Boxboard (FBB)

- Coated Recycled Board (CRB)

- Uncoated Recycled Board (URB)

- Other Cartonboard Grades

- Containerboard

- White-top Kraftliner

- Other Kraftliners

- White-top Testliner

- Other Testliners

- Semi-chemical Fluting

- Recycled Fluting

- Cartonboard

- By Product

- Folding Cartons

- Corrugated Boxes

- Other Products

- By End-User Industry

- Food

- Beverage

- Healthcare

- Personal Care

- Household Care

- Electrical and Electronics

- Other End-User Industries

- By Packaging Format

- Rigid (Corrugated, Solid Board)

- Semi-rigid (Folding Cartons)

- Flexible Paper (Sachets, Wraps)

- Molded Fibre and Pulp

Key Questions Answered in the Report

Which segment is growing fastest in Egypt’s paper-packaging landscape?

Cartonboard is set to post a 6.03% CAGR, driven by pharmaceutical and premium food applications.

How are government incentives impacting paper packaging exports?

The EGP 45 billion rebate scheme reimburses sustainable fiber-pack exporters within 90 days, spurring new capacity.

What main challenge threatens Egypt’s paper packagers?

Volatile global pulp prices and elevated freight costs erode margins for import-dependent mills and converters.

How large is the Egypt paper packaging market in 2026?

It is valued at USD 2.06 billion and is expected to reach USD 2.52 billion by 2031.

What is the growth rate forecast for Egypt’s paper packaging sector?

The sector is projected to record a 4.05% CAGR during 2026-2031.

Which grade dominates Egypt’s paper packaging demand?

Containerboard leads with 57.05% of 2025 revenue due to extensive corrugated shipping needs.

Page last updated on: