Bio-Implants Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

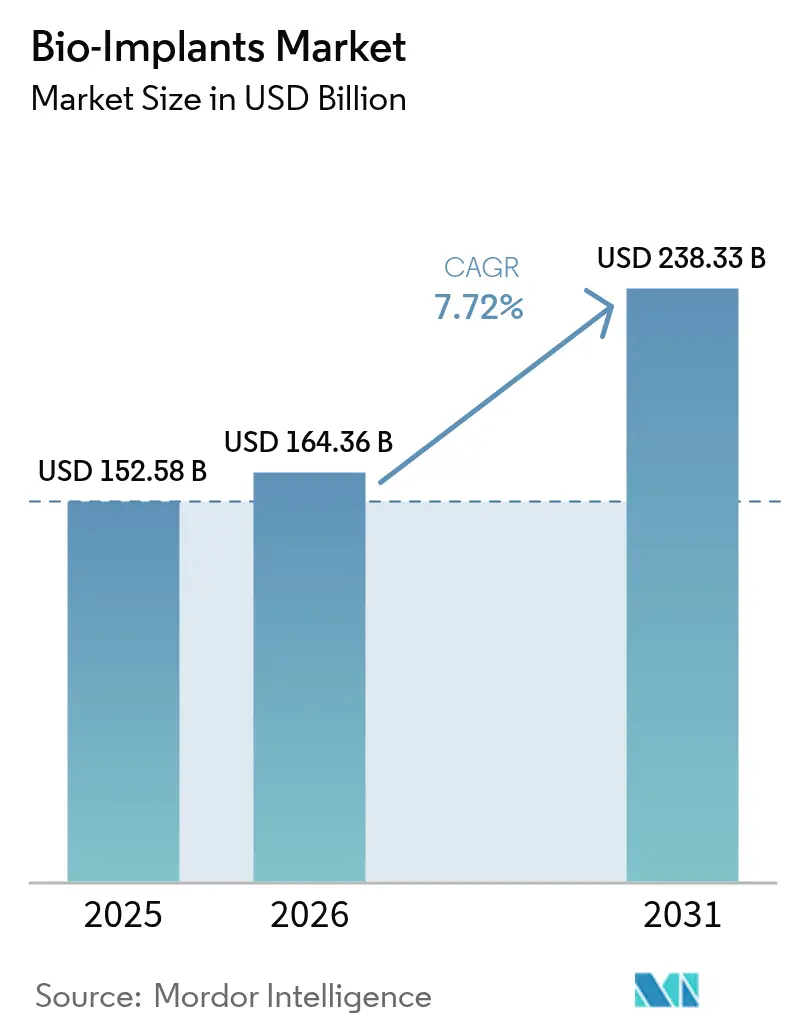

| Market Size (2026) | USD 164.36 Billion |

| Market Size (2031) | USD 238.33 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-Implants Market Analysis by Mordor Intelligence

The global bio-implants market size is expected to grow from USD 152.58 billion in 2025 to USD 164.36 billion in 2026 and is forecast to reach USD 238.33 billion by 2031 at 7.72% CAGR over 2026-2031. Rapid uptake is driven by population aging, surging chronic-disease prevalence, and the routine use of sensor-enabled devices that transmit real-time clinical data to care teams. Demand is reinforced by 3-D-printed patient-specific constructs that shorten theatre time and enhance post-operative outcomes, while bioresorbable materials eliminate follow-up extraction surgeries. Health-system moves toward value-based reimbursement are accelerating adoption in emerging economies where providers focus on total-episode cost rather than device price alone. Competitive intensity is rising as major suppliers acquire niche innovators to assemble complete musculoskeletal and cardiovascular portfolios.

Key Report Takeaways

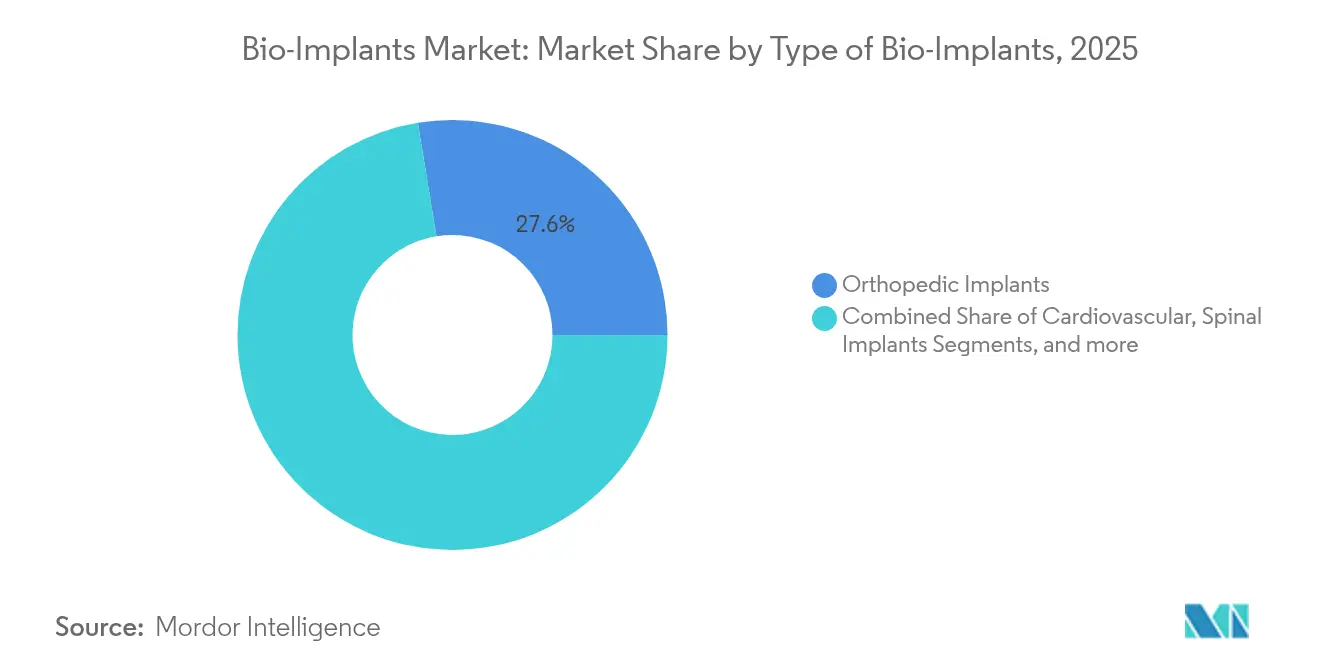

- By type, orthopedic implants led with 27.58% of the bio-implants market share in 2025; cardiovascular implants are projected to expand at an 8.23% CAGR through 2031.

- By material, metals and alloys accounted for 43.72% share of the bio-implants market size in 2025, while composite and hybrid biomaterials are forecast to grow at an 8.12% CAGR to 2031.

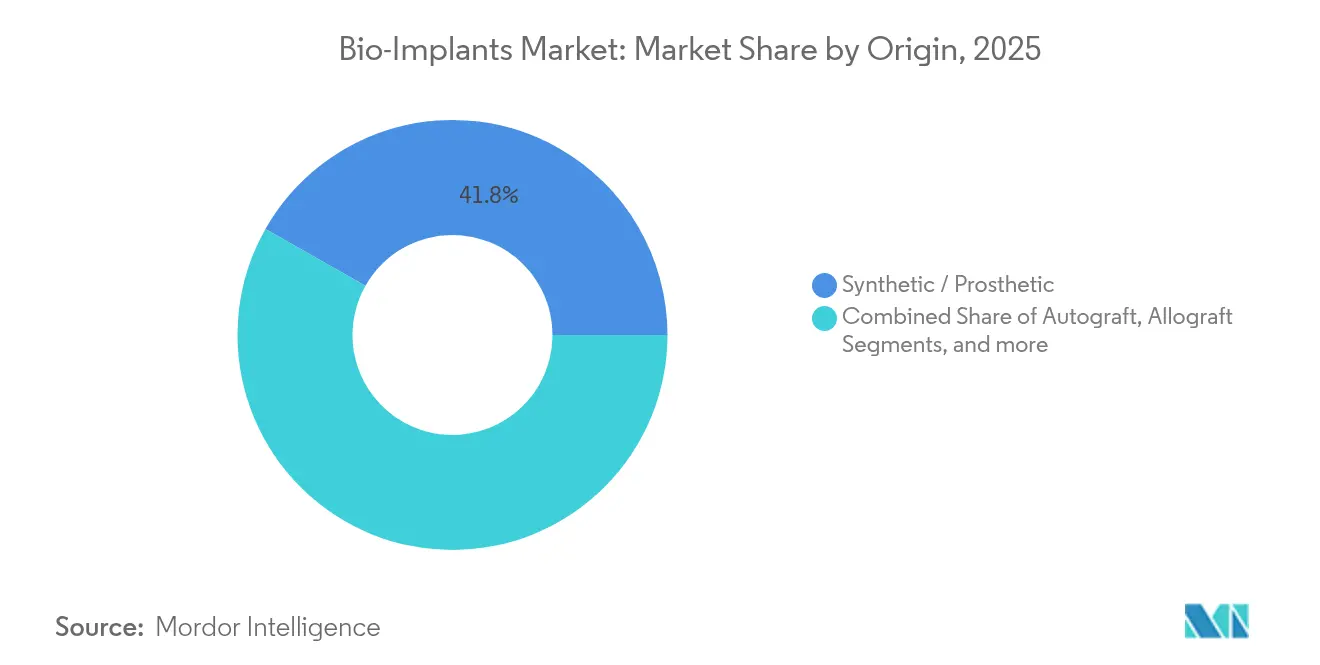

- By origin, synthetic implants held 41.80% of the bio-implants market size in 2025; xenograft materials are the fastest-advancing segment at an 8.28% CAGR.

- By end user, hospitals dominated with 53.66% of the bio-implants market share in 2025; specialty clinics are accelerating at an 8.19% CAGR through 2031.

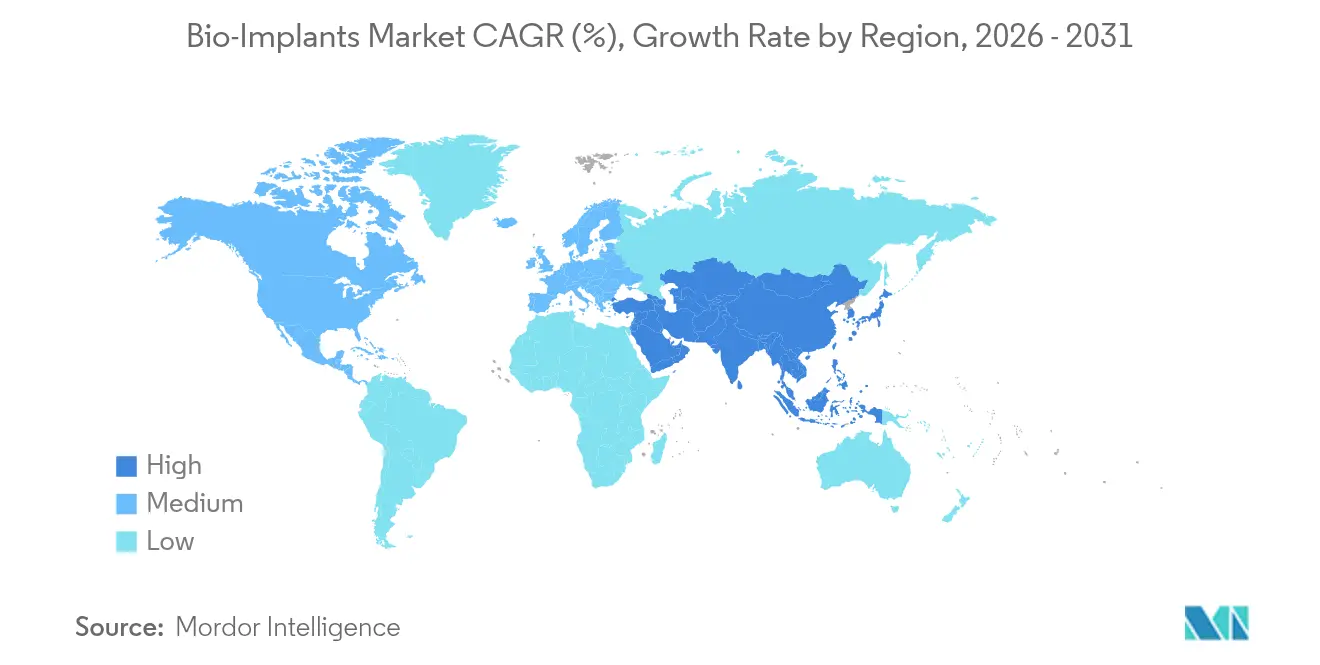

- By geography, North America commanded 48.12% revenue in 2025, whereas Asia-Pacific is set to record an 8.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bio-Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic & lifestyle diseases | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Growing preference for minimally-invasive surgeries | +1.2% | North America and EU; spreading to Asia-Pacific | Medium term (2-4 years) |

| Aging population accelerating joint-replacement volumes | +1.5% | Global, led by North America, Europe, Japan | Long term (≥ 4 years) |

| Surge in 3-D-printed, patient-specific implants | +0.9% | North America & EU core; adoption rising in Asia-Pacific | Medium term (2-4 years) |

| Commercialization of bioresorbable & smart sensor-enabled implants | +1.1% | Early uptake in developed markets, spreading globally | Medium term (2-4 years) |

| Value-based-care bundles boosting implant uptake in emerging markets | +0.7% | Asia-Pacific, Latin America, Middle East & Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic & Lifestyle Diseases

Diabetes, cardiovascular disease, and musculoskeletal disorders are reshaping demand patterns. Genentech’s Susvimo received United States Food and Drug Administration (FDA) approval in 2025 as the first continuous ocular drug-delivery implant needing only twice-yearly refills, underscoring how multifunctional devices now address chronic pathologies with fewer interventions. Healthcare systems in high-income countries are pivoting toward proactive management, favoring long-lasting implants that reduce rehospitalization.

Growing Preference for Minimally-Invasive Surgeries

Ambulatory surgery centers performed 44 million procedures in 2024 and will keep expanding as payers reimburse outpatient joint replacements. Implant manufacturers respond by creating devices optimized for shorter operative windows and same-day discharge protocols, increasing the addressable bio-implants market well beyond traditional hospital theatres.

Aging Population Accelerating Joint-Replacement Volumes

The global 65+ cohort is on track to double by 2050, and younger recipients now expect implants to survive 30+ years. Firms such as Zimmer Biomet are investing in wear-resistant surfaces that limit osteolysis and extend functional life. Patient-specific designs that map nuanced anatomical variations are gaining traction as longevity and fit become central purchase criteria.

Surge in 3-D-Printed, Patient-Specific Implants

Regulators have cleared restor3d’s total talus prosthesis, illustrating a clear pathway for additively manufactured patient-matched devices. Hospitals are installing point-of-care printers to shorten lead times and control inventory, a shift that broadens access and reduces waste. Lattice structures promoting bone ingrowth further enhance long-term fixation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unfavorable / fragmented reimbursement pathways | -1.2% | Worldwide, with larger drag in emerging markets | Long term (≥ 4 years) |

| High upfront cost of advanced implants | -0.8% | Global, most acute in price-sensitive regions | Medium term (2-4 years) |

| Supply-chain vulnerability for specialty biomaterials | -0.6% | Global | Medium term (2-4 years) |

| ESG & lifecycle-impact scrutiny delaying approvals | -0.5% | Global, affected more in developed regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Implants

Premium sensor-based devices remain expensive, making payers hesitate in regions where capital budgets are constrained. Suppliers are developing tiered portfolios so health systems can match functionality to economic reality without halting innovation.

Unfavorable / Fragmented Reimbursement Pathways

Regulators often approve technology years before reimbursement schedules adapt. Medicare’s 2025 draft guidance on clinical endpoints for knee osteoarthritis reflects ongoing attempts to align evidence standards, yet global inconsistency still delays commercialization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Bio-Implants: Cardiovascular Innovation Drives Growth

Orthopedic devices represented the single-largest revenue block in 2025, contributing 27.58% of the bio-implants market share. Cardiovascular implants, however, deliver the highest momentum with an 8.23% CAGR, powered by transcatheter valves and implantable hemodynamic sensors. The segment benefits from FDA breakthrough-device designations such as BiVACOR’s total artificial heart that target end-stage failure. Over the forecast horizon, smart pacemakers integrated with remote telemetry will further enlarge the cardiovascular footprint within the bio-implants market.

Orthopedic innovation stays robust through robotic guidance and improved tribology that extends bearing life. Neuro-stimulators leverage adaptive algorithms to recalibrate in response to patient feedback, while cochlear implants inch toward fully implantable form factors; the category is projected to reach USD 986.4 million by 2031. Ophthalmic platforms like Susvimo re-shape treatment frequency expectations, reinforcing steady demand across all implant lines.

By Material: Composite Innovation Challenges Metal Dominance

Metals and alloys accounted for 43.72% of 2025 revenue thanks to titanium’s unmatched strength-to-weight ratio, but composites will grow the fastest at 8.12% as polyether-ether-ketone (PEEK) and polylactic acid (PLA) variants mitigate stress shielding. Ceramics doped with antimicrobial silver ions diminish infection risk, and bio-active glass matrices encourage osteogenesis without inflammatory cascade. Gradient builds that shift from rigid cores to compliant outer zones imitate natural tissue and broaden indications for soft-tissue repair.

By Origin: Synthetic Dominance with Xenograft Acceleration

Synthetic constructs maintained a 41.80% revenue lead in 2025, valued for consistency and unlimited supply. Xenografts register the swiftest advance at 8.28% CAGR as decellularization protocols strip immunogenic proteins yet retain osteoinductive cues; dentin-derived xenograft powder now supports maxillofacial reconstruction. Allografts remain essential in complex spine fusion where autograft harvest volume is limited. Surgeons increasingly deploy hybrid grafting approaches that pair allograft carriers with bio-active xenograft fillers, improving volumetric stability.

By End User: Specialty Clinics Emerge as Growth Leaders

Hospitals retained 53.66% of 2025 sales as complex cardiac and neuro cases still require intensive settings. The specialty-clinic channel, however, is expanding at an 8.19% CAGR, buoyed by payer approval for outpatient shoulder and knee arthroplasty. Becker’s ASC Review notes that robotics and navigation now migrate to ambulatory theatres, enabling same-day discharge without compromising outcomes. Focused implant centers that bundle surgical and rehabilitation services deliver predictable pathways attractive to value-based purchasers.

Geography Analysis

North America held 48.12% of global revenue in 2025 as reimbursement parity and advanced R&D ecosystems speed adoption of closed-loop neuro-stimulators like Medtronic’s BrainSense platform, cleared by the FDA in 2025. Cross-border patient flows from Canada and Mexico further support procedure growth while diversified payer mixes stabilize price realization.

Asia-Pacific is the fastest-moving bio-implants market at an 8.11% CAGR. China supports domestic manufacturing, India aligns its regulatory code with international standards, and Japan’s super-aged society prioritizes joint and cardiac devices. Digital health infrastructure in South Korea accelerates remote monitoring uptake, and Australian research hubs host pivotal trials that de-risk regional launches.

Europe wrestles with Medical Device Regulation (MDR) certification bottlenecks—only 43 notified bodies oversee half-a-million devices—slowing market entry. Transition extensions to 2027 grant limited reprieve, yet firms must still meet stringent environmental requirements incorporated into new procurement criteria. Sustainability-minded hospitals increasingly request lifecycle analyses and recyclable packaging as part of tender bids.

Regulatory Landscape

Bio-implants are regulated as medical devices across major markets, with higher-risk implantables subject to the most stringent premarket review and post-market surveillance. In the United States, the FDA uses a risk-based approach (including 510(k), De Novo, and PMA pathways). In February 2026, the Quality Management System Regulation (QMSR) became effective, tightening and modernizing quality-system expectations that manufacturers must meet across design, production, and corrective-action processes.

In Europe, the EU Medical Device Regulation (MDR 2017/745) continues to shape conformity assessment through notified bodies, and ongoing bottlenecks keep compliance planning central for implant suppliers. The European Commission adopted Implementing Regulation (EU) 2026/977 on May 4, 2026, establishing uniform quality management and procedural requirements for notified body conformity-assessment activities, which affects timelines and evidence packages for Class IIb and Class III implantable devices. Regulators are also issuing more device-specific directions, including the FDA final guidance (May 2026) on patient-matched guides for orthopedic implants and the FDA reclassification (effective June 5, 2026) of certain resorbable calcium salt bone void fillers containing an aminoglycoside antibacterial into Class II with special controls.

Competitive Landscape

The bio-implants market is moderately consolidated. Johnson & Johnson’s DePuy Synthes portfolio covers orthopedics, trauma, and sports medicine, delivering an estimated 13% revenue share in 2024. Medtronic adds 4.86% with leadership in cardiovascular and neuromodulation. Strategic acquisitions illustrate a push toward full-line musculoskeletal offerings, exemplified by Enovis closing a EUR 800 million purchase of LimaCorporate to access patient-matched shoulder implants[3]Enovis Corporation, “Completion of LimaCorporate Acquisition,” enovis.com. Globus Medical’s USD 250 million takeover of Nevro extends its spine footprint into pain neuromodulation.

Digital differentiation is rising. Major vendors embed AI-driven planning software that pairs with sensor-laden hardware, creating data ecosystems difficult for smaller rivals to match. Academic-industry partnerships are accelerating intellectual-property creation in adaptive neuro-stimulators, and university spin-outs supply specialized algorithms that optimize closed-loop control. Sustainability positions compound competitive advantage as hospitals add environmental metrics to scorecards.

Bio-Implants Industry Leaders

ZimmerBiomet

Smith & Nephew Plc

Edwards

BioTronik Plc

aap Implantate AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and clinical-evidence shifts are creating whitespace for established implant categories and patient-specific workflows. In the EU, two delegated regulations adopted in March 2026 (published as EU 2026/1359 and EU 2026/1451) expanded the lists of Class IIb implantable and Class III devices benefiting from exemptions tied to technical documentation assessments and clinical investigation requirements under MDR. For implant suppliers, that provides a clearer path for well-established technologies while easing some notified-body load. These changes map onto manufacturer roadmaps for orthopedic and cardiovascular implant lines, where patient-matched solutions and procedure-enabling accessories are increasingly bundled into the competitive offer.

Cardiovascular and neurovascular platforms are also attracting active investment and portfolio integration, supporting opportunities in transcatheter therapies, minimally invasive access, and adjacent implant-enabled care pathways. Boston Scientifics May 2026 USD 1.5 billion strategic investment in MiRus (including rights to a nickel-free balloon-expandable TAVR system) and Medtronics June 2026 completion of the Scientia Vascular acquisition (neurovascular access) point to continued platform-building beyond single-device launches. The same pattern is visible in regenerative and long-duration implant concepts, including Xeltis initiating European commercialization of its aXess vascular access implant with a first commercial implant in July 2026, and Vivani Medicals July 2026 agreement with Novo Nordisk to evaluate a semaglutide implant (NanoPortal platform) for chronic weight management.

Recent Industry Developments

- July 2026: Paragon 28 announced the U.S. commercial launch of its Bone Transport System. The launch broadens options in limb reconstruction workflows that rely on implantable systems designed for complex orthopedic cases. It also supports competitive differentiation in a segment where procedural efficiency and reproducible outcomes influence adoption.

- December 2025: Edwards Lifesciences received U.S. FDA approval for the SAPIEN M3 transcatheter mitral valve replacement system to treat symptomatic moderate-to-severe or severe mitral regurgitation. The approval expands transcatheter therapy availability in structural heart, supporting a larger addressable patient pool for implantable valve systems. It also reinforces the shift toward minimally invasive cardiovascular implants moving from trials into routine clinical use.

- May 2024: The market continued to incorporate sensor-enabled and remotely monitored implant concepts into routine care pathways, alongside broader migration of procedures to outpatient and specialized settings. This shift increased emphasis on integrated ecosystems that combine implants, software, and care management. Manufacturers prioritized designs and data capabilities aligned with shorter stays and longitudinal monitoring needs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the bio implants market is defined as the global value of implantable medical products designed to replace, support, or enhance body structures, measured at the point of sale into healthcare delivery settings.

Scope exclusions: We exclude non-implant external prosthetics, disposable surgical tools used during implantation, and routine follow-up services that are billed separately from the implant device.

Segmentation Overview

- By Type of Bio-Implants

- Cardiovascular Implants

- Orthopedic Implants

- Spinal Implants

- Dental Implants

- Ophthalmic Implants

- Neurological & Cochlear Implants

- Other Implants

- By Material

- Metals & Alloys

- Polymers

- Ceramics & Bio-active Glass

- Composite & Hybrid Biomaterials

- Other Materials

- By Origin

- Autograft

- Allograft

- Xenograft

- Synthetic / Prosthetic

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial market structure, align definitions across implant categories, and collect country-level demand signals that later feed the model. We typically rely on public health and trade sources such as the World Health Organization, OECD health statistics, the US FDA public databases, Eurostat, and the World Bank for population aging, procedure proxies, and healthcare spend indicators.

On the commercial side, we also reviewed annual reports and investor presentations, along with regulatory and reimbursement updates and hospital system publications where available. A paid subscription for company financials and intelligence was used to cross-check reported implant revenues at a consolidated level, and a patent database was used to sense where material and design innovation is moving (for example, bioresorbable and sensor-enabled concepts). The desk research sources listed here are illustrative only, and we used additional public and paid sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done to pressure-test assumptions behind volumes, pricing, and adoption timing across major implant families, then confirm where demand shifts by region. We spoke with a mix of manufacturers, distributors, clinicians, and procurement stakeholders across APAC, EMEA, and the Americas, which helped close gaps left by public statistics and improved the final market splits and growth rates.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | APAC: 41% |

| Mid tier: 53% | Functional/Unit leaders: 41% | EMEA: 35% |

| Smaller Players: 19% | Managers: 43% | Americas: 24% |

Market-Sizing & Forecasting

Sizing started with a top-down build in which procedure-linked demand pools were reconstructed by implant family, then converted into value using typical unit intensity and average selling price ranges by region. To keep the model realistic, we corroborated results with selective bottom-up approximations, including sampled supplier revenue roll-ups and channel checks that connect shipped mix with observed pricing.

For bio implants, we tracked inputs such as the aging population share, orthopedic and cardiovascular procedure trends, implant penetration within eligible patient cohorts, the shift toward ambulatory surgical centers, and pricing movement driven by material choice (metals, polymers, ceramics) and reimbursement conditions. Where direct volume indicators were missing in smaller countries, proxy ratios were applied from comparable markets and then adjusted using healthcare spend per capita and specialist availability to avoid distorting totals.

For forecasting, we ran scenario analysis around procedure growth and price erosion or premiumization, and then applied a multivariate regression check at the regional level to keep the trajectory aligned with macro health spend and demographic change. Assumptions that were weak in desk research were re-checked during interviews, and only then were final growth rates applied to the modeled base year.

Data Validation & Update Cycle

Validation was done through triangulation across independent signals, followed by stepwise variance checks at category and regional levels before final sign-off. When a market output moved outside reasonable bounds, we traced it back to the driver level and re-checked volumes, pricing, and mix assumptions, then completed targeted re-contact with experts when needed.

Outputs were also compared against adjacent indicators, such as device import patterns, procedure growth commentary from public health bodies, and consolidated revenue disclosures, to confirm the direction was consistent. Reports are refreshed annually, and interim updates are made when a material event changes demand or pricing. Before delivery, a fresh analyst review pass is completed so clients receive the most current view possible.

Mordor Intelligence's Global Bio Implants Market Market Size Measured Against Other Published Estimates

Different published market values for bio implants often do not match because each publisher makes different choices on what counts as an implant, which year is treated as the base, and whether the number reflects manufacturer-level value or downstream hospital purchasing value. Currency timing and the way pricing is projected across mature and emerging regions also tend to widen the spread.

The biggest gaps in this market usually come from scope and value-chain treatment, especially when adjacent items like tissue engineering scaffolds, cochlear systems, or bundled service revenues are either included fully or only counted when sold as part of an implant product. Another common driver is growth posture, since some estimates assume aggressive procedure catch-up and premium materials everywhere, while others apply faster price erosion and slower adoption in cost-sensitive settings. In our work, the 2026 value is built from procedure-led demand pools and region-specific ASP logic, which keeps the device-only definition consistent across implant families, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 164.36 B (2026) | |

| Global Advisory Group A | USD 146.10 B (2025) | Uses an earlier base year and a longer forecast window, and its category totals appear to mix device value with broader bio-implant ecosystem items, which lowers comparability to a device-only 2026 figure. |

| Industry Publisher B | USD 136.96 B (2025) | Reported as a factory-gate value for 2025 and may include related services sold alongside goods, plus different pricing and growth assumptions that compress the base year level versus a demand-pool build. |

Overall, the spread in estimates is explained less by math and more by definition choices, timing, and how price and mix are carried forward. By keeping implant categories consistent, linking value to procedure-backed demand signals, and then cross-checking with selective supplier and channel indicators, the resulting number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size of the bio-implants market and how fast is it growing?

The bio-implants market is valued at USD 164.36 billion in 2026 and is projected to rise to USD 238.33 billion by 2031, registering a 7.72% CAGR.

Which implant category is expanding the quickest?

Cardiovascular implants show the strongest momentum, advancing at an 8.23% CAGR through 2031 on the back of transcatheter valves and remote-monitoring sensors.

Why are specialty clinics gaining share from hospitals?

Payer approval for outpatient joint and shoulder arthroplasty, along with robotics migrating to ambulatory settings, is driving an 8.19% CAGR for specialty clinics.

What regions offer the highest growth potential?

Asia-Pacific leads growth with an 8.11% CAGR to 2031, buoyed by large-scale healthcare investments and streamlined regulatory pathways.

How are smart sensor-enabled implants changing business models?

Devices that stream continuous physiological data enable subscription-based monitoring services, shifting revenue away from one-time hardware sales toward recurring service income.

What is the main regulatory hurdle in Europe?

Medical Device Regulation (MDR) certification bottlenecks, caused by only 43 notified bodies handling roughly 500,000 devices, are delaying product launches and dampening regional growth.

Page last updated on: