Woodworking Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.49 Billion |

| Market Size (2031) | USD 6.94 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Woodworking Machinery Market Analysis by Mordor Intelligence

The Woodworking Machinery Market size is projected to expand from USD 5.25 billion in 2025 and USD 5.49 billion in 2026 to USD 6.94 billion by 2031, registering a CAGR of 4.78% between 2026 to 2031.

The woodworking machinery market is supported by a rebound in residential construction and steady upgrades to automated CNC equipment that replace manual workflows, improving throughput and yield. Order pipelines for precision equipment are benefiting from higher housing starts in 2026, which lift demand for cabinetry, millwork, and interior fittings made on programmable routers, panel saws, and edge-processing lines. Equipment innovation is accelerating in Europe as German suppliers stabilize after a 2024 output fall and lean on automation and artificial intelligence to improve productivity and flexibility. Policy and compliance trends matter as well because the European Union Deforestation Regulation will require detailed material traceability at the end of 2026, encouraging digital production and documentation systems in export-focused shops. In China, pressure from a slower building cycle is pushing producers toward higher-value engineered wood processes and more precise machining to protect margins in competitive export channels.

Key Report Takeaways

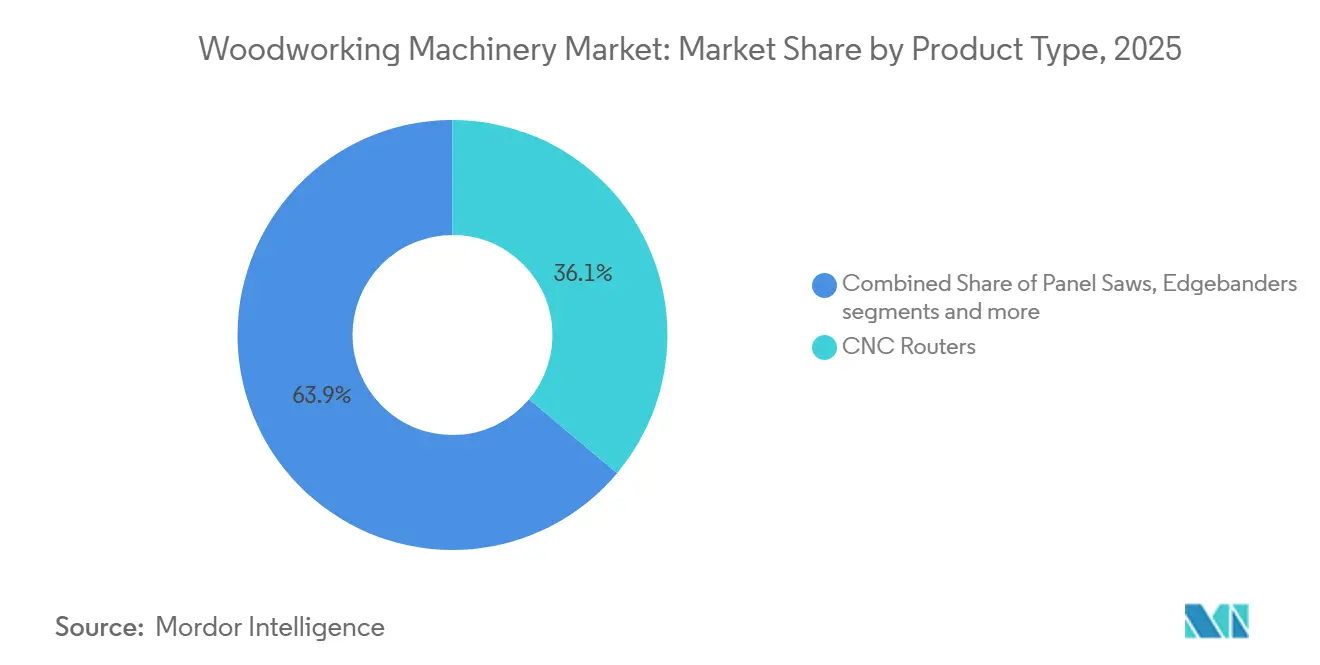

- By product type, CNC routers led with 36.1% of the woodworking machinery market share in 2025, while the category is projected to expand at a 5.8% CAGR through 2026-2031.

- By operating principle, the semi-automatic segment held 49.3% share in 2025, while fully automatic CNC recorded the highest projected growth at a 6.1% CAGR through 2026-2031.

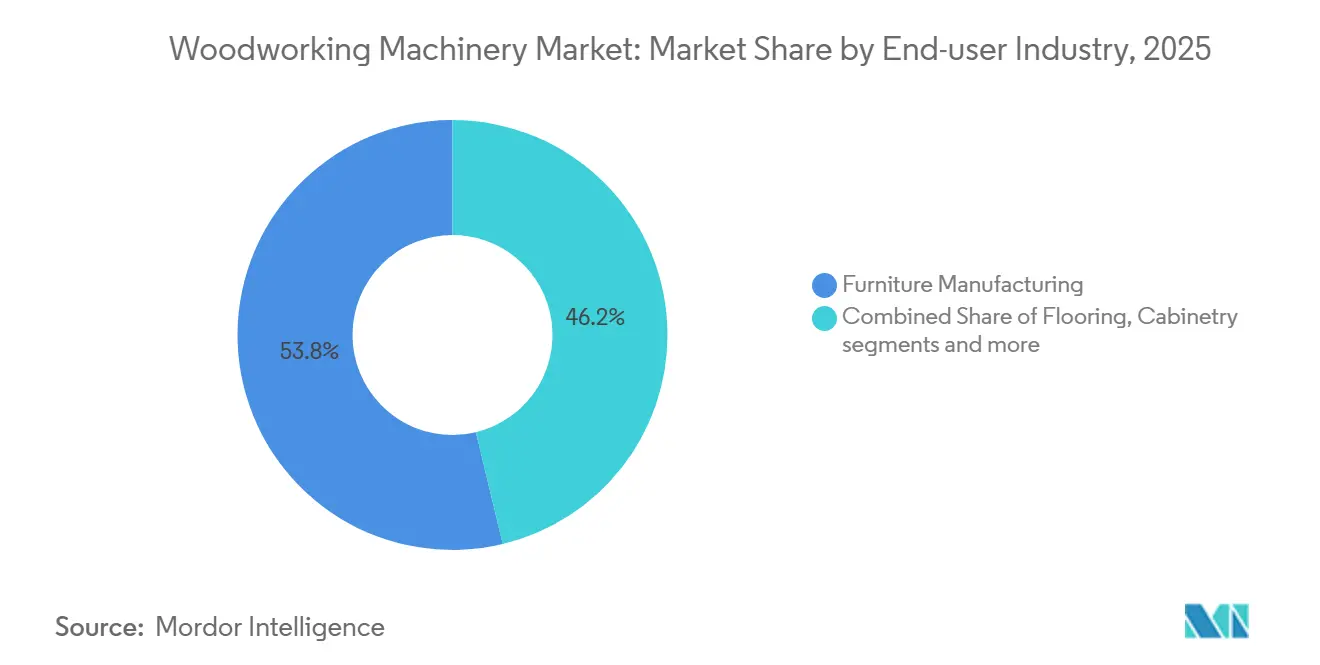

- By end-user industry, furniture manufacturing accounted for a 53.8% share of the woodworking machinery market size in 2025 and is advancing at a 5.2% CAGR through 2026-2031.

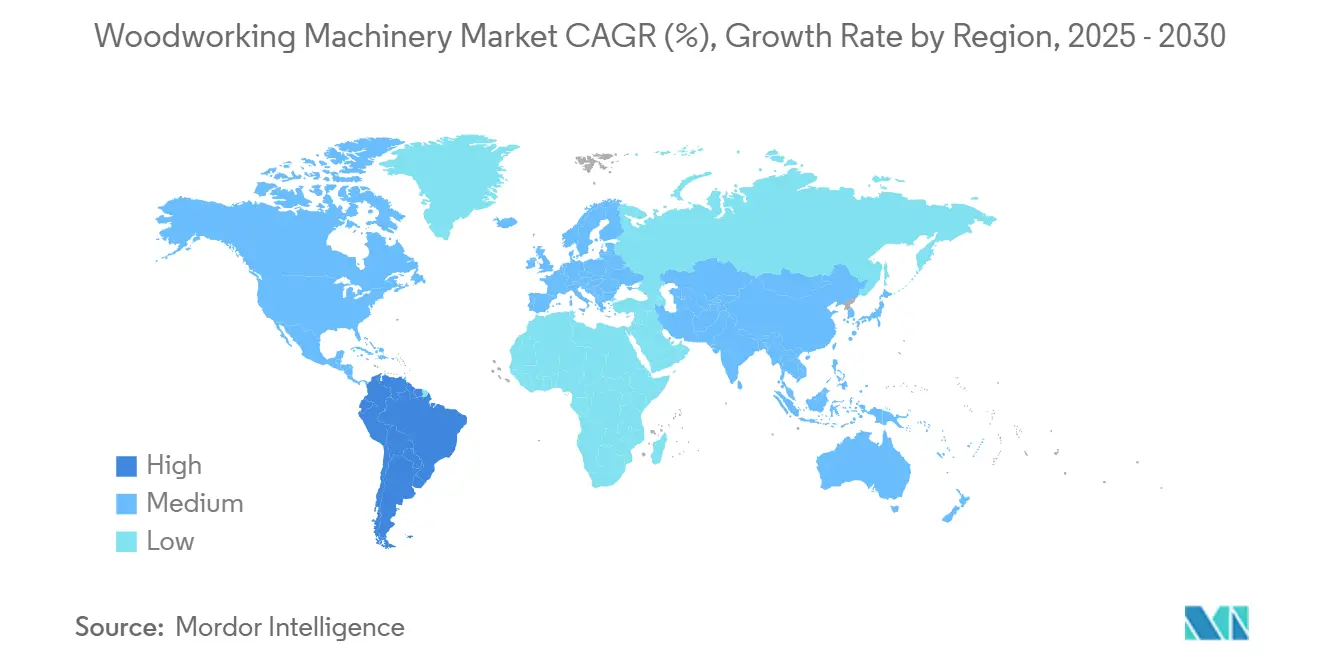

- By geography, Asia-Pacific held 40.8% of the woodworking machinery market share in 2025, while South America is set to grow the fastest at a 6.7% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Woodworking Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming Global Furniture Manufacturing Industry | +1.2% | Global, with heavy concentration in Asia-Pacific (China, India, Vietnam, Thailand) and spillover to North America | Medium term (2-4 years) |

| Growth in Modular and Customized Furniture Demand | +0.9% | North America & EU, early adoption in premium segments of APAC markets | Medium term (2-4 years) |

| Expansion of Residential and Commercial Construction Activity | +1.3% | Global; strongest in North America, moderate in the EU, accelerating in South America | Short term (≤ 2 years) |

| Labor Cost Pressures and Productivity Enhancement Needs | +1.4% | Global; acute in North America and Western Europe, emerging in higher-wage APAC cities | Short to Medium term (2-4 years) |

| Rising Popularity of Engineered Wood Products | +0.7% | Global, driven by sustainable-building codes in the EU and uptake in North America, CLT projects | Long term (≥ 4 years) |

| Growing Wood-based Interior Design and Flooring Trends | +0.5% | North America, the EU, and the premium residential segments in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Global Furniture Manufacturing Industry

Demand for furniture and interior products is reinforcing investment in CNC routers, edgebanders, and finishing lines that shorten setup time and minimize waste in variable-batch production. In the United States, residential construction momentum in early 2026 reinforces order pipelines for cabinetry, millwork, and interior fittings that depend on precision woodworking equipment and nesting-based panel processing.[1]U.S. Census Bureau, “Monthly New Residential Construction, January 2026,” U.S. Census Bureau, census.gov Chinese producers are consolidating around higher-value engineered products and export channels, encouraging upgrades to more precise machining centers to reduce scrap and improve finish quality.[2]USDA Foreign Agricultural Service, “Solid Wood Annual 2025,” USDA Foreign Agricultural Service, fas.usda.gov German machine builders stabilized after a 2024 production decline and are leaning into automation and software-driven control to serve flexible manufacturing requirements, which supports refresh cycles across medium and large plants. Together, these dynamics sustain demand for CNC-enabled production cells and integrated software that translate product configurations into tool paths without manual programming. As the woodworking machinery market evolves toward engineered wood, short-run customization, and digital traceability, suppliers with robust control systems and after-sales support networks are positioned to capture premium projects.

Growth in Modular and Customized Furniture Demand

Customer expectations for modular, made-to-fit cabinets and furniture continue to pull the woodworking machinery market toward flexible nesting, high-precision edge processing, and software-connected workflows that execute one-off jobs efficiently. Suppliers are displaying integrated machining cells and connected platforms that link order intake to production planning and predictive maintenance, which helps mid-market shops manage more customization with fewer unplanned stops. Modular architecture has a lower risk because manufacturers can add automation steps, smarter spindles, or faster material handling as order complexity rises rather than committing to a single, fixed configuration on day one. Compliance expectations also matter because the European Union Deforestation Regulation will require stronger digital traceability for wood products placed on the EU market at the end of 2026, which favors software-integrated shops that can automate documentation and batch segregation. Prepared manufacturers use these capabilities to quote fast, plan work by batch size, and transition jobs without lengthy downtime. The woodworking machinery market is aligning around this need for configurable throughput, with value tilted toward control systems, tool management, and service ecosystems that keep small lots moving at scale.

Expansion of Residential and Commercial Construction Activity

Construction is stabilizing in major economies, and that supports higher utilization of saws, routers, and sanders across cabinet shops, millwork producers, and timber fabricators. In January 2026, United States housing starts reached 1.487 million units on a seasonally adjusted annual basis, a 9.5% year-over-year increase that reinforces demand for finished wood products using precision CNC equipment. In Europe, the German sector is on a recovery path after contractions in 2024 and 2025, with industry reports pointing to automation and AI-driven production improvements as a lever to regain momentum, which feeds through to modern equipment purchases.[3]International Trade Administration, “Germany Woodworking Report,” U.S. Department of Commerce, trade.gov Construction and fit-out cycles also favor CNC-enabled workflows because they support shorter lead times and consistent quality on interior components across multi-unit projects. As mass timber gains share in permitted structures in select jurisdictions, large-format five-axis machining becomes more relevant for glulam beams and panelized elements. The woodworking machinery market benefits builders, general contractors, and fabricators, who request more precision and documentation from suppliers to meet green-building and schedule requirements.

Labor Cost Pressures and Productivity Enhancement Needs

Rising unit labor costs and a constrained pool of experienced CNC operators keep automation at the center of capital-spending plans. In late 2025, unit labor costs in U.S. manufacturing grew sharply while productivity lagged, and durable goods had an even steeper increase, which pressures wood-products producers that rely on manual handling. These conditions support investments in automated tooling, in-process sensing, and software-integrated planning to lift output per operator. Remote monitoring and connected consoles help managers schedule preventive maintenance and reduce unplanned stops, improving equipment utilization during second and third shifts. Plants that combine machinery upgrades with structured training cycles generally realize faster learning curves and consistent quality. As the woodworking machinery market moves toward lights-out cells and sensor-assisted workflows, the payback improves where wages are higher, and turnover is elevated.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Requirements for Advanced Machinery | -0.8% | Global; disproportionate barrier for small and medium enterprises in emerging markets and rural regions | Medium term (2-4 years) |

| Raw Material Price Volatility and Timber Supply Constraints | -1.1% | Global; most severe in North America due to tariff exposure and mill closures | Short term (≤ 2 years) |

| Shortage of Skilled Operators and Machine Programmers | -0.6% | North America, Western Europe, and urbanizing APAC regions | Medium to Long term (2-4+ years) |

| Environmental Concerns and Sustainable Forestry Pressures | -0.4% | EU (EUDR compliance), North America (FSC expectations), and export-focused manufacturers in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements for Advanced Machinery

Advanced CNC equipment requires meaningful upfront commitments, which slows adoption among small and mid-sized enterprises that face higher borrowing costs and tighter cash cycles. Shops balance the benefits of five-axis capability and robotic handling against the total cost of ownership, that include installation, tooling, software, dust collection, and operator training. Many buyers phase automation over time by starting with semi-automatic steps and then adding loaders, scanners, or faster drives as utilization rises, which spreads the investment across multiple years. Refurbished equipment provides a lower entry point but may require more maintenance and lack the newest control systems that support connected dashboards or traceability out of the box. Vendors that offer financing tied to service and training can help de-risk adoption for smaller buyers who need predictable monthly costs. These realities shape the pace of upgrades in the woodworking machinery market, especially outside major manufacturing corridors where technical support and parts logistics can be harder to secure.

Raw Material Price Volatility and Timber Supply Constraints

Volatile raw-material costs and tight availability complicate planning for panel mills, solid-wood fabricators, and downstream shops that run fixed-price contracts. China’s log and lumber imports fell in 2025, and the shift in sourcing patterns has downstream implications for panel supply and pricing, which pushes producers to optimize yield with higher-precision machining. The policy context adds uncertainty because the United States moved to examine security risks linked to timber and derivative imports, signaling that trade actions may shift supply conditions and pricing for inputs and equipment. In the European Union, the deforestation regulation requires elevated diligence and traceability, which can add operational steps for export-focused firms that rely on diverse hardwood feedstocks. State forestry guidance in the United States acknowledges that parcel-level geolocation remains complex for fragmented hardwood supply chains, so manufacturers should plan for system and process updates through 2026. These pressures yield optimization, waste reduction, and faster setup, central to offsetting input volatility, which puts more weight on CNC accuracy and software-integrated nesting. The woodworking machinery market reflects these constraints as buyers prioritize features that document material flows and maximize usable output per board foot.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: CNC Routers Propel Precision and Flexibility

CNC routers held 36.1% share in 2025 and are projected to grow at a 5.8% CAGR through 2031 as buyers seek configurable systems that handle complex geometries and frequent changeovers. The segment’s strength rests on nesting workflows that raise panel yield and automated tool management that reduces downtime between short runs. Panel saws remain common for standardized cutting because they are simpler and less expensive, although the shift toward digital control is persistent across higher-mix shops. Edgebanders, surface planers, and wide-belt sanders move in tandem with expectations for cleaner edges, tighter thickness tolerances, and uniform finishes on both custom and volume projects. Other machines like drills, tenoners, moulders, band saws, lathes, and mortisers keep specialized roles where joinery or turning are central to design or structural needs. The woodworking machinery market favors routers where work mixes are more variable, since software-integrated routing can compress lead times without major labor additions. Router vendors are also bundling nesting software and training to speed time to value in new installs. As a result, the woodworking machinery market size associated with CNC routers is set to expand in line with small-batch customization and software-centric workflows that prioritize speed and material efficiency.

The rest of the product landscape is bifurcating between single-purpose lines designed for throughput and flexible platforms tuned for changeovers. High-mix operations adopt routers that justify their price with labor savings and the ability to run unique jobs efficiently, while mass producers of standardized units still invest in dedicated lines optimized for volume. Replacement cycles are aligned to productivity gains because buyers weigh energy use, spindle speed, and control interface improvements in addition to mechanical precision. Emerging capabilities like connected consoles and predictive maintenance sit alongside faster drives, better vacuum systems, and higher-torque spindles that stabilize cuts on harder materials. The woodworking machinery market continues to cross-pollinate innovations across product categories because finish quality and tolerance expectations are rising on both custom and standard jobs. Over time, multifunctional systems that combine engraving, drilling, and profiling will further consolidate decisions around integrated platforms. This is driving the woodworking machinery industry to focus on end-to-end workflows and interoperability across routers, edgebanders, and finishing equipment.

By Operating Principle: Fully Automatic CNC Gains Ground Against Semi-Automatic Incumbents

Semi-automatic machinery held 49.3% share in 2025 due to its installed base and operator-led control, but fully automatic CNC systems are growing faster at a 6.1% CAGR through 2031. Plants are adding loaders, vision sensors, and in-process measurements to run unattended during overnight or weekend hours, which reduces dependence on scarce specialized labor. Manual equipment holds a niche for artisans and training environments where hands-on craft is central to the work. Production approaches vary across industries and regions, so the transition path often starts with semi-automatic steps and proceeds to full automation as order volume and product-mix variability increase. Safety and compliance are part of the decision because interlocks, guarding, and remote diagnostics map well to recognized occupational standards. The woodworking machinery market continues to adopt connected controls and sensors that support standardized quality with fewer manual adjustments at the machine.

The operating-principle shift also reflects broader changes in plant management and data use. Enterprise-resource-planning linkages and digital twins can map jobs from order entry to workcell execution, with utilization tracked in real time on dashboards. Production leaders decide where to set automation thresholds based on batch size, complexity, and workforce availability. Collaborative robots lower barriers for shops that want to move away from manual handling without full enclosure systems. Over time, predictive maintenance and remote service will become standard in fully automatic cells as buyers value uptime and speed. The woodworking machinery market is therefore migrating toward architectures that support remote monitoring, recipe-driven changeovers, and simplified operator roles, which helps balance labor constraints with throughput demands. Within the woodworking machinery industry, adoption paths will continue to be shaped by skills availability and the economic value of running lights-out on second and third shifts.

By End-user Industry: Innovations Driving Growth in Furniture and Construction Sectors

Furniture manufacturing accounted for 53.8% of demand in 2025 and is projected to grow at a 5.2% CAGR, sustained by Asia-Pacific exporters, North American modular cabinetry, and Europe’s premium segments. This mix creates steady orders for routers, edgebanders, drilling lines, and finishing systems used on upholstered frames, case goods, and solid-wood pieces. Construction and millwork are also expanding as residential and commercial buildings improve, which lifts demand for interior trim, doors, and windows, and stair components that require accurate profiling and edge quality. Where mass timber advances, five-axis machining is relevant for beams and panels that need compound angles and precision cuts. Flooring remains a specialized segment that combines high-speed moulding and sanding with the growing use of CNC for patterned assemblies and inlays. Across these end uses, short-run customization and quality documentation influence buying preferences toward software-integrated equipment. The woodworking machinery market reflects these needs as buyers standardize on digital workflows for quoting, programming, and production monitoring. As quality requirements tighten at retailers and end users, machinery choices also consider consistent finish, tolerance stability, and traceability in addition to speed.

Cabinetry spans both residential and institutional projects, which shapes machine specifications. Residential cabinets follow furniture-like customization with rapid changeovers and nesting, while institutional cabinets emphasize durability and code compliance for health care, education, and commercial kitchens. Hardware tolerances and finish standards are higher in many of these settings, which encourages the adoption of advanced edgebanders and drilling solutions. Across all sectors, the 2026 environment supports replacement cycles for aging assets and projects deferred during disruption years. Shops that integrate software-driven workflows see more predictable throughput and faster time to first part on new designs. As this pattern becomes more common, the woodworking machinery market size related to customization will continue to expand because variability is now a basic condition rather than an exception. Over the forecast period, the end-user mix will still be led by furniture, but growth in millwork and structural timber will play a larger role in new equipment demand.

Geography Analysis

Asia-Pacific accounted for 40.8% of global demand in 2025, anchored by China’s panel capacity, India’s expanding exports, and Southeast Asian contract manufacturing. South America shows the fastest trajectory at a 6.7% CAGR to 2031 as Brazil’s engineered-wood base scales and currency dynamics support foreign investment. North America represents a mature installed base focused on replacement, debottlenecking, and higher automation as labor remains tight. The United States recorded 1.487 million housing starts in January 2026, which underscores steady orders from cabinet and millwork shops for panel processing and finishing systems. Europe is stabilizing after declines in 2024 and 2025, and German suppliers are leaning into automation and AI-assisted production to regain output, a shift that reinforces product innovation and value-added features. China’s producers are trimming capacity in lower-margin segments and prioritizing upgrades that cut energy use and labor per unit, which supports demand for efficient lines and modern control software.

Southeast Asian hubs, including Vietnam, Thailand, and Indonesia, continue to build export reputations, and that raises expectations on quality control, documentation, and consistent finish. South America’s momentum reflects a smaller installed base paired with raw-material strengths and urban growth that together support new plant builds. The Middle East and Africa show sporadic project-led demand from fit-out contractors and joinery firms, though skill availability and import duties temper sustained cycles. In all regions, compliance for EU-bound products is set to become more stringent under the deforestation regulation at the end of 2026, which will boost demand for systems that document material origin and ensure batch integrity. As these conditions evolve, the woodworking machinery market will continue to reward suppliers with strong service networks and remote diagnostics that keep plants running across time zones. Regional preferences will reflect differences in product mix, building codes, labor availability, and sourcing, which will influence machine choice and automation depth.

Competitive Landscape

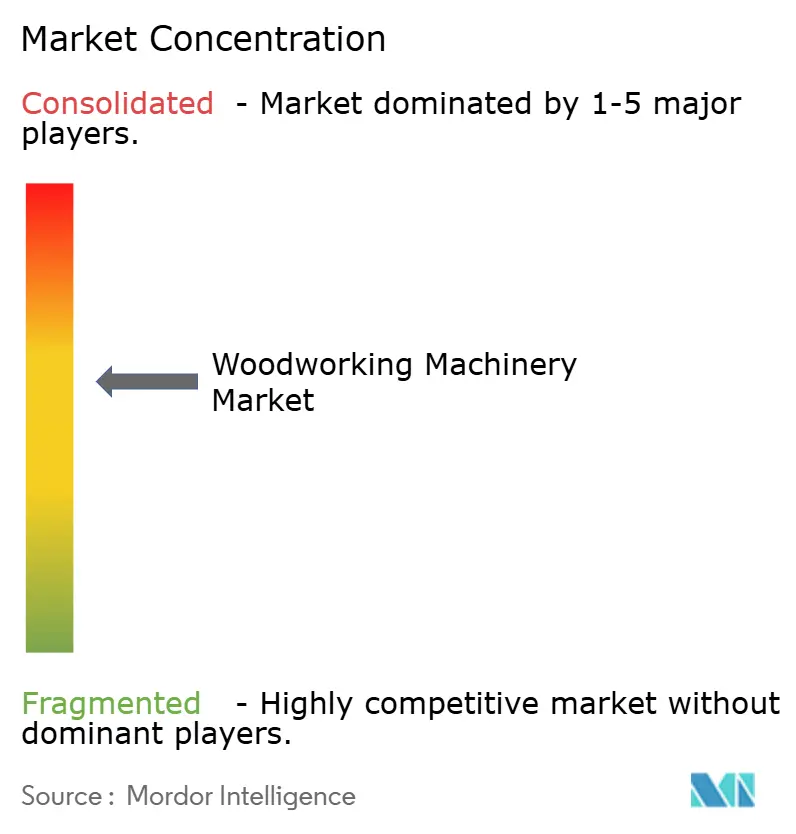

The woodworking machinery market is moderately Consolidated at the top, with global integrators competing alongside regional specialists. HOMAG Group improved earnings in fiscal 2025 on sales of EUR 1.372 billion and EBIT of EUR 76.1 million by optimizing costs and securing strong orders in timber house construction, even as furniture sector demand was steady. SCM Group is showcasing integrated technologies, from manufacturing execution systems to smart spindles and connected consoles that support predictive maintenance and real-time performance tracking, which positions the firm at the intersection of mechanics and digital control. Buyers continue to weigh total cost of ownership, service coverage, and software ecosystems because these factors determine uptime and speed on short-run, high-mix work. The woodworking machinery market rewards vendors that support fast installation, operator training, and remote diagnostics.

Strategy patterns show a split between premium integration and price-accessible options. Western suppliers emphasize service contracts, software subscriptions, and tailored integration projects that lock in value across years. Moves such as HOMAG’s full acquisition of Kallesoe Machinery in 2025 strengthened capabilities in mass timber and high-frequency pressing, which aligns with the growing use of engineered wood in permitted structures. Vendors also compete with lead times, financing options, and modular upgrade paths that allow plants to scale automation step by step. Regional distributors and service partners remain critical in local markets where fast parts availability and on-site training determine machine uptime. The woodworking machinery market continues to see Chinese and regional challengers in entry and mid ranges, which pressures incumbents to show clear lifecycle value through uptime and yield.

Technology roadmaps across leading brands converge on connectivity, usability, and quality control. Companies highlight IoT-enabled dashboards, digital twins for setup and validation, and safety systems that fit recognized standards. EU compliance requirements set to come into force in late 2026 add weight to digital traceability and batch control inside manufacturing cells. In North America and Europe, emissions and air quality rules for plywood and composite wood products persist as baseline constraints, which encourage more controlled finishing systems and integrated capture. As features converge, the woodworking machinery market differentiates through software usability, service depth, and integration skills that shorten time to first part and maintain uptime in multi-shift operations. The competitive balance will track how well vendors translate these features into measurable throughput and quality advantages.

Woodworking Machinery Industry Leaders

HOMAG Group

SCM Group

Biesse Group

Michael Weinig AG

Felder Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: HOMAG spotlighted automation and modern furniture production at Wood Tech 2026 in Warsaw, presenting machining, drilling, edgebanding, and panel-saw solutions along with training offers and software promotions.

- December 2025: The Forest Stewardship Council updated its chain-of-custody standard, adding a downstream operator category and simplifying declarations for micro and small primary operators in low-risk countries to ease compliance burdens.

- October 2025: The White House directed a Section 232 investigation into national-security risks from imports of timber, lumber, and wood derivatives, which could shape 2026 U.S. trade policies affecting inputs and machinery sourcing.

- May 2025: HOMAG Group acquired the remaining 29.4% of Kallesoe Machinery A/S to bolster high-frequency press capabilities for mass timber applications.

Global Woodworking Machinery Market Report Scope

The Woodworking Machinery Market is Segmented by Product Type (CNC Routers, Panel Saws, Edgebanders, Surface Planers, Wide-belt Sanders, and Other Machines), by Operating Principle (Conventional/Manual, Semi-Automatic, and Fully Automatic CNC), by End-user Industry (Furniture, Construction, Flooring, Cabinetry, and Other), and by Geography (North America, South America, Europe, Asia-Pacific, aMiddle East and Africa). Market Forecasts are Provided in Value (USD).

| CNC Routers |

| Panel Saws |

| Edgebanders |

| Surface Planers |

| Wide-belt Sanders |

| Other Machines (Drills, Tenoners, Milling Machines, Band Saws, Wood Lathes, Mortisers) |

| Conventional / Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Furniture Manufacturing |

| Construction & Millwork |

| Flooring |

| Cabinetry |

| Other Industrial Users (Plywood and Panel Manufacturing, Ship Building, Etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | CNC Routers | |

| Panel Saws | ||

| Edgebanders | ||

| Surface Planers | ||

| Wide-belt Sanders | ||

| Other Machines (Drills, Tenoners, Milling Machines, Band Saws, Wood Lathes, Mortisers) | ||

| By Operating Principle | Conventional / Manual | |

| Semi-Automatic | ||

| Fully Automatic CNC | ||

| By End-user Industry | Furniture Manufacturing | |

| Construction & Millwork | ||

| Flooring | ||

| Cabinetry | ||

| Other Industrial Users (Plywood and Panel Manufacturing, Ship Building, Etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the woodworking machinery market size today, and where is it headed by 2031?

The woodworking machinery market size was USD 5.3 billion in 2025 and is projected to reach USD 6.9 billion by 2031 at a 4.8% CAGR over 2026-2031.

Which product category leads demand within woodworking machinery?

CNC routers led with 36.1% share in 2025, and the segment is projected to grow at a 5.8% CAGR through 2031 as shops prioritize nesting, rapid changeovers, and precision on custom runs.

How is automation changing the competitive balance by operating principle?

Semi-automatic systems held 49.3% share in 2025, while fully automatic CNC is the fastest-growing mode at a 6.1% CAGR through 2031 as buyers invest in lights-out capability and in-process sensing.

What end-use drives the most equipment demand in 2026?

Furniture manufacturing is the largest end-use with a 53.8% share in 2025, and it is advancing at a 5.2% CAGR through 2031, supported by exports from Asia-Pacific and modular cabinetry momentum in North America.

Which region is most important for growth, and which is the largest by share?

Asia-Pacific held 40.8% share in 2025 and remains the largest region, while South America shows the fastest growth at a 6.7% CAGR to 2031, driven by engineered wood capacity and new plant investments.

What external forces could reshape demand for woodworking machinery in 2026?

Housing start trends, EU deforestation-compliance timelines, and potential U.S. trade policy changes are key variables, and each influences capital spending on CNC, traceability, and finishing systems.

Page last updated on: