Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.68 Billion |

| Market Size (2026) | USD 9.09 Billion |

| Market Size (2031) | USD 11.45 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Plastic Packaging Market Analysis by Mordor Intelligence

The Mexico plastic packaging market size is projected to expand from USD 8.68 billion in 2025 and USD 9.09 billion in 2026 to USD 11.45 billion by 2031, registering a CAGR of 4.73% between 2026 to 2031. A structural realignment of North American supply chains, near-shoring by United States brands, and Mexico’s status as the only domestic polypropylene producer are widening local converters’ cost advantage and ensuring steady resin availability. Brand-owner demand for recycled content is met by PetStar’s world-largest food-grade PET recycling plant, enabling converters to close material loops without long-haul logistics. Peso depreciation raised imported-resin costs in 2024-2025, but duty-free access to United States feedstocks under the USMCA cushioned margin pressure. Flexible formats aimed at e-commerce and direct-to-consumer channels, coupled with polypropylene closures that comply with tethered-cap rules, create incremental growth pockets for converters that can blend rapid line changeovers with automation-enabled quality control.

Key Report Takeaways

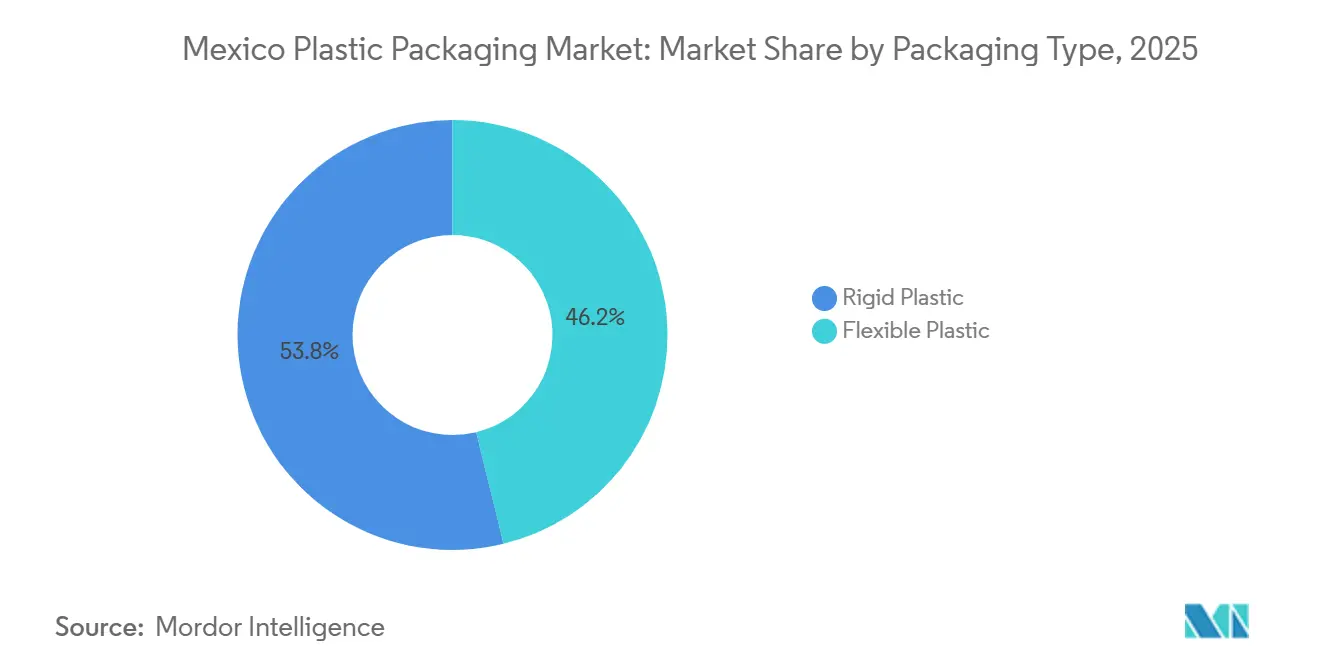

- By packaging type, rigid plastic held 53.82% of the Mexico plastic packaging market share in 2025, while flexible plastic is forecast to advance at a 5.09% CAGR through 2031.

- By material, polyethylene accounted for 27.54% of Mexico's plastic packaging market size in 2025, whereas polypropylene is projected to grow at a 5.89% CAGR to 2031.

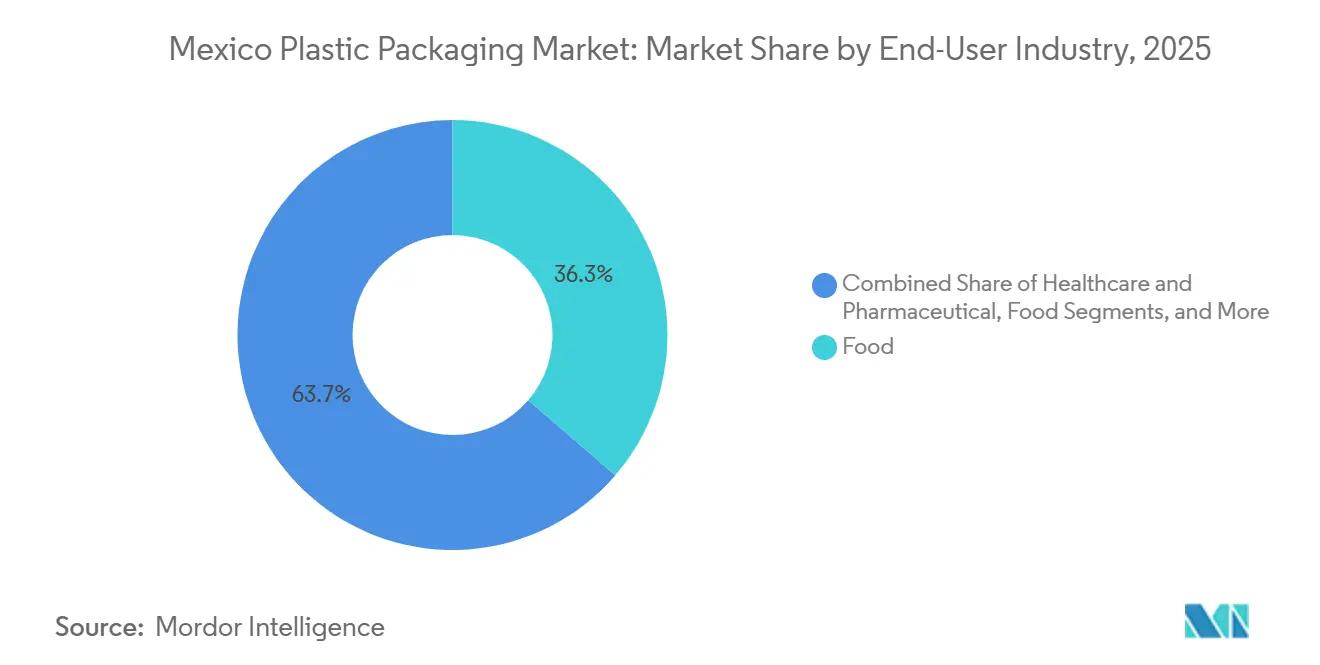

- By end-user, food applications commanded 36.32% share in 2025 and personal care is positioned to expand at a 5.64% CAGR over 2026-2031.

- By pack format, bottles and jars represented 31.12% of Mexico plastic packaging market size in 2025; stretch and shrink films record the highest growth at 4.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Access to Some of the Cheapest Plastic Imports From the United States | +1.2% | Northern border states and national | Short term (≤ 2 years) |

| Rising Packaged-Food and Industrial Output Fueling Domestic Demand | +1.1% | National; Bajío corridor early gains | Medium term (2-4 years) |

| Near-shoring of United States Brands Triggering Local Packaging Capacity Expansions | +0.9% | Northern and central states; Yucatán maquiladora zones | Medium term (2-4 years) |

| Growth of E-commerce and Direct-to-Consumer Brands | +0.7% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| High PET-Recycling Infrastructure Enabling Cost-Competitive rPET Packaging | +0.5% | National; Toluca and Tabasco hubs | Long term (≥ 4 years) |

| Investment in Advanced Manufacturing Technologies | +0.4% | Nuevo León, Querétaro, State of Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Access To Some Of The Cheapest Plastic Imports From The United States

United States exporters shipped USD 6.8 billion of primary-form plastics to Mexico in 2023, and Gulf Coast resin can reach Monterrey within 72 hours, trimming freight costs by up to 60% versus shipments to South American or Asian processors.[1]United States Census Bureau, “Trade in Goods with Mexico,” census.gov Alpek’s reference margin fell to USD 0.14 per pound in 3Q25, allowing Mexican converters to lock multi-year linear-low-density polyethylene contracts at historic lows. USMCA tariff-free clauses further reinforce supply security, while September 2025 reciprocal tariffs on PET imports into the United States coax beverage brands to source bottles from Mexican plants instead of Asia. This arbitrage accelerates investment in warehouse silos, hopper cars, and bulk-handling systems that let converters toggle between domestic and United States feedstocks with minimal downtime. Small and medium enterprises gain flexibility, yet large converters with purchasing power capture the widest spreads, redirecting cost savings into automation and quality-control upgrades.

Rising Packaged-Food And Industrial Output Fueling Domestic Demand

Mexico’s packaged-food value climbed to USD 100.4 billion in 2024 and will grow 5.4% annually through 2029, outpacing the 4.73% the Mexico plastic packaging market. More than 231,000 food-processing establishments generate USD 35.8 billion in output, bifurcating demand between multinational plants that require standardized PET bottles and regional cooperatives that need small-batch pouches. The IMMEX plastics and rubber subsector earned USD 6.0 billion from 598 maquiladora plants in 2024, underscoring the link between export assembly lines and secondary packaging such as anti-static trays and stretch films. Online food orders grew at a 51% CAGR from 2019-2023, prompting converters to integrate tamper-evident seals and microwave-safe polypropylene into flexible formats that cut spill-related returns for delivery platforms. Those able to attach peel-and-reseal zippers or portion-control dispensing features capture premium SKU contracts from convenience-oriented brands.

Near-Shoring Of United States Brands Triggering Local Packaging Capacity Expansions

Tetra Pak invested MXN 1 billion (USD 54.6 million) to enlarge its Mexicali caps plant in 2024-2025, reflecting how relocating assembly lines pushes suppliers to position production close to new factories.[2]Mexico Business News Staff, “Tetra Pak Expands Capacity and Clean Energy in Mexico in 2025,” mexicobusiness.news ALPLA and Coca-Cola FEMSA opened a USD 60 million PET recycling site in Tabasco capable of producing 50,000 metric tons, embedding closed-loop feedstock within the near-shoring corridor. Envases Universales expanded Guadalupe operations by USD 50 million in January 2025, scaling bottle runs with 30-100% recycled content for beverage and automotive clients. Berry Global switched all Mexican plants to renewable power in 2023, signaling that the energy mix is now embedded in contract award criteria for near-shored suppliers. Together, these moves confirm that capacity, sustainability, and logistics proximity now form a triad of mandatory capabilities for winning multinational tenders.

Growth Of E-Commerce And Direct-To-Consumer Brands

E-commerce penetration lags United States benchmarks, yet compound growth of 51% in online food ordering and even faster gains in personal care are rewriting packaging briefs. Fulfillment centers specify pre-stretched films with 200-300% elongation that prevent pallet collapse while shedding gram weight. Direct-to-consumer cosmetic labels opt for branded mailers that double as marketing touchpoints, prompting converters to embed QR codes for real-time authenticity checks. L'Oréal’s USD 80 million expansion in San Luis Potosí, which lifted local capacity 50%, anchors premium dispensing demand, including airless pumps and dual-chamber packs. AptarGroup’s April 2025 collaboration with Nutrioli showcases how closure innovation is migrating into edible-oil segments traditionally served by commodity caps. Converters adding small-batch digital printing and label-on-demand services capture subscription-box contracts that prize rapid artwork changeovers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Shift Toward Paper and Compostable Formats | -0.6% | Mexico City, Guadalajara, Monterrey | Medium term (2–4 years) |

| Intensifying State-Level Single-Use-Plastic Bans | -0.8% | Twenty states with varied enforcement | Short term (≤ 2 years) |

| Infrastructure Gaps in Compostable Alternatives | -0.3% | National; rural municipalities weakest | Long term (≥ 4 years) |

| Peso Volatility Raising Imported Resin Costs for Converters | -0.5% | National; unhedged converters hardest hit | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Shift Toward Paper And Compostable Formats

Fifty-four percent of Mexican shoppers now weigh environmental credentials, and 70% of personal care buyers seek eco-friendly packs, yet industrial composting hubs remain scarce outside major cities. Grupo Modelo’s USD 3.6 billion plan through 2027 prioritizes returnable glass, underscoring beverage producers’ hedging on substrate mix. The Mexico Plastics Pact, formed in 2024, targets the elimination of polystyrene, but compliance remains voluntary and uneven. Paper-lined kraft pouches still use polyethylene seals that hinder recyclability, and bio-based resin costs are 2-3 times those of virgin polyethylene, limiting uptake to premium SKUs. Converters face a capital-allocation dilemma when deciding whether to retrofit lines for polylactic acid or double down on lightweighting existing plastics.

Intensifying State-Level Single-Use-Plastic Bans

Mexico City’s prohibition on bags and single-use items catalyzed at least 20 similar state-level measures by 2025, yet inspection capacity varies, and fines span from none to MXN 339,420 (USD 17,000) per incident in the State of Mexico.[3]Expansión, “Prohibición de plásticos de un solo uso en el Estado de México,” expansion.mx The January 2026 General Law of Circular Economy mandates national extended producer responsibility plans, but fee schedules and digital registry details remain unresolved. Converters must juggle multiple SKUs: compliant paper or reusable formats for Mexico City, standard polypropylene cups for Puebla, and refillable PET bottles for Yucatán. Capital investment in modular tooling and quick-change molds climbs, squeezing cash flows for small processors. Harmonization before 2028 is unlikely, sustaining the compliance patchwork and favoring firms with multi-plant networks that can ship legal formats across borders overnight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Flexible Formats Gain Momentum Amid Logistics Shift

Flexible packaging is forecast to climb at 5.09% annually from 2026 to 2031, surpassing rigid packaging’s 4.73% growth, even though rigid captured 53.82% of value in 2025. The Mexico plastic packaging market linked to e-commerce has swelled as fulfillment centers prioritize pouches and laminated films to compress freight charges, while food-service chains still rely on rigid PET bottles and polypropylene jars for tamper-evidence.

Rigid formats remain essential in beverages and pharmaceuticals where heat stability, oxygen barriers, and regulatory compliance dominate purchasing criteria. Coca-Cola FEMSA and Arca Continental’s internal bottle-to-bottle loops secure 30% recycled content, locking in demand for rigid PET preforms that flexible suppliers cannot displace. Conversely, personal care brands convert concentrates into refill pouches, allowing flexible converters to capture incremental market share in Mexico's plastic packaging market through high-gloss rotogravure finishes and tactile varnishes that elevate shelf appeal.

By Material: Polypropylene Accelerates On Closure Innovation

Polyethylene held 27.54% of the 2025 value, dominating stretch films and chemical drums, yet polypropylene is poised for a 5.89% CAGR, the fastest among resins, as biaxially oriented formats and tethered-cap regulations spur adoption. Downward pressure on Alpek’s polypropylene margins lets converters lock multi-year supplies below five-year averages, securing input cost stability. The Mexico plastic packaging market size for polypropylene closures is rising as beverage brands phase in one-piece caps that stay attached after opening.

PET recycling capacity reached 51,000 metric tons yearly after ALPLA’s Planeta startup in Tabasco, pushing Mexico's plastic packaging market share for recycled PET higher in rigid bottles BKV-GMBH.DE. Barrier polymers such as ethylene-vinyl alcohol are used in modified-atmosphere packs for fresh produce, yet remain in niche volumes.

By End-User Industry: Personal Care Outpaces Aggregate Growth

Food held 36.32% of 2025 value, yet personal care will post 5.64% CAGR through 2031, driven by multinational investments like L'Oréal’s USD 80 million line expansion. Beauty brands specify airless pumps and refill pods, yielding higher revenue per kilogram than commodity food bottles, thus tilting the Mexico plastic packaging market toward margin-rich SKUs.

Beverage applications benefit from closed-loop PET recycling and branded returnable-bottle programs. Healthcare packaging grows steadily under NOM-241-SSA1-2025 requirements, while industrial chemical containers fluctuate with export-assembly volumes from the IMMEX corridor. Household cleaners add child-resistant polypropylene caps to meet safety norms, thereby boosting polypropylene demand in Mexico's plastic packaging industry.

By Pack Format: Stretch And Shrink Films Ride Distribution Boom

Bottles and jars controlled 31.12% of the 2025 value, but stretch and shrink films led growth at a 4.71% CAGR to 2031 as palletized exports of electronics, auto parts, and e-commerce parcels surge. Machine-grade film lines capable of 500 millimeter widths and anti-static additives secure multi-year orders from logistics giants.

In the dynamic landscape of packaging, caps, closures, and dispensing systems are at the forefront of innovation. A prime example is Aptar's Nutrioli project, which showcases the shift of precision-engineered components into the food sector. Meanwhile, pouches are gaining traction in the realms of detergents and concentrated products. Trays and tubs continue to be go-to choices for dairy products and ready-to-eat meals. This is particularly true as polypropylene-based microwaveable options are making it easier for consumers to transition away from traditional foamed polystyrene packaging.

Geography Analysis

Nuevo León anchors the northern cluster, housing Envases Universales’ five-plant network and attracting cross-border beverage, automotive, and electronics accounts that demand just-in-time deliveries. The State of Mexico and greater Mexico City host PetStar’s world-leading rPET plant and Tetra Pak’s processing-equipment site, balancing rigid-bottle recycling with aseptic-carton component production.

Querétaro leverages renewable-energy upgrades, such as Tetra Pak’s 1,000-panel solar array, to pitch itself as a sustainability showcase, while Baja California’s Mexicali concentrates cap output after Tetra Pak’s MXN 1 billion revamp. Tabasco, long overlooked, now hosts ALPLA’s PET recycling hub, decentralizing circular economy infrastructure beyond traditional corridors.

San Luis Potosí emerges as a personal-care cluster after L'Oréal’s capacity expansion, while the Yucatán Peninsula gains relevance through Grupo Modelo’s brewery modernization, which privileges returnable packaging. The Bajío corridor, Guanajuato, Aguascalientes, and Jalisco, hosts automotive supply chains that order anti-static trays and protective films. Southern states remain lower in intensity, but targeted brewery and tourism projects hint at gradual demand growth.

Competitive Landscape

Global majors Amcor, ALPLA, Mondi, and Berry Global maintain strong procurement leverage, securing steady resin flows and supporting multi-year supply contracts with beverage and personal care multinationals. Their Mexican plants combine large cavitation injection systems with AI-guided vision tools that cut defect rates in caps, films, and preforms, an approach exemplified by SACMI Classy-AI units installed at several closure lines. Scale also lets them amortize the cost of food-grade recycled resin, especially after Berry Global’s CleanStream process gained clearance for 100% recycled polypropylene in contact-sensitive applications. These advantages allow incumbents to defend key beverage and beauty contracts even as pricing pressure tightens. Competition among the top tier now centers on differentiating sustainability credentials rather than raw output.

A second stratum of regionally focused groups, led by Envases Universales, PetStar, Grupo Gondi, and Grupo Phoenix, exploits proximity to customers and quick changeover capability. Envases Universales added 110 direct jobs in Guadalupe after its USD 50 million expansion, which increased recycled-content bottle capacity and cut lead times for bottled-water brands in Monterrey and Reynosa. PetStar operates the world’s largest food-grade rPET plant in Toluca, processing 3.44 billion bottles a year and feeding closed-loop supply chains for Coca-Cola FEMSA and Arca Continental. Grupo Gondi pushes lightweight corrugated alternatives that compete with plastic secondary packs inside border maquiladora zones, while Grupo Phoenix targets dairy and dessert clients with IML polypropylene cups that withstand microwave reheating. These mid-scale players capture accounts that value agility and bilingual technical service over absolute global footprint.

Niche converters and emerging disruptors round out the field. Flexitek and Cintex specialize in short-run pouch printing for direct-to-consumer brands that refresh artwork several times a quarter. Plasticos Especializados produces anti-static trays for the Bajío electronics corridor, a segment insulated from state plastic bans because the packs rarely leave factory walls. UFlex, Mauser, Greif, and Clondalkin supply industrial drums, IBCs, and barrier liners demanded by chemical exporters and automotive paint shops. Although individually small, such specialists fill capability gaps that large players overlook, keeping overall market concentration moderate.

Mexico Plastic Packaging Industry Leaders

Amcor plc

ALPLA-Werke Alwin Lehner GmbH & Co KG

Mondi plc

Sonoco Products Company

Greif, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tetra Pak finished a MXN 1 billion (USD 54.6 million) capacity and clean-energy upgrade at its Mexicali caps plant, now supplying customers across Mexico, the United States, and South America.

- April 2025: Grupo Modelo unveiled a USD 3.6 billion plan for 2025-2027 that prioritizes returnable packaging and glass recycling across four breweries and 300,000 retail outlets.

- April 2025: AptarGroup and Nutrioli launched breakthrough edible-oil closures, extending dispensing innovation into food.

- January 2025: Envases Universales invested USD 50 million to expand its Guadalupe plant, adding 110 direct jobs and boosting recycled-content bottle output.

Mexico Plastic Packaging Market Report Scope

The Mexico Plastic Packaging Market Report is Segmented by Packaging Type (Rigid Plastic, Flexible Plastic), Material (Polyethylene, Polyethylene Terephthalate, Polypropylene, Polystyrene and EPS, Polyvinyl Chloride, EVOH and Other Barrier Plastics), End-user Industry (Food, Beverage, Healthcare and Pharmaceutical, Personal Care and Cosmetics, Household and Industrial Chemicals), Pack Format (Bottles and Jars, Caps and Closures and Dispensing Systems, Pouches and Sachets, Trays and Cups and Tubs, Stretch and Shrink Films), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Packaging Type

| Rigid Plastic |

| Flexible Plastic |

By Material

| Polyethylene (HDPE, LDPE, LLDPE) |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP and BOPP/CPP) |

| Polystyrene and EPS |

| Polyvinyl Chloride (PVC) |

| Ethylene-Vinyl Alcohol (EVOH) and Other Barrier Plastics |

By End-user Industry

| Food |

| Beverage |

| Healthcare and Pharmaceutical |

| Personal Care and Cosmetics |

| Household and Industrial Chemicals |

By Pack Format

| Bottles and Jars |

| Caps, Closures and Dispensing Systems |

| Pouches and Sachets |

| Trays, Cups and Tubs |

| Stretch and Shrink Films |

| By Packaging Type | Rigid Plastic |

| Flexible Plastic | |

| By Material | Polyethylene (HDPE, LDPE, LLDPE) |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP and BOPP/CPP) | |

| Polystyrene and EPS | |

| Polyvinyl Chloride (PVC) | |

| Ethylene-Vinyl Alcohol (EVOH) and Other Barrier Plastics | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Household and Industrial Chemicals | |

| By Pack Format | Bottles and Jars |

| Caps, Closures and Dispensing Systems | |

| Pouches and Sachets | |

| Trays, Cups and Tubs | |

| Stretch and Shrink Films |

Key Questions Answered in the Report

How large is the Mexico plastic packaging market in 2026?

The Mexico plastic packaging market size is valued at USD 9.09 billion in 2026.

What is the expected growth rate through 2031?

The market is forecast to register a 4.73% CAGR from 2026 to 2031.

Which packaging type is expanding the fastest?

Flexible plastic packaging is projected to grow at 5.09% annually through 2031, faster than rigid formats.

Why is polypropylene demand rising?

Biaxially oriented films and tethered-cap mandates, combined with lower feedstock prices from Alpek, push polypropylene to a 5.89% CAGR.

Which end-user segment will outpace overall growth?

Personal care and cosmetics is set for 5.64% CAGR as multinationals localize production and adopt premium dispensing systems.

How are state-level plastic bans affecting converters?

A patchwork of regulations forces converters to keep modular tooling that can switch between compliant and standard formats, raising capital costs.

Page last updated on: