Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

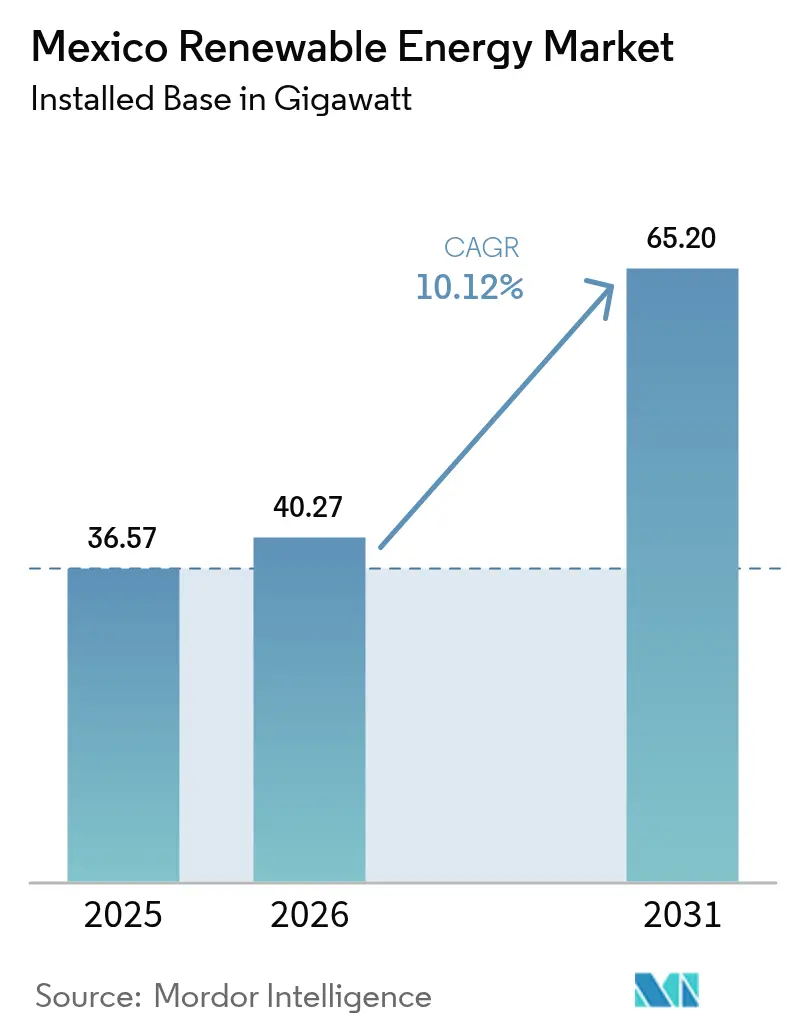

| Base Year Market Size (2025) | 36.57 gigawatt |

| Market Volume (2026) | 40.27 gigawatt |

| Market Volume (2031) | 65.2 gigawatt |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Renewable Energy Market Analysis by Mordor Intelligence

The Mexico Renewable Energy Market size is expected to grow from 36.57 gigawatt in 2025 to 40.27 gigawatt in 2026 and is forecast to reach 65.2 gigawatt by 2031 at 10.12% CAGR over 2026-2031.

Strong federal targets, cost-competitive solar photovoltaics, and fresh development-bank credit lines anchor this expansion while the new Electricity Sector Law preserves state control through the Federal Electricity Commission (CFE). Developers focus on high-irradiance northern states, repowering wind farms along the Gulf coast, and pairing batteries with new plants to clear interconnection queues. Corporate power-purchase agreements (PPAs) are increasingly bypassing utility procurement, funneling demand toward distributed generation systems with capacities below 10 MW. Meanwhile, peso volatility and local-content rules raise financing hurdles, prompting a decisive shift toward peso-denominated lending from NAFIN and Bancomext.

Key Report Takeaways

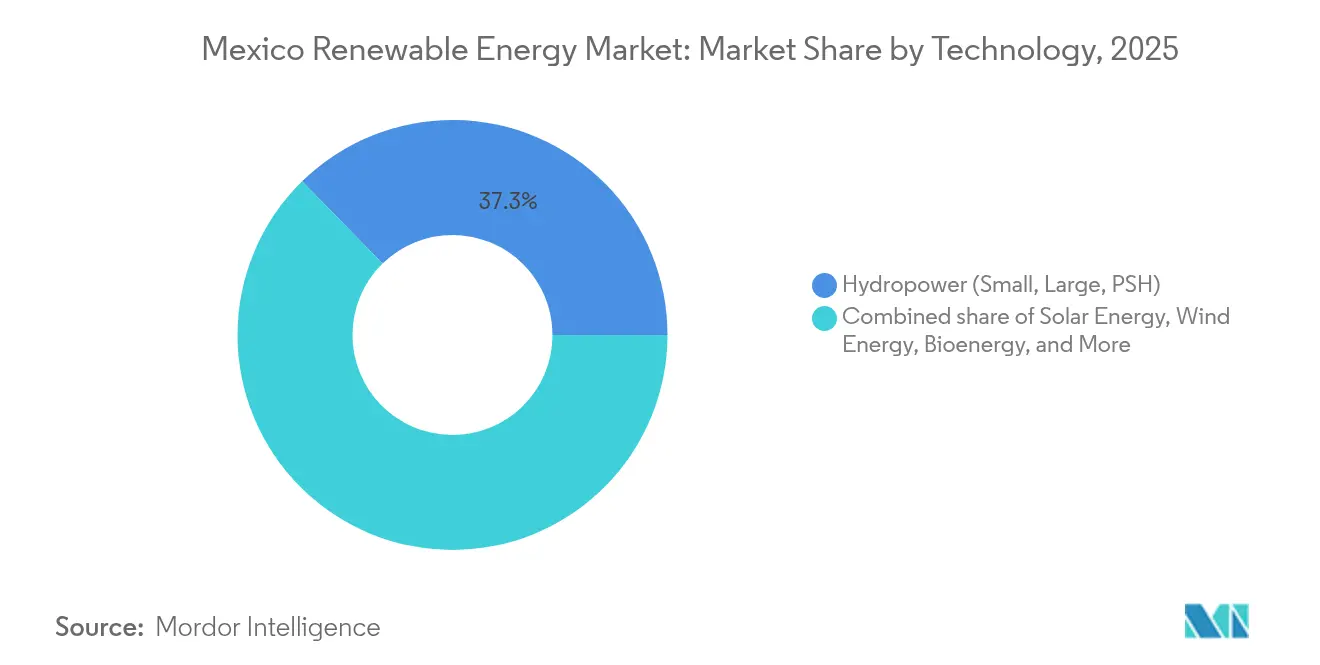

- By technology, hydropower accounted for 37.33% of the Mexican renewable energy market in 2025, while solar energy is advancing at a 14.02% CAGR through 2031.

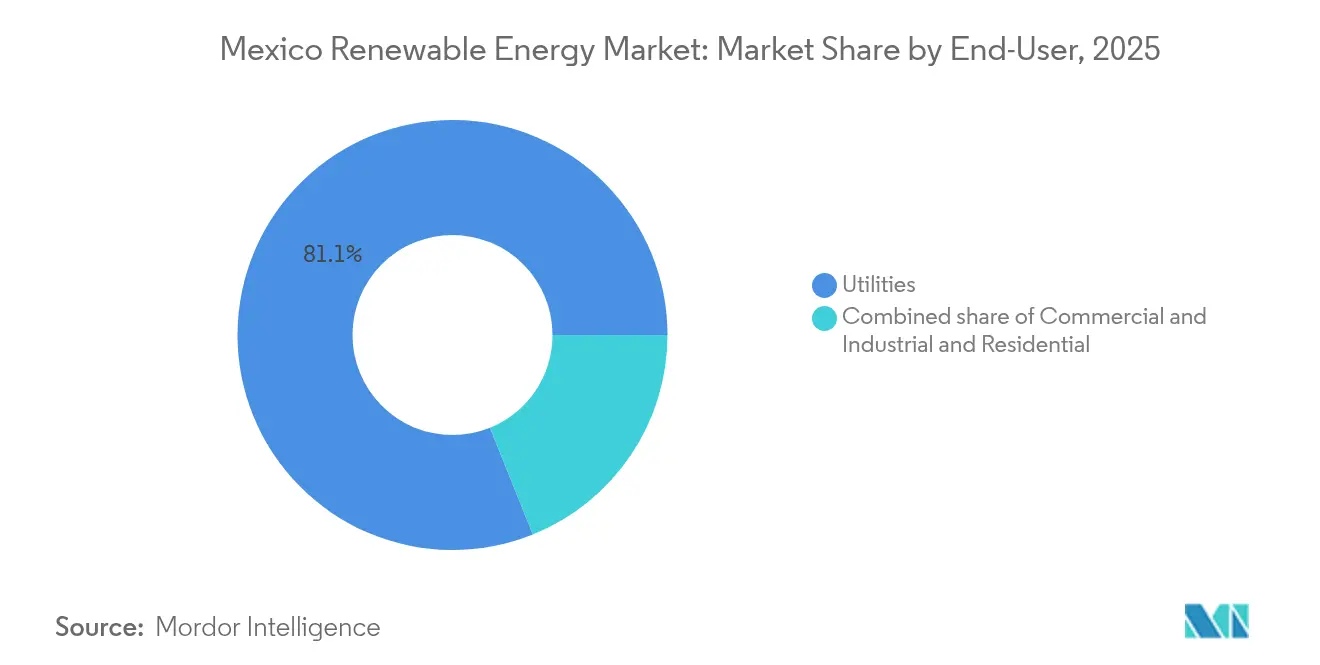

- By end-user, the utilities segment accounted for 81.10% of the Mexico renewable energy market size in 2025, while residential installations drove growth at a 14.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solar PV LCOE continues to undercut combined-cycle gas | +2.8% | National, with strongest gains in northern states (Sonora, Chihuahua) and Yucatán Peninsula | Medium term (2-4 years) |

| PPAs backed by corporate sustainability targets (C&I demand) | +1.9% | National, concentrated in industrial corridors (Nuevo León, Querétaro, Guanajuato) | Short term (≤ 2 years) |

| Wind repowering potential of ageing northern-coast farms | +1.5% | Oaxaca, Tamaulipas, Nuevo León | Medium term (2-4 years) |

| Grid-connected battery hybrids approved under CEL reform | +1.7% | National, early deployments in Baja California and Sonora | Long term (≥ 4 years) |

| Climate-linked development-bank credit lines (NAFIN, Bancomext) | +1.2% | National, prioritizing small and medium enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Solar PV LCOE Continues to Undercut Combined-Cycle Gas

The average utility-scale solar levelized cost of electricity reached USD 51/MWh in 2024, decisively lower than the gas-fired alternative, which must account for fuel volatility pricing.[1]International Energy Agency, “Renewables 2025 Analysis,” iea.org Mexico’s high solar irradiation, often exceeding 2,000 kWh/m², drives capacity factors that outclass those of its global peers and reshape merit-order dispatch. Gas units now shift toward peaking roles, stranding investments and freeing roughly USD 1.6 billion in annual US gas import costs.[2]Ember Climate, “Mexico Gas Import Savings Through Renewables,” ember-climate.org Solar’s zero marginal cost sharpens midday price troughs, prompting grid operators to heighten voltage and frequency controls. Developers counter curtailment risk by colocating battery storage, extracting peak-shaving and capacity-market revenues that lift project returns.

PPAs Backed by Corporate Sustainability Targets Drive C&I Demand

Multinational manufacturers, including General Motors, lock in fixed-price renewable PPAs to meet global decarbonization mandates, driving a 14.60% CAGR for commercial and industrial installations. Self-supply permits allow firms to skirt traditional utility tendering and transact bilaterally over private lines, while clean-energy certificates confirm compliance. Grupo Bachoco’s 26 MW distributed solar program, spanning 19 states, highlights how aggregated commercial and industrial (C&I) loads can achieve utility-scale economics. PPA tenors of 15-20 years reduce exposure to peso swings when paired with dollar-indexed clauses, anchoring long-term viability.

Wind Repowering Potential of Ageing Northern-Coast Farms

First-generation wind assets on the Tamaulipas coast approach life-cycle maturity. Modern turbines that double their nameplate capacity unlock a 1.4 percentage-point increase in the Mexico renewable energy market's CAGR. The Victoria project already yields 184 GWh per year on 49.5 MW capacity, displacing 72,345 tCO₂. Repowering leverages existing interconnection rights, reduces permitting lead times, and streamlines community consultations on land use. Sempra Infrastructure's 320 MW Cimarron expansion typifies investors banking on proven wind regimes and grid access.

Grid-Connected Battery Hybrids Approved Under CEL Reform

The March 2025 storage mandate confers clean-energy-certificate eligibility to renewable-plus-storage hybrids, raising the addressable revenue stack by 1.2 percentage points. Invenergy’s La Toba plant pairs 35 MW solar with 20 MW batteries to deliver ramping, frequency, and capacity services in fuel-scarce Baja California Sur. Streamlined interconnection protocols reduce approval times, while standardized technical codes ensure compliance with grid codes. Developers leverage merchant battery revenue to hedge intermittency congestion penalties under the new dispatch regime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intermittency congestion on Sistema Interconectado Nacional | -1.90% | National grid nodes | Short term (≤ 2 years) |

| Policy uncertainty post-2028 plan review | -2.10% | Nationwide | Long term (≥ 4 years) |

| Rising WACC tied to peso depreciation | -1.10% | National financing | Short term (≤ 2 years) |

| OEM supply-chain exposure to USMCA rules | -0.80% | Manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intermittency Congestion on the Sistema Interconectado Nacional

Variable generation has outpaced transmission build-out, slicing 1.9 percentage points off the Mexico renewable energy market CAGR. Only 2,600 km of new lines came online in five years, while 4,038 km remain under construction, forcing curtailments at peak production. Grid operator CENACE relies on thermal units to balance frequency, which escalates ancillary-service costs and erodes solar’s price advantage. Planned ±500 kV corridors aim to relieve congestion by 2027; however, permitting delays threaten to compromise timelines. Developers hedge exposure via hybrid storage or location-based hedging instruments to stabilize revenues.

Policy Uncertainty Post-2028 National Electricity Plan Review

The mandated 2028 policy review is expected to hinder growth as investors weigh potential shifts to CFE dominance.[3]Lourdes Melgar, “Mexico’s Electricity Reform and the State’s Role,” Baker Institute for Public Policy, bakerinstitute.org Prior reversals, such as dissolving autonomous regulators, signal unpredictability in governance. The horizons of clean-energy certificates, which are only two years, clash with 20-year asset lives, complicating revenue modeling. Sponsors are increasingly embedding change-in-law clauses and seeking multilateral wrap-around guarantees to mitigate regulatory risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Surges as Hydropower Holds Baseload

Hydropower retained 37.33% of Mexico's renewable energy market share in 2025, primarily driven by legacy dams such as Chicoasén and La Angostura, which supply firm power throughout the year. The segment benefits from existing reservoirs, mature operations and maintenance (O&M) routines, and limited environmental opposition compared to new large dams. Pumped-storage retrofits in northern states are under review, which could add peak-shaving flexibility without new impoundments. Solar is advancing at a 14.02% CAGR to 2031, the fastest clip within the Mexico renewable energy market, aided by continued module-cost deflation and a wave of corporate PPAs for distributed rooftops. CFE's plan to build nine utility-scale solar plants totaling 4.673 GW underscores the state utility's pivot toward photovoltaic capacity in inexpensive desert land across Sonora, Chihuahua, and Durango.

Repowering keeps wind competitive; 2.5 GW in the Isthmus of Tehuantepec will replace aging 2 MW turbines with 5 MW-plus machines, boosting production without requiring new land leases. Geothermal remains steady at approximately 950 MW from Los Azufres and Los Humeros, providing a valuable baseload for the Mexican renewable energy industry, despite capital-constrained expansion drilling. Bioenergy projects fueled by bagasse and municipal waste operate near sugar mills in Veracruz and Jalisco, selling surplus electricity into the grid while supplying process heat onsite. Ocean energy is still nascent; regulatory standards for marine technologies are pending, which keeps private investment sidelined.

By End-User: Residential Gains as Utilities Retain Dominance

Utilities captured 81.10% of total demand in 2025, reflecting the statutory priority of CFE and legacy PPAs signed before the 2025 reform. The March 2025 law secures CFE at ≥54% generation share, limiting merchant developers’ runway but also guaranteeing offtake for preferred hybrid projects that bolster grid reliability. Residential demand is expanding at a 14.25% CAGR and has topped 1.2 GW of distributed capacity in 2024, as net-metering now credits surplus power at 90% of the retail tariff, yielding paybacks of 5 to 7 years for typical rooftops. Geographic clustering is observed in higher-income districts of Mexico City, Monterrey, and Guadalajara, where high tariffs and accessible financing drive adoption patterns.

Commercial and industrial buyers are relying on behind-the-meter arrays that cover 30–50% of their daytime electricity needs, shielding them from grid-tariff escalation, which reached an 8% average increase in 2024. Auto-parts suppliers in Nuevo León are increasingly combining rooftop arrays with ground-mount carport systems to maximize on-site generation. The regulatory obligation to report private PPAs to SENER adds paperwork, but it has not slowed contracting volume; price certainty and ESG signaling outweigh the administrative costs. As distributed generation steps in where transmission is saturated, mid-sized developers are carving out profitable niches within the Mexico renewable energy industry.

Geography Analysis

Northern states, Sonora, Chihuahua, and Nuevo León, anchor solar growth, with irradiation surpassing 2,000 kWh/m² annually, delivering capacity factors of nearly 29%. Tamaulipas and Oaxaca continue to be wind stalwarts, hosting repowering campaigns that recycle grid interconnections and expedite commissioning. The Yucatan Peninsula, short on pipelines yet flush with tourism-driven load, demands a USD 30 billion grid overhaul by 2029 that will pair battery hybrids with solar peaker units.

Central Mexico, encompassing Mexico City and Guadalajara, excels at distributed solar for manufacturing clusters. PPAs often bundle renewable energy with voluntary carbon credits, cementing corporate decarbonization strategies. Cross-border opportunities on the Baja California-San Diego corridor hinge on synchronizing regulatory regimes under the USMCA to facilitate clean-power exports once transmission upgrades conclude in 2027.

Southern highlands leverage hydro and geothermal baseload yet wrestle with rugged terrain and slow right-of-way acquisition. Climate resilience planning now factors cyclonic rainfall patterns that threaten dam safety and wind-farm foundations. Emerging tidal prospects in Cozumel mark an early diversification into marine renewables, but the commercial impact will remain marginal through the forecast horizon.

Competitive Landscape

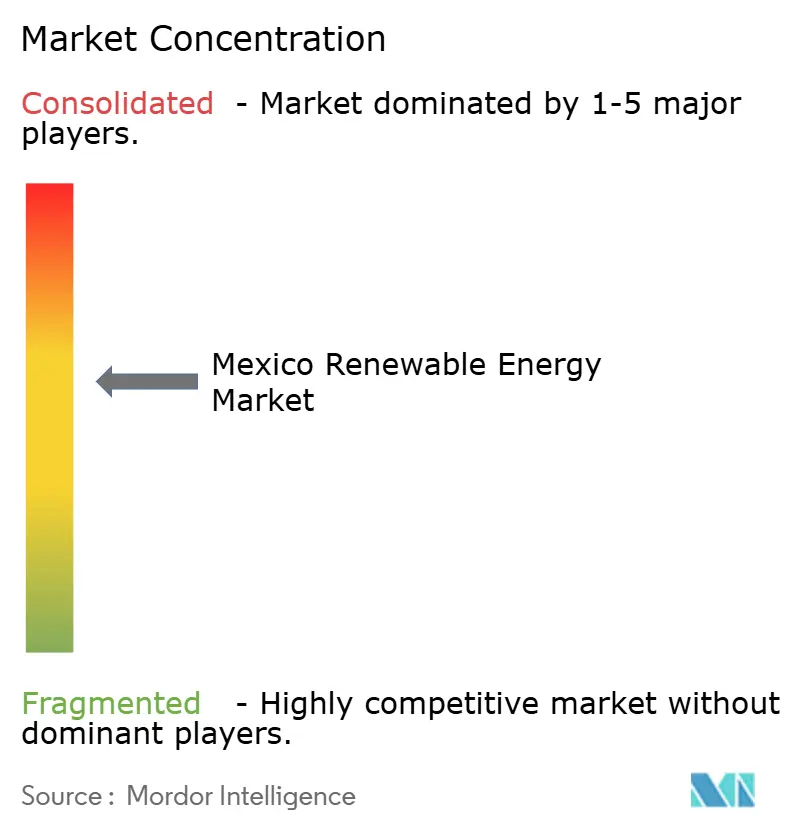

Market leadership rests on a moderate concentration of global utilities and domestic conglomerates that are able to ride regulatory shifts while sustaining balance-sheet strength. Iberdrola, Enel, and Acciona each exceed 1.2 GW operational capacity, leveraging digital O&M platforms to shave downtime and earn CENACE ancillary revenue. Sempra Infrastructure diversifies into storage-linked projects such as Cimarron, demonstrating technical synergies across gas, LNG, and renewables.

CFE remains the anchor player, funneling USD 12.3 billion into renewable additions and hydro retrofits while retaining dispatch prerogatives that can curtail private competitors during grid stress events. Domestic IPPs, such as Zuma Energía and Cubico, target solar and wind niches that majors overlook due to their size or land tenure complexity. Financing access increasingly differentiates winners: entities securing blended-finance tranches from the EIB, NADB, or NAFIN close deals faster and at lower interest rates.

Technology differentiation intensifies around hybrid solar-plus-storage designs, LIDAR wind-site validation, and AI-driven curtailment forecasting. Supply-chain localization remains a looming risk; firms investing in domestic blade or module assembly aim to pre-empt USMCA compliance issues and shorten shipping timelines. Competitive parity will likely hinge on holistic solutions, combining generation, demand response, and grid services, rather than lowest-cost kilowatt-hour alone.

Mexico Renewable Energy Industry Leaders

Comisión Federal de Electricidad (CFE)

Iberdrola SA

Acciona Energía

Enel Green Power

Zuma Energía

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mexico mandated battery storage for all new renewable energy plants, expanding the eligibility of clean-energy certificates to include hybrids.

- January 2025: The new Electricity Sector Law set CFE’s minimum 54% generation share and folded autonomous regulators into state entities.

- January 2025: CFE unveiled a USD 23.4 billion investment plan for the period up to 2030, earmarking USD 12.3 billion for renewable energy capacity.

- November 2024: Mexico’s National Electric Strategy aims to achieve 45% renewable electricity by 2030, involving 51 projects worth USD 22.3 billion.

Mexico Renewable Energy Market Report Scope

Renewable energy is the energy collected from renewable resources, such as sunlight, wind, water movement, and geothermal heat, that are naturally replenished.

The Mexican renewable energy market is segmented by technology and end user. By technology, the market is segmented into Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy. By technology, the market is segmented into Utilities, Commercial and Industrial, and Residential. For each segment, the installed capacity and forecasts are presented in gigawatts (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large is the Mexico renewable energy market in 2026?

The Mexico renewable energy market size reaches 40.27 GW in 2026 and is projected to hit 65.2 GW by 2031.

Which technology is growing fastest within the market?

Solar power leads growth, advancing at a 14.02% CAGR through 2031 on the back of falling module costs and mandated battery hybrids.

How does the new Electricity Sector Law affect private developers?

The law reserves 54% generation for CFE, yet leaves 46% available to private firms, creating a hybrid public-private model that still enables independent growth.

Why are Clean Energy Certificates important after the 2025 reform?

The restored CEL scheme lets hybrid battery projects earn tradable certificates, adding a new revenue stream and boosting project bankability.

How is policy uncertainty affecting new projects?

Anticipation of the 2028 National Electricity Plan has widened financing spreads and delayed some greenfield investments, particularly for offshore wind and advanced geothermal.

Page last updated on: