Active Implantable Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

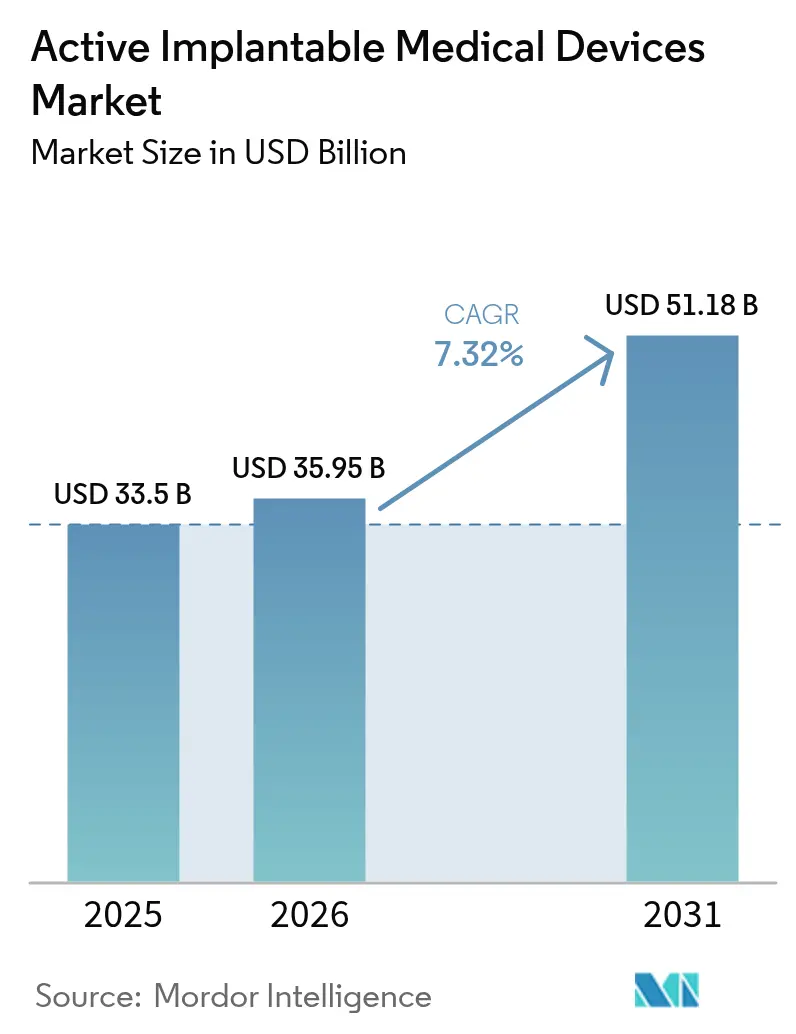

| Market Size (2026) | USD 35.95 Billion |

| Market Size (2031) | USD 51.18 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

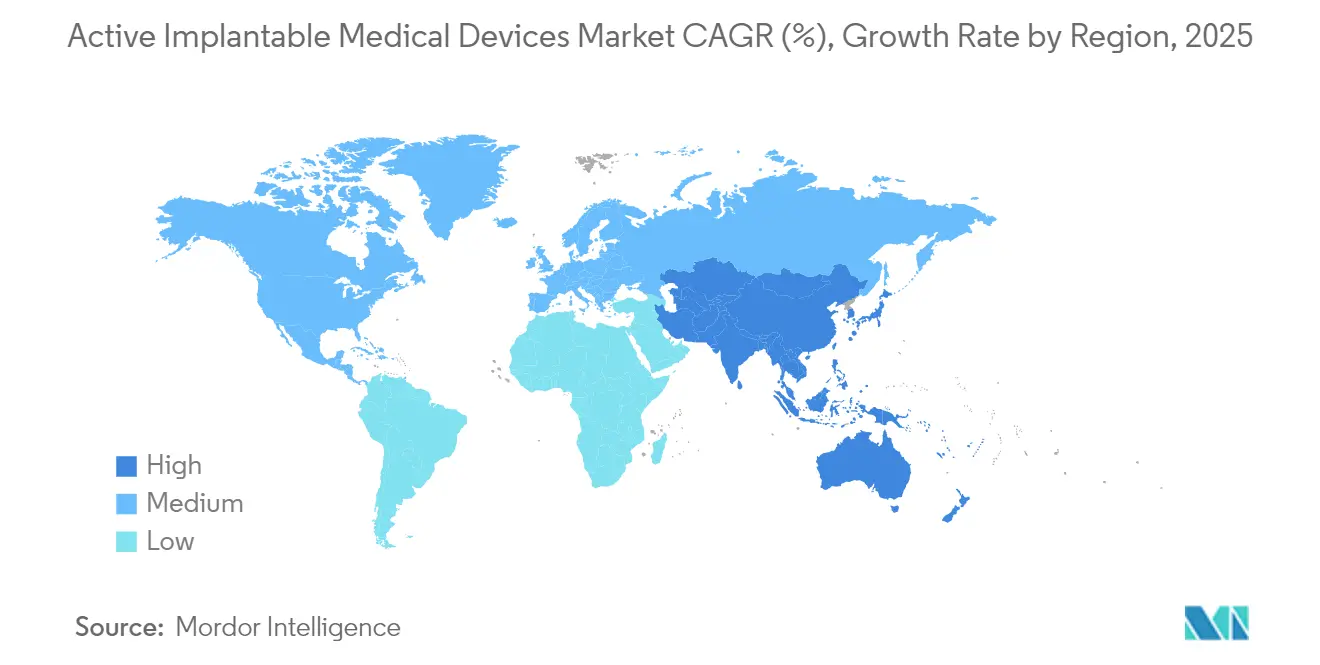

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Active Implantable Medical Devices Market Analysis by Mordor Intelligence

Active implantable medical devices market size in 2026 is estimated at USD 35.95 billion, growing from 2025 value of USD 33.50 billion with 2031 projections showing USD 51.18 billion, growing at 7.32% CAGR over 2026-2031. Rising life expectancy, rapid miniaturization of electronics, and expanding reimbursement frameworks are widening patient eligibility while shortening technology-adoption cycles. The uptake of AI-enabled remote monitoring has cut false cardiac alerts by up to 85%, easing clinician workload and increasing confidence in long-term device use. In parallel, the EU Medical Device Regulation (MDR) has extended transition deadlines to December 2027 for Class III implants, channeling demand toward manufacturers with strong quality systems[1]European Commission, “Medical Device Regulation Transition Update,” ec.europa.eu. Stabilization of the semiconductor supply chain after 2024 shortages is restoring production of sub-centimeter components essential for leadless and wireless architectures[2]U.S. Food & Drug Administration, “Breakthrough Devices Program,” fda.gov. Together, these dynamics reinforce a steady scale-up trajectory for the Active implantable medical devices market through 2030.

Key Report Takeaways

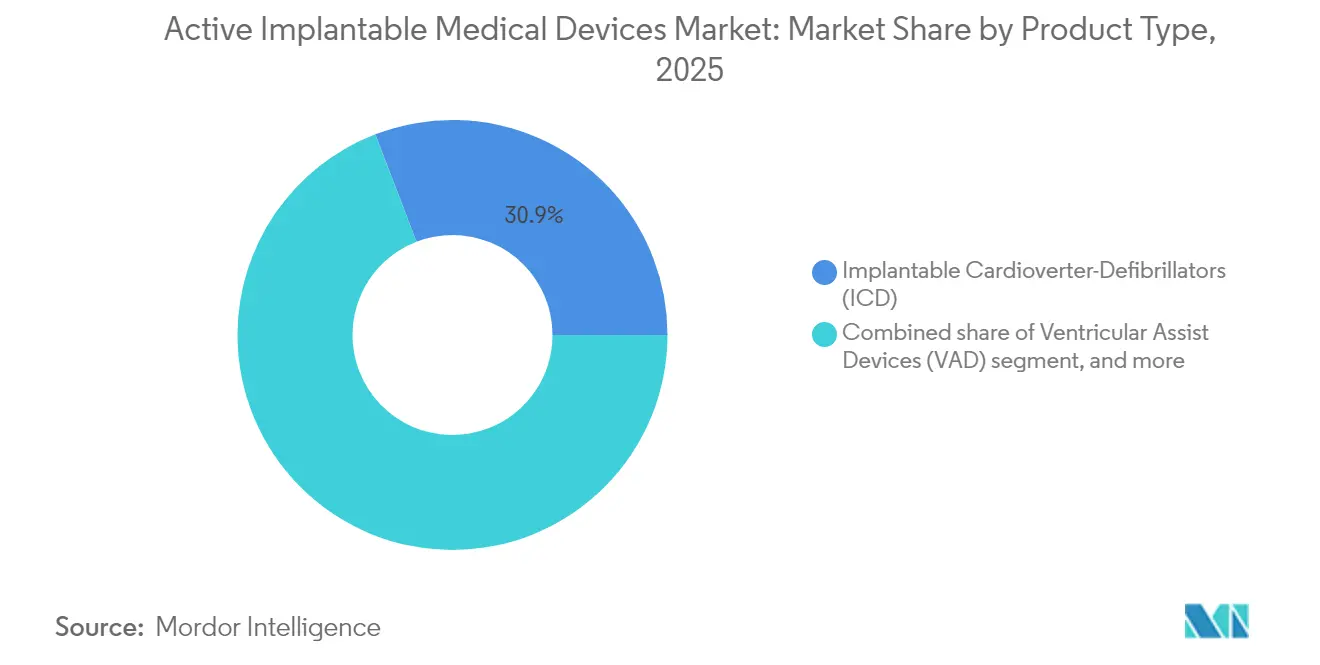

- By product type, implantable cardioverter-defibrillators led with 30.85% of the Active implantable medical devices market share in 2025, while implantable hearing devices are forecast to post a 9.05% CAGR to 2031.

- By application, cardiovascular disorders accounted for 54.90% of the Active implantable medical devices market size in 2025, and hearing-loss therapies are projected to advance at a 10.15% CAGR through 2031.

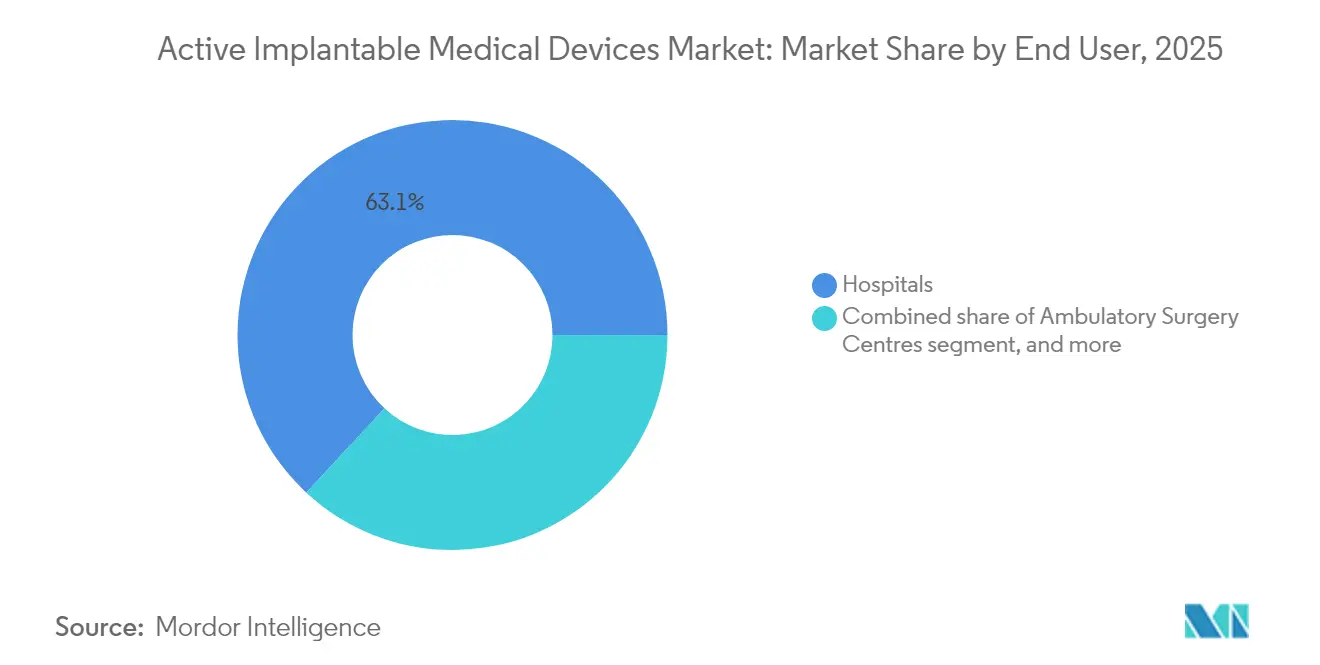

- By end user, hospitals controlled 63.10% revenue in 2025, yet specialty and ENT clinics are expected to expand at a 9.92% CAGR during 2026-2031.

- By technology, MRI-compatible devices captured 40.10% of the Active implantable medical devices market size in 2025, whereas leadless and wireless systems should rise at a 9.18% CAGR to 2031.

- By geography, North America dominated with 38.10% share in 2025, and Asia-Pacific is on track for an 8.32% CAGR, reflecting China’s volume-based procurement and Japan’s super-aged demographics.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Active Implantable Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Cardio-, Neuro- & Otologic Disorders | +1.8% | Global, concentrated in aging OECD markets | Long term (≥ 4 years) |

| Rapid Miniaturisation & MRI-Safe / Lead-Less Design Innovations | +1.5% | North America & EU leadership, accelerating APAC adoption | Medium term (2-4 years) |

| Ageing Population Expanding Implant-Eligible Pool | +1.2% | Japan, Germany, Italy, global ripple | Long term (≥ 4 years) |

| Favourable Reimbursement Expansion In OECD & China | +1.0% | OECD countries and China | Medium term (2-4 years) |

| AI-Enabled Remote Monitoring Algorithms Improving Real-World Outcomes | +0.9% | Early uptake in North America & EU, APAC following | Short term (≤ 2 years) |

| Breakthrough Bio-Resorbable Electronics Eliminating Explant Surgeries | +0.4% | Research hubs in US, EU, selected APAC centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardio-, Neuro- & Otologic Disorders

Heart failure impacts more than 64 million people worldwide and atrial fibrillation is expected to reach 17.9 million cases in developed markets by 2030, intensifying demand for implantable cardioverter-defibrillators and resynchronization devices. Parkinson’s disease affects around 10 million patients globally, spurring adoption of adaptive deep-brain stimulation systems that modulate therapy in real time. WHO forecasts that hearing loss will affect 700 million people by 2050, a trend accelerating cochlear-implant usage as fully implantable designs erase cosmetic barriers. Co-morbid disease profiles are also becoming more common, prompting multi-device implantation and underpinning sustained growth in the Active implantable medical devices market.

Rapid Miniaturization & MRI-Safe Leadless Design Innovations

Leadless pacemakers have shrunk to volumes below 1 cm³ while retaining 10-year battery life, and devices like Abbott’s AVEIR dual-chamber system synchronize atrioventricular pacing without transvenous leads. MRI protocols have progressed from conditional to fully unrestricted scanning at 3 Tesla, removing long-standing imaging barriers for device patients. Precision Neuroscience’s Layer 7 cortical interface, hosting 1,024 hair-thin electrodes, exemplifies the fine-scale fabrication now achievable. Bio-resorbable pacemakers that dissolve after therapy completion have completed first-in-human feasibility trials, hinting at a future where explant surgery becomes unnecessary. These advances lower infection risks, simplify procedures, and widen patient selection, strengthening momentum in the Active implantable medical devices market.

Ageing Population Expanding Implant-Eligible Pool

By 2030 the global population aged 65 years and older will reach 771 million, putting Japan at 29% senior share and Europe not far behind[3]United Nations, “World Population Prospects 2024,” un.org. Age-related arrythmias, neurodegenerative diseases, and sensory deficits collectively raise implant demand across cardiology, neurology, and otology specialties. Transcatheter techniques now allow minimally invasive ventricular assist device placement in frail patients who previously were not surgical candidates. Candidate criteria for cochlear implants have widened to include single-sided deafness and moderate hearing loss, boosting potential volume in an otherwise under-penetrated indication. Governments and insurers encourage such therapies to maintain older adults’ independence, cementing a demand floor for the Active implantable medical devices market.

Favourable Reimbursement Expansion in OECD & China

China’s volume-based procurement (VoBP) program has slashed cochlear-implant prices from 200,000 RMB to 50,000 RMB, quadrupling coverage eligibility under the National Medical Security Fund[4]National Healthcare Security Administration, “Volume-Based Procurement Device List,” nhsa.gov.cn. In the United States, the FDA Breakthrough Device pathway shortens review cycles for novel implants and triggers parallel Medicare coverage, exemplified by recent approvals in adaptive DBS and conduction system pacing. The EU MDR, despite early backlogs, ultimately standardizes evidence requirements and reduces multi-country duplication costs, benefitting large-scale launches across Europe. Value-based payer contracts reward devices that cut hospital readmissions, aligning fiscal incentives with technology that improves outcomes. Collectively these policy shifts underpin predictable reimbursement flows for the Active implantable medical devices market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device & Procedure Cost In Emerging Markets | −1.1% | Latin America, Southeast Asia, Sub-Saharan Africa | Medium term (2-4 years) |

| Stringent Cyber-Security / Regulatory Hurdles Lengthen Approvals | −0.8% | Global, notably EU & US | Short term (≤ 2 years) |

| Semiconductor Supply Bottlenecks For Ultra-Miniature Components | −0.6% | Global electronics value chain | Short term (≤ 2 years) |

| Battery-Material Sustainability Pressures On Lithium-Iodine Chemistry | −0.4% | Global, with emphasis on EU sustainability mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device & Procedure Cost in Emerging Markets

In many low- and middle-income regions, implant prices still exceed annual household income, limiting penetration to wealthy urban populations. Only 19% of residents in these economies have access even to basic diagnostics, highlighting systemic care gaps. Currency depreciation further inflates import costs for devices priced in hard currencies, while fragmented insurance coverage pushes most payments out of pocket. Local manufacturing policies in India and Brazil offer tax incentives, yet high-risk implant categories require specialized cleanroom production and intellectual property portfolios that few domestic firms possess. Training deficits compound the barrier, as implant procedures demand electrophysiologists and otologic surgeons who remain concentrated in flagship hospitals. Until financing models mature, cost will continue to cap the Active implantable medical devices market in numerous emerging territories.

Stringent Cybersecurity & Regulatory Hurdles Lengthen Approvals

The 2025 US PATCH Act obliges companies to embed real-time threat monitoring and software patching into all network-connected implants, increasing design complexity and audit requirements. In Europe, only 43 notified bodies handle roughly half a million device dossiers, stretching certification timelines for Class III implants to 24 months. Software-as-a-medical-device rules now require stand-alone clinical trials for embedded AI algorithms, a financial load that smaller innovators struggle to absorb. Post-market surveillance mandates 100% complaint trending and annual performance updates, compelling firms to invest in dedicated vigilance teams. These layers consolidate share toward multinationals capable of absorbing compliance overhead, tempering new-entry velocity into the Active implantable medical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Defibrillators Maintain Lead, Hearing Devices Accelerate

Implantable cardioverter-defibrillators captured a 30.85% slice of the Active implantable medical devices market size in 2025 thanks to their life-saving role in sudden-cardiac-death prevention among roughly 6 million US heart-failure patients. Subcutaneous and leadless formats reduce infection risk and enable MRI access, sustaining steady replacement cycles. Pacemakers stay relevant because dual-chamber leadless designs now correct complex arrhythmias without transvenous leads. Ventricular assist devices profit from magnetically levitated pumps that cut thrombosis, doubling two-year survival compared with previous generations.

Implantable hearing devices post the fastest trajectory at a 9.05% CAGR through 2031 as totally implantable cochlear implants enter pivotal trials and promise round-the-clock sound without external processors. Early data from MED-EL’s TICI feasibility study showed speech-recognition parity with standard models and higher patient satisfaction. Neurostimulators also benefit from closed-loop capabilities that cut overstimulation by 89%, while insertable loop recorders and drug-infusion pumps gain from personalized chronic-disease management. These dynamics collectively deepen product diversity and future-proof the Active implantable medical devices market.

By Application: Cardiovascular Dominance Faces Hearing-Loss Disruption

Cardiovascular disorders retained 54.90% of the Active implantable medical devices market size in 2025 driven by escalating heart-failure prevalence and broadening indications for conduction-system pacing and resynchronization. Abbott’s TriClip device reduced moderate-or-greater tricuspid regurgitation by 84% and improved Kansas City Cardiomyopathy Questionnaire scores, highlighting structural-heart opportunities. Neurological applications remain steady because adaptive deep-brain stimulation widens clinical benefit to previously refractory Parkinson’s subtypes.

Hearing-loss treatment is growing at a 10.15% CAGR to 2031 as WHO projects 700 million affected individuals, and fully implantable solutions erase long-standing stigma. Chronic pain management sees rising adoption of AI-driven spinal cord stimulators that auto-calibrate dosing, reducing opioid reliance. Endocrine use cases, such as closed-loop insulin delivery, represent an emerging adjacency that could inject fresh volume into the Active implantable medical devices market.

By End User: Hospitals Hold Scale, Specialty Centers Outpace

Hospitals controlled 63.10% revenue in 2025 due to broad infrastructure, intensive-care support, and teaching affiliations that accommodate complex ventricular assist or dual-chamber leadless implants. Academic medical centers serve as early-adopter hubs, accelerating diffusion to community facilities once procedural learning curves flatten.

Specialty and ENT clinics are projected to rise at 9.92% CAGR as minimally invasive techniques permit same-day discharge for pacemaker and cochlear-implant placements. Ambulatory surgery centers now manage straightforward battery replacements and loop-recorder insertions safely under local anesthesia. The home-care frontier is opening through connected cardiac monitors and cloud analytics, creating decentralised follow-up pathways that shrink hospital footprints yet enlarge the Active implantable medical devices market.

By Technology: MRI-Compatible Devices Dominate, Wireless Approaches Surge

MRI-compatible platforms commanded 40.10% share in 2025 because unrestricted imaging removes a critical treatment barrier for patients needing oncology or musculoskeletal scans. Abbott’s no-wait technology eliminated the traditional 6-week post-implant hold, enhancing patient throughput.

Leadless and wireless systems are forecast for a 9.18% CAGR, spurred by freedom from lead fractures that occur in 2-3% of conventional implants and require costly revisions. Abbott’s AVEIR dual-device communication proves multi-point pacing without physical leads, while rechargeable or bio-resorbable power sources promise to reduce future explants. Conventional devices persist in price-sensitive regions but face gradual substitution as economies of scale push premium-technology costs downward, broadening the worldwide Active implantable medical devices market.

Geography Analysis

North America held 38.10% of 2025 sales, fueled by Medicare coverage of breakthrough devices and a dense ecosystem linking academia, industry, and venture capital. The FDA Breakthrough Device pathway has compressed cardiac and neuro device approvals to under 150 days on average, allowing rapid clinician adoption. Robust reimbursement and established referral networks support high procedural volumes for leadless pacing and adaptive DBS systems. Yet value-based payment initiatives are pressuring suppliers to evidence longitudinal cost offsets, ushering in risk-sharing contracts that could reshape the Active implantable medical devices market’s pricing structure.

Asia-Pacific is set to grow at 8.32% CAGR between 2026 and 2031 thanks to China’s VoBP cost resets and accelerated National Medical Products Administration approvals of 270 innovative implants since 2017. Japan’s super-aged society fuels demand for small, long-life devices, while South Korea’s advanced fabrication capacity positions it as a leading export hub. India’s Production Linked Incentive scheme is drawing global OEMs to set up local final assembly, trimming logistics costs and supporting broader regional access. These shifts elevate Asia-Pacific’s weighting in the Active implantable medical devices market and create scale efficiencies for global suppliers.

Europe is navigating MDR transition bottlenecks that delay certification yet ultimately harmonize evidence standards. Germany remains a powerhouse in electrophysiology, and France’s digital-health reimbursement framework incentivizes AI-linked implants. Brexit adds a parallel UK approval pathway, raising planning complexity for dual-region launches. Nonetheless, the continent’s ageing demographic and universal coverage still assure steady device demand. Once notified-body capacity normalises, pent-up approvals could yield a release of new products and reinforce Europe’s place within the Active implantable medical devices market.

Competitive Landscape

The active implantable medical devices market is moderately concentrated, with Medtronic, Abbott, and Boston Scientific collectively approaching 55% global revenue. These multinationals deploy USD 2 billion-plus annual R&D budgets and operate vertically integrated manufacturing that secures microelectronic supply. AI-augmented therapy is a core differentiator: Medtronic’s BrainSense adaptive DBS is the first closed-loop Parkinson’s implant to adjust stimulation based on sensed neural activity, improving symptom control without manual reprogramming.

Strategic acquisitions are reshaping portfolios. Stryker’s USD 4.9 billion bid for Inari Medical extends its implant reach into mechanical thrombectomy and peripheral intervention. Globus Medical’s USD 250 million purchase of Nevro brings high-frequency neuromodulation assets into its spine franchise. Boston Scientific’s buyout of Silk Road Medical strengthens its presence in transcarotid access for stroke prevention, enhancing cross-selling depth.

Emerging firms are pushing new frontiers such as fully implantable cochlear devices, bio-resorbable scaffolds, and wireless brain-computer interfaces. However, tightening cybersecurity, MDR compliance, and capital intensity raise entry barriers, giving incumbents time to integrate these approaches before disruptive scale is achieved. The convergence of software, power-management, and biocompatible materials will likely dictate competitive reshuffling within the Active implantable medical devices market over the coming decade.

Active Implantable Medical Devices Industry Leaders

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

Cochlear Limited

BIOTRONIK SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA approves ENCELTO implant to deliver ciliary neurotrophic factor for macular telangiectasia type 2, marking the first cell-based neuroprotective ocular implant.

- June 2025: Stryker signs agreement to acquire Inari Medical for USD 4.9 billion, adding mechanical thrombectomy solutions to its portfolio.

- April 2024: Abbott commences ASCEND CSP trial evaluating conduction-system pacing ICD lead technology.

- April 2024: Precision Neuroscience gains FDA clearance for Layer 7 wireless cortical interface with 1,024 electrodes.

- March 2025: Envoy Medical enrolls first participants in Acclaim fully implanted cochlear-implant pivotal study.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the active implantable medical devices market as every battery-powered device placed wholly or partly inside a patient for at least thirty days; examples include pacemakers, implantable cardioverter-defibrillators, ventricular assist devices, neurostimulators, cochlear and bone-anchored hearing implants, insertable loop recorders, and infusion pumps. Revenues are valued at manufacturer selling price for original and replacement units across 24 countries, using 2025 dollars.

Scope Exclusions: Passive orthopedic, dental, or contraceptive implants and all external or wearable stimulators lie outside the scope.

Segmentation Overview

- By Product Type

- Pacemakers

- Implantable Cardioverter-Defibrillators (ICD)

- Ventricular Assist Devices (VAD)

- Neurostimulators

- Spinal Cord Stimulators

- Deep Brain Stimulators

- Vagus Nerve Stimulators

- Sacral Nerve Stimulators

- Implantable Hearing Devices

- Cochlear Implants

- Bone-Anchored Hearing Systems

- Insertable Loop Recorders

- Implantable Drug-Infusion Pumps

- By Application

- Cardiovascular Disorders

- Neurological Disorders

- Hearing Loss

- Chronic Pain Management

- Endocrine & Metabolic (e.g., Diabetes)

- By End User

- Hospitals

- Ambulatory Surgery Centres

- Specialty & ENT Clinics

- Home-Care Settings

- By Technology

- MRI-Compatible Devices

- Conventional Devices

- Leadless / Wireless Implants

- Rechargeable / Bio-resorbable Power Systems

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cardiologists, neurosurgeons, ENT surgeons, payors, and hospital buyers across North America, Europe, and Asia-Pacific. Dialogues clarified MRI-safe premiums, replacement cycles, leadless uptake, and reimbursement changes, letting us tune desk assumptions.

Desk Research

We mined FDA approvals, EUDAMED alerts, CMS procedure files, WHO morbidity tables, customs codes, and Eurostat health accounts to anchor prevalence and average selling prices. AdvaMed briefs and Heart Rhythm Society sheets refined device ratios, while paid assets such as D&B Hoovers and Factiva completed supplier revenue splits. The sources named illustrate, not exhaust, our secondary pool.

Market-Sizing & Forecasting

A top-down pool mixes national counts of sudden cardiac arrest, Parkinson's, epilepsy, and severe hearing loss with observed implant penetration. Supplier roll-ups, tenders, and sampled ASP × volume tests give bottom-up checks. Inputs share aged 65+, reimbursement ceilings, MRI-safe mix, battery life, and currency trends feed multivariate regression; prices follow exponential smoothing. Regional averages close data gaps before final triangulation.

Data Validation & Update Cycle

Outputs pass variance flags, peer review, and managerial sign-off. Models refresh yearly; recalls or policy shocks prompt interim updates, and each delivery includes a final validation sweep.

Why Mordor's Active Implantable Medical Devices Baseline Earns Trust

Published figures differ because some publishers bundle passive implants, apply varied price bases, or project from dated procedure counts.

Key gap drivers include certain providers quoting distributor revenues, others dropping insertable recorders or MRI-safe variants, and several still building from 2022 volumes. Mordor's 2025 build uses live procedures, current pricing, and an annual refresh discipline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.5 B (2025) | Mordor Intelligence | - |

| USD 35.2 B (2025) | Global Consultancy A | Bundles passive stimulators; uniform ASPs |

| USD 27.7 B (2025) | Regional Consultancy B | Excludes loop recorders; uses 2023 volumes |

| USD 27.4 B (2025) | Industry Portal C | Secondary data only; no clinician checks |

Transparent scope, live variables, and ongoing expert feedback enable Mordor to deliver a repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the active implantable medical devices market?

The active implantable medical devices market generated USD 35.95 billion in 2026 and is forecast to reach USD 51.18 billion by 2031.

Which product segment holds the largest share of the market?

Implantable cardioverter-defibrillators led with 30.85% of the active implantable medical devices market share in 2025.

Which region is growing the fastest for active implantable medical devices?

Asia-Pacific is projected to expand at an 8.32% CAGR between 2026 and 2031, driven by China’s volume-based procurement and Japan’s aging population.

How are AI-enabled features influencing the market?

AI-driven remote monitoring has reduced false cardiac alerts by up to 85% and is spurring broader adoption of next-generation implants across cardiology and neurology.

What technological trend is most disrupting traditional implant designs?

Leadless and wireless implants, which eliminate transvenous leads and related complications, are advancing at a 9.18% CAGR and reshaping device selection criteria.

Why do specialty and ENT clinics show rapid growth in device implantation?

Minimally invasive techniques now allow same-day discharge for many procedures, letting specialty clinics perform high-volume implantations efficiently and fueling a 9.92% CAGR in this setting.

Page last updated on: