Smart Implantable Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

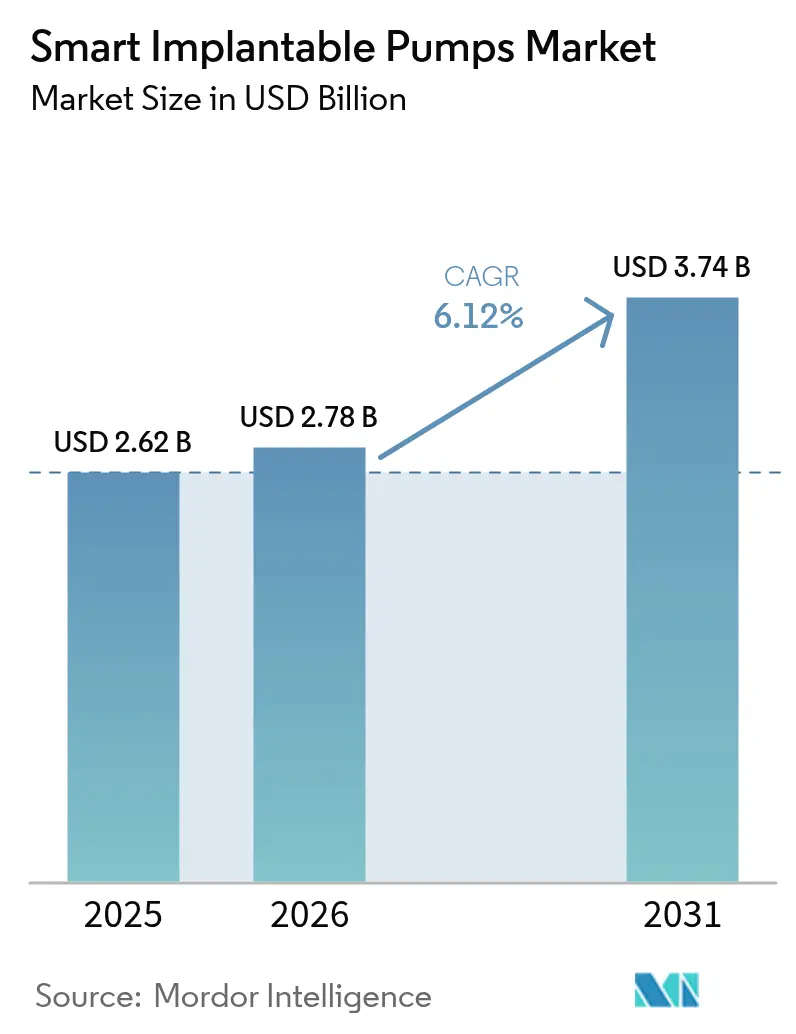

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Implantable Pumps Market Analysis by Mordor Intelligence

The Smart implantable pumps market size is expected to grow from USD 2.62 billion in 2025 to USD 2.78 billion in 2026 and is forecast to reach USD 3.74 billion by 2031 at 6.12% CAGR over 2026-2031. Closed-loop automation, cybersecurity-aligned fast-track approvals and the migration of infusion therapies from inpatient wards to home settings sustain a balanced demand curve. Perfusion systems anchor the revenue base thanks to proven clinical efficacy in chronic pain, while BioMEMS-enabled micro pumps open high-growth niches by achieving nano-scale dose accuracy. Reimbursement reforms under the NOPAIN Act lower patient out-of-pocket costs for out-of-hospital procedures, and interoperability partnerships among leading manufacturers strengthen ecosystem lock-in. At the same time, battery longevity challenges and exacting FDA cyber documentation requirements temper near-term enthusiasm but ultimately raise the entry barrier, benefiting compliant suppliers.

Key Report Takeaways

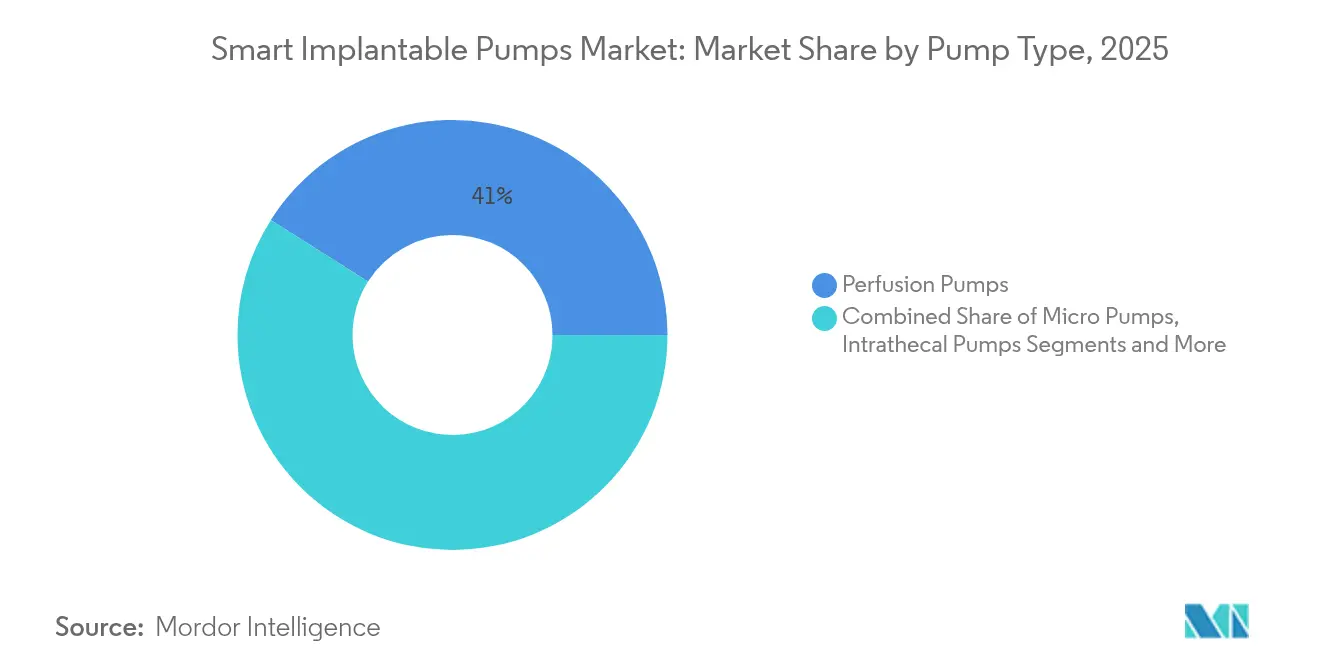

- By pump type, perfusion pumps held 41.02% of Smart implantable pumps market share in 2025, whereas micro pumps are projected to grow at 15.88% CAGR to 2031.

- By application, pain management accounted for the largest 37.01% revenue slice in 2025; oncology is on track for a 12.31% CAGR through 2031.

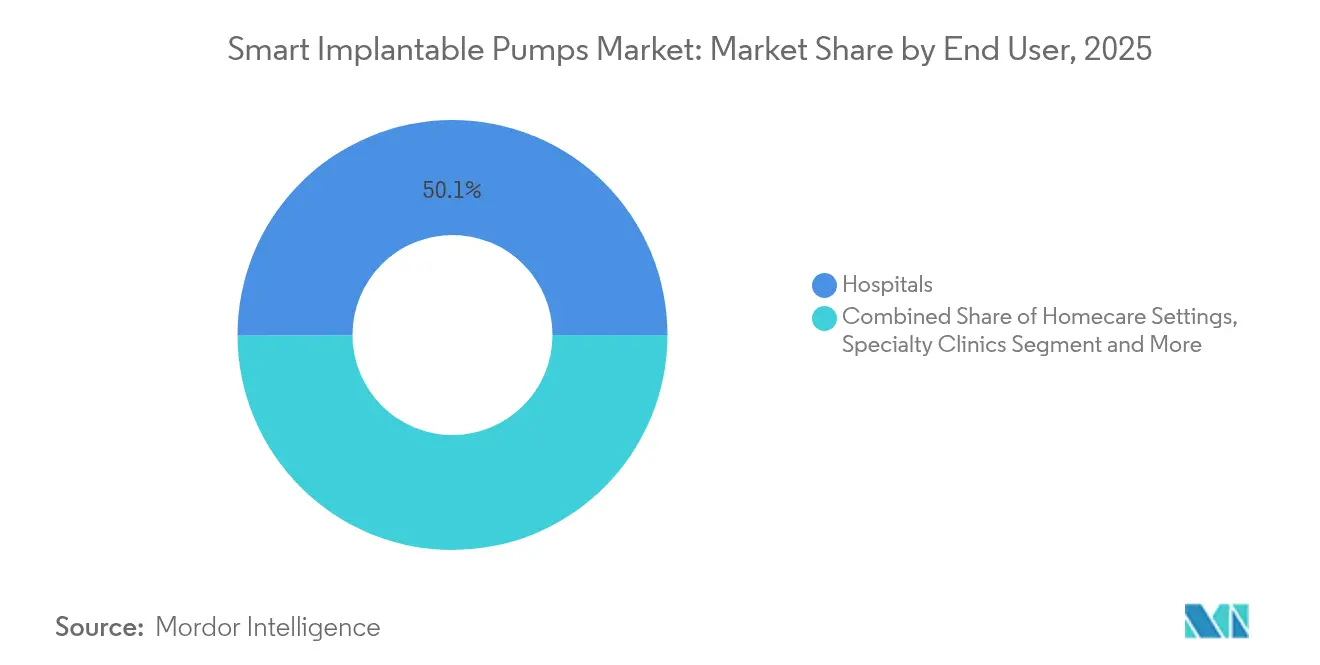

- By end user, hospitals commanded 50.05% of the Smart implantable pumps market size in 2025, while homecare settings are expanding the fastest at 10.12% CAGR.

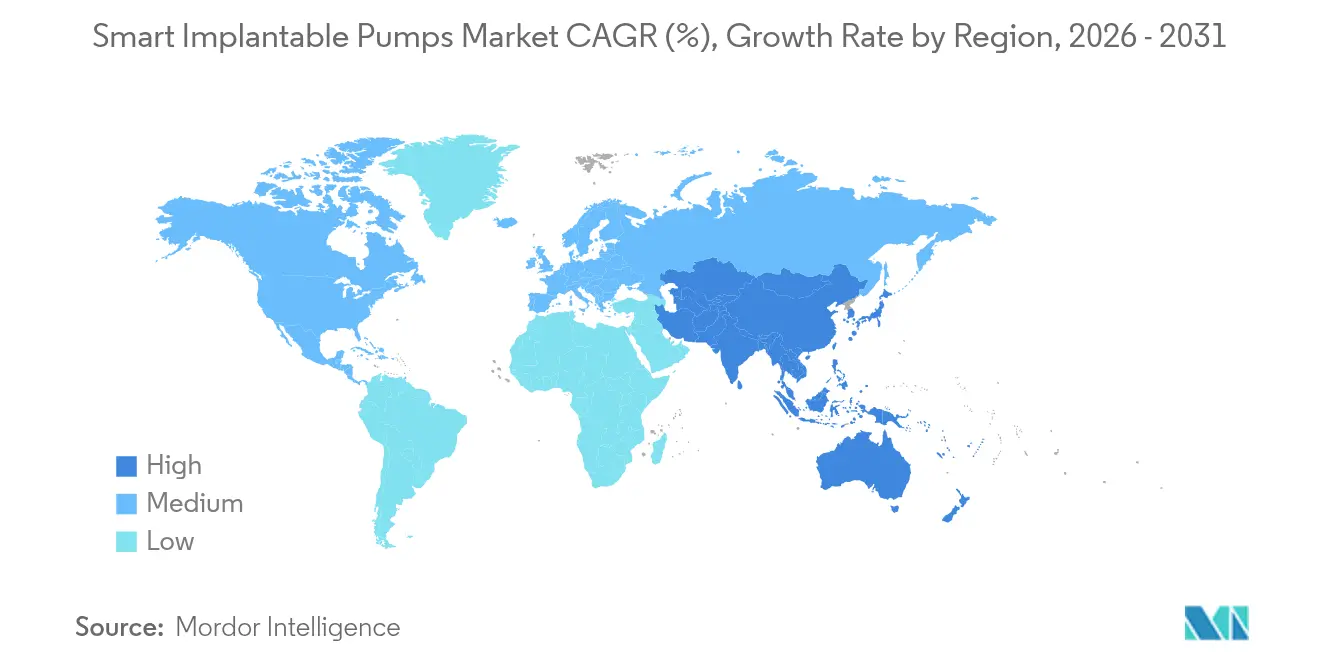

- By geography, North America led with 39.85% share in 2025, whereas Asia-Pacific is poised for a 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Implantable Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of chronic diseases | +1.8% | Global; especially North America and Europe | Long term (≥ 4 years) |

| Aging population and long-term care burden | +1.2% | Global; notably Asia-Pacific and Europe | Long term (≥ 4 years) |

| Advancements in closed-loop & IoT technology | +1.5% | North America and EU; scaling into Asia-Pacific | Medium term (2-4 years) |

| Shift to home-based and ambulatory care | +0.9% | North America and EU; early uptake in urban Asia-Pacific | Medium term (2-4 years) |

| Emergence of BioMEMS nano-fluidic micro-dosing | +0.7% | R&D hubs in North America and EU | Long term (≥ 4 years) |

| Cybersecurity-driven regulatory fast-tracking | +0.4% | Global; spearheaded by FDA and EU authorities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Prevalence Of Chronic Diseases

Global diabetes prevalence surpassed 537 million adults in 2025, widening the therapeutic field beyond pain management toward insulin, baclofen and chemotherapeutic delivery. Intrathecal baclofen pumps cut spasticity severity by 40.25% in multiple cohort analyses, directly improving motor performance in cerebral palsy. Registry reviews tracking 1,403 oncology cases documented durable pain control over 12 months when implantable systems replaced systemic opioids. Such outcome evidence underpins payer justification and accelerates prescriber confidence, driving incremental Smart implantable pumps market adoption across neurological and oncologic specialties.

Advancements In Closed-Loop & IoT-Enabled Pump Technology

Medtronic’s MiniMed 780G delivers >80% Time-in-Range results, surpassing ADA glycemic targets in real-world cohorts[1]Medtronic plc, “MiniMed 780G Real-World Data,” medtronic.com. Nevro’s HFX iQ integrates adaptive algorithms that tailor spinal stimulation parameters, illustrating the shift toward AI-directed therapy. FDA cybersecurity guidance issued in 2025 codifies secure-by-design principles, giving manufacturers a predictable path to clearance. Interoperability alliances, such as Abbott’s global CGM-pump integration deals, future-proof installed bases and extend recurring revenue streams.

Shift To Home-Based And Ambulatory Care

Separate Medicare payments of USD 2,284.98 per advanced infusion pump, effective 2025 under the NOPAIN Act, sharpen outpatient economics and reduce inpatient backlog[2]Avanos Medical, “ON-Q and ambIT Payment Under NOPAIN Act,” avanos.investorroom.com. Firmware-upgradable platforms such as SynchroMed III let clinicians recalibrate flow parameters remotely, maintaining vigilance while cutting clinic visits. Patient-reported data show 90% of chronic pain users would recommend intrathecal therapy, while 94% reduced systemic opioid reliance, underscoring a user-experience dividend that fuels Smart implantable pumps market expansion into domiciliary care.

Emergence of BioMEMS Nano-Fluidic Micro-Dosing

Silicon micro-pumps achieving 12 ml/min flow rates without counter-pressure prove scalability beyond laboratory prototypes. Piezoelectric devices now dispense 0.28 µL increments with no electromagnetic interference, aligning with implant safety needs. Sequentially triggerable nano-nozzle systems enable on-demand chronotherapy, pointing toward personalized circadian dosing matrices. Venture flows chasing a projected USD 24.5 billion BioMEMS sector underwrite ongoing R&D, positioning micro-engineered pumps as vital components in precision medicine and sustaining long-run Smart implantable pumps market momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny & recall risk | -0.8% | North America and EU | Medium term (2-4 years) |

| Battery longevity & biocompatibility issues | -1.1% | Global | Long term (≥ 4 years) |

| Escalating cyber-threat surface | -0.6% | Worldwide; most visible in connected pump segments | Short term (≤ 2 years) |

| Limited surgical expertise | -0.9% | Emerging markets primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny & Recall Risk

Section 524B now obliges every cyber-device submission to include a Software Bill of Materials, threat modeling and remediation road map, extending dossier volume and review times. ICU Medical’s 2025 warning letter illustrates the financial and reputational cost when legacy infusion platforms fall short of updated standards[3]Center for Devices and Radiological Health, “ICU Medical Warning Letter,” fda.gov. Design-control rigor mandated under 21 CFR 820 inflates development budgets but ultimately elevates product reliability. For smaller innovators, capital scarcity heightens acquisition likelihood, nudging the Smart implantable pumps market toward moderate concentration.

Battery Longevity & Biocompatibility Issues

Existing lithium packs demand change-outs every 5-7 years, exposing patients to repeated OR events and aggregate costs that curb adoption in price-sensitive locales. Foreign-body responses trigger fibrosis that can impair flow ports, as documented in multiple biomaterial studies. Anti-biofouling coatings under development at Wyss Institute prolong biosensor life by arresting bacterial adhesion, a breakthrough that could migrate to infusion pumps. Silicon IC encapsulation with PDMS extends hermeticity in accelerated aging tests but full physiological validation remains in progress. Persistent heavy-metal ion leaching pushes material science toward nickel-free alloys and polymer composites, but until resolved the drag on Smart implantable pumps market penetration persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Micro Pumps Drive Innovation

The segment generated 41.02% of 2025 revenue from perfusion models, anchoring the Smart implantable pumps market size in inpatient pain therapy. Micro pumps, however, exhibit a 15.88% CAGR that redefines growth math. Their MEMS sensors synchronize real-time flow with sensor feedback, facilitating sub-microliter precision and widening therapeutic scope to gene vectors and biologics. AI-optimized control loops, already standard in hybrid insulin platforms, migrate to micro pump architectures to personalize intra-day dosing. Supply-chain localization and wafer-level manufacturing cut cost curves, lowering entry thresholds for start-ups and thereby diversifying vendor rosters within the Smart implantable pumps market.

Second-generation perfusion units retain surgical mindshare thanks to simple programmability, but predictive maintenance modules now alert clinicians to reservoir depletions and catheter resistance spikes. Drug-eluting and iontronic variants join R&D pipelines, offering infection-mitigation and on-chip sterilization features that could reclaim share from competitive neuromodulation alternatives. As proprietary algorithms accrue real-world data, manufacturers consolidate dataset advantages that complicate late entrant catch-up.

By Application: Oncology Accelerates Growth

Pain management captured the largest slice of Smart implantable pumps market share at 37.01% in 2025 and remains favored by payers for opioid-sparing outcomes. Nonetheless, oncology registers the quickest 12.31% CAGR as hepatic-arterial and intrathecal chemotherapeutic pumps outperform systemic regimens in multiple survival and quality-of-life metrics. FDA PMA approval for Sequana’s alfapump underscores regulator willingness to green-light class III actives when survival benefit is evident.

Cardiovascular adoption tracks LVAD miniaturization, evidenced by CorWave’s first-in-human membrane pump implantation delivering physiologic pulsatility. Endocrinology trails but gains ground as biannual GLP-1 implants improve compliance in obesity management. Collectively, these emerging indications embed resilience into overall Smart implantable pumps market demand by reducing reliance on a single therapy area.

By End User: Homecare Settings Transform Delivery

Hospitals retained 50.05% revenue in 2025, benefiting from integrated surgical suites and intensivist oversight intrinsic to initial implantation. Yet, 10.12% CAGR in homecare signals a structural swing toward patient-managed therapy. Cloud-linked programmer wands allow clinicians to titrate flow remotely, cutting follow-up appointments and enabling decentralized care models. Specialty pain clinics utilize ambulatory pumps to discharge patients the same day, thereby capturing DRG savings under value-based purchasing schemes.

Ambulatory surgical centers combine capital-light infrastructure with anesthesia efficiency to slice procedural costs, a combination amplified by dedicated Medicare codes. Home infusion providers now recruit biomedical engineers to troubleshoot alerts, demonstrating ancillary employment spillovers from Smart implantable pumps market growth. The net effect shifts budgetary power from inpatient administrators to at-home service managers, reshaping future go-to-market strategies.

Geography Analysis

North America contributed 39.85% of 2025 turnover, underpinned by extensive payer coverage and a robust clinical trial ecosystem. Europe follows with CE solidarity enabling multi-country launches off a single dossier, though slower reimbursement cycles temper early uptake. China’s volume-based procurement and indigenous manufacturing grants stimulate local production of programmable pumps, lowering ASPs and broadening domestic access.

Asia-Pacific’s 9.18% CAGR arises from demographic aging and chronic disease incidence intersecting with state incentives for smart device localization. India’s frugal engineering adapts high-end models into cost-efficient variants suitable for tier-2 city clinics. Partnerships that bundle AI analytics with pump hardware appeal to public-health buyers focused on remote regions, reinforcing digital-health alignment in regional tender criteria.

Regulatory convergence initiatives, such as Singapore’s IMDRF leadership, reduce redundant clinical testing and accelerate cross-border registration. Concurrently, cybersecurity stipulations modeled on FDA precedents assure end users of data protection, narrowing the perceived quality gap versus Western imports. Steadily, these dynamics propel Smart implantable pumps market penetration deeper into populous economies while seeding global supply-chain resilience.

Competitive Landscape

Moderate consolidation typifies the Smart implantable pumps market: top incumbents leverage portfolio breadth and data ecosystems, while venture-backed entrants peel off high-innovation niches. Medtronic and Abbott solidified an interoperable CGM-pump hub, tethering glycemic analytics, infusion algorithms and cloud dashboards into a cohesive user journey. Boston Scientific’s selective acquisition of Intera Oncology aligns with a strategy of owning specialized, high-margin indications rather than broad platforms.

Vivani Medical pursues adherence-oriented implants, securing USD 3 million equity to progress once-yearly semaglutide dosing designs. ClearPoint Neuro exploits MRI-guided cannula navigation to expand procedural addressability in neurosurgical pumps. Cybersecurity capabilities, measured by SBOM transparency and zero-trust frameworks, emerge as deal-breaking selection criteria in tenders, favoring players with mature DevSecOps pipelines.

Patent filings cluster around low-profile reservoirs, hermetic micro-valves and adaptive closed-loop algorithms, signaling where firms perceive durable differentiation. Licensing cross-pollination flourishes: Beta Bionics integrates Abbott sensors into its bionic pancreas, evidencing an openness to modular cooperation amid intensifying platform wars. Overall, ecosystem control, rather than single-device supremacy, defines competitive advantage.

Smart Implantable Pumps Industry Leaders

Cognos Therapeutics, Inc.

Insulet Corporation

Intera Oncology

Medtronic plc

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CorWave performed the first human implantation of its wave-membrane LVAS at St Vincent’s Hospital in Sydney.

- December 2024: Sequana Medical secured FDA PMA for alfapump to treat refractory ascites associated with liver cirrhosis in the United States.

Global Smart Implantable Pumps Market Report Scope

Smart implantable pumps enable the monitoring of drug delivery rate exteriorly, which is beyond the abilities of conservative controlled release preparations. Implantable pumps consist of a reservoir placed subcutaneously and are connected through a catheter to deliver the drug into the desired body part. These pumps are used to deliver anti-spasmodic, chemotherapeutic agents and opioid drugs. The Smart Implantable Pumps market is segmented By pump type, application, end-user, and geography. The pump type segment is further fragmented into perfusion pumps and micro pumps. The application segment is further divided into pain, spasticity, cardiovascular, and others. The end user segment is further bifurcated into hospitals, ambulatory surgical centers, and others). The geography is further segmented into North America, Asia-Pacific, Europe, the Middle East and Africa, and South America. The report also elucidates the projected market sizes and trends for 17 different countries across major regions globally. It further offers the value (in USD) for the above segments.

| Perfusion Pumps |

| Micro Pumps |

| Programmable Insulin Pumps |

| Intrathecal Pumps |

| Drug-Eluting Pumps |

| Pain Management |

| Spasticity Management |

| Cardiovascular Disorders |

| Diabetes Management |

| Oncology |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Homecare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pump Type | Perfusion Pumps | |

| Micro Pumps | ||

| Programmable Insulin Pumps | ||

| Intrathecal Pumps | ||

| Drug-Eluting Pumps | ||

| By Application | Pain Management | |

| Spasticity Management | ||

| Cardiovascular Disorders | ||

| Diabetes Management | ||

| Oncology | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Homecare Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Smart implantable pumps market in 2031?

The sector is expected to reach USD 3.74 billion by 2031.

Which pump type is growing the fastest?

BioMEMS-enabled micro pumps are forecast to post a 15.88% CAGR through 2031.

Which therapeutic area is expanding most rapidly?

Oncology applications lead with a 12.31% CAGR over the forecast horizon.

How are reimbursement changes influencing adoption?

Separate Medicare payments of USD 2,284.98 per device in ambulatory settings significantly improve outpatient economics and encourage wider use.

What geographic region offers the highest growth potential?

Asia-Pacific is projected to grow at 9.18% CAGR thanks to aging demographics and local manufacturing initiatives.

What is a key technical hurdle for long-term implant performance?

Battery life limitations, currently requiring replacement every 5-7 years, remain the primary engineering challenge.

Page last updated on: