Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 359.44 Billion |

| Market Size (2031) | USD 458.31 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Equity Lending Market Analysis by Mordor Intelligence

The Global home equity lending market size was valued at USD 342.39 billion in 2025 and estimated to grow from USD 359.44 billion in 2026 to reach USD 458.31 billion by 2031, at a CAGR of 4.98% during the forecast period (2026-2031). Elevated “tappable” equity, locked-in low first-lien mortgage coupons, and tax-advantaged borrowing costs keep demand resilient even as traditional cash-out refinancing wanes. Lenders are capitalizing on record USD 32 trillion of U.S. homeowner equity by rolling out flexible lines of credit, hybrid draw structures, and bundled renovation financing. North America retains the lion’s share of originations, yet Asia-Pacific is posting the quickest uptake as China and India liberalize consumer-credit rules. Across every region, automated valuation models (AVMs) and AI-driven underwriting shave processing costs by hundreds of dollars per loan, allowing price competition even in a rising-rate backdrop.

Key Report Takeaways

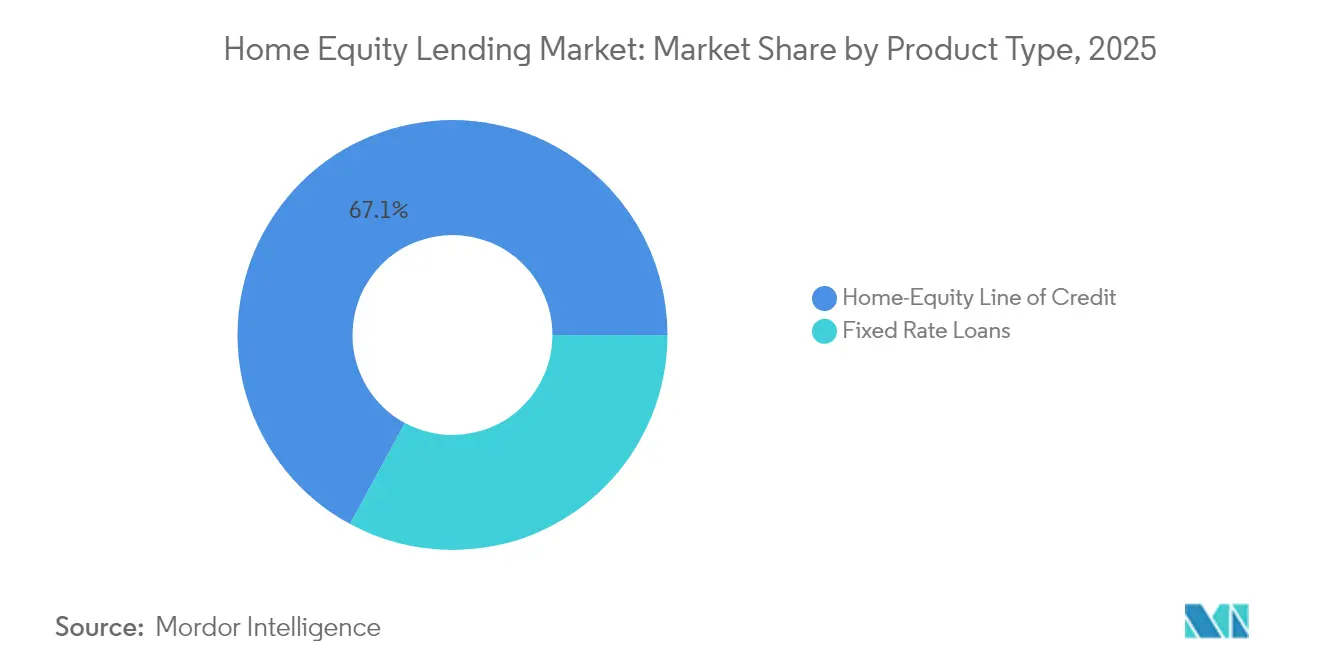

- By product type, home equity lines of credit (HELOCs) captured 67.10% share of the home equity lending market in 2025 and are forecasted to grow at a 6.08% CAGR through 2031.

- By provider, banks held 58.05% of the home equity lending market share in 2025, while fintech-led nonbanks posted the fastest 8.34% CAGR outlook.

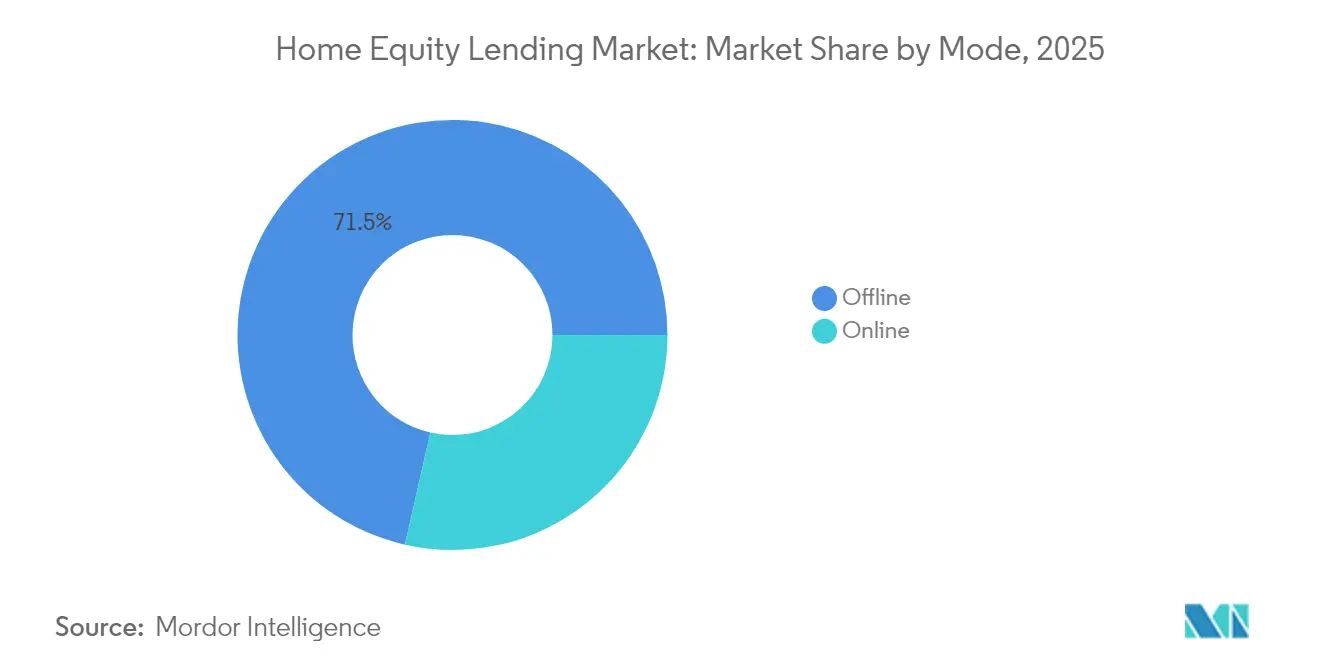

- By mode, offline channels retained a 71.45% share of the home equity lending market in 2025; online originations are growing 8.55% annually as digital document collection becomes mainstream.

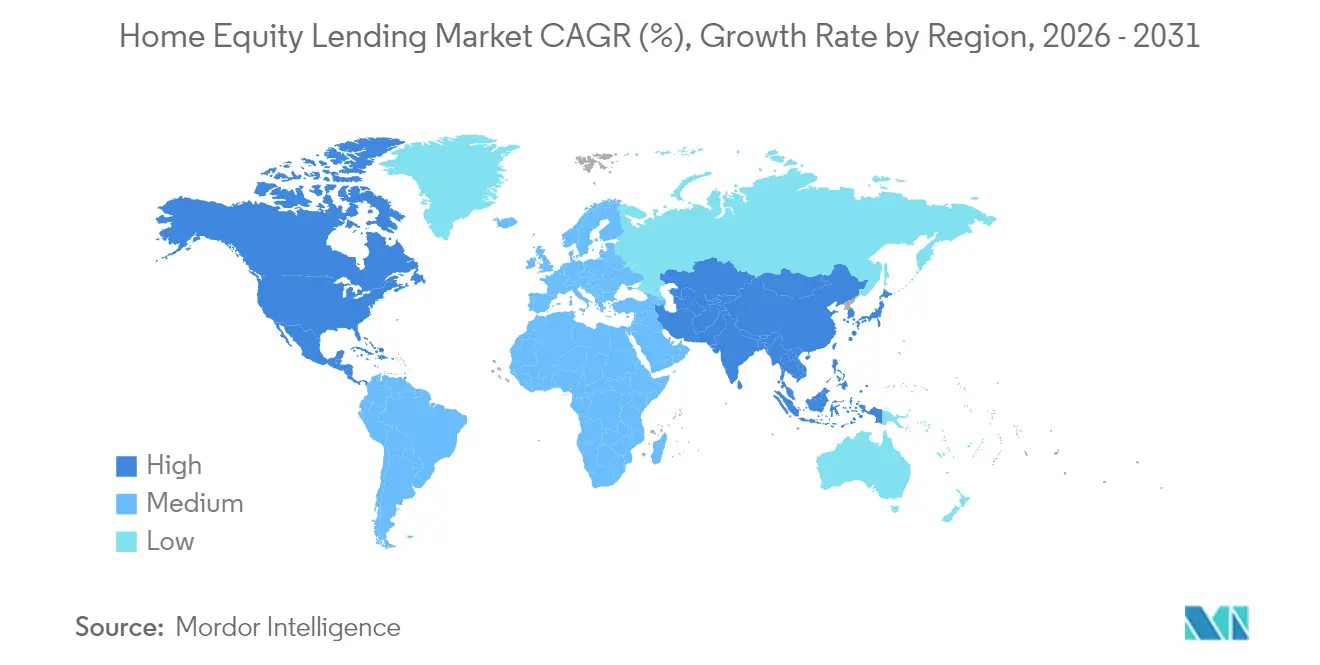

- By geography, North America commanded 63.05% share of the home equity lending market in 2025; Asia-Pacific is projected to widen at a 6.68% CAGR through 2031, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Equity Lending Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising home values expanding tappable equity | +1.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Digital lending platforms shortening approval times | +0.8% | Global, led by North America & Asia-Pacific | Medium term (2-4 years) |

| Favorable tax treatment of mortgage interest | +0.6% | North America, select European markets | Long term (≥ 4 years) |

| Embedded home-equity offers in fintech super-apps | +0.4% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Automated valuation models cutting costs | +0.7% | Global, early adoption in North America | Medium term (2-4 years) |

| Aging-housing-stock renovation boom | +0.5% | North America & Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Home Values Expanding Tappable Equity

Average tappable equity per U.S. homeowner closed 2024 at USD 203,000, a level that meaningfully lifts credit line ceilings without breaching 80% loan-to-value caps. Secondary metro areas, from Boise to Raleigh, now mirror price gains once confined to coastal hubs, broadening the addressable borrower pool. Because delinquency risk on primary residences remains low, lenders treat equity-backed credit as a defensive asset even in cyclical downturns. Credit unions leverage proximity to members to keep balances seasonally sticky, while specialty servicers bundle seasoned loans into high-grade securitizations for yield-hungry investors. Regional valuation peaks, however, foreshadow tighter underwriting in overheated sub-markets.

Digital Lending Platforms Shortening Approval Times

Best-in-class fintechs now fund a HELOC in under five days versus the conventional 45-60 day cycle, largely through straight-through processing and remote e-notary notarization. Figure Technologies alone surpassed USD 12.5 billion in funding by deploying blockchain-based lien management that slices fulfillment expenses. AVMs appear in 75% of transactions, eliminating appraiser bottlenecks and letting lenders quote same-day offers [1]“AVM Adoption Accelerates,” First American, firstam.com. Traditional banks are counterpunching with omnichannel rollouts that migrate branch workflows to cloud-native cores. Regulators are pressing for algorithmic fairness audits, adding cost but also erecting compliance barriers that favor scaled platforms.

Favorable Tax Treatment of Mortgage Interest

In the United States, interest linked to home-improvement HELOC draws remains deductible, lowering real borrowing costs by as much as 300 basis points for taxpayers in the top bracket. Similar allowances in Canada, the U.K., and the Netherlands cement home equity credit as a cheaper alternative to unsecured personal loans. Marketing campaigns highlight after-tax savings to affluent urban homeowners, a segment that also tends to pre-pay quickly, improving credit performance. Policy risk lingers, changes to deductibility could temper high-ticket renovation spending, so lenders are scenario-planning for margin compression.

Embedded Home-Equity Offers Inside Fintech Super-Apps

Embedded Home-Equity Offers inside fintech super-apps are becoming a powerful driver for the home equity lending market by integrating borrowing seamlessly into users’ everyday financial activities. Asian super-apps now surface real-time equity dashboards alongside payments, brokerage, and insurance, turning dormant home value into a one-tap liquidity option. Valley Strong Credit Union’s tie-up with Figure embeds a draw button directly in its app interface, nudging member engagement. Acquisition costs shrink when offers originate from an existing ecosystem, and younger borrowers show greater comfort pledging collateral digitally. These platforms reduce friction, personalize offers based on transaction behavior, and enable instant pre-approvals using embedded KYC and credit data. However, jurisdictional consumer-protection rules complicate roll-outs beyond core markets, requiring tailored compliance layers and partnerships with local entities.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising short-term interest rates elevating HELOC APRs | -0.9% | Global, most pronounced in North America | Short term (≤ 2 years) |

| Stagnant wage growth limiting debt-service capacity | -0.6% | Emerging markets, spill-over to developed economies | Medium term (2-4 years) |

| Data-privacy rules constraining alternative-data underwriting | -0.3% | Europe & North America, expanding globally | Long term (≥ 4 years) |

| Stricter post-crisis LTV caps limiting equity extraction | -0.4% | Global, varying by regulatory jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Short-Term Interest Rates Elevating HELOC APRs

Prime-linked HELOCs climbed above 7.5% in early 2025, curbing draw volumes as rate-sensitive borrowers await monetary easing[2]Brook Lea, “HELOC Rates Continue to Rise,” National Mortgage News, nationalmortgagenews.com. The rising cost of borrowing has made many consumers hesitant to tap into their home equity, especially for discretionary spending or non-essential renovations. Fixed-rate equity loans cushion some fallout, and lenders are piloting 5/1 hybrid structures that swap to adjustable after an introductory period. Credit unions face earnings volatility because many keep HELOCs on the balance sheet at variable coupons. This rate environment also dampens lender appetite for aggressive marketing, as elevated APRs reduce competitiveness against unsecured alternatives and fintech-driven BNPL products.

Stagnant Wage Growth Limiting Debt-Service Capacity in EMs

Stagnant wage growth is constraining debt-service capacity in emerging markets, acting as a significant restraint on home equity lending. Emerging-market households encounter debt-to-income ceilings even as property prices sprint ahead, suppressing origination potential in Brazil, Mexico, and parts of Southeast Asia. Gig-economy income volatility forces lenders to adopt cash-flow analytics over payslip reviews, but prudential regulators often lag these innovations, prolonging approval cycles. As a result, even creditworthy borrowers struggle to qualify for equity-backed credit under traditional underwriting models. Inflation-adjusted incomes have failed to keep pace with rising debt burdens, tightening affordability metrics. Additionally, lenders remain cautious amid uncertain macroeconomic conditions, further limiting product innovation and rollout in lower-income segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: HELOCs Dominate Through Flexibility

HELOCs held 67.10% of the home equity lending market share in 2025, a lead expected to widen as the segment advances at a 6.08% CAGR through 2031. Fixed-rate loans occupy a defensive niche among borrowers seeking payment certainty for renovation or debt-consolidation projects. The home equity lending market size attributed to HELOCs is forecast to reach USD 311.6 billion by 2031, equal to 68.00% of total originations. Credit unions reported November 2024 balances up 1.4% for closed-end equity loans and 2.6% for adjustable-rate mortgages, underscoring ongoing appetite.

Lenders are experimenting with combo products that lock an initial tranche at fixed terms while leaving a revolving line open for future draws. Marketing spotlights interest-only payment options that smooth household cash flow during renovation phases. Regulatory letters from the NCUA in late 2024 recommend tougher payment-shock stress tests, prompting portfolio managers to raise FICO and CLTV overlays on high-debt borrowers. Competitive momentum nevertheless favors HELOCs because their flexible advance feature matches today’s episodic funding needs—tuition, solar installations, and medical expenses—more cleanly than lump-sum alternatives.

By Provider: Banks Lead While Fintechs Accelerate

Banks commanded 58.05% of market share in 2025, but independent mortgage firms expanded their footprint in the small-balance lending segment, rising to 53% of loans under USD 100,000 from 50% two years earlier, while large banks slipped to just 15%. This shift signals growing borrower preference for faster, more flexible underwriting typically offered by nonbank lenders. Fintechs are exploiting cloud-native cores to post an 8.34% CAGR through 2031, edging their combined share toward one-quarter of the market. They leverage real-time income verification, mobile-first interfaces, and embedded analytics to streamline approvals. The home equity lending industry benefits when regulated banks co-opt fintech rails via white-label partnerships, enabling deposit-funded cost of capital with front-end speed parity. These alliances allow traditional players to stay competitive without rebuilding core systems, while fintechs gain regulatory cover and liquidity access through bank charters.

Portfolio economics differ sharply: depositories often retain servicing to deepen customer primacy, creating long-term cross-sell opportunities across mortgage, deposit, and investment products. This relationship-centric model helps banks maintain stickier funding bases and customer loyalty. In contrast, nonbanks typically monetize via forward bulk sales or securitization, prioritizing liquidity and asset turnover. FDIC research highlights systemic monitoring gaps in the nonbank segment, flagging liquidity-backed warehouse lines as a potential contagion vector during credit tightening. These exposures may amplify funding stress if interest rates spike or investor appetite wanes. Meanwhile, community banks cluster around branch-based cross-sell, bundling HELOCs with high-yield checking and wealth management to hold locally originated paper. Their strength lies in personalized service and geographic knowledge, though digital adoption remains uneven across this segment.

By Mode: Digital Transformation Accelerates

Offline engagements accounted for 71.45% of market share in 2025, reflecting document complexity, borrower caution, and legacy regulatory workflows. Many transactions still require notarization, in-person appraisals, or paper-based disclosures that slow full digital migration. However, click-to-close platforms are expanding volume at a 8.55% annual clip, driven by advances in e-signature compliance, remote ID verification, and lender appetite for operational efficiency. Borrowers aged 35 and under initiate 62% of applications digitally, reflecting their digital comfort and preference for speed, while the 55+ cohort remains the majority in-branch due to trust, familiarity, or limited digital access. This demographic split is prompting lenders to adopt segmented strategies, with tailored user experiences across age groups and property types.

Platform providers are baking analytics into the workflow—Arc Home’s HomeEQ portal lets brokers keep the servicing relationship while automating verifications and lien management, enabling faster turnaround without compromising loan quality. These platforms also allow lenders to flag documentation inconsistencies in real-time, reducing rework and improving compliance readiness. Compliance frictions persist around “know-your-customer” rules that mandate in-person ID confirmation above certain draw thresholds, especially in jurisdictions with tighter anti-fraud regulations. This adds operational friction, particularly for high-value HELOCs or multi-party ownership structures. Winning lenders therefore adopt omni-channel orchestration: a borrower may start online, upload income documents via smartphone, but finalize closing at a title office to satisfy notarization law. This blended model balances digital speed with regulatory assurance, enabling scale without sacrificing risk controls or borrower trust.

Geography Analysis

North America’s 63.05% grip in 2025 stems from codified lien laws, tax deductibility, and homeowners sitting on USD 32 trillion of aggregate equity. Canada’s reverse-mortgage niche is growing double-digits as aging owners monetize value without selling, with balances eclipsing CAD 7 billion (USD 5.5 billion) by 2025. Consolidation is reshaping scale economics: Rocket Companies now services 1 in 6 U.S. mortgages after absorbing Mr. Cooper in a USD 9.4 billion all-stock deal.

Asia-Pacific is the fastest-growing bloc at 6.68% CAGR, supported by regulatory easing in China, which lifted single-loan caps and extended tenors to seven years, and India, whose housing finance pool is projected to balloon significantly within five years. Japan’s major city banks are rolling out yen-denominated HELOCs pegged to the Tokyo Interbank Offered Rate, tapping households with sizeable unrealized gains from decades of urban appreciation. Yet slower wage growth tempers leverage expansion, prompting lenders to pilot income-share structures that synchronize repayment with earnings.

Europe, South America, and the Middle East & Africa represent a relatively limited market share but deliver important portfolio diversification. Euro-area mortgage growth sagged to a decade low in 2024 as the ECB tightened, though consultancies expect a 2025 rebound once rates stabilize. Brazil’s mortgage-to-GDP ratio climbed from 1.5% in 2003 to nearly 10% in 2018 but is leveling as real incomes flatten and underwriting standards strengthen. Gulf Cooperation Council markets are nibbling at equity-release pilots pegged to Sharia-compliant structures, with Dubai Islamic Bank rolling out a murabaha-based renovation facility.

Competitive Landscape

The market skews moderately concentrated. The top U.S. servicers control a considerable share of the market, but more than 250 originators jostle for regional and product niches. Rocket’s Mr. Cooper acquisition added USD 663 billion of servicing rights, vaulting its portfolio to USD 2.1 trillion. Wells Fargo keeps shares through cross-selling into its 68 million retail customers, revealing a 47% jump in Q4 2024 net income amid a pivot toward relationship-driven originations. Figure Technologies became the nation’s largest nonbank HELOC source, tallying USD 12.5 billion funded at sub-50-basis-point fulfillment cost.

Strategic archetypes bifurcate between scale aggregators and tech disruptors. Consolidators target servicing float, funding acquisitions via stock, while driving IT synergies that strip duplicate platforms. Disruptors lean on instantaneous credit decision-making, blockchain lien recordation, and referral embeddedness in real-estate portals. The January 2025 CFPB guidance on equity contracts forces all players to refresh disclosures, arguably advantaging compliance-mature incumbents over thinly staffed startups.

White-space remains in underserved small-balance lending where unit economics favor nimble independents. Community institutions deploy high-touch advisory models that generate cross-product stickiness. Fintechs, by contrast, are beta-testing synthetic HELOC securitizations to recycle capital faster, a move that could both escalate secondary-market depth and draw regulatory gaze.

Home Equity Lending Industry Leaders

Bank of America Corporation

U.S Bank

PNC Financial Services

Truist Financial Corp.

Figure Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Rocket Companies agreed to acquire Redfin for USD 1.75 billion in stock, merging search, realty, and mortgage fulfillment into a single platform

- February 2025: Old Second Bancorp purchased Evergreen Bank Group for USD 197 million, lifting combined assets to USD 7.1 billion and deepening consumer-lending reach

- January 2025: The Consumer Financial Protection Bureau issued sweeping guidance on home equity contracts, reiterating Truth in Lending Act standards and releasing bilingual consumer advisories

- September 2024: ConnectOne Bancorp merged with The First of Long Island Corporation, forging a USD 14 billion-asset franchise concentrated in the New York metro

Global Home Equity Lending Market Report Scope

Home equity lending is a type of loan that allows the homeowner to borrow against the equity in their homes. The loan amount is provided on the basis of the difference between the home's current market value and the mortgage balance due in it.

The home equity lending market is segmented by types, by service providers, and by region. By type, the market is segmented into fixed-rate loans and home equity lines of credit. By service providers, the market is segmented into banks, online, credit unions, and others. By region, the market is segmented into North America, South America, Europe, Asia Pacific, Middle East and Africa. The report offers market sizes and forecasts for the home equity lending market in value (USD) for all the above segments.

By Product Type

| Fixed Rate Loans |

| Home Equity Line of Credit |

By Provider

| Banks |

| Credit Unions |

| Non-Banking Financial Institutions |

| Others (Fintech, Brokers, etc.) |

By Mode

| Online |

| Offline |

By Region

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Fixed Rate Loans | |

| Home Equity Line of Credit | ||

| By Provider | Banks | |

| Credit Unions | ||

| Non-Banking Financial Institutions | ||

| Others (Fintech, Brokers, etc.) | ||

| By Mode | Online | |

| Offline | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current home equity lending market size?

The home equity lending market size stood at USD 359.44 billion in 2026 and is projected to rise to USD 458.31 billion by 2031.

How fast is the home equity lending market growing?

The market is expanding at a 4.98% CAGR between 2026 and 2031, propelled by record homeowner equity and digital underwriting efficiencies.

Which product segment dominates the home equity lending market?

HELOCs dominate with 67.10% share in 2025 and an expected 6.08% CAGR through 2031.

Which region shows the fastest growth in home equity lending?

Asia-Pacific leads with a 6.68% CAGR outlook, underpinned by regulatory liberalization and a growing middle class.

Page last updated on: