India Metal Additive Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

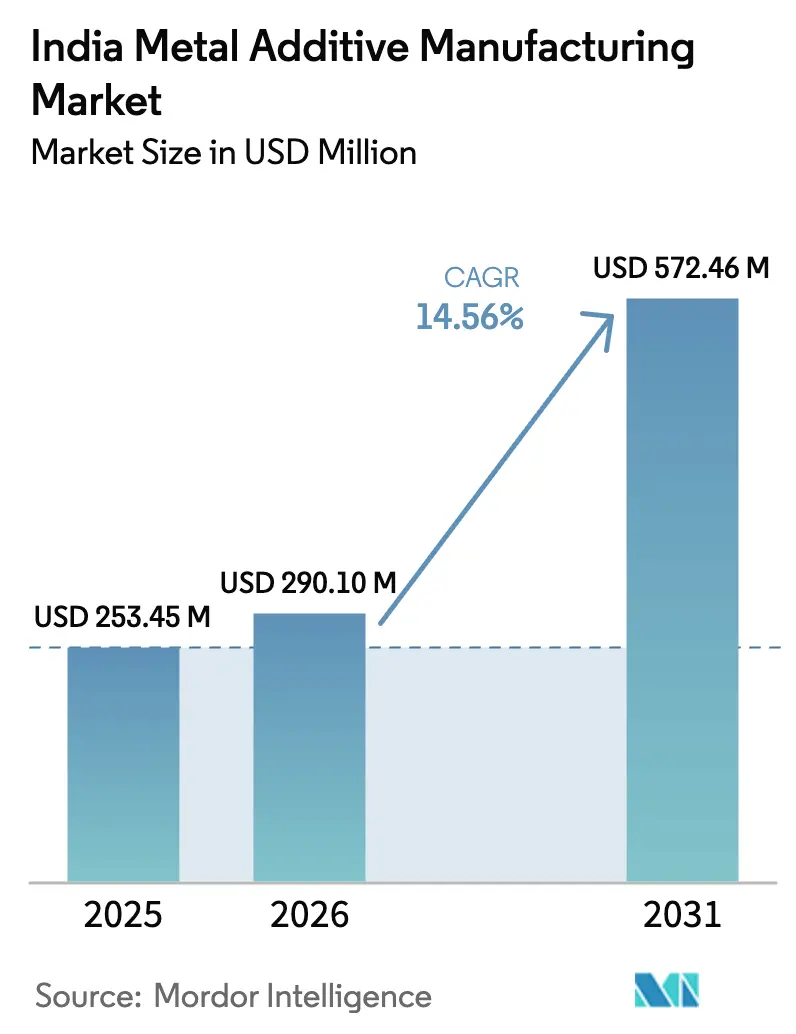

| Base Year Market Size (2025) | USD 253.45 Million |

| Market Size (2026) | USD 290.10 Million |

| Market Size (2031) | USD 572.46 Million |

| Growth Rate (2026 - 2031) | 14.56% CAGR |

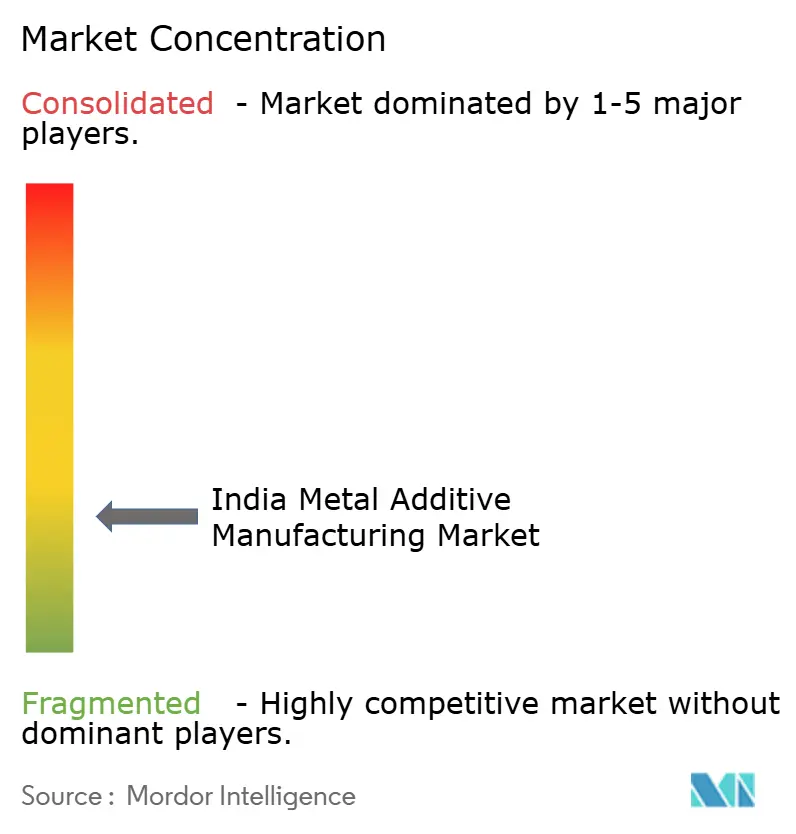

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Metal Additive Manufacturing Market Analysis by Mordor Intelligence

The India Metal Additive Manufacturing Market size was valued at USD 253.45 million in 2025 and is estimated to grow from USD 290.10 million in 2026 to reach USD 572.46 million by 2031, at a CAGR of 14.56% during the forecast period (2026-2031).

Expansion reflects the convergence of policy-led indigenization with rising aerospace, defense, and electric vehicle demand that is shifting production from subtractive methods to layer-based metal fabrication. The National Strategy for Additive Manufacturing, operationalized through the Ministry of Electronics and Information Technology, targets indigenous machine development, material localization, and workforce skilling to build a resilient value chain. Public procurement and certification priorities in aerospace and defense are guiding capital allocation toward qualified machines, materials, and process controls within established technology corridors in Bengaluru, Hyderabad, Pune, Nashik, Chennai, and Coimbatore. Suppliers equipped with validated build parameters, post-processing routes, and non-destructive test capabilities are best positioned to convert policy signals into series production contracts across strategic programs.

Key Report Takeaways

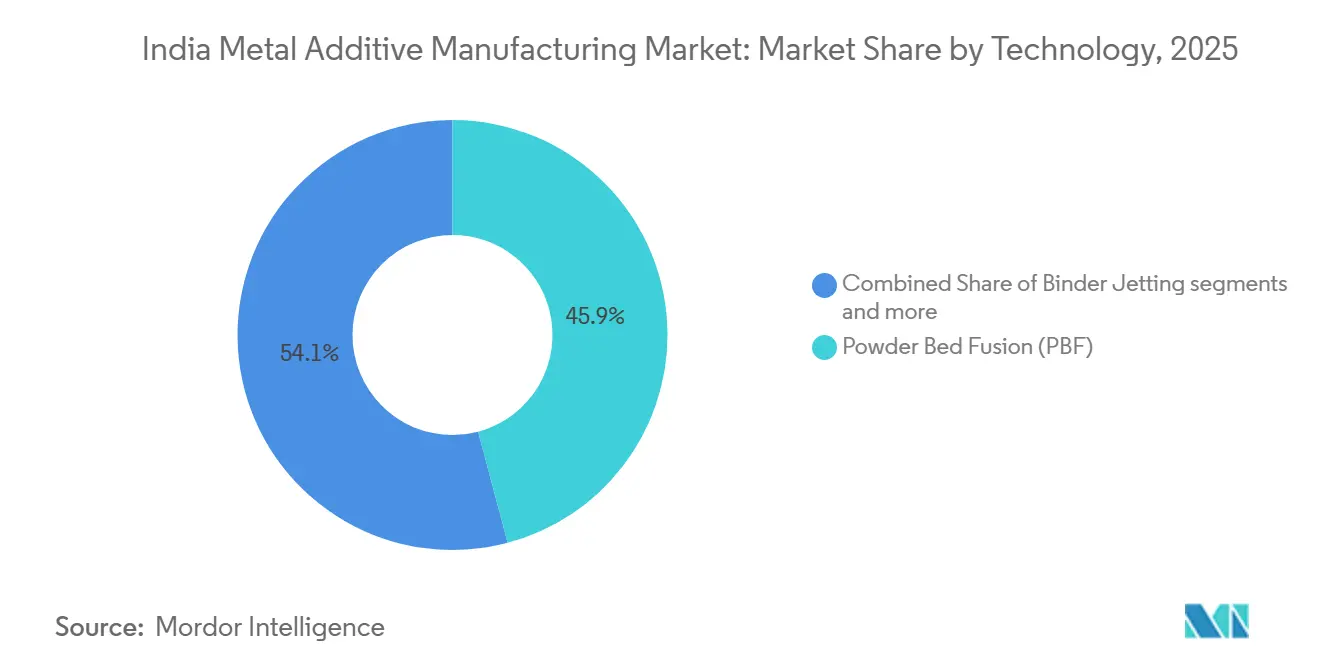

- By technology, Powder Bed Fusion led the India metal additive manufacturing market size with 45.87% share in 2025, while Binder Jetting recorded the highest projected growth at a 15.78% CAGR through 2031.

- By material type, Titanium accounted for a 37.81% India metal additive manufacturing market share of tonnage in 2025, while Precious Metals logged the fastest projected 16.34% CAGR to 2031.

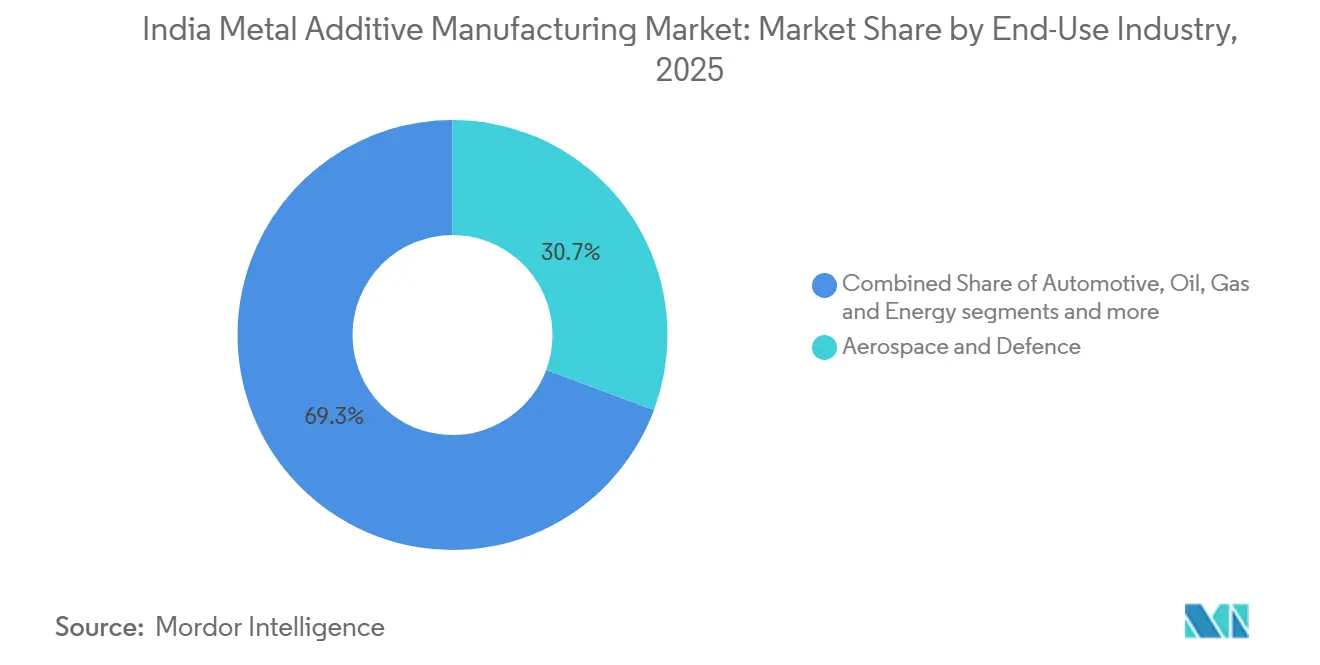

- By end-use industry, Aerospace & Defence held 30.67% revenue share in 2025, while Construction is projected as the fastest growing segment at a 17.12% CAGR through 2031.

- By geography, West India captured 37.81% share in 2025, while South India is projected to grow at a 16.87% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Metal Additive Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Aerospace and Defense Indigenization Programs | +3.2% | National, strongest in Bengaluru, Hyderabad, Pune | Medium term (2-4 years) |

| Government's Make in India and Atmanirbhar Bharat Initiatives | +2.8% | National, concentrated in Maharashtra, Karnataka, Tamil Nadu, and Telangana. | Medium term (2-4 years) |

| Cost Advantages for Low-Volume and Complex Part Production | +2.7% | National, early in aerospace, medical devices, and tooling hubs | Medium term (2-4 years) |

| Automotive Industry's Shift Toward Electric Vehicles | +2.6% | West and South corridors with EV clusters | Short term (≤ 2 years) |

| Expansion of India's Space Program | +1.9% | National, centered in Bengaluru, Chennai, Thiruvananthapuram | Long term (≥ 4 years) |

| Rising Demand for Customized Medical Implants and Prosthetics | +1.4% | Metro clusters scaling to Tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Aerospace and Defense Indigenization Programs

Higher capital outlays and ringfenced domestic procurement are channeling demand for qualified metal AM components in air, land, and naval platforms across propulsion, structural, and thermal systems.[2]Defence Research and Development Organisation, “DRDO News,” DRDO, drdo.gov.in Program announcements for next-generation aero engines elevate the role of printed injectors, liners, and complex cooling channels that benefit from repeatable powder-bed processes and robust post-processing. Mission timelines and platform upgrades tighten requirements for certified machines, powders, and heat treatment routes, which favors experienced service bureaus and integrators embedded in aerospace clusters. Standardization guidance aligned with ISO and ASTM practices is being adopted across airworthiness and naval classification pathways, which supports reliable series production of critical parts as test data matures.[3]Indian Register of Shipping, “Additively Manufactured Metallic Parts for Marine and Offshore Applications,” IRCLASS, irclass.org These shifts expand the opportunity space for the Indian metal additive manufacturing market by linking procurement pipelines to domestic qualification capacity.

Government's Make in India and Atmanirbhar Bharat Initiatives

The national roadmap places additive manufacturing among frontier technologies with significant GDP upside, outlining plug-and-play industrial parks and shared infrastructure that reduce entry barriers for capital-intensive metal printers.[1]NITI Aayog, “Reimagining Manufacturing: India’s Roadmap to Global Leadership in Advanced Manufacturing,” NITI Aayog, niti.gov.in Policy measures emphasize indigenous machine development, localized materials, and a trained workforce so small and mid-sized firms can access advanced systems without prohibitive up-front costs. Competitive grants from the Technology Development Board further direct resources toward commercializing domestic metal and ceramics 3D printing technologies and enabler subsystems across the value chain. These interventions link procurement priorities with industrial capability-building, which accelerates qualification cycles for parts, machines, and materials aligned with national standards. The result for the Indian metal additive manufacturing market is a broader funnel of certified suppliers ready to serve regulated applications and time-bound projects.

Cost Advantages for Low-Volume and Complex Part Production

Single-piece metal AM designs in propulsion and other critical systems compress time from concept to test by removing tooling and assembly steps, which unlocks economic advantages at low volumes and high complexity. Research and procurement priorities for integrated cooling, lattice structures, and conformal channels internal to parts support AM-first approaches where conventional processes reach geometric limits. Patient-specific cranial and orthopedic implants show high clinical fit rates that reduce pre-operative rework, demonstrating a cost-of-care rationale for precision AM parts. Gold and platinum jewelry designs leverage AM to reduce precious metal weight while maintaining intricate aesthetics, which addresses consumer price sensitivity when bullion prices rise. These adoption patterns reinforce the Indian metal additive manufacturing market’s role, where batch sizes are limited, and part complexity is beyond four-axis machining.

Automotive Industry's Shift Toward Electric Vehicles

The PM E-DRIVE scheme and related phased manufacturing steps mandate domestic assembly of key subsystems, which creates pull for lightweight brackets, heat sinks, and housings where AM reduces mass while retaining mechanical integrity. Program design disincentivizes CKD imports, directing suppliers toward localized solutions that increasingly exploit binder jetting for thermal-dissipation designs not feasible with die-casting. Investment commitments under PLI and OEM pilot lines are setting up pathways from prototypes to series runs, contingent on fatigue validation and homologation, which progresses the adoption curve. Domestic metals expansion plans reflect the broader shift to aluminum-intensive EV platforms, which complements AM’s role in topology-optimized parts and tooling for lower-volume variants. These dynamics open a cost-performance window for the Indian metal additive manufacturing market in EV-focused hubs across West and South India.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extremely High Equipment and Material Costs | -3.1% | National, most acute for MSMEs in Tier-2/3 clusters | Short term (≤ 2 years) |

| Limited Availability of Qualified Metal Powders Domestically | -2.4% | National, strongest in aerospace corridors | Medium term (2-4 years) |

| Lack of Standardization and Quality Certification Frameworks | -1.8% | National, regulated sectors are most affected | Long term (≥ 4 years) |

| Insufficient Awareness Among Traditional Manufacturing Sectors | -1.3% | Tier-2/3 machining clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extremely High Equipment and Material Costs

Capital outlays for industrial-grade metal AM systems and their consumables remain high for the country’s MSME base, which constrains adoption without access to shared infrastructure or pay-per-use models. Titanium powder pricing, combined with duties on specialty alloys, raises per-kilogram costs for aerospace-grade feedstocks relative to mature supply chains in other regions. Upstream moves to beneficiate ilmenite into titanium slag are building raw material resilience, yet downstream atomization capacity will take time to meet aerospace-grade sphericity and oxygen thresholds for powders. National plans for frontier-technology parks with shared equipment can reduce the burden, though the geographic spread of suppliers means localized service bureaus still matter for logistics and support. These cost and availability headwinds temper near-term penetration of the Indian metal additive manufacturing market in cost-sensitive end uses.

Limited Availability of Qualified Metal Powders Domestically

High reliance on imported titanium and nickel-alloy powders increases input costs and extends lead times, which compresses margins and slows qualification cycles for flight-critical and safety-critical applications. Upstream beneficiation projects to convert ilmenite into titanium slag improve resource security, yet aerospace-grade atomization capacity and powder-quality controls require multi-year scaling to meet sphericity and oxygen thresholds. Standards and classification pathways continue to align with ISO and ASTM, but powder reuse protocols and batch-to-batch consistency remain gating items for wider deployment in regulated end uses. Precious metal feedstock localization is advancing, though high-temperature alloys critical to aerospace and energy still depend on qualified imports while domestic ecosystems mature. As powder sources diversify and qualification datasets grow, the India metal additive manufacturing market will gain resilience against supply shocks and reduce landed costs across production programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Laser Precision Drives Aerospace Qualification

Powder Bed Fusion accounted for 45.87% of the installed base in 2025, reflecting airworthiness needs for sub-50-micron resolution and repeatability in turbine, injector, and thermal management parts validated through non-destructive evaluation and structured post-processing. This precision, combined with mature process controls and hot isostatic pressing routines, aligns with aerospace qualification flows that emphasize consistent microstructures and mechanical properties across complex geometries. Binder Jetting is the fastest-growing technology at a projected 15.78% CAGR to 2031, sustained by economics in tooling and medium-volume parts where sintering and infiltration deliver acceptable properties for automotive and industrial buyers. Directed Energy Deposition supports repair and remanufacture use cases, including blade-tip restoration and on-site or near-site part reinforcement, which shortens downtime for engines and shipboard systems. Technology selection correlates with certification readiness, so qualification frameworks favor PBF for flight hardware today while Binder Jetting expands in cost-sensitive applications as datasets mature.

Adoption patterns also mirror national R&D priorities for lattice structures, conformal cooling, and build-parameter optimization that raise first-time-right rates and cut rework. This strengthens the opportunity in the Indian metal additive manufacturing market, where tooling amortization would otherwise hinder complex, low- to mid-volume runs. Within technology choices, the Indian metal additive manufacturing market share for PBF benefits from airworthiness and classification guidance aligned with ISO and ASTM, while Binder Jetting’s qualification playbook continues to evolve on material systems and sintering repeatability. As certification data accumulates for electron-beam variants, wire-arc routes, and hybrid platforms, multi-technology facilities can tailor processes to part function and lifecycle requirements. These certification-driven choices are reshaping go-to-market strategies for both OEMs and service bureaus in India’s regional clusters.

By Material Type: Titanium Anchors Aerospace, Precious Metals Surge in Jewellery

Titanium held a 37.81% share of 2025 tonnage, anchored by propulsion and structural applications where high strength-to-weight ratios justify higher powder prices in qualified builds and post-processing regimes. This share reflects ongoing national moves to secure upstream titanium resources and establish processing links that will, over time, support localized powder production for aerospace grades. Precious Metals post the fastest trajectory at a projected 16.34% CAGR, with jewelry clusters adopting AM to reduce weight while preserving intricate lattice and filigree design elements. Local feedstock initiatives for platinum and related alloys aim to compress lead times and lower landed costs for domestic manufacturers as volumes scale. Stainless steel and aluminum remain workhorse materials for industrial parts and automotive brackets, where lower raw material costs enable adoption at smaller batch sizes.

Nickel superalloys such as Inconel in propulsion and high-temperature components grow with national programs that prioritize thermal efficiency and reliability, which reinforces demand for repeatable builds and validated heat treatments. Medical-grade cobalt chrome retains a niche for implants where biocompatibility is essential, with clinical fit outcomes improving for patient-specific designs. The Indian metal additive manufacturing market size at the material level expands in line with certified powder availability, especially as atomization and quality controls deepen for titanium and nickel alloys. Jewelry applications push Precious Metals adoption while industrial and aerospace needs sustain titanium and nickel-alloy demand, creating a three-speed material landscape that vendors align to through qualified powder portfolios. These material dynamics reinforce a balanced mix spanning high-performance aerospace, cost-conscious industrial parts, and consumer luxury categories.

By End-Use Industry: Growth Amid Strategic Partnerships and Regulatory Focus

Aerospace & Defence accounted for 30.67% of 2025 revenue, supported by higher domestic procurement and propulsion programs that prioritize additively manufactured injectors, liners, and heat exchangers with certified process controls. Qualification-led sourcing favors facilities with deep non-destructive testing capabilities and prequalified build parameters, which shortens the path from prototypes to flight hardware. Partnerships between integrators and machine OEMs focus on assembly simplification and function integration, lowering part counts and improving maintainability in space and aviation systems. These patterns anchor near-term growth for the Indian metal additive manufacturing market in regulated applications that reward repeatability and certification maturity. Automotive adoption builds through EV-focused pilots that move from prototype tooling to sintered metal parts, paced by validation and homologation milestones.

Construction posts the highest projected CAGR to 2031 as infrastructure projects pilot large-format metal deposition for connectors and structural joints, cutting on-site welding time and enabling modular assembly. Healthcare and dental advance with patient-specific implants and surgical guides, leveraging high accuracy and tailored designs that reduce intraoperative adjustments. Tooling and industrial goods capitalize on binder jetting’s economics for complex inserts and cores, which reduces cycle times and costs for mid-volume production runs. The Indian metal additive manufacturing market size for end-use segments reflects a two-track pattern where aerospace and defense maintain share through certification depth, and construction, tooling, and jewelry deliver faster growth from application economics. Electronics and semiconductors remain emergent with thermal management parts and RF enclosures, while oil, gas, and energy adoption tracks long-duration field trials for corrosion-resistant and high-temperature service.

Geography Analysis

West India, anchored by Maharashtra and Gujarat, held 37.81% share in 2025, supported by Pune’s aerospace-automotive corridor and Mumbai’s jewelry manufacturing ecosystem that increasingly uses AM for complex, lightweight designs. Industrial users in Pune extend AM into landing gear and defense subsystems, leveraging regional machining depth and metallurgical know-how for qualification and scale-up. Jewelry manufacturers in Mumbai and Rajkot use lattice and filigree structures to cut precious metal weight while retaining design detail, supported by industry programs and training from sector bodies. The Indian metal additive manufacturing market share concentration in the West reflects this mix of aerospace, automotive, and jewelry demand tied to cluster-specific strengths.

South India is projected as the fastest-growing region at a 16.87% CAGR through 2031, led by Bengaluru’s aerospace ecosystem and Hyderabad’s National Centre for Additive Manufacturing that anchors R&D and commercialization support. Chennai’s automotive belt integrates AM for EV-focused heat sinks and next-generation tooling under domestic assembly mandates, which boosts adoption once validation is complete. Regional facilities ramp capabilities in process simulation, parameter optimization, and post-processing, which improve first-time-right builds for intricate components. The Indian metal additive manufacturing market size in the South is also supported by academic-industry collaboration and public programs that lower the barrier to early pilots.

North India builds share in medical and automotive hubs across Delhi NCR, Gurgaon, and Noida, where patient-specific implants, tooling, and fixtures drive steady adoption. Central India progresses through upstream minerals and materials initiatives that can enable future powder localization, enhancing the resilience of metal feedstocks as projects mature. East and North-East focus on capability building and skill development that seed future industrial users, while national plans for shared infrastructure aim to reduce geographic disparities in access to qualified equipment. Overall, regional momentum aligns with cluster strengths and policy support that connect qualified suppliers to time-bound programs and end-use pilots.

Competitive Landscape

India’s metal AM ecosystem brings together global OEMs and domestic integrators that run application centers and service bureaus across aerospace, automotive, industrial, and jewelry use cases. Domestic firms focus on design-to-part services and application-specific process development, embedding close to customers in Pune, Bengaluru, Hyderabad, Chennai, and Mumbai. Aerospace and defense needs for certified parts elevate players with robust quality systems, non-destructive testing, and HIP capacity, which increases switching costs once part families are qualified. Strategic moves include partnerships that consolidate assemblies into fewer printed components, lowering part counts and simplifying supply chains in space and aviation. Local materials initiatives in precious metals expand options for jewelry designers and reduce import dependence for select feedstocks.

Certification readiness shapes competitive positioning more than raw hardware specifications, especially in regulated sectors where process controls and repeatability are paramount. Indigenous machine makers emphasize prequalified material sets and tuned process windows that reduce time to first-article acceptance for non-critical and semi-critical parts. Global OEMs combine machine, materials, and software stacks with training and application support to accelerate adoption curves at customer sites. This mix of offerings meets demand patterns where the Indian metal additive manufacturing market needs both deep certification pathways for aerospace and cost-per-part competitiveness for automotive, tooling, and jewelry. As shared infrastructure and R&D programs scale, more suppliers can move from prototype-only to production-ready status.

Upstream resource strategies such as titanium beneficiation strengthen long-term powder resilience and can support expansion in aerospace-grade materials once atomization capabilities mature. Downstream, alliances with defense primes and space agencies create qualified part pipelines for components that benefit from AM’s geometric freedom and consolidation. In consumer categories, precious metal AM expands catalog flexibility and shortens design-to-showcase cycles for mid- to high-end segments. Together, these dynamics suggest a competitive environment where certification strength, application know-how, and materials access are key levers for share gains in the Indian metal additive manufacturing market.

India Metal Additive Manufacturing Industry Leaders

Wipro 3D

Intech Additive Solutions

Bharat Fritz Werner (BFW Additive)

GE Additive (India)

EOS India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DRDO’s Gas Turbine Research Establishment invited bids from Indian firms for the Advanced High Thrust Class Engine program targeting nearly 120 kilonewton thrust, which positions AM injectors and liners as enablers for next-generation aero engines.

- July 2025: The Technology Development Board launched a call for proposals to support metals and ceramics 3D printing and enabler technologies, extending financial assistance for commercialization.

- June 2025: Platinum Guild International announced the commercial launch of a 3D-printed platinum jewelry collection fabricated via laser powder bed fusion, signaling scalability for intricate lattice designs

- June 2025: Precious Alloys Pvt. Ltd. inaugurated a domestic platinum grain atomization facility designed to localize feedstock and reduce costs for jewelry manufacturers.

India Metal Additive Manufacturing Market Report Scope

The India Metal Additive Manufacturing Market Report is Segmented by Technology (Powder Bed Fusion, Binder Jetting, Directed Energy Deposition, and Others), by Material Type (Stainless Steel, Aluminum, Titanium, Cobalt Chrome, Nickel Alloys, Precious Metals, and Others), by End-Use Industry (Aerospace and Defence, Automotive, Healthcare and Dental, Oil Gas and Energy, Tooling and Industrial Goods, Electronics and Semiconductors, Construction, and Jewellery and Art), and Geography. Market Forecasts are Provided in Terms of Value in USD

| Powder Bed Fusion (PBF) |

| Binder Jetting |

| Directed Energy Deposition (DED) |

| Other Metal AM Processes |

| Stainless Steel |

| Aluminum |

| Titanium |

| Cobalt Chrome |

| Nickel Alloys |

| Precious Metals (e.g., gold, silver, platinum) |

| Others (custom alloys, high-temp superalloys) |

| Aerospace & Defence |

| Automotive |

| Healthcare & Dental |

| Oil, Gas & Energy |

| Tooling & Industrial Goods |

| Electronics & Semiconductors |

| Construction |

| Jewellery & Art |

| North India (Delhi, Haryana, UP, Punjab) |

| West India (Maharashtra, Gujarat, Goa) |

| South India (Karnataka, Tamil Nadu, Telangana, Kerala) |

| East & North-East India |

| Central India (MP, Chhattisgarh) |

| By Technology | Powder Bed Fusion (PBF) |

| Binder Jetting | |

| Directed Energy Deposition (DED) | |

| Other Metal AM Processes | |

| By Material Type | Stainless Steel |

| Aluminum | |

| Titanium | |

| Cobalt Chrome | |

| Nickel Alloys | |

| Precious Metals (e.g., gold, silver, platinum) | |

| Others (custom alloys, high-temp superalloys) | |

| By End-Use Industry | Aerospace & Defence |

| Automotive | |

| Healthcare & Dental | |

| Oil, Gas & Energy | |

| Tooling & Industrial Goods | |

| Electronics & Semiconductors | |

| Construction | |

| Jewellery & Art | |

| By Region | North India (Delhi, Haryana, UP, Punjab) |

| West India (Maharashtra, Gujarat, Goa) | |

| South India (Karnataka, Tamil Nadu, Telangana, Kerala) | |

| East & North-East India | |

| Central India (MP, Chhattisgarh) |

Key Questions Answered in the Report

What is the current size and growth outlook for the Indian metal additive manufacturing market?

The Indian metal additive manufacturing market size was USD 253.45 million in 2025 and is projected to reach USD 572.46 million by 2031 at a 14.56% CAGR over 2026-2031.

Which end-use segments are leading, and which are growing fastest in India?

Aerospace & Defense led with 30.67% of 2025 revenue, while Construction is projected to record the highest growth to 2031 based on pilot adoption of large-format metal deposition.

Which technologies are most widely adopted today and why?

Powder Bed Fusion dominates due to precision and mature qualification pathways for aerospace parts, while Binder Jetting grows fastest as sintering economics attract automotive and tool users.

What materials are seeing the strongest adoption in India?

Titanium holds the largest share by tonnage due to aerospace and propulsion uses, and Precious Metals are expanding quickly in jewelry for weight reduction and complex designs.

Which regions are leading or accelerating within India?

West India led with a 2025 share centered on aerospace-automotive hubs and jewelry clusters, while South India is projected as the fastest-growing corridor supported by NCAM and EV-focused supply chains.

What are the main barriers to wider adoption, and how are they being addressed?

High equipment and powder costs, limited domestic qualified feedstocks, and evolving certification frameworks are the core challenges, with shared infrastructure, upstream titanium initiatives, and national standards workstreams mitigating these constraints over time.

Page last updated on: