Vietnam Express Delivery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

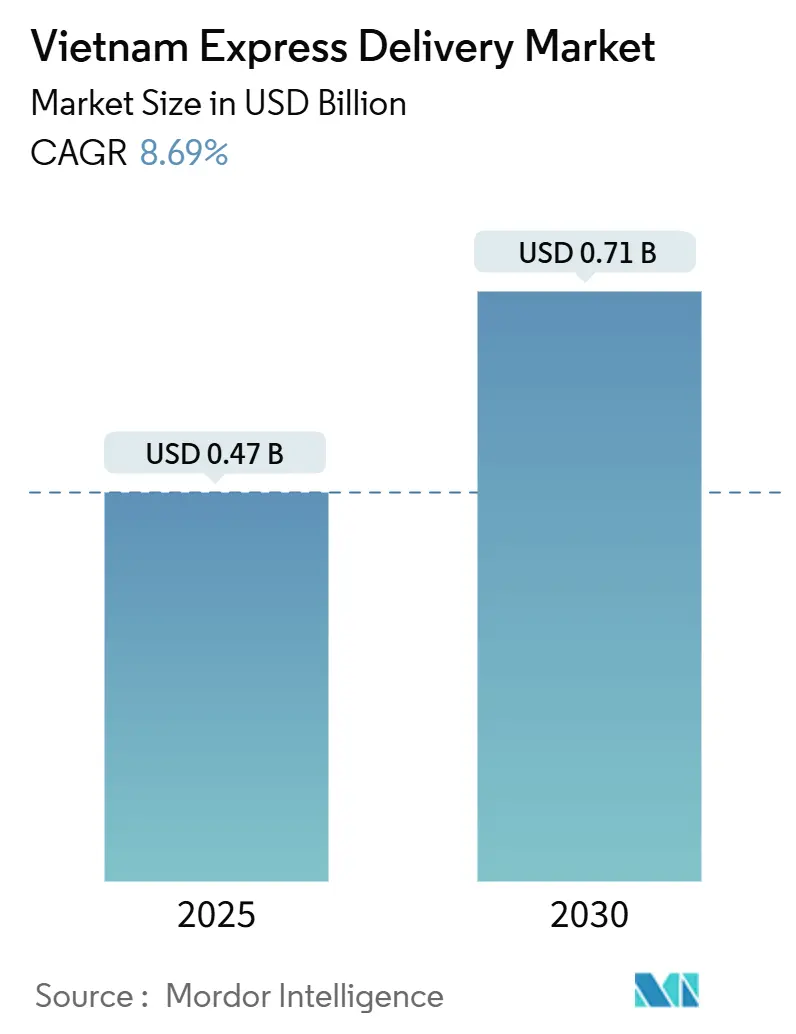

| Market Size (2025) | USD 0.47 Billion |

| Market Size (2030) | USD 0.71 Billion |

| Growth Rate (2025 - 2030) | 8.69% CAGR |

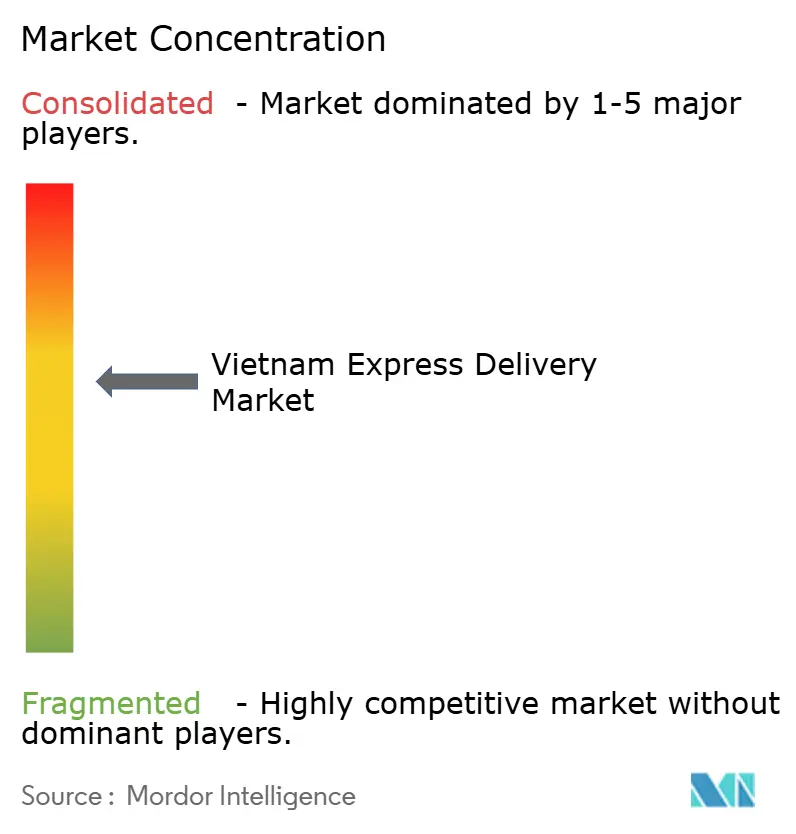

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Express Delivery Market Analysis by Mordor Intelligence

The Vietnam Express Delivery Market size is estimated at USD 0.47 billion in 2025, and is expected to reach USD 0.71 billion by 2030, at a CAGR of 8.69% during the forecast period (2025-2030).

Digital-native consumers drive parcel density as e-commerce revenue climbed above USD 25 billion in 2024, while a VND 791 trillion public investment program expands expressways and airports to accelerate transit times. Competitive intensity heightens because major platforms operate captive fleets, compressing margins close to 3% yet catalyzing 99% automation at new super-hubs. Cross-border corridors with China and ASEAN spur the fastest-growing international flows, and foreign capital injections supply technology such as AI routing and electric vehicles that raise service benchmarks. Tight regulatory timetables on plastic-free packaging from 2026 and Extended Producer Responsibility requirements reshape cost structures and stimulate packaging redesigns.

Key Report Takeaways

- Domestic destinations held 61.83% of Vietnam express delivery services market share in 2024; the international segment is forecast to expand at a 9.10% CAGR to 2030.

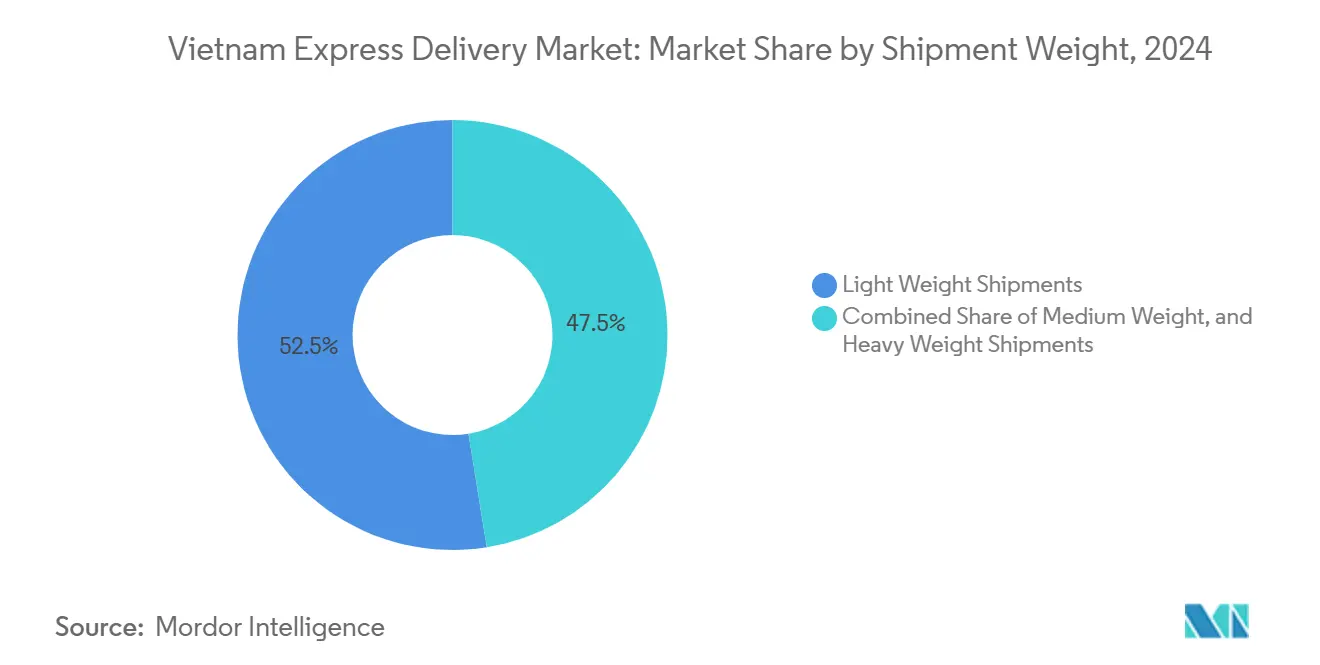

- Light weight parcels commanded 52.54% share of the Vietnam express delivery services market size in 2024 and are advancing at an 8.87% CAGR through 2030.

- By model, B2C deliveries captured 56.38% revenue share in 2024, while the same segment records the highest projected CAGR at 9.28% to 2030.

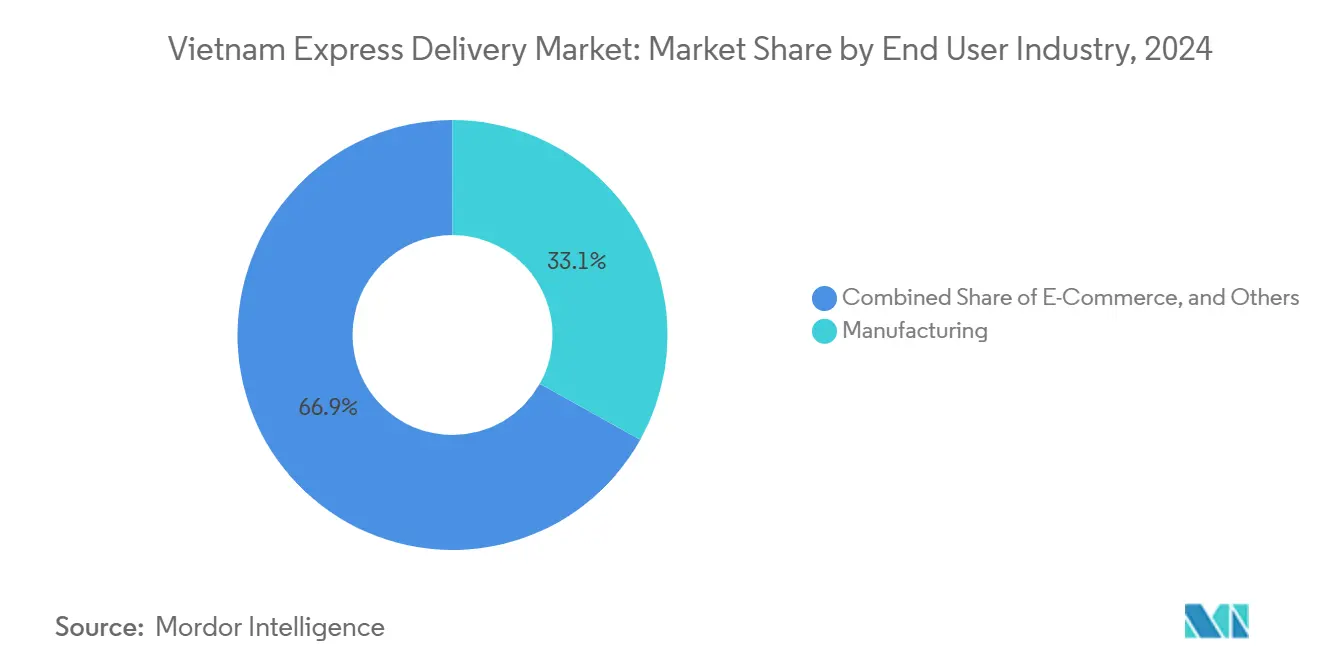

- Manufacturing end users accounted for 33.10% share of the Vietnam express delivery services market size in 2024; e-commerce is projected to climb at a 9.78% CAGR through 2030.

- Road transport led with 52.88% share in 2024; air transport is expected to post an 8.92% CAGR to 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with Vietnam being one of the contributors. Our global express delivery market size represents that cumulative total.

Vietnam Express Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive B2C parcel volumes from ≥25% annual e-commerce growth | +3.2% | National, Ho Chi Minh City, Hanoi, Da Nang | Short term (≤ 2 years) |

| Government expressway and airport build-out slashing transit times | +2.1% | National corridor focus | Medium term (2-4 years) |

| Platform-subsidized "free shipping" deepening demand for fast delivery | +1.8% | Urban centers, Tier-2 cities | Short term (≤ 2 years) |

| Foreign CEP entrants injecting capital and technology | +1.4% | Major economic zones | Medium term (2-4 years) |

| Rapid uptake of QR / e-wallet payments cutting COD cost | +0.9% | Urban areas | Short term (≤ 2 years) |

| Surging TikTok live-commerce spikes | +0.7% | National, youth clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive B2C parcel volumes from more than 25% annual e-commerce growth

Successful deliveries on the five largest platforms climbed to 2.2 billion units in 2024, reshaping distribution economics and enabling carriers to finance high-speed crossbelt sorters that process 99,000 items per hour. High mobile-commerce penetration surpassing 70% among 18- to 35-year-olds elevates order frequency, while border-province same-day cross-border services tighten delivery promises. Operators such as SPX Express and J&T Express embed directly inside platform ecosystems, migrating from third-party status to quasi-in-house logistics partners. Economies of scale encourage rural network build-outs, and the youth demographic’s affinity for flash sales fuels overnight parcel surges that challenge capacity planning. Cross-border e-commerce adds a premium layer, with 48-hour Hanoi and Ho Chi Minh City delivery targets now standard on select China-origin SKUs[1]“Public Investment Plan 2025,” Vietnam Ministry of Planning and Investment, mpi.gov.vn.

Government expressway and airport build-out slashing transit times

The 3,000-kilometer North–South expressway program shortens Hanoi–Ho Chi Minh City truck times from over 30 hours to under 18, letting carriers consolidate hubs yet sustain next-day coverage. Long Thanh International Airport moves toward Phase 1 handover in 2025, unlocking 1.2 million-ton cargo throughput and positioning Vietnam as a Mekong gateway. Digital customs and smart border checkpoints cut clearance windows from hours to minutes, benefiting small-parcel trade. Capital-intensive operators able to redesign networks around these nodes enjoy cost leverage, whereas smaller couriers struggle to match service guarantees. Regional ASEAN transport accords further harmonize standards, amplifying velocity gains on north-south and east-west corridors[2]“Infrastructure Development Program,” Vietnam Ministry of Transport, mt.gov.vn.

Platform-subsidized "free shipping" deepening consumer addiction to fast delivery

Platform incentives move logistics fees from shopper to marketplace P&L, reducing order thresholds and raising purchase frequency 35–40%. Shopee’s captive SPX network and Lazada’s multi-carrier program signal how subsidies shape retention economics. The model forces standalone couriers to pursue hyper-efficiency at low price points, compressing industry margins near 3%. Consumer expectation of two-day delivery in tier-2 cities becomes pervasive, pushing carriers to automate even mid-tier depots. The sustainability of cost absorption hinges on ad monetization and scale; any subsidy pullback risks sudden demand elasticity yet could lift sector profitability.

Foreign CEP entrants injecting capital and technology (automation, AI, EV fleets)

J&T Express raised USD 451 million in its 2023 IPO, accelerating Vietnam network expansion with 99% accuracy sorters and 99,000-parcel-per-hour belts. Electric vans deployed by Viettel Post and DHL address air-quality regulations and shave fuel expenditure, though charging infrastructure remains limited. AI-driven route engines adjust to real-time congestion, lifting first-attempt success above 95% and freeing capacity. Capital-heavy foreign operators set technology tempo, compelling local firms to seek strategic investors or niche specializations. EV fleets and AI tools emerge as table stakes for bids from large enterprise shippers.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban traffic congestion inflating last-mile costs | -1.9% | Ho Chi Minh City, Hanoi | Short term (≤ 2 years) |

| Fragmented SME courier base keeps price wars and 3% margin ceiling | -1.2% | National | Medium term (2-4 years) |

| Environmental rules banning single-use plastic packaging from 2026 | -0.8% | National | Medium term (2-4 years) |

| Talent gap: <10% of logistics workforce formally trained | -0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban traffic congestion inflating last-mile costs

Peak-hour speeds of 15–20 km/h in Ho Chi Minh City inflate delivery cost per stop by 25–35%, necessitating larger fleets and overtime. Motorcycle couriers confront parking limits and narrow alleys, elongating walk distances and dwell times. Fuel consumption rises, and predictable time windows erode, pushing operators toward evening delivery slots. City authorities pilot cargo-lane regulations and off-peak incentives, yet material relief remains elusive in the near term. Autonomous two-wheel concepts surface but face regulatory clearance hurdles[3]“Urban Traffic Management Report,” Ho Chi Minh City Department of Transport, sggp.org.vn.

Fragmented SME courier base keeps price wars and 3% margin ceiling

Thousands of family-run couriers undercut listed tariffs, keeping industry net margin near 3% despite scale economies. Customer switching costs stay low as service differentiation converges around similar delivery promises. Licensing processes and partial foreign equity caps impede consolidation, allowing micro-players to persist. Price pressure forces larger firms to hunt for non-delivery revenue such as fulfillment, fintech, or advertising. Without policy reform or a shake-out triggered by compliance spending, fragmentation will cap sector pricing power[4]“Environmental Regulations and EPR Implementation,” Vietnam Ministry of Natural Resources and Environment, monre.gov.vn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing scale meets e-commerce momentum

Manufacturing held 33.10% share in 2024, anchored by electronics, garment, and machinery clusters that enlist express services for line-down critical components. The Vietnam express delivery services market size tied to manufacturing benefits from export-oriented factories integrating express lanes for urgent samples or high-value devices. Meanwhile, e-commerce posts the fastest 9.78% CAGR, reflecting platform outreach beyond tier-1 metros. Convergence emerges as producers adopt D2C storefronts, blending industrial and retail flows within the same network.

Healthcare lanes show double-digit growth as tele-pharmacy and clinical trial logistics expand. Financial institutions use express for secure document runs and payment card issuance, although digitization progressively reduces physical volumes. Wholesale and retail trade remains relevant for store replenishment in modern-trade formats, yet faces cannibalization by drop-ship models.

By Destination: International flows accelerate as domestic matures

Domestic deliveries commanded 61.83% of Vietnam express delivery services market share in 2024 on the back of concentrated urban consumption. Growth levels moderate as metro penetration peaks, pushing carriers into lower-density rural districts with higher unit costs. In contrast, international shipments chart a 9.10% CAGR, buoyed by ASEAN and RCEP tariff harmonization that makes sub-2 kg parcels economically viable. Digital customs initiatives slash border dwell times, while improved road links to Guangxi enable same-day cross-border fashion arrivals. Currency volatility introduces planning risk, prompting hedging strategies among leading operators.

Extending service portfolios, larger firms now bundle DDP (Delivered Duty Paid) and in-cart tax estimation tools that simplify overseas purchases for Vietnamese consumers. The international arm also benefits from Long Thanh’s cargo slots, which carve out overnight Hanoi-Bangkok and Ho Chi Minh-City–Singapore frequencies. Competitive positioning shifts toward carriers with brokerage licenses and bonded warehousing, reinforcing barriers to new entrants.

By Model: B2C predominance tracks consumer-led growth

B2C orders supplied 56.38% of Vietnam express delivery services market size in 2024 and will grow at 9.28% CAGR through 2030 as discretionary consumption rises. Couriers integrate via API with marketplace back-ends, enabling auto-manifest generation and real-time tracking push alerts. Consumer-to-consumer flows bloom on social-commerce apps, yet remain rate-sensitive and ride-hail oriented. Business-to-business lanes retain importance owing to dependable volume and longer contracts, cushioning revenue volatility during retail seasonality swings.

Platform-linked carriers secure volume guarantees, but also shoulder service-level penalties for miss picks and late delivery. B2B customers, by contrast, pay premiums for timed deliveries and reverse-logistics for warranty returns. Independent couriers cultivate hybrid models to diversify mix and stabilize cash flow.

By Shipment Weight: Light parcels dominate volume, medium captures margin

Light weight parcels under 2 kg held 52.54% share of the Vietnam express delivery services market size in 2024, with “free shipping” and mobile checkout promoting basket fragmentation. Automated crossbelt systems are calibrated for this weight class, cutting per-piece sort cost below USD 0.02 and raising throughput. Apparel, accessories, and small electronics dominate the stream, and platforms subsidize delivery to maintain conversion even on low-value orders. Medium weight packages (2–20 kg) offer richer contribution margins, serving SMEs who prize reliability over cents per kilo. Heavy shipments lag within express due to alternative LTL providers.

Packaging miniaturization and SKU repack solutions continue to shift traffic toward light categories. Yet enterprise digitization opens fresh medium-weight lanes such as spare-part replenishment shipped direct to factory scale lines, expanding B2B express utility. Carriers build dual-zone sorters to segregate flows and maximize asset productivity across divergent parcel profiles.

By Mode of Transport: Road reigns, air gains

Road retained 52.88% modal share in 2024 thanks to flexible first- and last-mile reach and ongoing expressway completions. Intercity times compress, letting operators move cutoff times later while meeting next-day SLAs. Nevertheless, air shipping obtains an 8.92% CAGR as cross-border and high-value domestic shipments seek overnight speed. Long Thanh International Airport’s cargo pier adds bandwidth, and integrated carriers pre-lease capacity to secure space.

Intermodal models blend night-haul trucks to regional air hubs with short-haul flights to distant provinces, balancing cost and velocity. Waterway and nascent drone trials reside in “Others,” gaining relevance for remote Mekong communities and highland districts when regulatory clearance evolves. Urban congestion, however, revives interest in rail cargo shuttles for trunk routes, though feasibility studies continue.

Geography Analysis

Metro clusters of Ho Chi Minh City, Hanoi, and Da Nang anchor the Vietnam express delivery services market, generating dense pickup-delivery loops that sustain short SLAs and justify automation capex. Rural districts lag on density but represent latent upside as smartphone penetration and 4G coverage rise. Government subsidies for rural digitalization and cashless payments stimulate demand north of 10% per year in provinces such as Thai Binh and An Giang.

Cross-border focused provinces Lang Son and Lao Cai record the highest shipment velocity uplift, leveraging smart checkpoints that cut customs times to minutes. Central coast industrial zones utilize express corridors to dispatch high-value electronics to ASEAN clientele. Southern corridor upgrades connect Can Tho’s agri-exports to global cold-chain networks, creating specialized express niches.

Internationally, China accounts for the bulk of inbound parcels, but Thailand, Singapore, and Malaysia shipments register double-digit growth as ASEAN consumers buy Vietnamese fashion and beauty SKUs. Currency-hedged pricing and VAT auto-collection reduce friction. Environmental compliance differs by market, compelling carriers to adapt packaging specs per destination to avoid fines.

Coverage of the express delivery market by Mordor Intelligence spans a wide geographic footprint, with detailed country-level intelligence for Germany and United States, each shaped by local operating conditions.

Competitive Landscape

The Vietnam express delivery services industry features moderate fragmentation with domestic champions Viettel Post, Vietnam Post, and GHN battling foreign-backed J&T Express and SPX Express. Automation superiority defines leadership; new Hung Yen and Lang Son hubs achieve 99% automated sort ratios and 60% manpower savings. AI route engines and predictive demand platforms cut van mileage 15% and raise first-attempt delivery above 95%.

Foreign investors such as Kerry Logistics fund expansion, injecting capital for cold-chain and bonded warehousing. Gig-economy platforms like Ahamove and GrabExpress offer hyperlocal fulfillment, intensifying price competition on last mile. Margin discipline remains elusive, and most operators diversify into cross-docking, fulfillment, or fintech services to lift contribution.

Strategic moves include DHL’s Ho Chi Minh City gateway expansion with pharma cold rooms, FedEx’s carbon-neutral EV fleet launches, and VNPost’s province-wide digital upgrade trimming handling times 40%. M&A speculation circles SME couriers unable to meet 2026 packaging regulations. Technology adoption speed and capital access appear decisive in shaping market share trajectories by 2030.

Vietnam Express Delivery Industry Leaders

-

Viettel Post

-

SPX Express

-

Giao Hang Tiet Kiem (GHTK)

-

Vietnam Post (VNPost)

-

J&T Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SPX Express began building a 170,000 m² automated mega-hub in Hung Yen with 7 million-parcel daily capacity and Q3 2025 commissioning target.

- February 2025: Viettel Post opened its VND 3,300 billion (USD 132 million) Logistics Park in Lang Son, deploying 200 AGV robots and reaching 99% automation.

- January 2025: GHN unveiled "Giao Hang NANG" AI suite at ViLOG 2025 for heavy-shipment optimization.

- December 2024: J&T Express expanded its Hanoi hub to 38,000 m², lifting throughput to 2.4 million parcels daily.

Vietnam Express Delivery Market Report Scope

| Domestic |

| International |

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Road |

| Air |

| Others |

| By Destination | Domestic |

| International | |

| By Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| By Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| By End User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| By Mode of Transport | Road |

| Air | |

| Others |

Key Questions Answered in the Report

How fast is parcel volume growing in the Vietnam express delivery services market?

Parcel volumes are rising in line with e-commerce growth that has exceeded 25% annually, lifting successful deliveries to 2.2 billion units in 2024.

What is the forecast size of the Vietnam express delivery services market by 2030?

The Vietnam express delivery services market size is expected to reach USD 0.71 billion by 2030, reflecting an 8.69% CAGR.

Which shipment weight segment leads volumes?

Light weight parcels under 2 kg dominate with 52.54% share in 2024 due to fashion, electronics, and consumer goods orders.

Why are margins so low in Vietnam’s express delivery space?

Thousands of SME couriers and platform-subsidized “free shipping” keep average net margin near 3%, forcing carriers to pursue efficiency gains.

How do new environmental rules affect carriers?

The 2026 ban on single-use plastic packaging raises per-parcel costs 15–20% and requires reverse-logistics systems for reusable materials.

Which transport mode is gaining share fastest?

Air transport is projected to grow at 8.92% CAGR to 2030, helped by Long Thanh International Airport and rising cross-border demand.

Page last updated on: