Blow Molded Containers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

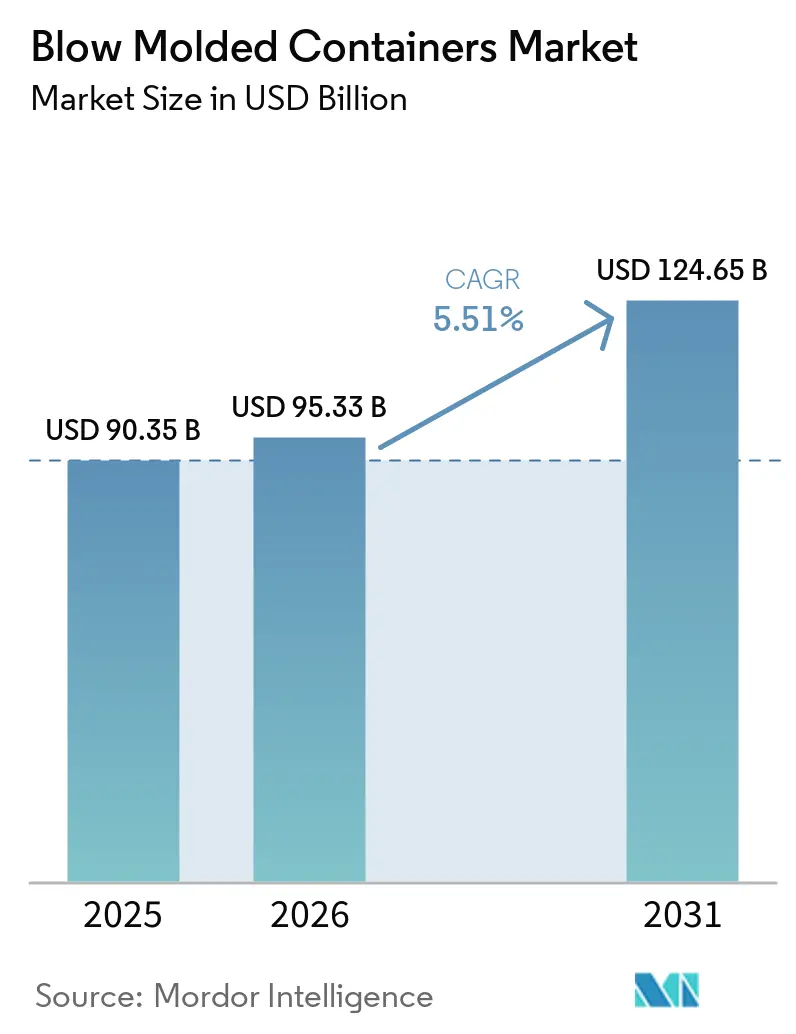

| Market Size (2026) | USD 95.33 Billion |

| Market Size (2031) | USD 124.65 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blow Molded Containers Market Analysis by Mordor Intelligence

The Blow Molded Containers Market size is projected to expand from USD 90.35 billion in 2025 and USD 95.33 billion in 2026 to USD 124.65 billion by 2031, registering a CAGR of 5.51% between 2026 to 2031. Brand owners are adopting recycled content to address rising Extended Producer Responsibility (EPR) fees. Plasma-coated polyethylene terephthalate (PET) is reducing the market share of glass in the premium beverages and pharmaceuticals industries. On-site, just-in-time blow molding is improving lead times, reducing inventory levels, and offering converters modular tooling flexibility. The requirements of e-commerce shipping are driving the development of stronger, appropriately-sized bottles capable of withstanding automated fulfillment processes. The Asia-Pacific region, with its significant concentration of petrochemical feedstock and integrated converter clusters, is well-positioned to capture these opportunities.

Key Report Takeaways

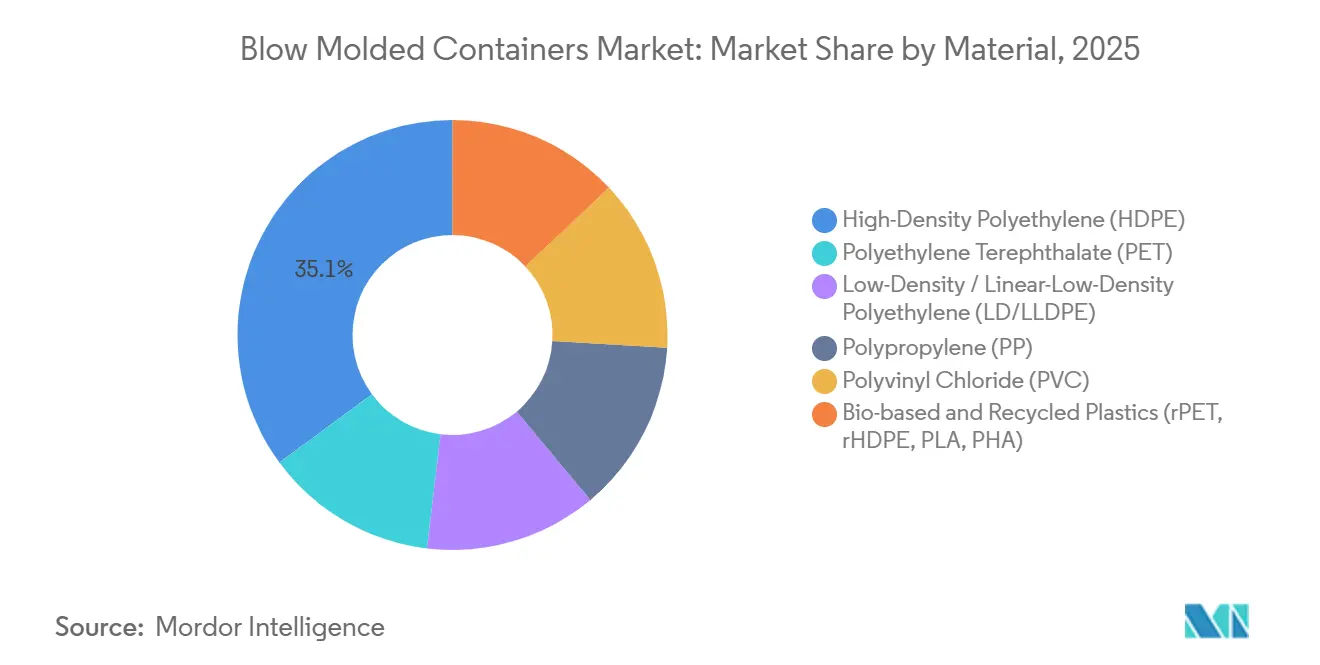

- By material, High-Density Polyethylene (HDPE) held 35.11% of blow molded containers market share in 2025, while bio-based and recycled plastics are advancing at a 5.64% CAGR through 2031.

- By container type, bottles led with 64.12% revenue share in 2025; specialty shapes posted the fastest 5.88% CAGR to 2031.

- By technology, extrusion blow molding commanded 46.68% of the blow molded containers market size in 2025, and stretch blow molding is growing at a 5.89% CAGR through 2031.

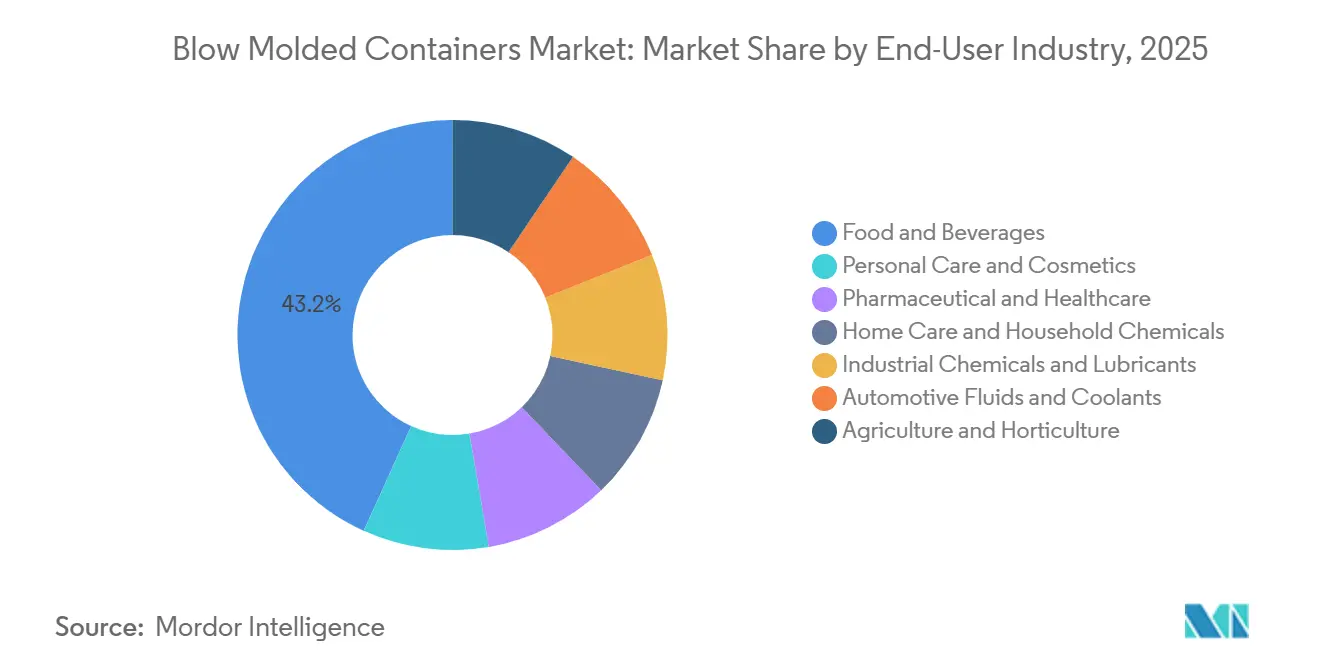

- By end-user industry, food and beverages captured 43.22% share in 2025, whereas pharmaceuticals and healthcare are expanding at a 6.12% CAGR to 2031.

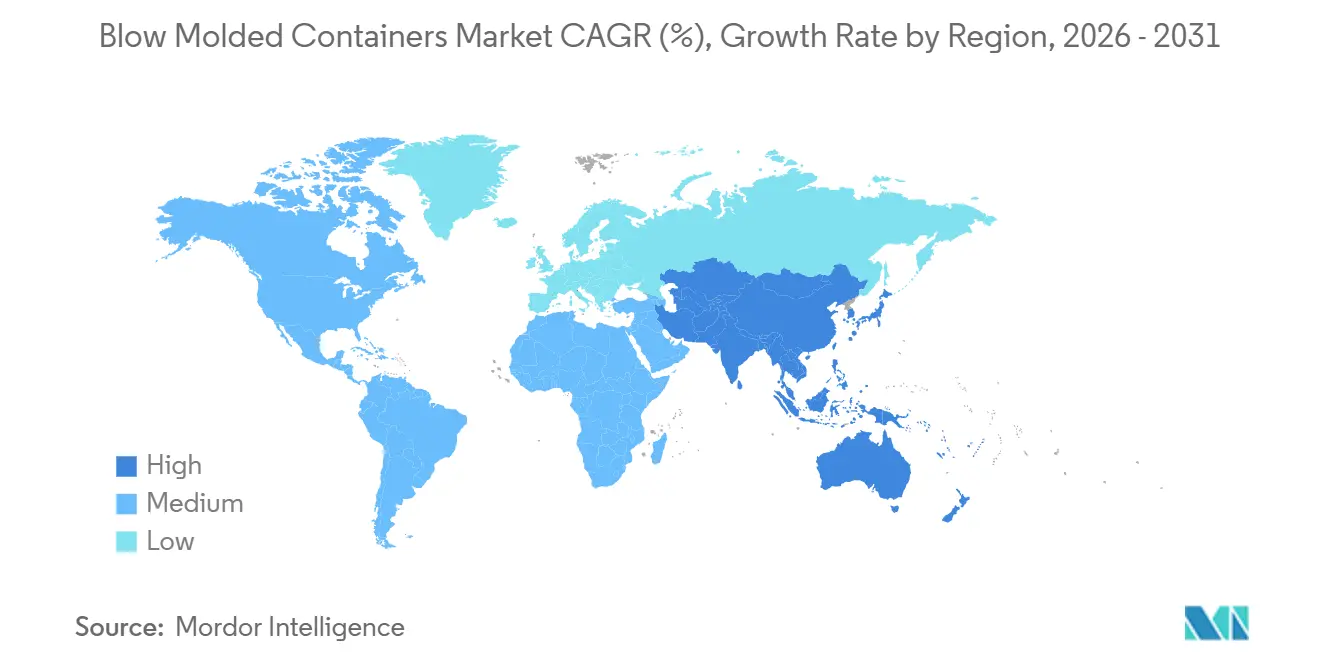

- By geography, Asia-Pacific accounted for 41.18% share in 2025 and is progressing at a 6.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blow Molded Containers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in single-serve and on-the-go beverages | +0.9% | Global, with concentration in North America, Western Europe, and urban APAC markets | Medium term (2-4 years) |

| E-commerce home-delivery logistics expansion | +0.7% | Global, led by North America and China; accelerating in India and Southeast Asia | Short term (≤ 2 years) |

| Brand shift to mono-material designs for recyclability | +1.1% | Europe and North America; emerging in APAC due to EPR adoption | Medium term (2-4 years) |

| Plasma-coated PET enabling glass-like barrier | +0.6% | Europe and North America premium beverage/pharma; pilot adoption in APAC | Long term (≥ 4 years) |

| On-site, just-in-time blow-molding at fillers | +0.8% | North America and Europe; early trials in Brazil and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Single-Serve and On-the-Go Beverages

Unit-dose formats are expanding in both beverage and pharmaceutical stock-keeping units (SKUs), with a preference for lightweight polyethylene terephthalate (PET) bottles under 500 milliliters. Manufacturers using modular tooling systems are addressing the increasing complexity of SKUs without incurring inventory challenges. For example, FlexBlow platforms enable mold changes in less than five minutes, improving operational efficiency[1]FlexBlow, “Modular On-Site Systems,” flexblow.com . Closure designs are also evolving, with developments such as flip-top sports caps and built-in straws shifting value emphasis from bottle bodies to neck finishes, enhancing functionality and convenience.

E-commerce Home-Delivery Logistics Expansion

Automated fulfillment centers are introducing higher drop heights and vibration profiles, leading to the adoption of ribbed sidewalls and reinforced bases. These design changes increase resin usage by 8-12% but help prevent damage claims, ensuring product integrity during transit. Additionally, European Union (EU) regulations penalizing empty space within parcels are driving brands to adopt right-sized geometries that optimize the use of shipping cartons efficiently, reducing shipping costs and improving sustainability[2]European Parliament, “New EU Rules on Packaging and Packaging Waste,” europarl.europa.eu.

Brand Shift to Mono-Material Designs for Recyclability

The Association of Plastic Recyclers revised its certification criteria in 2025, restricting polyethylene terephthalate (PET) bottle certification to designs with labels that detach in wash tanks. This revision made 22% of European stock-keeping units (SKUs) non-compliant. In response, companies such as Amcor met their target of 100% recyclable packaging in 2025, resulting in a shift from adhesive labels to in-mold or direct printing solutions. These changes were introduced to improve recyclability and align with evolving regulatory requirements.

Plasma-Coated PET Enabling Glass-Like Barrier

KHS Plasmax technology applies a 50-nanometer silicon oxide (SiOx) barrier, reducing oxygen ingress by 95% and extending the shelf life of sensitive liquids to 18 months. The pharmaceutical industry is increasingly adopting this technology, transitioning biologics from glass vials to plasma-coated PET bottles. This shift eliminates breakage risks during cold-chain logistics and enhances the durability of packaging for sensitive products.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | -0.5% | Global, with acute exposure in import-dependent regions (Europe, Japan, India) | Short term (≤ 2 years) |

| European Union PPWR 30% recycled-content mandate | -0.3% | Europe; indirect impact in export-oriented APAC and Latin America | Medium term (2-4 years) |

| Brand pilots of paper-based rigid packs | -0.2% | Europe and North America premium beverage/cosmetics; limited APAC penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Price Volatility

Polyethylene prices decreased by 15% year-on-year in early 2026; however, monthly fluctuations of 18-22% continue to impact converters operating under fixed-price sales agreements. Recycled Polyethylene Terephthalate (rPET) flake is priced at a 25-35% premium over virgin resin, as only 58% of collected Polyethylene Terephthalate (PET) in Europe qualifies for food-grade applications. This disparity in pricing is driven by the limited availability of food-grade rPET, which is further constrained by inefficiencies in the recycling process.

European Union PPWR 30% Recycled-Content Mandate

Converters are incurring additional costs of EUR 200-300 (USD 235.69-353.53) per ton for food-grade rPET to comply with the 2030 recycled-content mandate under the European Union Packaging and Packaging Waste Regulation (PPWR). Moreover, the use of colored PET and non-compatible labels leads to Extended Producer Responsibility (EPR) fees that are three to five times higher compared to clear mono-material bottles. These increased costs are compelling manufacturers to reassess their packaging strategies to align with regulatory requirements while managing financial implications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Grades Gain Despite HDPE’s Volume Lead

High-density polyethylene (HDPE) accounted for 35.11% of 2025 revenue, driven by its chemical resistance and impact durability, which are essential for packaging milk, detergents, and industrial chemicals. The blow-molded containers market linked to bio-based and recycled plastics is projected to grow at a compound annual growth rate (CAGR) of 5.64% through 2031, supported by environmental, social, and governance (ESG) initiatives from investors. TotalEnergies Corbion’s Luminy polylactic acid (PLA) reached a production capacity of 75,000 tons in 2025 to support bottled water pilot projects. While polyethylene terephthalate (PET) continues to dominate carbonated soft drink packaging with lightweight 15-gram 500-milliliter bottles, market saturation and the rise of refillable glass programs limit further growth. Recycled-content polyolefins are advancing in the value chain, with INEOS’s rPP1025C containing 70% recyclate while meeting the stiffness requirements for cosmetics-grade applications.

Polyvinyl chloride (PVC) is losing market share in Western Europe, dropping to single-digit levels due to concerns over phthalates. Polyhydroxyalkanoates (PHA), despite their marine biodegradability potential, remain constrained by production capacities below 5,000 tons. HDPE’s established presence in extrusion blow molding (EBM) provides some insulation against rapid displacement, but the competitiveness of HDPE will increasingly depend on recycled HDPE (rHDPE) blends and advancements in color-sorted separation systems as extended producer responsibility (EPR) fees become more stringent.

By Container Type: Specialty Shapes Outpace Commodity Bottles

Bottles accounted for 64.12% of 2025 revenue, but specialty shapes, such as handleware jugs, dual-chamber dispensers, and airless pumps, are expected to grow at a faster CAGR of 5.88%. Greif’s dual-compartment canisters, which separate reactive adhesives until use, extend shelf life by four times. Airless polyethylene terephthalate (PET) containers preserve the potency of vitamin-C serums by preventing oxygen ingress, enabling premium pricing in the skincare market. Graham Packaging’s AccuStrength software reduces handleware gram weights by 11-15%, saving 8,000-10,000 tons of HDPE annually across North America.

Jars and pots are transitioning from injection-molded polypropylene (PP) to extrusion-blown HDPE, which allows for faster tool changes. Meanwhile, drums and intermediate bulk containers (IBCs) are consolidating around United Nations (UN)-certified formats. As bottles increasingly become recyclable commodities, innovations in dispensing mechanisms and ergonomic designs are emerging as key differentiators to maintain brand margins.

By Technology: Stretch Blow Molding Leads Efficiency Race

Extrusion blow molding held a 46.68% market share in 2025. However, stretch blow molding is projected to grow at a CAGR of 5.89% through 2031, driven by efficiency improvements such as SIPA’s Xtreme Syncro, which reduces energy consumption by 10% and increases throughput by 15%. Krones’ Contiform reclaim loops cut blowing air usage by 30%, resulting in cost savings of EUR 0.012 (USD 0.014) per bottle. Injection blow molding, while holding a single-digit market share, remains critical for applications requiring high precision, such as pharmaceutical vials, where dimensional tolerances of ±0.1 millimeters are essential.

By End-User Industry: Pharma Outpaces Food & Beverage

The food and beverage industry accounted for 43.22% of the 2025 demand. However, the pharmaceutical and healthcare segment is expected to grow at a CAGR of 6.12%, driven by serialization requirements that necessitate tamper-evident packaging formats. Beauty brands are experimenting with refillable outer shells to reduce single-use packaging volumes, though the supporting infrastructure is still in its early stages. Industrial chemicals and lubricants continue to favor United Nations (UN)-marked jerry cans, particularly in Asia and the Middle East, where manufacturing activity is increasing and driving demand.

Geography Analysis

Asia-Pacific accounted for 41.18% of the projected 2025 revenue and is growing at a compound annual growth rate (CAGR) of 6.22%. China's integrated petrochemical clusters in Guangdong and Zhejiang improve raw material flow efficiency, while India's Drugs and Cosmetics Act mandates tamper-evident bottles across 10,000 drug manufacturing plants.

North America benefits from the adoption of on-site blow molding and USD 14 billion in reshored plastics investments since 2020. Logoplaste operates 62 embedded plants, reducing clients' carbon dioxide (CO₂) emissions by 12,000 tons annually. Europe faces challenges such as resin premiums and energy price volatility, but is investing in recycled polyethylene terephthalate (rPET) production lines to meet Packaging and Packaging Waste Regulation (PPWR) recycled-content requirements. In the Middle East and Africa, new installations, including Asepto's USD 126 million aseptic line in Egypt, position the region as a potential export hub for the Commonwealth of Independent States (CIS) and Sub-Saharan markets.

Deposit-return schemes in Germany and Scandinavia support polyethylene terephthalate (PET) collection; however, rPET shortfalls persist at 0.7 million tons annually, necessitating imports from Turkey and Saudi Arabia. These feedstock dynamics reinforce Asia-Pacific's cost advantage and sustain its significant share in the blow molded containers market.

Competitive Landscape

The blow molded containers market is moderately fragmented. Logoplaste’s wall-to-wall model, implemented at customer sites, eliminates the need for secondary packaging and has resulted in a threefold increase in its North American revenue since 2021. Greif generated USD 1.8 billion in containerboard sales in 2025, redirecting its focus to 68 polymer plants and targeting USD 120 million in cost savings by fiscal 2026.

Technological advancements are critical. SIPA’s Xtreme Syncro enables converters to reduce costs by EUR 0.015 per bottle while maintaining profit margins. Similarly, Krones’ artificial intelligence (AI)-driven Contiform technology has reduced scrap rates to 0.5%, cutting costs by EUR 0.01 (USD 0.01) per unit. Smaller converters that lack the financial capacity to invest in such upgrades are experiencing margin pressures and industry consolidation. This trend is highlighted by Pretium Packaging’s USD 900 million debt restructuring and a USD 50 million equity infusion in 2026.

Emerging opportunities include refillable outer-shell systems, plasma-coated polyethylene terephthalate (PET) for oxygen-sensitive liquids, and bio-based polymers designed to address coastal single-use plastic bans. Achieving success in these areas will depend on securing a reliable supply of recycled polyethylene terephthalate (rPET) and optimizing energy-efficient stretch blow molding processes.

Blow Molded Containers Industry Leaders

ALPLA

Plastipak Holdings, Inc.

Graham Packaging

Amcor plc

Silgan Plastics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: INEOS has introduced rPP1025C, a polypropylene (PP) grade containing 70% recycled content, specifically developed for applications such as blow-molded containers, including cosmetics jars and caps. The product has received approvals from the United States Food and Drug Administration (FDA) and RecyClass, ensuring compliance with safety and recycling standards.

- October 2024: Asepto invested USD 126 million in an aseptic packaging plant in Egypt, with a target production capacity of 12 billion packs annually. This investment is expected to support the growing demand for blow-molded containers, which are widely used in the packaging of liquid products across Africa, Europe, and the Middle East.

Global Blow Molded Containers Market Report Scope

Blow molded containers are hollow plastic products, including bottles, jugs, and tanks, produced by inflating heated, molten plastic inside a closed mold using high-pressure air. This process, commonly utilizing materials such as High-Density Polyethylene (HDPE), Polyethylene Terephthalate (PET), or Polypropylene (PP), facilitates the production of lightweight, durable, and complex shapes.

The blow molded containers market is segmented by material, container type, technology, end-user industry, and geography. By material, the market is segmented into high-density polyethylene (HDPE), polyethylene terephthalate (PET), low-density/linear-low-density polyethylene (LD/LLDPE), polypropylene (PP), polyvinyl chloride (PVC), and bio-based and recycled plastics (rPET, rHDPE, PLA, PHA). By container type, the market is segmented into bottles, jars and pots, jerry cans and f-style containers, drums and intermediate bulk containers (IBCS), and specialty shapes (handleware, dual-chamber, etc.). By technology, the market is segmented into extrusion blow molding (EBM), injection blow molding (IBM), and stretch blow molding (SBM). By end-user industry, the market is segmented into food and beverages, personal care and cosmetics, pharmaceutical and healthcare, home care and household chemicals, industrial chemicals and lubricants, automotive fluids and coolants, and agriculture and horticulture. The report also covers the market size and forecasts for blow molded containers in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| High-Density Polyethylene (HDPE) |

| Polyethylene Terephthalate (PET) |

| Low-Density/Linear-Low-Density Polyethylene (LD/LLDPE) |

| Polypropylene (PP) |

| Polyvinyl Chloride (PVC) |

| Bio-based and Recycled Plastics (rPET, rHDPE, PLA, PHA) |

| Bottles |

| Jars and Pots |

| Jerry Cans and F-style Containers |

| Drums and Intermediate Bulk Containers (IBCs) |

| Specialty Shapes (Handleware, Dual-chamber, Etc.) |

| Extrusion Blow Molding (EBM) |

| Injection Blow Molding (IBM) |

| Stretch Blow Molding (SBM) |

| Food and Beverages |

| Personal Care and Cosmetics |

| Pharmaceutical and Healthcare |

| Home Care and Household Chemicals |

| Industrial Chemicals and Lubricants |

| Automotive Fluids and Coolants |

| Agriculture and Horticulture |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | High-Density Polyethylene (HDPE) | |

| Polyethylene Terephthalate (PET) | ||

| Low-Density/Linear-Low-Density Polyethylene (LD/LLDPE) | ||

| Polypropylene (PP) | ||

| Polyvinyl Chloride (PVC) | ||

| Bio-based and Recycled Plastics (rPET, rHDPE, PLA, PHA) | ||

| By Container Type | Bottles | |

| Jars and Pots | ||

| Jerry Cans and F-style Containers | ||

| Drums and Intermediate Bulk Containers (IBCs) | ||

| Specialty Shapes (Handleware, Dual-chamber, Etc.) | ||

| By Technology | Extrusion Blow Molding (EBM) | |

| Injection Blow Molding (IBM) | ||

| Stretch Blow Molding (SBM) | ||

| By End-User Industry | Food and Beverages | |

| Personal Care and Cosmetics | ||

| Pharmaceutical and Healthcare | ||

| Home Care and Household Chemicals | ||

| Industrial Chemicals and Lubricants | ||

| Automotive Fluids and Coolants | ||

| Agriculture and Horticulture | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Blow Molded Containers Market?

The Blow Molded Containers Market size is projected to expand from USD 90.35 billion in 2025 and USD 95.33 billion in 2026 to USD 124.65 billion by 2031, registering a CAGR of 5.51% between 2026 to 2031.

Which material currently leads global demand?

High-density polyethylene holds 35.11% revenue share due to chemical resistance and impact durability.

Which region is expanding fastest?

Asia-Pacific is growing at a 6.22% CAGR, supported by integrated petrochemical clusters and regulatory catch-up.

How are converters responding to EU recycled-content mandates?

They are locking multi-year rPET supply contracts and redesigning bottles as clear mono-material formats to avoid higher EPR fees.

Page last updated on: