Medical Plastics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

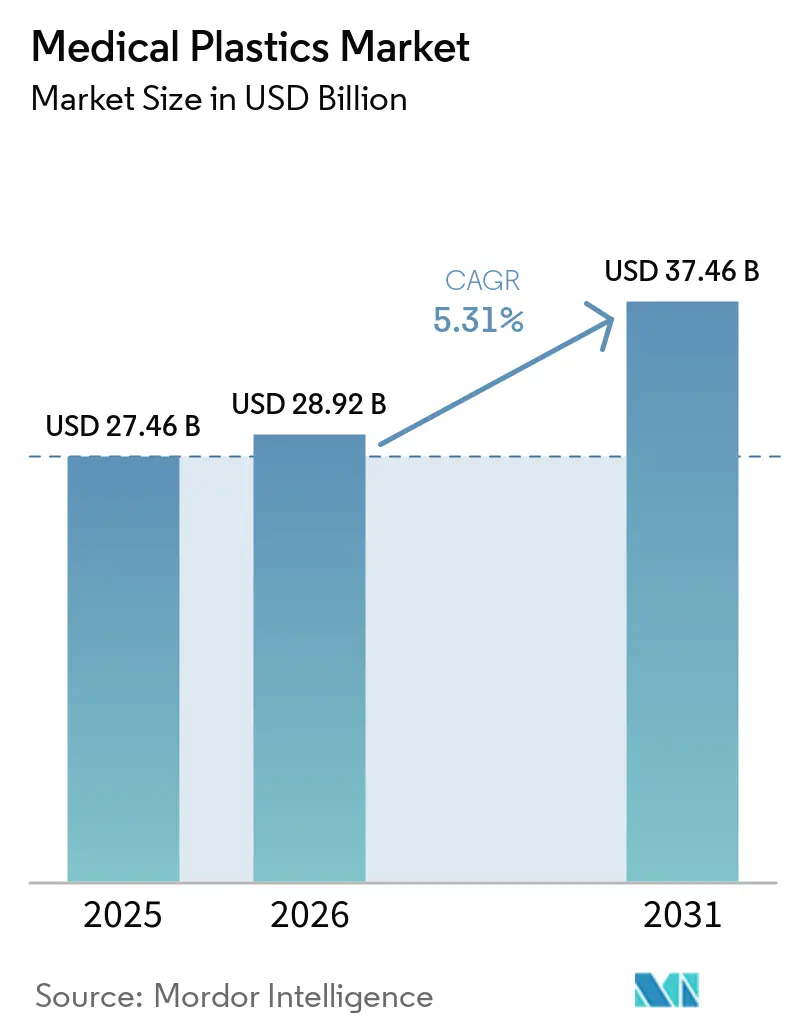

| Market Size (2026) | USD 28.92 Billion |

| Market Size (2031) | USD 37.46 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

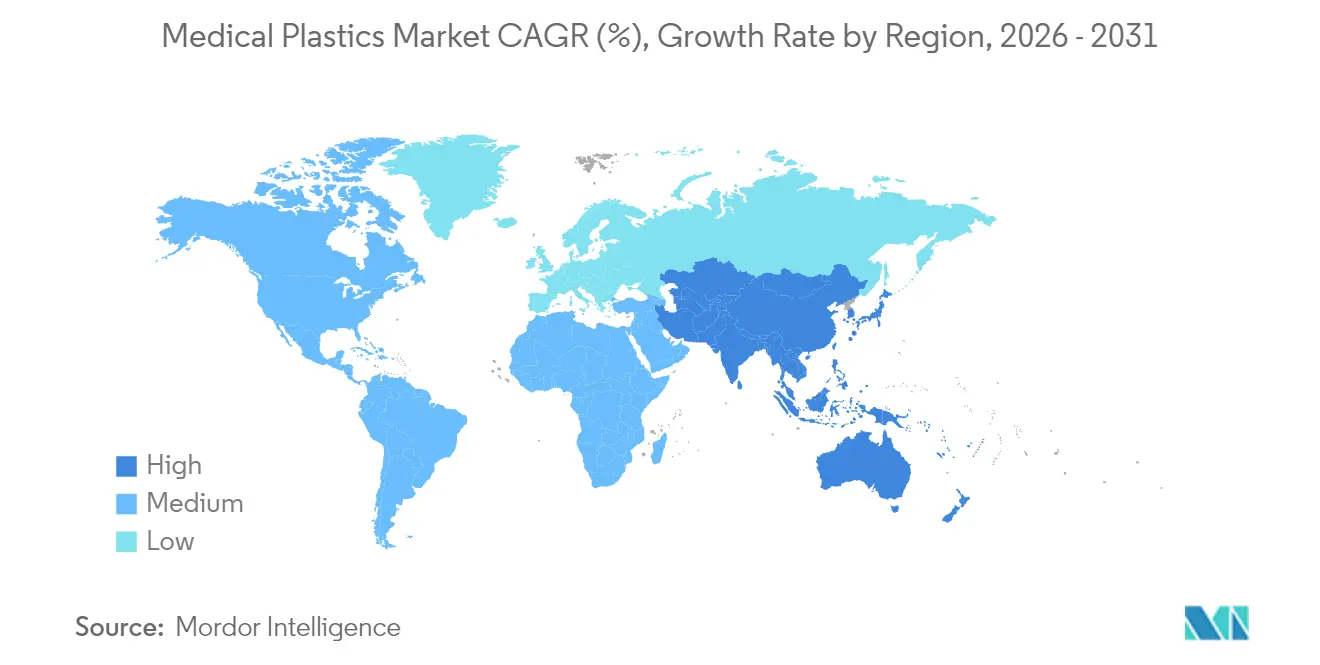

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Plastics Market Analysis by Mordor Intelligence

The Medical Plastics market size is expected to grow from USD 27.46 billion in 2025 to USD 28.92 billion in 2026 and is forecast to reach USD 37.46 billion by 2031 at 5.31% CAGR over 2026-2031. Softer outpatient models, rapid device miniaturization, and government-backed manufacturing incentives are raising demand for lightweight, sterile polymers across disposables, drug-delivery systems, and patient-specific implants. Polypropylene remains the workhorse thanks to its balanced cost-performance profile, while polyether-ether-ketone (PEEK) is scaling quickly in high-value implants because of its bone-like mechanical behavior. Injection molding keeps its lead for mass-volume precision parts, yet additive manufacturing is reshaping personalized care workflows. Asia-Pacific combines the largest installed capacity with the fastest consumption growth, driven by policy support in China and India and an expanding regional export hub for class II and class III devices.

Key Report Takeaways

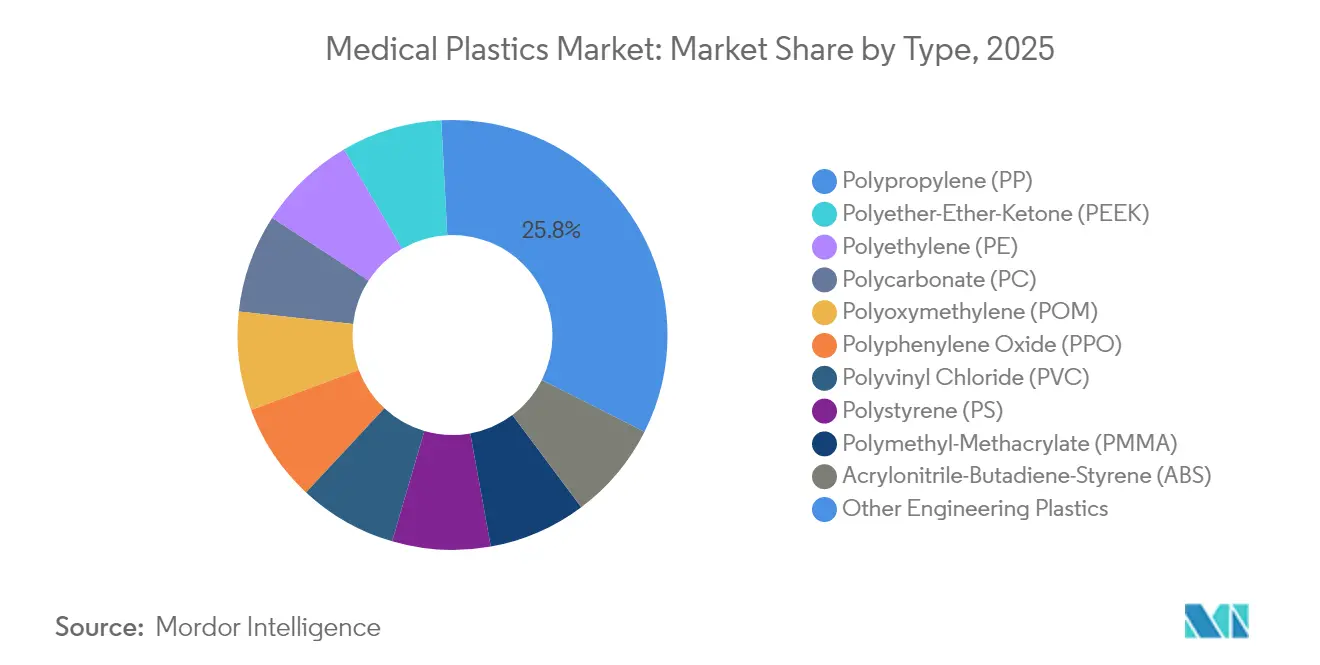

- By polymer type, polypropylene led with 25.83% revenue share in 2025, while PEEK is projected to expand at a 5.62% CAGR through 2031.

- By process, injection molding accounted for 42.35% of the medical plastics market share in 2025; 3-D printing records the strongest 5.58% CAGR to 2031.

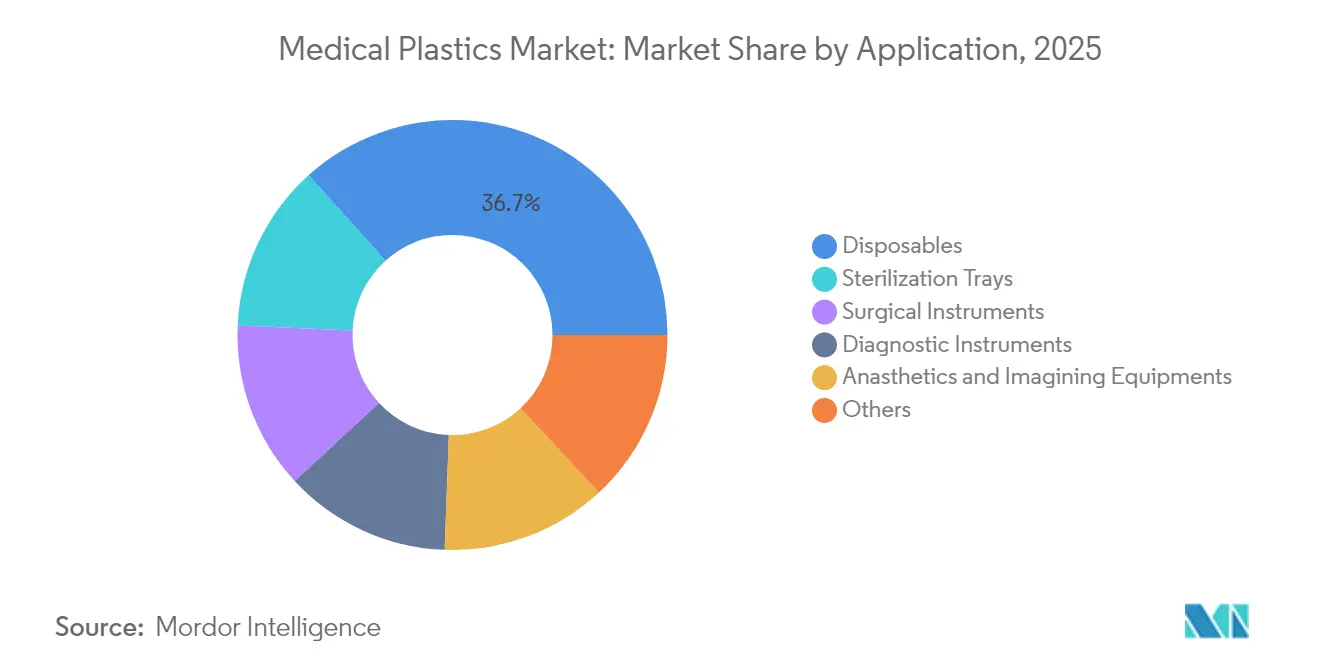

- By application, disposables captured 36.68% of the medical plastics market size in 2025, whereas the other applications bucket (drug-delivery devices and pharmaceutical packaging) advances at a 5.92% CAGR through 2031.

- By region, Asia-Pacific commanded 41.12% of the medical plastics in 2025 and is growing at 5.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Plastics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward home-based care | +1.2% | North America and Europe; spillover to Asia-Pacific | Medium term (2-4 years) |

| Miniaturized catheters and wearables | +0.8% | Global, highest relevance in North America and Europe | Medium term (2-4 years) |

| Asian domestic-manufacturing incentives | +1.3% | China, India, Japan | Short term (≤ 2 years) |

| 3-D-printed patient-specific implants | +0.9% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Growth of Connected Drug-Delivery Pumps | +0.7% | Global, with concentration in developed markets | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Shift toward Home-Based Care Requiring Lightweight Single-Use Devices

Healthcare delivery is moving from hospital wards to living rooms, urging designers to prioritize portability, intuitive interfaces, and strict infection control. Lightweight, single-use polypropylene, polycarbonate, and PEEK components tolerate steam, ethylene oxide, and radiation cycles while keeping weight low, a vital attribute for wearable pumps and point-of-care diagnostics. The PDA Miniverse Conference 2025 emphasized that home-care models also catalyze digital monitoring solutions, compelling polymers to protect sensitive sensors and batteries. Single-use product expansion answers infection-prevention protocols but makes waste management a parallel priority. Suppliers that can balance sterility, strength, and recyclability position themselves for long-term gains in the medical plastics market.

Miniaturization of Catheters and Wearables Elevating Demand for High-Purity Polycarbonate

Cardiovascular and neurovascular surgeons favor slimmer, more flexible catheters that navigate tortuous anatomy. High-purity polycarbonate, such as Covestro’s Makrolon, delivers transparency, dielectric strength, and dimensional stability, supporting catheter walls below 0.4 mm without compromising burst pressure. Wearable heart monitors increasingly embed optical sensors and micro-batteries; polycarbonate’s clarity and sterilization compatibility allow extended use in ambulatory settings. The resulting material pull-through strengthens the market across diagnostic and therapeutic devices alike.

Government Incentives for Domestic Medical-Device Manufacturing in Asia

Production-linked incentives worth INR 3,420 crore (USD 410 million) encourage Indian firms to localize syringe, catheter, and glove lines, directly fueling resin off-take[1]Department of Pharmaceuticals, “Boosting the Indian Medical Devices Industry,” Government of India, pharma-dept.gov.in. China’s ‘Made in China 2025’ blueprint tags high-end medical equipment as a priority, lifting polymer demand for imaging housings and dialysis disposables. Subsidized land, faster regulatory pathways, and expanded export credit insurance shorten time-to-market for local converters. These national programs translate into near-term volume spikes and long-term strategic depth, reinforcing Asia-Pacific’s outsized role in the medical plastics market.

Rapid Adoption of 3-D-Printed Patient-Specific Implants Accelerating PEEK Utilization

FDA clearance of the first 3-D-printed PEEK cranial implant in 2024 validated additive manufacturing for permanent implants. PEEK matches cortical bone modulus and is radiolucent, enabling clear post-operative imaging. Surgeons now combine CT data with lattice algorithms to print lightweight, porous geometries that foster osseointegration. Market adoption has crossed orthopedics into maxillofacial, spinal, and cardiovascular reconstructions, underpinning the fastest-growing polymer segment.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns over medical plastics | −0.9% | Global, peak intensity in Europe | Long term (≥ 4 years) |

| Limited recycling infrastructure | −0.7% | North America and Europe | Medium term (2-4 years) |

| Increasing Competition from Alternative Materials | -0.5% | Global, with early adoption in Europe | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Environmental Concerns Regarding Medical Plastics

Healthcare facilities generate 70% of sanitary waste by volume, mostly single-use plastics. The EU Single-Use Plastics Directive is already restricting certain polymer formats, while the U.S. Environmental Protection Agency aims to eliminate plastic leakage by 2040[2]U.S. Environmental Protection Agency, “National Strategy to Prevent Plastic Pollution,” epa.gov. These policies encourage material substitution, lower packaging weights, and drive audits of scope-3 emissions. Manufacturers that invest early in compostable resins, mono-material designs, and take-back schemes mitigate compliance risk, yet face margin pressure. Sustainability metrics will therefore shape procurement decisions and could temper traditional volume growth in the medical plastics market.

Limited Recycling Infrastructure for Medical-Grade Plastics Heightens Disposal Expenses

Only 9% of global plastic waste is recycled, and medical polymers add complexity through contamination and multi-layer formats. A B. Braun-led pilot diverted 18,000 lb of hospital plastics in eight months but highlighted cost, floor-space, and training gaps hprc.org. Research urges simultaneous improvements in product design, segregation protocols, and policy incentives to close the loop. Until infrastructure scales, disposal fees will keep rising and act as a headwind in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polypropylene Reigns, PEEK Gains Momentum

Polypropylene accounted for 25.83% of the medical plastics market share in 2025, anchored in syringes, IV bags, and catheter hubs that require chemical resistance and steam-autoclave tolerance. The material’s density of 0.9 g/cm³ supports lighter shipping loads, reinforcing its cost advantage. Polymer scientists are exploring catalytic depolymerization to transform spent PP masks into ECG electrodes, an initiative that could lower landfill volumes while adding value.

PEEK is projected to log a 5.62% CAGR to 2031, outpacing all other engineering resins. Demand stems from spinal cages, dental abutments, and cranial plates printed to patient CT data. The medical plastics market size for PEEK-based implants is poised to expand as material suppliers commercialize high-flow grades that shorten print cycles without sacrificing crystallinity. Radiolucency and modulus matching make PEEK attractive versus titanium, and emerging recycling programs for machining scraps enhance its sustainability profile.

By Process: Injection Molding Holds Scale While 3-D Printing Disrupts

Injection molding represented 42.35% of market share in 2025 by virtue of cycle-time efficiency and micron-level repeatability. Gas-assisted and thin-wall variants shave resin usage in connector bodies and ventilator housings. Computer vision and AI-driven cavity balancing further reduce scrap rates, a key cost driver in low-margin disposables. The medical plastics market size tied to injection molding thus remains resilient.

3D Printing captures less total volume today, yet is growing 5.58% annually, the fastest among processes. Stereolithography dominates dental aligners, where one million parts are printed daily. Powder-bed fusion of PEEK and bioresorbables is scaling into trauma plates and soft-tissue scaffolds. Hospitals adopting in-house printers shorten lead times from weeks to days, a value proposition that will push the medical plastics market toward mass customization.

By Application: Disposables Lead, Connected Drug-Delivery Advances

Disposables retained a 36.68% share in 2025 on the back of infection-control mandates and rising outpatient procedures. Syringe-in-barrel innovations, closed-loop catheter systems, and low-dead-volume connectors improve dose accuracy while reducing pathogen exposure. Yet these single-use volumes elevate waste-management scrutiny, compelling buyers to audit resin provenance and life-cycle impacts. Even so, the medical plastics industry continues to rely on disposables for frontline infection control.

The other-applications segment, which clusters drug-delivery devices and pharmaceutical packaging, will expand 5.92% per year through 2031. Digital dose-tracking pumps require optically clear, solvent-resistant housings that safeguard circuitry; transparent copolymer polycarbonates are emerging candidates. Demand for tamper-evident, high-barrier vials that preserve next-generation biologics adds further traction. These developments sustain growth momentum within the medical plastics market.

Geography Analysis

Asia-Pacific captured 41.12% of the market in 2025 and is forecast to widen its lead at a 5.76% CAGR. China’s export of medical devices to ASEAN hit USD 4.4 billion in 2023, a testament to regionalized supply chains. Japan contributes precision molding know-how that supports high-end diagnostic components. These dynamics position Asia as both a manufacturing hub and a consumption epicenter for the medical plastics market.

North America remains the innovation nucleus, especially for 3-D-printed implants and connected therapeutics. Stringent FDA class-II and class-III standards drive the adoption of resins with well-documented biocompatibility, and hospital construction trends favor modular outpatient clinics needing lightweight, recyclable fixtures.

Europe approaches the market through a sustainability prism. The Single-Use Plastics Directive pressures device makers to switch from styrenics to lower-impact copolymers or biodegradable alternatives. In Germany and the Netherlands, pilot recycling hubs are testing closed-loop programs for PET tracer vials and PVC masks. Academic-industry consortia funded under Horizon Europe add to the research pipeline that targets circular medical plastics market solutions. Meanwhile, South America and the Middle-East and Africa expand baseline healthcare infrastructure, prioritizing affordable disposables and basic diagnostic kits as entry points.

Competitive Landscape

The medical plastics market is highly fragmented, and hundreds of regional compounders serve niche sterilizable grades. Mid-tier specialists pursue market share through targeted certifications. Teknor Apex broadened its thermoplastic elastomer (TPE) portfolio for biopharmaceutical tubing in November 2024, offering low-extractable grades that withstand aggressive cleaning agents. Digital twins and AI-driven process controls further differentiate suppliers able to minimize scrap and speed validation. Collectively, these moves intensify competition yet also accelerate innovation within the medical plastics market.

Medical Plastics Industry Leaders

Celanese Corporation

Dow

DuPont

SABIC

Solvay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Teknor Apex expanded its medical-grade TPE line for biopharmaceutical tubing applications, targeting low-extractables performance.

- May 2024: Covestro has opened a new solvent-free polycarbonate copolymer plant in Antwerp, targeting applications in the electronics and healthcare sectors. The facility underscores the company’s commitment to sustainable, high-performance materials.

Global Medical Plastics Market Report Scope

The Medical Plastics market report includes:

| Traditional Plastics | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polystyrene (PS) | |

| Polyvinyl Chloride (PVC) | |

| Engineering Plastics | Acrylonitrile-Butadiene-Styrene (ABS) |

| Polycarbonate (PC) | |

| Polymethyl-Methacrylate (PMMA) | |

| Polyether-Ether-Ketone (PEEK) | |

| Polyoxymethylene (POM) | |

| Polyphenylene Oxide (PPO) | |

| Other Engineering Plastics |

| Injection Molding |

| Extrusion |

| Blow Molding |

| 3-D Printing / Additive Manufacturing |

| Others (Compression, Thermoforming) |

| Disposables |

| Sterilization Trays |

| Surgical Instruments |

| Diagnostic Instruments |

| Anasthetics and Imagining Equipments |

| Others (Drug-Delivery Devices, Pharmaceutical and Device Packaging) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacifc | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Traditional Plastics | Polyethylene (PE) |

| Polypropylene (PP) | ||

| Polystyrene (PS) | ||

| Polyvinyl Chloride (PVC) | ||

| Engineering Plastics | Acrylonitrile-Butadiene-Styrene (ABS) | |

| Polycarbonate (PC) | ||

| Polymethyl-Methacrylate (PMMA) | ||

| Polyether-Ether-Ketone (PEEK) | ||

| Polyoxymethylene (POM) | ||

| Polyphenylene Oxide (PPO) | ||

| Other Engineering Plastics | ||

| By Process | Injection Molding | |

| Extrusion | ||

| Blow Molding | ||

| 3-D Printing / Additive Manufacturing | ||

| Others (Compression, Thermoforming) | ||

| By Application | Disposables | |

| Sterilization Trays | ||

| Surgical Instruments | ||

| Diagnostic Instruments | ||

| Anasthetics and Imagining Equipments | ||

| Others (Drug-Delivery Devices, Pharmaceutical and Device Packaging) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacifc | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the global medical plastics market in 2026?

The market is valued at USD 28.92 billion in 2026.

How fast will the market grow through 2031?

It is projected to expand at a 5.31% CAGR, reaching USD 37.46 billion by 2031.

Which polymer holds the largest share of the market?

Polypropylene leads with 25.83% share because of its cost-effectiveness and versatility in single-use devices.

Which application category represents the biggest revenue contributor?

Disposables command 36.68% of global revenue, driven by strict infection-control protocols.

Which region dominates medical plastics demand today?

Asia-Pacific accounts for 41.12% of global consumption and also records the fastest 5.76% CAGR to 2031.

Page last updated on: