PLC, SCADA, And DCS Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 464.90 Million |

| Market Size (2031) | USD 619.80 Million |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PLC, SCADA, And DCS Training Market Analysis by Mordor Intelligence

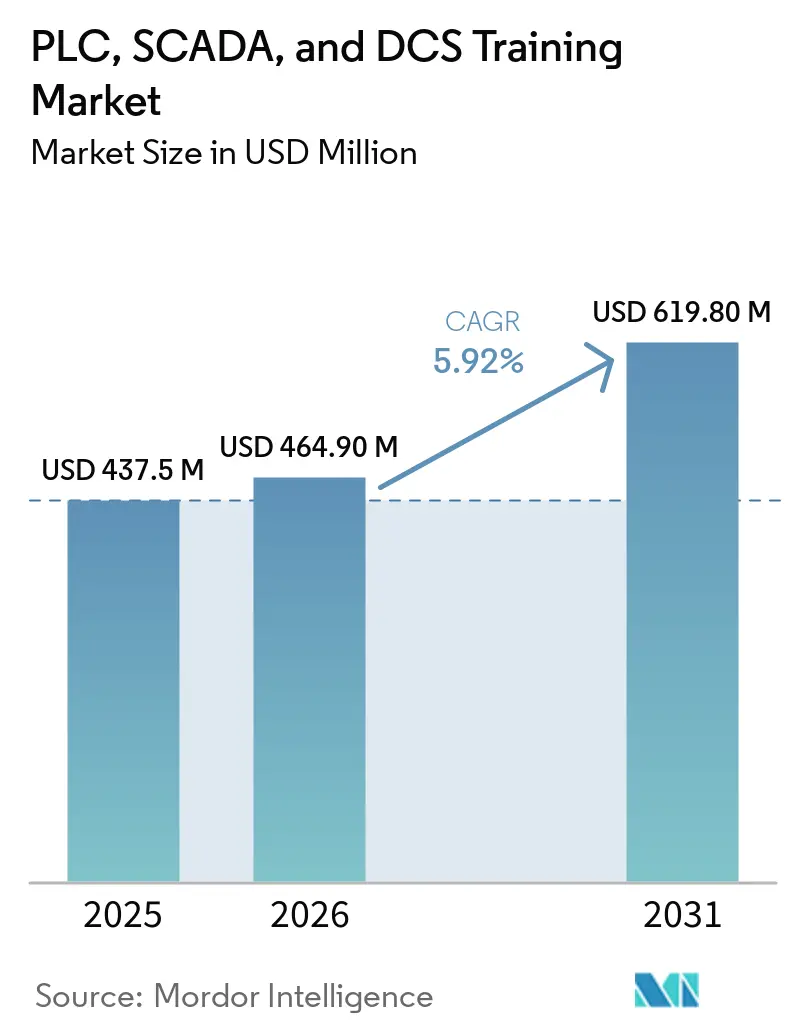

The PLC, SCADA, And DCS Training Market size is projected to expand from USD 437.5 million in 2025 and USD 464.90 million in 2026 to USD 619.80 million by 2031, registering a CAGR of 5.92% between 2026 to 2031.

A steady shift toward connected, cloud-ready control environments keeps demand firm for role-based training that blends control engineering, cybersecurity, and IT data skills. Employers continue to prefer formats that compress time-to-competency and lower time away from operations, which supports the rise of blended learning and virtual labs. Vendors are also linking credentials to support tiers and lifecycle services to anchor customer loyalty and ensure up-to-date skills as product releases evolve. Cybersecurity frameworks, especially IEC 62443, are shaping curricula content and assessment methods as plants harden OT assets. The PLC, SCADA, and DCS Training market is also influenced by brownfield modernization, where dual competency across legacy and current platforms is now a baseline expectation rather than an advanced skill.

Key Report Takeaways

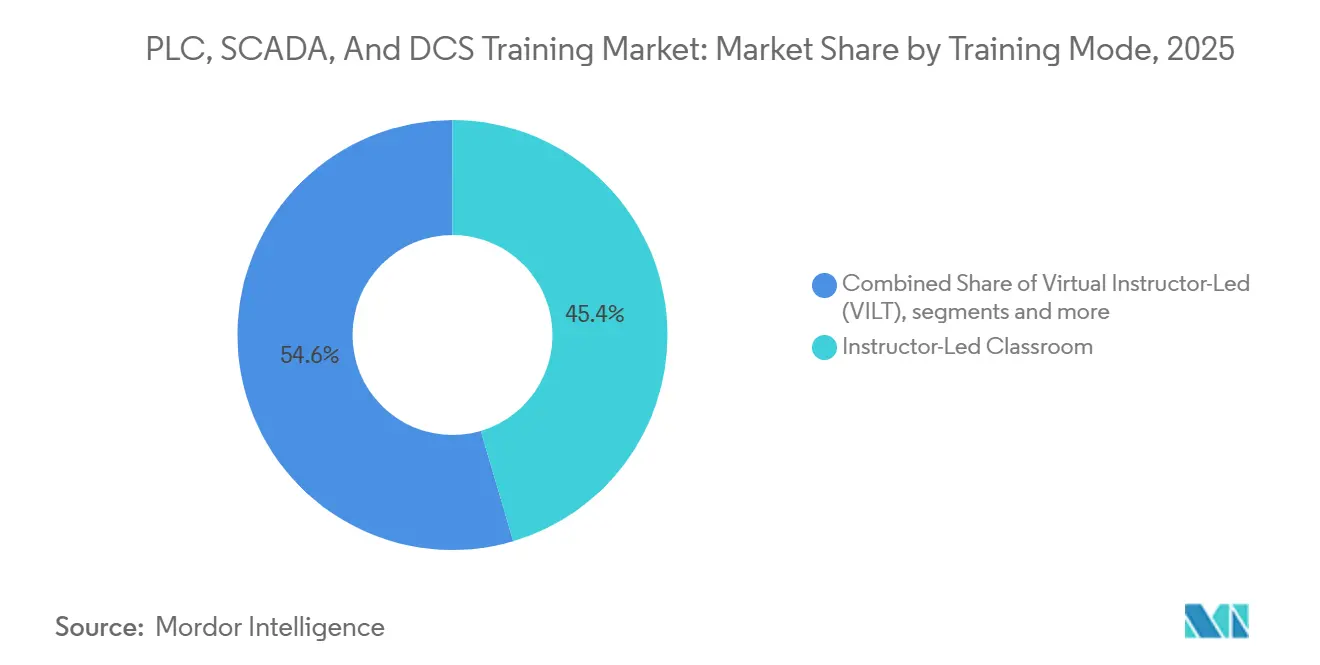

- By training mode, instructor-led classroom sessions held 45.44% of the PLC, SCADA, and DCS training market share in 2025, while blended learning is on track for an 11.64% CAGR through 2031.

- By system type, PLC training accounted for 54.35% of the PLC, SCADA, and DCS training market share in 2025, while SCADA training is projected to grow at a 10.38% CAGR between 2026 and 2031.

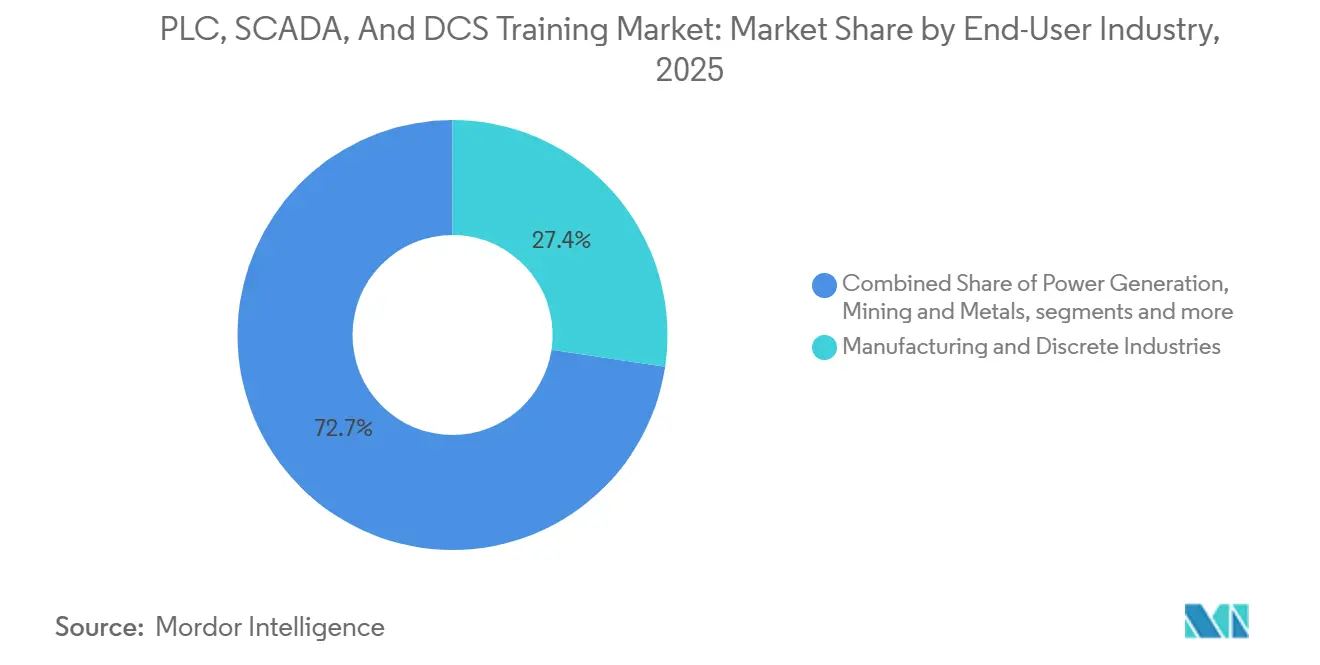

- By end-user industry, manufacturing and discrete accounted for 27.35% of the PLC, SCADA, and DCS training market share in 2025, while pharmaceuticals and life sciences are forecast to expand at 11.36% CAGR through 2031.

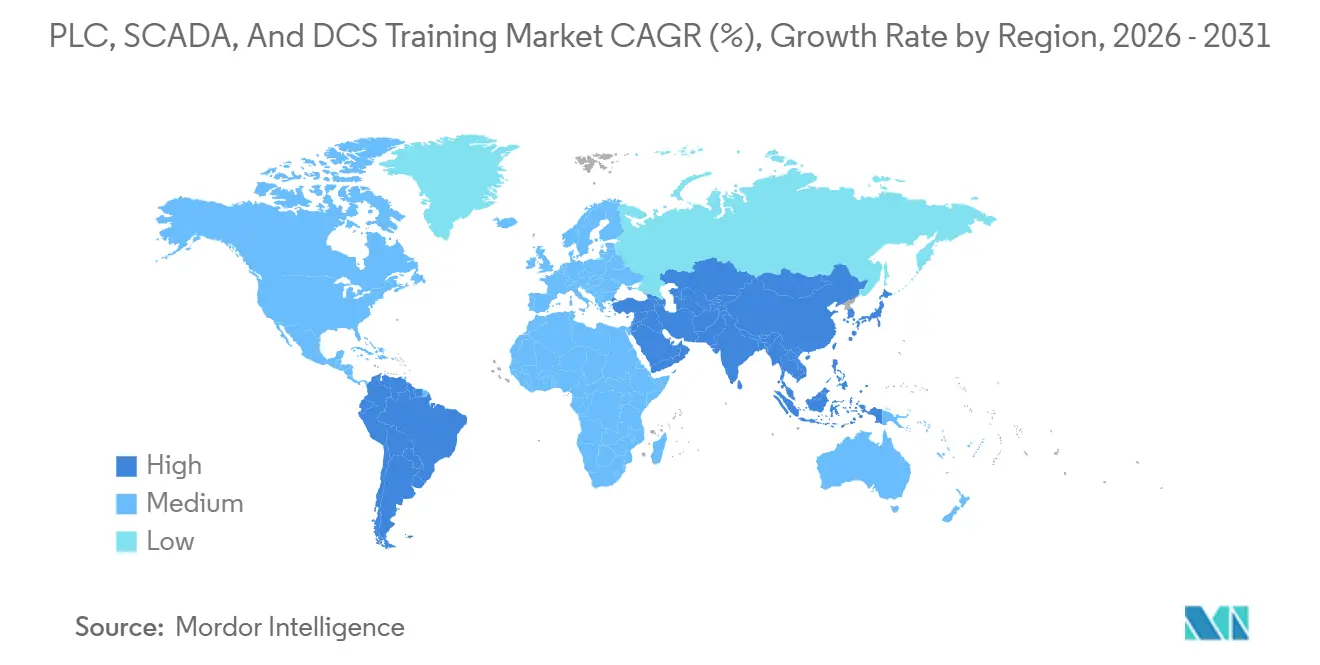

- By geography, Asia-Pacific accounted for 39.44% of the PLC, SCADA, and DCS training market share in 2025, while the Middle East and Africa are projected to advance at 12.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PLC, SCADA, And DCS Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brownfield migrations require retraining programs | +1.2% | Global, with a concentration in North America's legacy installations and European process industries | Medium term (2-4 years) |

| OEM certifications increasingly mandated globally | +0.9% | Global, spill-over to the Middle East & Africa, driven by Vision 2030 procurement standards | Long term (≥ 4 years) |

| Workforce shortages in industrial automation | +1.8% | North America core, acute in Cleveland, Southeast Wisconsin; spreading to Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Remote monitoring growth drives SCADA skills | +1.1% | Global, with early gains in oil and gas in the Middle East, utilities in Europe, and mining in Australia | Medium term (2-4 years) |

| IEC 62443 role-based training adoption | +0.8% | Europe and the Middle East lead, North America follows, and Asia-Pacific has nascent adoption in critical infrastructure | Medium term (2-4 years) |

| Digital twins embedded in training curricula | +1.0% | North America and Europe core, expanding to the Asia-Pacific semiconductor and automotive clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Brownfield Migrations Require Retraining Programs

Equipment owners are transitioning from aging PLC and DCS platforms to current integrated engineering environments, which require engineers to maintain fluency in both outgoing and incoming systems during staged cutovers to protect uptime. Training catalogs from major OEMs explicitly address migration tracks and role-based transition modules because greenfield-style onboarding does not cover dual-system competencies needed for brownfield projects[1]Siemens, “SITRAIN | Siemens,” Siemens, siemens.com. System integrators also flag a shortage of legacy-system expertise as senior personnel retire, heightening the need for structured retraining that can be validated during critical phases such as commissioning and start-up. OEM education services have expanded migration-focused courses and advanced transition labs so technicians can practice on emulated and current releases without production risk. Regional hiring data confirms that time-to-fill for technical roles extends commissioning timelines, which reinforces the case for retraining incumbent staff rather than relying on external hires. This dual-competency need now overlaps with cybersecurity and network segmentation practices, as migration projects often coincide with upgrades to segmented architectures and secure remote access. Structured migration learning paths with hands-on labs and post-assessment checkpoints are therefore becoming the norm for plants modernizing controls while operating at capacity.

OEM Certifications Increasingly Mandated Globally

Vendors have aligned customer support, warranty features, and software access with verified competency pathways, moving certification from a nice-to-have to a practical requirement for complex deployments. Rockwell ties role-based learning plans to validated proficiency and integrates Evaluate, Train, Practice, and Assess cycles so employers can track outcomes and align privileges to skill level[2]Rockwell Automation, “Competency Learning Plans,” Rockwell Automation, rockwellautomation.com. Honeywell structures multi-tier programs that combine classroom hours, supervised labs, and proctored exams to distinguish foundational knowledge from field-proven expertise. Security certifications are also normalizing across the ecosystem through ISASecure schemes that require secure development lifecycle evidence and system-level validation against IEC 62443, which then cascades into integrator and operator training plans. Siemens runs partner qualification and certification programs that help employers benchmark multi-level proficiency and align procurement with verifiable skill badges. As plants adopt more cloud-connected SCADA and more frequent release cycles, certification cycles are tightening to ensure teams remain current on platform features and secure configuration practices. The PLC, SCADA, and DCS Training market is therefore influenced by procurement policies that link vendor support tiers and project eligibility to staff credentials.

Workforce Shortages in Industrial Automation

Persistent shortages in automation technicians, PLC programmers, and controls engineers raise the premium on structured training that can compress ramp-up times and reduce vacancy-related project delays. Regional data shows extended vacancy durations for automation roles, prompting manufacturers to invest in internal upskilling programs rather than rely solely on external recruitment. Employers report that hybrid skill sets are the scarcest, such as personnel who can bridge legacy platforms and modern stacks, or who can operate at the intersection of controls and networks, which is harder to source from typical job markets. Engineering services companies highlight how fragmented toolchains, for example, multiple CAD and control environments, narrow the candidate pool and increase time-to-hire, which puts additional value on cross-platform training. The shortage also shifts training demand toward shorter cycles and modular formats that align with shift rotations, reducing travel overhead while still demonstrating competency through practical assessments. As automation spending expands into new geographies and sectors, these constraints spread beyond historical hubs, broadening the addressable base for standardized curricula tailored to local needs. The PLC, SCADA, and DCS Training market, therefore, grows in part because employers cannot scale modernization or reliability projects without parallel investment in human capital.

Remote Monitoring Growth Drives SCADA Skills

Training demand is shifting toward SCADA roles that require proficiency in IIoT connectivity, cloud aggregation, API-driven analytics, and secure remote operations. Course providers have introduced masterclasses centered on substation automation and remote monitoring that integrate security practices and real-time data analysis, reflecting the hybrid skill profile required on modern grids and distributed assets[3]Tonex, “Substation Automation and Remote Monitoring Masterclass,” Tonex, tonex.com. Vendors are standardizing training on topics such as VPN configuration, certificate handling, and dashboarding as SCADA architectures integrate enterprise IT patterns and remote workforce practices. Operator training also emphasizes cloud platforms for model management and scenario practice, enabling teams to collaborate from multiple sites without travel. Curricula now blend control fundamentals with hands-on labs in historical data extraction, time-series tooling, and KPI visualization, mirroring day-to-day workflows across distributed assets. This rebalancing strengthens the case for structured, multi-role learning paths that include configuration, operations, and security modules within the same program. As a result, the PLC, SCADA, and DCS Training market sees outsized growth in programs that enable secure, reliable remote operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Training budgets cyclic with CAPEX cycles | -0.7% | Global, acute during economic downturns in manufacturing-dependent regions | Short term (≤ 2 years) |

| High opportunity cost of downtime events | -0.5% | Global, most severe in continuous process industries with 24/7 operations | Short term (≤ 2 years) |

| Siloed vendor ecosystems hinder cross-training | -0.4% | Global, particularly pronounced in multi-vendor brownfield environments | Long term (≥ 4 years) |

| Credential inflation confuses employer signals | -0.3% | North America and Europe where competing certification bodies create complexity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Training Budgets Cyclic with CAPEX Cycles

Training demand expands during commissioning waves and slows when budgets rotate toward maintenance and lean operations, which can delay or narrow upskilling plans. Industry association research ties workforce gaps to productivity and downtime risks. Yet, many plants still defer training when capital plans tighten because course fees and travel compete with other spend categories[4]PMMI, “2025 Inside the Workforce Gap,” PMMI, pmmi.org. OEM catalogs show multi-day instructor-led courses and lab-based practicums that require time away from the plant, which increases the perceived cost during the budget cycle. Vendors are countering this with contractual mechanisms that pre-commit funds and match training allocations to stabilize investment across quarters. Employers also look to blended formats and virtual labs to reduce travel and shift coverage burdens while maintaining practical exercises. Persistent hiring gaps reinforce the logic of training during slowdowns to prepare for the next investment cycle. Still, not all firms have the governance or incentives to maintain steady investment in skills programs through the cycle.

High Opportunity Cost of Downtime Events

Unplanned downtime creates a constant risk that can disrupt scheduled training, draw staff out of courses, and reduce return on learning investments. Association analysis links skills shortages to production losses, which amplifies management hesitation to release operators for multi-day sessions when schedules are tight. Vendors are addressing this with training environments that allow compressed scenario-based exercises, including instructor-configurable malfunction cases with performance tracking that fit within shift rotations. Offshore and remote operations face additional constraints in travel and logistics, which is leading to in-situ immersive offerings that reduce physical movement while preserving skills validation. When failures occur during training windows, overtime, and contractor rates, these indirect costs further complicate program scheduling and budgets. Short-course certificates and modular programs mitigate disruption risk by sequencing content into shorter blocks that can be completed between planned outages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Training Mode: Blended Learning Emerges as Preferred Enterprise Format

Instructor-led classroom training accounted for 45.44% of 2025 revenue, while blended learning is projected to grow at a 11.64% CAGR through 2031 as employers balance hands-on labs with flexible online instruction. The PLC, SCADA, and DCS Training market benefits from blended tracks that reduce time away from production while preserving practical skills that require supervised exercises. OEMs and academies have formalized blended structures that pair self-paced modules with instructor-led labs, so learners arrive prepared for hands-on tasks, reducing overall seat time without sacrificing outcomes. Training teams have emphasized completion and satisfaction data as they scale blended modalities for large cohorts and distributed workforces, which supports enterprise buy-in for repeat cohorts. Virtual instructor-led training using cloud-hosted control environments gives participants access to emulated controllers and engineering tools from any location, which democratizes hardware access for smaller sites. Course providers also use microlearning and e-learning primers to reduce classroom time, while still requiring lab validation to meet certification thresholds.

Enterprises continue to favor formats that integrate immersive simulators and digital twins, enabling operators to practice failure recovery and interlock logic without equipment risk. This model delivers consistent training experiences across shifts and can be conducted in shorter sessions that align with staffing realities and uptime priorities. Regional needs, including language and localized regulations, are driving providers to offer tailored content with the same blended architecture, enabling enterprises to standardize curricula across sites. Vendors that combine blended content with outcome-based competency models and role-based performance checks are seeing stronger repeat adoption. The PLC, SCADA, and DCS Training market is expected to keep shifting toward blended and virtual labs as plants scale skill verification under staffing pressure.

By System Type: SCADA Acceleration Driven by Cloud and Cybersecurity Convergence

PLC training accounted for 54.35% of 2025 revenue, yet SCADA programs are projected to expand at a 10.38% CAGR between 2026 and 2031 as remote operations and cloud aggregation reshape skill requirements. The PLC, SCADA, and DCS Training market reflects how controller programming remains the largest installed-skills base, while SCADA curriculum now integrates secure connectivity, historian analytics, and dashboarding for multi-site visibility. SCADA training tracks emphasize topics such as VPNs, certificate authorities, user roles, and alarm rationalization, all aligned with modern security and operations practices. As architectures evolve, cross-system modules that integrate PLC, SCADA, and enterprise data flows become increasingly important, though curricula often remain segmented by vendor stacks. Plants that operate both discrete and continuous processes still rely on DCS-specialist training for batch recipe management, historian workflows, and advanced control that frame operator decisions. Vendors are aligning DCS operator training with digital twin exercises so operators can rehearse abnormal events and tune responses to reduce potential downtime and safety incidents.

SCADA programs also align with standards and role-based security to ensure operators manage privileged access while meeting compliance needs. Training providers continue to package SCADA learning with networking fundamentals and time-series analytics, so teams can recognize patterns and respond more quickly to anomalous conditions. Tools and workflows that previously lived in silos are increasingly bundled into single course sequences. The PLC, SCADA, and DCS Training market is projected to see the fastest growth in SCADA-related roles where IT-OT convergence and remote operations are strategic priorities.

By End-User Industry: Pharmaceutical Surge on GMP Validation Mandates

Manufacturing and discrete accounted for 27.35% of 2025 spend, while pharmaceuticals and life sciences are forecast to grow at 11.36% CAGR through 2031 due to validation and data integrity mandates. The PLC, SCADA, and DCS Training market captures this shift as curricula in regulated industries combine control skills with computer system validation, audit trails, and electronic records and signatures concepts that connect directly to production release decisions. Training providers emphasize lifecycle validation and risk-based approaches that integrate quality attributes and process parameters with automated logic, helping teams align engineering changes with compliant operations. In the machinery and discrete sectors, demand focuses on PLCs, motion, and safety, with vendors offering role-based pathways that culminate in third-party safety credentials when required.

Continuous process industries reinforce investment in DCS operator training and advanced alarm management, while utilities and water networks focus on SCADA and secure remote management across dispersed assets. Food and beverage and mining programs continue to grow as plants improve traceability and condition-based maintenance, while course content is adapted to sector-specific use cases. Cross-industry alignment on cybersecurity strengthens the case for shared modules on IEC 62443 fundamentals, role-based access, and network segmentation, which sit alongside sector-specific specializations. The PLC, SCADA, and DCS Training market is shaped by this dual track of sector-specific depth and cross-cutting security and data literacy.

Geography Analysis

Asia-Pacific accounted for 39.44% of global revenue in 2025, as manufacturing ecosystems across China, India, Japan, and Southeast Asia expanded the installed base of automation technologies. The PLC, SCADA, and DCS Training market in the region benefits from OEM investment in training portals and local delivery, which scales capacity for controller, SCADA, safety, and cybersecurity curricula. Vendors and partners in India and Southeast Asia continue to roll out practical programs for PLCs, robotics, and SCADA operations, with multi-week options that complement shorter skill refreshers across plant roles. Singapore’s Industry 4.0 and 5.0 collaborations between associations, academies, and OEMs are expanding capacity for professional training lines that standardize lab experiences and hands-on commissioning practice. As more plants adopt digital twin approaches, regional teams leverage vendor platforms for operator rehearsal and competency acceleration without the need for centralized travel. The PLC, SCADA, and DCS Training market in Asia-Pacific is therefore anchored by localized delivery at scale and formats that align with high-throughput production environments.

The Middle East and Africa are projected to advance at 12.35% CAGR through 2031 as industrial diversification and infrastructure programs increase training demand in process industries and utilities. Regional programs emphasize cybersecurity-aligned training and role-based competency for operators, engineers, and maintainers in critical infrastructure sectors. OEMs are adding immersive and virtual training elements that reduce logistics complexity across large geographic footprints and remote sites. The PLC, SCADA, and DCS Training market in the region continues to shift toward blended, on-site-ready learning systems that can be deployed within operating facilities. As more industrial users adopt cloud historians and centralized operations centers, SCADA operator training in the region integrates security practices, alarm management, and KPIs tailored to multi-site fleets. Cross-industry partnerships with technical academies are expected to increase the throughput of entry-level technicians, followed by OEM-specific upskilling on installed platforms.

North America maintains a significant presence with university partnerships, OEM training hubs, and integrator ecosystems, though demographic and hiring constraints continue to shape training formats. The PLC, SCADA, and DCS Training market in North America reflects strong employer preference for outcome-based competency models that align with job roles and measure proficiency with practical exams. Employers are scaling blended and virtual labs to reduce travel time while ensuring students still complete hands-on assessments before earning credentials. Enterprise training centers and regional labs continue to add capacity for robotics, controls, and vision systems, enabling employers to send cohorts in staggered blocks. Programs in Europe remain diverse, with national languages, regulations, and legacy modernizations driving country-level differences; OEM academies and local partners are expanding training rooms, stations, and instructors to meet demand. The PLC, SCADA, and DCS Training market in South America centers on core manufacturing clusters and sector-specific demand in mining, where operator and maintenance training on PLCs and SCADA systems remains a priority, supported by vendor-led programs and partner networks.

Competitive Landscape

The PLC, SCADA, and DCS Training market features three strategic archetypes that compete and collaborate across the value chain. OEM academies anchor training on proprietary platforms with roadmaps that translate into regular course updates and structured certification tiers aligned to customer support levels. Independent providers and integrator academies offer cross-platform skills on networking, data connectivity, and visualization that complement vendor stacks and ease multi-vendor operations. Associations and standards bodies set the baseline for cybersecurity and interoperability, which is embedded into training as organizations harden networks and adopt secure development practices.

Leading vendors are integrating competency frameworks and performance-based assessments to align learning outcomes to plant roles. Rockwell’s role-based learning plans formalize progression from fundamentals to advanced practice through practical validation, helping employers link permissions and responsibilities to proven skill levels. Emerson has continued to extend dynamic simulation and HMI tooling so operator and engineer training can incorporate scenario practice, UI configuration, and multi-language runtime elements that reflect real operations. Honeywell’s events and roadmaps highlight a shift in training toward oversight of more autonomous control rooms, with content that adapts to monitoring and exception management skills.

Immersive learning and digital twins are now common across competitive offerings as vendors seek to compress experiential learning and reduce onboarding risk. AVEVA’s operator training ecosystem integrates cloud collaboration to reduce travel and enable distributed learning on the same process models. Yokogawa’s immersive VR training enhances onsite instruction when physical access to equipment is constrained, supporting a wider range of facilities and remote operations. The PLC, SCADA, and DCS Training market is expected to see further convergence of AI-guided tutoring, incident simulation, and analytics-driven coaching across vendor and partner ecosystems as the skills mix shifts toward IT-OT convergence.

PLC, SCADA, And DCS Training Industry Leaders

Rockwell Automation

Siemens AG

ABB Ltd.

Schneider Electric

Honeywell International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: LKH Precicon, in partnership with Ngee Ann Polytechnic and industry partners, launched a five-year initiative to develop Singapore’s first Industry 4.0 and 5.0 training line to support public professional training.

- December 2025: Polytec North America opened the Polytec Technology Training Center in Houston with automation, robotics, and vision-system technologies to support specialized skills development for regional customers.

- November 2025: Rockwell Automation and ICT Academy partnered to launch the Youth Empowerment Program in India to train students in AI, data analytics, and robotic process automation, expanding access to applied technology education.

- February 2025: Cisco and Rockwell Automation signed a Memorandum of Understanding to expand the Digital Skills for Industry program in India, focused on cybersecurity, networking, IoT, data science, AI, programming, and automation technologies for IT and OT roles.

Global PLC, SCADA, And DCS Training Market Report Scope

PLC, SCADA, and DCS training market refers to the education and skill development industry that trains professionals to design, operate, and maintain industrial automation systems used for machine control (PLC), remote monitoring and control of large systems (SCADA), and complex process automation in continuous industries like oil, gas, and power (DCS).

The PLC, SCADA, and DCS Training Market Report is Segmented by Training Mode (Instructor-Led Classroom, Virtual Instructor-Led, and More), System Type (PLC, SCADA, DCS), End-User Industry (Oil & Gas, Power Generation, Manufacturing & Discrete, Chemicals & Petrochemicals, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Instructor-Led Classroom |

| Virtual Instructor-Led (VILT) |

| Self-Paced e-Learning |

| Blended Learning |

| PLC |

| SCADA |

| DCS |

| Oil & Gas |

| Power Generation |

| Manufacturing & Discrete |

| Chemicals & Petrochemicals |

| Food & Beverage |

| Pharmaceuticals & Life Sciences |

| Water & Wastewater |

| Mining & Metals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Training Mode | Instructor-Led Classroom | |

| Virtual Instructor-Led (VILT) | ||

| Self-Paced e-Learning | ||

| Blended Learning | ||

| By System Type | PLC | |

| SCADA | ||

| DCS | ||

| By End-User Industry | Oil & Gas | |

| Power Generation | ||

| Manufacturing & Discrete | ||

| Chemicals & Petrochemicals | ||

| Food & Beverage | ||

| Pharmaceuticals & Life Sciences | ||

| Water & Wastewater | ||

| Mining & Metals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the PLC, SCADA, and DCS Training market?

The PLC, SCADA, and DCS Training market size is USD 464.90 million in 2026 and is projected to reach USD 619.80 million by 2031 at a 5.92% CAGR.

Which delivery model is growing fastest in the PLC, SCADA, and DCS Training market?

Blended learning that combines digital modules with instructor-led labs is the fastest-growing delivery model, with an 11.64% CAGR through 2031 supported by virtual labs and digital twin environments.

Which system type will lead growth within the PLC, SCADA, and DCS Training market?

SCADA training is projected to grow fastest at 10.38% CAGR as remote operations, cloud historians, and secure connectivity expand required competencies.

Where is regional demand most significant within the PLC, SCADA, and DCS Training market?

Asia-Pacific holds the largest revenue share, while the Middle East and Africa record the fastest growth in infrastructure and diversification initiatives.

How are vendors differentiating training offers in the PLC, SCADA, and DCS Training market?

Vendors are tying certifications to support tiers, expanding role-based paths, and embedding digital twins and immersive labs to compress time-to-competency and validate performance.

What standards most influence curricula in the PLC, SCADA, and DCS Training market?

IEC 62443 drives role-based cybersecurity training across control system stakeholders, with implementer and specialist certifications shaping course structures and assessments.

Page last updated on: