Single-Use Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

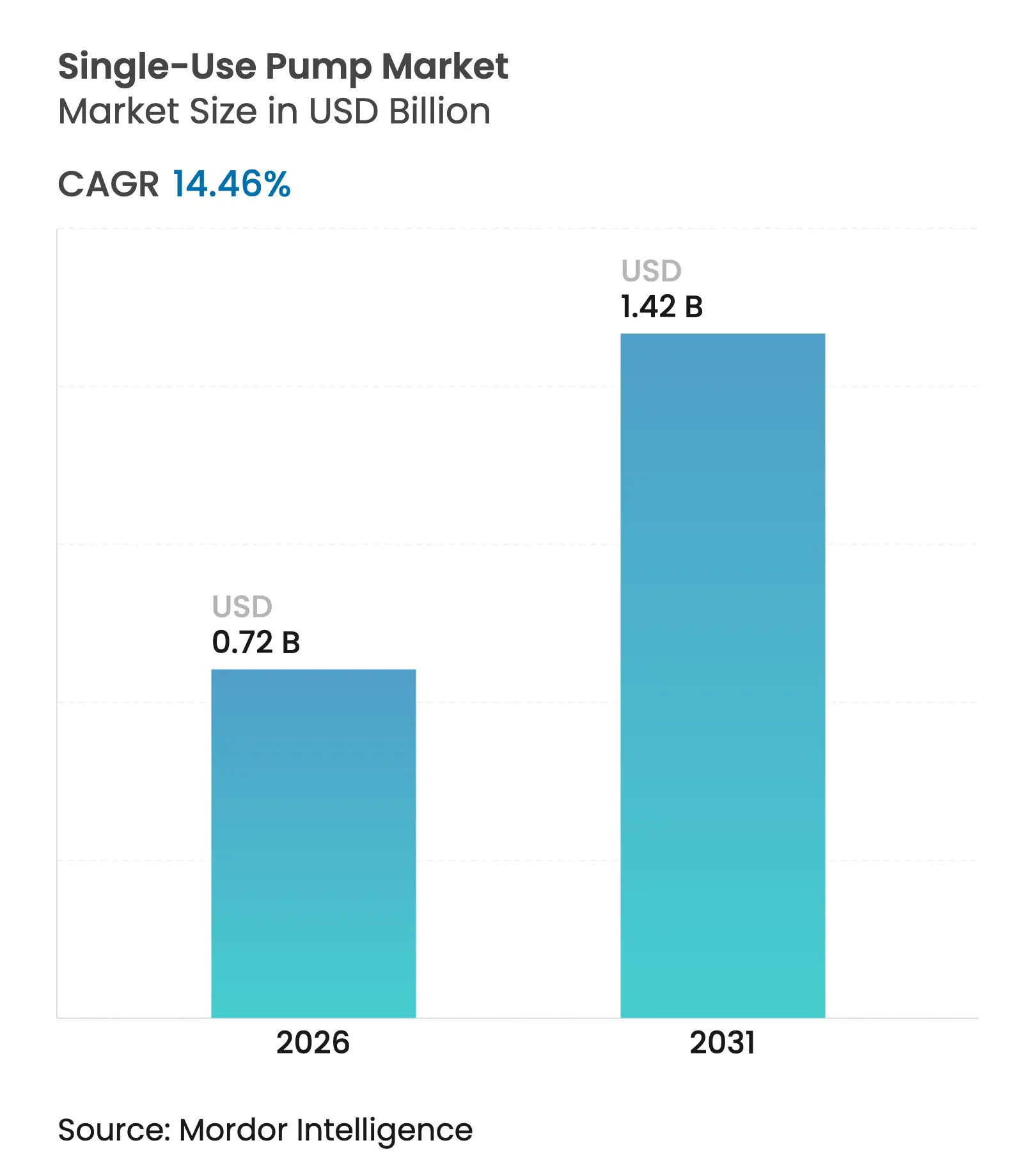

| Market Size (2026) | USD 0.72 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 14.46 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Single-Use Pump Market Analysis by Mordor Intelligence

Single-use pump market size in 2026 is estimated at USD 0.72 billion, growing from 2025 value of USD 0.63 billion with 2031 projections showing USD 1.42 billion, growing at 14.46% CAGR over 2026-2031. Strong momentum follows the biopharmaceutical shift toward disposable production lines that eliminate cross-contamination risk and shorten cleaning validation cycles. Growth is reinforced by rapid biologics capacity expansions, steady innovation in low-shear peristaltic and diaphragm designs, and the aggressive build-out of contract development and manufacturing organization (CDMO) facilities seeking flexible scale-up options. Investors view single-use fluid handling as a route to cut time-to-market for advanced therapies, while equipment suppliers capture rising demand for modular, automation-ready systems. Competitive intensity remains moderate, with a blend of diversified flow-technology firms and niche specialists racing to widen portfolios through acquisitions and joint development programs.

Key Report Takeaways

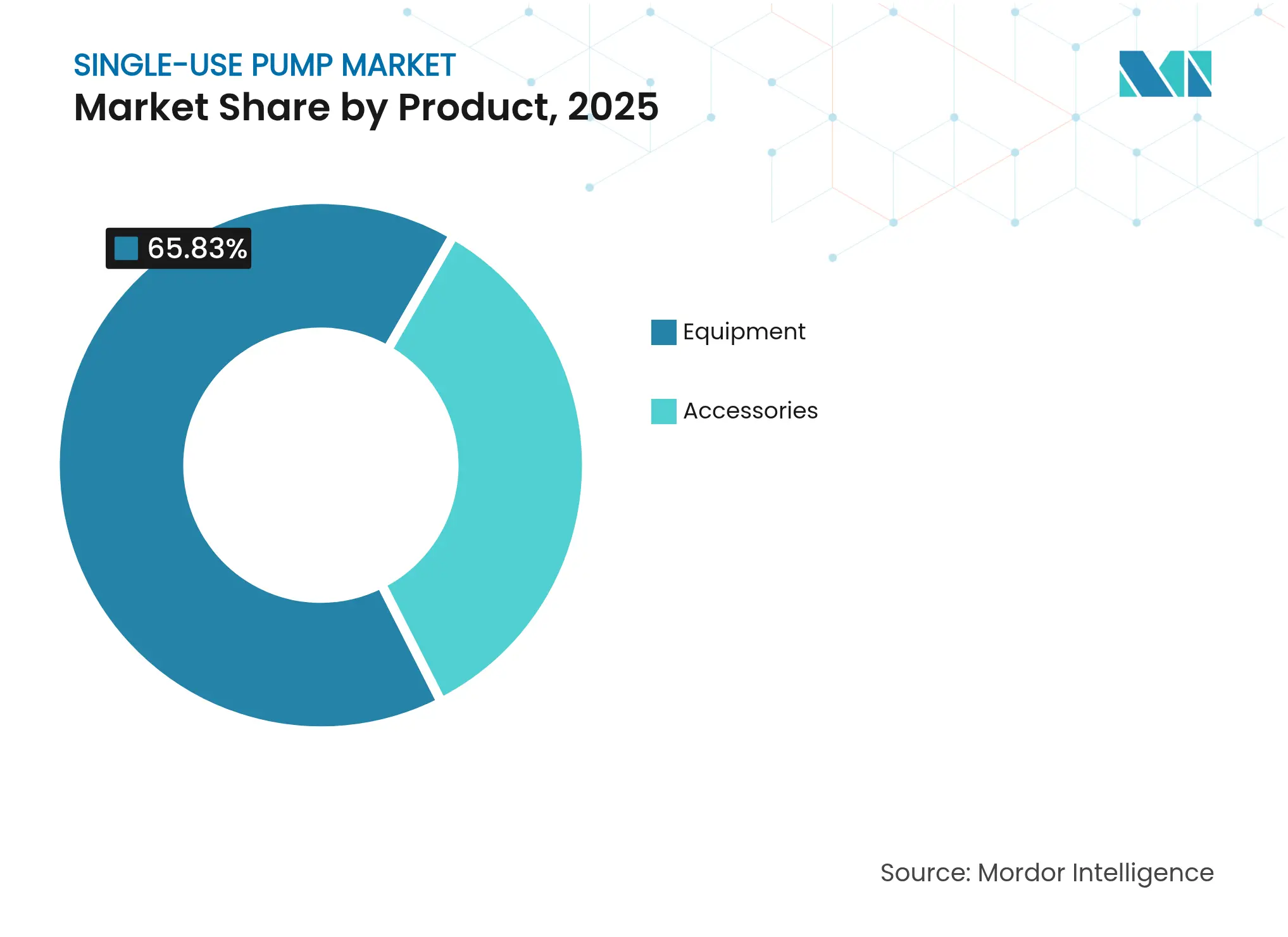

- By product, equipment led with 65.83% of single-use pump market share in 2025, whereas accessories posted the fastest 18.12% CAGR to 2031.

- By flow rate, low-flow pumps captured 53.96% of single-use pump market share in 2025, while high-flow models are expanding at a 15.4% CAGR through 2031.

- By application, upstream processes held 45.15% of the single-use pump market size in 2025; downstream operations are projected to rise at a 15.92% CAGR between 2026-2031.

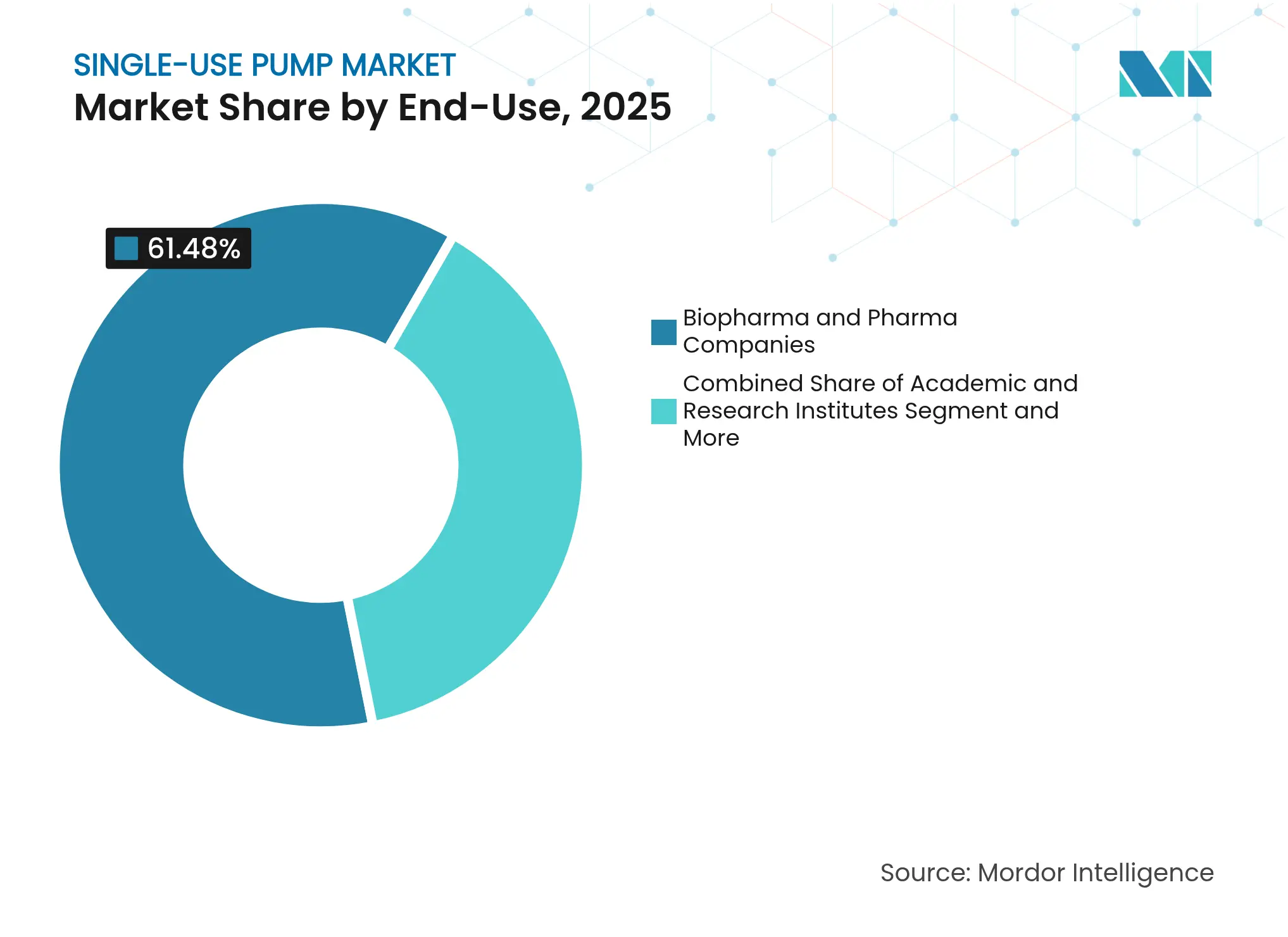

- By end-use, biopharma firms commanded 61.48% share of the single-use pump market size in 2025, yet CROs and CMOs record the highest 16.12% CAGR to 2031.

- By material, medical-grade polyethylene retained 46.77% share in 2025, whereas fluoropolymer liners are on track for an 17.74% CAGR to 2031.

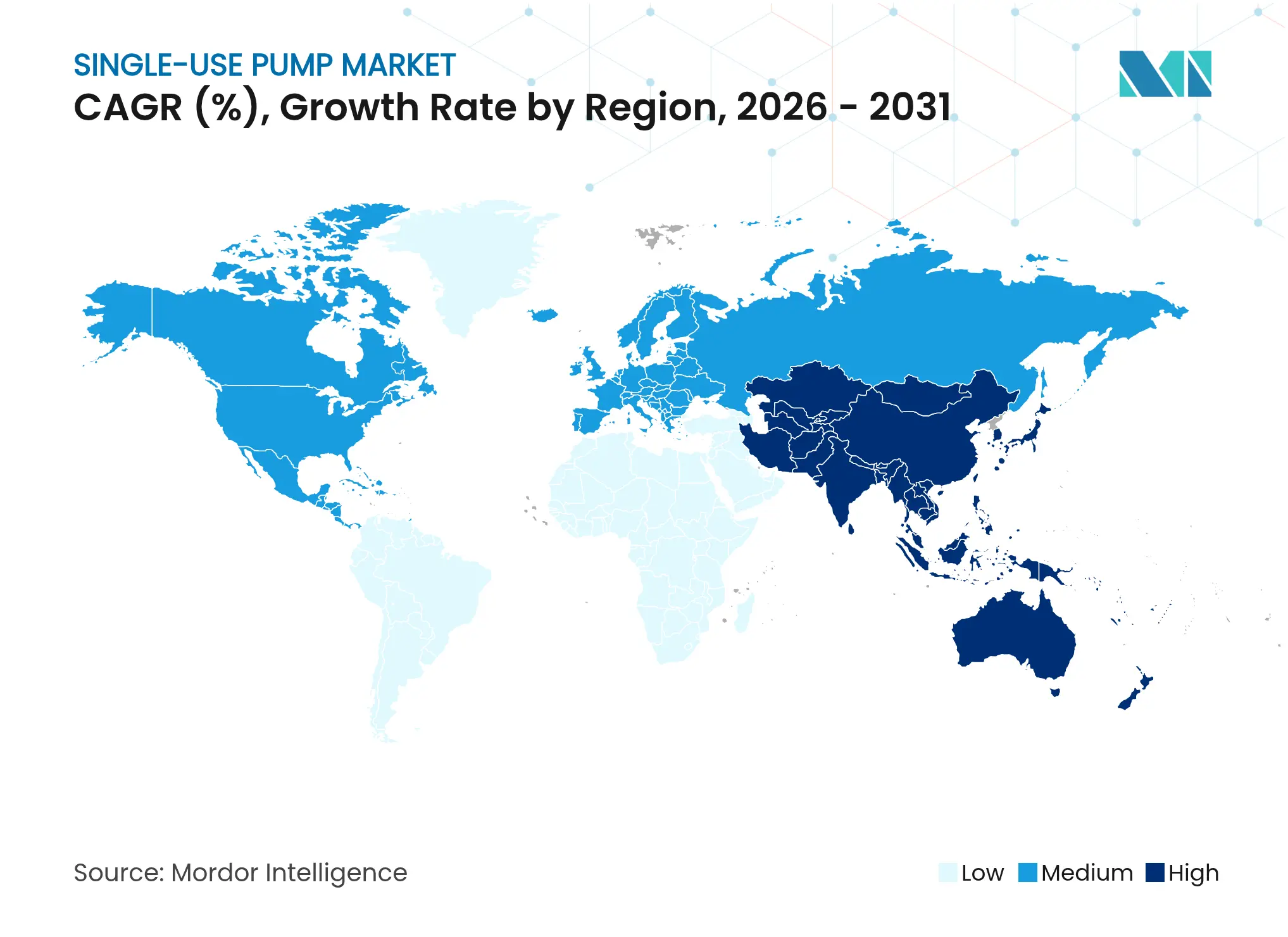

- By geography, North America generated 37.22% of 2025 revenue; Asia-Pacific is forecast to advance at a 15.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single-Use Pump Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Adoption Of Single-Use Bioprocessing In Biologics

Manufacturing

Rising Adoption Of Single-Use Bioprocessing In Biologics

Manufacturing

| +2.5% | Global, with concentration in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.5%

| Geographic Relevance:

Global, with concentration in North America & EU

| Impact Timeline:

Medium term (2-4 years)

|

Technological Advances In Low-Shear Peristaltic &

Diaphragm Designs

Technological Advances In Low-Shear Peristaltic &

Diaphragm Designs

| +1.8% | Global, led by North America & Western Europe | Long term (≥ 4 years) | |||

Growing Chronic-Disease Prevalence Spurring Demand For

Advanced Therapies

Growing Chronic-Disease Prevalence Spurring Demand For

Advanced Therapies

| +2.2% | Global, with highest impact in North America & APAC | Long term (≥ 4 years) | |||

Expansion Of CDMO Capacity For Rapid Scale-Up

Expansion Of CDMO Capacity For Rapid Scale-Up

| +2.8% | Global, with significant growth in APAC & Europe | Medium term (2-4 years) | |||

Decentralised Modular Vaccine Facilities Post-COVID

Decentralised Modular Vaccine Facilities Post-COVID

| +1.5% | Global, with focus on emerging markets | Short term (≤ 2 years) | |||

ESG Mandates Favouring Water- & Energy-Saving Pump

Solutions

ESG Mandates Favouring Water- & Energy-Saving Pump

Solutions

| +1.2% | Primarily EU & North America, expanding to APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Adoption of Single-Use Bioprocessing in Biologics Manufacturing

Global biologics producers are replacing stainless-steel infrastructure with disposable platforms to turn over batches faster and trim capital risk. Fujifilm Diosynth allocated USD 1.6 billion in 2024 for eight 20,000 L single-use bioreactors that double its capacity and remove weeks of cleaning downtime[1]Fujifilm Diosynth Biotechnologies, “Company Announces USD 1.6 Billion Investment,” fujifilmdiosynth.com. Lotte Biologics earmarked USD 1 billion to reach top-ten CDMO status by relying on fully disposable suites that allow multi-product changeovers within hours. Although consumables raise per-batch costs by 25-29%, the saved validation time accelerates new therapy launches, outweighing expense concerns. Samsung Biologics and SK pharmteco jointly invested USD 260 million in Korea to standardize single-use layouts, signalling this model as the mainstream for new greenfield plants.

Technological Advances in Low-Shear Peristaltic & Diaphragm Designs

Pump makers are engineering gentle fluid paths to prevent protein aggregation during circulation. Watson-Marlow’s Quantum pump pairs ReNu SU cartridges with precise servo control to transport sensitive monoclonal antibodies under minimal shear. Magnetic-bearing devices from Levitronix remove mechanical contact altogether, eliminating friction and extending cartridge life. Conveying Wave Technology (CWT) moves fluids through an oscillating chamber, delivering ±1% dosing accuracy while reducing chemical exposure by 97.5%[2]Spirax-Sarco, “Watson-Marlow Fluid Technology Solutions,” spiraxgroup.com. Such innovations underpin reliable scale-up for cell and gene therapies where product loss is costly.

Growing Chronic-Disease Prevalence Spurring Demand for Advanced Therapies

Rising incidence of cancer, autoimmune conditions, and rare genetic disorders intensifies the pipeline of complex biologics, driving upstream and downstream volumes that single-use pump market vendors aim to serve. Precision drugs often require small, high-value batches processed under stringent sterility. Disposable pumping lines minimise cross-contact risk when manufacturers alternate between niche therapies. Health-system pressure to shorten development timelines further tilts decisions toward ready-to-install skids that align with accelerated approval pathways.

Expansion of CDMO Capacity for Rapid Scale-Up

CDMOs race to offer turnkey production to sponsors lacking internal infrastructure. CordenPharma’s EUR 900 million peptide build-out and Terumo’s multiproduct expansion highlight demand for platforms that adapt to shifting molecule portfolios. Global single-use pump market suppliers benefit as contract sites prefer standardised, vendor-qualified cartridges that meet diverging client protocols. BioProcess International estimates 16.5 million litres of global bioprocess capacity in 2025, with China and India adding the largest shares to pursue Western outsourcing contracts. This capacity wave anchors steady pump sales across facility lifecycles.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited Suitability In High-Pressure Downstream Filtration

Limited Suitability In High-Pressure Downstream Filtration

| -1.2% | Global, particularly impacting large-scale operations | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.2%

| Geographic Relevance:

Global, particularly impacting large-scale operations

| Impact Timeline:

Medium term (2-4 years)

|

High Upfront Device Cost Vs. Legacy Pumps

High Upfront Device Cost Vs. Legacy Pumps

| -0.8% | Cost-sensitive markets, primarily emerging economies | Short term (≤ 2 years) | |||

Regulatory Scrutiny On Plastic Waste & PFAS Leachables

Regulatory Scrutiny On Plastic Waste & PFAS Leachables

| -1.5% | EU & North America leading, expanding globally | Long term (≥ 4 years) | |||

Volatile Supply Of Medical-Grade Polymer Resins

Volatile Supply Of Medical-Grade Polymer Resins

| -1.1% | Global, with acute impact in North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Suitability in High-Pressure Downstream Filtration

Ultrafiltration and diafiltration steps for high-concentration monoclonal antibodies run above 3 bar, exceeding safety margins for many disposable casings. The United States FDA emphasises precise pressure control during sterile filtration, adding validation hurdles when polymer integrity is uncertain[3]US FDA, “Essential Drug Delivery Outputs Guidance,” fda.gov. Hybrid facilities often pair single-use lines upstream with stainless-steel skids downstream, diluting the simplicity advantage that motivates disposable adoption. Intensifying demand for high-viscosity formulations suitable for subcutaneous delivery compounds the pressure challenge, as pumps must maintain accuracy despite rising fluid resistance.

Regulatory Scrutiny on Plastic Waste & PFAS Leachables

European PFAS proposals threaten fluoropolymer supply chains that underpin high-performance liners. Saint-Gobain shifted its PharmaFluor FEP tubing to non-fluorinated polymerisation aids, while Sartorius warned that future bans could extend to PVDF filters. The FDA’s 2024 draft rule elevates extractables and leachables testing, mandating full chemical profiles for every disposable component. Compliance raises certification lead-times and cost, encouraging conservative purchasing in green-minded regions. Vendors respond by investing in recyclable materials and closed-loop recovery programs, yet infrastructure remains nascent.

Segment Analysis

By Product: Equipment Dominance Drives Innovation

Equipment generated 65.83% revenue in 2025, reflecting the fundamental role of pumps at every bioprocess stage. Peristaltic units remain the cornerstone for aseptic fluid transfer, while quaternary diaphragm systems gain share in precision dosing for chromatography buffers. The single-use pump market size for equipment is projected to expand steadily as suppliers bundle hardware with sensing and control software. Accessories trail in absolute terms yet deliver the fastest 18.12% CAGR, fueled by batch-to-batch replacement of tubing, connectors, and pump cartridges. Leading vendors roll out integrated fluid-path kits, capturing lifecycle value after the initial skid sale.

Consumable revenue benefits from predictable procurement cycles embedded in current good manufacturing practice documentation. Watson-Marlow’s WMArchitect suite packages quick-fit manifolds and irradiation-ready tubing sets, enabling operators to achieve sub-15-minute changeovers. Niche firms focus on sterile weldable connectors and gamma-stable elastomers that address regulatory push for closed processing. Rising adoption of continuous bioprocessing further supports accessory volumes, as extended campaigns require periodic switch-out of wetted parts to uphold sterility within multiday runs.

Note: Segment shares of all individual segments available upon report purchase

By Flow Rate: Low-Flow Precision Meets High-Flow Scaling

Low-flow pumps dominated with 53.96% revenue in 2025, driven by cell and gene therapy protocols that mandate tight volumetric accuracy below 100 L/min. These systems safeguard fragile cells and reduce reagent waste during small-batch production. High-flow platforms are picking up momentum at a 15.4% CAGR, supported by expanding 5,000 L to 20,000 L single-use bioreactors in commercial monoclonal antibody plants. The single-use pump market size tied to high-flow tasks gains from escalating harvest volumes and perfusion strategies that circulate large media quantities daily.

Design divergence remains pronounced. Low-flow devices accentuate pulsation damping and pressure stability at sub-2 bar operation, whereas high-flow skids optimise motor torque and tubing wall strength to run continuous 24/7 campaigns. Modular stator assemblies enable manufacturers to calibrate identical drive units for distinct flow envelopes, lowering inventory costs. The rise of perfusion and continuous capture blurs historic cut-offs, prompting R&D toward pumps with variable-speed algorithms that auto-adjust to online biomass readings.

By Application: Downstream Processing Accelerates

Upstream steps retained 45.15% revenue in 2025 due to entrenched disposable bioreactor adoption and routine media transfers. Yet downstream operations post the leading 15.92% CAGR as producers tackle purification bottlenecks for high-titre biologics. Single-use chromatography skids, virus-filtration lines, and bulk-drug-substance fill systems embed pumps to drive constant flow through membranes and columns. The segment also benefits from process analytical technology frameworks pushing for closed, automated post-harvest phases.

Downstream growth hinges on cost-reduction imperatives: purification can represent more than half of total manufacturing expense for some recombinant proteins. Thermo Fisher’s purchase of Solventum’s filtration unit underscores strategic value in integrated single-use downstream suites. Pump vendors respond by incorporating low-hold-up volume manifolds and in-line pressure sensors that maintain uniform trans-membrane gradients, meeting regulatory expectations for consistent critical quality attributes.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End-Use: CDMO Growth Reshapes Demand

Biopharmaceutical innovators and large pharma entities produced 61.48% of 2025 demand, prioritising validated, audit-ready hardware. However, single-use pump market demand from CROs and CMOs is growing at 16.12% CAGR, stemming from sponsor outsourcing and capacity constraints at originator firms. Contract operators standardise on versatile pump brands to flex across multiple client molecules without lengthy qualification loops.

Antylia Scientific’s evolution from Cole-Parmer reflects supplier pivot toward the CDMO customer base, emphasising rapid-delivery service and global cartridge availability. Academic sites remain smaller buyers yet act as proving grounds for cutting-edge formats such as disposable micro-pumps integrated into benchtop perfusion platforms. Increasing adoption of personalised medicine drives interest in single-use metering pumps capable of handling sub-litre batch volumes with pharmaceutical-grade accuracy.

Note: Segment shares of all individual segments available upon report purchase

By Material of Construction: Fluoropolymers Address Compatibility Challenges

Medical-grade polyethylene held 46.77% revenue in 2025 thanks to broad solvent tolerance and easy extrusion into tubing. Polypropylene satisfies elevated temperature cycles, while silicone elastomers secure peristaltic compression performance. Fluoropolymer liners, headed for an 17.74% CAGR, gain from unparalleled inertness that safeguards viral vector integrity and minimises extractables. Transition toward high-pH viral inactivation buffers and solvent-rich purification workflows bolsters demand for expanded polytetrafluoroethylene and perfluoroalkoxy resin coatings.

Regulatory scrutiny accelerates innovation in low-PFAS alternatives. Gore’s STA-PURE containers and Syensqo’s capacity expansion illustrate commitment to advanced barrier films compliant with tightening European thresholds. Simultaneously, resin shortages and logistic bottlenecks prompt dual-sourcing strategies, with OEMs qualifying redundant polymer grades to guarantee uninterrupted supply.

Geography Analysis

North America captured 37.22% of 2025 revenue on the strength of mature biomanufacturing clusters, well-defined regulatory guidance, and solid venture funding for advanced therapy pipelines. The FDA’s Quality Management System Regulation (QMSR) alignment with ISO 13485, effective 2026, streamlines cross-border device approvals and could accelerate new pump launches. Dover Corporation reported 7% organic growth in its pump division in Q1 2025, attributed largely to biopharma component shipments, highlighting resilient replacement demand. Research spending within the National Institutes of Health and Biomedical Advanced Research and Development Authority also supports pilot-scale installations across academic hubs.

Asia-Pacific is the fastest climber, advancing at a 15.08% CAGR toward 2031 as governments invest billions to achieve vaccine self-reliance and capture biologics outsourcing. Singapore’s state-backed mRNA vaccine push and South Korea’s USD 1.92 billion budget to become a top vaccine hub exemplify public-private collaboration. China and India expand Current Good Manufacturing Practice (CGMP) compliant capacity to serve multinational sponsors seeking cost-efficient production. Cytiva executives cite rapid growth in cell and gene therapy facilities enabled by fast-track regulatory channels in Australia, Japan, and Korea.

Europe commands a substantial share backed by stringent quality norms and deep biologics pipelines. Implementation of revised Good Manufacturing Practice Annex 1 in 2025 elevates sterility expectations, promoting wider uptake of disposable pumps that remove cleaning dead-legs. The European Shortages Monitoring Platform, mandatory from February 2025, incentivises flexible capacity capable of quick product switches, a core benefit of single-use. Regional suppliers however face input-cost volatility as resin pricing swings and PFAS legislation tightens, raising production-planning complexity.

Competitive Landscape

Market Concentration

The single-use pump market displays moderate fragmentation yet high technical barriers. Watson-Marlow Fluid Technology Solutions, PSG Dover, and Xylem spearhead innovation, leveraging decades of fluid-path expertise. Watson-Marlow’s broadened identity underscores diversification beyond traditional peristaltic lines into complete fluid-management ecosystems. Strategic acquisitions intensify competition: PSG Dover absorbed Cryogenic Machinery Corp in 2025 to access specialty cold-chain pumps applicable to advanced therapies. Nordson obtained Atrion in 2024, adding infusion and cardiovascular technologies that share polymer science and compliance competencies with single-use bioprocess pumps.

Partnerships between pump makers and sensor firms create integrated skids that fulfil process analytical technology mandates, raising switching costs for buyers. Firms that embed digital twinning and real-time calibration functions position themselves favourably for continuous manufacturing adoption. Niche suppliers carve out share in microbatch or ultralow-shear segments, though scale limitations and validation resources restrict market reach. Entry newcomers must navigate complex biocompatibility testing and secure gamma-compatible materials, barriers that sustain incumbents’ pricing power.

Single-Use Pump Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Nordson completed its Atrion acquisition, enlarging its medical device fluid-delivery offerings.

- April 2024: Xylem introduced the Jabsco PureFlo 21 single-use pump aimed at biopharma downstream operations.

Table of Contents for Single-Use Pump Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Adoption Of Single-Use Bioprocessing In Biologics Manufacturing

- 4.2.2Technological Advances In Low-Shear Peristaltic & Diaphragm Designs

- 4.2.3Growing Chronic-Disease Prevalence Spurring Demand For Advanced Therapies

- 4.2.4Expansion Of CDMO Capacity For Rapid Scale-Up

- 4.2.5Decentralised Modular Vaccine Facilities Post-COVID

- 4.2.6ESG Mandates Favouring Water- & Energy-Saving Pump Solutions

- 4.3Market Restraints

- 4.3.1Limited Suitability In High-Pressure Downstream Filtration

- 4.3.2High Upfront Device Cost Vs. Legacy Pumps

- 4.3.3Regulatory Scrutiny On Plastic Waste & PFAS Leachables

- 4.3.4Volatile Supply Of Medical-Grade Polymer Resins

- 4.4Technological Outlook

- 4.5Porter's Five Forces

- 4.5.1Bargaining Power of Suppliers

- 4.5.2Bargaining Power of Buyers

- 4.5.3Threat of New Entrants

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Equipment

- 5.1.1.1Peristaltic Pumps

- 5.1.1.2Quaternary Diaphragm Pumps

- 5.1.1.3Centrifugal Pumps

- 5.1.1.4Other Equipment

- 5.1.2Accessories

- 5.1.2.1Tubing & Connectors

- 5.1.2.2Pump Chambers & Cartridges

- 5.1.2.3Sensors & Controllers

- 5.2By Flow Rate

- 5.2.1High-Flow (>100 L/min)

- 5.2.2Low-Flow (<100 L/min)

- 5.3By Application

- 5.3.1Upstream Bioprocessing

- 5.3.2Downstream Bioprocessing

- 5.3.3Laboratory / Small-Scale Processing

- 5.4By End-Use

- 5.4.1Biopharma & Pharma Companies

- 5.4.2CROs & CMOs

- 5.4.3Academic & Research Institutes

- 5.4.4Other End Users

- 5.5By Material of Construction

- 5.5.1Medical-Grade Polyethylene

- 5.5.2Polypropylene

- 5.5.3Silicone Elastomers

- 5.5.4Fluoropolymer Liners

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1ESI Ultrapure

- 6.3.2Fluid Flow Products Inc.

- 6.3.3High Purity New England

- 6.3.4Interscience

- 6.3.5Levitronix

- 6.3.6PSG (Dover)

- 6.3.7PumpCell

- 6.3.8SMC Corporation

- 6.3.9Watson-Marlow Fluid Technology Solutions

- 6.3.10Xylem

- 6.3.11Nordson Corporation

- 6.3.12Cole-Parmer

- 6.3.13Verder Group

- 6.3.14Graco Inc.

- 6.3.15IDEX Corporation

- 6.3.16Quattroflow

- 6.3.17Entegris

- 6.3.18Valmet Flow Control

- 6.3.19Masterflex (Avantor)

- 6.3.20Biopure Technology

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Single-Use Pump Market Report Scope

As per the scope of the report, single-use pumps are specialized pumping systems designed for one-time use, primarily in biopharmaceutical manufacturing processes. They ensure contamination-free product handling and compliance with strict regulatory standards, enhancing operational efficiency and safety.

The single-use pump market is segmented by product, flow rate, end-use, and geography. By product, the market is segmented as equipment and accessories. By flow rate, the market is segmented as high flow and low flow. By end-use, the market is segmented as biopharmaceutical & pharmaceutical companies, CROs & CMOs, and others. The report also covers the market sizes and forecasts for the single-use pumps market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).