United States Express Delivery Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

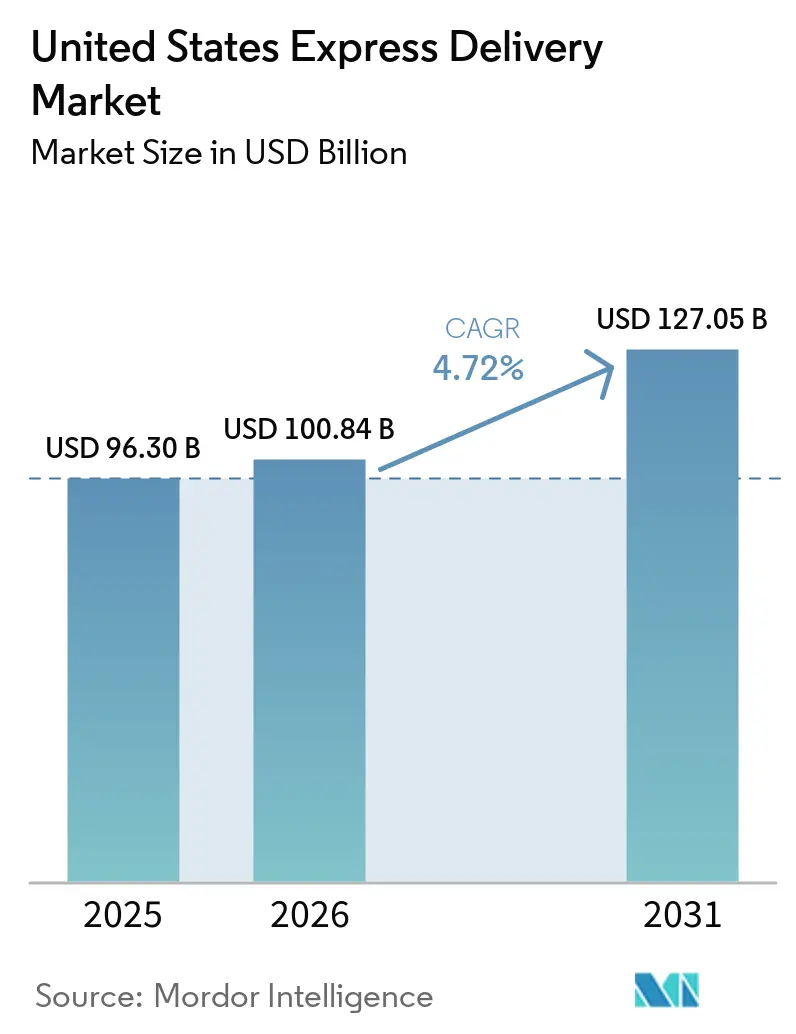

| Base Year Market Size (2025) | USD 96.30 Billion |

| Market Size (2026) | USD 100.84 Billion |

| Market Size (2031) | USD 127.05 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

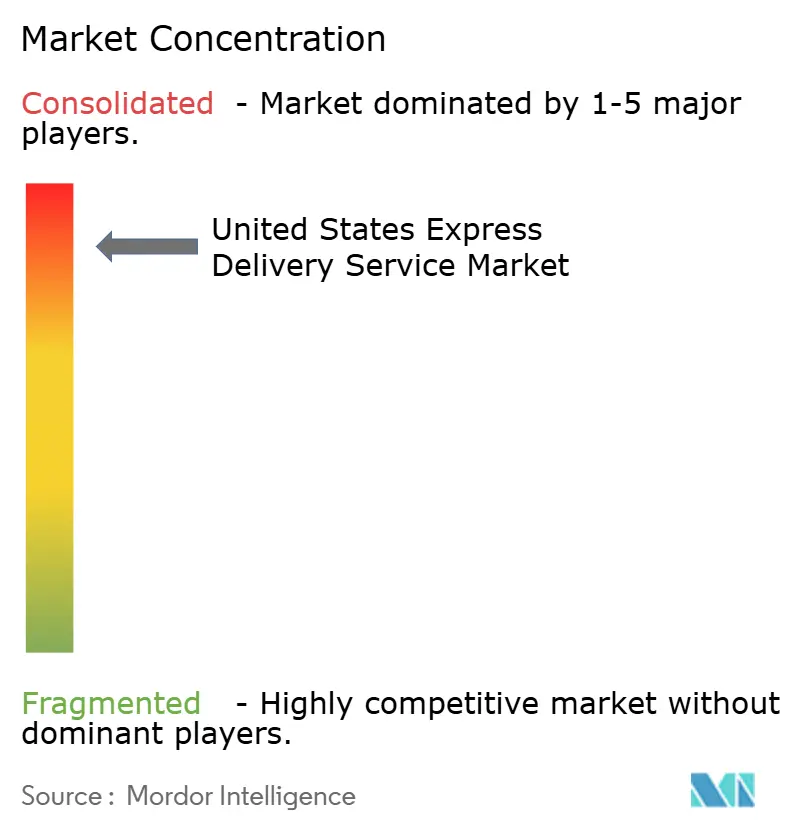

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Express Delivery Market Analysis by Mordor Intelligence

The United States express delivery market size was valued at USD 96.30 billion in 2025 and estimated to grow from USD 100.84 billion in 2026 to reach USD 127.05 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031). Structural e-commerce fulfillment changes, tightening healthcare cold-chain regulations, and rapid last-mile innovations continue to redefine competitive priorities. Amazon’s ability to offer same-day or next-day service on 60% of volume across the top 60 metropolitan statistical areas has locked consumer expectations on speed, pushing traditional carriers to upgrade networks and add technology-enabled agility. Federal Aviation Administration slot caps at hubs such as Newark are amplifying the strategic value of ground networks and creating entry points for nimble regional carriers[1]Federal Aviation Administration, “Congestion Management at Newark Liberty International Airport,” govinfo.gov . Meanwhile, UPS’s new Ground Saver tier and the United States Postal Service’s Delivering for America cost-reduction roadmap are polarizing the service landscape between high-service express offerings and cost-optimized ground products[2]United Parcel Service, “Introducing UPS Ground Saver,” about.ups.com. As enterprises increasingly adopt micro-fulfillment, time-critical spare-parts programs, and temperature-controlled logistics, the United States express delivery market is set to maintain balanced, sustainable momentum.

Key Report Takeaways

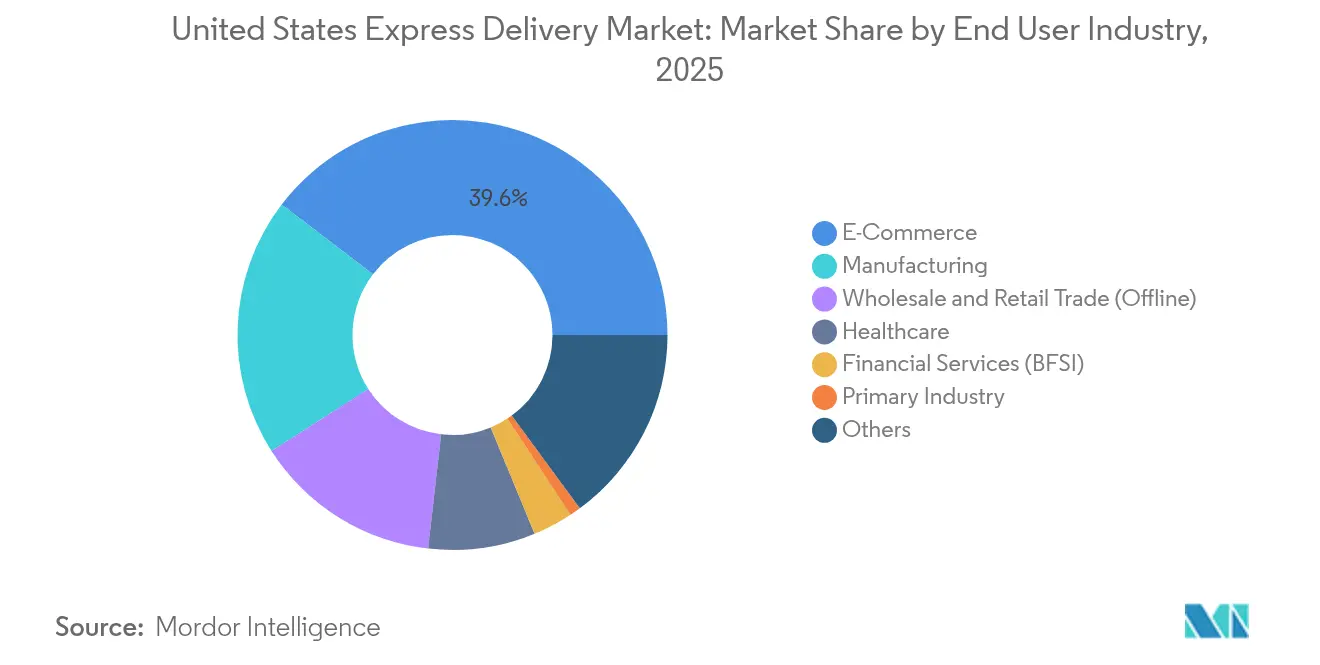

- By end user industry, E-commerce accounted for 39.62% of the United States express delivery market share in 2025, while wholesale and retail trade (offline) shows the highest 5.62% CAGR (2026-2031) projection.

- By destination, the domestic sub-segment held 62.10% of the United States express delivery market size in 2025, while international express services are forecast to post the strongest 5.73% CAGR between 2026-2031.

- By delivery commitment, time-definite-express led with 50.65% revenue share in 2025; day-definite-express is expected to expand at a 5.03% CAGR between 2026-2031.

- By mode of transport, road services commanded 51.05% of 2025 revenue, whereas air services are projected to register the highest 4.99% CAGR between 2026-2031.

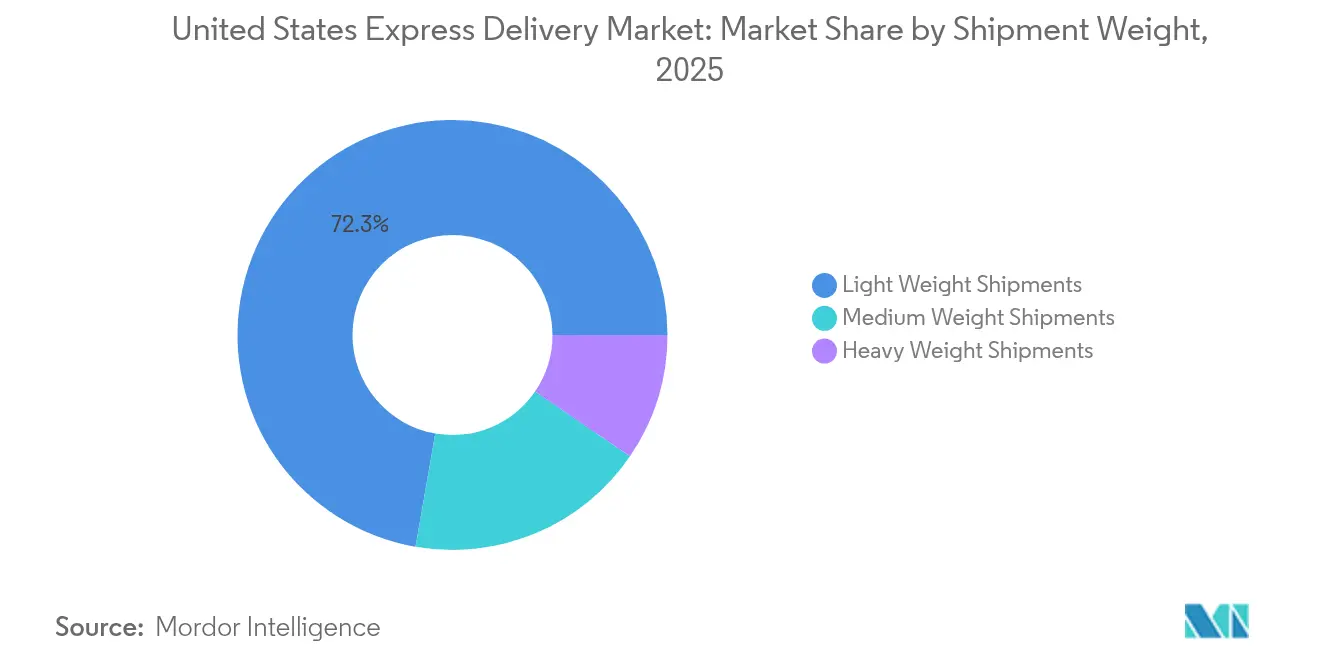

- By shipment weight, light weight parcels accounted for 72.25% revenue share in 2025; the medium weight category is advancing at a 5.26% CAGR between 2026-2031.

- By business model, the business-to-consumer (B2C) segment led with 61.35% revenue share in 2025, yet business-to-business (B2B) is projected to grow at 5.47% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United states contributes to a system defined not by any single country or region but by the interaction of many. The global express delivery market data by Mordor Intelligence represents that combined structure.

United States Express Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of same-day and next-day e-commerce parcels in top-60 MSAs | +1.8% | Top-60 MSAs; spillover to secondary markets | Short term (≤ 2 years) |

| Retailers’ shift to micro-fulfillment centers boosting “zone-0/1” express volumes | +1.2% | Urban cores; expanding to suburbs | Medium term (2-4 years) |

| Tightening healthcare cold-chain compliance fueling temperature-controlled express demand | +0.9% | National; pharma corridors | Long term (≥ 4 years) |

| International inbound surge driven by cross-border returns from China-origin marketplaces | +0.7% | West Coast ports; inland DCs | Medium term (2-4 years) |

| Subscription commerce and direct-to-consumer brands driving predictable express volume growth | +0.5% | National, with higher concentration in affluent suburban markets | Medium term (2-4 years) |

| “2-hour” drone/van hybrid networks gaining traction for time-critical B2B spare parts | +0.4% | Industrial clusters; select pilot metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Same-Day and Next-Day E-Commerce Parcels in Top-60 MSAs

Amazon fulfilled 4 billion same-day or next-day orders domestically in 2024, showcasing the operational impact of its regionalized fulfillment model. This achievement created a cascading requirement for comparable velocity among competitors, with 99% of large players in the United States same day delivery market aiming to offer some form of same-day delivery by 2025. Express carriers are doubling same-day facilities and reallocating urban sortation capacity to protect high-yield corridors. The United States express delivery market is therefore concentrating capital in the densest metropolitan areas, leading to a two-tier service structure that challenges nationwide coverage economics. In rural zones, carriers are piloting drones and autonomous vans as viable substitutes for costly truck-based routes, highlighting a technology-led push for inclusive service reach.

Retailers’ Shift to Micro-Fulfillment Centers Boosting “Zone-0/1” Express Volumes

Automated micro-fulfillment centers shorten average parcel miles to under five, enabling ground-priced shipments to meet express-level speed targets. Amazon’s Project Juniper roll-out illustrates how modular robotics can retrofit underutilized retail footprints into sub-hour fulfillment nodes. Express providers gain incremental revenue by offering zone-skipping, scheduled pick-ups, and managed returns tailored to these urban nodes. Yet, scaling micro-fulfillment remains capital intensive, and early grocery-focused enthusiasm has moderated as volumes normalize. Continuous robotics upgrades and flexible racking are improving ROI, allowing the United States express delivery market to capture premium, ultra-local traffic despite cooling hype cycles.

As Healthcare Cold-Chain Compliance Tightens, Premium Express Services Stand to Gain

DHL’s EUR 2 billion (USD 2.20) billion commitment to healthcare logistics by 2030 allocates half of the capital to the Americas, adding GDP-certified hubs and expanding cryogenic capacity[3]DHL Group, “DHL Invests EUR 2 Billion to Expand Healthcare Logistics,” group.dhl.com . FedEx is introducing advanced telemetry and insulated reusable containers to safeguard biologics throughout transit. Stringent FDA guidelines now mandate more granular temperature auditing, creating regulatory barriers that favor incumbents with validated networks. Clinical trial logistics magnify the imperative, because delays jeopardize patient safety and product pipelines. As a result, healthcare consignors accept premium fees for guaranteed hand-offs, supporting higher yield per kilo in the United States express delivery market.

International Inbound Growth on Cross-Border Returns from China-Origin Marketplaces

Temu and SHEIN have overtaken several Western platforms in United States cross-border transaction volume, pushing inbound parcels upward and raising return ratios tied to fit and quality dissatisfaction[4]International Post Corporation, “2024 Cross-Border E-Commerce Shopper Survey,” ipc.be . Carriers now market prepaid label programs and consolidated return centers to streamline reverse flows. Policy risk has intensified after removal of the USD 800 de minimis exemption on many shipments, escalating customs requirements and tariffs. Express networks that provide brokerage, harmonized code validation, and duty calculators are capturing share from platforms reliant on slower postal channels. Consequently, international inbound parcels reinforce the revenue mix diversity of the United States express delivery market despite higher compliance costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ground-express modal substitution as shippers trade down for cost optimization | -1.4% | National; cost-sensitive segments | Short term (≤ 2 years) |

| Labor union agreements escalating last-mile cost per stop | -0.8% | Unionized Northeast and Midwest | Medium term (2-4 years) |

| Airport capacity curfews limiting night-sort expansion in tier-1 hubs | -0.6% | Major metropolitan airports; Northeast corridor | Long term (≥ 4 years) |

| Rising fuel costs pressuring delivery economics and route optimization | -0.5% | National; long-distance lanes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ground-Express Modal Substitution as Shippers Trade Down for Cost Optimization

Shippers are gravitating toward economical tiers such as UPS Ground Saver to mitigate inflationary pressures. Consumer research confirms that 90% of buyers accept longer waits in exchange for free shipping, eroding the urgency premium once unique to express. FedEx and UPS instituted 5.9-6.6% general rate increases for 2025 but are blending ground and express operations to preserve service dependability. USPS’s Ground Advantage compounds the margin squeeze by offering reliable two-to-five-day options at aggressive pricing. Aggregate volume migration toward deferred tiers dampens near-term revenue expansion across the United States express delivery market.

Labor Union Agreements Escalating Last-Mile Cost per Stop

The 2024 UPS-Teamsters contract lifted full-time delivery driver wages to an average USD 95,000, with part-timers starting no lower than USD 21 per hour. Mandatory wage escalators through 2028 and reduced forced overtime raise cost per delivery stop, especially during holiday surges. Carriers have responded by accelerating roll-outs of handheld route-sequencing software and deploying more lightweight electric vans to offset fuel and labor. However, last-mile tasks remain labor-intensive and resistant to full automation. The differential widens between unionized integrators and non-union regionals, creating both risk and opportunity inside the United States express delivery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: E-Commerce Leadership Faces Offline Retail Challenge

E-Commerce held a 39.62% share of the United States express delivery market size in 2025, anchoring daily volume expectations. Apparel and beauty items dominate shipment counts, and returns management is a critical ancillary service.

Wholesale and Retail Trade (Offline) bookings are expected to grow fastest at 5.62% CAGR (2026-2031) as brick-and-mortar chains launched store-to-door express fulfillment, narrowing the service gap with online-only rivals. Manufacturing relies on overnight parts to minimize production disruption, while healthcare drives premium yields because cold chain failures carry compliance penalties. Financial services send fewer parcels but require ironclad chain-of-custody controls, sustaining a niche premium for secure express. Vertical specialization thus remains a durable strategy for margin preservation in the United States express delivery market.

By Destination: Cross-Border Complexity Drives Premium Pricing

International express is projected to record a 5.73% CAGR (2026-2031) trajectory, while the domestic channel sustained a larger base with 62.10% of the United States express delivery market size in 2025. Increased document verification, tariff calculations, and return logistics confer pricing power on integrators possessing brokerage depth. Nearshoring under the USMCA framework accelerates intra-regional lanes such as Mexico–United States, producing shorter average line-haul distances yet not eroding premium service demand.

Domestic growth, though slower, benefits from e-commerce densification, spare-parts urgency, and temperature-controlled pharmaceuticals that cannot tolerate deferred transit. Amazon’s regional inventory placement elevated customer expectations for 24-hour delivery windows across the continental footprint. The United States express delivery market, therefore, maintains a dual-engine model in which domestic volume secures network density and international parcels deliver a higher yield.

By Delivery Commitment: Time-Definite Services Command Premium Despite Growth Lag

Time-Definite-Express retained 50.65% share in 2025, proving that enterprises with mission-critical needs still pay for guaranteed service. Financial services, aerospace, and life-sciences consignors dominate this tier, stressing liability control over rate.

Day-Definite-Express grew at 5.03% CAGR (2026-2031) as consumers valued reliability over pure speed. FedEx’s Network 2.0, which merges ground and express infrastructure, exemplifies how carriers are offering multi-day certainty through one integrated platform. The United States express delivery market positions day-definite as a mid-price lever that cushions volume migration away from premium overnight products without cannibalizing ground entirely.

By Shipment Weight: Medium Weight Segment Drives Industrial Growth

Light Weight parcels held 72.25% of the United States express delivery market share in 2025 by virtue of steady e-commerce flows. They remain the bread-and-butter of residential delivery rounds.

Medium Weight consignments, ranging 5-31.5 kg, led growth at 5.26% CAGR (2026-2031) as industrial automation, renewable-energy maintenance, and medical equipment sectors demanded just-in-time components. UPS is trialing conveyor retrofits that manage medium parcels without manual touches, preserving throughput efficiency. Heavy Weight volumes remain niche because LTL carriers offer lower per-kilo costs; nonetheless, premium same-day services for bulky equipment keep a foothold in the United States express delivery market.

By Mode of Transport: Air Services Resilient Despite Ground Dominance

Road services handled 51.05% of parcels in 2025, reflecting cost advantages and increasingly optimized hub-and-spoke routing. Smart dispatch software and growing EV fleets further enhance ground cost structures.

Air services still posted a 4.99% CAGR (2026-2031), buoyed by medical isotopes, high-value electronics, and next-morning commitments. FAA slot constraints at Newark and other tier-1 hubs compel carriers to redirect flights or invest in secondary airports. Drone and autonomous fixed-wing trials are accumulating flight hours after beyond-visual-line-of-sight approvals, hinting at disruptive cost curves once regulatory maturity arrives. The United States express delivery market accordingly retains multimodal flexibility to hedge infrastructure bottlenecks.

By Model: B2B Segment Accelerates on Industrial Demand

Business-to-Consumer (B2C) orders preserved a 61.35% share in 2025, powered by platform-based retail and subscription models. Residential delivery density allows route optimization that offsets high stop counts.

Business-to-Business (B2B) consignments outperformed at 5.47% CAGR (2026-2031), driven by predictive maintenance programs that require parts under 24 hours to avoid line shutdowns. Carriers package dashboards that funnel IoT sensor alerts directly into shipment labels, reducing downtime exposure. Consumer-to-Consumer (C2C) traffic remains limited due to marketplace policies that funnel most peer-to-peer commerce through retailer-managed channels. Increasing industrial automation will likely lift B2B margins further within the United States express delivery market.

Geography Analysis

Population density, infrastructure maturity, and regulatory context create pronounced regional differences inside the United States express delivery market. The Northeast corridor, stretching from Boston to Washington D.C., packs dense demand but also faces night-time flight curfews and runway reconstructions that cap airlift capacity. Carriers have diversified into regional sort centers in Pennsylvania and New Jersey to preserve next-day coverage while sidestepping airside restrictions. Long-haul trucking lanes from these hubs reduce overreliance on constrained airports and maintain delivery guarantees.

The West Coast adds sizable international flow, with trans-Pacific import parcels landing at Los Angeles, Long Beach, and Seattle-Tacoma before funneling into Amazon’s same-day network that now covers 140 metro zones. State labor laws and higher wages inflate cost bases; nonetheless, proximity to Asia accelerates customs processing and keeps high-yield premium traffic in the region. Cross-border volumes from Canada and especially Mexico have risen as nearshoring blurs domestic and international categorization, supporting lane diversification within the broader United States express delivery market.

Southern states such as Texas, Florida, Georgia, and Arizona form the fastest-growing theater for new fulfillment centers thanks to business-friendly regulations and inbound population migration. Lower labor costs, land availability, and multimodal access catalyze seven-day delivery schedules that pull traffic from older Northeast facilities. Energy, aerospace, and semiconductor clusters increase demand for temperature-controlled and oversized express loads, ensuring balanced growth across residential and industrial segments. Drone corridors initiated under state economic-development programs further expand the technological frontier of the United States express delivery market by connecting sparsely populated zones into mainstream networks.

The express delivery market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Germany and Vietnam, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The United States express delivery market is structurally concentrated around UPS and FedEx, yet competitive pressure is intensifying from Amazon Logistics, USPS, and agile regionals. UPS is juggling premium labor investment with product line expansion, such as Ground Saver, aiming to fence off cost-sensitive defections while nurturing high-service enterprise contracts. FedEx Network 2.0 targets USD 2 billion in efficiencies by merging pickup, sort, and delivery functions across formerly siloed units, unlocking route density and shared assets.

Amazon continues to self-insource volume, piloting AI route planners, humanoid pick-robots, and electric vans that reduce per-stop cost and improve mapping accuracy. USPS leans on legislative reforms and network redesign to chip away at low-weight ground parcels, especially for SMB shippers who prefer flat pricing and Saturday delivery. Regionals such as OnTrac extend seven-day schedules and have merged with LaserShip to build a 31-state footprint, challenging the integrators in densely populated zones.

Strategic mergers and acquisitions are reshaping supply dynamics. DSV’s acquisition of DB Schenker for EUR 14.3 billion (USD 15.78 billion) expands end-to-end service breadth and invites European players to contest the United States express lanes. Purolator’s Livingston International purchase sharpens cross-border brokerage expertise, facilitating faster customs throughput. SpeedX’s 2024 Accelerated Global Solutions buyout signals a parcel upstart’s ambition to breach the half-billion-dollar revenue threshold. Technology, labor economics, and cross-border facilitation together define the evolving chessboard of the United States express delivery market.

United States Express Delivery Industry Leaders

United Parcel Service of America, Inc. (UPS)

FedEx

United States Postal Service (USPS)

DHL Group

OnTrac (formerly LaserShip/OnTrac)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Group committed EUR 2 billion (USD 2.20 billion) through 2030 to expand Americas healthcare logistics capacity.

- March 2025: United States Postal Service implemented refined service standards under Delivering for America, targeting USD 36 billion in savings over 10 years.

- February 2025: Purolator bought Livingston International, enhancing brokerage and freight forwarding reach.

- December 2024: FedEx revealed plans to spin off its LTL freight unit to focus resources on express and ground parcels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States express-delivery market as all time-definite, track-and-trace parcel services, documents or packages up to 70 kg, moved by integrated networks via road or air for B2B, B2C, and C2C customers.

Scope exclusion: Freight above 70 kg and non-tracked letter mail are not included.

Segmentation Overview

- Destination

- Domestic

- International

- By Route

- Inter-Region

- Intra-Region

- By Route

- Delivery Commitment

- Time-Definite-Express (TDE)

- Day-Definite-Express (DDE)

- Mode of Transport

- Air

- Road

- Others

- Shipment Weight

- Heavy Weight Shipments

- Light Weight Shipments

- Medium Weight Shipments

- Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

- End User Industry

- E-Commerce

- Financial Services (BFSI)

- Healthcare

- Manufacturing

- Primary Industry

- Wholesale and Retail Trade (Offline)

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with hub managers of national carriers, fulfillment 3PLs, healthcare cold-chain shippers, and urban last-mile start-ups across various states. These discussions tested secondary assumptions on average stop density, fuel-surcharge pass-throughs, and same-day service uptake, ensuring every major user cohort and geography was represented.

Desk Research

We began with shipment-value series from the US Census Bureau Quarterly Services Survey, Bureau of Transportation Statistics freight tables, and USPS financial filings. Trade indicators such as the Pitney-Bowes Parcel Shipping Index and National Retail Federation e-commerce dashboards helped us size domestic parcel pools. Company 10-Ks, investor decks, and D&B Hoovers profiles clarified carrier yields and private-operator revenue bands, while UPU customs data and Volza shipment records validated cross-border flows. This source list is illustrative; many other public and subscription references supported data checks.

Market-Sizing & Forecasting

A top-down build linking e-commerce GMV, business mailing spend, and per-order parcel ratios sets the 2024 base. Then, selective bottom-up roll-ups (sampled ASP × volume, channel checks) validate totals. Key variables include parcels per online order, jet-fuel spot prices, union wage indices, inbound Asia-US air-freight tonnage, and metropolitan population growth. A multivariate regression model, trained on 2017-2024 history, projects 2025-2030 while scenario analysis assesses disruptive tech such as autonomous vans.

Data Validation & Update Cycle

Outputs face variance thresholds, peer review, and, when needed, re-interviews. Models refresh annually, with interim updates when material events, labor contracts, fuel spikes, and regulatory shifts arise, so clients receive the latest view.

Credibility of United States Express Delivery Service Baseline

Published numbers diverge because firms select different service mixes, ignore USPS revenue, or refresh data on uneven cadences.

According to Mordor Intelligence, the 2025 US express-delivery market stands at USD 96.30 billion. Regional Consultancy A folds broader courier, express, and parcel (CEP) activity into its estimate, pushing its 2024 figure to USD 133.2 billion, while Global Consultancy B omits postal revenue yet still posts USD 120.21 billion for 2024.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 96.30 B (2025) | Mordor Intelligence | - |

| 133.20 B (2024) | Regional Consultancy A | Combines CEP and contract logistics revenue |

| 120.21 B (2024) | Global Consultancy B | Excludes USPS and uses static 2020 ASPs |

The comparison shows peers swing wide, either overstating totals by bundling non-express services or understating by trimming essential channels, whereas Mordor's disciplined scope and annual refresh provide a balanced, transparent baseline users can replicate with confidence.

Key Questions Answered in the Report

What is the current United States express delivery market size?

The United States express delivery market size stands at USD 100.84 billion in 2026 and is projected to reach USD 127.05 billion between 2026-2031.

Which shipment weight category is growing fastest?

Medium Weight parcels between 5 kg and 31.5 kg are expanding at a 5.26% CAGR (2026-2031) due to industrial spare-parts demand and specialized equipment moves.

Why are international inbound parcels rising?

Chinese marketplaces such as Temu and SHEIN have accelerated cross-border sales, increasing both inbound deliveries and return volumes that require express handling.

How are labor costs affecting carriers?

The 2024 UPS-Teamsters agreement lifted wages significantly, prompting carriers to invest in automation and route optimization to offset higher cost per stop.

Which region is seeing the highest express delivery growth?

The Southeast and Southwest, led by Texas and Florida, are experiencing rapid facility expansion because of population influx, favorable regulations, and new distribution centers.

What role does healthcare logistics play in market growth?

Stricter cold-chain compliance and pharmaceutical innovation are driving premium express demand, supported by large investments such as DHL’s USD 2.20 billion program for new Pharma Hubs.

Page last updated on: