Intrathecal Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

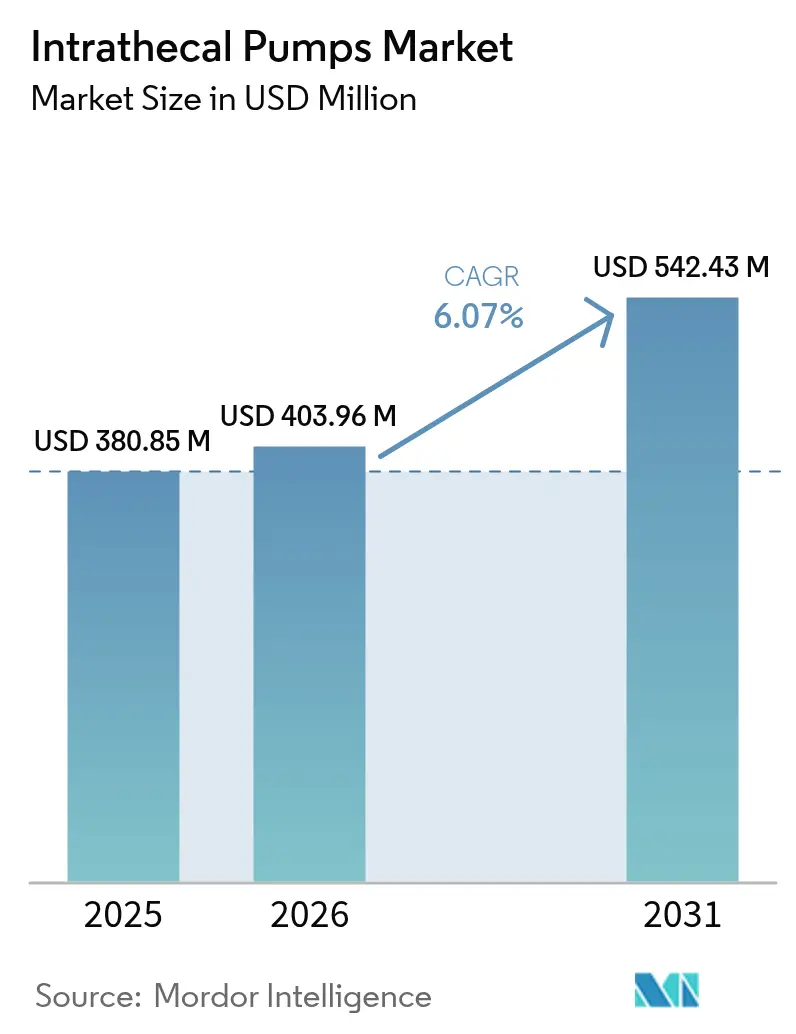

| Market Size (2026) | USD 403.96 Million |

| Market Size (2031) | USD 542.43 Million |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

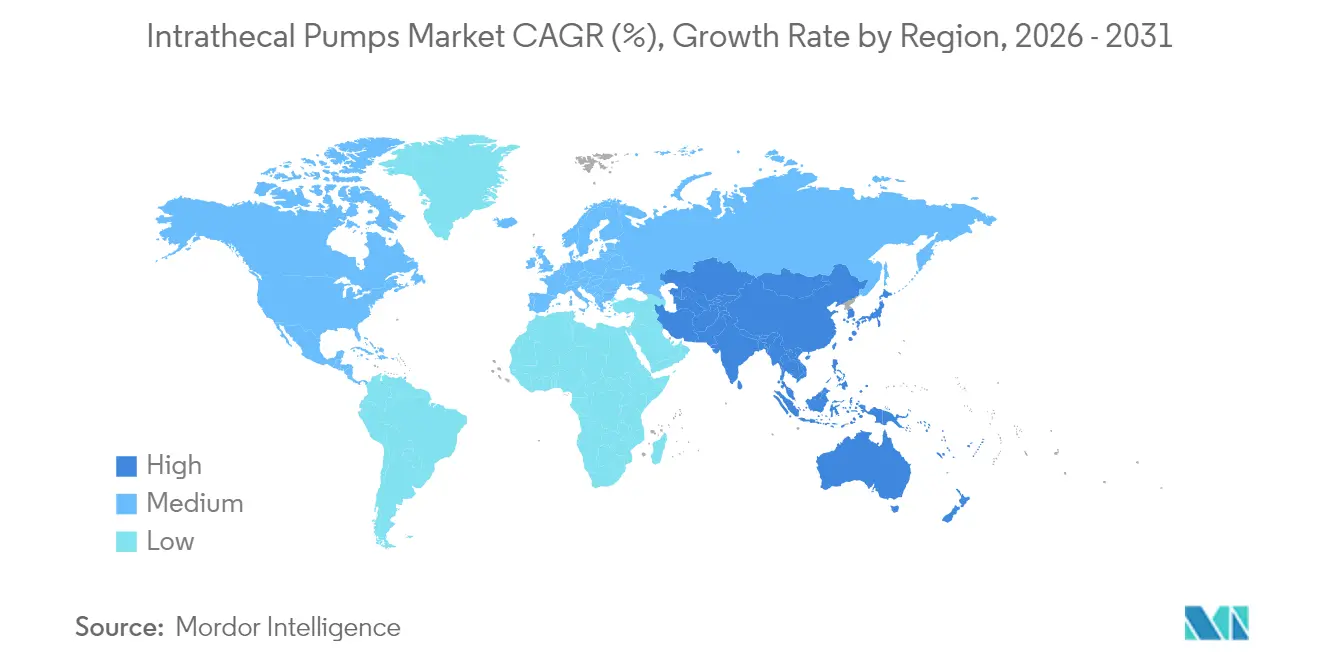

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

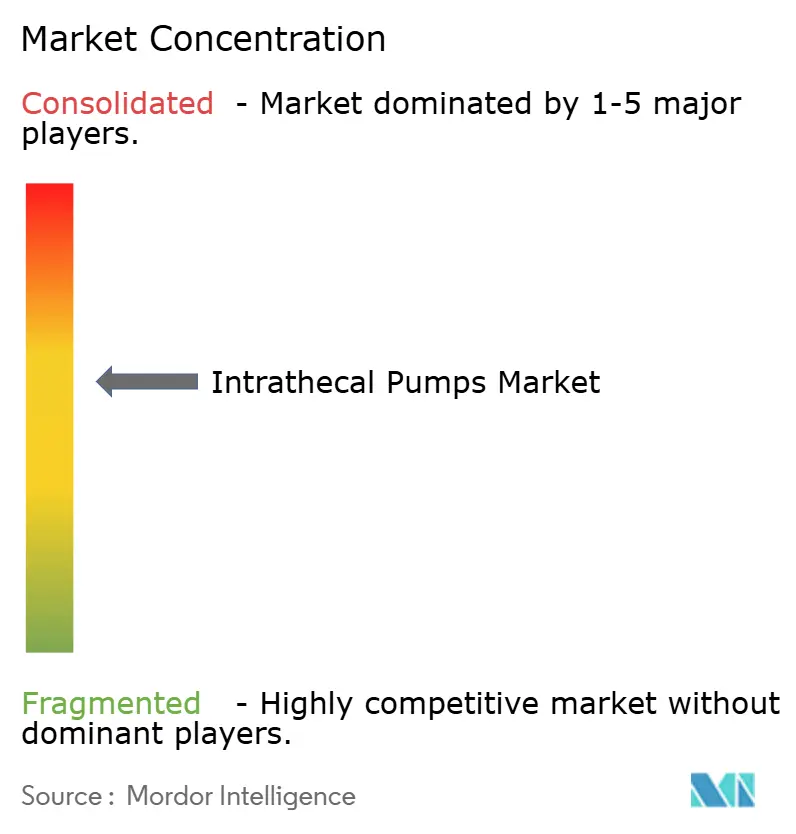

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intrathecal Pumps Market Analysis by Mordor Intelligence

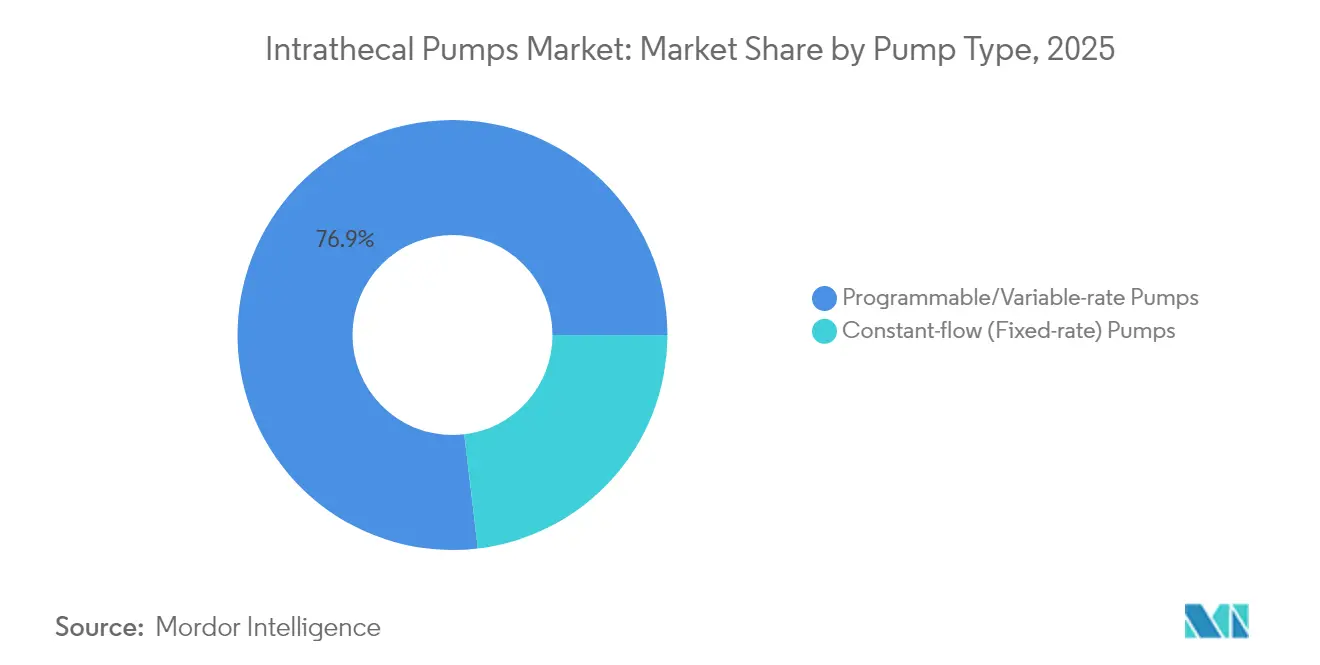

Intrathecal pumps market size in 2026 is estimated at USD 403.96 million, growing from 2025 value of USD 380.85 million with 2031 projections showing USD 542.43 million, growing at 6.07% CAGR over 2026-2031. Steady demand springs from the clinical shift toward targeted drug delivery that limits systemic opioid exposure while improving therapeutic precision. Hospitals increasingly favor programmable pumps that allow dose titration aligned with circadian rhythms, and payers expand coverage as economic models prove cost savings within three years of implantation. Programmed variable-rate devices dominate the intrathecal pumps market with 77.55% 2024 share, reflecting physician preference for sophisticated control algorithms. Baclofen remains the leading drug class by revenue, yet ziconotide registers the fastest uptake on the strength of evidence in opioid-refractory pain. North America retains nearly half of global revenue thanks to robust reimbursement and a deep specialist base, whereas Asia-Pacific leads growth as health systems upgrade chronic pain and spasticity services. Moderate competitive intensity persists: Medtronic defends leadership through SynchroMed III upgrades and extensive clinical data, while Boston Scientific and Flowonix Medical push MRI-conditional or closed-loop functionality to capture unmet needs.

Key Report Takeaways

- By pump type, programmable and variable-rate systems commanded 76.88% of intrathecal pumps market share in 2025; constant-flow pumps are expected to trail while programmable units expand at a 9.94% CAGR through 2031.

- By product class, baclofen accounted for a 41.10% share of intrathecal pumps market size in 2025; ziconotide is forecast to grow at an 11.38% CAGR to 2031.

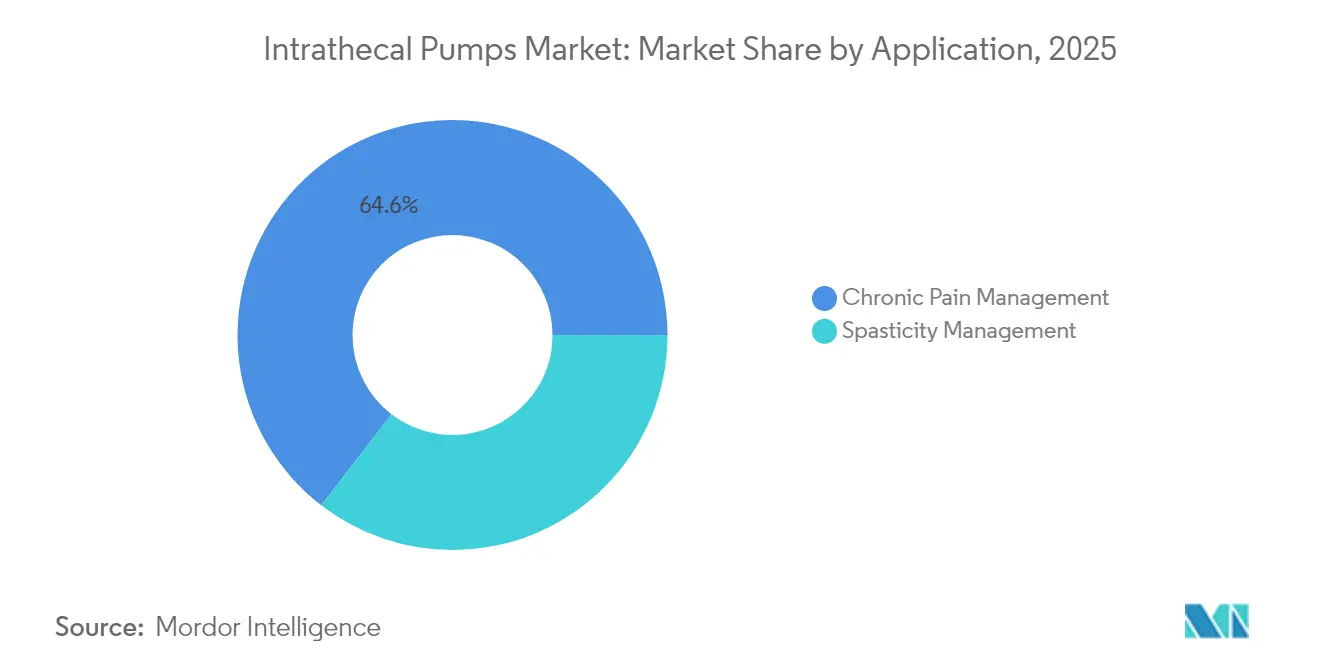

- By application, chronic pain management held 64.55% of intrathecal pumps market share in 2025; spasticity management is moving ahead at a 9.12% CAGR through 2031.

- By end user, hospitals and clinics held 60.10% share of the market in 2025, while home-care & long-term care settings posts the strongest CAGR at 10.44% through 2031.

- By geography, North America led with 48.10% revenue share in 2025; Asia-Pacific is on track for a 10.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intrathecal Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic back pain & spasticity | +1.2% | Global with concentration in North America & Europe | Long term (≥ 4 years) |

| Rising demand for targeted drug-delivery alternatives to systemic opioids | +1.5% | North America & Europe primary, expanding to APAC | Medium term (2-4 years) |

| Rapid technology upgrades (programmable / MRI-conditional pumps) | +0.8% | Global, led by developed markets | Short term (≤ 2 years) |

| Payer-driven opioid-stewardship programs boosting pump adoption | +1.1% | North America primary, Europe secondary | Medium term (2-4 years) |

| AI-guided refill-dose algorithms improving clinic throughput | +0.6% | North America & Europe, selective APAC markets | Long term (≥ 4 years) |

| Expansion into neuro-oncology enabled by MRI-safe designs | +0.7% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence Of Chronic Back Pain & Spasticity

An aging population and sedentary lifestyles keep the addressable pool for intrathecal therapy expanding, with 50 million adults in the United States alone reporting chronic pain[1]Centers for Disease Control, “Chronic Pain in the United States,” cdc.gov. Rising survival after spinal cord injury and multiple sclerosis enlarges the spasticity segment, and studies show intrathecal baclofen cuts spasticity scores by 40.25% and lifts motor function by 9.62% in cerebral palsy. Better outcomes spur referrals from primary care to specialist centers that house pump surgery programs. Hospitals treat pumps as long-term value propositions that reduce readmissions and bolster patient-reported quality of life. The intrathecal pumps market therefore penetrates deeper into neurology clinics and rehabilitation facilities.

Rising Demand For Targeted Drug-Delivery Alternatives To Systemic Opioids

Health systems confronting opioid misuse pivot toward modalities requiring minimal systemic dosing: intrathecal morphine uses roughly 1/300th of the oral amount yet sustains analgesia. The 2025 NOPAIN Act gives non-opioid devices a separate Medicare payment, nudging hospitals to adopt pump therapy[2]Avanos Medical, “ON-Q* Elastomeric Infusion Pump,” avanosmedical.com. Half of implanted patients discontinue systemic opioids within 12 months, supporting payer initiatives that link reimbursement to opioid-sparing outcomes. The intrathecal pumps market rides these stewardship programs as formularies explicitly list pumps as preferred non-opioid interventions.

Rapid Technology Upgrades (Programmable / MRI-Conditional Pumps)

FDA clearance of closed-loop systems such as Inceptiv enables real-time physiologic feedback, with 88% of users preferring automated adjustments. Equal importance lies in MRI compliance: 80% of candidates need at least one MRI inside five years. Newly launched variable-rate pumps allow wireless, cloud-based dosing schedules that match activity patterns, though hospitals invest in cybersecurity layers to mitigate hacking risk. Superior clinical outcomes and streamlined workflows sustain premium pricing, steering budget committees to allocate capital. Consequently, programmable platforms remain the main revenue engine of the intrathecal pumps market.

Payer-Driven Opioid-Stewardship Programs Boosting Pump Adoption

Policies such as Wisconsin Medicaid’s 2025 update now cover pumps for spasticity and pain under clearer prior-authorization rules. Economic models show pumps reach cost neutrality within three years by slashing drug expenditures and emergency visits. Payers mandate objective screening protocols that boost clinician confidence, and bundled payments reward facilities that demonstrate quality improvements. The intrathecal pumps market experiences accelerated procedure volumes as institutions align with value-based metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device & implantation cost | -1.8% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Low clinical-staff awareness in emerging markets | -1.2% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Hospital cybersecurity concerns over wireless programmers | -0.4% | North America & Europe primarily | Short term (≤ 2 years) |

| Titanium-alloy supply-chain bottlenecks post-2024 | -0.3% | Global manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device & Implantation Cost

Acquisition of an implantable pump exceeds USD 20,000, and surgical fees, programmer hardware, and follow-up push the initial bundle higher[3]Aetna, “Infusion Pumps – Medical Clinical Policy Bulletins,” aetna.com. The multi-disciplinary expertise needed for implantation raises operational overhead, making return-on-investment math difficult for smaller hospitals. Insurers demand exhaustive documentation of previous conservative failures, delaying therapy onset. Budget-strained health systems in Latin America and parts of APAC allocate funds to primary care rather than advanced devices, slowing market entry even though total three-year cost is favorable versus systemic opioids.

Low Clinical-Staff Awareness In Emerging Markets

Physician familiarity remains concentrated in tertiary centers, leaving district hospitals without trained implanters. Language barriers reduce uptake of latest English-language guidelines, and lack of standardized certification limits clinician confidence. Consequently, referral pathways are fragmented, and eligible patients often receive oral narcotics instead. Manufacturers respond with virtual training platforms, yet time-zone alignment and bandwidth constraints hamper reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Programmable Systems Drive Innovation

Programmable pumps delivered 76.88% revenue in 2025 and are on a 9.94% growth slope, confirming their status as the mainstay of the intrathecal pumps market. Advanced models integrate wireless charging and 99% five-year survival, minimizing replacement surgeries. Constant-flow pumps retain a contingent niche for straightforward regimens and lower capital outlay. Hospitals adopt dual-inventory strategies, reserving variable-rate devices for complex neuralgia or multi-drug cocktails while allocating constant-flow units to end-of-life cancer pain. Surveys show neurologists value fine-grain programming that mirrors circadian patterns, especially for dystonia and spasticity.

AI modules analyze dosing history, automatically proposing flow adjustments that physicians review. Long-term data indicate reduced side effects and fewer emergency titrations compared with fixed-rate systems, reinforcing the premium footprint of programmable technology. The intrathecal pumps industry continues to funnel R&D toward battery chemistry, miniaturization, and Bluetooth-Low-Energy modules that meet hospital network standards.

By Product Class: Baclofen Dominance with Ziconotide Momentum

Baclofen remained the anchor drug, holding 41.10% of intrathecal pumps market size in 2025 and continuing steady adoption thanks to a well-documented safety profile in spasticity bmcneurol.biomedcentral.com.

Ziconotide’s 11.38% CAGR underlines growing confidence following updated PACC titration protocols that mitigate neuropsychiatric events. Morphine and hydromorphone persist for palliative cancer indications, while bupivacaine serves mixed neuropathic pain. Combination reservoirs deliver synergistic effects at lower individual doses, lowering adverse events. Pipeline nanoparticle formulations aim for extended stability, which could shrink refill frequency and expand indications. The intrathecal pumps market therefore balances entrenched baclofen demand with agile ziconotide growth.

By Application: Pain Management Leadership with Spasticity Growth

Chronic pain management contributed 64.55% of intrathecal pumps market share in 2025, helped by broadened indications such as complex regional pain syndrome. Cancer pain registries show 85% of patients gained at least 20% pain relief after pump implantation, and palliative care teams increasingly consider pumps earlier. Spasticity management climbs at a 9.12% CAGR as neurologists view severe tone disorders as controllable rather than inevitable. Cerebral palsy cohorts demonstrate functional gains that support school participation. Dual-symptom protocols are tested, combining baclofen for tone and low-dose opioids for pain. Future adoption in neuro-oncology will further blur application lines, raising the intrathecal pumps market ceiling.

By End-user: Hospital Dominance with Home Care Growth

Hospitals and clinics produced 60.10% revenue in 2025, reflecting surgical expertise concentration and the need for sterile refill suites. Ambulatory surgery centers capture minor but growing volumes by offering outpatient implantation packages under regional anesthesia. Home care shows 10.44% CAGR, propelled by remote programming and telehealth follow-up. Cloud dashboards enable clinicians to adjust doses without clinic visits, which benefits rural populations. Long-term care facilities integrate pumps for elderly residents to avoid polypharmacy and cognitive decline. Pandemic-driven modernization of home monitoring infrastructure should push community penetration higher, granting the intrathecal pumps market wider geographic reach.

Geography Analysis

North America commanded 48.10% of global revenue in 2025 due to clear reimbursement, an extensive specialist base, and strong manufacturer presence. Medicare’s consistent coding structure shortens billing cycles, while private insurers align with opioid-reduction targets. Research investments nurture continuous device upgrades and feed rapid clinical adoption.

Europe follows a structured pathway emphasizing evidence-based funding schemes such as Germany’s NUB program that annually supports novel pump technologies. The British Pain Society’s 2024 guideline update clarifies patient selection and standardizes dosing, leading to harmonized referrals across the region. Aging demographics and chronic disease burdens guarantee sustained volume.

Asia-Pacific represents the fastest-expanding segment at 10.44% CAGR, fueled by Japan’s universal coverage, China’s ongoing health-system reforms, and India’s private-sector hospital boom. Academic centers in Seoul and Singapore run collaborative pump registries that build localized evidence. Cost remains the foremost barrier, but public–private partnerships and medical tourism increasingly bridge gaps. Consequently, the intrathecal pumps market stands to witness rapid volume growth once reimbursement pathways mature across Asian economies.

Competitive Landscape

The intrathecal pumps market features moderate concentration. Medtronic controls a sizeable installed base, exceeding 300,000 cumulative implants through 2025 with its SynchroMed line. Boston Scientific leverages MRI-compatible WaveWriter systems and hybrid electrical-drug platforms, seizing share in refractory pain segments. Flowonix Medical focuses on lower-profile titanium housings and customizable software to appeal to neuro-oncology specialists.

Strategic emphasis has migrated toward integrated care ecosystems: vendors couple hardware with cloud dashboards, AI analytics, and catheter monitoring. Regulatory recalls of competitive external infusion pumps in 2024 opened a credibility gap that incumbents swiftly filled with reliability campaigns. Partnerships emerge between device makers and pharma companies to develop proprietary intrathecal formulations, locking customers into closed supply chains. Start-ups gain FDA STeP support for flexible control modules, but scaling remains constrained by capital needs. Over the forecast horizon, competition will revolve around cybersecurity robustness, MRI depth rating, and service packages that reduce provider workload.

Intrathecal Pumps Industry Leaders

Tricumed Medizintechnik GmbH

Teleflex, Inc.

Flowonix Medical, Inc.

Medtronic plc

Johnson & Johnson (Codman/Cerenovus)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Avanos Medical secured separate Medicare payment for its ON-Q and ambIT infusion pumps under the NOPAIN Act.

- July 2024: Alcyone Therapeutics advanced enrollment in the PIERRE study evaluating the ThecaFlex DRx system for spinal muscular atrophy.

Global Intrathecal Pumps Market Report Scope

As per the scope of the report, intrathecal pumps are generally used to treat cancer pain, pain from failed surgeries, or where high doses of opioids and/or morphine are required. These pumps are placed under the skin of the abdomen through the surgery and deliver medicine through the catheter to the cerebrospinal fluid in the patient's spinal cord. This enables the pump to deliver a more accurate dose of medication compared to oral medicines.

The intrathecal pumps market is segmented by product class (baclofen, hydromorphone, morphine, bupivacaine, and others), application (pain management and spasticity management), end-user (hospitals & clinics, ambulatory surgery centers), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America).

The report offers the value (in USD ) for the above segments.

| Programmable/Variable-rate Pumps |

| Constant-flow (Fixed-rate) Pumps |

| Baclofen |

| Morphine |

| Hydromorphone |

| Bupivacaine |

| Ziconotide |

| Other APIs (Clonidine, Prialt combinations) |

| Chronic Pain Management |

| Spasticity Management |

| Hospitals & Clinics |

| Ambulatory Surgery Centers |

| Home-care & Long-term Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pump Type | Programmable/Variable-rate Pumps | |

| Constant-flow (Fixed-rate) Pumps | ||

| By Product Class | Baclofen | |

| Morphine | ||

| Hydromorphone | ||

| Bupivacaine | ||

| Ziconotide | ||

| Other APIs (Clonidine, Prialt combinations) | ||

| By Application | Chronic Pain Management | |

| Spasticity Management | ||

| By End-user | Hospitals & Clinics | |

| Ambulatory Surgery Centers | ||

| Home-care & Long-term Care Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the intrathecal pumps market?

The market is valued at USD 403.96 million in 2026 and is forecast to climb to USD 542.43 million by 2031.

Which pump type holds the largest share of the intrathecal pumps market?

Programmable and variable-rate systems account for 76.88% of 2025 revenue and show the fastest growth trajectory.

Which drug class leads sales in intrathecal therapy?

Baclofen leads with 41.10% share, while ziconotide records the quickest CAGR at 11.38%.

Which region grows the fastest in the intrathecal pumps market outlook?

Asia-Pacific advances at a 10.44% CAGR through 2031, buoyed by expanding healthcare infrastructure and chronic disease prevalence.

How do intrathecal pumps lower systemic opioid use?

Typical intrathecal morphine doses are about 1/300th of oral equivalents, and 51% of implanted patients discontinue other opioids within one year, supporting stewardship goals.

Page last updated on: