Laboratory Vacuum Pumps Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

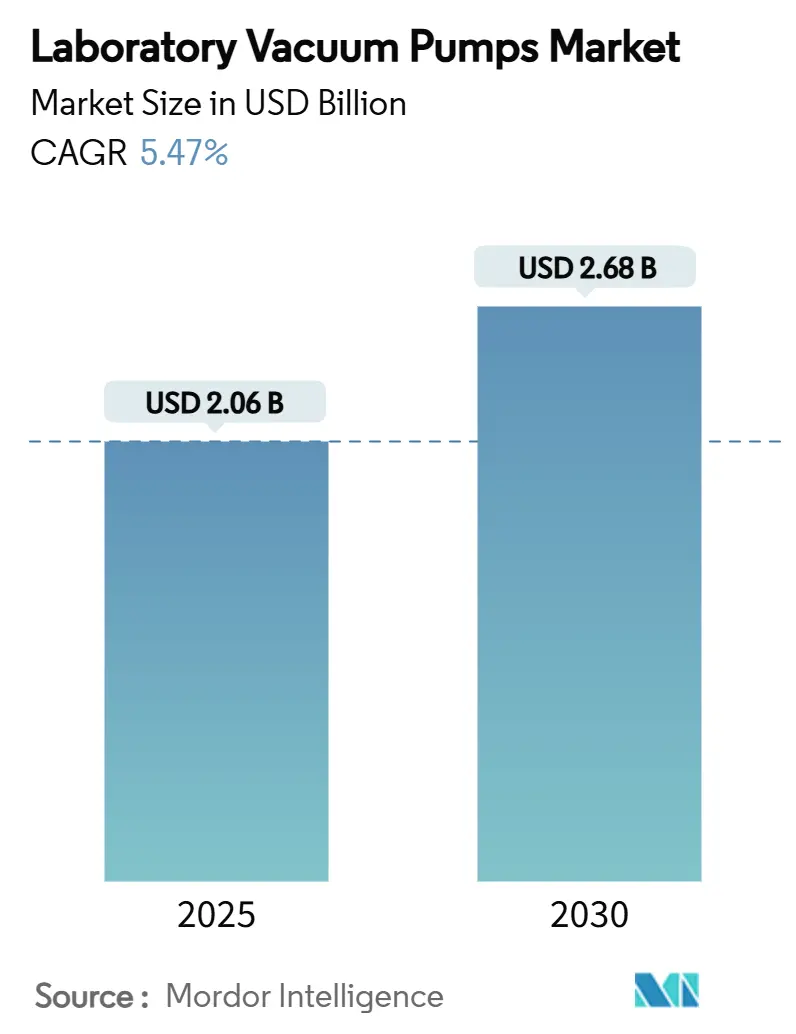

| Market Size (2025) | USD 2.06 Billion |

| Market Size (2030) | USD 2.68 Billion |

| Growth Rate (2025 - 2030) | 5.47% CAGR |

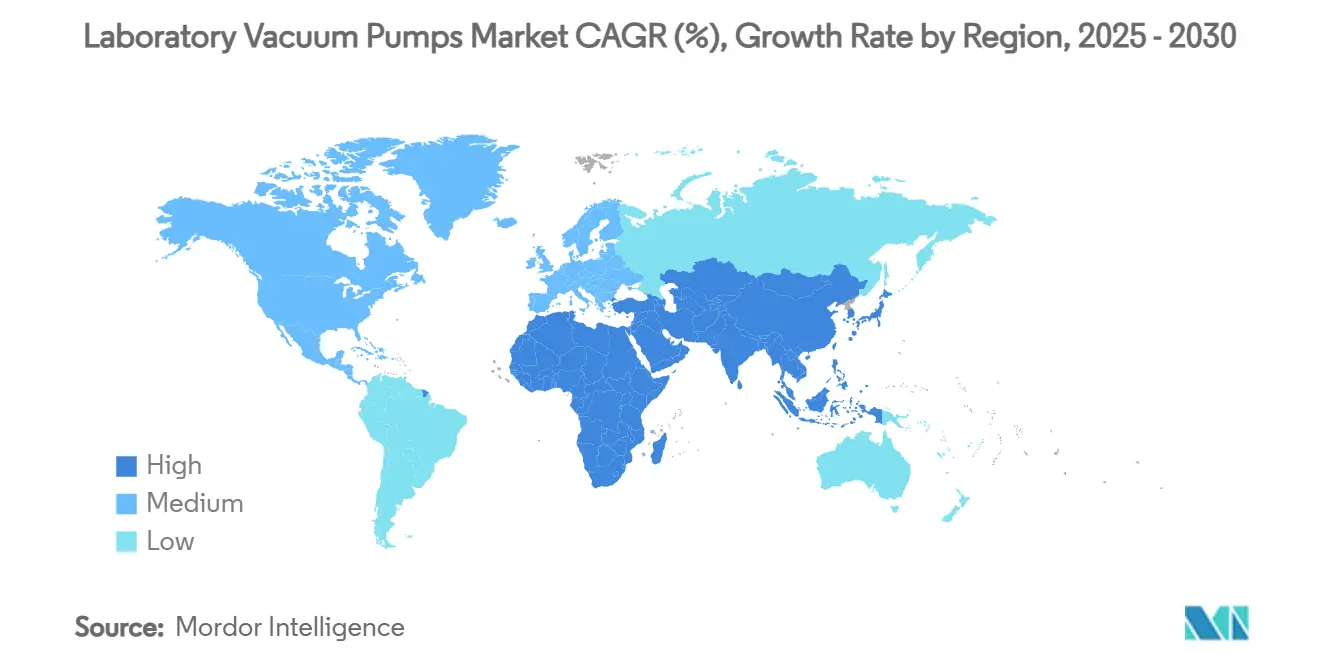

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

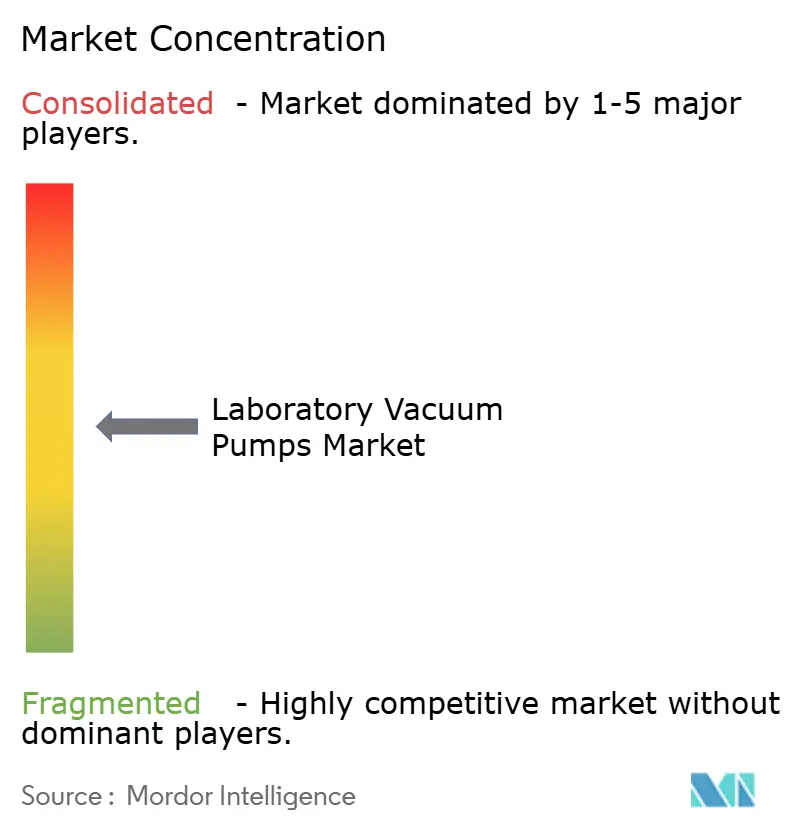

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Vacuum Pumps Market Analysis by Mordor Intelligence

The laboratory vacuum pumps market size reached USD 2.06 billion in 2025 and is forecast to expand to USD 2.68 billion by 2030 at a 5.47% CAGR. Robust pharmaceutical R&D funding, tighter aseptic-processing rules, and the push for contamination-free laboratory environments collectively anchor demand, while oil-free technologies underpin the shift away from legacy oil-sealed systems. Regulatory scrutiny of cleanroom pressure differentials accelerates equipment upgrades in North America, whereas Asia-Pacific growth stems from the realignment of contract manufacturing to Indian providers after the US Biosecure Act. Consolidation—exemplified by Atlas Copco’s purchase of Oerlikon’s vacuum unit—signals the importance of scale, diversified product portfolios, and regional service networks. Energy-efficient designs also gain traction as laboratories pursue cost savings and green-lab certifications.

Key Report Takeaways

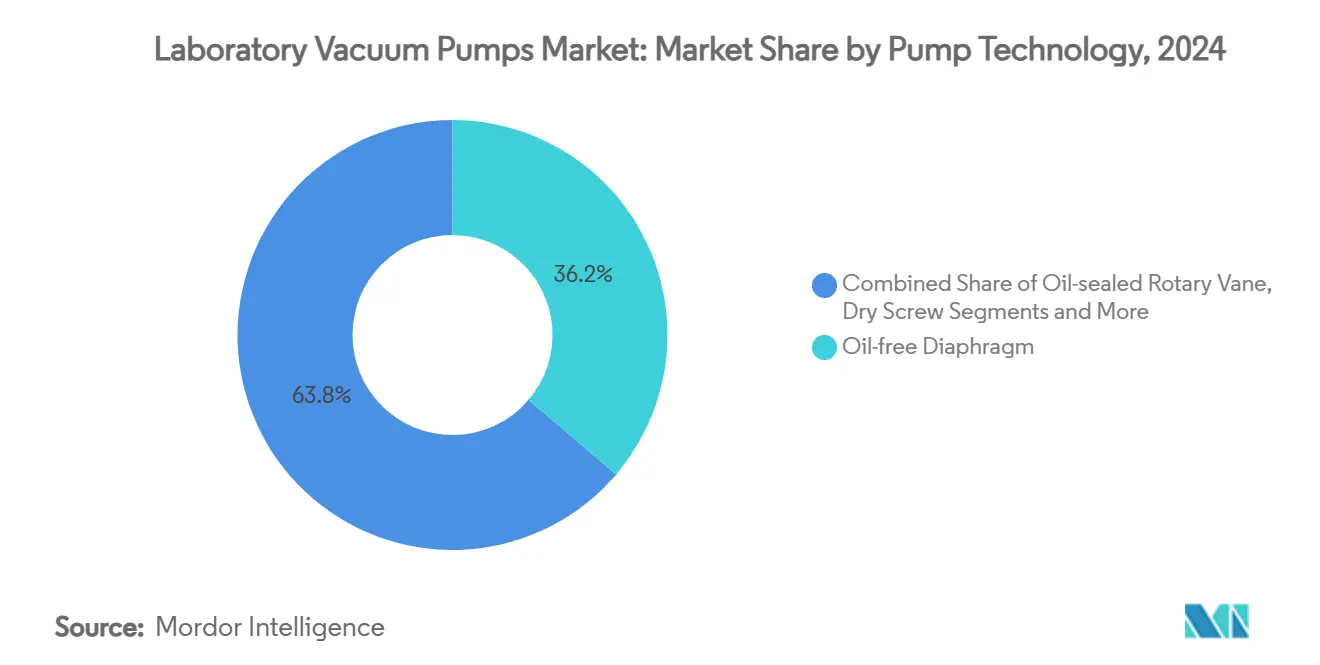

- By pump technology, oil-free diaphragm pumps led with 36.23% revenue share in 2024; dry scroll pumps are projected to expand at a 22.34% CAGR through 2030.

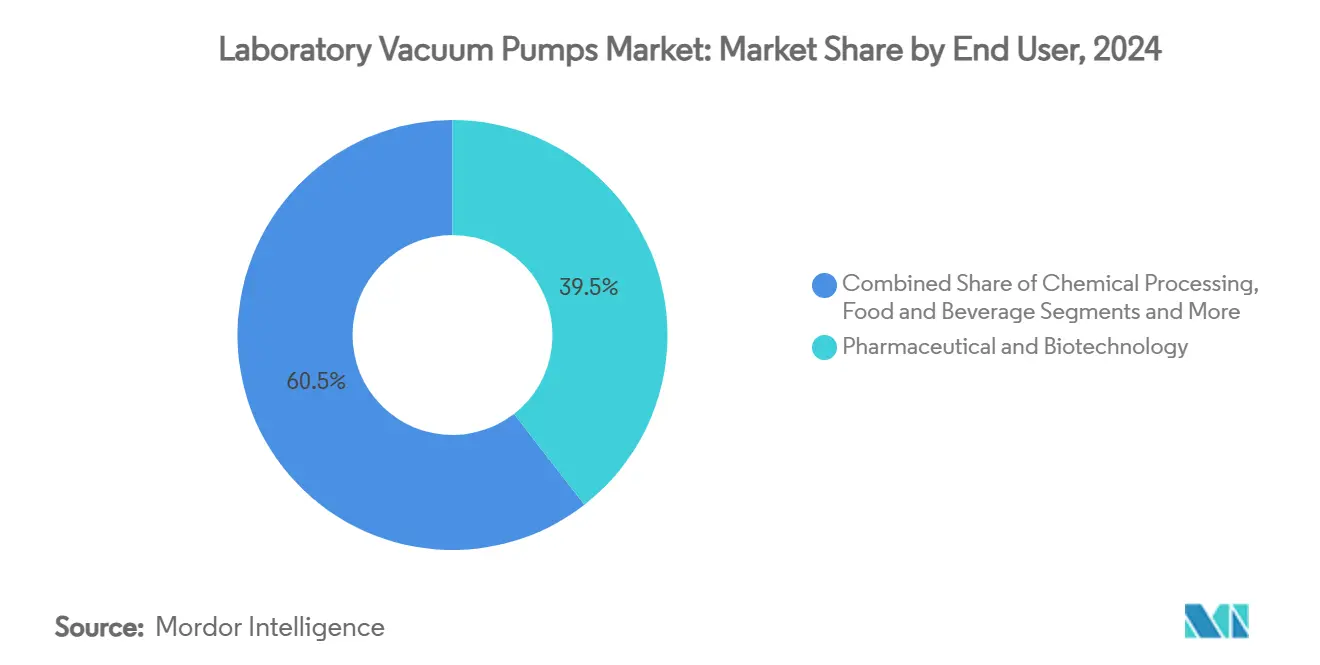

- By end-user, pharmaceutical and biotechnology laboratories held 39.47% of laboratory vacuum pumps market share in 2024, while clinical and diagnostic laboratories are expected to record the fastest 12.78% CAGR to 2030.

- By application, filtration and solvent removal accounted for 26.43% of the laboratory vacuum pumps market size in 2024; mass spectrometry and GC-MS applications are positioned to grow at a 20.53% CAGR to 2030.

- By geography, North America commanded 31.22% of the laboratory vacuum pumps market size in 2024, whereas Asia-Pacific is forecast to log a 20.43% CAGR through 2030.

Global Laboratory Vacuum Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in biopharma R&D expenditure | +1.2% | North America & EU centric but global influence | Medium term (2-4 years) |

| Rapid adoption of oil-free pump technologies | +0.8% | Global, led by pharmaceutical hubs | Short term (≤ 2 years) |

| Laboratory automation & remote compatibility | +0.9% | APAC core with spill-over to North America | Medium term (2-4 years) |

| Energy-efficiency incentives | +1.1% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Demand from analytical instruments | +0.7% | Clinical diagnostics worldwide | Short term (≤ 2 years) |

| Expansion of CRO/CDMO capacity | +0.6% | APAC, particularly India & Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Biopharma R&D Expenditure

Escalating budgets for biologics and personalized therapies push laboratories to adopt pumps that reach the fine-vacuum range of 1 to 10^-3 mbar without sacrificing pumping speed. These capabilities minimize freeze-dryer cycle times and safeguard high-value biologics from degradation. Tighter aseptic-processing rules elevate vacuum pumps from auxiliary tools to critical infrastructure, ensuring cleanroom pressure stability. Pharmaceutical sponsors increasingly specify oil-free units to avoid cross contamination and simplify validation paperwork. As a result, premium pricing for contamination-free solutions supports margin expansion among technology leaders, sustaining growth momentum across the laboratory vacuum pumps market.

Rapid Adoption of Oil-Free (Dry) Pump Technologies

Dry screw and dry scroll pumps deliver ultimate pressures below 0.01 torr while eliminating effluent disposal, aligning with modern contamination-prevention protocols. Variable-pitch rotor designs improve compression efficiency and thermal stability, allowing operators to handle aggressive solvents without seal damage. Although capital costs run 40–60% higher than oil-sealed units, laboratories report lower lifetime expenses due to reduced maintenance and zero oil disposal. Environmental compliance is simplified, particularly for volatile organic compound workflows. These combined factors accelerate oil-free pump penetration, reshaping technology preferences inside the laboratory vacuum pumps market.

Laboratory Automation & Remote-Operation Compatibility

Robotic sample prep platforms and autonomous workflows depend on vacuum pumps equipped with digital interfaces, on-board diagnostics, and IoT connectivity.[1]Samantha Y. Chong et al., “Modular, Multi-Robot Integration of Laboratories,” Chemical Science, rsc.org Remote monitoring allows engineers to track ultimate pressure, vibration, and temperature in real time, triggering predictive maintenance alerts before unplanned downtime. As hybrid working models take hold, operators require systems that continue to run with minimal on-site supervision. Pump suppliers now bundle Ethernet and OPC-UA protocols as standard, making vacuum systems integral nodes in connected lab architectures. This evolution elevates equipment reliability and documentation quality, further boosting demand within the laboratory vacuum pumps market.

Energy-Efficiency Incentives from Green-Lab Programmes

New US Department of Energy test procedures for compressors incentivize laboratories to replace legacy oil-sealed pumps with energy-efficient dry technologies.[2]U.S. Department of Energy, “Energy Conservation Program: Test Procedure for Compressors,” federalregister.govGreen-lab certification programmes reimburse a portion of capital spending when installations demonstrate kWh reductions against baseline equipment. Busch’s COBRA NC series, for instance, records up to 55% electricity savings during battery-cell production runs. Lower operating costs boost return on investment, turning sustainability mandates into practical budget decisions. Energy-efficiency therefore adds long-term momentum to the laboratory vacuum pumps market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost & TCO for advanced pumps | −0.9% | Global, most acute for small labs | Short term (≤ 2 years) |

| Stringent purity / contamination-free rules | −0.4% | North America & EU pharma hubs | Medium term (2-4 years) |

| On-chip micro-vacuum alternatives | −0.3% | Tech centers in North America & APAC | Long term (≥ 4 years) |

| Supply-chain scarcity of high-performance elastomers | −0.2% | Global, specialised applications hardest hit | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & Total Cost of Ownership

Oil-free scroll and screw pumps often command 40–60% price premiums versus oil-sealed rotary vane models, stretching the budgets of academic and midsized contract labs. Specialized maintenance requirements, including precision bearing replacement, add to lifecycle expense. Budget-constrained facilities therefore postpone upgrades, extending the operating life of depreciated assets that fall short of new performance norms. Financing challenges are greater when laboratories must also modernize fume hoods, biosafety cabinets, and analytical instruments concurrently. Persistently high entry costs curb near-term adoption rates inside sections of the laboratory vacuum pumps market.

Stringent Purity / Contamination-Free Requirements

FDA guidance on aseptic processing compels facilities to validate every pressure boundary and airborne particle count, placing vacuum pumps under strict qualification.[3]U.S. Food and Drug Administration, “21 CFR 211.42 — Design and Construction Features,” ecfr.gov Pumps must function in ISO 5 environments without shedding particulates or oils, which constrains equipment options and increases documentation workloads. Smaller suppliers lacking deep regulatory experience struggle to certify products, limiting competitive pricing. Extended validation protocols can delay facility start-ups by months, elevating opportunity costs. These factors collectively temper uptake in the laboratory vacuum pumps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Technology: Oil-Free Systems Drive Innovation

Oil-free diaphragm pumps accounted for 36.23% of the laboratory vacuum pumps market size in 2024, underscoring their entrenched role in contamination-sensitive tasks. Their PTFE diaphragms yield chemical resistance and low maintenance, keeping total cost of ownership predictable for clinical and biotech users. Dry scroll pumps, projected to advance at a 22.34% CAGR, leverage spiral geometries to compress gases smoothly, reducing vibration and enabling placement adjacent to analytical instruments. Oil-sealed rotary vane pumps retain relevance in cost-conscious academic labs, primarily handling filtration where stringent cleanliness is unnecessary. Dry screw designs gain popularity in high-throughput pharmaceutical freeze-dryers by achieving ultimate pressures below 0.01 torr while venting solvent vapors without generating waste oils. Liquid ring pumps remain the choice for condensable-vapor duties, though water-usage concerns spur hybrid variants that recycle sealing liquid. Cryogenic and turbomolecular pumps dominate ultra-high-vacuum physics research, a specialist niche that offers limited volume but stable margins. Across technologies, IoT-enabled controllers collect vibration, temperature, and pressure data to predict failures, reflecting an industry-wide transition toward smart maintenance regimes.

Hybrid pump packages now combine scroll and turbo stages to broaden dynamic pressure ranges in compact footprints. Pfeiffer Vacuum’s 2024 release of an enhanced rotary vane line demonstrates how legacy formats evolve through new alloys and energy-saving drives. Atlas Copco’s portfolio integration of Oerlikon’s technologies adds cryo and turbo options, allowing cross-selling into semiconductor fabs that demand oil-free exhaust for plasma etch tools. Integration depth benefits customers who prefer single-vendor kits covering roughing through high vacuum stages with harmonized service schedules. Consequently, technology convergence and product bundling enhance vendor lock-in, reinforcing the competitive positioning of top suppliers within the laboratory vacuum pumps market.

By End-User Industry: Pharmaceutical Dominance Amid Clinical Growth

Pharmaceutical and biotechnology facilities captured 39.47% of laboratory vacuum pumps market share in 2024 due to their rigorous contamination controls and high equipment density. Lyophilization of monoclonal antibodies and gene-therapy vectors requires faultless vacuum performance over long cycles, pushing demand for robust dry screw pumps. Compliance audits encourage redundant pump arrays to guarantee uptime, effectively doubling installed bases at new plants. Conversely, clinical and diagnostic laboratories represent the fastest-growing cohort with a 12.78% CAGR, as polymerase-chain-reaction and mass-spectrometry testing continue migrating into regional hospitals. These labs favor compact scroll and diaphragm units that fit under benchtops, emphasizing quiet operation and simple maintenance.

Chemical processing end-users adopt corrosion-resistant liquid ring or PTFE-lined diaphragm pumps for solvent recovery, valuing durability over ultimate vacuum depth. Food & beverage manufacturers integrate sanitary-design pumps for aroma extraction and packaging, where 3-A sanitary standards dictate easy cleanability. Academic and government institutions, constrained by grant cycles, prolong service lives through refurbishment contracts, creating niche revenue for third-party service firms. CDMO expansion in India and Southeast Asia spurs bulk orders for skid-mounted vacuum packages, often bundled with freeze-dryers and isolators under EPC contracts. Collectively, the diversifying customer mix incentivizes OEMs to offer modular platforms configurable to multiple workflows, strengthening resilience across the laboratory vacuum pumps market.

By Application: Analytical Instruments Accelerate Demand

Filtration and solvent removal held 26.43% of the laboratory vacuum pumps market size in 2024, reflecting the ubiquity of rotary evaporators and membrane filters in daily lab routines. Oil-free diaphragm pumps dominate these tasks by delivering moderate vacuums without backstreaming oils onto glassware. Mass spectrometry and GC-MS segments, poised for a 20.53% CAGR, require stable high-vacuum conditions and minimal vibration. Turbomolecular backing pumps paired with dry scroll roughing units ensure fast pump-down and consistent base pressure for ion optics. Freeze-drying lines employ multistage dry screw or hybrid pumps to sustain deep vacuums for days, demanding high reliability and solvent tolerance. Rotary evaporation workflows receive efficiency gains from variable-speed drive pumps that match pressure to solvent characteristics, shrinking cycle times.

Vacuum concentration systems increasingly integrate with robotic sample handlers, automatically adjusting pressure ramps to prevent foaming and cross contamination. New chromatographic instruments ship with embedded diagnostics that recommend pump maintenance intervals based on accumulated load data, minimizing downtime. Battery-manufacturing R&D labs employ dry pumps inside glove-boxes to protect lithium-metal anodes, opening adjacent high-growth niches. Overall, application diversification balances cyclical pharmaceutical demand, underpinning steady performance across the laboratory vacuum pumps market.

Geography Analysis

North America retained leadership with 31.22% of the 2024 laboratory vacuum pumps market size, sustained by FDA-driven GMP compliance and a dense cluster of biotech firms around Boston, San Diego, and Toronto. Upgrade cycles accelerated as companies prepared for Annex 1 harmonization, spurring orders for oil-free and energy-efficient models. Government grants under the US CHIPS Act also supported semiconductor tool investments that require high-vacuum pumping, adding cross-sector demand. Service networks are mature, enabling rapid turnaround for preventive maintenance and unplanned repairs, which further cements vendor stickiness in the region.

Europe contributes a balanced mix of pharmaceutical, academic, and battery-technology demand. Germany and the United Kingdom maintain life-sciences clusters that emphasize GMP upgrade projects, while Nordic countries prioritize green-lab certifications, elevating sales of energy-efficient dry screw pumps. Eastern Europe benefits from Pfeiffer Vacuum’s Romanian expansion, which cuts lead times and positions the company to serve regional OEMs. Regulatory convergence across the EU simplifies product approvals for multinational vendors, yet local after-sales partnerships remain essential for language and compliance nuances.

Asia-Pacific, forecast to post a 20.43% CAGR, is the primary growth engine for the laboratory vacuum pumps market. India’s CDMO boom attracts large-scale cleanroom projects, each requiring multiple pump technologies—roughing, backing, and booster—to cover production through analytical testing. China’s semiconductor investments demand ultra-clean dry pump lines for etch and deposition tools, notwithstanding ongoing supply-chain decoupling. South-East Asian countries, led by Singapore and Vietnam, capitalize on 4.5% GDP growth to expand diagnostics manufacturing, while local governments offer tax holidays for equipment imports. These dynamics collectively erode North America’s share, although Western vendors often supply the high-end systems imported into Asia.

South America remains value-conscious, with Brazil modernizing vaccine plants following lessons from the pandemic, thereby adopting energy-efficient scroll pumps. The Middle East and Africa continue to develop pharmaceutical hubs in Saudi Arabia and the UAE, where economic diversification strategies prioritize drug manufacturing and clinical trial logistics. Limited local technical expertise makes turnkey solutions with remote monitoring attractive. Across all regions, service-network depth and financing solutions determine vendor selection, reinforcing a tiered competitive landscape inside the laboratory vacuum pumps market.

Competitive Landscape

Industry consolidation intensified after Atlas Copco agreed to acquire Oerlikon’s vacuum business in March 2024, adding cryo and turbo capabilities to its portfolio. The pending purchase of Korea’s Kyungwon Machinery in 2025 will extend Atlas Copco’s reach into oil-free screw technology and boost its Asian footprint. Busch Group’s recognition as world market leader underscores the benefits of broad product coverage and synchronized service networks. Pfeiffer Vacuum’s brand repositioning toward “Fab Solutions” reflects the strategic pivot to integrated offerings rather than standalone components, directly targeting semiconductor fabs.

Competition also hinges on technological differentiation. Dry screw pumps with patented rotor profiles deliver higher solvent-handling capacity, while scroll pumps with self-lubricating tips enable longer maintenance intervals. Vendors race to embed edge-computing modules that run predictive algorithms, lowering unscheduled downtime. DOE energy standards incentivize continuous R&D into variable-speed drives and regenerative-braking features that cut power draw during idle periods. These innovations amplify switching costs, placing smaller manufacturers at a disadvantage unless they forge OEM partnerships.

Regional service presence remains decisive. DXP Enterprises’ 2024 acquisition of MaxVac broadens field-service reach on the US West Coast, catering to semiconductor and biotech clients that demand 24/7 support. Meanwhile, European OEMs localize assembly in Southeast Asia to avoid import duties and shorten delivery cycles. Strategic collaboration with integrators—supplying complete freeze-dryer skids or mass spectrometer packages—provides OEMs with deeper customer intimacy, locking in parts and service revenue across the lifecycle. Together, these forces shape a moderately consolidated laboratory vacuum pumps market where the top five companies control an estimated 55–60% of global revenues.

Laboratory Vacuum Pumps Industry Leaders

Busch Vacuum Solutions

Atlas Copco

KNF Neuberger

VACUUBRAND

Agilent Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Atlas Copco Group announced plans to acquire Kyungwon Machinery Industry Co., Ltd., enhancing its oil-injected and oil-free screw compressor and vacuum portfolio pending Q3 2025 closure.

- December 2024: Busch Group inaugurated an expanded production site for Pfeiffer Vacuum in Cluj County, Romania, equipped with photovoltaics for sustainable power.

- November 2024: DXP Enterprises Inc. acquired MaxVac Inc., strengthening its vacuum pump service capabilities for electronics, semiconductor, and biomedical customers.

Global Laboratory Vacuum Pumps Market Report Scope

| Oil-free Diaphragm |

| Oil-sealed Rotary Vane |

| Dry Scroll |

| Dry Screw |

| Liquid Ring |

| Others (Cryogenic, Turbomolecular, etc.) |

| Pharmaceutical & Biotechnology |

| Chemical Processing |

| Food & Beverage |

| Academic & Government Research |

| Clinical & Diagnostic Laboratories |

| Others |

| Filtration & Solvent Removal |

| Rotary Evaporation |

| Freeze-Drying / Lyophilisation |

| Mass Spectrometry & GC-MS |

| Vacuum Concentration |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pump Technology | Oil-free Diaphragm | |

| Oil-sealed Rotary Vane | ||

| Dry Scroll | ||

| Dry Screw | ||

| Liquid Ring | ||

| Others (Cryogenic, Turbomolecular, etc.) | ||

| By End-user Industry | Pharmaceutical & Biotechnology | |

| Chemical Processing | ||

| Food & Beverage | ||

| Academic & Government Research | ||

| Clinical & Diagnostic Laboratories | ||

| Others | ||

| By Application | Filtration & Solvent Removal | |

| Rotary Evaporation | ||

| Freeze-Drying / Lyophilisation | ||

| Mass Spectrometry & GC-MS | ||

| Vacuum Concentration | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current laboratory vacuum pumps market size?

The laboratory vacuum pumps market size stood at USD 2.06 billion in 2025.

What compound annual growth rate is projected for the market?

The market is forecast to expand at a 5.47% CAGR between 2025 and 2030.

Which pump technology is expected to grow the fastest?

Dry scroll pumps are projected to record a 22.34% CAGR through 2030, the highest among all technologies.

Which region will deliver the strongest growth?

Asia-Pacific is expected to post the fastest expansion, with a 20.43% CAGR driven by rising CDMO investments and semiconductor demand.

Asia-Pacific is expected to post the fastest expansion, with a 20.43% CAGR driven by rising CDMO investments and semiconductor demand.

Oil-free systems cut contamination risk, lower lifetime operating costs, and align with energy-efficiency incentives, making them preferable to oil-sealed alternatives.

Page last updated on: